Sample Category Title

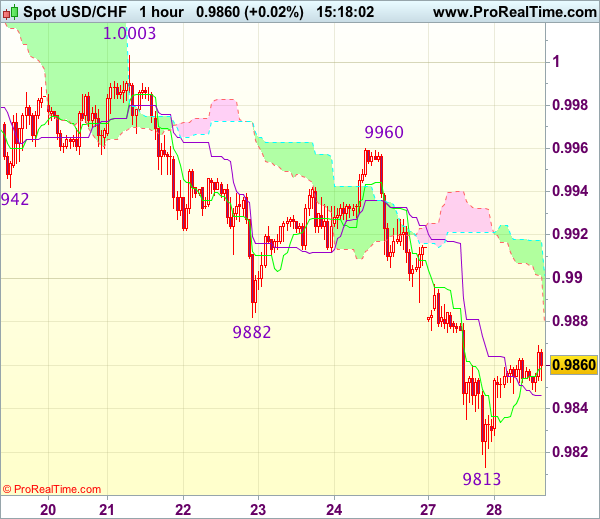

Trade Idea : USD/CHF – Sell at 0.9910

USD/CHF - 0.9833

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 0.9837

Kijun-Sen level : 0.9864

Ichimoku cloud top : 0.9932

Ichimoku cloud bottom : 0.9921

Original strategy :

Sell at 0.9910, Target: 0.9800, Stop: 0.9945

Position : -

Target : -

Stop : -

New strategy :

Sell at 0.9910, Target: 0.9800, Stop: 0.9945

Position : -

Target : -

Stop : -

The greenback found support at 0.9813 yesterday and has recovered, suggesting consolidation above this level would be seen and corrective bounce to 0.9880 is likely but upside should be limited to 0.9900-10 and bring another decline later, below said support at 0.9813 would confirm recent decline has resumed and extend weakness to 0.9795-00, however, loss of downward momentum should prevent sharp fall below 0.9770-75 (100% projection of 1.0171-0.9942 measuring from 1.0003), bring rebound later.

In view of this, would not chase this fall here and we are looking to sell dollar on subsequent rebound as 0.9900-10 should limit upside. Only above said resistance at 0.9960 would abort and signal low is formed, bring retracement of recent decline towards indicated previous resistance at 1.0003.

Cable – Bulls To Resume After Shallow Correction, 200SMA Eyed

Cable eased to 1.2550 zone in early European trading on Tuesday, after being flat in Asia, following Monday's spike to fresh multi-week high at 1.2613.

Probe above strong barriers at 1.2568/ 80 (24 / 09 Feb highs) so far did not result in close above them to confirm break.

Current easing could be seen as correction (signaled by reversal of slow stochastic from overbought zone) before broader bulls resume.

Sustained break above 1.2568/80 triggers is needed to open way towards targets at 1.2689 (falling 200SMA) and 1.2704 (02 Feb high).

Dips were so far shallow and held by initial support at 1.2550 zone, however, deeper correction cannot be ruled out.

Rising daily cloud offers strong support at 1.2420, reinforced by ascending daily Tenkan-sen, which should contain extended downticks.

Sterling may show stronger volatility during these days, as official divorce process between the UK and the EU starts tomorrow.

Res: 1.2580, 1.2613, 1.2671, 1.2689

Sup: 1.2550, 1.2523, 1.2500, 1.2467

EURUSD Is Consolidating Under Cracked 200SMA, Further Upside Favored

The Euro is consolidating under Monday's fresh high at 1.0905 (the highest traded since 11 Nov 2016), posted on Monday.

Bullish acceleration after Monday's gap-higher opening, cracked strong 200SMA barrier (1.0877), but failed to close above it, suggesting prolonged consolidation, before bulls resume.

Daily technicals maintain strong bullish momentum for further upside.

Sustained break above 200SMA would open next pivot at 1.0931 (Fibo 61.8% of 1.1298/1.0339), break of which would attract psychological 1.1000 barrier.

Rising hourly cloud continues to underpin, with solid support at 1.0821 (Monday's low, reinforced by weekly Kijun-sen), expected to contain consolidation and keep yesterday's gap unfilled.

Conversely, signals of deeper correction could be expected on loss of 1.0821 handle, with extension below 1.0760 (Friday's close) to confirm scenario.

Res: 1.0877, 1.0905, 1.0931, 1.1000

Sup: 1.0847, 1.0821, 1.0800, 1.0759

Markets Recover After Dow Suffered Longest Losing Streak Since 2011

Markets are calmer today after a steep selloff on Monday driven by concerns that Friday's decision to cancel voting on Obamacare bill might lead to difficulties to push through other U.S. pro-growth plans. Asian equities are back to green territory, oil prices recovered slightly, fixed income markets are steady, and similarly currency markets are moving in narrow trading ranges.

At this stage, U.S. markets will remain the key driver for global investors. The Dow Jones industrial average dropped for eight consecutive days heading into Monday; the longest losing streak since 2011, but nothing dramatic here given that the total declines are less than 2%. This selloff is obviously not a good sign, but it shows that investors are not yet in a stage of fear, but are somewhat on the defensive side.

Tax reforms, infrastructure spending, and deregulation. this is what's next on Trump's administration agenda. The success of execution on any of these legislations is probably lower now than it was just last week, but investors are still giving President Trump the benefit of the doubt. However, if they see that these plans will face the same destiny as the Health Care Act, markets will soon turn to aggressive selling as the expected companies' earnings growth and pace of economic recovery are not enough to support currently overstretched valuations.

The fixed income markets are not showing signs of enthusiasm either. U.S. Treasury bonds yield curve is flattening again with U.S. 10-year yields down more than 9% from March highs, and 30-year yields fell below 3%. This explains why the dollar lost much of its value, but more importantly, it indicates that fixed income investors do not see real signs of acceleration in inflation and economic growth.

Investors will turn their attention to Europe this week as U.K.'s Prime Minister Theresa May will officially trigger article 50 on Wednesday and start the two-year journey into the unknown. Meanwhile, Scottish Parliament is set to vote today on whether to hold another independence referendum. Interestingly, the pound was the best major performing currency yesterday rising 0.7% against the dollar. While the sterling strength was more of a USD weakness story, I believe any approach towards 1.27 will be a selling opportunity. The BoE seemed somehow hawkish when Kristin Forbes voted to raise rates on March 16, but I don't think this will be enough to overcome the challenges awaiting the U.K. when negotiations kick off with the E.U.

EURUSD May Face Some Limited Upside

On the updated count of EURUSD we see price trading in a possible zig-zag correction of a higher degree, with waves A and B already completed. Current bullish rally is wave C then, that can be in final stages if we consider that there is possible to count five subwaves up from 1.0495 swing low. So from an Elliott Wave perspective market may turn south with three waves minimum back to the area of a former wave four, at 1.0760. A sharp impulsive decline beneath that price would indicate that top is in place, so until that happens we need to keep in mind possible extensions up to 1.1000 area.

EURUSD, 4H

ECB Policymakers Provide More “Hawkish” Hints

The euro strengthened yesterday, following some relatively "hawkish" remarks from ECB Executive Board members Sabine Lautenschlager and Jens Weidman. Lautenschlager indicated that although the current ultra-loose ECB policy is necessary for now, the Bank should be prepared to change its stance as soon as the data are stable and there is a sustainable path towards the ECB's price stability objective. Weidman's comments were along the same lines. He said that he would like to see a less expansionary policy, but there is no sustainable price growth yet to justify something like that. Today, we will get to hear from another ECB Executive Board member, Benoit Coeure, and it will be interesting to see whether his comments echo those of his colleagues. If so, the euro could come under renewed buying interest.

Even though yesterday's comments are far from a clear signal that the ECB may actually change its policy anytime soon, they add to expectations that the era of ultra-loose monetary policy is approaching its final stages. They also place even more emphasis on the bloc's preliminary CPI data for March that come out on Friday, especially on the core rate. According to President Draghi this is the data point the Bank pays the most attention to. The rate is expected to have remained unchanged for the fourth consecutive month, but a potential uptick in coming months could fuel further speculation over a potential reduction in ECB stimulus as early as next year.

EUR/JPY traded higher on the aforementioned remarks, after it hit support once again near the 119.50 (S1) support territory. Nevertheless, the rebound was stopped by the 120.35 (R1) resistance. Even though the common currency outperformed most of its counterparts the last couple of weeks, it still underperformed the much stronger yen. This is evident by the price structure on the 4-hour chart where a near-term downtrend is in place since the 13th of March. Yes, we expect the euro to continue strengthening against other currencies, but we see the likelihood that it remains on the back foot against its Japanese peer, at least in the next few days. The bears may take advantage of the 120.35 (R1) resistance and perhaps pull the trigger for another test near 119.50 (S1).

Today's highlights

During the European day, the economic calendar is relatively light. The only noteworthy indicators we get are Sweden retail sales and PPI, both for February.

In the US, the Conference Board consumer confidence index for March is due out. The forecast is for the figure to have declined, but to still remain at an elevated level. We also get the S&P/Case-Shiller house price index for January, as well as the Richmond Fed manufacturing index for March. However, none of these indicators is usually a major market mover.

Since we get only second-tier indicators today, market participants are likely to lock their gaze on the six speakers we have on the agenda. Besides ECB's Coeure, we have speeches from Fed Chair Janet Yellen, Kansas City Fed President Esther George, Dallas Fed President Robert Kaplan, Bank of Canada Governor Stephen Poloz and Riksbank Governor Stefan Ingves. Although all of these speakers are important, we think that Yellen, Poloz, and Coeure are the three likely to steal the show.

With regards to Yellen, her comments will probably be scrutinized for any hints on when the Fed may raise rates next, and whether the summer FOMC meetings are appropriate candidates for such action. Having said that, we don't expect any major deviation from her comments two weeks ago at the March FOMC meeting, where she maintained a somewhat cautious tone, and did not offer any clear signs regarding the next rate move. If she continues to keep her cards close to her chest, then the reaction in USD may be limited.

As for BoC Governor Poloz, we have to note that in his last few appearances he maintained a more-dovish-than-expected tone, indicating that another rate cut remains on the table should downside risks materialize in the Canadian economy. USD/CAD edged north yesterday after it hit support at 1.3320 (S1) to emerge above the downside resistance line taken from the peak of the 9th of March. In our view, the break shifts the near-term outlook back to the upside and as such, we expect a test near 1.3410 (R1) soon. A break above that zone is possible to pave the way for our next resistance of 1.3440 (R2). The catalyst for further advances in this pair could be another set of dovish remarks by Governor Poloz today.

EUR/JPY

Support: 119.50 (S1), 118.70 (S2), 118.50 (S3)

Resistance: 120.35 (R1), 120.70 (R2), 121.45 (R3)

USD/CAD

Support: 1.3320 (S1), 1.3275 (S2), 1.3210 (S3)

Resistance: 1.3410 (R1), 1.3440 (R2), 1.3500 (R3)

GBP/JPY Daily Outlook

Daily Pivots: (S1) 138.29; (P) 138.70; (R1) 139.36; More...

Intraday bias in GBP/JPY remains neutral at this moment. Deeper decline is mildly in favor as long as 140.60 resistance holds. Below 137.75 will target 136.44 support and below. But we'd expect support from 50% retracement of 122.36 to 148.42 at 135.39 to contain downside and bring rebound. On the upside, break of 140.60 resistance will turn bias to the upside and send GBP/JPY through 144.77 resistance. Overall, price actions from 148.42 are forming a consolidation pattern.

In the bigger picture, price actions from 122.36 medium term bottom are still seen as a corrective pattern. Main focus is on 38.2% retracement of 195.86 to 122.36 at 150.42. Rejection from there will turn the cross into medium term sideway pattern. Or, sustained break of 50% retracement of 122.36 to 148.42 at 135.39 will turn outlook bearish for a test on 122.36 low. Though, sustained break of 150.42 will extend the rebound towards 61.8% retracement of 195.86 to 122.36 at 167.78.

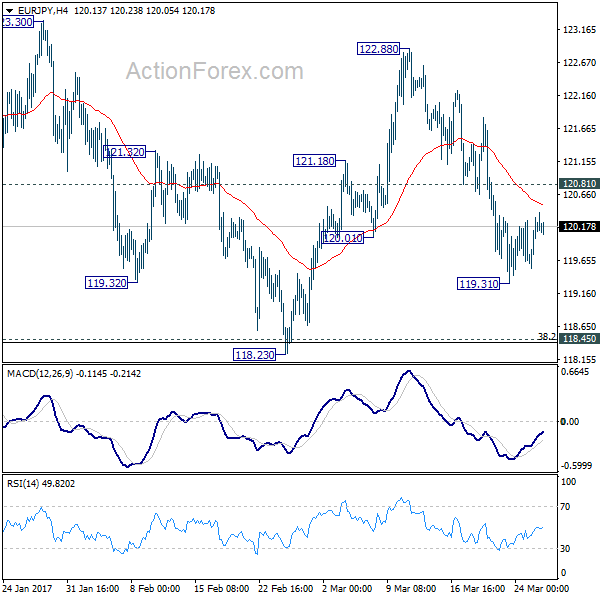

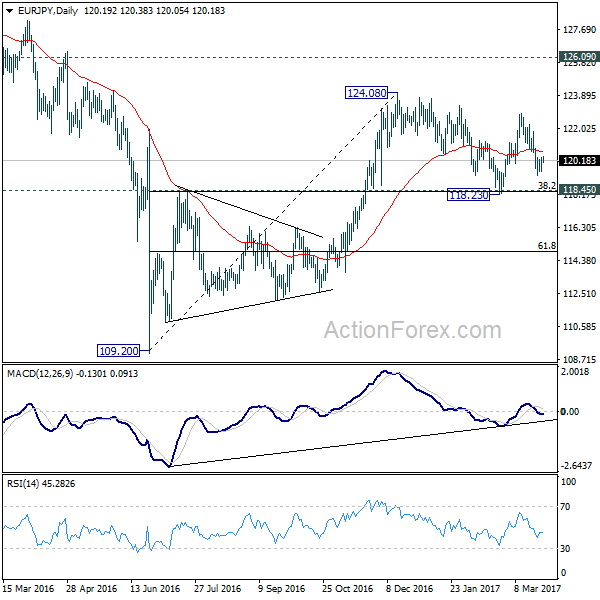

EUR/JPY Daily Outlook

Daily Pivots: (S1) 119.73; (P) 120.02; (R1) 120.51; More...

Intraday bias in EUR/JPY remains neutral for the moment. Below 119.31 will extend fall from 122.88 to 118.23 low. But we'd expect strong support from 118.45 key cluster support level (38.2% retracement of 109.20 to 124.08 at 118.39) to contain downside and bring rebound. On the upside, above 120.81 minor resistance will turn bias back to the upside for 124.08 high. Overall, price actions from 124.08 are developing into a consolidative pattern and upside breakout is expected later.

In the bigger picture, we're holding on to the view that medium term rise from 109.20 is still in progress. Focus is on 126.09 key resistance level. Sustained break will confirm completion of the whole decline from 149.76. And rise from 109.20 is of the same degree as the fall from 149.76. In such case, further rally would be seen to 104.04 resistance and possibly above before topping. Meanwhile, rejection from 126.09, or firm break of 118.45 cluster support, will likely extend the fall from 149.76 through 109.20 low.

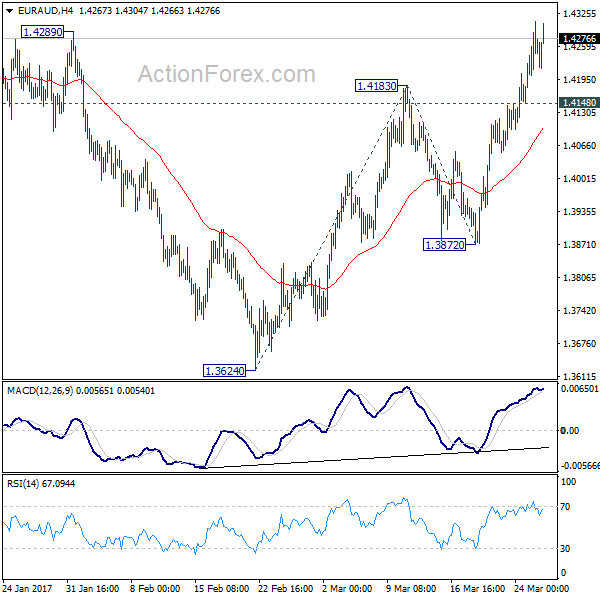

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.4186; (P) 1.4248; (R1) 1.4323; More...

Intraday bias in EUR/AUD remains on the upside for the moment. Current rise from 1.3624 should target 100% projection of 1.3624 to 1.4183 from 1.3872 at 1.4431 next. Decisive break there will indicate upside acceleration and target 1.4721 key resistance. On the downside, below 1.4148 minor support will turn bias neutral and bring consolidations first before staging another rally.

In the bigger picture, price actions from 1.6587 medium term top are viewed as a corrective pattern. Such correction could be completed after testing 1.3671 support. Break of 1.4721 cluster resistance (38.2% retracement of 1.6587 to 1.3624 at 1.4756) should confirm this case and target 61.8% retracement at 1.5455 and above. Overall, we'd expect the up trend from 1.1602 to resume later. However, sustained break of 1.3671 will invalidate our bullish view and would turn focus back to 1.1602 long term bottom.

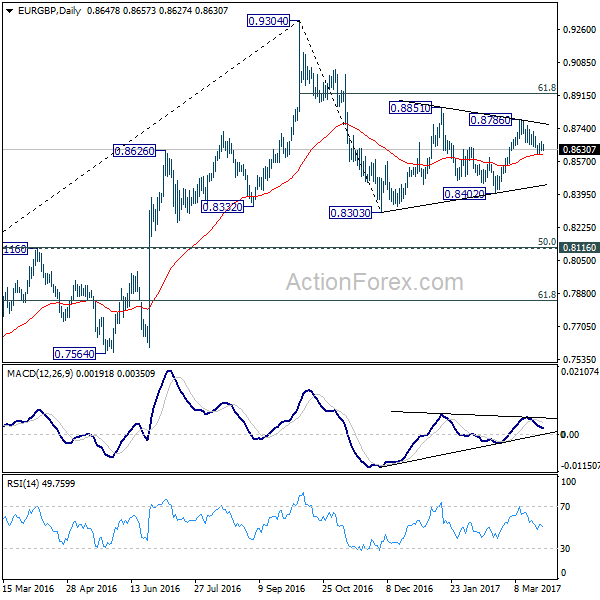

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8624; (P) 0.8649; (R1) 0.8674; More...

Intraday bias in EUR/GBP remains neutral for the moment. With 0.8699 minor resistance intact, deeper decline is mildly in favor. Below 0.8604 will target 61.8% of 0.8402 to 0.8786 at 0.8549 and possibly below. In that case, we'll look for support above to 0.8402 to bring another rebound before completing that correction from 0.8303. On the upside, above 0.8699 will turn bias back to the upside for 0.8786. Break will target 61.8% retracement of 0.9304 to 0.8303 at 0.8922 to finish the pattern from 0.8303. Overall, price actions from 0.8303 are forming a corrective pattern, as the second leg of the correction from 0.9304.

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. Deeper fall cannot be ruled out yet. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside. Overall, the corrective pattern would take some time to complete before long term up trend resumes at a later stage. Break of 0.9304 will pave the way to 0.9799 (2008 high).