Sample Category Title

Dollar Recovers as Sentiments Stabilized, No Change in Bearishness

Dollar gains some ground against European majors and Yen as market sentiments stabilized mildly. But near term outlook remains bearish and more downside should be seen in the greenback in near term. DJIA closed down -0.22% at -20550.98 after diving to as low as 20412.80. S&P 500 also closed down -0.1% at 2341.59 after hitting as low as 2322.25. Both indices drew support from 55 day EMAs and pared much losses before close. Nikkei recovers today by gaining 1.14% and is back above 19200. US President Donald Trump will remain a focus of the markets as his ability to implement his policies is in serious doubt. Trump will sign another executive order today to curb enforcement of climate regulations.

Chicago Fed Evans: Two is the "right number" for rate hike

Chicago Fed President Charles Evans said that US President Donald Trump's failure on health care act added to the many uncertainties remained. For him, two rate hikes this year "might be the right number if there's a little bit more uncertainty". And, "to the extent that I gain more confidence in the forecast I have, that would be a good indicator that I could perhaps support three." Some media quoted four hikes as a possibility but according to Evans, that's only "if things really take off, if we get continued strong growth and if underlying inflation really picks up".

Separately, Dallas Fed President Robert Kaplan reiterated his preference for a gradual pace of tightening. He noted that "you don't want to just slam on the brakes. You want to ease off of the accelerator first". And, at the same time, "monetary policy does operate with a lag."

ECB Praet: Premature to talk about stimulus exit

ECB Chief Economist Peter Praet indicated that deflation risk in the region is gone. Yet, it remains "premature to talk about exit". By contrast, Bundesbank President Jens Weidmann once again called for "less expansive" monetary policy. Indeed, Weidmann has been urging ECB to review the bond buying program. For instance, he questioned last week why "the ECB governing council shouldn't slowly consider an exit from very loose monetary policy". ECB executive board member Sabine Lautenschläger said the central bank should "prepare for a change in the policy and as soon as the data is stable and we have a sustainable path towards our objective of price stability then we are well prepared to do."

Scotland FM Sturgeon: Frustrated by not being listened

In UK, Prime Minister Theresa May met Scotland's First Minister Nicola Sturgeon in Glasgow yesterday for a meeting that last around an hour. Sturgeon expressed afterwards that she was "frustrated by a process that appears not to be listening. She has called for another independence referendum and the Scottish Parliament is expected to back her today. On the other hand, May repeated that "now is not the time" for another independence referendum for Scotland but kept herself open for one after Brexit process is complete.

UK PM May is scheduled to trigger Article 50 for Brexit tomorrow. Ahead of that, Brexit secretary David Davis said that the government had a "huge contingency plan" for UK leaving EU without a deal. Davis said there will be measures to restore control to the borders and the new system would be "properly managed". But he didn't specify anything on the changes to the immigration system.

On the data front...

US data are the main features today with trade balance, wholesale inventories, S&P Case-Shiller house price and consumer confidence featured.

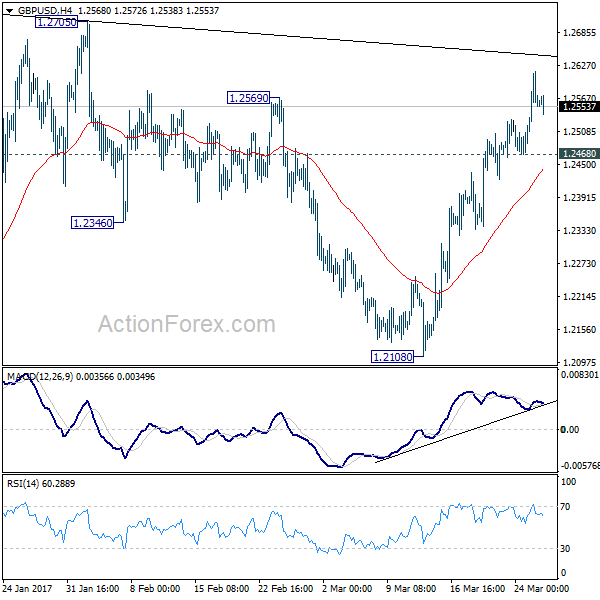

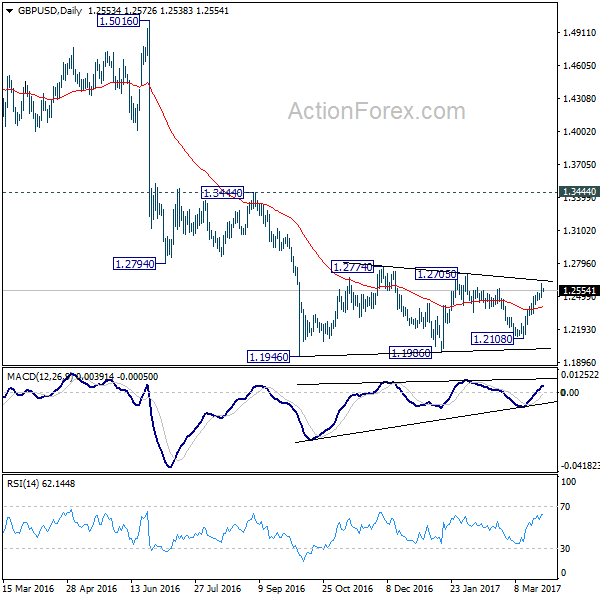

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2488; (P) 1.2551; (R1) 1.2621; More...

GBP/USD retreats mildly after hitting 1.2614. With 1.2468 minor support intact, further rise would be seen to 1.2705/74 resistance zone. Rise from 1.2108 is seen as part of the consolidation pattern from 1.1946. We'd expect upside to be limited by 1.2705/2774 to bring down trend resumption eventually. On the downside, below 1.2468 minor support will turn bias back to the downside for 1.2108 support first. Though, sustained break of 1.2774 will extend the rise towards 1.3444 key resistance level.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term reversal yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 12:30 | USD | Advance Goods Trade Balance Feb | -66.6B | -69.2B | ||

| 12:30 | USD | Wholesale Inventories Feb P | 0.20% | -0.20% | ||

| 13:00 | USD | S&P/Case-Shiller Composite-20 Y/Y Jan | 5.60% | 5.60% | ||

| 14:00 | USD | Consumer Confidence Mar | 113.7 | 114.8 |

Asian Market Update: Markets Recover As Selling On Failed US Healthcare Bill Subsides

Markets recover as selling on failed US healthcare bill subsides

US Session Highlights

(RU) Senate Intel Committee reportedly requests White House aide Jared Kushner to be interviewed regarding prior Russia meeting - press

(MX) Mexico Central Bank Gov Carstens: if bilateral relations go well, peso could strengthen to levels seen before the US election or even more - press interview

(QA) Qatar Energy Min: OPEC supply cut deal must be judged over the agreement's full cycle

(US) MAR DALLAS FED MANUFACTURING ACTIVITY: 16.9 V 22.0E

US markets on close: Dow -0.2, S&P500 -0.1%, Nasdaq +0.2%

Best Sector in S&P500: Healthcare

Worst Sector in S&P500: Telecom

Biggest gainers: HCA +5.2%, UHS +3.4%, BBY +3.0%, VIAB +2.9%, FLS +2.9%

Biggest losers: FCX -4.7%, FTR -3.4%, HAL -3.3%, KIM -2.6%, SEE -2.5%

At the close: VIX 12.5 (-0.5 pts); Treasuries: 2-yr 1.27% (+2bps), 10-yr 2.37% (-3bps), 30-yr 2.98% (-2bps)

US movers afterhours

PSIX: Announces strategic investment and collaboration agreement with Weichai America Corp; +47.7% afterhours

RHT: Reports Q4 $0.61 v $0.61e, R$629M v $619Me; +5.3% afterhours

DRI: Reports Q3 $1.32 v $1.27e, R$1.88B v $1.86Be (earnings released a day early); Raises FY17 $3.95-4.00 v $3.93e, guides SSS ~1.5%; +3.9% afterhours

SNX: Reports Q1 $1.82 v $1.66e, R$3.52B v $3.50Be; +2.2% afterhours

DECK: Red Mountain (3.3% stake) calls on Deckers to explore sale of the company; +1.8% afterhours

HUN: Guides Q1 adj EBITDA to exceed $274M; provides restart time-line for Pori, Finland Pigment Facility; +0.7% afterhours

Politics

(US) US White House press secretary Spicer: August is potential target date for tax reform, depends on consensus on 'big issues'

(US) Seven Democratic Senators ask Carl Icahn to explain role in the Trump administration - press

(US) House Ways & Means Chair Brady (R-TX): not looking to repeal Obamacare taxes via upcoming tax reform legislation

(US) White House said to consider infrastructure and tax reform as a package deal; Prepared to work with Democrats after feeling burned by Freedom Caucus - Axios

Asia Key economic data:

(KR) SOUTH KOREA Q4 FINAL GDP Q/Q: 0.5% V 0.4%E; Y/Y: 2.4% V 2.3%E

(AU) Australia ANZ Roy Morgan Weekly Consumer Confidence Index: 113.8 v 112.0 prior

Asia Session Notable Observations, Speakers and Press

Key Asian equity indices are higher with the exception of the mainland, as market takes note of the rebound on Wall St to much more benign losses relative to the tumble in the morning session. Investors are willing to test a bottom in hopes that the White House has learned its lesson from the healthcare debacle to seek a broader consensus as it moves forward to more economy sensitive tax reform, deregulation, and infrastructure investment. Indeed, an Axios report notes that Trump is prepared to work more with the Democrats after feeling burned by Freedom Caucus while combining tax reform with an infrastructure investment initiative that may be an easier sell to the left. However, POTUS was also active on Twitter late on Monday, claiming that Democrats will come to him to fix healthcare once Obamacare fails

In FX, JPY was under some early pressure on risk-on flows, with USD/JPY rising about 25pips above 110.80. Other USD majors are consolidating recent greenback selling in narrow ranges with an eye on Tuesday's Consumer Confidence data.

Asia economic calendar is very light until Friday of this week. Today's only notable data were Q4 GDP figures from South Korea, where final prints rose slightly from prelim levels on smaller decline in construction investment and CAPEX.

In China, CNY weakened after PBoC set its yuan fix lower for the first time in 5 days. PBoC also skipped its open market operations for the first time in 3 days pledging it will maintain relatively tight liquidity. On that note, Hong Kong earnings season is entering its final stretch with China's top banks on tap for FY16 results.

China

(CN) China Govt: China continues to face serious challenges in cutting steel overcapacity

(CN) PBoC said to maintain relatively tight liquidity - Chinese press

(CN) China Finance Ministry: Jan-Feb profit for China SOEs rose 40.3% y/y to CNY301.9B; Rate of growth rose from 1.7% in 2016 and 14.2% y/y - Chinese press

Japan

(JP) Former BOJ Chief Economist Momma: BOJ should adopt rate guidance to improve its communication with the market and give clearer signals on the direction of borrowing costs

(JP) Japan Fin Min Aso: Japan Cabinet asks for smooth enactment of FY17 budget

Korea

(KR) North Korea said to have conducted another missile engine test last Friday - financial press

Asian Equity Indices/Futures (00:30ET)

Nikkei +1.0%, Hang Seng +0.5%, Shanghai Composite -0.3%, ASX200 +1.2%, Kospi +0.2%

Equity Futures: S&P500 +0.2%; Nasdaq +0.2%; Dax +0.1%; FTSE100 +0.1%

FX ranges/Commodities/Fixed Income (00:30ET)

EUR 1.0855-1.0870; JPY 110.50-110.80; AUD 0.7610-0.7635; NZD 0.7035-0.7050

Apr Gold -0.1% at $1,255/oz; May Crude Oil +0.5% at $47.98/brl; May Copper -0.3% at $2.63/lb

SPDR Gold Trust ETF daily holdings rise 2.7 tonnes to 835.3 tonnes

(CN) PBOC SETS YUAN MID POINT AT 6.8782 V 6.8701 PRIOR; First weaker setting in 5 days

(CN) PBoC skips open market operations for 3rd straight session; Said to drain ¥70B

(AU) Australia MoF (AOFM) sells A$150M in 2.0% 2035 inflation-indexed Bonds; avg yield: 1.0930%; bid-to-cover: 5.63x

Asia equities/Notables/movers by sector

Consumer discretionary: 493.HK Gome Electrical Appliances +1.0% (FY16 result); 1055.HK China Southern Airlines -2.2% (cooperation with American Airlines); 3197.JP Skylark Co -4.4% (Bain Capital may sell partial stake); MTR.AU Mantra Group +11.9% (buyout speculation); MYR.AU Myer Holdings -5.0% (block trade)

Consumer staples: 1610.HK COFCO Meat Holdings +1.7% (FY16 result)

Financials: 1112.HK Biostime International Holdings +5.2%, 1918.HK Sunac China Holdings +9.4% (annual result)

Industrials: 822.HK Kai Shui International Holdings +3.3%, 3969.HK China Railway Signal & Communication Corporation -3.0% (FY16 result)

Technology: 110.HK China Fortune -2.9% (profit warning); 6899.HK Ourgame International Holding -6.0%, 981.HK Semiconductor Manufacturing International Corp +3.6% (FY16 result); 2039.HK China International Marine Containers Group +3.2% (FY16 result)

Materials: 893.HK China Vanadium Titano-Magnetite Mining -4.6% (FY16 result); SYR.AU Syrah Resources +5.4% (signs MOU)

US Fixed Income Markets Are Also Losing Some Momentum

Market movers today

It is a fairly thin data calendar today.

In the US, we are due to get Conference Board Consumer Confidence for March. The preliminary numbers from the University of Michigan for March indicate that consumer confidence remained at a very high level in March and we expect the Conference Board figures to confirm this impression. Hence, we estimate the March Conference Board figure will be 114.0.

Selected market news

Global risk sentiment improved after the sell-off prompted by the failure by the US Congress to pass legislation to repeal Obamacare. This morning, most Asian indices are rebounding in line with the recovery in US stocks yesterday. US Fixed income markets are also losing some momentum after the rally since mid-March. Equity markets appear to have taken comfort in the fact that less aggressive fiscal policies in the US may prompt weaker inflation pressures, which will allow the Federal Reserve to refrain from hiking rates as much as it has indicated. Yesterday, Fed Bank of Chicago President Charles Evans said that two hikes may be the right amount of tightening for the US economy this year, given the uncertainty surrounding the outlook for inflation and government spending.

Ahead of the expected triggering of Article 50 by the UK government this week, tension is already growing between the EU and the UK government. UK Brexit Secretary David Davis said that Britain will pay ‘nothing like' the sums of money European Union officials have floated as needing to be paid when the UK leaves. Over the weekend, EU commission president Jean- Claude Juncker said the UK will be expected to pay around GBP50bn (covering liabilities such as pensions for EU officials, infrastructure projects and the bail-out of Ireland). The UK side is rebuking such figures as there has been ‘no explanation' for the amount.

In South Africa, political risk premia flared up again after Finance Minister Pravin Gordhan was called back from an investor road trip to London by President Jacob Zuma. This prompted speculation that Gordhan will be replaced as Finance Minister by Brian Molefe, a relatively new member of parliament. Molefe has sat on the boards of some of South Africa's biggest stateowned enterprises and has also worked at the Treasury. We think the markets will see him as a weaker minister than Gordhan if he is appointed to the role. As a result, the USD/ZAR shot up by 2% yesterday when the news broke. We think that the ZAR could weaken by more in the coming days if the stories take hold.

USDJPY Elliott Wave View: Extension lower

We are taking the more aggressive view in USDJPY and calling the rally to 115.48 on 3/10 as Intermediate wave (B). Decline from there is unfolding as a 5 waves impulse Elliott wave structure with an extension in wave 3. Down from 115.5, Minor wave 1 ended at 114.46 and Minor wave 2 ended at 115.2. Minor wave 3 is extended and further subdivided into 5 impulse waves where Minute wave ((i)) ended at 112.88, Minute wave ((ii)) ended at 113.56 and Minute wave ((iii)) ended at 110.59, Minute wave ((iv)) ended at 111.34, and Minute wave ((v)) of 3 is proposed complete at 110.077. Minor wave 4 bounce is currently in progress towards 111.27 – 112.02 area, which is 23.6 – 38.2 retracement of Minor wave 3, before further downside is seen to complete Minor wave 5 towards as low as 106.85 – 108.5 area. Bounce is expected to be limited and shallow.

If the current bounce gets too big, then as an alternate, the move lower in USDJPY from 115.5 high is unfolding as a zig zag Elliottwave structure where Minor wave A ended at 110.077 low with subdivision of 5 impulsive waves . In this alternative view, current bounce will then be bigger as it’s a Minor wave B bounce to correct decline from 3/10 high (115.52), but still as far as pivot at 115.2 stays intact, pair should resume lower again in Minor C. This alternate view is the less aggressive view but still calling for more downside in the pair as far as pair stays below 3/10 high. In both views (aggressive and less aggressive), we don’t like buying the pair.

1 Hour USDJPY Elliott Wave Chart

AUDUSD Stuck Within A Consolidation Pattern

Key Points:

- Price action trading sideways within a consolidative pattern.

- RSI Oscillator trending lower.

- Watch for a break down in the days ahead.

The past few days has seen the AUDUSD continue to trend in largely a sideways manner within a relatively tight 50 pip range. Subsequently, there has been little in the way of a defined trend and the pair remains meandering around 50% of the March move at 0.7619. However, there is likely to be a breakout in the coming week given that there are some key economic events pending that may, finally, fuel a move for the Aussie.

In particular, the AU HIA New Home Sales figures are likely to be watched closely given the current precariousness of the Australian property market. There have been some indications of a slowdown over the past few months and the large lending institutions are certainly skittish about their exposure. Subsequently, we may see the impact of restricted credit flowing through the new home sales figures. A significant miss could see the pair under pressure as the market takes a negative short term view of the Aussie.

Also, there is plenty of scope for volatility on the greenback side of the fence in the days ahead. The U.S. Final FDP and Unemployment Claims figures are due out Thursday and are likely to fuel a revaluation for the USD. In particular, a jobless claims result below the forecasted 245k could be just the thing the greenback needs to rally against most of the cross pairs. This is a fairly realistic scenario and could additionally bring about a needed breakdown for the Aussie.

From the technical perspective, price action is now trending lower, within its consolidative range, towards a key support zone at 0.7605. This is a major downside hurdle for the pair, representing the low from February, and will need to be breached to signal the commencement of a pullback. In addition, the RSI Oscillator is also trending lower, within neutral territory, indicating that there is still plenty of room to move on the downside.

Ultimately, it remains to be seen which direction the pair will break in the near term but the reality is that break it must. The consolidative pattern has lasted for a significant period of time at the 50% of March level and a breakout is now all but inevitable. However, the evidence is suggesting that we are likely to see a downside move, especially given the presently high valuation for the Aussie. Subsequently, keep a keen watch on the pair over the next few days as a move through support at 0.7605 could signal the start of a sharp depreciatory phase.

Has The Silver Rally Done Its Dash Or Is More Still To Come?

Key Points:

- ABCD wave could see further gains after a near-term moderation.

- MACD and EMA suggestive of general bullish trend in the long-term

- Fundamentals also supportive of extending bullish momentum.

Silver's long-term uptrend may be due for a spell of moderation moving ahead as the metal prepares to make a final push higher in the coming weeks. Specifically, the combination of a number of technical forces is beginning to put pressure on silver prices, even if the general bias remains long-term bullish.

Firstly, if we take a look at the daily chart a few things become readily apparent. For one, the combination of the declining trend line and some highly oversold stochasticreadings are practically begging for a reversal in the coming sessions. However, it's also clear that this reversal will likely be short-lived and more of a moderating movement than a serious change in momentum. As a result, any near-term losses should be capped by the 23.6% Fibonacci level at around the 17.791 handle and the uptrend should resume around this point.

All this being said, what exactly is the evidence supporting continued bullishness over the coming weeks? Primarily, we would look to the fairly convincing ABCD wave that is becoming clearer on the above daily chart to support the argument for additional gains in silver prices. However, we can also see that the EMA bias and the MACD signal line crossover are supportive of this forecast which should see the metal pushing the 19.00 handle moving ahead. Gains beyond this price currently seem unlikely, given the robust zone of resistance present around this handle.

From a fundamental perspective, we have even greater reason to suspect that the uptrend will remain in place after a short period of moderation. Unsurprisingly, this has everything to do with Trump and the uncertainty his administration presents for the US. Indeed, only yesterday the Fed's Evans spoke on how the recent failure of the GOP's Healthcare bill demonstrates rising uncertainty and political risk in the US. As one would expect, growing unease over the stability of the world's largest economy and military power has been a key driver of safe haven investment prices over the past weeks and this momentum doesn't look like its ready to evaporate anytime soon.

Ultimately, the agreement of both the technical and fundamental forecasts discussed above present a fairly strong argument for a near-term slip followed by a resumption of the uptrend. In particular, the presence of the ABCD wave and the ongoing turmoil of the Trump presidency should be the two key drivers informing the metal's movement and both should be monitored closely.

Foreign Exchange Market Commentary

EUR/USD

The unwind of the 'Trump trade' gathered momentum this Monday, resulting in the EUR/USD pair rallying to a fresh yearly high of 1.0905 at the beginning of the US session. Risk aversion dominated the Asian and European sessions, after the US GOP decided to pull out the healthcare bill set to overhaul the Obamacare late Friday. Speculative interest is now wondering if the US new administration will be able to push forward its pro-growth agenda, promised during the campaign.

The common currency gapped lower at the weekly opening, further rallying after London's opening after the release of a better-than-expected German IFO confidence survey, which showed that than business sentiment unexpectedly improved in March, up to 112.3 from a previous 111.1, the highest reading since mid 2011. The US released a minor report, the Dallas Fed manufacturing index, which fell in March to 16.9 from previous 24.5, while a Fed's Evan hit the wires, adding nothing new on monetary policy to what the market already knew.

The dollar recovered some ground in the US afternoon as Wall Street bounced from fresh six-week lows, but overall remains subdued, and at risk of falling further. The 4 hours chart for the EUR/USD pair shows that the price is well above the 1.0820/30 region, the 50% retracement of the post-US election's decline and former yearly high, while the 20 SMA keeps advancing below it. Technical indicators in the mentioned chart have lost upward strength, pulling modestly lower within overall readings, not enough to suggest further declines ahead. Buying interest is likely waiting in the mentioned 1.0820/30 region, although a break below it could result in a slide down to 1.0790, where the pair will fill the weekly opening gap.

Support levels: 1.0765 1.0730 1.0700

Resistance levels: 1.0830 1.0870 1.0910

USD/JPY

The USD/JPY pair tumbled to a fresh yearly low of 110.10 this Monday, undermined by a continued decline in worldwide equities that fueled demand for the safe-haven yen. Trump's defeat on his healthcare bill fueled demand for Treasury bonds, which sent yields lower at the beginning of the day. The 10-year note yield fell to 2.36% before recovering modestly to end the day in the red anyway at 2.38%. The yield of the two-year note traded as low as 1.236%, before also recovering modestly. Nevertheless, the pair is intrinsically bearish, now trading below the previous yearly low of 110.62, the immediate resistance. In the 4 hours chart, the price remains well below its 100 and 200 SMAs, with the shortest crossing below the largest but both still lagging amid the strength of the latest bearish move, whilst technical indicators have lost their upward strength after correcting oversold readings, indicating that the current advance is just corrective. The pair has a major support at 109.90, the 50% retracement of the late 2016 rally, and a break below it should see the bearish momentum accelerate this Tuesday.

Support levels: 110.30 109.90 109.50

Resistance levels: 110.65 111.00 111.45

GBP/USD

The GBP/USD pair traded as high as 1.2614, its highest in almost two months, before pulling back to settle around 1.2565. There were no macroeconomic news in the UK, with broad dollar's weakness leading the way higher. UK PM Theresa May is expected to trigger the Brexit process next Wednesday, March 29th, and ahead of the announcement, met with Scottish PM Nicola Sturgeon. Sturgeon has called for a second Scotland independence referendum, against May's will, but the terror attack from last week has interrupted the tense relations between them both. After officially lunching the Brexit, the UK will have two years to negotiate new arrangements, after which it will no longer be subject to EU treaties. The latest downward corrective movement has not been enough to confirm an interim top in the pair, as it would take a break below 1.2535, the 23.6% retracement of the January´s rally to see it falling further. In the 4 hours chart, the price is also developing above a bullish 20 SMA, whilst technical indicators have retreated within positive territory, with the Momentum nearing 100, but the RSI around 67, this last losing downward strength and pretty much indicating limited selling interest at the time being.

Support levels: 1.2535 1.2500 1.2465

Resistance levels: 1.2585 1.2620 1.2660

GOLD

Spot gold closed the day higher at $1,255.78 a troy ounce after peaking at a fresh 1-month high of 1,260.95, retreating in US trading hours as risk aversion eased partially, but with the dollar anyway beaten by the Obamacare repeal bill's failure. With two more US Fed rate hikes priced in, the commodity seems poised to extend its recovery, as the FOMC no longer weighs on gold while political woes seem to be only beginning across the world. The daily chart for the commodity shows that the price managed to extend above its 200 DMA for the first time since late October 2016, while technical indicators have barely lost their upward strength within overbought territory, rather reflecting diminishing volumes at the end of the day than suggesting upward exhaustion. In the shorter term and according to the 4 hours chart, the risk remains towards the upside, as the price is well above a bullish 20 SMA, now the immediate dynamic support at 1,248.95, whilst technical indicators have resumed their advances within positive territory after correcting overbought conditions.

Support levels: 1.248.95 1,240.90 1,233.25

Resistance levels: 1,263.80 1,272.80 1,283.10

WTI CRUDE

Oil prices fell this Monday, with West Texas Intermediate crude oil futures ending the day at $47.69 a barrel. The commodity edged lower, despite oil producers pledged to extend their output cut deal past June during a weekend meeting. Russia was the only country that assisted to the meeting but said it needs more time before making a decision. The US benchmark bounced after retesting last week low of 47.07, but anyway maintains the bearish bias, as in the daily chart, the 20 DMA is now crossing below the 200 DMA far above the current level, the Momentum indicator eases its recovery below the 100 level, while the RSI indicator turned back south around 30, all of which supports additional declines towards the 45.00 region. In the 4 hours chart, the price is below its 20 SMA, although the indicator has lost is bearish slope and turned horizontal, whilst technical indicators have recovered within negative territory, but remain below their mid-lines, limiting chances of an upward corrective movement.

Support levels: 47.00 46.40 45.90

Resistance levels: 48.30 48.80 49.50

DJIA

Wall Street tumbled at the opening, with the three main American indexes falling to fresh six-week lows amid declines in overseas equities led by risk aversion. Fears that US President Donald Trump won't be able to deliver the growth agenda that includes tax reforms and infrastructure investment arose after the GOP had to pulled out the healthcare bill last Friday. Equities trimmed most of their intraday losses as concerns eased modestly, and the Nasdaq Composite managed to close in the green, up 11 points to 5,840.37. The Dow Jones and the S&P, however, closed in the red, with the first shedding 46 points to 20,550.91 and the second closing at 2,341.59, down 0.10%. The Dow closed in the red for eighth consecutive session, with the worst performer being Chevron that fell 1.48%, followed by Goldman Sachs that shed 1.39%. El du Pont was the best performer adding 1.27%, followed by Pfizer that gained 0.68%. The daily chart for the Dow shows that technical indicators decelerated their declines near oversold readings, but also that the benchmark posted a lower low and a lower high below a bearish 20 DMA, all of which maintains the risk towards the downside. In the 4 hours chart, the index remains below a sharply bearish 20 SMA, currently providing a dynamic resistance at 20,614, while technical indicators have bounced within bearish territory, but present limited upward strength, in line with the loner term perspective.

Support levels: 20,528 20,467 20,409

Resistance levels: 20,614 20,648 20,707

FTSE 100

The FTSE 100 settled at 7,293.50, down 0.59% or 43 points, but off its daily low of 7,254. Distrust on Trump's ability to activate the growth agenda promised after his victory sent investors away from high yielding assets. A stronger Pound also weighed on the Footsie, and within the benchmark, mining-related equities led the decline, as base metals fell on the continued unwind of the Trump trade, with Antofagasta being the worst performer, down 4.70%, followed by Glencore that shed 4.38%. Next led advancers, up 2.47% followed by Centrica that added 1.43%. Technical readings in the daily chart favor additional declines, as the index stands further below its 20 SMA, the Momentum indicator holds flat around 100, while the RSI indicator heads south around 45. In the 4 hours chart, the 20 SMA has crossed below the 100 SMA above the current level, while the Momentum indicator failed to surpass its 100 level before resuming its decline, and the RSI indicator consolidates around 38, all of which maintains the risk towards the downside.

Support levels: 7,284 7,254 7,220

Resistance levels: 7,319 7,357 7,392

DAX

European equities extended their decline at the beginning of the week, following the lead of their Asian counterparts. The German DAX shed 67 points and settled at 11,996.07, although it recovered above the 12,000 level in after-hours trading, amid Wall Street's bounce from intraday multi-week lows. Industrial and utilities-related equities led the decline within the German benchmark, with RWE AG losing 1.78%, followed by Heidelberg Cement that lost 1.38% and ThyssenKrupp that closed down 1.33%. Infineon Technologies was the best performer by adding 0.53%. Despite the early intraday decline, the daily chart for the DAX shows that it settled above a bullish 20 SMA, whilst the Momentum indicator holds neutral around its mid-line and the RSI indicator turned lower, but holds at 56, limiting chances of further declines. In the shorter term and according to the 4 hours chart, the index is biased higher, as it's currently trading above its 20 and 100 SMAs, both around 11,980, while the RSI indicator aims higher around 52 and the Momentum also advances modestly above its mid-line.

Support levels: 11,976 11,928 11,880

Resistance levels: 12,055 12,091 12,139

AUD/USD: Aussie Trading On A Stronger Footing In The Morning Session

For the 24 hours to 23:00 GMT, the AUD rose 0.08% against the USD and closed at 0.7620.

LME Copper prices declined 1.9% or $109.0/MT to $5673.5/MT. Aluminium prices declined 0.1% or $1.5/MT to $1916.0/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7625, with the AUD trading 0.07% higher against the USD from yesterday’s close.

The pair is expected to find support at 0.7604, and a fall through could take it to the next support level of 0.7583. The pair is expected to find its first resistance at 0.7647, and a rise through could take it to the next resistance level of 0.7669.

With a lack of major economic releases in Australia today and tomorrow, investors will focus on Australia’s HIA new home sales data for February, slated to release on Thursday.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

EUR/USD: German Business Confidence Increased To Its Strongest Level Since 2011 In March

For the 24 hours to 23:00 GMT, the EUR rose 0.23% against the USD and closed at 1.0864, after Germany's Ifo business climate index surprisingly advanced to a nearly seven-year high level of 112.3 in March, underscoring optimism over the health of the nation's business sector, despite rumblings of protectionism across the Euro-zone. Markets expected the index to remain steady at a revised level of 111.1, registered in the prior month.

Additionally, the nation's Ifo business expectations index climbed more-than-expected to a level of 105.7 in March, against market expectations of an advance to a level of 104.3 and after recording a reading of 104.2 in the prior month. Also, the nation's Ifo current assessment index registered an unexpected rise to a level of 119.3 in March, confounding expectations of a drop to a level of 118.3 and compared to a level of 118.4 in the previous month.

In the US, the Chicago Federal Reserve (Fed) President, Charles Evans, stated that three interest rate hikes remain more plausible this year, but two rate hikes are also conceivable, as the outlook remains uncertain, particularly with the latest failure of the healthcare bill. Nevertheless, he also added that the central bank could raise interest rates four times this year if inflation picks up markedly.

Separately, the Dallas Fed President, Robert Kaplan, indicated that he would support further monetary policy tightening if the US economy continues to show progress and nears the central bank's dual mandate of full employment and 2.0% inflation.

In the Asian session, at GMT0300, the pair is trading at 1.0859, with the EUR trading slightly lower against the USD from yesterday's close.

The pair is expected to find support at 1.0830, and a fall through could take it to the next support level of 1.0801. The pair is expected to find its first resistance at 1.0896, and a rise through could take it to the next resistance level of 1.0933.

With no crucial economic releases in the Euro-zone today, investors would direct their attention to a speech by the US Fed Chief, Janet Yellen, scheduled later today. Moreover, the US CB consumer confidence index for March as well as advance goods trade balance and wholesale inventories data, both for February, will garner a significant amount of market attention.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

GBP/USD: Pound Trading A Tad Higher In The Asian Session

For the 24 hours to 23:00 GMT, the GBP rose 0.4% against the USD and closed at 1.2561.

In the Asian session, at GMT0300, the pair is trading at 1.2563, with the GBP trading slightly higher against the USD from yesterday’s close.

The pair is expected to find support at 1.2510, and a fall through could take it to the next support level of 1.2456. The pair is expected to find its first resistance at 1.2616, and a rise through could take it to the next resistance level of 1.2668.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.