Sample Category Title

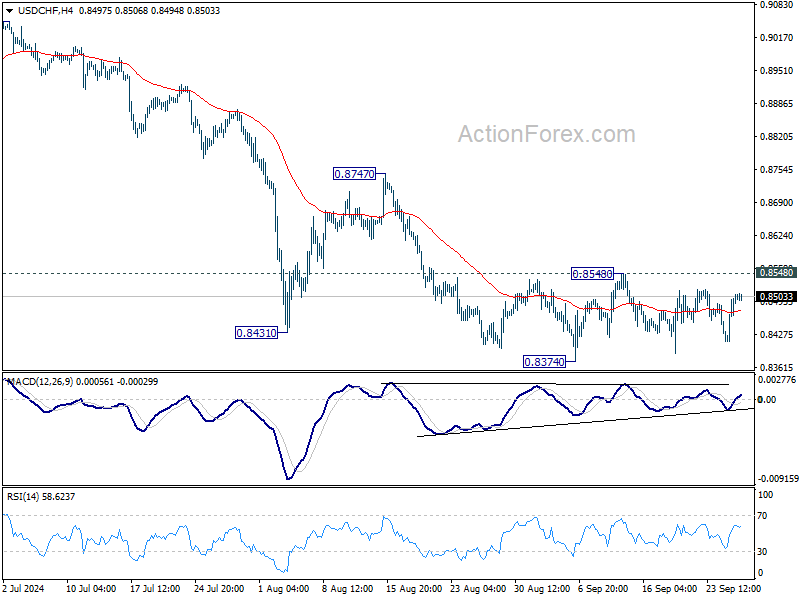

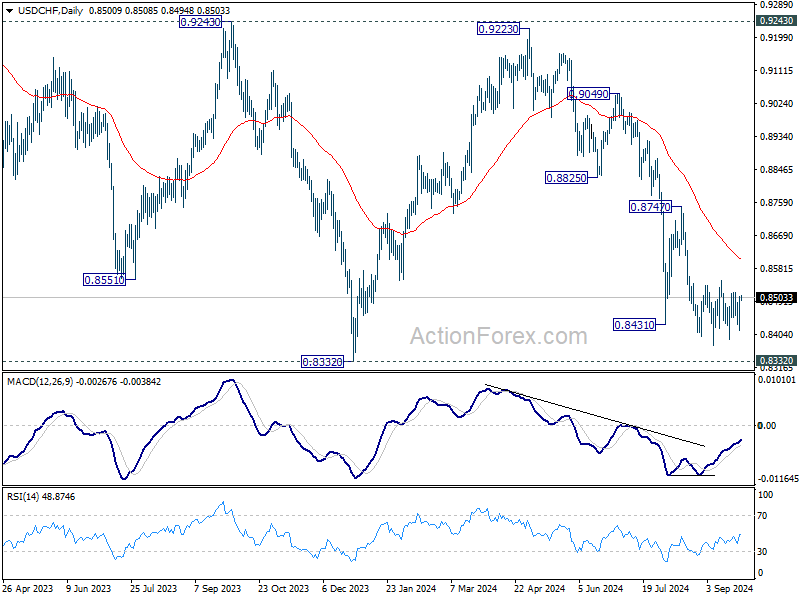

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8444; (P) 0.8475; (R1) 0.8536; More…

No change in USD/CHF's outlook as range trading continues and intraday bias stays neutral. On the downside, break of 0.8374 will resume the fall from 0.9223 to retest 0.8332 low. Decisive break there will indicate larger down trend resumption. However, break of 0.8548 resistance will confirm short term bottoming, and turn bias back to the upside for 0.8747 resistance.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with fall from 0.9223 as the second leg. Strong support could be seen from 0.8332 to bring rebound. Yet, overall outlook will continue to stay bearish as long as 0.9243 resistance holds. Firm break of 0.8332, however, will resume larger down trend from 1.0146 (2022 high).

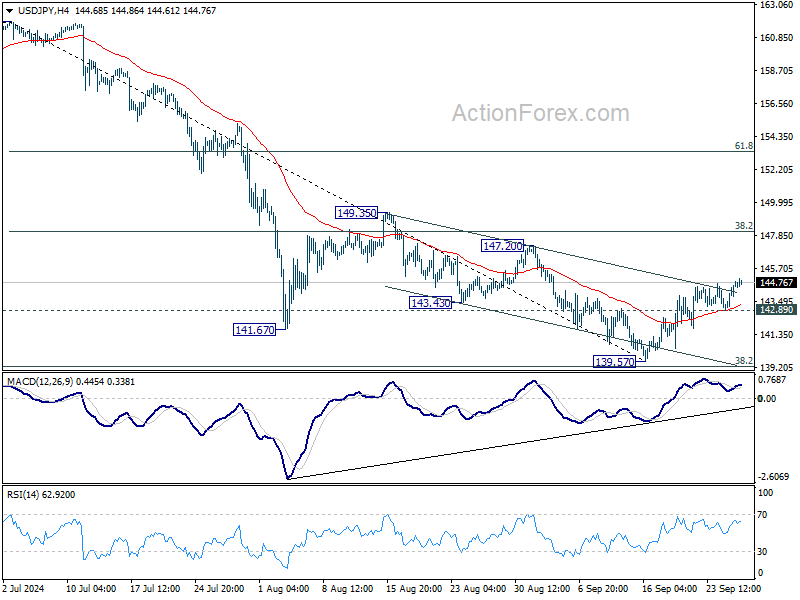

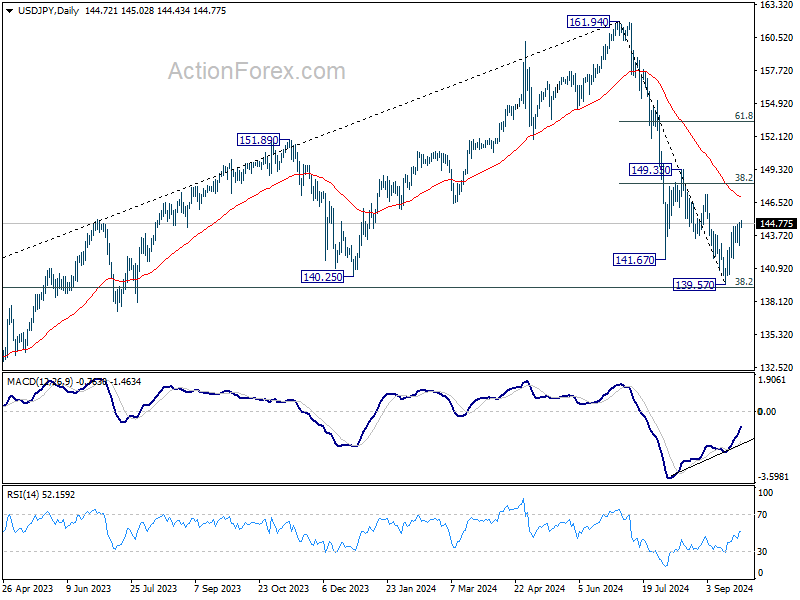

USD/JPY Daily Outlook

Daily Pivots: (S1) 143.49; (P) 144.17; (R1) 145.42; More...

USD/JPY's rebound from 139.57 short term bottom is still in progress and intraday bias stays on the upside. Further rally would be seen to 38.2% retracement of 161.94 to 139.57 at 148.11. On the downside, below 142.89 minor support will turn bias to the downside for retesting 139.57 instead.

In the bigger picture, fall from 161.94 medium term top is seen as correcting whole up trend from 102.58 (2021 low). Strong support could be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to contain downside, at least on first attempt. But in any case, risk will stay on the downside as long as 149.35 resistance holds. Sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

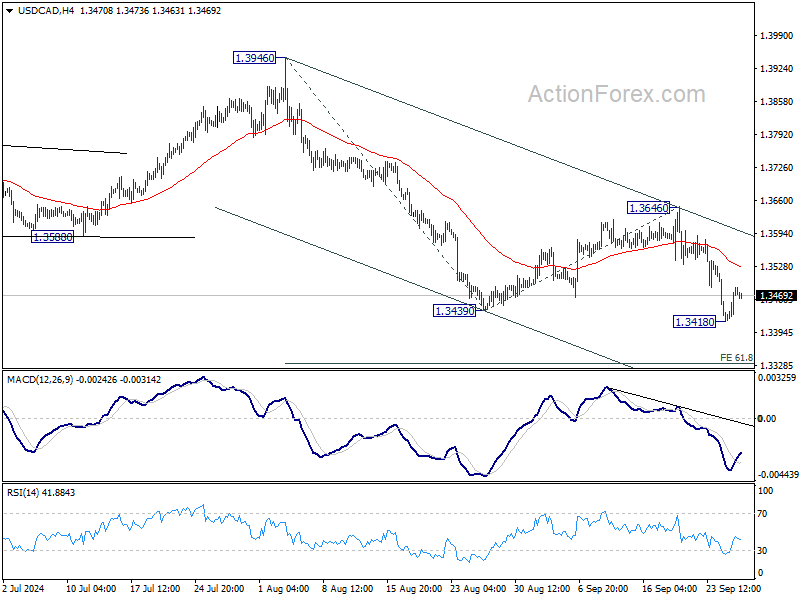

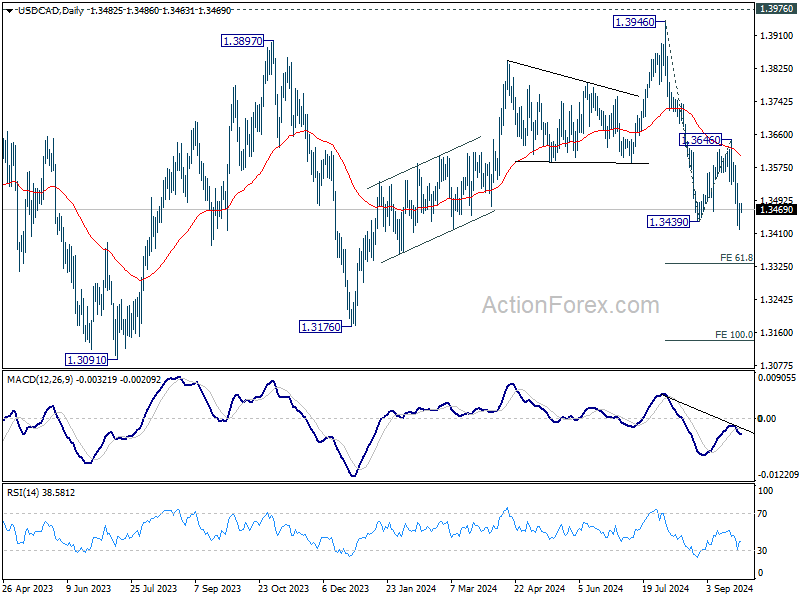

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3439; (P) 1.3466; (R1) 1.3511; More...

A temporary low is formed at 1.3418 with current recovery, and intraday bias in USD/CAD is turned neutral first. Some consolidations would be seen first, but outlook will stay bearish as long as 1.3646 resistance holds. Below 1.3418 will resume the decline from 1.3946 to 61.8% projection of 1.3946 to 1.3439 from 1.3646 at 1.3333.

In the bigger picture, corrective pattern from 1.3976 (2022 high) is extending with another falling leg. While deeper decline could be seen, strong support should emerge above 1.2947 resistance turned support to bring rebound. Rise from 1.2005 (2021 low) is still in favor to resume at a later stage.

Waiting on Speech by Fed Powell With Second Tier US Data

Markets

Core bond yields grinded higher yesterday in a news-poor trading session. With the move both US and German yields recouped most of Tuesday’s intraday losses. Net daily changes varied between +2 bps (2-yr) and +5.6 bps (10-yr, 30-yr) in the US and +1.3 bps (30-yr) and +3 bps (5-yr) in Germany. China’s equity boost to the broader equity markets fizzled. The EuroStoxx50 shed about 0.5%, major indices in the US were flat to down 0.7% (DJI). Currency markets were the playground of technical traders. The dollar started weak with the trade-weighted index testing the September lows around 100.2 and EUR/USD attacking the 1.1202 resistance level. But the greenback prevented a break lower and some return action kicked in instead. DXY eventually closed just south of 101 and EUR/USD slid back to 1.1133. JPY weakness helped USD/JPY to close at the highest level in three weeks (144.75).

It’s as if the Chinese were reading along. Some quotes coming from the Politburo during its monthly huddle jolted a dull Asian session in its final trading hours. Chinese authorities promise to implement “forceful” interest rate cuts and said they’ll ensure the necessary fiscal spending. The latter is seen as a critical complementary element to the string of monetary measures announced this Monday aimed to jumpstart the economy. The growing sense of urgency is underscored by the fact that the Politburo discussed the economic situation at the September meeting, whereas this is usually done only in April, July and December. The Chinese CSI300 stock index promptly extended gains to 3%. USD/CNY (7.018) holds on to previous gains. We expect to see some positive fall-out on European markets. Bourse futures suggested a solid green open. For most of the day, though, it’ll be waiting on a speech by Fed chair Powell with second tier US data (jobless claims, durables) offering some minor distraction in the run-up. Powell appears at the annual US Treasury Market Conference and is scheduled to speak along with another heavyweight, NY Fed’s Williams. Powell’s remarks are pre-recorded and there’s no Q&A but any reference to monetary policy may still affect trigger-happy (money) markets looking to add to easing bets. A 50 bps November cut is priced in for 60%. (Front-end) US yields and the dollar remain vulnerable in the current circumstances.

News & Views

The Czech National Bank (CNB) yesterday as expected further reduced its policy ate by 25 bps to 4.25%. The decision was approved by 6 members. One MPC member voted for a 50 bps step. In its communication, the board left the door open to (gradual) further easing. This process is supported by slower growth and slow wage rises, a stronger koruna and above all by increased easing expectations by the major central banks. Still, CNB communication maintained some leaning against the wind elements and stresses that it is necessary to persist with tight monetary policy. It will carefully consider any further rate cuts as risks to inflation still might still resurface. In this respect, August inflation slightly surprised to the upside (2.2%), partly due to higher food prices but also due to services inflation. Ongoing high inflation expectations also are a source of caution. KBC expects the CNB to continue a path of gradual easing, reducing the policy rate 25 bps at each of the next meetings till (including) February 2025. The krona yesterday eased slightly to EUR/CZK 25.16, but this was mainly due to broader market sentiment.

In its semi-annual financial stability report, the reserve Bank of Australia (RBA) assessed that the pressures from high inflation and restrictive monetary policy continue to be felt across the economy, but the share of borrowers experiencing severe financial stress remains small. Business insolvencies have increased sharply over the past couple of years following the removal of pandemic-era support, though they are only slightly above pre-pandemic levels as a share of all businesses. The RBA expects rates will be cut in the period ahead, but for now maintains a wait-and-see approach on the start of its easing cycle. (Too fast) easing is seen as a risk: ‘’Domestic vulnerabilities could increase if households respond to any easing in financial conditions by taking on excessive debt.” Aside from domestic factors, the RBA mainly sees external/risk challenges to financial stability, including vulnerabilities from complexity and interconnectedness in a digitalised world, imbalances in China's financial sector and disorderly adjustments in global asset prices that can spill over to Australia's financial system.

Graphs

GE 10y yield

The ECB cut policy rates by 25 bps in June and in September. Stubborn inflation (core, services) make follow-up moves less evident. We expect the central bank to stick with the quarterly reduction pace. Disappointing US and unconvincing-to-outright-weak EMU activity data dragged the long end of the curve down. The move accelerated during the early August market meltdown.

US 10y yield

The Fed kicked off its easing cycle with a 50 bps move. It is headed towards a neutral stance now that inflation and employment risks are in balance. Conservative SEP unemployment forecasts risk being caught up by reality and with it the dot plot (50 bps more cuts in 2024). We hold our call for two more 50 bps cuts this year. Pressure on the front of the curve and weakening eco data keeps the long end in the defensive for now as well.

EUR/USD

EUR/USD moved above the 1.09 resistance area as the dollar lost interest rate support at stealth pace. US recession risks and bets on fast and large rate cuts trumped traditional safe haven flows into USD. An ailing euro(pean economy) only briefly offset some of the general USD weakness. EUR/USD’s dollar-driven ascent is nearing resistance around 1.12 again.

EUR/GBP

The BoE delivered a hawkish cut in August. Policy restrictiveness will be further unwound gradually on a pace determined by a broad range of data. The strategy similar to the ECB’s balances out EUR/GBP in a monetary perspective. But the economic picture is increasingly diverging to the benefit of sterling. EUR/GBP succumbed to horrible European September PMI’s. Support at 0.84 broke and brings the 2022 low (0.8203) on the radar.

German Gfk consumer climate rises to -21.2, stabilizing at low level

Germany's GfK Consumer Climate index for October showed a marginal improvement, rising from -21.9 to -21.2, though falling short of the expected -21.0. Despite the slight uptick, overall consumer sentiment remains weak. Economic expectations dipped from 2.0 to 0.7 in September, while income expectations saw a stronger rise, from 3.5 to 10.1. The willingness to buy also improved, increasing from -10.9 to -6.9, while the willingness to save climbed from 10.7 to 12.0.

Rolf Bürkl, consumption expert at NIM, cautioned against overinterpreting this minor improvement. He stated, “After the severe setback in the previous month, the slight improvement in consumer climate can be interpreted more as a stabilization at a low level.”

He further added, "The consumer climate has not improved since June 2024, and the slight increase cannot be seen as the start of a noticeable recovery." In addition to the ongoing challenges of wars, crises, and inflation, the labor market has emerged as a new source of concern in recent months, weighing on consumer sentiment.

Where Are The Oil Bulls?

The global economy is settling into a newfound stability and central banks can continue to cautiously cut rates, said the OECD yesterday, but warned that the major central banks should maintain their data-dependent approach and be ‘prudent’ while cutting their rates. We are all looking at you Jerome Powell!

Anyway, one thing that stood out in that report was the group’s projections for the UK. The OECD said that the UK economy will grow more this year and next year than previously forecasted and print the best performance among the group of G7 economies, after the US, and that despite a sticky inflation. And the UK’s sticky inflation is one more reason to believe that the Bank of England (BoE) will keep the pace of its rate cuts slower than its major peers. Both improved prospects and cautious BoE stance are supportive of the pound sterling. Cable traded past the 1.34 yesterday, at the highest levels since spring 2022, and the EURGBP trends understandably lower with the diverging fortunes and outlook for the UK and the European economies – especially with Germany that’s under pressure and that ‘must carry out reforms’ according to the OECD. The only thing that could get on the way of the sterling bulls is the upcoming Autumn Budget which could pour some cold water on enthusiasm that the new Labour leadership will strengthen the back of the UK’s shattered economy post-Brexit, pandemic and energy crisis. The government needs money to boost spending and growth, but the finances are not in a good shape.

Oil bulls nowhere to be found

The upbeat outlook from the OECD, the rising tensions in the Middle East, the 4.5-mio barrel dive in US oil inventories last week (that pushed the US oil inventories to the lowest levels in 2.5 years) and the big stimulus measures from China did little to cheer oil investors up. US crude slipped below the $70pb again, and remains under a visible selling pressure this morning. Investors continue to trim their net speculative long positions in crude despite price supportive factors. Inability to pull out the $70/72pb offers this week increases the chances of a fresh attempt on the $65pb level in the coming weeks.

US GDP in focus

Stock markets weren’t in a particularly bullish mood yesterday. Investors preferred moving to the sidelines and leave the S&P500 and Nasdaq hang near their ATH levels before today’s GDP print from the US and tomorrow’s core PCE read. The US economy is expected to have grown by 3% in Q2 – and Atlanta Fed’s GDPNow Forecast now suggests that growth may have remained robust near that level in Q3. A robust growth data is good for those who bet that the Federal Reserve (Fed) will achieve the soft-landing that it dreams of. But it will also make investors think twice about their expectation for the next Fed meetings. Activity on Fed funds futures currently assesses more than a 60% chance for a second 50bp cut from the Fed in November… and there is nothing – in the economic data – that would justify such move besides greed. Therefore, a sufficiently strong GDP read has the potential to bring the bulls back to the market and send the US stock markets to fresh highs, but too much strength in the economic data should – at some point – encourage a scaling back of the Fed expectations and lead to consolidation and maybe – but just maybe – a minor downside correction in the stock markets.

But for now, the bulls have undeniably a stronger grip on the market. Nasdaq futures are up this morning on the back of surprisingly strong sales and profit forecasts from Micron Technology thanks to AI demand. Shares surged nearly 15% in the afterhours trading, and the post-earnings rally should help Micron return above its 200-DMA and eventually secure a floor near the $100 per share.

Zooming out, the AI fatigue gives signs of dissipating, as the Fed boost gives AI stocks fresh room to breathe, as part of a broader boost to risk appetite. Nvidia extends gains with joy above the 50-DMA, while Vaneck’s Semiconductor ETF held ground near its 200-DMA and is drilling above its 100-DMA this week.

Dollar’s misfortune

The US dollar rebounded yesterday against most majors, but the outlook remains negative for the greenback as the Fed’s major peers keep a cautious dovish bias as inflation eases, without however feeling the urge to boost their economies before making sure that inflation goes into a deeper sleep. The EURUSD retreated after testing levels above the 1.12 resistance. The USDJPY is flirting with the 145 level, and the USDCHF consolidates a touch below the 0.85 level before the Swiss National Bank (SNB) decision this morning. The SNB will probably cut its rates by 25bp. But the latter will hardly encourage the franc bulls to reverse course. The USDCHF is expected to consolidate and see a minor rebound in the short run with the expectation that the market and the Fed will come back to their senses regarding their overly dovish policy outlook, but in fine, the broadly negative dollar outlook – which is also due to the exploding US debt – is expected to keep the franc, other majors and gold well supported against the greenback.

SNB to Cut Rates by 25bp Today, But It’s a Close Call

In focus today

Today, we expect the SNB to cut policy rates by 25bp to 1.00%, but stress that it is a close call between 25bp and 50bp as inflation has underperformed the SNB's forecast, the real trade-weighted CHF has appreciated notably, and GDP has been higher than expected. Jordan has previously stated that the neutral nominal rate is around 1.00% and we think they will be satisfied with a more gradual pace rather than going directly to below the neutral nominal rate.

In the US, we have speeches from both Powell (15.20 CET), Williams, and Kashkari while in the euro area Lagarde is scheduled to speak at 15.30 CET.

Overnight, in Japan the ruling Liberal Democratic Party will elect a new leader and thus PM. With the recent hawkish turn from the BoJ looking highly politically influenced, markets should find this election interesting. Abenomics loyalists preferring a slow normalisation of monetary policies as well as hawks are on the ticket in an election that will be heavily influenced by behind-the-scenes arm wrestling among party heavyweights.

We also get Tokyo inflation data overnight for September, a good indicator of countrywide data released in three weeks.

China releases industrial profit growth overnight, which has been running around 4% in recent months below the long-term average of 8%. With growth struggling in August, we expect to see a move lower in profit growth.

Economic and market news

In geopolitics, while Israeli airstrikes on Hizbollah in Lebanon have continued throughout the week, yesterday the US and several G7 allies publicly called for a 21-day ceasefire to prevent an escalation to all-out war.

The Riksbank cut the policy rate by 25bp as widely expected. The guidance delivered was to the dovish side which caused markets to raise pricing to 48bp of cuts in November (prev. 37bp), but otherwise the market reaction was muted.

Equities: Global equities were lower yesterday, displaying notable sectoral and regional differences. Cyclical sectors such as technology and materials, along with utilities, outperformed even as the long end of the yield curve moved higher in the US and gold prices increased. This combination is rare and difficult to explain solely from a top-down perspective. A key factor was the Chinese stimulus bonanza, which continues today with discussions about an exceptional liquidity injection into banks. This stimulus has propelled Chinese stocks higher again today, steering them toward their best week in a long stretch. We are also observing side effects in other Asian markets this morning, notably with Japanese indices surging by more than 2%. In the US yesterday, the market movements were as follows: Dow -0.7%, S&P 500 -0.2%, Nasdaq +0.04%, and Russell 2000 -1.2%.

FI: With no major macro news out, EGB rates rose through yesterday's session, as markets moderated ECB rate cut expectations for next year. The Bund curve was 2-3bp higher across tenors, while peripherals saw some widening. The persistent uncertainty on the French budget outlook pushed long-end OAT yields up by 5bp, as PM Barnier's new government warned that the deficit could exceed 6% of GDP next year. The Bund ASW-spread tightened through the session, now trading just below 30bp. Risk sentiment is strengthening this morning due to rumours of an additional USD 142bn injection from Chinese authorities into the banking system.

FX: The USD rallied in the US session as EUR/USD dropped from above 1.12 to the lower end of the 1.11-1.12 range. USD/JPY has closed in on 145. In Scandies, both USD/NOK and EUR/NOK made huge leaps. The latter now trades in the higher end of the 11.70-11.80 range. USD/SEK seemed prepared to go for a test of 10.00, but instead the broad dollar rally sent the cross closer to 10.20. Today's big G10 FX event is the SNB rate decision. We look for a 25bp cut with a dovish tilt, while the market is priced at 35bp.

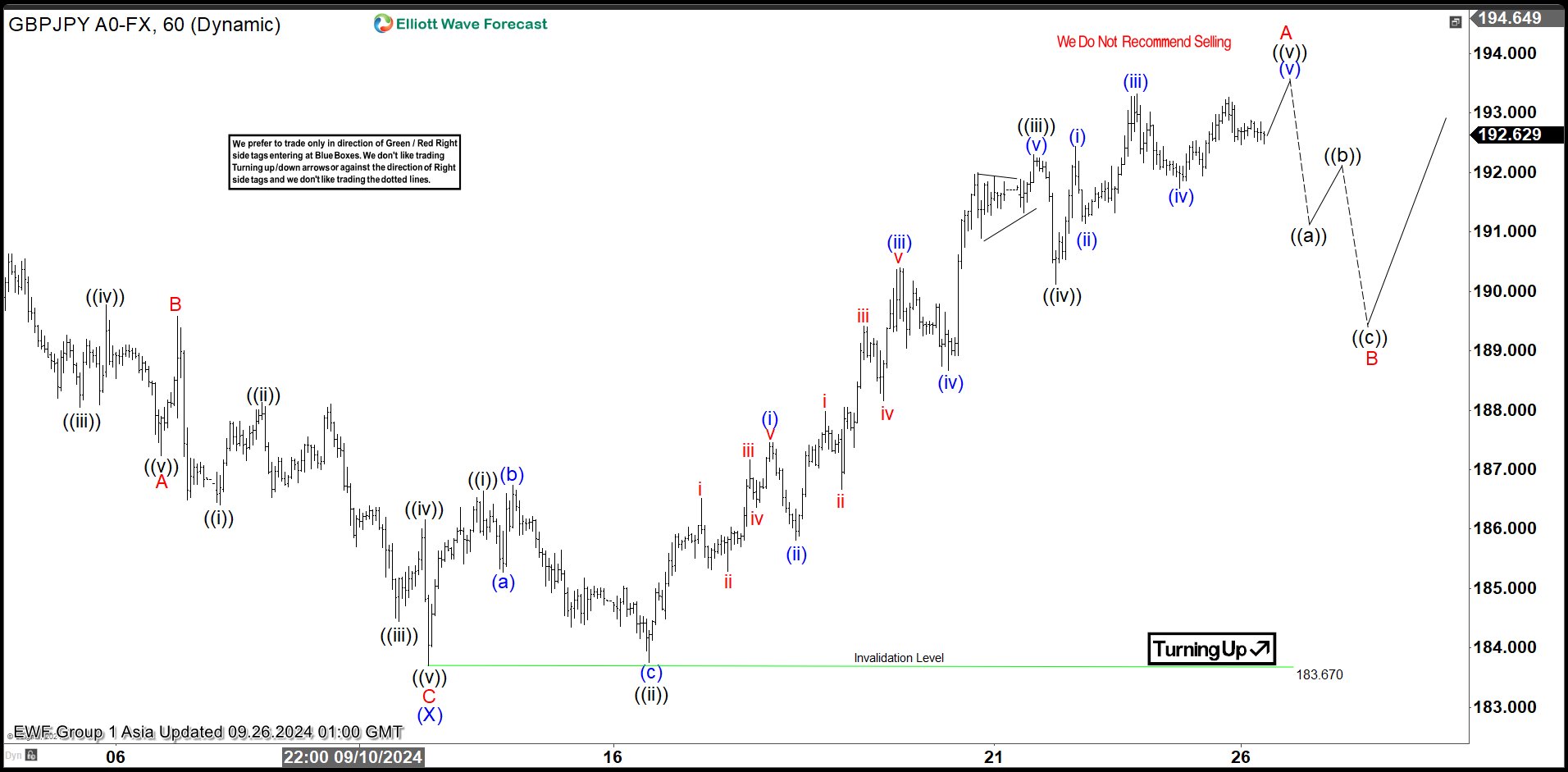

Short Term Elliott Wave Impulse in GBPJPY Favors Higher

Cycle from 8.5.2024 low in GBPJPY is in progress as a double three Elliott Wave structure. Up from 8.5.2024 low, wave (W) ended at 193.48 and pullback in wave (X) ended at 183.67. Internal subdivision of wave (X) unfolded as a zigzag. Down from wave (W), wave A ended at 187.23 and wave B ended at 189.58. Wave C lower ended at 183.67 which completed wave (X). Pair has turned higher in wave (Y) with internal subdivision as a zigzag structure.

Wave A of (Y) is in progress as a 5 waves impulse Elliott Wave structure. Up from wave (X), wave ((i)) ended at 186.63 and pullback in wave ((ii)) ended at 183.75. Pair has resumed higher in wave ((iii)). Up from wave ((ii)), wave (i) ended at 187.45 and wave (ii) ended at 185.81. Wave (iii) higher ended at 190.39 and wave (iv) ended at 188.66. Final wave (v) higher ended at 192.3 which completed wave ((iii)). Pullback in wave ((iv)) ended at 190.12. Expect pair to end wave ((v)) of A soon, then it should pullback in wave B to correct cycle from 9.11.2024 low in 3, 7, 11 swing before pair resumes higher again. Near term, as far as pivot at 183.67 low stays intact, expect dips to find buyers in 3, 7, 11 swing for further upside.

GBPJPY 60 Minutes Elliott Wave Chart

GBPJPY Elliott Wave Video

https://www.youtube.com/watch?v=YLNqPnOEfrQ

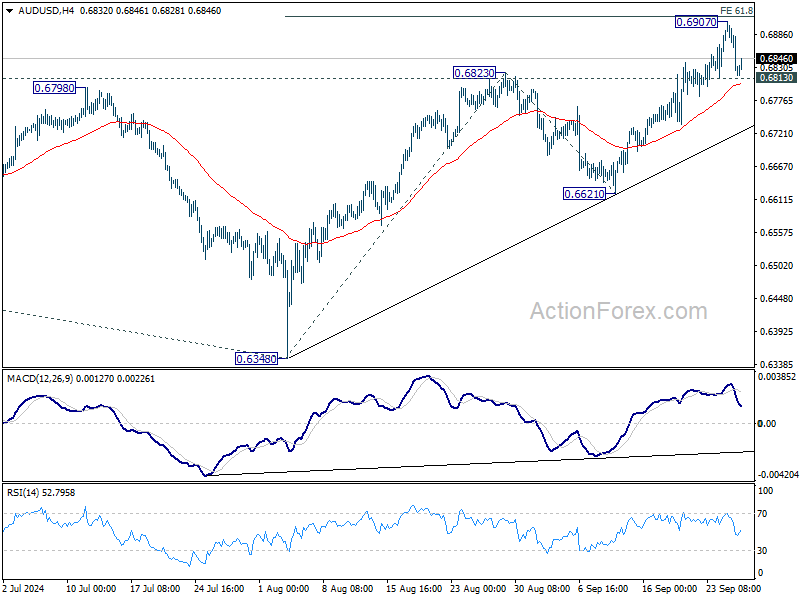

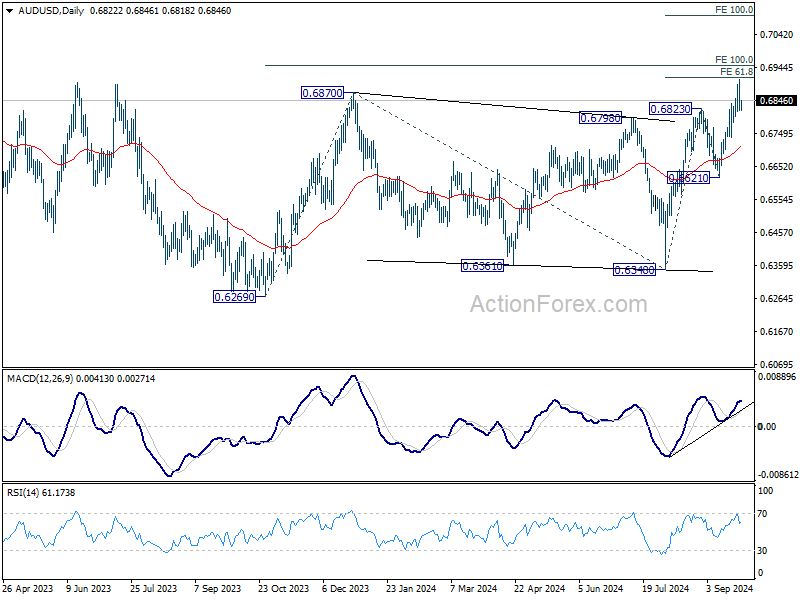

AUD/USD Daily Report

Daily Pivots: (S1) 0.6791; (P) 0.6850; (R1) 0.6881; More...

With current retreat, a temporary top is in place at 0.6907 in AUD/USD, just ahead of 61.8% projection of 0.6348 to 0.6823 from 0.6621 at 0.6915. Intraday bias is turned neutral for consolidations first. While deeper retreat cannot be ruled out, outlook will stay bullish as long as 0.6221 support holds. Sustained break of 0.6915 will pave the way to 100% projection at 0.7096 next.

In the bigger picture, overall, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern, with rise from 0.6269 as the third leg. Firm break of 0.6870 resistance will target 100% projection of 0.6269 to 0.6870 from 0.6340 at 0.6941, and then 138.2% projection at 0.7179. This will now remain the favored case as long as 0.6621 support holds.

Risk-On Sentiment Drives Asian Markets; Focus Shifts to SNB Rate Decision

Asian markets are maintaining a risk-on tone today, despite the lackluster US market performance overnight. Sentiment remains buoyed by China’s recent monetary stimulus measures, even as doubts linger about their overall effectiveness due to the absence of significant fiscal support. Nevertheless, stocks in Hong Kong and China continue to trade higher. In Japan, Nikkei is benefiting from Yen weakness, which further extended after BOJ minutes revealed a deeply divided board on future tightening measures.

Dollar bounced back strongly after dipping through July’s lows against Euro. However, this rebound seems driven more by quarter-end flows rather than a meaningful shift in market sentiment. Investors are also waiting on comments from key Fed officials today, including Chair Jerome Powell and New York Fed President John Williams. Yet, it's unlikely that these speeches will offer any fresh insights into November's rate cut plans. While today's jobless claims and durable goods orders, along with tomorrow's PCE inflation data, may cause minor market fluctuations, the primary focus is on next week's non-farm payrolls report as the fourth quarter begins.

For the week so far, Loonie is leading the pack, followed by Aussie and then Kiwi. Yen remains the weakest, with Euro and Swiss Franc trailing behind. Both Dollar and British Pound are positioned in the middle. Swiss Franc merits particular attention today due to the upcoming SNB rate decision.

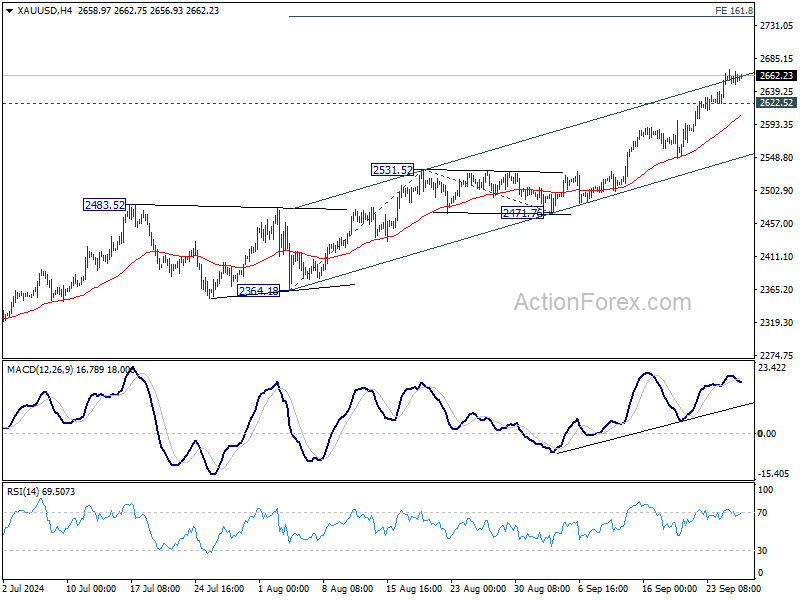

Technically, while Gold is losing some upside momentum as seen in D MACD, it's just consolidating in tight range near the newly established record high. Outook will stay bullish as long as 2622.52 support holds. Sustained trading above near term channel resistance would prompt upside acceleration to 161.8% projection of 2364.18 to 2631.52 from 2471.76 at 2742.51 next.

In Asia, at the time of writing, Nikkei is up 2.38%. Hong Kong HSI is up 2.32%. China Shanghai SSE is up 0.64%. Singapore Strait Times is up 0.44%. Japan 10-year JGB yield is up 0.022 at 0.834. Overnight, DOW fell -0.70%. S&P 500 fell -0.19%. NASDAQ rose 0.04%. 10-year yield rose 0.045 to 3.781.

SNB Decision: Conservative 25bps cut or aggressive 50bps?

SNB is set to announce its rate decision today, and the financial markets are rife with speculation. A significant gap has emerged between market expectations and those of economists regarding the magnitude of the rate cut. While a majority of economists are forecasting a 25 bps cut, market pricing suggests a nearly even split between the likelihood of a 25 bps cut and a more aggressive 50 bps reduction.

Several compelling arguments support the case for SNB to "front-load" its policy easing with a larger cut. First and foremost is the sharp decline in inflation. Last month, inflation dropped to 1.1%, well below the SNB's estimate of 1.5% for Q3, and far below the upper limit of its 0-2% target range. The government projects inflation to drop further to just 0.7% next year, suggesting that inflationary pressures are diminishing faster than anticipated. This may compel SNB to act decisively to counter deflationary risks.

Additionally, weak economic performance in the Eurozone, compounded by the strength of the Swiss Franc, is placing considerable strain on Swiss industries. The poor performance of Eurozone purchasing managers’ indices adds weight to the argument for a 50 bps cut to support economic activity in Switzerland.

However, SNB faces constraints. With policy rate currently at 1.25%, there is limited room for rate cuts before reaching zero. Some economists argue that SNB should hold back some policy measures for future flexibility.

According to a Bloomberg survey, only one out of 32 economists expects a 50 bps cut, while two predict no change. The remaining 29 economists anticipate a 25 bps reduction to bring the rate to 1.00%. Similarly, a Reuters poll found that 30 out of 32 economists expect a 25 bps cut, with one forecasting a 50 bps reduction and another expecting rates to hold steady. Looking ahead to the end of the year, opinions are split: 16 economists believe the rate will be at 1.00%, 15 predict it will drop to 0.75%, and one expects it to remain at 1.25%.

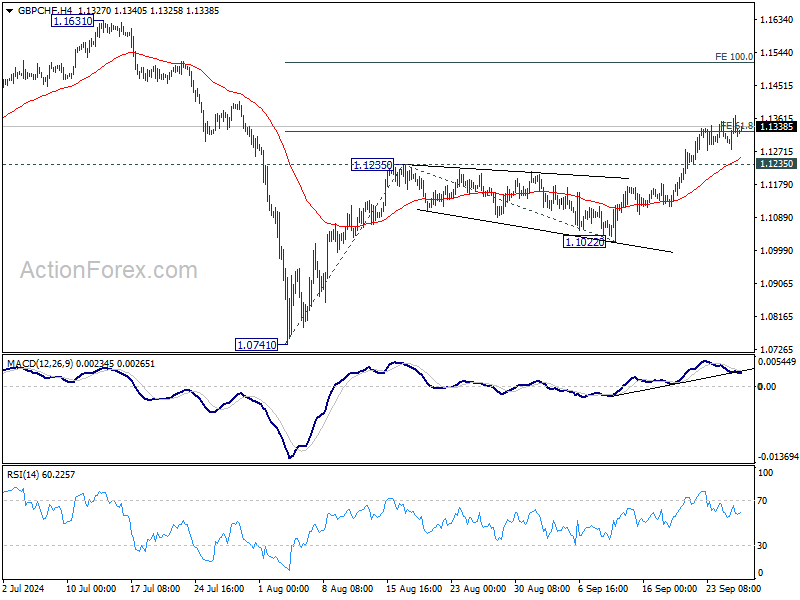

Technically, GBP/CHF's rally stalled after hitting 61.8% projection of 1.0741 to 1.1235 from 1.1022 at 1.1327. But further is expected as long as 1.1235 resistance turned support holds. Sustained trading above 1.1327 will pave the way to 100% projection at 1.1516 next.

BoJ minutes show divided views on rate hike timing

Minutes from BoJ's July meeting reveal a split among policymakers on the pace of future rate hikes. While BOJ raised its short-term interest rate to 0.25% by a 7-2 vote, differing opinions emerged on how quickly further increases should occur.

One member argued that if price trends follow the bank’s outlook, it would be “necessary” to proceed with further tightening. Another suggested that with inflation projected to reach its target by H2 of fiscal 2025, the policy rate should gradually rise toward the neutral rate, estimated at around 1%. This member cautioned against rapid rate increases and favored a “timely and gradual” approach to avoid shocks to the economy.

However, some members expressed concerns about the risks of moving too quickly. One warned that monetary policy normalization should not be an end in itself and urged caution in monitoring the risks tied to policy shifts. Another highlighted that inflation expectations were "not being anchored at 2 percent", suggesting the need to avoid excessive market speculation about future rate hikes.

The minutes also reflect "high uncertainties regarding the level of the neutral interest rate" about Japan’s neutral interest rate, given the long period without rate hikes. One member noted the difficulty of setting policy based on estimates of the neutral rate, calling for flexibility in adjusting policy based on evolving economic conditions.

Fed’s Kugler backs more rate cuts as focus shifts to employment

Fed Governor Adriana Kugler expressed "strong" support for last week's 50bps rate cut, signaling her inclination toward "additional cuts" in the federal funds rate.

In her speech overnight, Kugler emphasized that while the focus remains on bringing inflation down to the 2% target, attention should now begin to "shift attention to the maximum-employment side" Fed's dual mandate.

The labor market "remains resilient," she noted, but stressed that FOMC must now carefully balance its objectives. Fed should aim to maintain progress on disinflation while avoiding "unnecessary pain and weakness" in the broader economy.

Looking ahead

While SNB rate decision is the main even in European session, Germany will release Gfk consumer sentiment and EUrozone will publish M3 money supply. Later in the day, US will release GDP final, durable goods orders, jobless claims, and pending home sales.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6791; (P) 0.6850; (R1) 0.6881; More...

With current retreat, a temporary top is in place at 0.6907 in AUD/USD, just ahead of 61.8% projection of 0.6348 to 0.6823 from 0.6621 at 0.6915. Intraday bias is turned neutral for consolidations first. While deeper retreat cannot be ruled out, outlook will stay bullish as long as 0.6221 support holds. Sustained break of 0.6915 will pave the way to 100% projection at 0.7096 next.

In the bigger picture, overall, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern, with rise from 0.6269 as the third leg. Firm break of 0.6870 resistance will target 100% projection of 0.6269 to 0.6870 from 0.6340 at 0.6941, and then 138.2% projection at 0.7179. This will now remain the favored case as long as 0.6621 support holds.

Economic Indicators Update

| GMT | CCY | EVENTS | ACT | F/C | PP | REV |

|---|---|---|---|---|---|---|

| 23:50 | JPY | BoJ Minutes | ||||

| 06:00 | EUR | Germany GfK Consumer Sentiment Oct | -21 | -22 | ||

| 07:30 | CHF | SNB Interest Rate Decision | 1.00% | 1.25% | ||

| 08:00 | CHF | SNB Press Conference | ||||

| 08:00 | EUR | ECB Economic Bulletin | ||||

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y Aug | 2.50% | 2.30% | ||

| 12:30 | USD | Initial Jobless Claims (Sep 20) | 226K | 219K | ||

| 12:30 | USD | GDP Annualized Q2 F | 3.00% | 3.00% | ||

| 12:30 | USD | GDP Price Index Q2 F | 2.50% | 2.50% | ||

| 12:30 | USD | Durable Goods Orders Aug | -2.80% | 9.80% | ||

| 12:30 | USD | Durable Goods Orders ex Transport Aug | 0.10% | -0.20% | ||

| 14:00 | USD | Pending Home Sales M/M Aug | 0.90% | -5.50% | ||

| 14:30 | USD | Natural Gas Storage | 52B | 58B |