Sample Category Title

Summary 7/15 – 7/19

Monday, Jul 15, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 22:30 | NZD | Business NZ PSI Jun | 43 | |

| 23:01 | GBP | Rightmove House Price Index M/M Jul | 0% | |

| 02:00 | CNY | GDP Y/Y Q2 | 5.10% | 5.30% |

| 02:00 | CNY | Industrial Production Y/Y Jun | 5.00% | 5.60% |

| 02:00 | CNY | Retail Sales Y/Y Jun | 3.30% | 3.70% |

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y Jun | 3.90% | 4.00% |

| 02:00 | CNY | GDP Q/Q Q2 | 1.10% | 1.60% |

| 06:00 | EUR | Germany Retail Sales M/M May | 0.00% | -1.20% |

| 06:30 | CHF | PPI M/M Jun | 0.10% | -0.30% |

| 06:30 | CHF | PPI Y/Y Jun | -1.80% | |

| 09:00 | EUR | Eurozone Industrial Production M/M May | -1.00% | -0.10% |

| 12:30 | USD | Empire State Manufacturing Index Jul | -8 | -6 |

| 12:30 | CAD | Manufacturing Sales M/M May | 0.20% | 1.10% |

| 12:30 | CAD | Wholesale Sales M/M May | 2.00% | 2.40% |

| 14:30 | CAD | BoC Business Outlook Survey |

| GMT | Ccy | Events | |

|---|---|---|---|

| 22:30 | NZD | Business NZ PSI Jun | |

| Forecast: | Previous: 43 | ||

| 23:01 | GBP | Rightmove House Price Index M/M Jul | |

| Forecast: | Previous: 0% | ||

| 02:00 | CNY | GDP Y/Y Q2 | |

| Forecast: 5.10% | Previous: 5.30% | ||

| 02:00 | CNY | Industrial Production Y/Y Jun | |

| Forecast: 5.00% | Previous: 5.60% | ||

| 02:00 | CNY | Retail Sales Y/Y Jun | |

| Forecast: 3.30% | Previous: 3.70% | ||

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y Jun | |

| Forecast: 3.90% | Previous: 4.00% | ||

| 02:00 | CNY | GDP Q/Q Q2 | |

| Forecast: 1.10% | Previous: 1.60% | ||

| 06:00 | EUR | Germany Retail Sales M/M May | |

| Forecast: 0.00% | Previous: -1.20% | ||

| 06:30 | CHF | PPI M/M Jun | |

| Forecast: 0.10% | Previous: -0.30% | ||

| 06:30 | CHF | PPI Y/Y Jun | |

| Forecast: | Previous: -1.80% | ||

| 09:00 | EUR | Eurozone Industrial Production M/M May | |

| Forecast: -1.00% | Previous: -0.10% | ||

| 12:30 | USD | Empire State Manufacturing Index Jul | |

| Forecast: -8 | Previous: -6 | ||

| 12:30 | CAD | Manufacturing Sales M/M May | |

| Forecast: 0.20% | Previous: 1.10% | ||

| 12:30 | CAD | Wholesale Sales M/M May | |

| Forecast: 2.00% | Previous: 2.40% | ||

| 14:30 | CAD | BoC Business Outlook Survey | |

| Forecast: | Previous: | ||

Tuesday, Jul 16, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 04:30 | JPY | Tertiary Industry Index M/M May | 0.20% | 1.90% |

| 09:00 | EUR | Eurozone Trade Balance (EUR) May | 20.3B | 19.4B |

| 09:00 | EUR | Germany ZEW Economic Sentiment Jul | 44.3 | 47.5 |

| 09:00 | EUR | Germany ZEW Current Situation Jul | -73 | -73.8 |

| 09:00 | EUR | Eurozone ZEW Economic Sentiment Jul | 50.2 | 51.3 |

| 12:15 | CAD | Housing Starts Y/Y Jun | 259K | 265K |

| 12:30 | CAD | CPI M/M Jun | 0.10% | 0.60% |

| 12:30 | CAD | CPI Y/Y Jun | 2.90% | |

| 12:30 | CAD | CPI Median Y/Y Jun | 2.70% | 2.80% |

| 12:30 | CAD | CPI Trimmed Y/Y Jun | 2.80% | 2.90% |

| 12:30 | CAD | CPI Common Y/Y Jun | 2.40% | 2.40% |

| 12:30 | USD | Retail Sales M/M Jun | -0.20% | 0.10% |

| 12:30 | USD | Retail Sales ex Autos M/M Jun | 0.10% | -0.10% |

| 12:30 | USD | Import Price Index M/M Jun | 0.20% | -0.40% |

| 14:00 | USD | Business Inventories May | 0.30% | 0.30% |

| 14:00 | USD | NAHB Housing Market Index Jul | 44 | 43 |

| 22:45 | NZD | CPI Q/Q Q2 | 0.50% | 0.60% |

| 22:45 | NZD | CPI Y/Y Q2 | 4.00% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 04:30 | JPY | Tertiary Industry Index M/M May | |

| Forecast: 0.20% | Previous: 1.90% | ||

| 09:00 | EUR | Eurozone Trade Balance (EUR) May | |

| Forecast: 20.3B | Previous: 19.4B | ||

| 09:00 | EUR | Germany ZEW Economic Sentiment Jul | |

| Forecast: 44.3 | Previous: 47.5 | ||

| 09:00 | EUR | Germany ZEW Current Situation Jul | |

| Forecast: -73 | Previous: -73.8 | ||

| 09:00 | EUR | Eurozone ZEW Economic Sentiment Jul | |

| Forecast: 50.2 | Previous: 51.3 | ||

| 12:15 | CAD | Housing Starts Y/Y Jun | |

| Forecast: 259K | Previous: 265K | ||

| 12:30 | CAD | CPI M/M Jun | |

| Forecast: 0.10% | Previous: 0.60% | ||

| 12:30 | CAD | CPI Y/Y Jun | |

| Forecast: | Previous: 2.90% | ||

| 12:30 | CAD | CPI Median Y/Y Jun | |

| Forecast: 2.70% | Previous: 2.80% | ||

| 12:30 | CAD | CPI Trimmed Y/Y Jun | |

| Forecast: 2.80% | Previous: 2.90% | ||

| 12:30 | CAD | CPI Common Y/Y Jun | |

| Forecast: 2.40% | Previous: 2.40% | ||

| 12:30 | USD | Retail Sales M/M Jun | |

| Forecast: -0.20% | Previous: 0.10% | ||

| 12:30 | USD | Retail Sales ex Autos M/M Jun | |

| Forecast: 0.10% | Previous: -0.10% | ||

| 12:30 | USD | Import Price Index M/M Jun | |

| Forecast: 0.20% | Previous: -0.40% | ||

| 14:00 | USD | Business Inventories May | |

| Forecast: 0.30% | Previous: 0.30% | ||

| 14:00 | USD | NAHB Housing Market Index Jul | |

| Forecast: 44 | Previous: 43 | ||

| 22:45 | NZD | CPI Q/Q Q2 | |

| Forecast: 0.50% | Previous: 0.60% | ||

| 22:45 | NZD | CPI Y/Y Q2 | |

| Forecast: | Previous: 4.00% | ||

Wednesday, Jul 17, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:00 | AUD | Westpac Leading Index M/M Jun | 0% | |

| 06:00 | GBP | CPI M/M Jun | 0.30% | |

| 06:00 | GBP | CPI Y/Y Jun | 2.00% | 2.00% |

| 06:00 | GBP | Core CPI Y/Y Jun | 3.40% | 3.50% |

| 06:00 | GBP | RPI M/M Jun | 0.40% | |

| 06:00 | GBP | RPI Y/Y Jun | 2.90% | 3.00% |

| 06:00 | GBP | PPI Input M/M Jun | 0.10% | 0.00% |

| 06:00 | GBP | PPI Input Y/Y Jun | -0.10% | |

| 06:00 | GBP | PPI Output M/M Jun | 0.10% | -0.10% |

| 06:00 | GBP | PPI Output Y/Y Jun | 1.70% | |

| 06:00 | GBP | PPI Core Output M/M Jun | 0.20% | |

| 06:00 | GBP | PPI Core Output Y/Y Jun | 1.00% | |

| 09:00 | EUR | Eurozone CPI Y/Y Jun F | 2.50% | 2.50% |

| 09:00 | EUR | Eurozone CPI Core Y/Y Jun F | 2.90% | 2.90% |

| 12:30 | USD | Building Permits Jun | 1.40M | 1.40M |

| 12:30 | USD | Housing Starts Jun | 1.30M | 1.28M |

| 13:15 | USD | Industrial Production M/M Jun | 0.30% | 0.90% |

| 13:15 | USD | Capacity Utilization Jun | 78.60% | 78.70% |

| 14:30 | USD | Crude Oil Inventories | -3.4M | |

| 18:00 | USD | Beige Book | ||

| 23:50 | JPY | Trade Balance (JPY) Jun | -0.89T | -0.62T |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:00 | AUD | Westpac Leading Index M/M Jun | |

| Forecast: | Previous: 0% | ||

| 06:00 | GBP | CPI M/M Jun | |

| Forecast: | Previous: 0.30% | ||

| 06:00 | GBP | CPI Y/Y Jun | |

| Forecast: 2.00% | Previous: 2.00% | ||

| 06:00 | GBP | Core CPI Y/Y Jun | |

| Forecast: 3.40% | Previous: 3.50% | ||

| 06:00 | GBP | RPI M/M Jun | |

| Forecast: | Previous: 0.40% | ||

| 06:00 | GBP | RPI Y/Y Jun | |

| Forecast: 2.90% | Previous: 3.00% | ||

| 06:00 | GBP | PPI Input M/M Jun | |

| Forecast: 0.10% | Previous: 0.00% | ||

| 06:00 | GBP | PPI Input Y/Y Jun | |

| Forecast: | Previous: -0.10% | ||

| 06:00 | GBP | PPI Output M/M Jun | |

| Forecast: 0.10% | Previous: -0.10% | ||

| 06:00 | GBP | PPI Output Y/Y Jun | |

| Forecast: | Previous: 1.70% | ||

| 06:00 | GBP | PPI Core Output M/M Jun | |

| Forecast: | Previous: 0.20% | ||

| 06:00 | GBP | PPI Core Output Y/Y Jun | |

| Forecast: | Previous: 1.00% | ||

| 09:00 | EUR | Eurozone CPI Y/Y Jun F | |

| Forecast: 2.50% | Previous: 2.50% | ||

| 09:00 | EUR | Eurozone CPI Core Y/Y Jun F | |

| Forecast: 2.90% | Previous: 2.90% | ||

| 12:30 | USD | Building Permits Jun | |

| Forecast: 1.40M | Previous: 1.40M | ||

| 12:30 | USD | Housing Starts Jun | |

| Forecast: 1.30M | Previous: 1.28M | ||

| 13:15 | USD | Industrial Production M/M Jun | |

| Forecast: 0.30% | Previous: 0.90% | ||

| 13:15 | USD | Capacity Utilization Jun | |

| Forecast: 78.60% | Previous: 78.70% | ||

| 14:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: -3.4M | ||

| 18:00 | USD | Beige Book | |

| Forecast: | Previous: | ||

| 23:50 | JPY | Trade Balance (JPY) Jun | |

| Forecast: -0.89T | Previous: -0.62T | ||

Thursday, Jul 18, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | AUD | Employment Change Jun | 20.0K | 39.7K |

| 01:30 | AUD | Unemployment Rate Jun | 4.10% | 4.00% |

| 06:00 | CHF | Trade Balance (CHF) Jun | 5.05B | 5.81B |

| 06:00 | GBP | Claimant Count Change Jun | 50.4K | |

| 06:00 | GBP | ILO Unemployment Rate (3M) May | 4.40% | 4.40% |

| 06:00 | GBP | Average Earnings Including Bonus 3M/Y May | 5.70% | 5.90% |

| 06:00 | GBP | Average Earnings Excluding Bonus 3M/Y May | 6.00% | |

| 12:15 | EUR | ECB Deposit Rate | 3.75% | 3.75% |

| 12:15 | EUR | ECB Main Refinancing Rate | 4.25% | 4.25% |

| 12:30 | USD | Initial Jobless Claims (Jul 12) | 225K | 222K |

| 12:30 | USD | Philadelphia Fed Manufacturing Jul | 2.9 | 1.3 |

| 12:45 | EUR | ECB Press Conference | ||

| 14:30 | USD | Natural Gas Storage | 55B | 65B |

| 23:01 | GBP | GfK Consumer Confidence Jul | -11 | -14 |

| 23:30 | JPY | National CPI Y/Y Jun | 2.80% | |

| 23:30 | JPY | National CPI Core Y/Y Jun | 2.70% | 2.50% |

| 23:30 | JPY | National CPI Core-Core Y/Y Jun | 2.10% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | AUD | Employment Change Jun | |

| Forecast: 20.0K | Previous: 39.7K | ||

| 01:30 | AUD | Unemployment Rate Jun | |

| Forecast: 4.10% | Previous: 4.00% | ||

| 06:00 | CHF | Trade Balance (CHF) Jun | |

| Forecast: 5.05B | Previous: 5.81B | ||

| 06:00 | GBP | Claimant Count Change Jun | |

| Forecast: | Previous: 50.4K | ||

| 06:00 | GBP | ILO Unemployment Rate (3M) May | |

| Forecast: 4.40% | Previous: 4.40% | ||

| 06:00 | GBP | Average Earnings Including Bonus 3M/Y May | |

| Forecast: 5.70% | Previous: 5.90% | ||

| 06:00 | GBP | Average Earnings Excluding Bonus 3M/Y May | |

| Forecast: | Previous: 6.00% | ||

| 12:15 | EUR | ECB Deposit Rate | |

| Forecast: 3.75% | Previous: 3.75% | ||

| 12:15 | EUR | ECB Main Refinancing Rate | |

| Forecast: 4.25% | Previous: 4.25% | ||

| 12:30 | USD | Initial Jobless Claims (Jul 12) | |

| Forecast: 225K | Previous: 222K | ||

| 12:30 | USD | Philadelphia Fed Manufacturing Jul | |

| Forecast: 2.9 | Previous: 1.3 | ||

| 12:45 | EUR | ECB Press Conference | |

| Forecast: | Previous: | ||

| 14:30 | USD | Natural Gas Storage | |

| Forecast: 55B | Previous: 65B | ||

| 23:01 | GBP | GfK Consumer Confidence Jul | |

| Forecast: -11 | Previous: -14 | ||

| 23:30 | JPY | National CPI Y/Y Jun | |

| Forecast: | Previous: 2.80% | ||

| 23:30 | JPY | National CPI Core Y/Y Jun | |

| Forecast: 2.70% | Previous: 2.50% | ||

| 23:30 | JPY | National CPI Core-Core Y/Y Jun | |

| Forecast: | Previous: 2.10% | ||

Friday, Jul 19, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 06:00 | GBP | Retail Sales M/M Jun | -0.40% | 2.90% |

| 06:00 | EUR | Germany PPI M/M Jun | 0.10% | 0.00% |

| 06:00 | EUR | Germany PPI Y/Y Jun | -2.20% | |

| 06:00 | GBP | Public Sector Net Borrowing (GBP) Jun | 12.0B | 14.1B |

| 08:00 | EUR | Eurozone Current Account (EUR) May | 38.6B | |

| 12:30 | CAD | Industrial Product Price M/M Jun | 0.00% | |

| 12:30 | CAD | Raw Material Price Index Jun | -1.00% | |

| 12:30 | CAD | Retail Sales M/M May | -0.20% | 0.70% |

| 12:30 | CAD | Retail Sales ex Autos M/M May | 1.20% | 1.80% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 06:00 | GBP | Retail Sales M/M Jun | |

| Forecast: -0.40% | Previous: 2.90% | ||

| 06:00 | EUR | Germany PPI M/M Jun | |

| Forecast: 0.10% | Previous: 0.00% | ||

| 06:00 | EUR | Germany PPI Y/Y Jun | |

| Forecast: | Previous: -2.20% | ||

| 06:00 | GBP | Public Sector Net Borrowing (GBP) Jun | |

| Forecast: 12.0B | Previous: 14.1B | ||

| 08:00 | EUR | Eurozone Current Account (EUR) May | |

| Forecast: | Previous: 38.6B | ||

| 12:30 | CAD | Industrial Product Price M/M Jun | |

| Forecast: | Previous: 0.00% | ||

| 12:30 | CAD | Raw Material Price Index Jun | |

| Forecast: | Previous: -1.00% | ||

| 12:30 | CAD | Retail Sales M/M May | |

| Forecast: -0.20% | Previous: 0.70% | ||

| 12:30 | CAD | Retail Sales ex Autos M/M May | |

| Forecast: 1.20% | Previous: 1.80% | ||

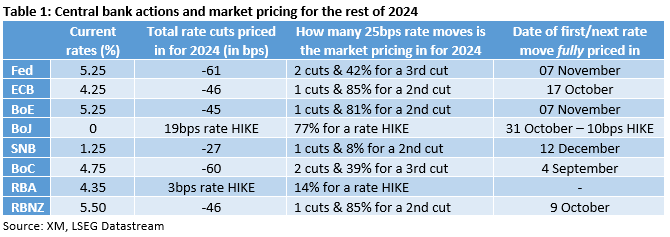

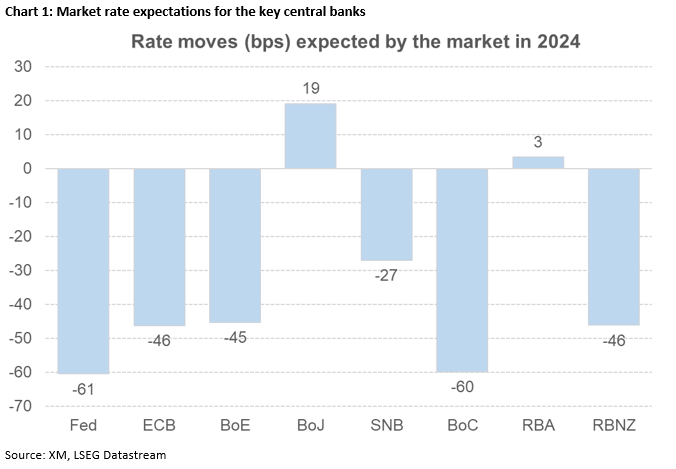

A September Fed Rate Cut Could Lead to Easing Spree During end-2024

- Market prices in at least two rate cuts from Fed

- ECB, BoE expected to follow suit despite divergent economic conditions

- SNB and BoC could ease further; RBNZ possibly close to a summer rate cut

- BoJ and RBA could surprise with rate hikes during 2024

We are halfway into 2024 and the countdown for this year’s key event, the US presidential election, has already started. With geopolitics taking a backseat lately, despite both the Ukrainian-Russian and Israeli-Hamas conflicts remaining unresolved, political risk is expected to affect market sentiment, as seen lately in the euro area.

Amidst these developments, the key central banks are trying to implement their strategy. The ECB, the Swiss National Bank and the Bank of Canada have already started to ease their monetary policy stance while the Bank of Japan has managed to hike once so far in 2024. The remaining central banks, and predominantly the Fed, remain on the sidelines. Ahead of the next round of central bank meetings, what is the market pricing in for the rest of 2024?

The Fed to follow in the ECB's footsteps?

The recent US labour market data and the June CPI report have probably firmly opened the door to the much-discussed rate cuts by the Fed. The market is currently pricing in 61bps of rate easing in 2024, which translates to two 25bps rate cuts and a 41% chance for a third similarly sized move. Considering the November presidential election and the June 2024 dot plot penciling in one rate cut, the market might be getting too optimistic, especially if the data improves over the summer.

Turning to the ECB, when a central bank announces its first rate cut, the path is assumed to be fixed towards further accommodation. As made evident by recent ECB members' comments, this is not the case now. Having said that, the market is currently expecting 46bps of easing in 2024, which means one full 25bps rate move and around 90% possibility of a second rate cut. Interestingly, political developments in France could tip the balance in favour of more rate cuts down the line.

The market expects both the BoE and the RBZN to start cutting soon

The market expects almost two rate cuts by both the Bank of the England and the Reserve Bank of New Zealand in 2024. The recent aggressive drop in UK headline inflation could have opened the door to a rate cut by the BoE, but the political developments forced it to go into a brief hibernation. With the general election out of the picture, another weak CPI report on July 17 could materially increase the chance of a rate cut at the August 1 meeting, which includes the quarterly monetary policy report.

Similarly, the RBNZ’S dovish shift at its most recent meeting surprised the market since just 40 days ago the RBNZ was considering the rate hike option. The market has quickly adapted to the new status quo by pricing in a total easing of 46bps by year-end, with a considerable probability of a summer rate cut if the imminent quarterly CPI surprises on the downside.

BoC and SNB cut rates, market expects more

Responding to easing inflation, both the BoC and the SNB eased their monetary policy stance over the past few months. In the case of the former, the Canadian economy has not been firing into all cylinders with unemployment rising to the highest level since February 2022. Ignoring the recent upside surprise in monthly inflation, the market continues to fully price in two rate cuts in 2024, with a sizeable possibility of a third one towards the end of the year.

Turning to the SNB and the two rate cuts already announced were partly unexpected but probably justified due to the low inflation rate and the continued strengthening of the franc. The SNB stands ready to ease further, with the market currently fully pricing in another 25bps rate cut at the December meeting.

BoJ to hike again, RBA thinking about it

The BoJ remains on the lonely path of tightening its monetary policy stance. The April rate hike was welcomed by the market, but BoJ’s recent inactivity has raised a few eyebrows, weakening the yen. Japanese authorities could be hoping that a sustained worsening of US data and the mild hawkishness of the BoJ could help the yen recover. The market is looking for 19bps of rate hikes by the BoJ in 2024 with the next 10bps rate hike expected at the September meeting. Firstly though, the market awaits the full details of the bond buying programme tapering.

The Reserve Bank of Australia is the only other central bank thinking about rate hikes. Stickier inflation and a tight labour market are keeping Governor Bullock et al on their toes with the minutes from the June meeting confirming the RBA’s intention to hike rates if needed. The market is tentatively pricing in 3bps of tightening in 2024 but RBA’s rates outlook will probably be gravely affected by the July 31 CPI print for the second quarter of 2024.

Week Ahead – ECB Set to Hold Rates, Plethora of Data on the Way

- ECB is not expected to cut in July but will it signal one for next meeting?

- Retail sales will be the main highlight in the United States

- UK CPI report will be vital for BoE’s August decision

- China GDP data to kickstart busy week

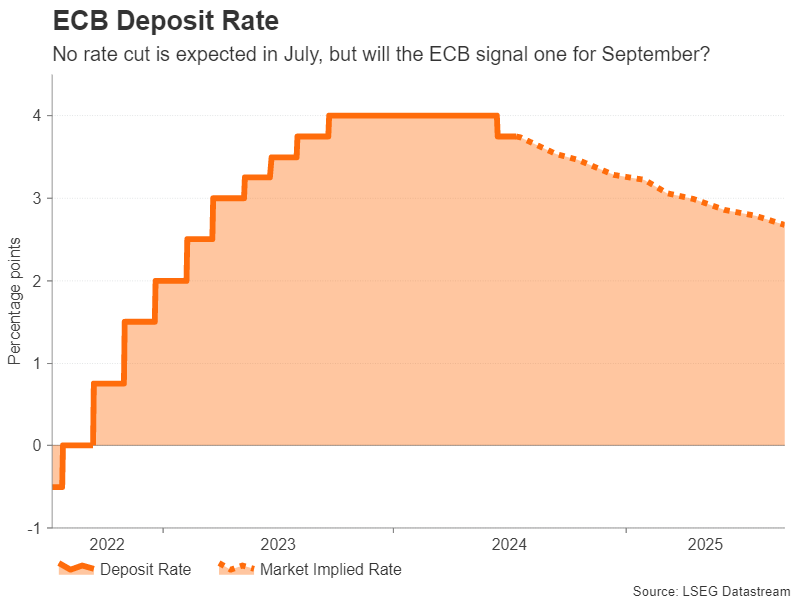

ECB meets amid sticky inflation

The European Central Bank concludes its two-day policy meeting on Thursday but no change in interest rates is anticipated after trimming them by 25 basis points at last month’s gathering. The June decision proved to be somewhat controversial, as policymakers inadvertently locked themselves into cutting rates before all the data was in. An uptick in both inflation and wage growth right before the meeting was not something that the Governing Council wanted to see, but not cutting rates would probably have been even more embarrassing.

The ECB justified its decision by pointing out the risk of undershooting its inflation target if it waited too long. Since then, inflation has fallen back marginally and there’s indications that pay pressures are cooling even though wage growth remains elevated.

Hence, there seems to be a strong majority for at least one more cut in 2024, but views vary about a third reduction. However, this is a debate for another day and policymakers are almost certain to keep rates unchanged on Thursday and reassess the risks when they regroup in September.

Markets are not fully convinced about a third cut either and if President Lagarde refrains from providing any explicit forward guidance, the euro could extend its recent gains. But should she commit to a cut in September, that would be negative for the single currency.

Markets are not fully convinced about a third cut either and if President Lagarde refrains from providing any explicit forward guidance, the euro could extend its recent gains. But should she commit to a cut in September, that would be negative for the single currency.

Also to keep an eye on next week are the ZEW economic sentiment survey out of Germany on Tuesday, and the final estimates of Eurozone CPI for June on Wednesday.

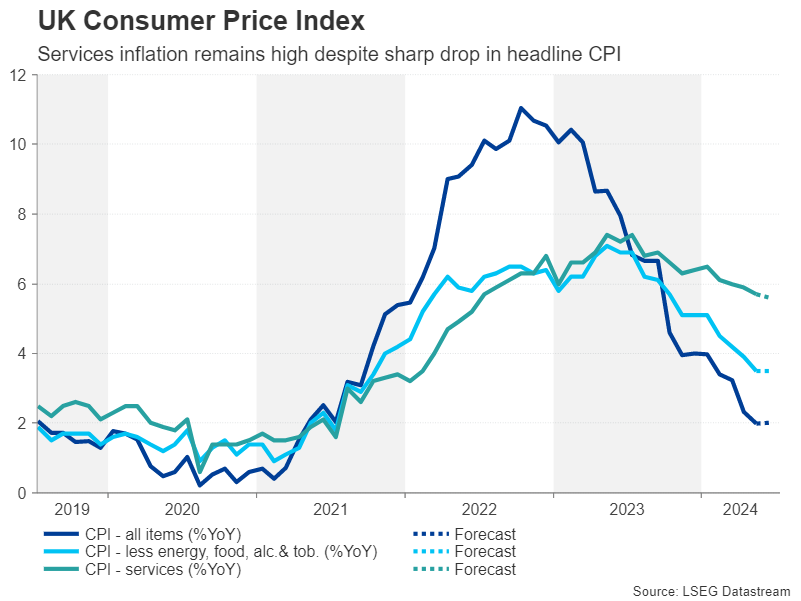

Pound bulls face CPI test

The British pound has been enjoying a sizeable rally in July, helped by a softer US dollar as well as by Labour winning a large majority in the UK general election, ending years of a turmoil under the Tories. But that’s not all. Despite headline inflation falling to the Bank of England’s 2% target in June, services inflation remains too high for comfort at 5.7%, something that the Bank’s chief economist Huw Pill stressed just this week. In addition, with the British economy seeing a revival in growth momentum, there isn’t a very strong urgency to lower rates imminently.

With markets split 50/50 about an August cut and policymakers probably undecided too, next week’s updates on inflation, employment and retail sales could be decisive.

The June CPI report is out first on Wednesday, labour market stats for May will follow on Thursday, and retail sales for June are due on Friday.

Any further moderation in core and services CPI, as well as in wage growth, could seal the deal for an August rate cut, potentially knocking sterling lower. Yet, given the euro’s and yen’s woes, plus the improving outlook for the UK economy, further progress on the inflation front that gives the BoE the green light to cut rates soon might not be too catastrophic for the pound.

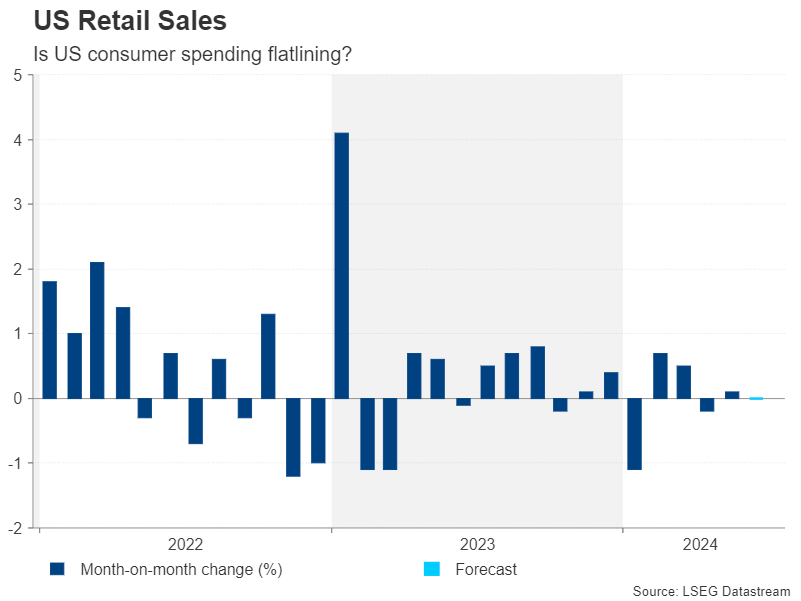

Are US consumers tightening their belts?

Over in the US, the Federal Reserve is also not in a hurry to start slashing rates, but investors are increasingly confident about a move in September. Inflation is edging down again after stalling earlier in the year, while Chair Powell noted that the labour market has cooled lately. Consumer spending also appears to be slowing and there could be more evidence of this in Tuesday’s retail sales figures.

Retail sales are expected to have stayed unchanged at 0.0% m/m in June after rising by just 0.1% in May. Any unexpected bounce back in retail sales could bring a halt to the dollar’s slide.

Investors will also be tracking manufacturing gauges from the New York and Philadelphia Feds on Monday and Thursday, respectively, while on Wednesday, there will be a flurry of releases, including building permits, housing starts and industrial production.

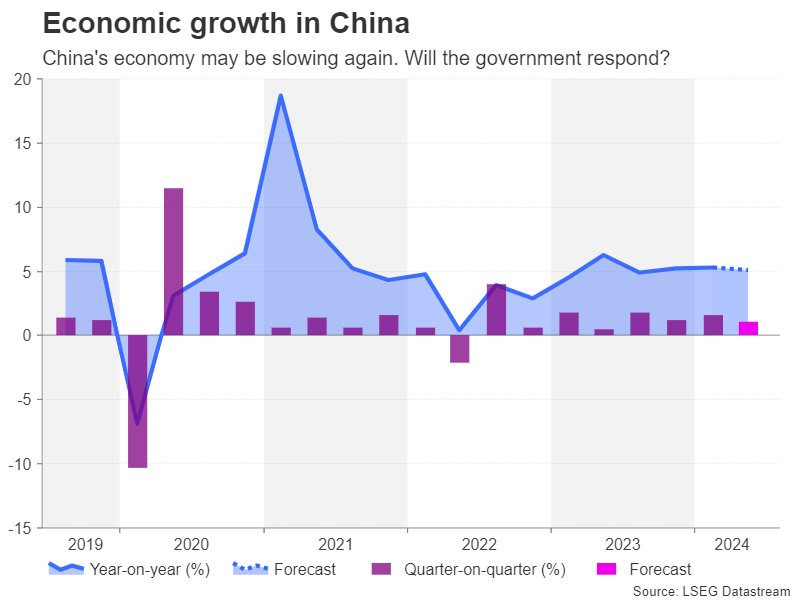

China’s economy likely slowed in Q2

Despite numerous efforts to boost the flagging economy, the Chinese government has been unable to turn things around. Although the downturn in the property market has started to ease, the crisis is far from being over, and the stock market is struggling to recover from a three-year slump.

Investor and consumer confidence therefore remain low, weighing on business and household spending. Industrial production has started to show some signs of life this year, but retail sales have been sluggish. The June readings for both will be watched on Monday alongside the GDP estimate for the second quarter.

China’s economy likely grew by 1.1% on a quarterly basis in the three months to June, a slowdown from the 1.6% pace in the first quarter. The year-on-year rate is also forecast to have eased from 5.3% to 5.1%.

Whilst investors have come to expect less-than-spectacular GDP numbers out of China in recent quarters, a downside surprise could still hurt market sentiment at the start of the trading week, hitting regional stocks and risk-sensitive currencies such as the Australian dollar.

However, a bad set of figures might prompt policymakers to come up with bolder measures. The country’s Communist Party leaders meet on July 15-18 for what is called the Third Plenum, which is typically held every five years, usually in the autumn but was delayed in 2023. The meeting focuses on long-term economic reforms and goals but it’s unclear if it will be followed by any immediate policy responses.

Meanwhile, aussie traders will additionally be monitoring domestic employment numbers on Thursday.

Canada, Japan New Zealand also awaiting CPI data

Inflation in Canada unexpectedly ticked higher in May, dampening hopes for a back-to-back rate cut in July. Unless the June report that’s out on Tuesday points to some easing in price pressures, the Bank of Canada will likely stay on hold at least until September. On the other side of the argument is the weakening of the labour market, which is limiting the loonie’s upside amid the greenback’s broad selloff.

The BoC’s survey on the business outlook due on Monday and Friday’s retail sales data might shed more light on the state of economy but the focus will primarily be on the CPI readings.

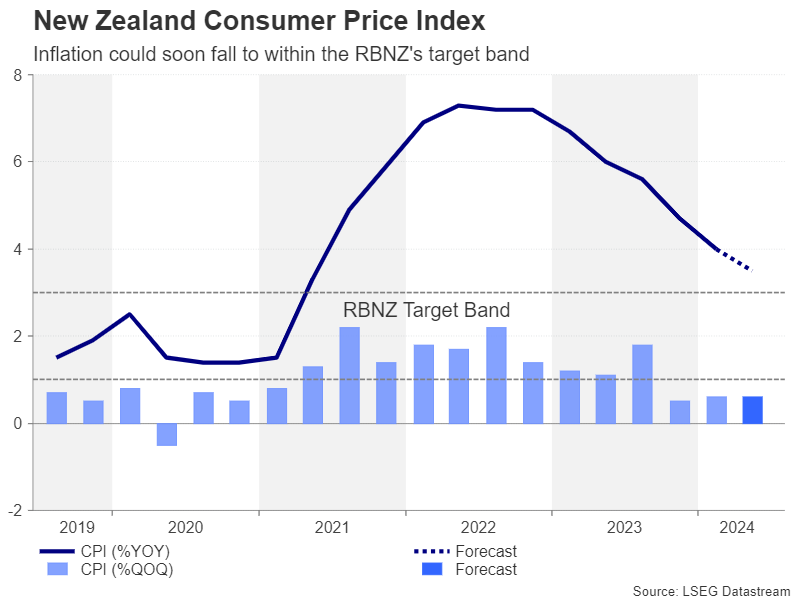

In New Zealand, the quarterly CPI publication on Wednesday will be just as crucial for rate cut bets. The Reserve Bank of New Zealand leaned to the dovish side at its latest meeting, sounding upbeat about the prospect of inflation hitting its 1-3% target band in the second half of the year. The kiwi could face fresh selling pressure if the Q2 CPI print takes the RBNZ one step closer to its target range.

Wrapping up the week on Friday will be Japan’s CPI numbers. As the Bank of Japan’s July 31 meeting approaches, the CPI data will be scrutinized for final clues as to whether a rate hike is likely this month. The BoJ has hinted that the expected announcement on bond tapering at the next gathering should not be seen as putting the rate hike decision on hold. But investors are still not convinced there’s a strong enough case to raise rates further, so any upside surprises in June CPI could lift the yen.

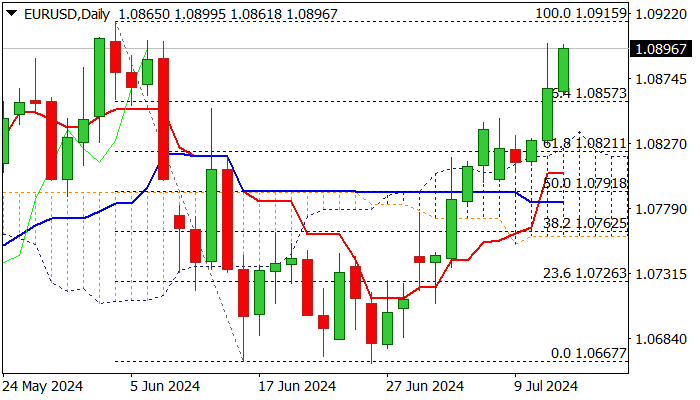

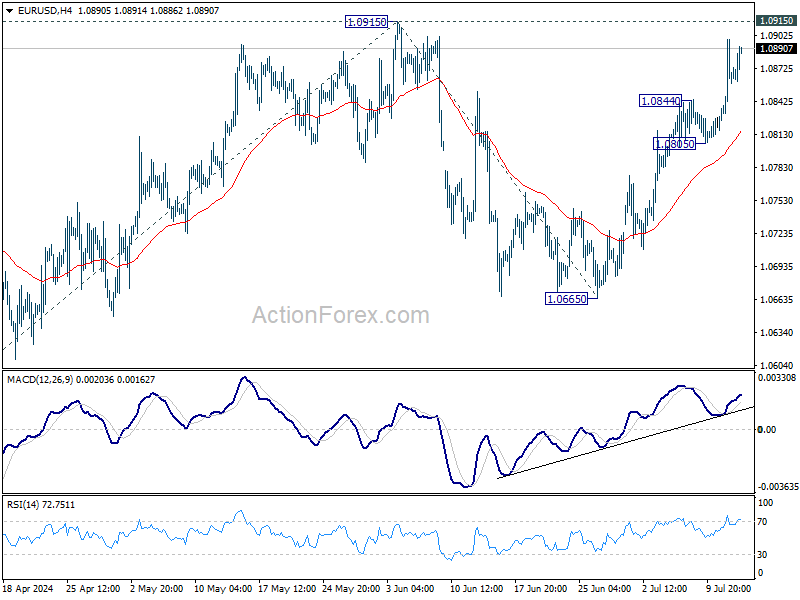

EUR/USD Outlook: Bulls Hold Grip for Further Advance

EURUSD continues to trend higher, with minimal negative impact from hotter than expected US PPI data (Jun 0.2% m/m vs 0.1% f/c and 0.0% in May).

The latest bull-leg extends into third straight and day pressuring Thursday’s post US CPI spike high (1.0898) which guards pivotal barriers at 1.0919 (Jun 4), 1.0981 (Mar 8) and 1.10 (psychological).

The pair is also on track for the third consecutive weekly gain, with expectations for further upside, should fundamentals remain favorable.

Broken Fibo 76.4% barrier (1.0857) offers initial support, followed by more significant daily cloud top (1.0835)

Res: 1.0900; 1.0919; 1.0981; 1.1000.

Sup: 1.0857; 1.0835; 1.0821; 1.0800.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0829; (P) 1.0864; (R1) 1.0904; More....

No change in EUR/USD's outlook and intraday bias stays on the upside for retesting 1.0915 resistance. Decisive break there will resume whole rally from 1.0601 and target 100% projection of 1.0601 to 1.0915 from 1.0665 at 1.0919 next. For now, risk will stay on the upside as long as 1.0805 support holds, in case of retreat.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern that could still be in progress. Break of 1.0601 will target 1.0447 support and possibly below. On the upside, firm break of 1.0915 resistance will start another rising leg back to 1.1138 resistance instead.

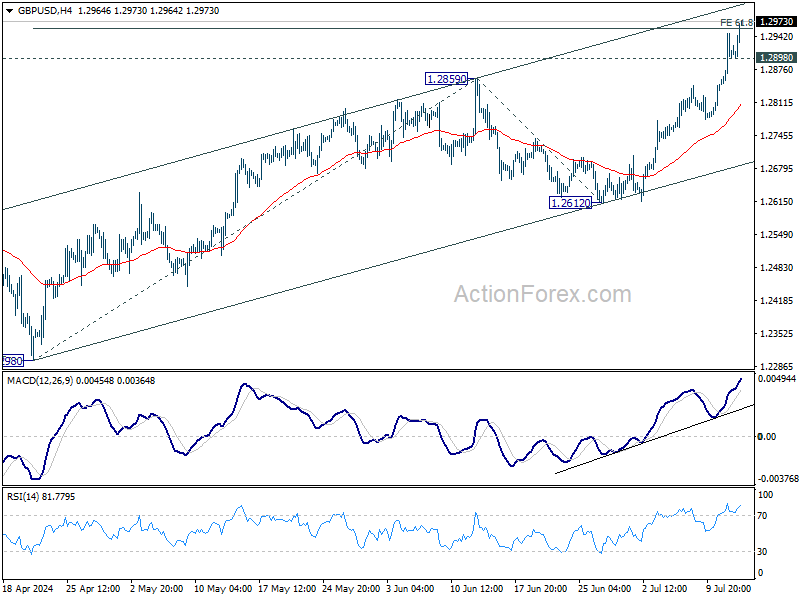

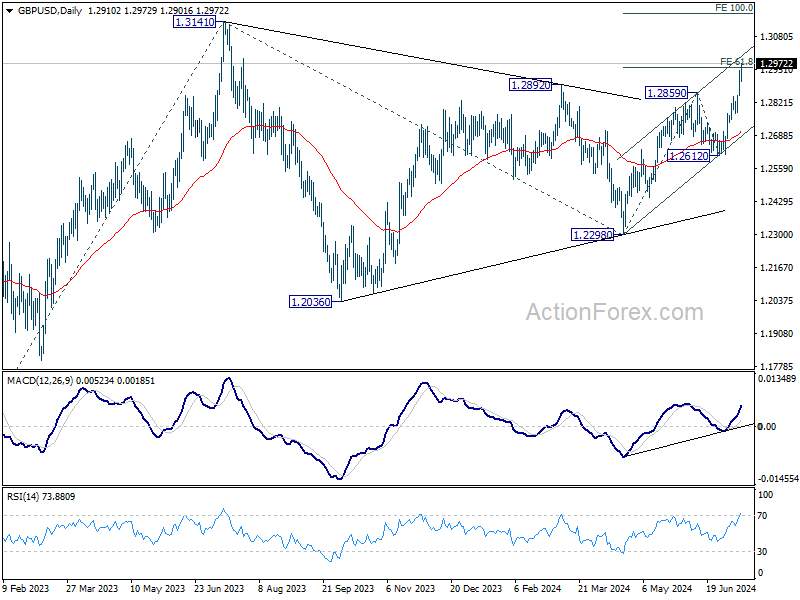

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2858; (P) 1.2903; (R1) 1.2960; More...

Intraday bias in GBP/USD remains on the upside for the moment. Decisive break of 61.8% projection of 1.2298 to 1.2859 from 1.2612 at 1.2959 would prompt upside acceleration through 1.3141 resistance to 100% projection at 1.3173. On the downside, below 1.2845 resistance turned support will turn intraday bias neutral first.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern which might have completed with three waves to 1.2298 already. This will now remain the favored case as long as 1.2612 support holds. Firm break of 1.3141 will target 61.8% projection of 1.0351 (2022 low) to 1.3141 (2023 high) from 1.2298 at 1.4022.

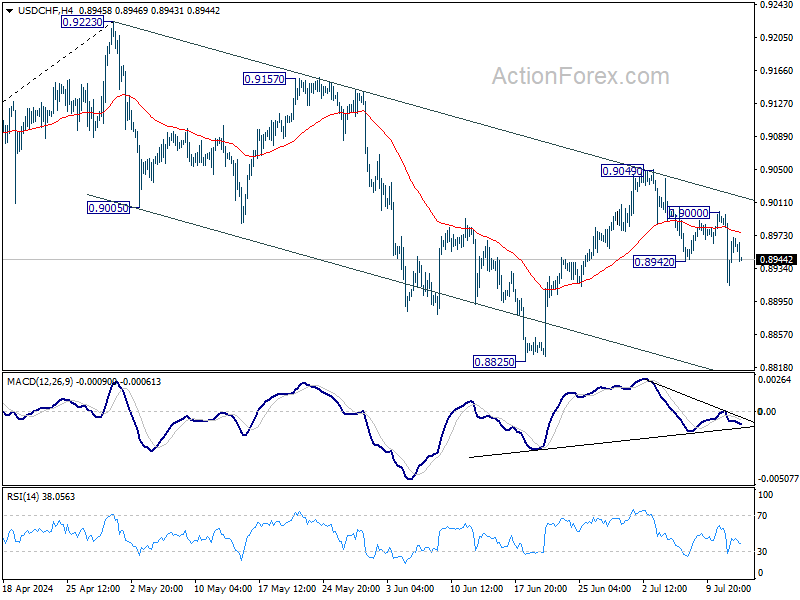

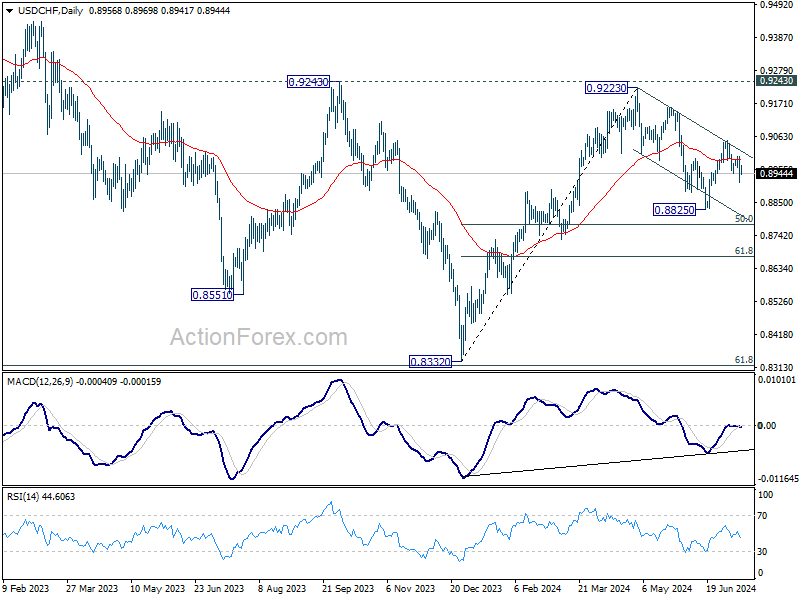

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8919; (P) 0.8961; (R1) 0.9007; More…

No change in USD/CHF's outlook as further decline is expected with 0.9000 resistance intact. Deeper decline would be seen to 0.88825 support. Fall from 0.9223 should be in progress with near term channel intact. Break of 0.8825 will target 50% retracement of 0.8332 to 0.9223 at 0.8778 next. However, break of 0.9000 will turn bias back to the upside for 0.9049 resistance instead.

In the bigger picture, focus remains on 0.9223/9243 resistance zone. Decisive break there would suggest larger bullish trend reversal and turn outlook bullish. Nevertheless, rejection by 0.9223/43 will keep medium term outlook neutral at best, for more range trading between 0.8332/9243 first.

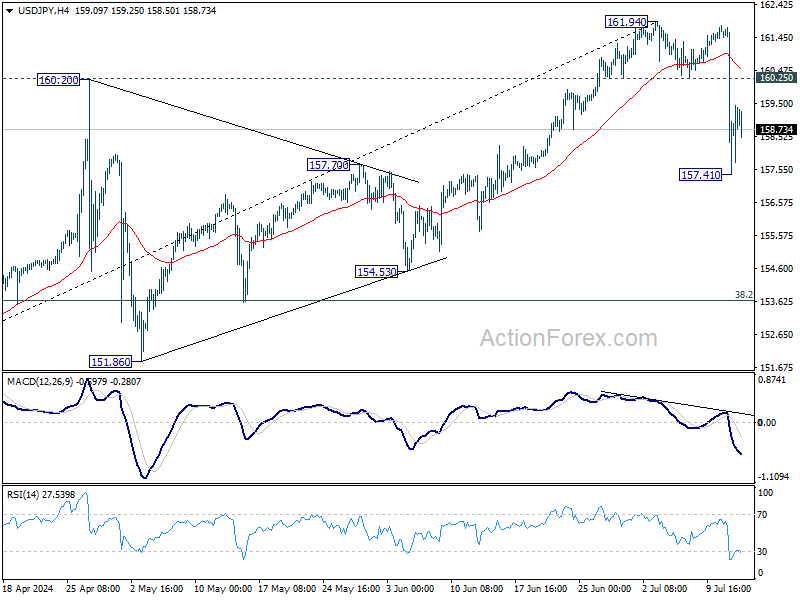

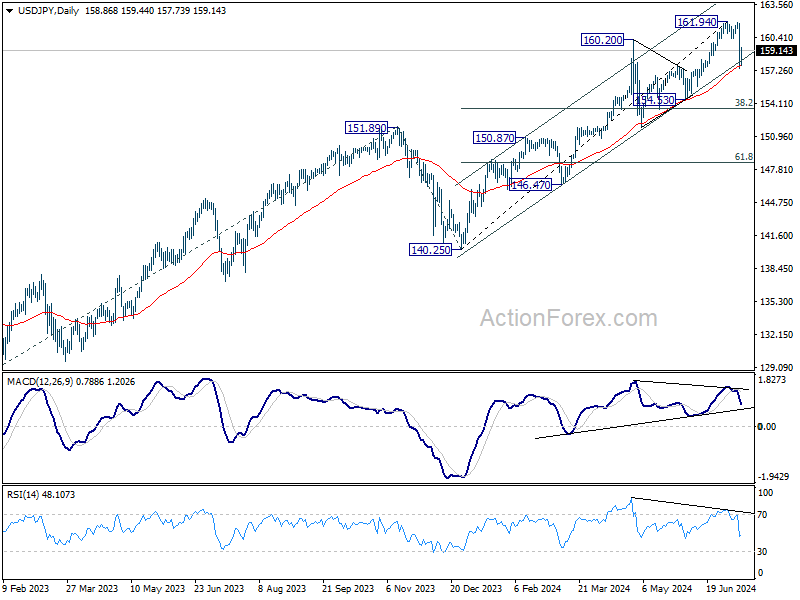

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 156.97; (P) 159.37; (R1) 161.30; More...

No change in USD/JPY's outlook. Deeper decline is expected with 160.25 support turned resistance intact. Fall from 161.94 is seen as corrective the five-wave rally from 140.25. Sustained break of 55 D EMA (now at 157.71) will affirm this bearish case. Next target will be 38.2% retracement of 140.25 to 161.94 at 163.65.

In the bigger picture, long term up trend is still in progress. Further rise is expected as long as 154.53 support holds. Next target is 100% projection of 127.20 (2023 low) to 151.89 (2023 high) from 140.25 at 164.94. However, sustained break of 154.53 will raise the chance of larger scale correction and target 140.25/151.89 support zone.

Dollar Softens Post-PPI Release, Yet Selling Momentum Remains Limited

Dollar is under some selling pressure in early US session despite stronger-than-expected PPI readings. However, downside momentum of the greenback is relatively limited. The post-CPI selloff yesterday did not gain significant traction, partly because stock markets unexpectedly retreated. Currently, futures are indicating a flat opening, and if activity in risk markets remains subdued in this final session of the week, Dollar might stabilize, at least temporarily.

Meanwhile, Japanese Yen is undergoing a consolidation phase after yesterday's significant gains—the largest daily rally against Dollar since late 2022. Although there has been no official confirmation from Japanese officials regarding intervention in the currency markets, data released by BoJ today suggests that the scale of intervention was likely around JPY 3.5T.

The estimate on Japan's intervention is derived from movements observed in the central bank's accounts. Notably, BoJ's current account balance is expected to decrease by JPY 3.2T due to government fiscal factors by next Tuesday, a stark contrast to the JPY 333B increase forecasted by private money brokers prior to the suspected intervention. Further clarity on these interventions will be available when official monthly data is released on July 31.

Reviewing the weekly performance across currency markets, New Zealand Dollar remains the weakest, closely followed by Dollar and then Swiss Franc. On the stronger side, Yen leads, followed by Sterling and Euro. Australian Dollar and Canadian Dollar are positioned in the middle of the performance spectrum.

In Europe, at the time of writing, FTSE is up 0.19%. DAX is up 0.22%. CAC is up 0.65%. UK 10-year yield is up 0.0524 at 4.131. Germany 10-year yield is up 0.045 at 2.513. Earlier in Asia, Nikkei fell -2.45%. Hong Kong HSI rose 2.59%. China Shanghai SSE rose 0.03%. Singapore Strait Times rose 0.65%. Japan 10-year JGB yield fell -0.0336 to 1.050.

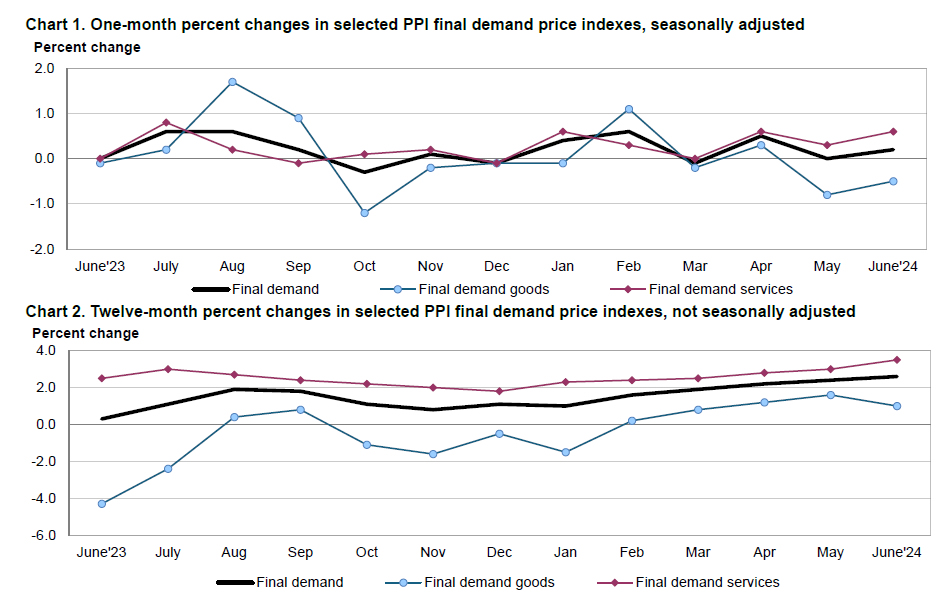

US PPI rises 0.2% mom, 2.6% yoy, largest annual advance in more than a year

US PPI for final demand rose 0.2% mom in June, slightly above expectation of 0.1% mom. PPI rose 2.6% yoy for the 12 months ended in June, above expectation of 2.2% yoy. That's also the largest annual advance since March 2023.

PPI less foods, energy, and trade services were unchanged at 0.0% mom. For the 12 months period, PPI less foods, energy, and trade services rose 3.1% yoy.

New Zealand BNZ manufacturing freefalls to lowest non-lockdown level since 2009

New Zealand BusinessNZ Performance of Manufacturing Index fell sharply from 46.6 to 41.1 in June, well below the long-term average of 52.6 and marking the lowest non-lockdown monthly level since February 2009.

Breaking down the details, production dropped from 44.0 to 35.4, and new orders fell from 43.9 to 38.8. These sub-40 activity levels for production and new orders are the lowest seen outside of COVID lockdowns since November 2008. Employment also declined significantly, from 50.4 to 43.8, its lowest non-COVID monthly result since July 2019. Finished stocks decreased from 52.3 to 47.9, while deliveries remained unchanged at 44.9.

BusinessNZ's Director of Advocacy, Catherine Beard, expressed significant concern over the "freefall in activity from May to June," highlighting the severe challenges facing a sector that has been contracting for the past 15 months. The proportion of negative comments surged to 76.3%, up from 63.5% in May and 69% in April, with respondents highlighting an overall economic slowdown and tough recessionary conditions.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 156.97; (P) 159.37; (R1) 161.30; More...

No change in USD/JPY's outlook. Deeper decline is expected with 160.25 support turned resistance intact. Fall from 161.94 is seen as corrective the five-wave rally from 140.25. Sustained break of 55 D EMA (now at 157.71) will affirm this bearish case. Next target will be 38.2% retracement of 140.25 to 161.94 at 163.65.

In the bigger picture, long term up trend is still in progress. Further rise is expected as long as 154.53 support holds. Next target is 100% projection of 127.20 (2023 low) to 151.89 (2023 high) from 140.25 at 164.94. However, sustained break of 154.53 will raise the chance of larger scale correction and target 140.25/151.89 support zone.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | NZD | Business NZ PMI Jun | 41.1 | 47.2 | 46.6 | |

| 03:00 | CNY | Trade Balance (USD) Jun | 99.1B | 85.1B | 82.6B | |

| 03:00 | CNY | Trade Balance (CNY) Jun | 704B | 590B | 586B | |

| 04:30 | JPY | Industrial Production M/M May F | 3.60% | 2.80% | 2.80% | |

| 12:30 | CAD | Building Permits M/M May | -12.20% | -5.00% | 20.50% | 23.40% |

| 12:30 | USD | PPI M/M Jun | 0.20% | 0.10% | -0.20% | 0.00% |

| 12:30 | USD | PPI Y/Y Jun | 2.60% | 2.20% | 2.20% | |

| 12:30 | USD | PPI Core M/M Jun | 0.40% | 0.20% | 0.00% | 0.30% |

| 12:30 | USD | PPI Core Y/Y Jun | 3.00% | 2.50% | 2.30% | |

| 14:00 | USD | Michigan Consumer Sentiment Jul P | 68.5 | 68.2 |

US PPI rises 0.2% mom, 2.6% yoy, largest annual advance in more than a year

US PPI for final demand rose 0.2% mom in June, slightly above expectation of 0.1% mom. PPI rose 2.6% yoy for the 12 months ended in June, above expectation of 2.2% yoy. That's also the largest annual advance since March 2023.

PPI less foods, energy, and trade services were unchanged at 0.0% mom. For the 12 months period, PPI less foods, energy, and trade services rose 3.1% yoy.