Sample Category Title

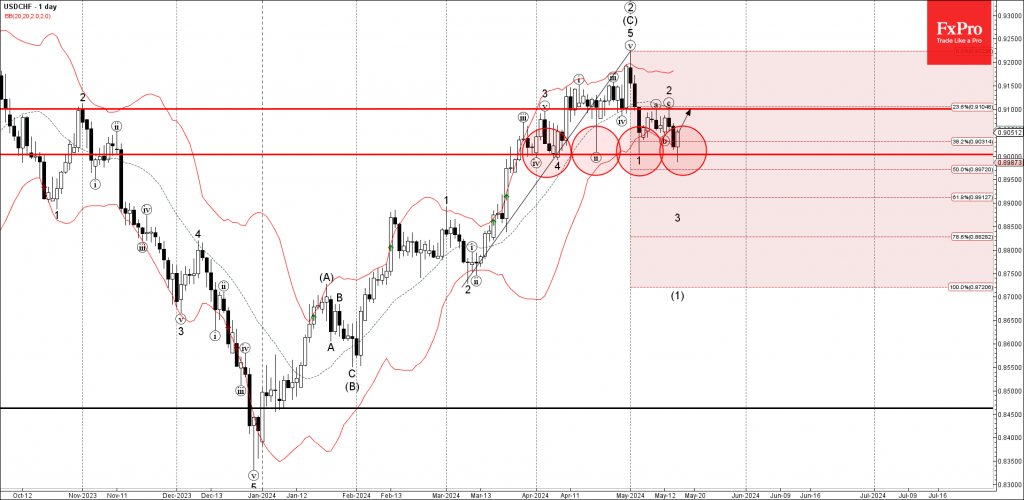

USDCHF Wave Analysis

- USDCHF reversed from round support level 0.9000

- Likely to rise to resistance level 0.9100

USDCHF currency pair recently reversed up from the round support level 0.9000 (which stopped the previous corrections iv, 4 ii, 1).

The support level 0.90000 was strengthened by the lower daily Bollinger Band and by the 50% Fibonacci correction of the previous upward impulse from March.

Given the strong daily uptrend, USDCHF currency pair can be expected to rise further to the next resistance level 0.9100, top of the previous waves a, 2.

Sunset Market Commentary

Markets

Since the May 1 Fed decision/communication dominos fell in place for markets to embrace a correction on the April higher-for-long rally in US (and broader) yields. Despite US inflation holding sticky, Fed Chair Powell ‘reassured’ markets that policy was tight enough. Slow progress in inflation only caused to Fed to delay a first rate cut. A rate hike remains highly unlikely. Most activity data (payrolls, retail sales) and sentiment indicators (ISM’s, Michigan consumer confidence, Empire manufacturing) printed softer than expected post-FOMC, suggesting no need for the Fed to slow demand even further. Indicators of inflation expectations admittedly showed no one-on-one link between a (presumed) slowdown in activity and a further deceleration in inflation. Still markets were happy to read some further softening in prices pressures in yesterday’s April CPI report, even as it was close to expectations. After yesterday’s additional softening, the market correction finally reached technical and ‘logical’ barriers, suggesting some consolidation. The US 2-y yield tested the 4.7% area, starting point of the yields’ ascent post the March US CPI release and revisited after the payrolls. After the recent correction, it probably won’t be that easy for the 2-y yield to decline aggressively further with markets again fully discounting a first Fed rate cut in September, with additional easing also priced in toward the end of the year and in 2025 (4% end next year?). The 10-y yield is at risk of closing the week below 4.37% (38% retracement rise since late December). Today’s US data were mixed. Jobless claims (222k) remained slightly higher than what we got used to up until recently. Housing starts and building permits were below consensus and the Philly Fed business outlook also declined more than hoped for. Admittedly, US import and export prices rebounded more than expected. US bond markets for now didn’t draw any big directional conclusion. The US yield curve inverts slightly with the 2-y adding 5.5 bps and the 30-y little changed . In a Reuters interview, NY Fed president Williams sees the economy moving to a better balance, but it’s too soon to cut rates based on these data. Several other Fed policy makers will speak later today. German yields are gaining modestly (1.5-3.5 bps). Equities are taking a breather after nearing (Eurostoxx 50) or touching (US indices) peak levels yesterday. (EuroStoxx 50 -0.4%, S&P 500 +0.1% ). The dollar shows signs of bottoming. DXY rebounds to 104.50 (104.11 this morning). EUR/USD’s test of the 1.0885/1.0895 area is rejected (1.0865). Reprieve for the yen from the broader USD correction again proved short-lived. USD/JPY easily rebounds to 155.4 (153.6 this morning).

News & Views

Norway’s economy grew for a fourth quarter in a row in 2024Q1. Norwegian mainland GDP (ex-energy) rose 0.2% q/q following an upwardly revised 0.3% in 2023Q4. While topping the Norges Bank’s projection for a stagnation, some details take away some shine. Household consumption, for one, dropped 0.7%. A steep 2.2% drop in goods consumption was only partially offset by increased services spending (0.2%). Gross fixed capital formation fell sharply, also outside of housing, Norway Statistics noted, adding that the numbers can be volatile. Government consumption rose 0.5% while a sharper uptick in imports (1%) than in exports (0.4%) meant a negative contribution from net exports. Either way, the economy keeps humming along and seems to vindicate the Norges Bank at the May meeting. It then said that “The data so far could suggest that a tight monetary policy stance may be needed for somewhat longer [beyond autumn] than we envisaged in March”, more so against the backdrop inflation still stays well above the 2% target. The krone does lose some marginal ground after hitting a speed bump around EUR/NOK 11.6 in the previous days.

Polish core inflation eased as expected from 4.6% to 4.1% in April in what could be the last base effect driven drop for months to come. Monthly dynamics showcase ongoing strong price pressures. Depending on the gauge, core prices rose between 0.7 and 1.2% m/m, the fastest pace in about a year. These kind of numbers and the expected core CPI trajectory going forward are unlikely to sway already hawkish NBP policymakers towards a rate cut anytime soon. Most of them consider end this year as the earliest possible timing with the beginning of 2025 the more probably option. The Polish zloty as a result continues to trade strong with EUR/PLN hovering near multiyear lows around 4.26.

Graphs

EUR/PLN: zloty holding near strongest levels since early 2020 as sticky inflation suggests persistent interest rate support.

US 2-y yield holding above 4.7% support area as quite some Fed easing is already discounted after the recent market easing.

EUR/NOK: NOK recently profited from global risk rally. Decent data suggest NB won’t be in a hurry to cut rates anytime soon.

Oil (Brent) tries to avoid a break lower as markets still ponder the demand outlook.

Euro Edges Lower After ECB’s Financial Stability Warning

The euro has posted slight losses on Thursday. EUR/USD is down 0.20%, trading at 1.0860 in the North American session at the time of writing.

ECB warns of risks to financial stability

The ECB’s Financial Stability Review expressed concern that financial stability could be affected by the possibility of “adverse economic and financial surprises”. Geopolitical tensions such as in Ukraine and the Middle East had the potential to trigger large market reactions to negative news and the report warned that elections in the US and the European Union added more uncertainty. Still, the report found that overall threats to financial stability in the EU had lessened compared to the previous report six months ago.

The eurozone is showing signs of recovery and that has prompted the ECB to signal that it plans to lower interest rates next month, although it hasn’t provided any hints about rate plans after June.

US CPI drops to 3.4%, US dollar slips

A drop in April CPI on Wednesday reversed a trend of inflation moving higher and raised expectations of a Fed rate cut. The stock market responded with sharp gains while the US dollar was broadly lower and fell 0.54% against the euro on Wednesday.

The markets have priced in a September rate cut at 74% and a rate cut before the end of the year at 94%, according to the CME FedWatch tool.

Overlooked by all the attention to the inflation report, US retail sales fell sharply to 3% y/y in April, down from a revised 3.8% in March. Monthly, retail sales were flat, compared to a revised 0.6% in March. This points to consumers cutting down on spending due to high interest rates and could be a sign that the strong US economy is cooling down.

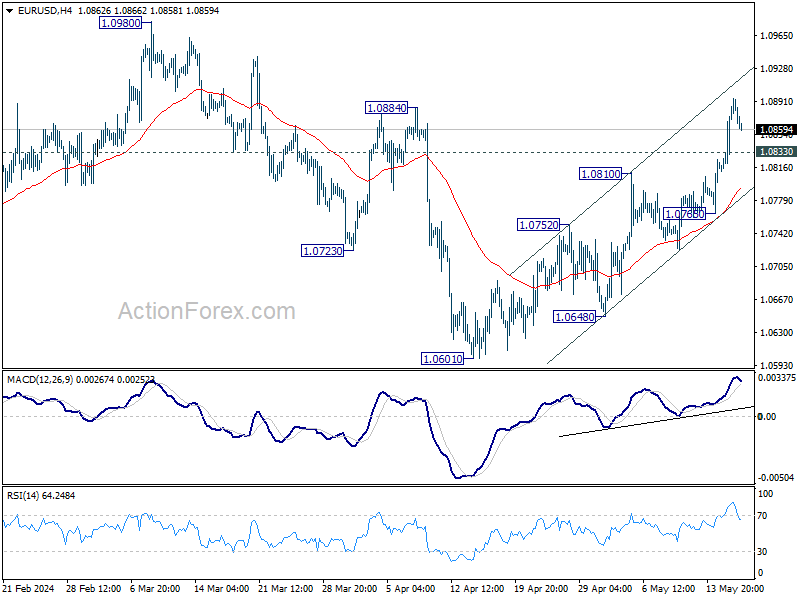

EUR/USD Technical

- EUR/USD is testing support at 1.0861. Below, there is support at 1.0836

- There is resistance at 1.0909 and 1.0934

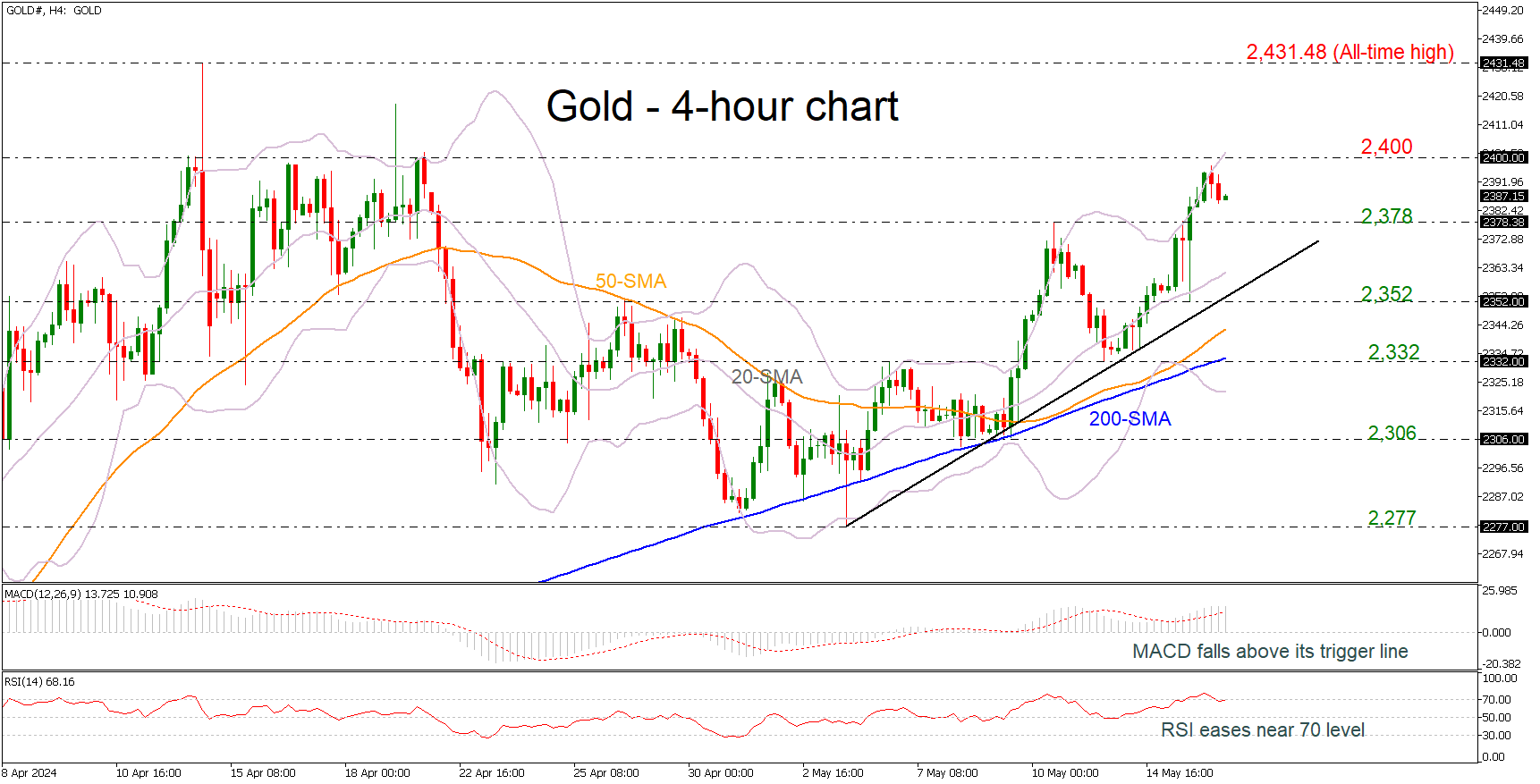

Gold Retreats After Hitting Upper Bollinger Band

- Gold remains bullish in near term

- RSI moves horizontally below 70 level

Gold prices recorded their second session of losses in the 4-hour chart after a failed attempt to break significantly above the 2,400 round level. Chances for a reversal are increasing as the RSI is pointing south after the climb in the overbought region, while the MACD is weakening its momentum above its trigger and zero lines.

Another step lower may reach a key support at 2,378, where the price stopped last Friday. Should this prove a weak obstacle, the selling could pick up speed until the 2,352 bottom, where any violation would bring more pressure to the market with the price probably stretching further down to test the 50- and the 200-period simple moving averages (SMAs) at 2,341 and 2,332 respectively.

Alternatively, in case of a rebound, immediate resistance could come from 2,400, before the focus shifts to the all-time of 2,431.48 again, which if surpassed, would confirm the long-term ascending tendency.

In the medium-term picture the price is still increasingly bullish as long as it holds well above the 200-day SMA and near the upper Bollinger band in the 4-hour chart, which is still rising.

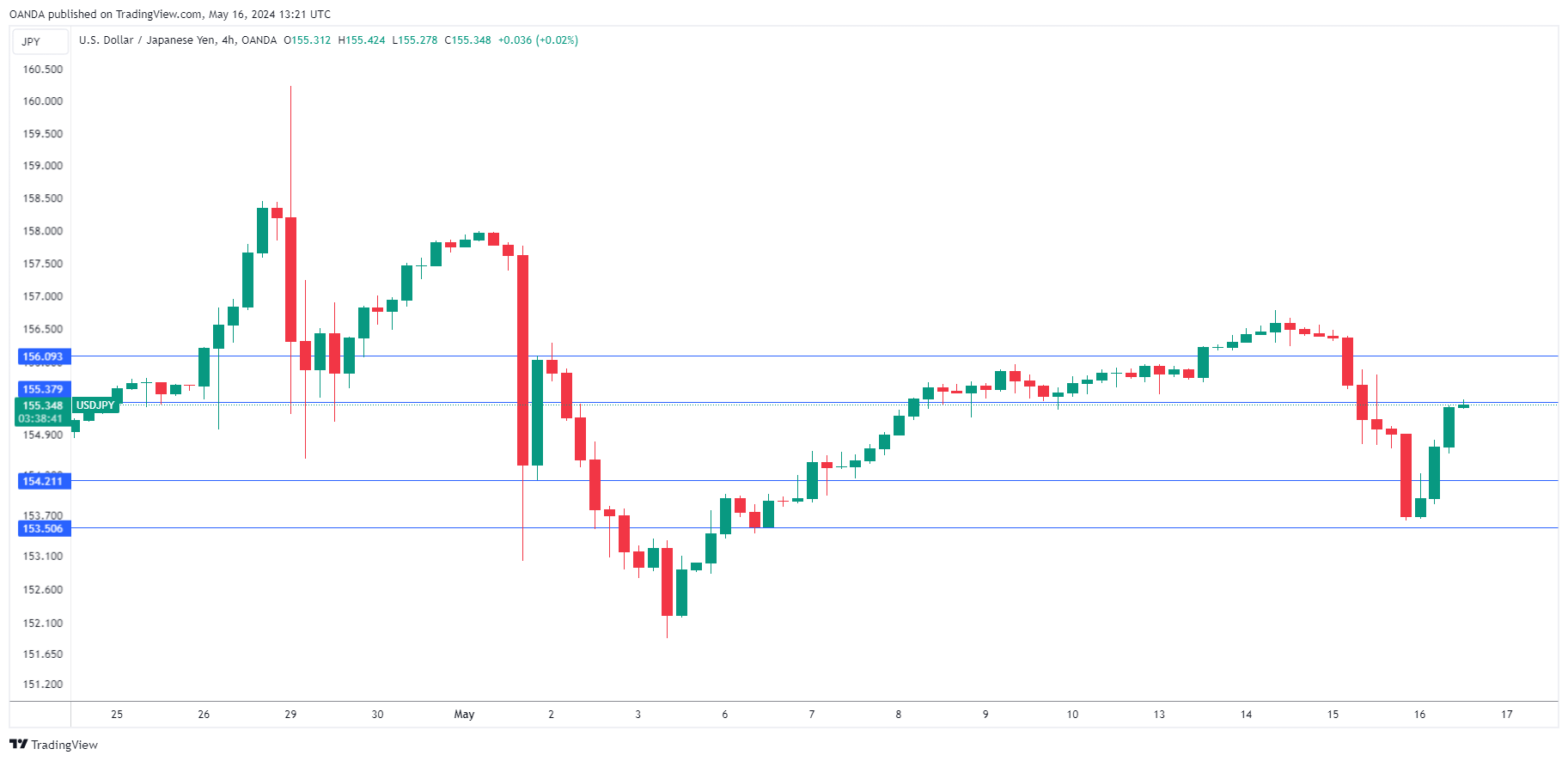

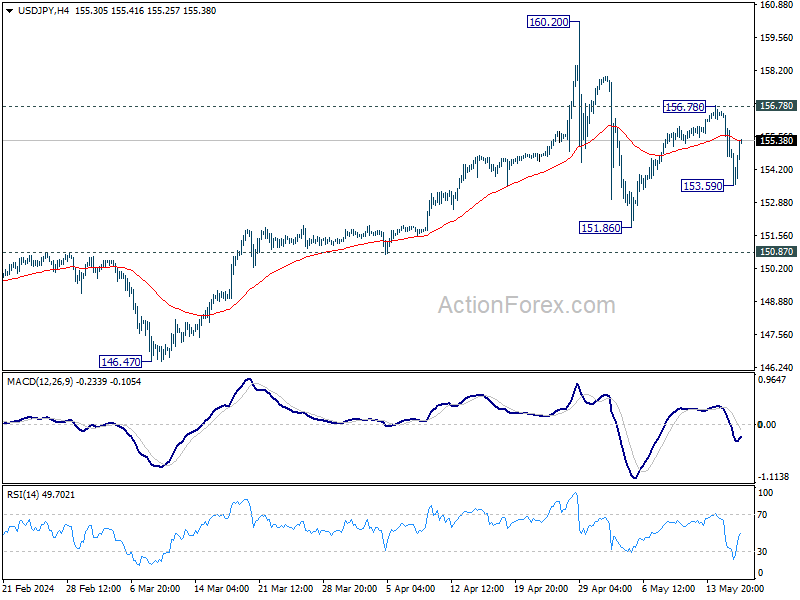

USD/JPY Steady as Japanese Economy Contracts

The Japanese yen climbed as much as 0.85% earlier on Thursday but has pared most of those gains. USD/JPY is trading at 155.38, up 0.31% in the European session.

Japan’s economy contracted in the first quarter. GDP declined by 2% y/y in the first quarter, following a revised 0% reading in Q4 2023. This was weaker than the market estimate of -15.%. On a quarterly basis, GDP declined by 0.5%, down from a revised 0% reading and just above the market estimate of -0.4%.

The disappointing GDP release was a result of weak private consumption, which declined for a fourth consecutive quarter. Consumers and companies cut spending due to high inflation and sluggish wage growth. As well, exports decreased in the first quarter, as global demand remains weak.

Yen surges as US inflation eases to 3.4%

After several US inflation reports which pointed to higher inflation, April CPI reversed directions and dropped from 3.5% to 3.4%. The decline in inflation, especially in the core rate, raised expectations of a Fed rate cut and sent the yen surging 0.98% in the aftermath of the inflation report. The markets have priced in a September rate cut at 70% and a rate cut before the end of the year at 92%, according to the CME FedWatch tool.

Overlooked by all the attention to the inflation report, US retail sales fell to 3% y/y in April, down sharply from a revised 3.8% in March. Monthly, retail sales were flat, compared to a revised 0.6% in March. This points to consumers cutting down on spending due to high interest rates and high inflation.

USD/JPY Technical

- USD/JPY pushed below support at 154.21 earlier and put pressure on support at 153.51

- There is resistance at 155.38 and 156.08

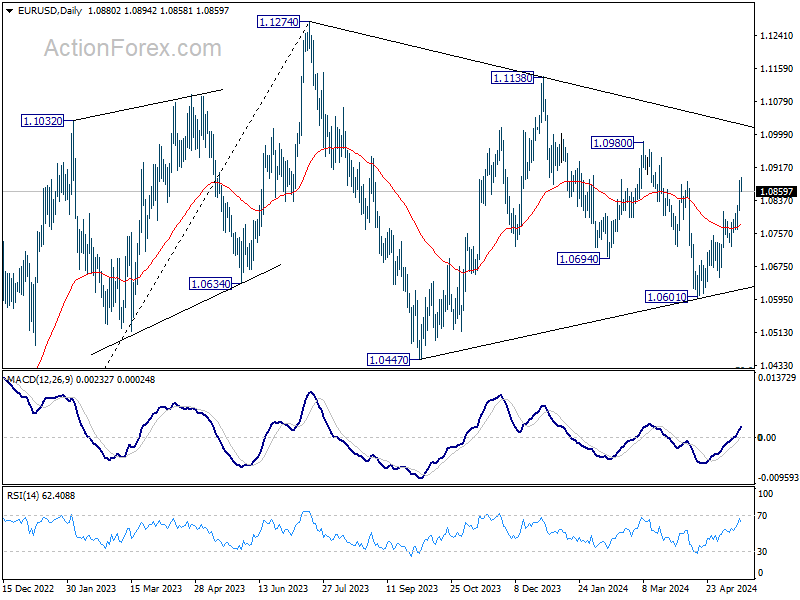

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0783; (P) 1.0804; (R1) 1.0842; More...

Intraday bias in EUR/USD remains on the upside for the moment. Current rise from 1.0601 is in progress for 1.0980 resistance. Decisive break there will confirm that whole fall from 1.1138 has completed already. On the downside, below 1.0833 minor support will turn intraday bias neutral first. But further rally is expected as long as 1.0765 support holds, in case of retreat.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern. Fall from 1.1138 is seen as the third leg and could have completed. Firm break of 1.1138 will argue that larger up trend from 0.9534 (2022 low) is ready to resume through 1.1274 high. On the downside, break of 1.0601 will extend the corrective pattern instead.

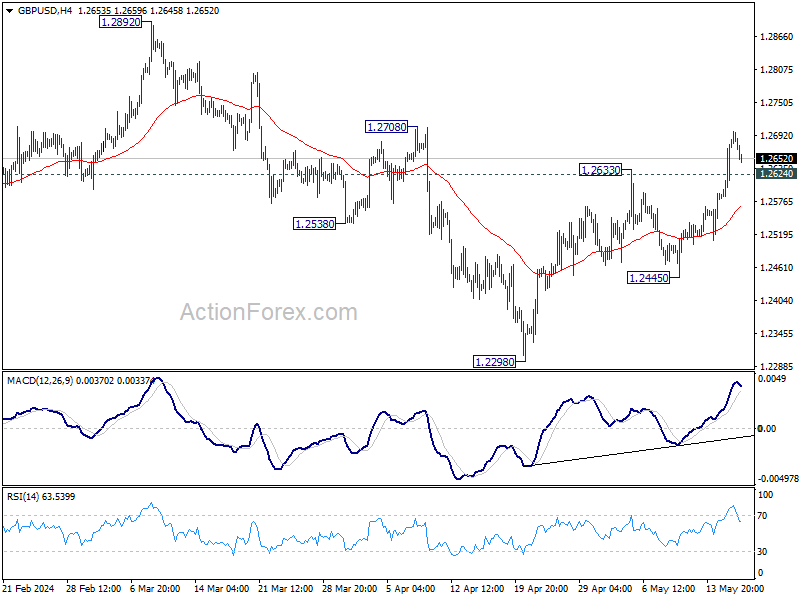

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2610; (P) 1.2648; (R1) 1.2725; More...

Intraday bias in GBP/USD remains on the upside for the moment. Rise from 1.2298 is in progress. Firm break of 1.2780 will pave the way to 1.2892 resistance next. On the downside, below 1.2624 minor support will turn intraday bias neutral first. But further rally will remain in favor as long as 1.2445 support holds in case of retreat.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern. Fall from 1.2892 is seen as the third leg which might have completed already. Break of 1.2892 resistance will argue that larger up trend from 1.0351(2022 low) is ready to resume through 1.3141. Meanwhile, break of 1.2298 support will extend the corrective pattern instead.

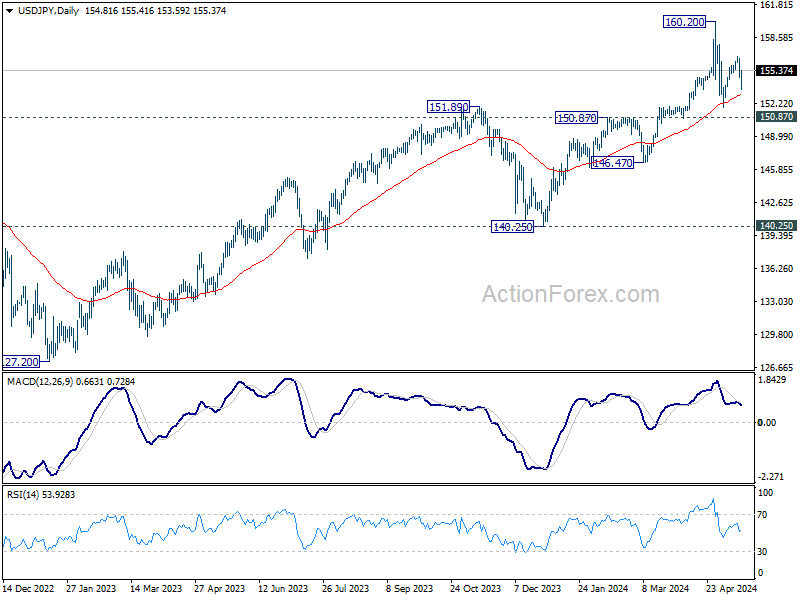

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 154.21; (P) 155.38; (R1) 156.08; More...

Intraday bias in USD/JPY is turned neutral with current recovery. Outlook is unchanged that fall from 156.78 is seen as the third leg of the corrective pattern from 160.20 high. Below 153.59 will target 151.86 support and possibly below. However, break of 156.78 will resume the rebound from 151.86 towards 160.20 high instead.

In the bigger picture, a medium term top might be formed at 160.20. But as long as 150.87 resistance turned support holds, fall from there is seen as correcting rise from 150.25 only. However, decisive break of 150.87 will argue that larger correction is possibly underway, and target 146.47 support next.

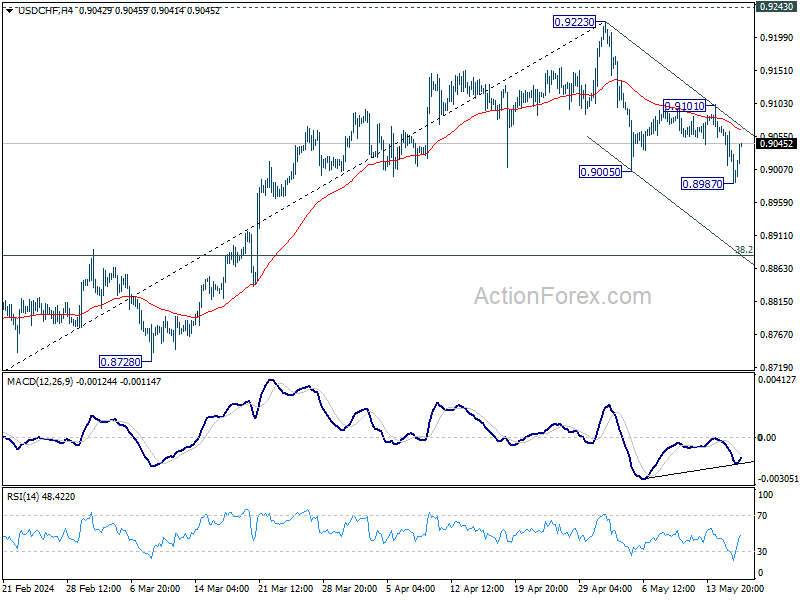

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9001; (P) 0.9036; (R1) 0.9057; More....

Intraday bias in USD/CHF is turned neutral again first with current recovery. But further decline is expected as long as 0.9101 resistance holds. Break of 0.8987 will resume the whole fall from 0.9223 and target 38.2% retracement of 0.8332 to 0.9223 at 0.8883 next. However, break of 0.9101 will turn bias back to the upside for stronger rebound.

In the bigger picture, price actions from 0.8332 medium term bottom are tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance, followed by sustained break of 38.2% retracement of 0.8332 to 0.9223 at 0.8883 will strengthen this case, and maintain medium term bearishness. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish for 1.0146.