Sample Category Title

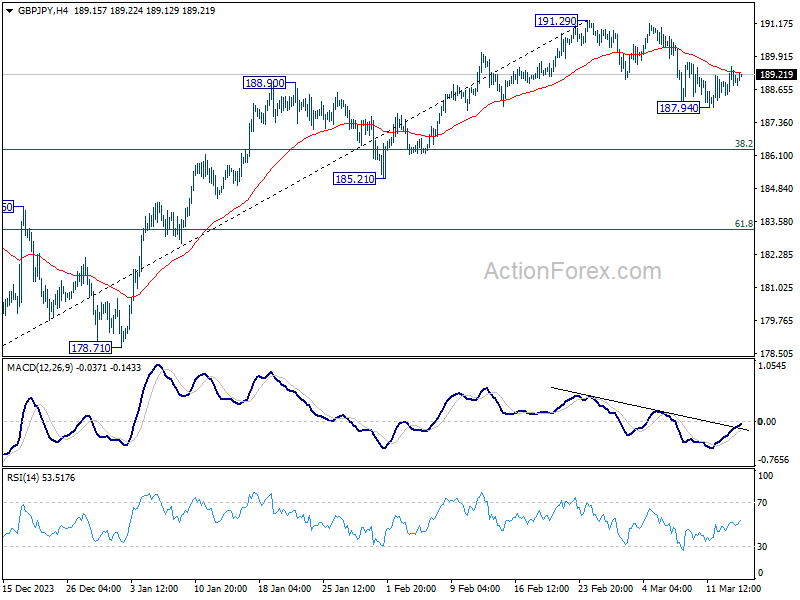

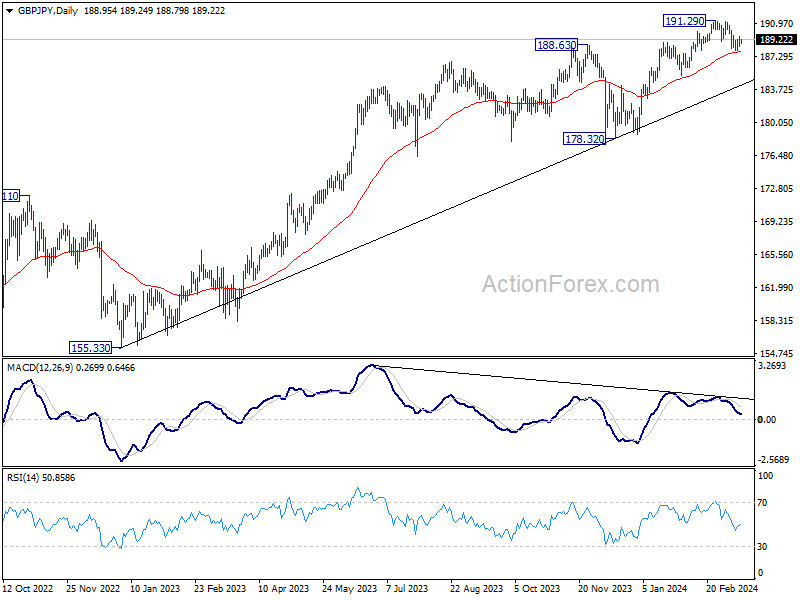

GBP/JPY Daily Outlook

Daily Pivots: (S1) 188.48; (P) 189.02; (R1) 189.61; More.....

Outlook in GBP/JPY remains unchanged and intraday bias stays neutral. On the downside, below 187.94 will resume the decline from 191.29 to 38.2% retracement of 178.32 to 191.29 at 186.33. Sustained break there will raise the chance of larger scale correction and target 61.8% retracement at 183.27. On the upside, though, firm break of 55 4H EMA (now at 189.29) will retain near term bullishness and bring retest of 191.29 high.

In the bigger picture, up trend from 123.94 (2020 low) is in progress. Medium term outlook will stay bullish as long as 178.32 support holds. Next target is 195.86 long term resistance (2015 high).

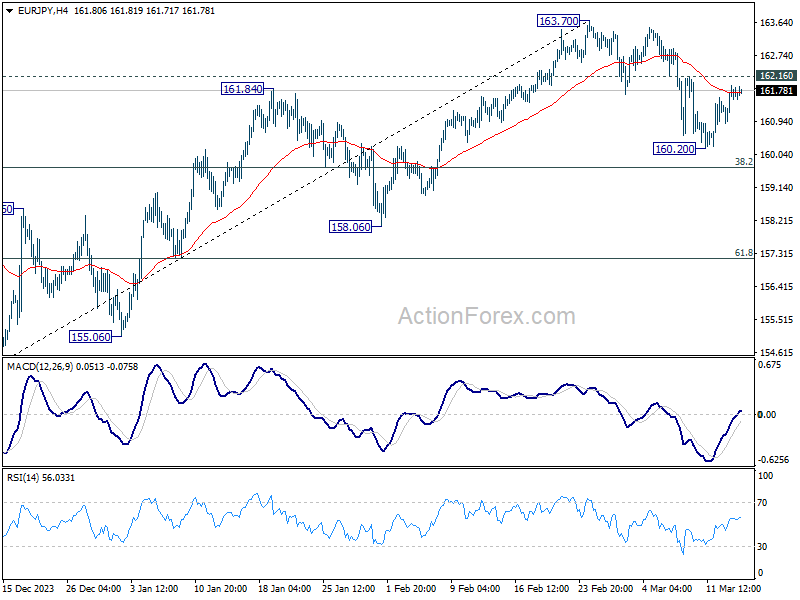

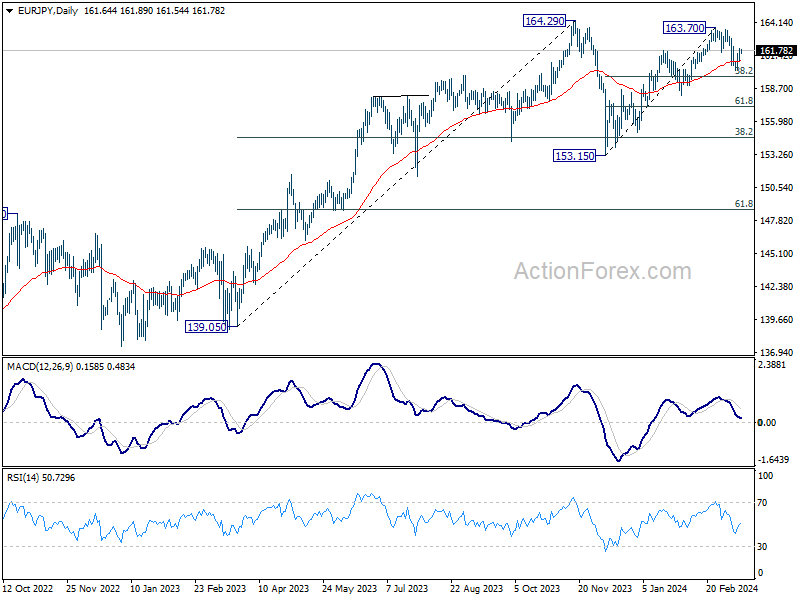

EUR/JPY Daily Outlook

Daily Pivots: (S1) 161.13; (P) 161.54; (R1) 162.18; More...

Intraday bias in EUR/JPY remains neutral and outlook is unchanged. On the downside, below 160.20 will resume the fall from 163.70 to 38.2% retracement of 153.15 to 163.70 at 159.66. Sustained break there will indicate that fall from 163.70 is reversing whole rise from 153.13, and target 61.8% retracement at 157.18. On the upside, though, above 162.16 minor resistance will retain near term bullishness, and bring retest of 163.70.

In the bigger picture, price actions from 164.29 medium term top are seen as a correction to rise from 139.05 which could still be extending. As long as 148.38 resistance turned support holds (2022 high), larger up trend from 114.42 (2020 low) is expected to resume through 164.29 at a later stage. Next target would be 169.96 (2008 high).

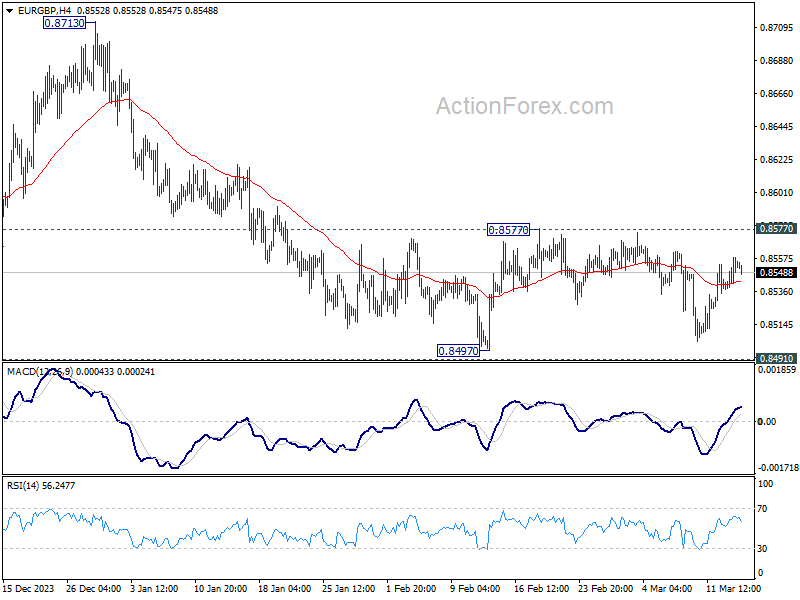

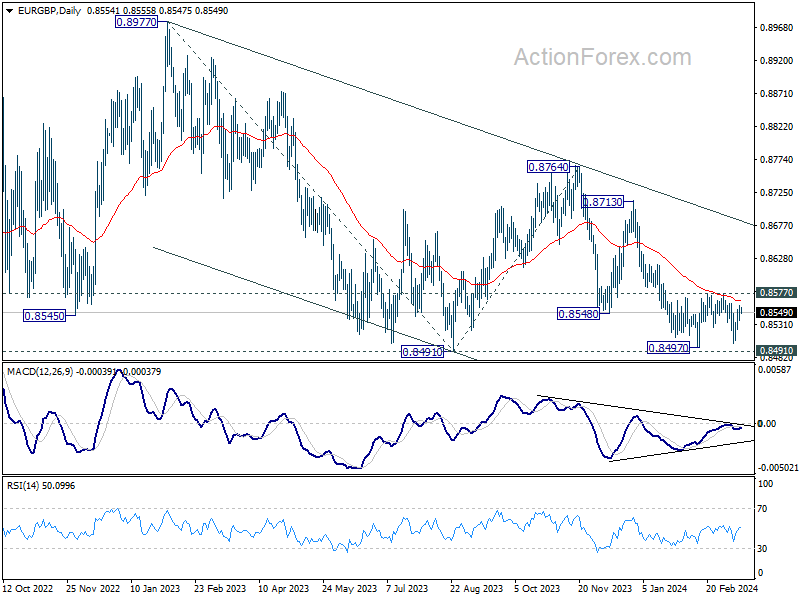

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8540; (P) 0.8550; (R1) 0.8565; More...

EUR/GBP is still bounded in range of 0.8497/8557 and intraday bias remains neutral. On the downside decisive break of 0.8491/7 support zone will confirm larger down trend resumption and target 0.8464 projection level first. Nevertheless, firm break of 0.8577 will turn bias back to the upside for stronger rebound.

In the bigger picture, fall from 0.8764 is seen as another leg in the whole down trend from 0.9267 (2022 high). Outlook will stay bearish as long as 0.8713 resistance holds. Break of 0.8491 will target 61.8% projection of 0.8977 to 0.8491 from 0.8764 at 0.8464.

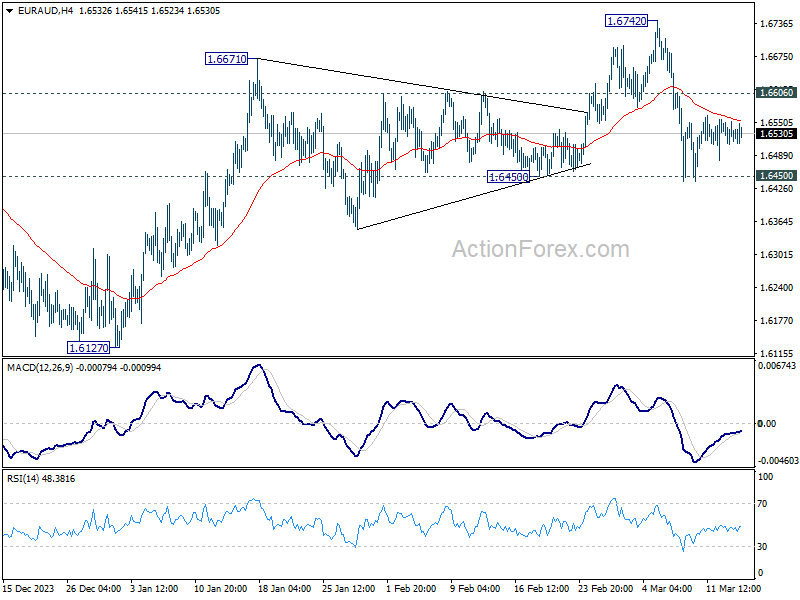

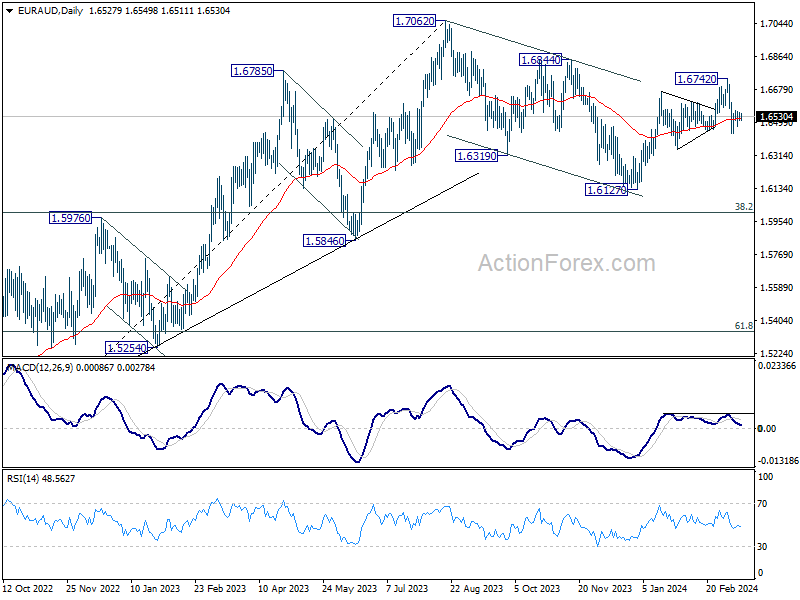

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6511; (P) 1.6536; (R1) 1.6559; More...

Range trading continues in EUR/AUD and intraday bias stays neutral at this point. On the downside, decisive break of 1.6450 support will argue that whole rebound from 1.6127 has completed with three waves up to 1.6742 already. Near term outlook will be turned bearish for 1.6127 again, to extend the whole corrective pattern from 1.7062. Nevertheless, strong rebound from current level, followed by break of 1.6606 minor resistance, will retain near term bullishness and bring retest of 1.6742.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low). Break of 1.6844 resistance will argue that this up trend is ready to resume through 1.7062 high. In case of another fall, strong support should be seen around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound.

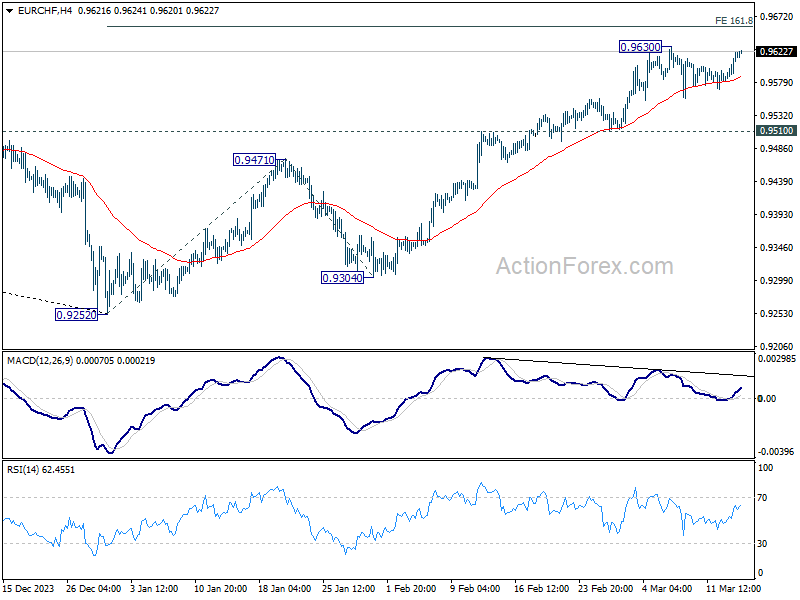

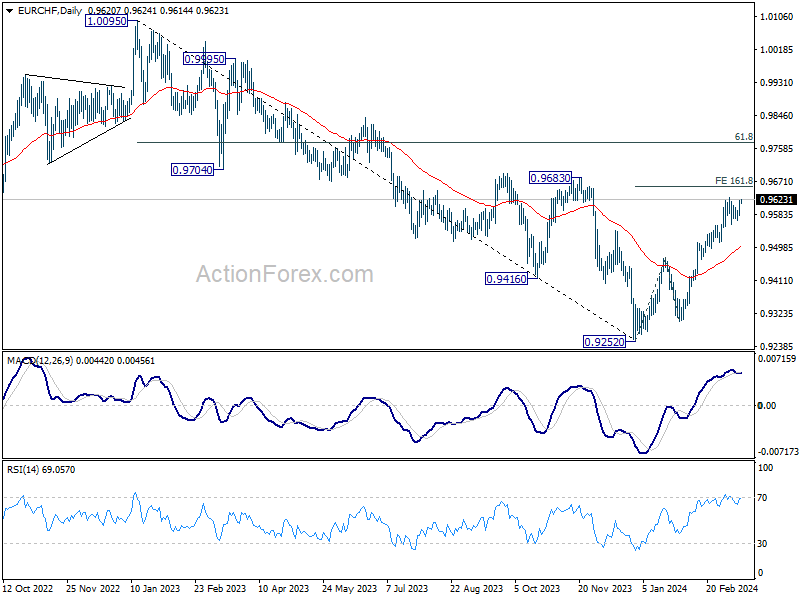

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9596; (P) 0.9610; (R1) 0.9635; More...

EUR/CHF is staying below 0.9630 despite today's recovery. Intraday bias remains neutral first. As long as 0.9510 support holds, further rally is still expected. On the upside, break of 0.9630 will resume the rise from 0.9252 and target 161.8% projection of 0.9252 to 0.9471 from 0.9304 at 0.9658 next. However, considering bearish divergence condition in 4H MACD, firm break of 0.9510 will turn bias back to the downside for deeper fall.

In the bigger picture, as long as 0.9683 resistance holds, rebound from 0.9252 are seen as a corrective move only. Larger down trend is expected to resume through 0.9252 after the correction completes. However, firm break of 0.9683 and sustained trading above 55 W EMA (now at 0.9620) will argue that 0.9252 is already a medium term bottom. Stronger rise would then be seen 61.8% retracement of 1.0095 to 0.9252 at 0.9773 and above.

Focus on Swedish inflation and US Retail Sales

In focus today

In the US, February retail sales and PPI are due for release today. Consensus expects a rebound in retail sales after the unusually weak January print, which might have been distorted by heavy seasonal adjustments at the start of the year. Markets will also follow if the sticky price pressures seen in the CPI earlier this week will be reflected in the PPI as well.

In Sweden, we get the inflation numbers for February. We forecast CPIF at 2.4% y/y and CPIF excl. energy at 3.5% y/y. The fall in core inflation can mainly be attributed to clothing, food, rent and hotel/restaurant prices (in that order of magnitude). However, uncertainty remains high not least because the impact of rent increases is difficult to predict and after a lower-than-expected increase in January, the risk remains to the upside. From the Riksbank, Anna Breman will be participating at a conference on the topic of sustainable finance and the Riksbank will publish a fresh payment report.

In Norway, the regional network survey is scheduled for release. The survey pointed to a drop in activity in Q1. Signs that the rate peak has been reached seem to have improved the sentiment among both corporates and households, and hence we expect that growth prospects will return to positive ground, albeit it should be noted that this does not mean that growth will pick up sharply into the summer, but just stop falling further.

Overnight, Japan's biggest labour union federation, Rengo, releases the first tally of pay deals. This will be the first indication whether wage growth will be strong enough this year to support a sustainable inflation pressure. The results of the spring wage negotiations will be absolutely key to the Bank of Japan's decision whether to start tightening policies.

In China, we also get overnight data. The PBOC releases the 1-year Medium-term Lending Facility (MLF) rate, but it is expected to be unchanged as PBOC likely awaits clearer signals of Fed easing. The 5-year MLF rate, which is a mortgage rate benchmark, was surprisingly cut by 25bp last month and is unlikely to be cut again already. However, PBOC has clearly signalled over the past week that the direction for rates is down and that they have more leeway when other central banks start easing as well. Moreover, Chinese house prices for February will also be released. The print can be seen as an important bellwether for a turn-around in the Chinese housing market. Last month data surprised to the upside, bringing some rays of light.

Economic and market news

What happened yesterday

In the US, the House of Representatives has passed a bill demanding ByteDance, the Chinese owner of TikTok, to divest its U.S. assets within six months or risk a ban. However, the bill's future in the Senate is still uncertain, as discussions persist. The bill marks the most recent step in a series of measures taken in Washington to address national security concerns regarding China.

In the euro area, industrial production declined more than expected in January amid December production being revised down, printing -3.2% m/m (cons: -1.8%) and -6.7% y/y (cons: -3.0%). Hence, the euro area industry starts the year on a weak footing and will likely not contribute to growth before the Q2 or Q3 of 2024. Note, that the decline was driven especially by the very volatile Irish industrial production that dropped 34% m/m due to a base effect from, most likely, a large patent in December.

Also, the ECB announced changes to its operational framework for implementing monetary policy. The key takeaways include the fact that the governing council will continue to steer the monetary policy stance through the deposit facility rate (DFR). The minimum reserve requirements remain unchanged at 1%, and the remuneration of minimum reserves will likewise stay unchanged at 0%.

Additionally, the main refinancing operations (MRO) rate will be adjusted so that the spread between the MROs and the DFR will be reduced to 15bp from the current spread of 50bp. Moreover, the rate on the marginal lending facility (MLF) will also be adjusted, maintaining the spread between the MLF rate and the rate in the MROs at 25bp. These changes will commence with the sixth maintenance period of 2024, beginning on September 18, 2024.

In the UK, January GDP data was fully in line with consensus, coming in at 0.2% m/m, -0.3% y/y and -0.1% 3M/3M. The market reaction was muted.

In geopolitics, US and Iranian officials reported that in January, the US engaged in secret talks with Iran in an effort to convince Tehran to leverage its influence over the Houthis to cease attacks on ships in the Red Sea. Oman facilitated the talks, with Omani officials shuttling between representatives from both nations. Additionally, U.S. Secretary of State Antony Blinken portended that the US is working towards setting up a maritime aid corridor into Gaza.

Equities: Global equities were marginally lower yesterday despite most sectors ending higher. However, with tech and healthcare lower a huge share of the index was dragging down. Europe outperformed the US and once again cross regional sector performance was very different. One can easily be caught wrong footed when looking at volatility, and especially the volatility in AI-related stocks. Hence, we recommend not to focus too much on the day-to-day change in sentiment but rather use the signs from the macro side which in our opinion hold the clues for the medium-term outlook. In US yesterday, Dow +0.1%, S&P 500 -0.2%, Nasdaq -0.5% and Russell 2000 +0.3%. Asian markets are mostly higher this morning together with European and US futures.

FI: European yields rose across the board yesterday albeit with limited news to trade on. The 10y German yield ended up 3bp on the day. The general tightening trend of for example the German ASW swap spread and the BTPs-Bund spread continued, with the ASW-spread crossing 30bp.

FX: A relatively quiet day with the recent USD respite proving short-lived as EUR/USD climbed somewhat. Not much action in Scandies as both SEK and NOK trades mostly sideways. EUR/GBP continued to climb steadily higher, whereas EUR/PLN remains below 4.30.

Crude Oil Prices Rise as Ukraine Hits Russian Refineries

Direction was mixed yesterday, as Tuesday’s hotter-than-expected US CPI print gave cold feet to investors regarding the Federal Reserve’s (Fed) ability to cut interest rates as soon as in June. The S&P 500 and Nasdaq consolidated near record, energy stocks helped tempering losses in the S&P500 as technology stocks traded down. The dollar index rebounded as the selloff in Treasuries accelerated despite a strong 30-year bond auction.

Today, focus is on the US retail sales and producer price inflation data. Retail sales are expected to have rebounded following a relatively weak read in January, while producer prices are expected to have risen in February, fueled by higher energy prices. Normally, I would expect higher-than-expected retail sales and higher-than-expected PPI data to temper the Fed rate cut bets, back a further rise in US yields and the dollar, and trigger a downside correction in the US stock markets.

Speaking of oil prices, the positive pressure is building after the EIA data confirmed a 1.5 mio barrel fall in US oil inventories last week, and after Ukraine attacked major Russian oil refineries with drones and damaged around 12% of the country’s oil-processing capacity. The barrel of US crude tested the $80pb level. Offers near $80pb could be cleared on the back of rising tensions, yet I doubt that we will see a sustainable rise in oil prices above this level when the geopolitical jitters disappear from the headlines. There is still a strong resistance within the $80/82pb range.

Elsewhere, tensions between the US and China are on the rise again, as US House passed a bill to ban Tiktok unless the Chinese ByteDance sells the platform to a third party that would comply with the US data security demands. The bill is on its way to the White House. The US accuses China to use the user data and build propaganda using the platform. The affair is highly political of course, and it is one more major point that opposes the two presidential candidates, Biden and Trump. Biden says he will sign the bill, while Trump says banning TikTok would give too much power to Facebook, that he openly dislikes – as the platform imposed a ban on the ex-President after the Capitol riot back in 2021. Meta didn’t react much to the news.

Meanwhile

European stocks extended gains and hit fresh record as energy and luxury names led the rally higher yesterday. The EURUSD consolidates gains below the 1.10 level and should see a solid resistance into this level, especially if we see another hot inflation report from the US today. European Central Bank’s (ECB) Wunsch said yesterday that the bank may eventually start lowering the interest rates without being sure that inflation is returning to the 2% target, and that the latter decision could come ‘before so long’. Listening to Lagarde and other ECB members, it sounds like a June cut is a done deal, unless a significant surprise occurs on the inflation front. But a lot can change from now to June. If tensions between Ukraine and Russia escalate in a way to boost oil prices, we will certainly see the central banks constrained to delay their rate cut plans. For now, however, the expectation is that the ECB will start cutting in June and cut 4 times this year. The bank also announced changes to its operational framework in a way to allow the banks in different locations to ask for liquidity that they need, so that the monetary policy could be more flexible to better meet the various needs of various economies across the bloc as excess liquidity dries out. The market reaction to the latter changes is expected to be limited.

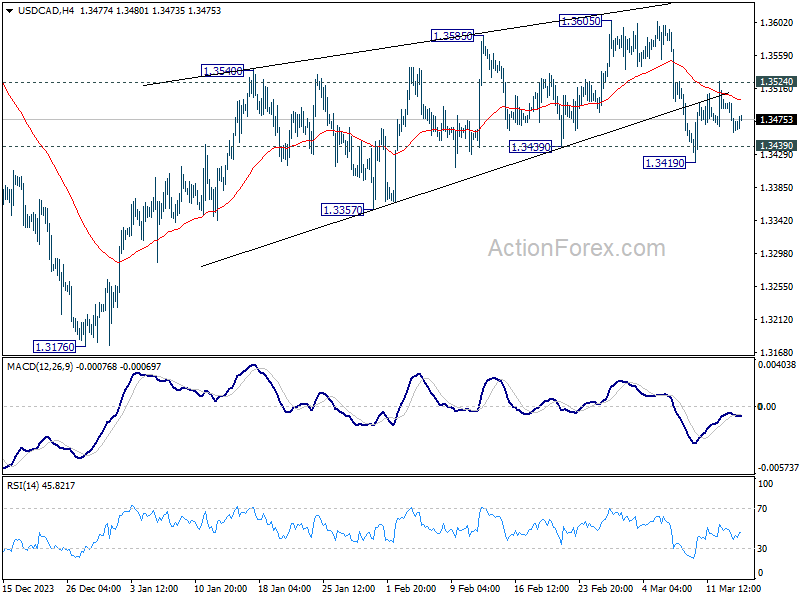

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3453; (P) 1.3476; (R1) 1.3494; More...

No change in USD/CAD's outlook and intraday bias stays neutral. On the downside, break of 1.3419 and sustained trading below 1.3439 support will argue that rebound from 1.3176 has completed as a corrective move to 1.3605. Near term outlook will be turned bearish for 1.3357 support first. On the upside, though, break of 1.3524 minor resistance will revive near term bullishness, and turn bias back to the upside for retesting 1.3605 resistance instead.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern only. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Overall, larger up trend from 1.2005 (2021 low) is still expected to resume through 1.3976 at a later stage.

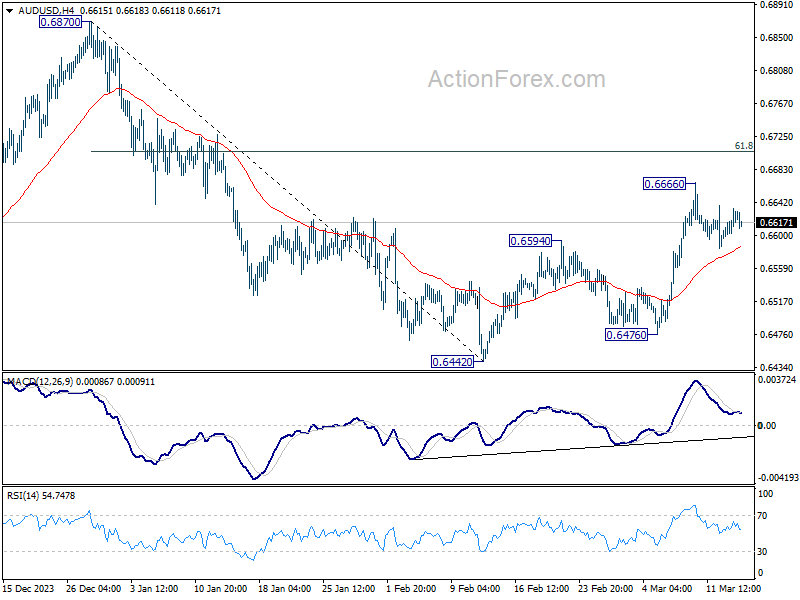

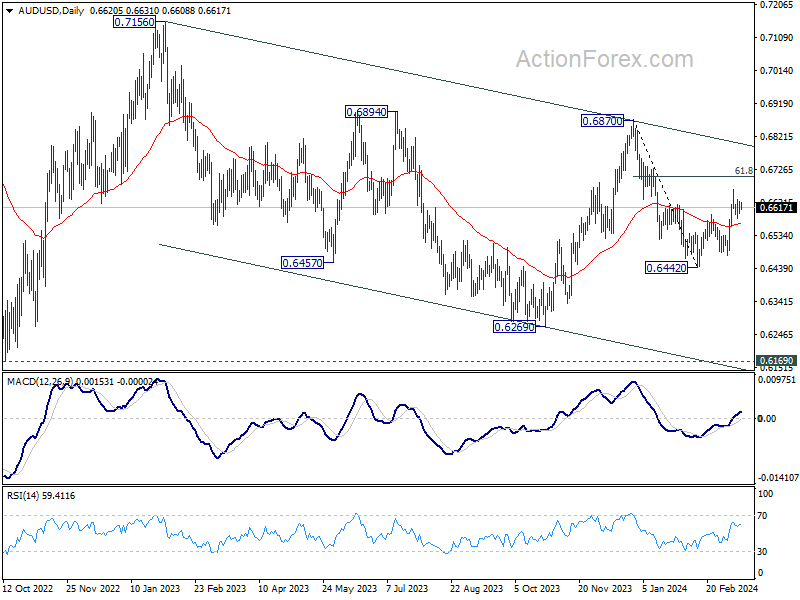

AUD/USD Daily Report

Daily Pivots: (S1) 0.6603; (P) 0.6619; (R1) 0.6638; More...

Intraday bias in AUD/USD remains neutral and outlook is unchanged. Another rise will be mildly in favor as long as 55 4H EMA (now at 0.6586) holds. Above 0.6666 will resume the rebound from 0.6442 to 61.8% retracement of 0.6877 to 0.6442 at 0.6707 next. Sustained trading above there will argue rise from 0.6442 is probably resuming whole rally from 0.6269. Nevertheless, sustained break of 55 4H EMA will revive near term bearishness and bring retest of 0.6442 low instead.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which might still be in progress. Overall, sideway trading could continue in range of 0.6169/7156 for some more time. But as long as 0.7156 holds, an eventual downside breakout would be mildly in favor.

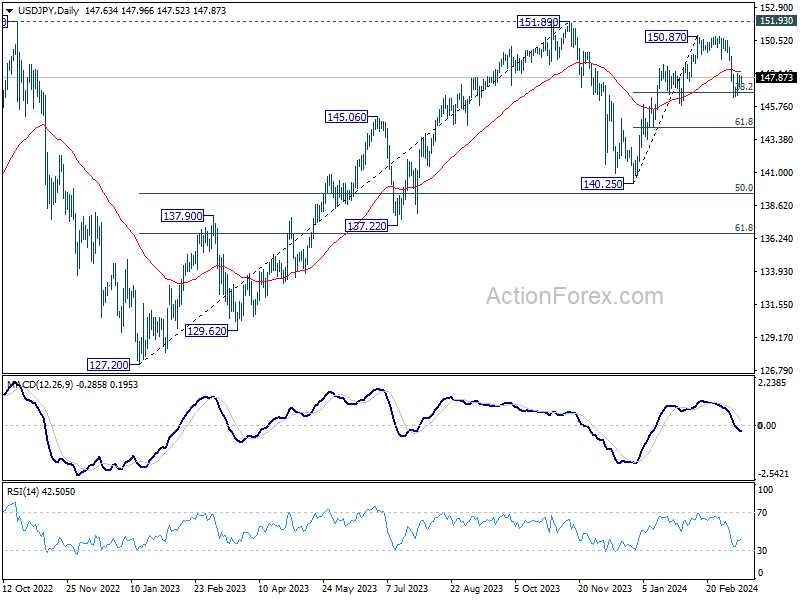

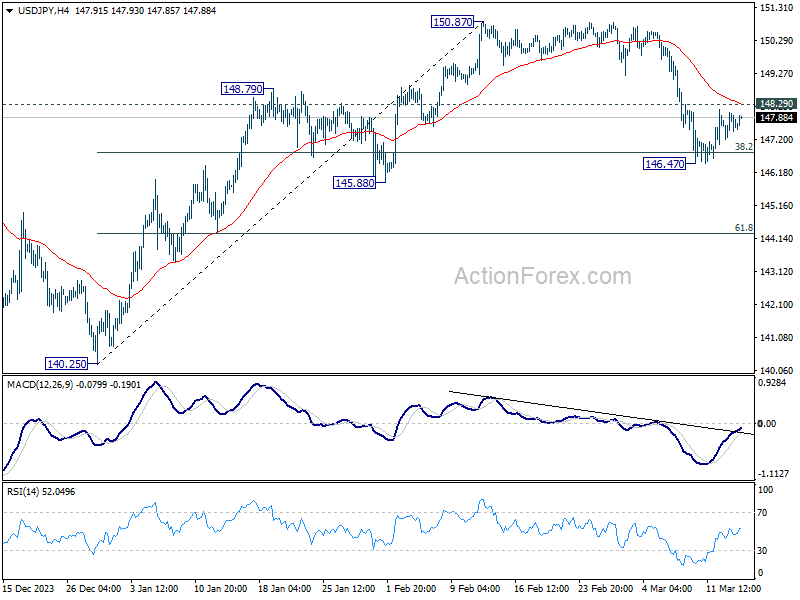

USD/JPY Daily Outlook

Daily Pivots: (S1) 147.31; (P) 147.68; (R1) 148.12; More...

Intraday bias in USD/JPY remains neutral for the moment. On the downside, sustained break of 38.2% retracement of 140.25 to 150.87 at 146.81 will argue that fall from 150.87 is reversing the whole rally from 140.25. In this case, deeper decline would be seen to 61.8% retracement at 144.30 and below. Nevertheless, strong support from 146.81, followed by break of 148.29 minor resistance resistance, will argue that fall from 150.87 is merely a correction, which has completed already. Retest of 150.87 should be seen next.

In the bigger picture, no change in the view that price action from 151.89 (2023 high) are correction to up trend from 127.20 (2023 low). The question is whether this correction has completed at 140.25, or extending with fall from 150.87 as the third leg. Sustained break of above mentioned 146.81 fibonacci level will favor the latter case. But even so, downside should be contained by 50% retracement of 127.20 to 151.89 at 139.54.