Sample Category Title

Hotter-Than-Expected Inflation Will Likely Call for Caution at Next Week’s FOMC Meeting

Inflation in the US accelerated, not only in terms of monthly headline figure but everywhere, both core and headline, and both yearly and monthly figures came in hotter-than-expected. While gasoline prices counted among the major drivers of monthly inflation, shelter, electricity, used cars, air travel and clothes remained the major drivers of inflation on a yearly basis. That was not an encouraging CPI read. The US 2-year yield spiked past 4.60% on fear that the Federal Reserve (Fed) may not be able to cut the rates as soon as we think it will, and the 10-year advanced to 4.17% after the sale of a $39 billion worth of 10-year notes. The US dollar index made an attempt past the 103 level, and major currencies retreated against a broadly stronger greenback on softer dovish Fed expectations. The EURUSD tested the 1.09 level and gold fell to $2150 per ounce.

Key takeaway: Hotter-than-expected inflation will likely call for caution at next week’s FOMC meeting and get the Fed members to sound cautious about the timing and the number of rate hikes that they have in mind for this year. Happily, we don’t need to speculate much as the new dot plot is due as soon as next week. For now, the June cut expectation remains the base-case scenario – with a slightly lower 66% assessed to it after yesterday’s inflation update, and the Fed is expected to cut three times before the end of the year. But don’t dream rosy, the Fed members will probably sound cautious about the risk of inflation uptick.

Big caps can’t care less

Stock markets shrugged off the bad vibes from the unideal CPI data in a record time. The S&P500 fell as a kneejerk reaction to a hotter-than-expected inflation data but losses remained very short-lived, and the index advanced to a fresh record instead on narrative that, yes, inflation was hotter-than-expected, but it could’ve been worse.

Of course, if we function that way, we don’t need data anymore. So let’s admit that yesterday's stock market reaction to the data was unusual and irrational. The bullish trend is too strong to let go of and FOMO – fear of missing out - the AI rally is the major driver of the big-cap stocks right now.

On the other hand, inflation is not necessarily bad news for AI-related stocks. Higher inflation coupled with decreased pricing power for companies means stronger efforts to cut costs. And there is nothing better than turning to AI to cut costs effectively without necessarily giving up productivity. In this context, AI could be a hedge against an extended period of above-target inflation. But does that justify the 7% jump in Nvidia’s stock price yesterday?

BoE doves reassured

Sterling fell against the dollar as softer-than-expected jobs data in the UK reassured the Bank of England (BoE) doves and boosted the expectation of rate cuts this year to almost three following the data. Cable fell below 1.2750 yesterday but the pair has rebounded since and is ready to test the 1.28 resistance this morning as the BoE is not in a rush to start cutting rates either. Released this morning, GDP numbers came in line with expectations while construction output rose more than expected. The positive data should temper the pound selloff.

Wages, wages

In Japan, all eyes are on wages negotiations as many Japanese unions disclose their pay deals with employers this week. Yen traders are closely watching the news as any pickup in wages should boost inflation expectations and get the Bank of Japan (BoJ) to exit the negative rates sooner rather than later. So far, it seems that big corporations meet wage demands. Japan’s biggest union group Rengo will give its initial count on Friday, and it’s expected to secure a pay rise of above 4% - a thing that has not happened in three decades due to a sticky deflation in Japan. Any positive surprise on the wages front should boost the BoJ hawks and the speculation that the BoJ could hike rates as soon as next week. The USDJPY saw support below the 147 this week but the downside risks prevail. I believe that the BoJ will more likely to give a strong hint that it will hike rates than hike next week. But no one knows how the BoJ will hike rates. Would they rather surprise the market or prepare investors? It’s been so long since the BoJ last hiked rates.

US crude rebounds

US crude tested the 200-DMA to the upside as the API data printed a 5.5-mio barrel fall in US oil inventories last week. OPEC raised its economic outlook for the year and said that oil demand will increase by 2.25mbpd this year and by 1.85mbpd next year. That was unchanged from their previous forecast. Still, oil bulls remained timid above the 200-DMA and the barrel of US crude is trading below this level this morning. A delay in Fed cuts could further reinforce offers above $80pb level.

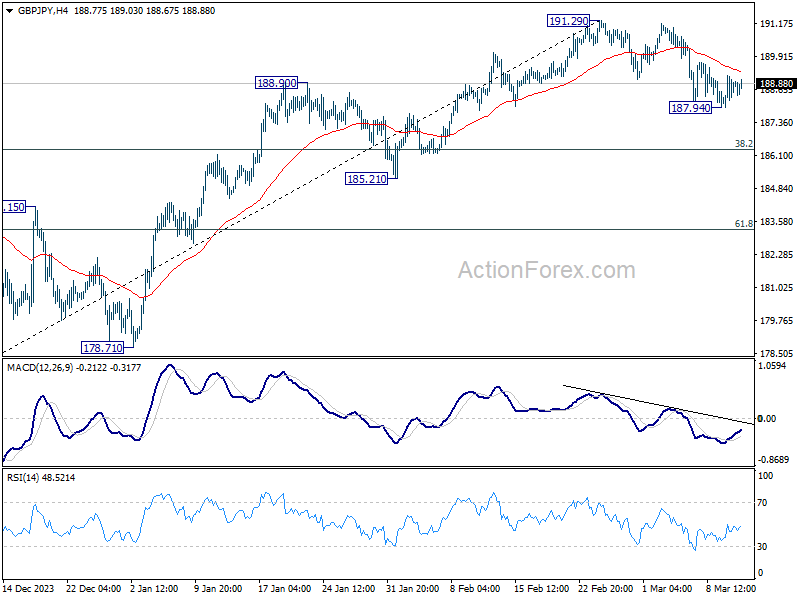

GBP/JPY Daily Outlook

Daily Pivots: (S1) 188.20; (P) 188.70; (R1) 189.42; More.....

Intraday bias in GBP/JPY stays neutral for the moment. On the downside, below 187.94 will resume the decline from 191.29 to 38.2% retracement of 178.32 to 191.29 at 186.33. Sustained break there will raise the chance of larger scale correction and target 61.8% retracement at 183.27. On the upside, though, firm break of 55 4H EMA (now at 189.33) will retain near term bullishness and bring retest of 191.29 high.

In the bigger picture, up trend from 123.94 (2020 low) is in progress. Medium term outlook will stay bullish as long as 178.32 support holds. Next target is 195.86 long term resistance (2015 high).

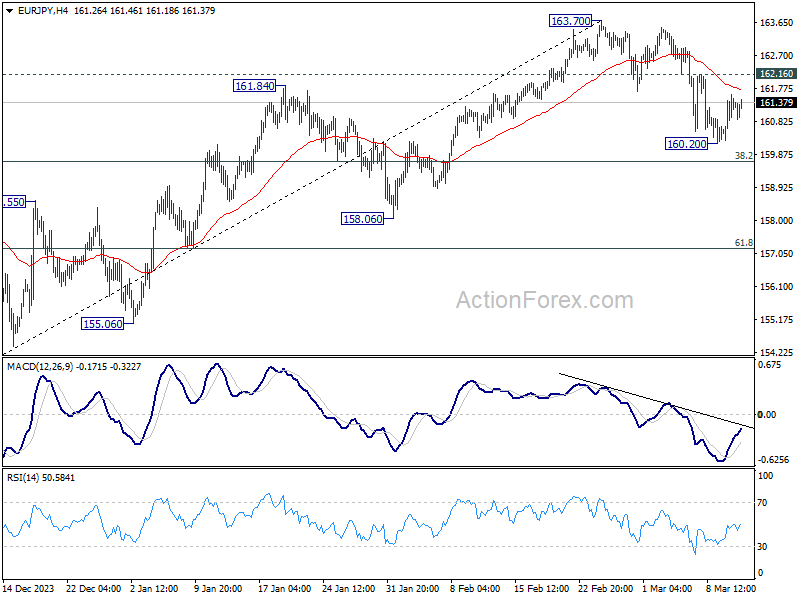

EUR/JPY Daily Outlook

Daily Pivots: (S1) 160.54; (P) 161.08; (R1) 161.88; More...

Intraday bias in EUR/JPY stays neutral at this point. On the downside, below 160.20 will resume the fall from 163.70 to 38.2% retracement of 153.15 to 163.70 at 159.66. Sustained break there will indicate that fall from 163.70 is reversing whole rise from 153.13, and target 61.8% retracement at 157.18. On the upside, though, above 162.16 minor resistance will retain near term bullishness, and bring retest of 163.70.

In the bigger picture, price actions from 164.29 medium term top are seen as a correction to rise from 139.05 which could still be extending. As long as 148.38 resistance turned support holds (2022 high), larger up trend from 114.42 (2020 low) is expected to resume through 164.29 at a later stage. Next target would be 169.96 (2008 high).

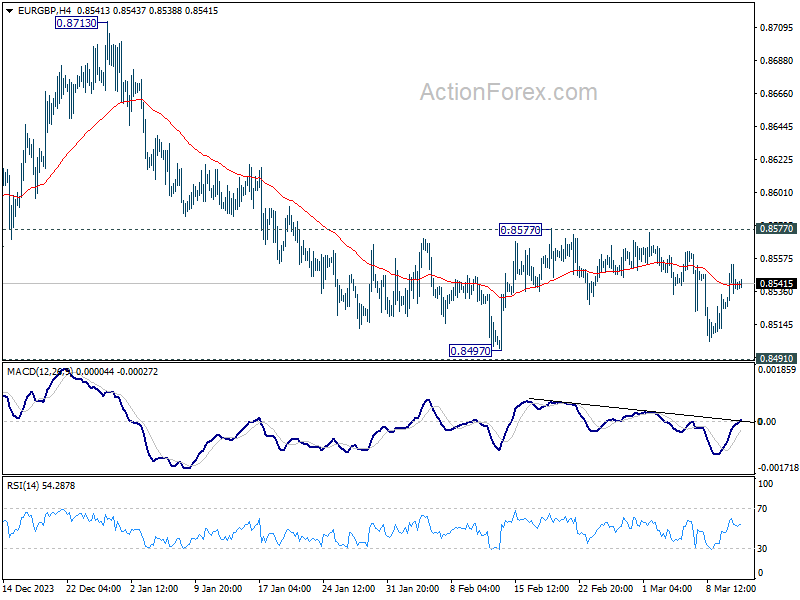

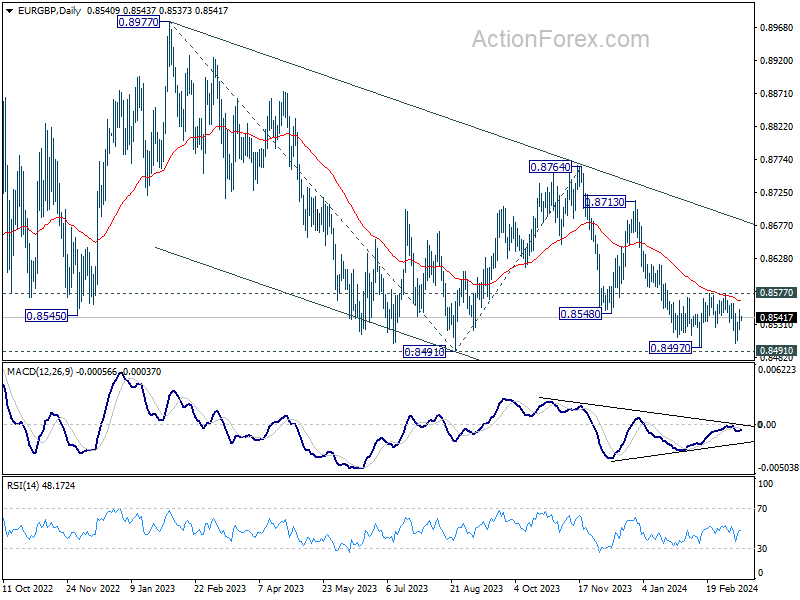

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8521; (P) 0.8538; (R1) 0.8557; More...

Intraday bias in EUR/GBP remains neutral as it's still bounded in range trading. On the downside decisive break of 0.8491/7 support zone will confirm larger down trend resumption and target 0.8464 projection level first. Nevertheless, firm break of 0.8577 will turn bias back to the upside for stronger rebound.

In the bigger picture, fall from 0.8764 is seen as another leg in the whole down trend from 0.9267 (2022 high). Outlook will stay bearish as long as 0.8713 resistance holds. Break of 0.8491 will target 61.8% projection of 0.8977 to 0.8491 from 0.8764 at 0.8464.

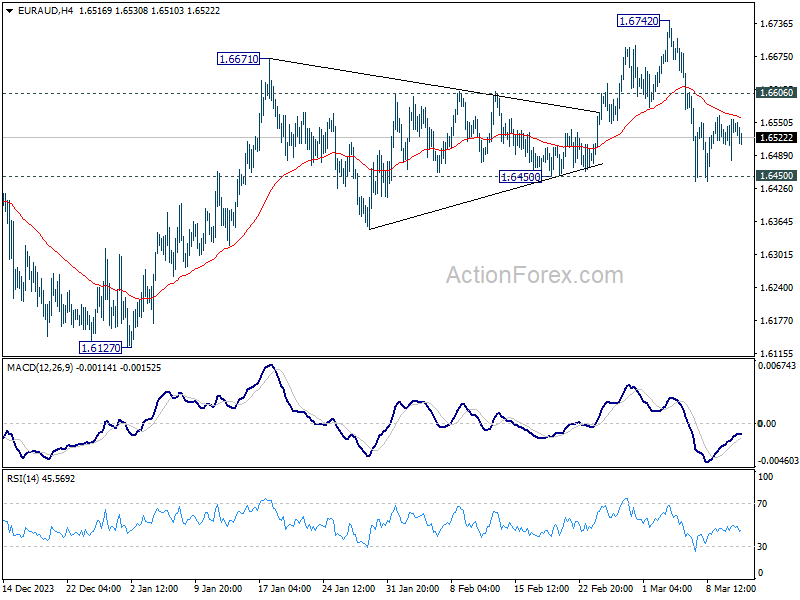

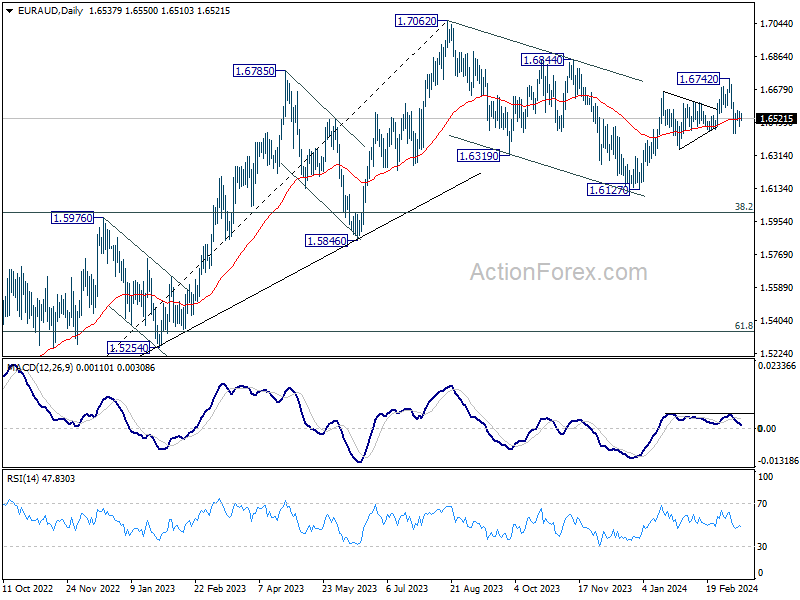

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6494; (P) 1.6528; (R1) 1.6573; More...

Intraday bias in EUR/AUD remains neutral as range trading continues. On the downside, decisive break of 1.6450 support will argue that whole rebound from 1.6127 has completed with three waves up to 1.6742 already. Near term outlook will be turned bearish for 1.6127 again, to extend the whole corrective pattern from 1.7062. Nevertheless, strong rebound from current level, followed by break of 1.6606 minor resistance, will retain near term bullishness and bring retest of 1.6742.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low). Break of 1.6844 resistance will argue that this up trend is ready to resume through 1.7062 high. In case of another fall, strong support should be seen around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound.

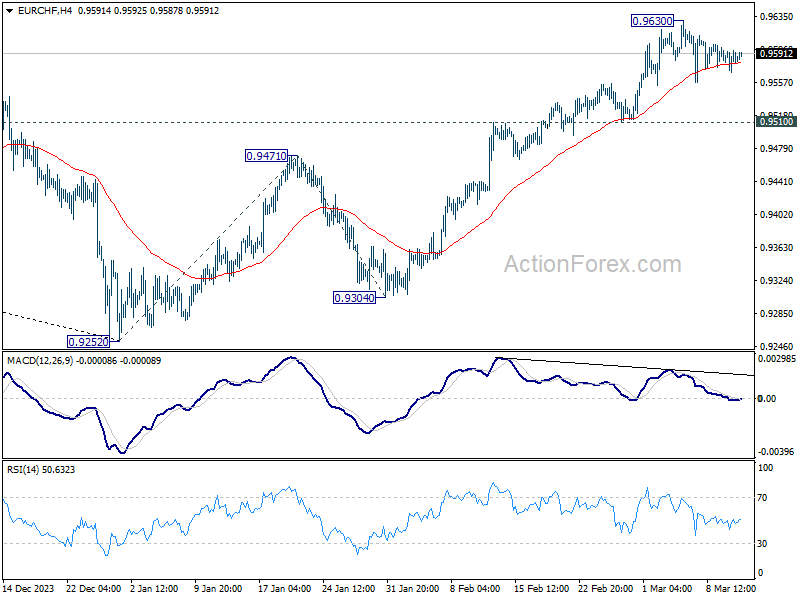

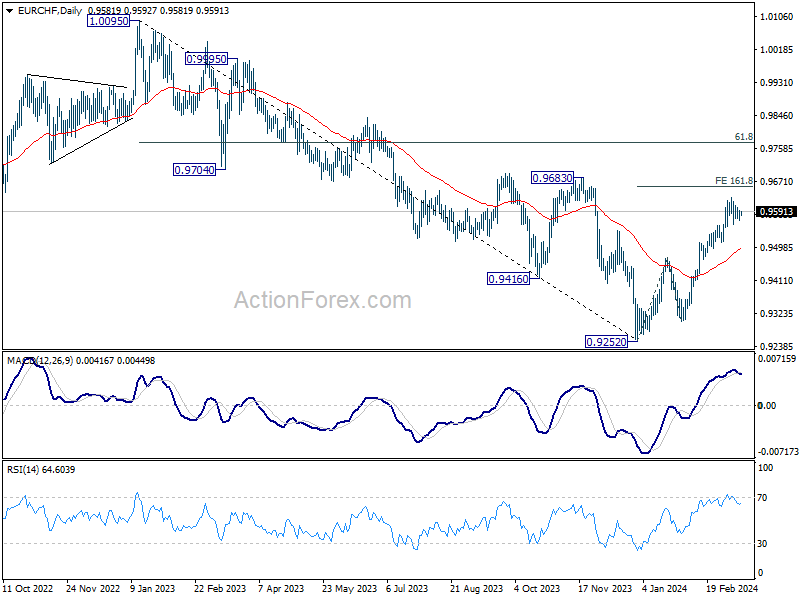

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9572; (P) 0.9585; (R1) 0.9598; More...

EUR/CHF is still extending the consolidation from 0.9630 and intraday bias stays neutral. As long as 0.9510 support holds, further rally is still expected. On the upside, break of 0.9630 will resume the rise from 0.9252 and target 161.8% projection of 0.9252 to 0.9471 from 0.9304 at 0.9658 next. However, considering bearish divergence condition in 4H MACD, firm break of 0.9510 will turn bias back to the downside for deeper fall.

In the bigger picture, as long as 0.9683 resistance holds, rebound from 0.9252 are seen as a corrective move only. Larger down trend is expected to resume through 0.9252 after the correction completes. However, firm break of 0.9683 and sustained trading above 55 W EMA (now at 0.9620) will argue that 0.9252 is already a medium term bottom. Stronger rise would then be seen 61.8% retracement of 1.0095 to 0.9252 at 0.9773 and above.

UK GDP Data and Euro Area Industrial Production Figures on Today’s Menu

In focus today

In the euro area, we receive industrial production figures for January. It will be interesting to see how actual production fared in January as soft indicators have shown improvements and the global manufacturing cycle has bottomed out. Also, the ECB is set to unveil its new operational framework.

In the UK, at 8:00 CET we get the monthly GDP figures for January.

In Sweden, today's focus is on speeches from Riksbank deputy governors Flodén at 08:50 CET and Breman at 09:00 CET regarding the economic situation and current monetary policy.

Economic and market news

What happened overnight

In the US, as highly anticipated, the presidential election this year will very likely be a rematch of the 2020 election, as both President Joe Biden and former President Donald Trump secured the required number of delegates to become their parties' nominees. However, this was unofficially confirmed last week when Nikki Haley pulled out of the race.

In Japan, Reuters sources reported that the BoJ is likely to provide numerical guidance on its future bond purchases after it is soon expected to exit its long-standing yield curve control policy and negative rates. Purchases would remain close to current levels to avoid abrupt spikes in yields. Furthermore, some of the biggest Japanese companies, including Toyota, Panasonic, and Nissan, have offered their largest pay raises in decades during the annual wage negotiations. Hence, this could add support to sustainable inflation pressure.

In Europe, Governing Council member Pierre Wunsch (hawk) reiterated that the ECB may need to take a risk by implementing an interest rate cut soon, despite concerns over high wage inflation and service price increases.

What happened yesterday

In the US, February CPI came in slightly above expectations. Headline inflation was 0.44% m/m SA (consensus +0.4%) while core inflation was 0.36% m/m SA (consensus 0.36%), The details were somewhat concerning for the Fed as well - for instance non-housing services inflation, which is the key point of focus for the Fed, remained steady from January. For more details, see Global Inflation Watch, 12 March. Additionally, the NFIB's February survey showed that the small business optimism index edged down to the lowest level since May amid inflation concerns.

In Germany, the final inflation print confirmed the flash release of 2.5% y/y (0.4% m/m) increase in CPI and core CPI at 3.4% y/y. The underlying details reveal a softer inflation print than the headline figure due to package holidays and the VAT increase on food in restaurants.

In the UK, the labour report for January/February was released yesterday. Wage growth came in lower than expected across the board with average weekly earnings excl. bonus at 6.1% 3M/YoY. Similarly, the KPMG/REC report on UK jobs, which was released early Monday night showed continued broad easing in the labour market with starting salaries rising at the slowest pace for almost three years and vacancies declining rapidly. With official data still suffering from poor data quality, the BoE increasingly relies on the KPMG/REC survey as a leading indicator for wage growth and of labour market tightness.

On the geopolitical stage, President Biden announced that the US will provide a new USD 300m military aid package for Ukraine - albeit the USD 300m is merely a fraction of a USD 60bn aid package Congress has debated over the past few months. Likewise, the EU is set to agree on a new EUR 5bn military aid fund later today, reported by the Financial Times yesterday. Finally, a vessel carrying 200 tonnes of food for Gaza departed from Cyprus, which is part of a pilot project to establish a new sea route for aid to Gaza.

Equities: Global equities were higher yesterday despite a mixed US CPI report and higher yields. Looking at the sector rotation it also reveals this was not just about a very benign inflation outlook but also part of what we call the AI-frenzy with very elevated volatility in some single names. This sign of exuberance is as a standalone negative for the equity outlook. In US yesterday, Dow +0.6%, S&P 500 +1.1%, Nasdaq +1.5% and Russell 2000 -0.02%. Asian markets are mixed this morning with Japan lower and China higher. US and European futures are mostly positive.

FI: Global rates zig zagged as the immediate reaction to the US inflation release yesterday, but the market interpretation ended up being clearly to the hawkish side. The US treasury curve bear flattened as markets shaved off expectations for US rate cuts in 2024. 10Y UST yields were up 6bp, while the US breakeven inflation curve rose from the front. 10Y Bund yields rose 3bp with the Bund ASW-spread continuing to drift lower, ending the day in 30.1. The tightening of spreads was also evident in the 10Y BTP-Bund, which dropped to 127bp yesterday - the lowest since end-2021.

FX: The US CPI pushed yields higher, which in turn supported the greenback. NOK and JPY struggled vs the USD, and EUR/GBP ended the day higher amid a weak UK labour market report. NOK/SEK traded heavy and hit the lowest levels since December.

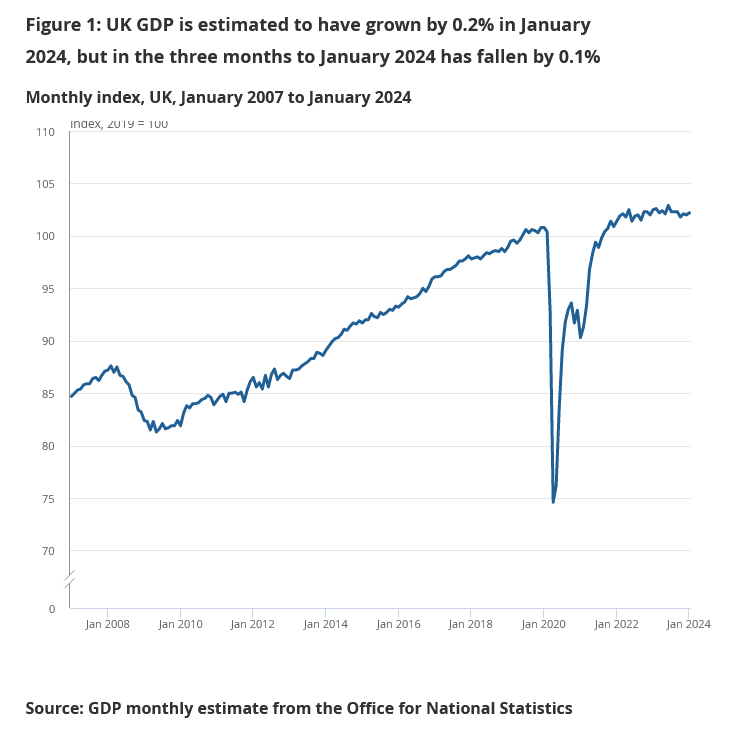

UK GDP grows 0.2% mom in Jan, matches expectations

UK GDP expanded by 0.2% mom in January, matched expectations. Services was up 0.2% mom, and was the largest contributor to growth. Production fell -0.2% mom while construction grew 1.1% mom.

In the three months to January, GDP has fallen by -0.1% 3mo3m. Services was flat. Production fell -0.2% 3mo3m. Construction fell -0.9% 3mo3m.

CHF/JPY Technical: Potential Major Bullish Trend Exhaustion

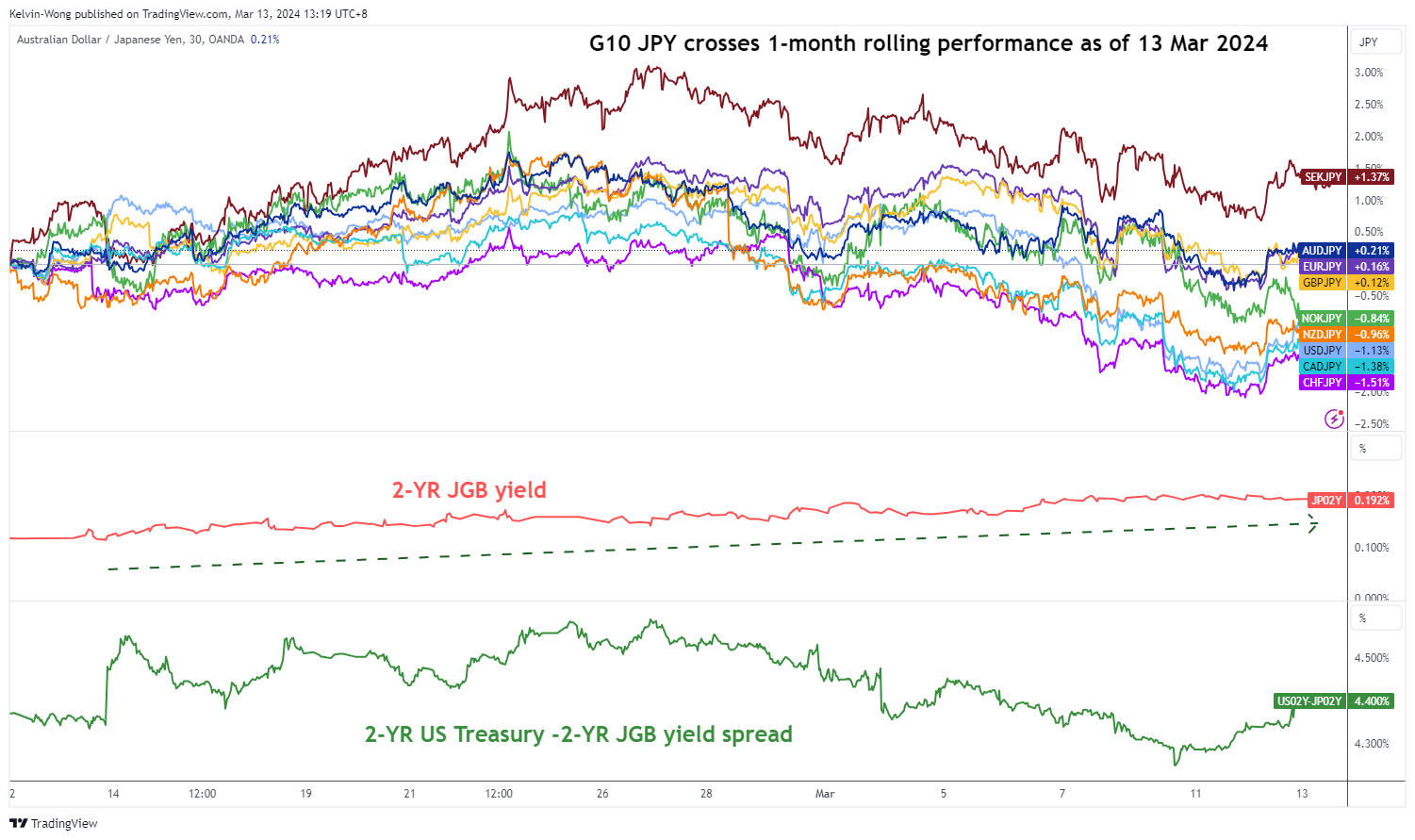

- The recent significant increase of a total of 20 bps in the 2-year JGB yield since the start of the year has come in line with the highly anticipated rosy results of the annual wage negotiations in Japan.

- In the past week, the JPY crosses have come under downside pressure as the carry trade strategy loses its appeal.

- Watch the 168.75 key short-term resistance on the CHF/JPY.

The JPY crosses have continued to face downside pressure in the recent week ahead of key related risk events such as the release of the preliminary FY 2024/2025 wage negotiation results in Japan by the latest labour union federation, Rengo on this Friday, 15 March (see Fig1).

Expectations have been optimistic as the consensus forecast is pegged at an average pay rise of 3.85% for FY 2024/2025 (above last year’s annualized gain of 3.58%), and if It turns out as expected, it will be the largest wage increase in Japan since 1993.

JPY crosses under downside pressure as carry trade strategy loses appeal

Fig 1: 1-month rolling performances of G-10 JPY crosses as of 13 Mar 2024 (Source: TradingView, click to enlarge chart)

The CHF/JPY is the worst performer among the JPY crosses as it shed -1.50% based on a one-month rolling performance basis as of today, 13 March in line with the rosy anticipated outcome of the Japanese employee’s wage negotiation results.

The primary driver of JPY strength has been the rising 2-year Japanese Government Bond (JGB) yield as it rose by a whopping 20 basis points (bps) from close to 0% at the start of January to 0.20% on 11 March as market participants have started to price in a more hawkish Bank of Japan (BoJ) going forward to either scrapped off its short-term negative interest rates policy next Tuesday, 19 March or on the 26 April monetary policy meeting.

Bearish “Ascending Wedge” detected in CHF/JPY

Fig 2: CHF/JPY major & medium-term trends as of 13 Mar 2024 (Source: TradingView, click to enlarge chart)

The major uptrend phase of CHF/JPY in place since the 13 January 2024 low of 137.44 is likely in jeopardy through the recent appearance of an impending bearish “Ascending Wedge” configuration that has taken shape from the 3 October 2023 low (see Fig 2).

The formation of the “Ascending Wedge” suggests a potential major bullish trend exhaustion condition as the magnitude of its upper boundary that connects its “higher highs” is lesser than the slope of its “lower lows” (lower boundary).

In addition, the daily RSI momentum indicator has flashed a bearish divergence condition.

Oscillating within a minor descending channel

Fig 3: CHF/JPY short-term trend as of 13 Mar 2024 (Source: TradingView, click to enlarge chart)

In the shorter term as seen on its hourly chart, the price actions of CHF/JPY have started to oscillate within a minor descending channel in place since 29 February 2024 high of 171.50.

If the 168.75 short-term pivotal resistance is not surpassed to the upside, it may see further potential weakness to expose the next intermediate support at 166.55 (close to the lower boundary of the “Ascending Wedge) in the first step (see Fig 3).

On the other hand, a clearance above 168.75 negates the bearish tone for the next near-term resistance to come in at 169.50 (also the downward-sloping 20-day moving average).

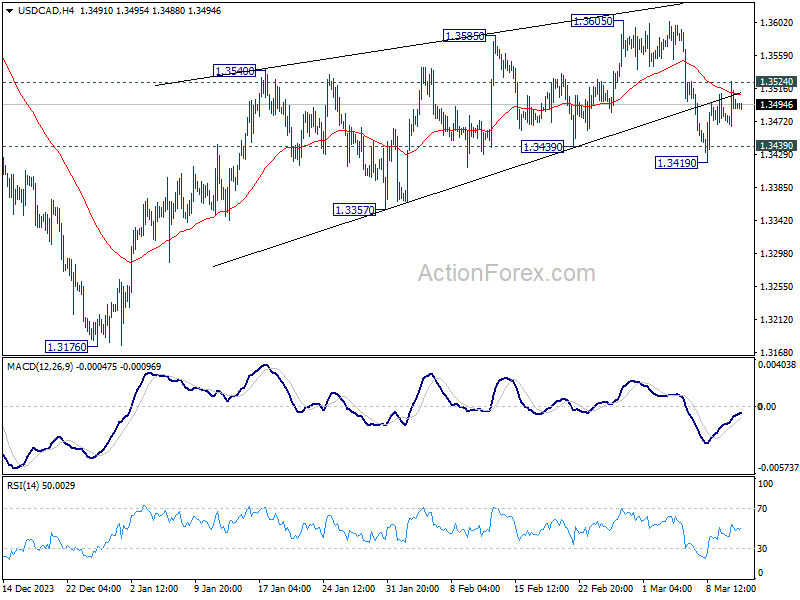

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3463; (P) 1.3495; (R1) 1.3522; More...

Intraday bias in USD/CAD remains neutral for the moment. On the downside, break of 1.3419 and sustained trading below 1.3439 support will argue that rebound from 1.3176 has completed as a corrective move to 1.3605. Near term outlook will be turned bearish for 1.3357 support first. On the upside, though, break of 1.3524 minor resistance will revive near term bullishness, and turn bias back to the upside for retesting 1.3605 resistance instead.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern only. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Overall, larger up trend from 1.2005 (2021 low) is still expected to resume through 1.3976 at a later stage.