Sample Category Title

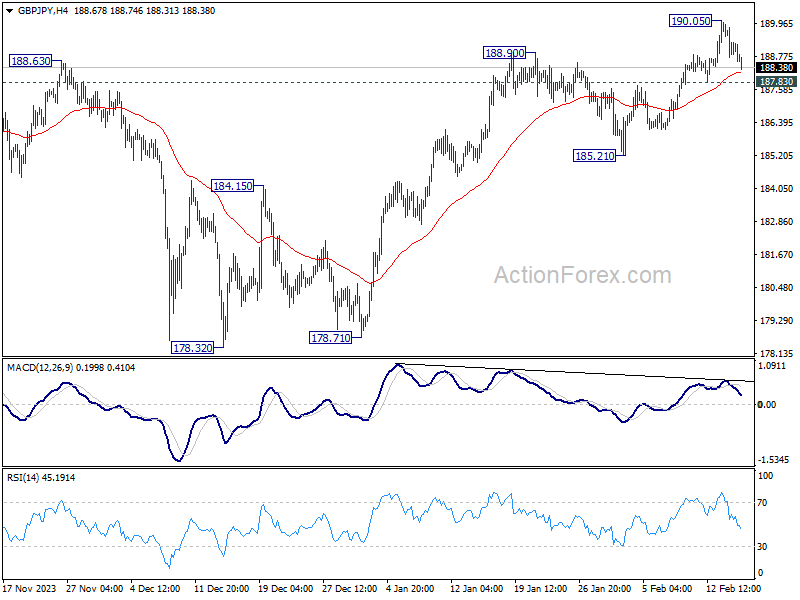

GBP/JPY Daily Outlook

Daily Pivots: (S1) 188.70; (P) 189.31; (R1) 189.87; More...

Intraday bias in GBP/JPY remains neutral at this point, for consolidations below 190.05. Break 190.05 will resume larger up trend. However, break of 187.83 will turn bias to the downside for deeper correction back to 185.21 support instead.

In the bigger picture, up trend from 123.94 (2020 low) in in progress. Medium term outlook will stay bullish as long as 178.32 support holds. Next target is 195.86 long term resistance (2015 high).

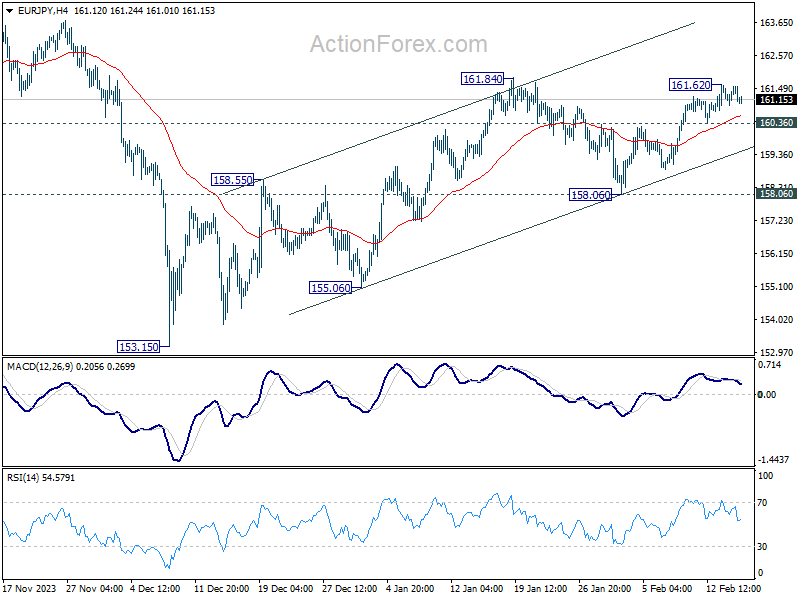

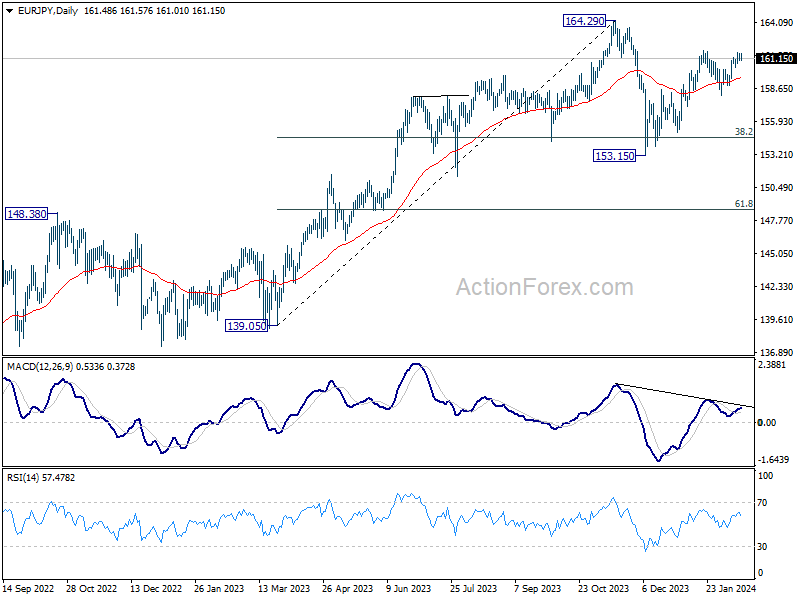

EUR/JPY Daily Outlook

Daily Pivots: (S1) 161.14; (P) 161.37; (R1) 161.77; More...

Intraday bias in EUR/JPY is turned neutral first as it retreated ahead of 161.84 resistance On the upside, firm break of 161.84 will confirm resumption of whole rise from 153.15. Next target is a retest on 164.29 high. On the downside, however, below 160.36 will extend the pattern from 161.84 with another falling leg, and turn bias to the downside for 158.06 support instead.

In the bigger picture, price actions from 164.29 medium term top are seen as a correction to rise from 139.05 only. As long as 148.38 resistance turned support holds (2022 high), larger up trend from 114.42 (2020 low) is expected to resume through 164.29 at a later stage. Next target would be 169.96 (2008 high).

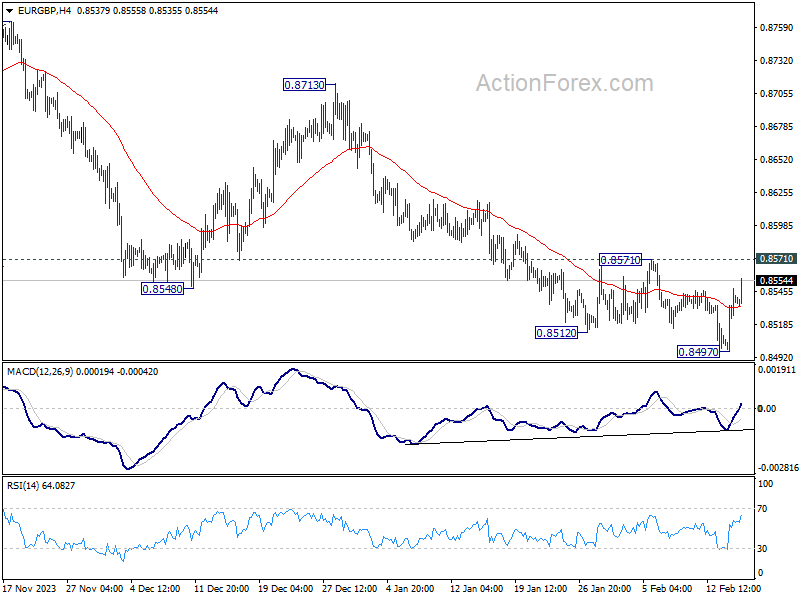

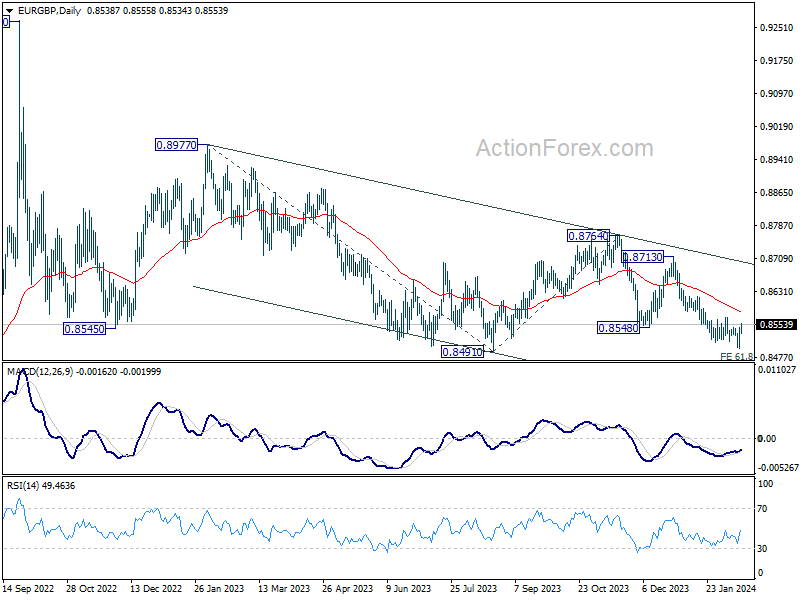

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8507; (P) 0.8528; (R1) 0.8558; More...

Intraday bias in EUR/GBP as it's capped below 0.8571 resistance despite extended recovery. On the downside, break of 0.8497 will resume extend recent fall to 0.8464 projection level. Nevertheless, considering bullish convergence condition in 4H MACD, sustained break of 0.8571 will confirm short term bottoming, and turn bias back to the upside for stronger rebound.

In the bigger picture, fall from 0.8764 is seen as another leg in the whole down trend from 0.9267 (2022 high). Outlook will stay bearish as long as 0.8713 resistance holds. Break of 0.8491 will target 61.8% projection of 0.8977 to 0.8491 from 0.8764 at 0.8464.

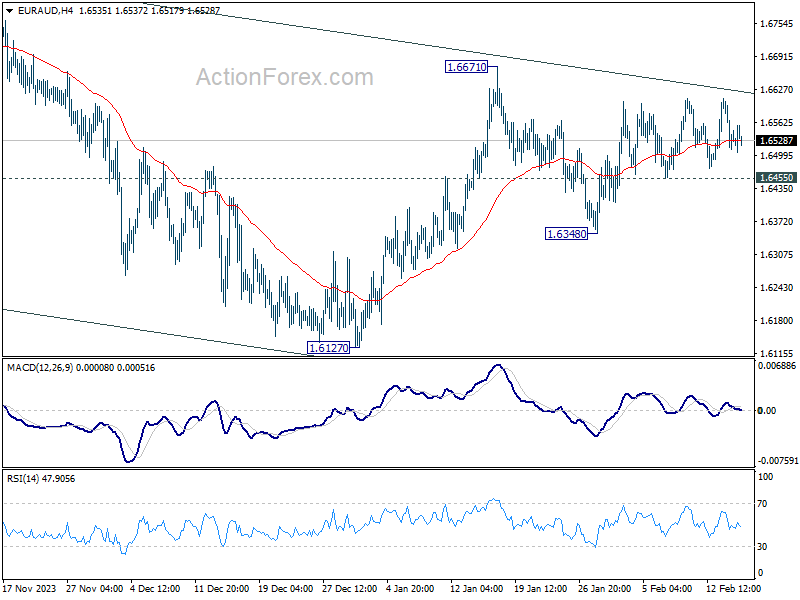

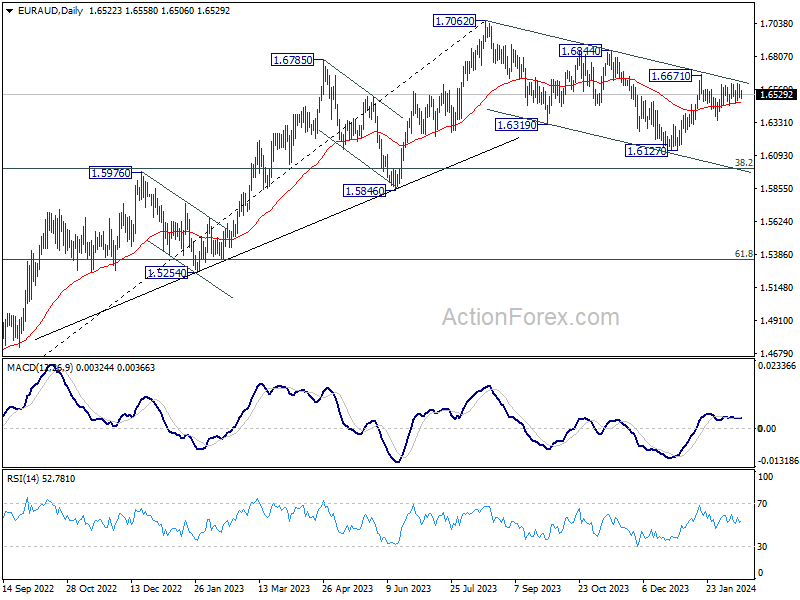

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6490; (P) 1.6549; (R1) 1.6584; More...

EUR/AUD is still bounded in sideway trading and intraday bias remains neutral. On the upside, decisive break of 1.6671 will revive the case that whole correction from 1.7062 has completed with three waves down to 1.6127. Further rally should then be seen to 1.6844 resistance for confirmation. Nevertheless, below 1.6455 minor support will turn bias to the downside for 1.6348 and possibly below.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low). Break of 1.6844 resistance will argue that this up trend is ready to resume through 1.7062 high. In case of another fall, strong support should be seen around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound.

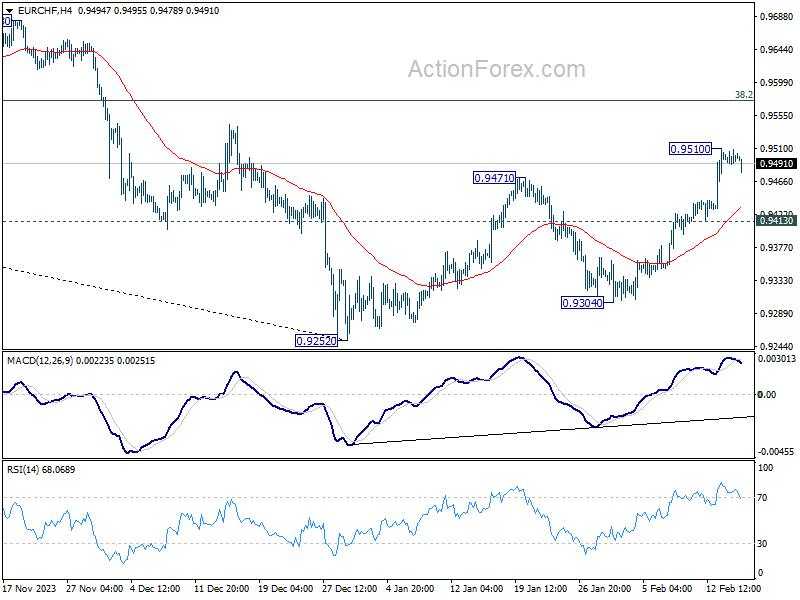

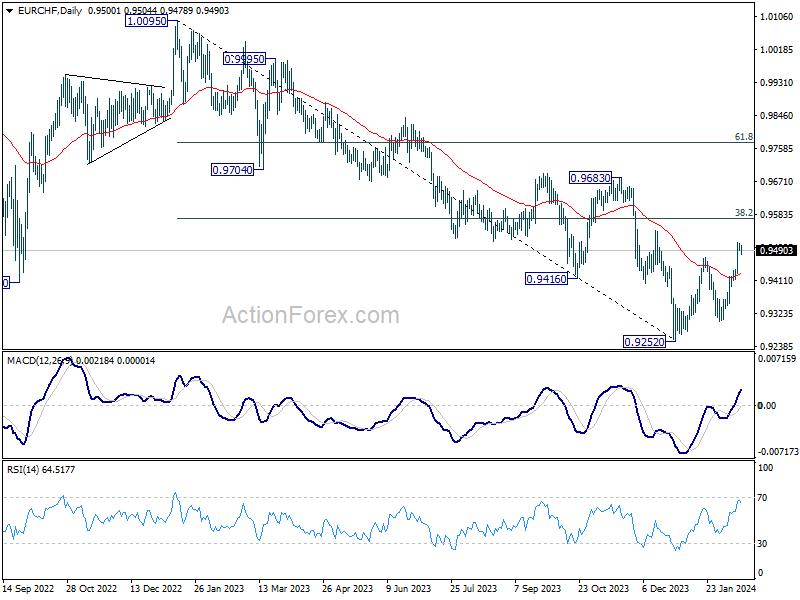

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9490; (P) 0.9500; (R1) 0.9513; More...

Intraday bias in EUR/CHF is turned neutral first with current retreat, and some consolidations could be seen first. But downside should be contained by 0.9413 minor support to bring another rally. On the upside, break of 0.9510 will resume the rebound from 0.9252 and target 0.9574 fibonacci level and above.

In the bigger picture, price actions from 0.9252 are tentatively seen as a correction to the five-wave down trend from 1.0095 (2023 high). Further rise would be seen to 38.2% retracement of 1.0095 to 0.9252 at 0.9574. But overall medium term outlook will remain bearish as long as 0.9683 resistance holds.

Japanese GDP Unexpectedly Contracted in Q4

Markets

Broader markets recovered from the big post-CPI swings yesterday in absence of new drivers. US Treasuries rebounded, but technical breaks through resistance levels (in yield terms) weren’t undone. US yields eventually returned 8.5 bps (3-yr) to 2.8 bps (30-yr). Dovish Chicago Fed governor Goolsbee downplayed the upshot in monthly inflation dynamics, saying that inflation can be a bit higher while still being on track to 2%. He doesn’t support waiting until the 2% inflation goal before cutting policy rates, labelling monetary policy currently as being quite restrictive. Finally, he emphasized that the Fed’s inflation goal in based on PCE deflators and not on this week’s published CPI inflation. The January stickiness of (CPI) inflation was partly because of shelter which has a far bigger weight in CPI calculations compared to the way PCE deflators are constructed. January PCE data will only be released on February 29. Washington-based Fed governor Barr (vice-chair for supervision) after (US) market close backed the official Fed guidance that more good data are needed before begin the process of reducing policy rate. A careful approach is needed given the limited historical experience with current growth and inflation dynamics. He welcomed goods price deflation which helped pull inflation off peak levels, but suggests that that trend has played out. He hopes on ebbing housing inflation and moderating wage growth to help pull services inflation down. ECB vice-governor de Guindos and Bundesbank Nagel held their respective neutral and hawkish views. Central bank focus will today shift to ECB President Lagarde’s hearing before the Committee on Economic and Monetary Affairs of the European Parliament. US eco data are plenty including retail sales, the empire manufacturing survey, Philly Fed business outlook, weekly jobless claims, export/import prices and industrial production. We expect data on balance to put US Treasuries back under selling pressure.

European and US stock markets recovered as well yesterday, gaining 0.5% to 1%. EUR/USD set a new YTD low at 1.0695 before rebounding towards 1.0730. EUR/GBP went on a two-day rollercoaster ride, testing 0.85 on strong labour market data on Tuesday, but swinging back to 0.8550 yesterday on slightly better inflation figures. Disappointing Q4 GDP data this morning suggest that yesterday’s market direction will be the dominant one today as well. GDP declined by 0.3% Q/Q (technical recession) with investments (+1.4% Q/Q) failing to make up for declining consumption (-0.1% Q/Q) and (net) exports. On top, Q3 GDP data faced downward revisions.

News & Views

Australian employment barely grew in January. Only 0.5k jobs were added, a fraction of the 25k rebound that was expected following a sharp drop in December (-62.7k). A slightly bigger rise in full time employment compensated for a drop in part-timers. The unemployment rate rose from 3.9% to 4.1%, topping the 4% mark for the first time since January 2022. Head of Australia’s labour statistics bureau Jarvis nuanced however, by saying that this “coincided with a higher-than-usual number of people who were not employed but who said they will be starting or returning to work in the future.” The participation rate remained steady at 66.8%, below the 67.3% record high of November last year but well above pre-pandemic levels. Monthly hours worked fell by 2.5%, which Jarvis attributed to changing market dynamics around the summer holiday period (more people taking annual leave). The Australian dollar lost some ground in the wake of the underwhelming report. AUD/USD after touching the 0.65 big figure returned to 0.648 currently. Australian swap yields ease between 6.7 and 7.9 bps across the curve. A first rate cut is for 96% priced in at the June meeting. This compared to over 60% just yesterday.

Japanese GDP unexpectedly contracted in Q4 of last year. Shrinking 0.1% q/q after a -0.8% contraction in Q3 puts the island in a technical recession. Net exports’ contribution was insufficient to make up for weak business spending and private consumption. Waning demand complicates the picture for the Bank of Japan which is looking to exit its ultra-easy monetary policy. While today’s data doesn’t derail those plans per se, it does suggest the window of opportunity may be closing. The Japanese yen advances this morning but that has more to do with intervention speculation after USD/JPY topped the 150 barrier two days ago. The pair is still hovering north of that level as of this morning.

UK slides into technical recession with -0.3% qoq GDP contraction in Q4

UK GDP contracted -0.3% qoq in Q4, worse than expectation of -0.1% qoq. This downturn was a collective result of declines across all primary sectors: services saw a -0.2% dip qoq, production tumbled by -1.0% qoq, and construction experienced a significant -1.3% qoq fall. Following -0.1% qoq contraction in Q3, these figures confirm UK's entry into a technical recession.

December's GDP data offered a slight respite with a marginal -0.1% mom decrease, better than expectation of -0.2% mom. That followed 0.2% mom growth in November, and -0.5% mom contraction in October. Services fell -0.2% mom. Production grew 0.6% mom. Construction fell -0.5% mom.

Reflecting on the entire year of 2023, UK's GDP saw a meager 0.1% growth, a stark contrast to 4.3% expansion in 2022. This marks the weakest annual performance since the 2009 financial crisis, with the exception of the pandemic-stricken year of 2020.

Full UK monthly GDP release and quarterly GDP release.

USD/JPY: Lingering Below 151.40/95 Major Resistance Zone

- JPY weakness failed to materialize after Japan’s Q4 GDP came in way below expectations.

- Fear of looming BoJ’s intervention to put a halt to recent JPY weakness after MoF’s vice finance minister Masato Kanda’s warnings yesterday on the recent rapid moves in the FX markets ex-post hotter than expected US CPI data release.

- Short-term upside momentum of US dollar strength against JPY has started to ease.

Flash Q4 2023 GDP data for Japan has indicated that the Japanese economy slipped into a technical recession as it shrank – 0.1% q/q (-0.4% y/y) in the October to December period over a downward revised -08% q/q (-3.3% y/y) for Q3 2023 that shocked market participants as the consensus was in favour of +0.3% q/q (+1.4% y/y) recovery in Q4.

Interestingly, in the past where most of the time a deterioration in key Japanese economic data tended to inflict a significant intraday sell-off in the JPY as market participants inferred that the Bank of Japan (BoJ) was likely to maintain its decades-long of ultra dovish monetary policy and even evoke unconventional quantitative easing to spur demand growth which in turn resulted in a persistent weak JPY.

JPY did not sell off in light of Japan entering into a technical recession

This time around the JPY does the reverse, it has strengthened by +0.30% on an intraday basis against the US dollar at this time of the writing, and the 10-year Japanese Government Bond (JGB) remained steady at 0.72%, a similar level seen three weeks ago.

Two possible drivers can be explained by such abnormality in the current movement of the JPY.

A weak JPY is likely the indirect main driver of weak domestic consumption

Firstly, private domestic consumption which accounts for more than 50% of the Japanese economy has declined for the third successive quarter amid elevated cost pressures (-0.2% q/q in Q4 23 vs. -0.3% q/q in Q3 23), below the consensus estimate of 0%.

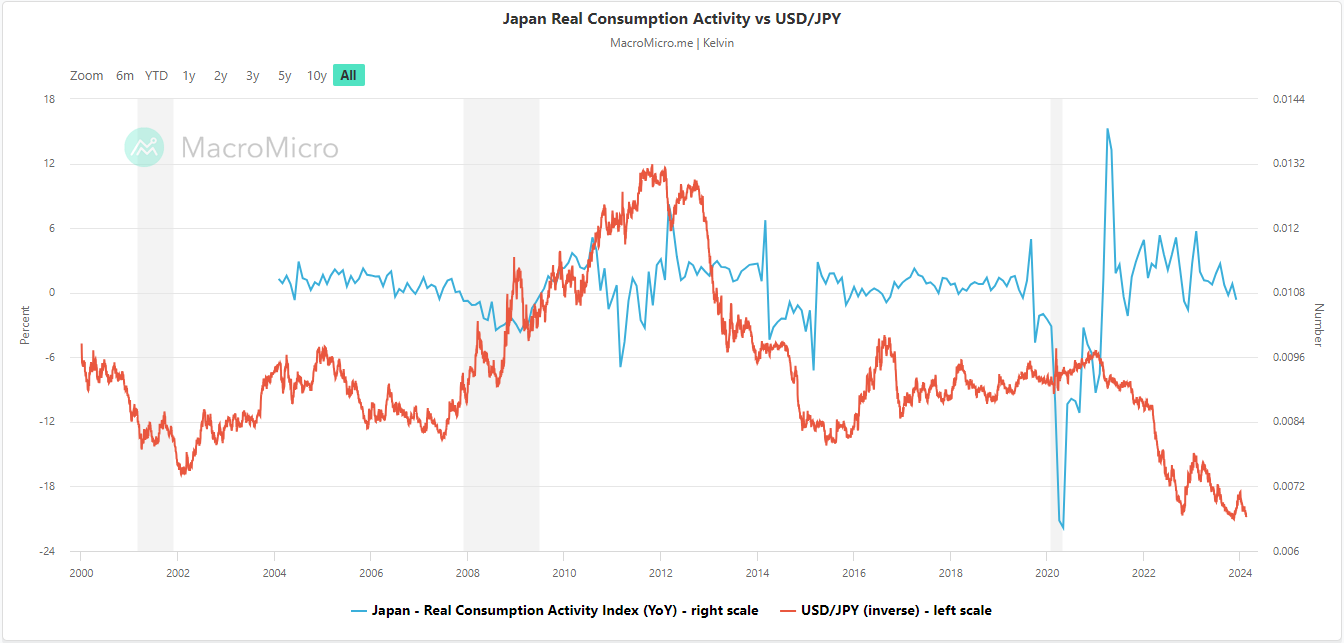

The indirect causation is the persistent weak JPY trend seen in the past two years that could not offset elevated external cost-push-driven global inflationary pressures that eroded consumers’ purchasing power and dampened demand.

This direct correlation can be depicted in the chart (Fig 1) where the monthly Japan Real Consumption Activity Index peaked at +15.27 y/y in April 2021 and declined to -0.66% y/y most recently in December 2023.

Fig 1: Japan Real Consumption Activity Index vs. USD/JPY (inverse) as of 15 Feb 2024 (Source: MacroMicro , click to enlarge chart)

This trend of real consumption deflation has moved in synch with a weakening JPY by taking the inverse of USD/JPY over the same period.

Hence, a weak JPY is unlikely to be able to spur economic growth at this juncture for Japan which in turn may not yield any marginal benefits for BoJ to keep maintaining its ultra-accommodative monetary policy stance.

Risk of looming FX intervention

Considering the hotter-than-expected US CPI inflation data that shocked the markets on Tuesday, 13 February, the US dollar spiked up across the board, and it strengthened by almost 1% against the JPY.

It has immediately prompted Japan’s top official in charge of foreign exchange matters, Ministry of Finance vice-minister Masato Kanda to issue a remark that he believed that some of the recent movements in the USD/JPY are speculative in nature and undesirable.

He added that authorities are on call 24 hours a day, 365 days a year, and are always ready to take appropriate steps as needed. Given such “stern” verbal intervention, we cannot rule out that actual intervention may take place soon if USD/JPY continues to march northwards rapidly.

Short-term upside momentum is losing inertia for USD/JPY

Fig 2: USD/JPY medium-term trend as of 15 Feb 2024 (Source: TradingView, click to enlarge chart)

Fig 3: USD/JPY short-term trend as of 15 Feb 2024 (Source: TradingView, click to enlarge chart)

The recent bullish momentum seen in the USD/JPY since the start of this week, 12 February has started to lose inertia.

The hourly RSI momentum indicator has staged a momentum bearish breakdown after it hit an extreme overbought condition on Wednesday, 14 February (ex-post US CPI).

These bearish observations have taken form right below the risk and major resistance zone of 151.40/151.95.

A break below the lower neutrality range level of 149.60 may see further near-term weakness to expose the next intermediate support zone of 148.80/40 (also the 20-day moving average).

On the flip side, a clearance above 150.70 (upper neutrality range) may see the major resistance zone coming in at 151.40/95.

All’s Well That Ends Well

The market has been very quick in swallowing and digesting this Tuesday’s less than ideal inflation data from the US – which showed that inflation in the US didn’t ease as much as expected in January, remember that data? It was just two days ago, it was supposed to be important, and potentially trend changing. Interestingly, the kneejerk market reaction remained short lived. The fact that inflation in other places, like in the UK, didn’t pick up certainly helped cementing the idea that, this is certainly just a blip in the disinflation trend, and if it’s not, the Chicago Federal Reserve’s (Fed) Goolsbee said that slightly higher inflation data for a few months will still be consistent with a further easing toward the Fed’s 2% target. Staff at the European Central Bank (ECB) sounded more poetic, posting the world’s cheesiest central bank message ‘roses are red, violets are blue, we’re nearing our target, and we will reach too’. So, it’s in this atmosphere of love and hope that investors got their thoughts together and put on their dip-buyer heads, went out there and chased good deals – if you can call them good at the current levels.

And know that even The Big Short’s Michael Burry – who is famous for shorting stocks and who was short the chip stocks last year, short the S&P500 and short the Nasdaq – has no more short positions in his portfolio according to the latest 13F filings. The most famous short trader of the history threw in the towel. He is now long health and tech stocks.

The S&P500 rebounded almost 1%, technology stocks led rally. Uber, for example, jumped nearly 15% after announcing its first-ever buyback of $7bn to celebrate its first-ever annual net profit since it became public. Its Asian competitor Lyft jumped more than 60% but that was a mistake – the company was confused between 50 and 500bp. It’s more than just one zero on a press release.

Now, back to serious stuff, the US 2 and 10-yer yields retraced the post-CPI jump on market’s ignorance of the inflation risks that should delay the first rate cut from the Fed. The US dollar gave back field. But note that, despite the bulls keeping their faces on, the expectation of Fed rate cuts is not what it used to be at the start of the year. Investors will focus on retail sales, and some manufacturing indices today to continue guessing when the Fed will move. Stronger retail sales should weaken the Fed doves, while soft manufacturing should support them. The market pricing suggests 3 fully priced rate cuts, and a fourth cut priced at around 70%. That’s less than the 4 rate cuts priced for the ECB.

As such, the euro’s depreciation against the US dollar remains well supported by fundamentals. There is one thing, though. The dovish ECB expectations are fueled by soft growth and falling inflation in the euro area. But a broadly stronger US dollar is inflationary for the rest of the world because everything from commodities to oil are negotiated in USD terms. Therefore, the hawkish shift from the Fed and a stronger US dollar could lead to an undesired U-turn in European inflation, soften the ECB doves’ hand and throw a floor under the EURUSD selloff.

Happily, energy prices are not yet threatening enough. In this context, the barrel of US crude fell sharply, after trading above the 200-DMA, as the latest EIA data printed an 8.5-mio barrel increase in oil inventories last week. Nat gas futures continue to dive as well, driven by soft demand due to record high production, ample supplies, and mild winter both in Europe and the US.

Elsewhere, data released this morning in Japan showed that the country unexpectedly entered recession in Q4. The economy shrank 0.1%, while analysts were expecting a 0.3% expansion. The private consumption declined for the 3rd straight quarter. If the latter didn’t trigger a fresh selloff in the Japanese yen due to the heavy threat of direct intervention.

All Eyes on US Retail Sales

In focus today

In the US, January retail sales and industrial production data is due for release. Consensus expects some moderation in retail sales growth, even though early credit card data suggests that consumption has remained brisk at the start of the year as well. The NAHB housing market index and initial claims data will also be released today.

In the euro area, the European Commission releases its economic forecasts, including GDP and inflation estimates. As the Commission and the ECB use similar models, the projections could give hints of what to expect from the ECB's staff projections at the March meeting. Additionally, ECB President Lagarde will make public remarks today.

An empty Swedish Macro calendar awaits today. However, two Riksbank speakers Erik Thedéen and Anna Breman are set to speak on two different events. Thedéen will kick things off as his event starts 08.30 CET, followed by Breman at 16.20 CET. Both speeches are themed as "The economic situation and current monetary policy".

Economic and market news

What happened overnight?

In Japan, national accounts for Q4 unexpectedly came in at -0.1% after -0.7% in Q3. The decline stems primarily from weak consumption and capital expenditure. With two consecutive GDP contractions, Japan is now in a technical recession, while Germany has surpassed Japan to become the world's third-largest economy. The print complicates the monetary policy outlook for Bank of Japan, although the policy outlook much depends on the spring wage negotiations.

What happened yesterday?

In Norway, mainland-GDP printed 0.2% q/q in Q4 (Danske: 0.2%, cons: 0.1%). While the print signals some recovery in Q4, we find the details weaker as strong growth in private consumption was partly due to higher electricity consumption. Additionally, mainland exports contributed to the upside, whereas investments acted as a solid drag. Growth seems a bit stronger than Norges Bank (NB) expected in the December MPR (0.0%), but we still believe that capacity utilisation is moving downwards and will allow Norges Bank to cut rates once other central banks start cutting.

In the UK, inflation came in lower than expected in January at 4.0% y/y (cons: 4.1%) and core at 5.1% (cons: 5.2%). Looking at the seasonally adjusted monthly developments CPI was 0.24% m/m and core inflation was just 0.16% m/m s.a. Importantly, service inflation was just 0.03% m/m s.a., which is highlighted as an important component by the BoE.

In the euro area, industrial production surprised to the upside in December, printing 2.6% m/m compared to consensus of -0.2% m/m. However, the uptick is attributed to a large increase in capital goods of 20.5% m/m, driven by a large patent in Ireland (Irish industrial production rose 44.5% y/y). Non-durable goods production saw only a muted increase of 0.2% m/m. The total euro area Q4 industrial production figure was 0.0% q/q in line with GDP. Hence, the industry ended the year on a weak footing but still better than in Q3 in a sign that the worst of the manufacturing slump is behind us.

Equities: Global equities were higher yesterday as inflation and central bank fear abated. Most visible in the small caps with Russell 2000 rising 2.4% after the massive sell-off following CPI data Tuesday. Add to that most indices ended close to day-high and futures are higher again. Hence, our conclusion yesterday that CPI should not lead to a change in the current dominating narrative seems to also be the conclusion global investors reached yesterday. In US Dow +0.4%, S&P 500 +0.96%, Nasdaq +1.3% and Russell 2000 +2.4%. Asian markets mostly higher this morning led by Japan as dollar-yen crosses 150. European futures are up almost half a percent today while US futures are in marginal gains.

FI: European yields declined after the lower-than-expected UK inflation data, and the 10Y German government bonds did not cross the 2.4% level. There was also a rebound in the US Treasury market with a decent decline in bond yields across the curve.

FX: Yesterday's price action was characterised as a (part) reversal of the post US CPI price action from Tuesday: cyclically sensitive currencies gained while the USD was among the underperformers. Alongside the SEK the NOK was the biggest outperformer with the Norwegian currency showing remarkable resilience amid Brent Crude falling 2 USD/bbl. Despite the rise in equities the GBP traded on the weak side while USD/JPY remains north of the psychologically important 150-level despite verbal intervention from the Japanese authorities.