Sample Category Title

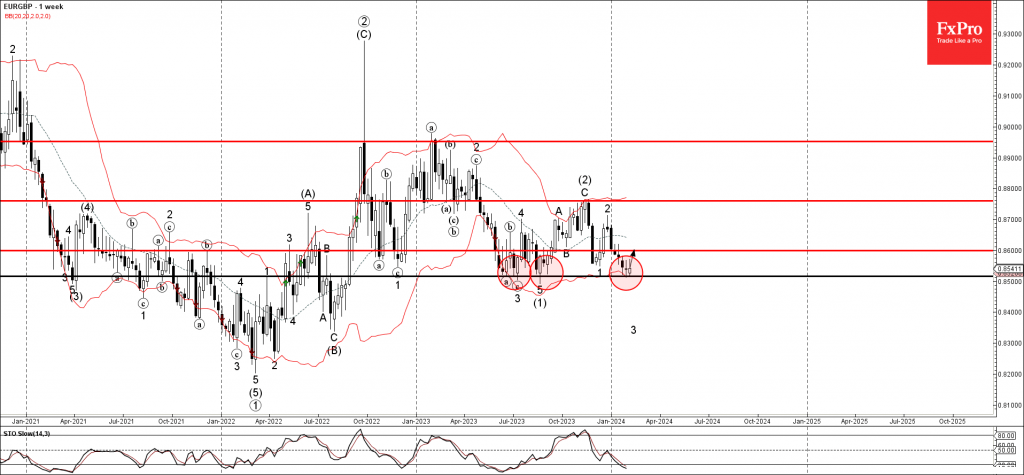

EURGBP Wave Analysis

- EURGBP reversed from support level 0.8515

- Likely to rise to resistance level 0.8600

EURGBP currency pair recently reversed up from the support level 0.8515, which has been reversing the price from the middle of 2023.

The support level 0.8515 was strengthened by the lower weekly Bollinger Band and by the lower daily Bollinger Band.

Given the oversold weekly Stochastic and the strength of the nearby support level 0.8515, EURGBP currency pair can be expected to rise further to the next resistance level 0.8600.

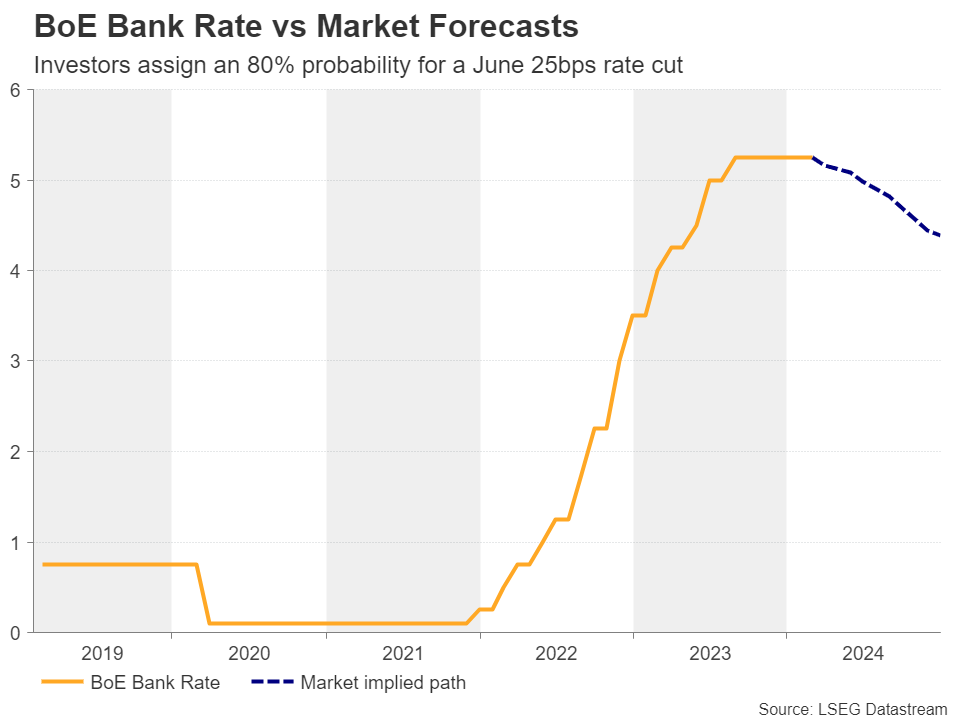

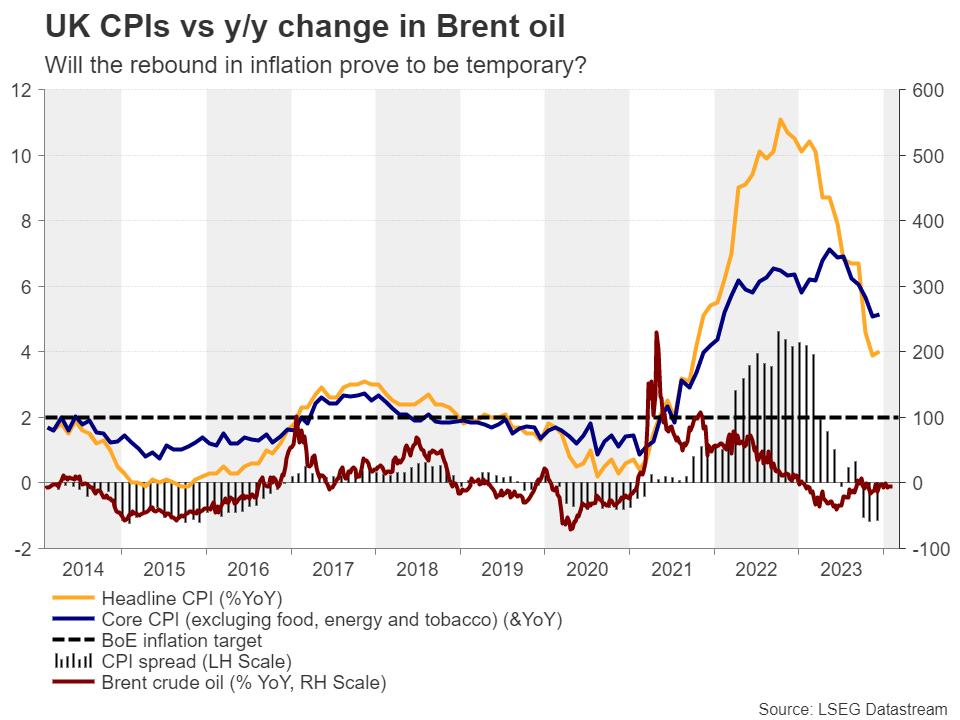

Pound Traders Lock Gaze on UK Inflation and GDP Data

- Investors price in rate cuts despite BoE’s ‘higher for longer’ mantra

- Will the UK CPI and GDP data confirm that view?

- CPI inflation on Wednesday (07:00 GMT), GDP on Thursday (07:00 GMT)

Traders assign an 80% chance of a June BoE rate cut

When they last met, Bank of England (BoE) policymakers decided to keep interest rates unchanged at 5.25%. However, the decision was not unanimous. Two members voted for raising interest rates by another 25bps and one favored a same-sized rate cut.

Although officials removed from the statement the part saying that further tightening may be required if inflationary pressures persist, at the press conference following the decision, Governor Bailey pushed back against rate cut expectations, saying that they are not yet at a point where they can lower borrowing costs, adding that policy needs to stay sufficiently restrictive for sufficiently long.

That said, remarks by chief economist Huw Pill this week had a somewhat more dovish flavor, with the senior BoE official noting that key gauges of price pressures were not yet at a level that would permit easing policy, but also that there is no need for inflation to hit 2% before they begin to do so. “Lowering interest rates is a reward to the economy for better inflation performance,” he also said, allowing market participants to continue penciling in a high 80% chance for a first quarter-point reduction in June.

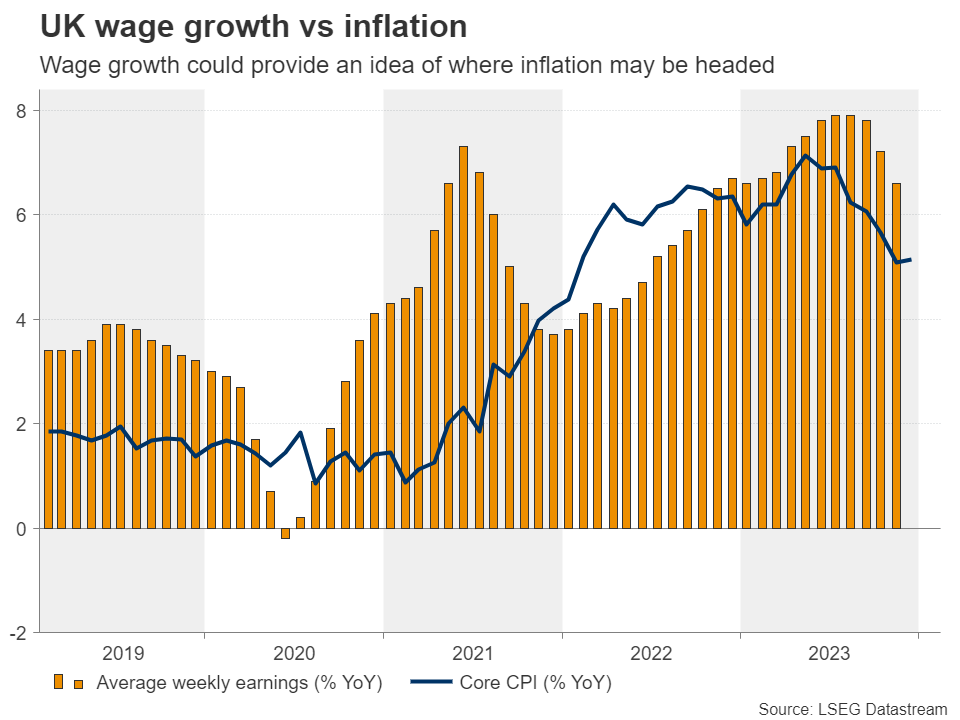

Inflation could further slow, recession may have been avoided

With all that in mind, pound traders will stay locked in front of their screens next week, as the calendar is packed with UK economic releases. On Tuesday, the jobs report for December is due to be released, with the focus likely to fall on average weekly earnings as investors try to figure out where inflation may be headed next.

Yet, the centerpiece may be Wednesday’s CPI numbers for January. According to the UK PMIs for the month, although rising ocean freight rates resulted in cost burdens across the manufacturing sector and despite service providers signaling another steep rise in input prices, overall, prices charged by private sector firms increased at the weakest pace since last October. This likely shifts the risks surrounding the CPI numbers to the downside.

Though, with the y/y change in oil prices remaining close to zero, the gap between the headline and core inflation rates may continue to narrow, which means that the headline rate may not decline as much as the core one.

Be that as it may, slowing inflation may corroborate the market’s view that the BoE will start lowering borrowing costs in the summer, but the expectations about the pace of subsequent reductions may also depend on growth related data. On Thursday, the preliminary GDP data for Q4 and the month of December are due to be released, alongside the industrial and manufacturing production stats for the same month.

The downside revision of the Q3 GDP print revealed that the economy shrank 0.1%, and the 0.3% monthly contraction for October sparked recession fears, but those fears receded after the November monthly rate clocked at at 0.3%. Ergo, Thursday’s data may attract extra attention as it may confirm whether the UK economy has dodged a bullet.

According to the NIESR GDP estimate, the UK economy flatlined in the last three months of 2023, and should this be the case, the release may be cheered by pound traders. However, it is unlikely to tempt them to raise their BoE implied rate path. Any GDP related gains may remain limited and short-lived, especially if inflation further slows the day before. For the pound to end up gaining and sustaining those gains, an upside surprise may be needed. Retail sales are also due to be released on Friday.

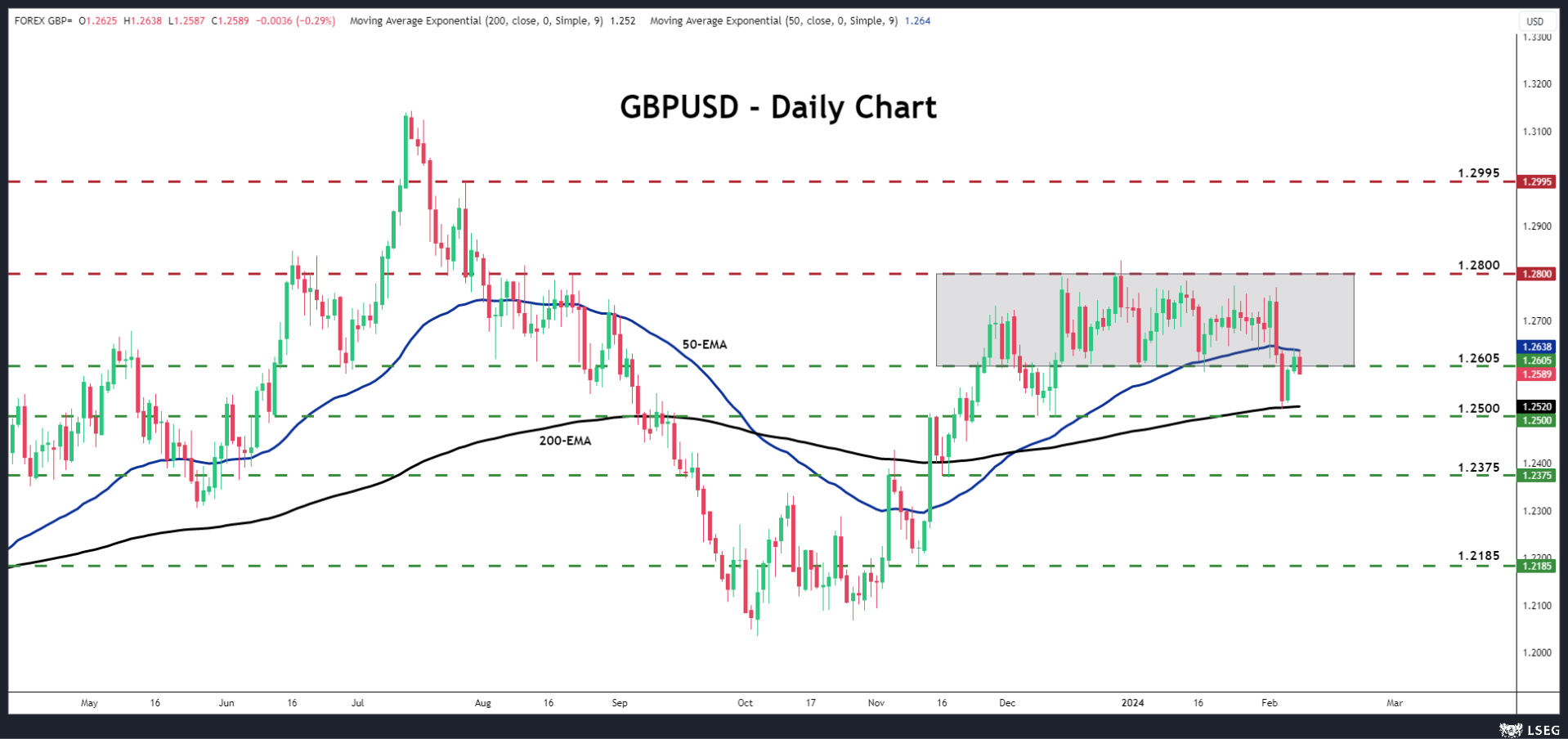

Pound/dollar could turn south again

From a technical standpoint, on February 5, pound/dollar fell below the lower end of the sideways range that was in place since December 14. However, just the following day, it rebounded after hitting support slightly above the 1.2500 zone and the 200-day exponential moving average (EMA). The recovery allowed the pair to test the 50-day EMA before turning south again.

A slowdown in UK inflation on Tuesday could result in more selling, with the bears aiming for another test near the psychological barrier of 1.2500. However, growth data confirming the no-recession case may be a reason for a pause around there. For the outlook to be considered bullish, the pair may need to climb all the way above the upper bound of the range at around 1.2800.

A slowdown in UK inflation on Tuesday could result in more selling, with the bears aiming for another test near the psychological barrier of 1.2500. However, growth data confirming the no-recession case may be a reason for a pause around there. For the outlook to be considered bullish, the pair may need to climb all the way above the upper bound of the range at around 1.2800.

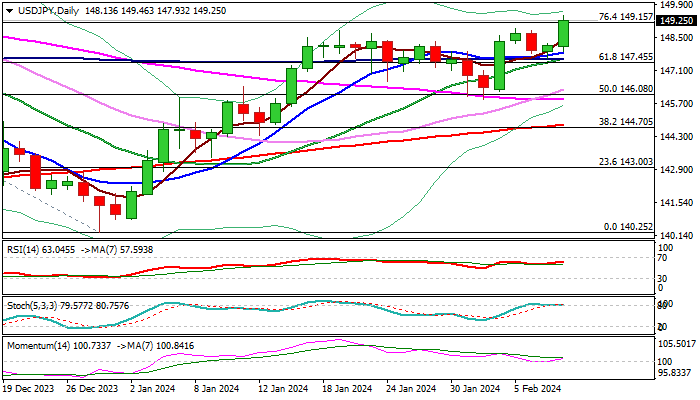

USD/JPY: Rallies on Diverging BoJ/Fed Rate Outlook

USDJPY rallied on Thursday (up 0.80% until early hours of the US session) as BoJ kept dovish stance in rate talks which deflated yen, while dollar appreciated from growing signs that the Fed would slow the action towards rate cuts in 2024.

The pair rose to the highest in more than two months, as fresh strength broke above former top at 148.80 (Jan 19), signaling an end of 148.80/145.89 corrective phase and bullish continuation.

Break of Fibo barrier at 149.15 (76.4% of 151.90/140.25) generated fresh bullish signal (which will require verification on close above this level) for attack at psychological 150 resistance.

Rising positive momentum and moving averages in full bullish configuration on daily chart, underpin the action, though overbought stochastic warns that bulls may face headwinds on approach to 150 barrier.

Rising 10DMA (147.90) should contain dips to keep bulls intact for 150+ acceleration.

Res: 149.70; 150.00; 150.77; 151.43.

Sup: 149.15; 148.80; 147.90; 147.45.

Sunset Market Commentary

Markets

Japanese stock markets and JPY still account for today’s biggest market move in a telling sign about current market momentum. The Nikkei closed slightly over 2% higher. USD/JPY sets a new YTD high at 149.40 with both the psychologic 150 mark and the 2022 (151.95) and 2023 (151.91) tops coming dangerously close. EUR/JPY escapes a narrow downward trend channel, rising to 160.50. It’s unlikely that this is what BoJ deputy governor Uchida had in mind when he spoke to local business leaders this morning. He advocated ending the negative interest rate policy, putting QE asset buying programmes (barely used of late) to bed and officially leaving the yield curve control policy (currently flexible cap of 1% at 10yr yield). While this trio of measures would be a big turn in BoJ monetary policy, Uchida also stressed that it is hard to imagine a path in which the BoJ would then keep raising interest rates rapidly. Financial conditions are set to remain easy. This “nuance” is what markets triggered into using their favoured JPY pressure tool: a weaker currency. Especially as USD and EUR profit (relatively) from a retreat in aggressive easing speculation. At the current weakening pace, it won’t take long before the Japanese Ministry of Finance turns to verbal (and effective?) FX interventions.

US weekly jobless claims were today’s sole data point of interest up until now (US 30-yr bond auction still to come). Unfortunately they printed almost bang in line with consensus at 218k. Central bank speeches didn’t deliver fireworks either. ECB Wunsch warns that wage rises are holding up rate cuts and that there’s value in waiting for more numbers. Richmond Fed Barkin joined the recent chorus to be patient on cutting rates as well. US yields currently add 1.5 bps (2-yr) to 3.9 bps (30-yr). German yields increase by 1.5 bps to 3 bps across the curve. General risk sentiment isn’t influenced yet by the spreading uncertainty over US (& European) bank exposure to US commercial real estate. The EuroStoxx50 rallies 0.8% to a new YTD/cycle high. Major US benchmarks open flattish. EUR/USD is trapped between 1.0750 and 1.08. In central Europe, the Czech National Bank accelerated from a 25 bps rate cut in December, to a 50 bps move today (to 6.25%). The Board voted 6-1 with one arguing for a 75 bps rate cut. The Czech currency is under new selling pressure with EUR/CZK rising above 25 for the first time since May last year.

News & Views

Riksbank Deputy Governor Jansson indicated that especially Swedish core inflation has recently fallen a little faster than expected. At the same time the economy continues to cool, reducing the risk of inflation becoming entrenched. This makes it possible to cut the policy rate earlier than indicated late last year. Still, monetary policy need to be characterized by caution. He doesn’t rule out a March cut, but sees it as not very likely. For now, it is more realistic to start cutting rates in May or June. Jansson doesn’t mention the currency as a risk for early rate cuts, unlike other MPC members including governor Thedeen in the minutes of the January meeting published yesterday. Despite the U-turn in the RB assessment, the krone recently held relatively stable (EUR/SEK .11.28).

The National Bank of Poland kept its policy rate unchanged at 5.75% yesterday. NBP governor Glapinski at the post meeting press conference (today) had a chance to give some insight on the NBP’s intentions going forward. Except for some small changes related to incoming data since the January meeting, the policy statement/assessment was almost identical to last meeting. The NBP sees inflation cooling. Especially headline inflation (6.2% Y/Y) might decline substantially in Q1 (2.5% in March) with slower progress seen for core inflation. However, the NBP still sees uncertainties related to regulatory and fiscal policy of the new government, with higher VAT, higher energy prices and (public) wage increases posing material upside risks for inflation in H2 (projection range of 3-8% by year end). Glapinski said that the NBP is committed to work with the government. The NBP statement sees the zloty now consistent with fundamentals and supporting the decrease in inflation. March projections should bring some more clarity. For now Glapinski still doesn’t see further rates cuts this year. EUR/PLN (4.33) declines modestly today.

Fed’s Barkin: We’ve got some time to be patient

Richmond Fed President Thomas Barkin highlighted the strength of the labor market and the encouraging trend of decreasing inflation in a Bloomberg TV interview. The cautious yet optimistic outlook grants Fed a period of watchful waiting before starting interest rate cuts.

"It's a very strong labor market still, and so gratified to see inflation coming down, hoping it continues to come down," Barkin remarked.

Barkin further indicated willingness to adopt a patient approach in the coming months. "I think we've got some time to be patient," he stated. Fed will get "a few more months" of inflation data and he desires "to see that trend continue and broaden".

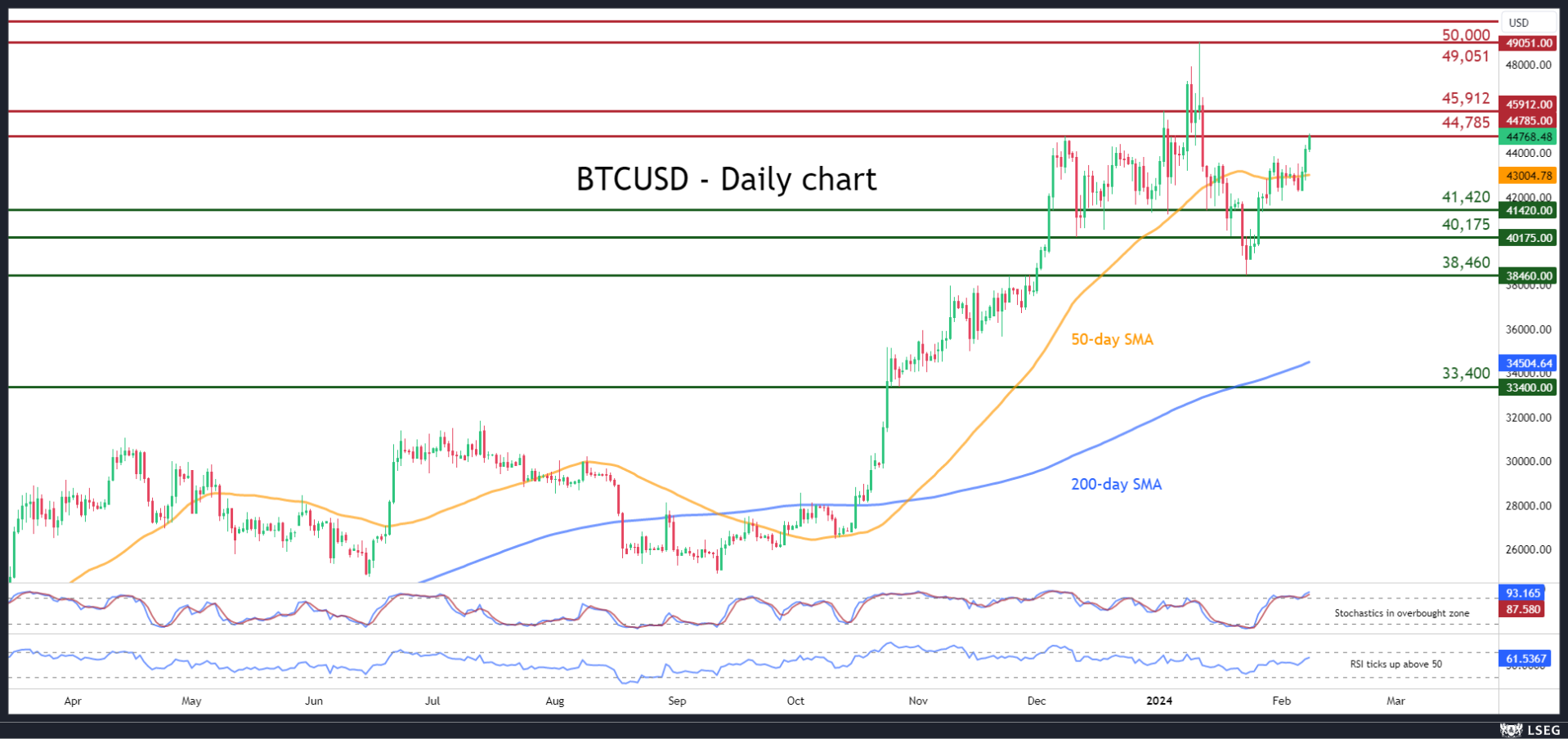

BTCUSD Advances Towards Crucial Resistance

- BTCUSD ascends sharply after claiming 50-day SMA

- Currently challenges the December peak of 44,785

- Momentum indicators are starting to look overbought

BTCUSD (Bitcoin) experienced a strong decline from its recent two-year peak of 49,051, dropping to as low as 38,460. However, the price has managed to storm back and recoup a significant part of its losses, testing the crucial 44,785 resistance zone on Thursday.

If the price conquers the December peak of 44,785, the bulls could then aim for the January resistance of 45,912. A jump above the latter could shift the spotlight to the two-year high of 49,051. Surpassing that region, Bitcoin could surge to fresh multi year highs, where the 50,00 psychological mark could serve as the next resistance territory.

On the flipside, should the advance falter, the inside swing low of 41,420 could act as the first line of defence. In case of a downside violation, the price may face the December support of 40,175. Further declines might encounter strong support at the 2024 bottom of 38,460.

In brief, BTCUSD’s advance has accelerated after the profound break above the 50-day simple moving average (SMA). Therefore, the focus now shifts on the December peak of 44,785, where a failure to conquer that region could trigger a pullback.

EUR/USD Eyes German Inflation

EUR/USD is slightly lower on Wednesday. In the North American session, the euro is trading at 1.0751, down 0.20%.

German inflation expected at 0.2%

Germany’s CPI is expected at 0.2% m/m on Friday, which would confirm the initial estimate from two weeks earlier. On an annualized basis, the initial estimate for CPI came in at 2.9% in January, down sharply from 3.7% in December. A deceleration in energy and food costs was the driver of the downturn in January, which was the lowest inflation rate since June 2021. Core inflation has also been falling, with the initial estimate showing a drop to 3.4%, its lowest rate since June 2022.

The drop in German inflation is not all that surprising, as the eurozone’s largest economy has been struggling. Germany’s manufacturing sector has been in prolonged decline and the services sector is sputtering, with five declines in the past six months. The economy declined in the fourth quarter and another contraction in Q1 would mean that Germany will have entered a technical recession. The eurozone is also grappling with a weak economy, with the latest evidence earlier this week as retail sales declined 1.1% m/m in December.

Despite weak economic conditions in the eurozone and Germany, the European Central Bank has been hesitant to cut interest rates. ECB members have expressed concern that inflation could make a comeback if the ECB were to cut rates too early. That could force the ECB to raise rates again and the optics of such a zig-zag would be disastrous. For now, the ECB remains hawkish on rate policy and is content to continue holding rates until inflation falls closer to the 2% target.

Since last week’s Fed meeting, a host of Fed members have delivered the message that inflation is heading in the right direction but the Fed plans to be patient and is in no rush to lower rates. The markets have taken note of the Fed’s pushback and have pared expectations of a rate cut in March to 18%, down from over 70% in January, according to the CME’s Fed Watch tool.

EUR/USD Technical

- EUR/USD tested support at 1.0746 earlier. Below, there is support at 1.0704

- There is resistance at 1.0822 and 1.0864

USD/JPY Slides After BOJ Uchida’s Hawkish Comments

The Japanese yen is down sharply on Thursday. In the European session, USD/JPY is trading at 149.12, up 0.64%. This is the yen’s lowest level against the US dollar since November 27.

BoJ’s Uchida hints at policy shift

The Bank of Japan dropped its latest hint of a shift in monetary policy earlier today. BoJ Deputy Governor Shinichi Uchida said that even if the BoJ were to end negative rates, it was unlikely to “keep raising the interest rate rapidly”. Uchida added that the central bank would likely terminate its massive stimulus once the goal of a sustainable and stable inflation rate of 2% was within reach.

The BoJ has been carefully laying the groundwork for normalising policy, which would be a sea-change in policy and would likely send the Japanese yen sharply higher. An exit from negative rates, which is equivalent to a hike in rates, appears to be a question of timing. The markets are expecting the central bank to make a move in March or April, although the June meeting is also a possibility.

The Federal Reserve continues to push back against rate cut expectations. Four Fed officials signalled on Wednesday that the Fed is not on the cusp of a historic interest rate cut after its steep rate-tightening cycle which has tamed inflation.

Since last week’s policy meeting, a string of Fed members have come out with the message that inflation is heading in the right direction but the Fed plans to be patient and is in no rush to lower rates. The markets have taken note of the Fed’s reluctance and have pared expectations of a rate cut in March to 18%, down from over 70% in January, according to the CME’s Fed Watch tool.

USD/JPY Technical

- USD/JPY is testing resistance at 149.05. Above, there is resistance in 149.33

- There is support at 148.42 and 148.02

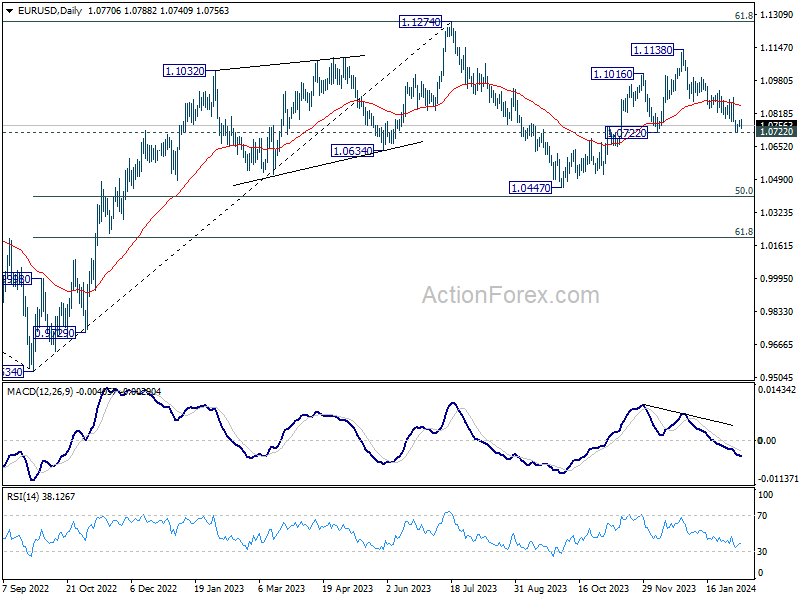

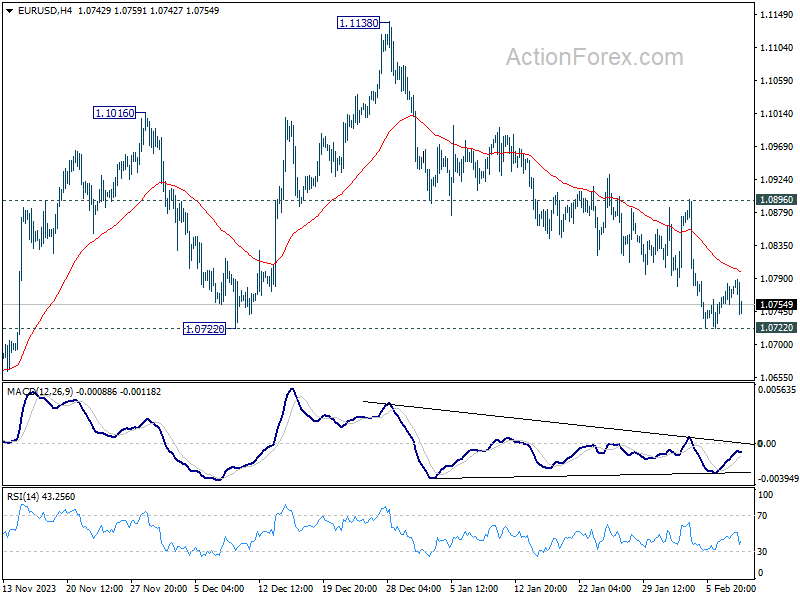

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0755; (P) 1.0770; (R1) 1.0787; More...

EUR/USD is still holding above 1.0722 support and intraday bias stays neutral. On the downside, decisive break of 1.0722 will argue that whole rise from 1.0447 has completed. Deeper fall would then be seen to target this low. On the upside, break of 1.0896 resistance is needed to indicate short term bottoming. Otherwise, risk will stay on the downside in case of recovery.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and possibly below.