Sample Category Title

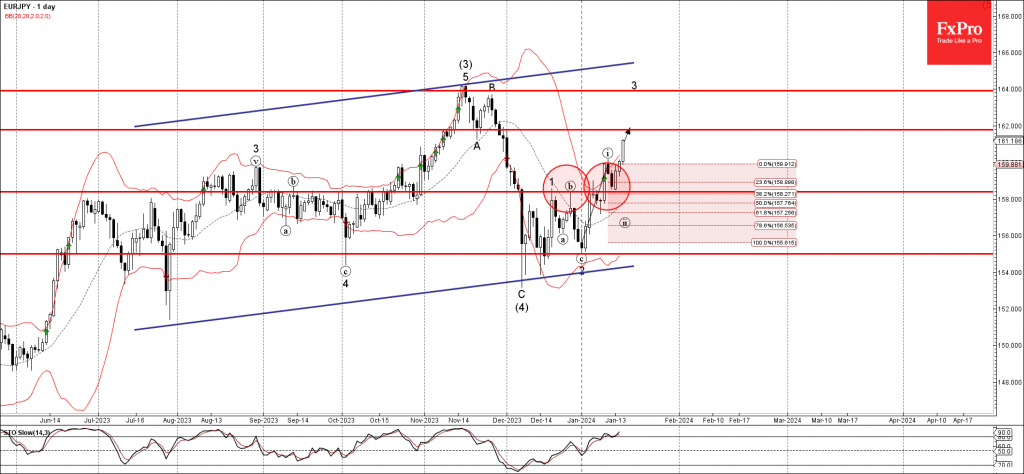

EURJPY Wave Analysis

- EURJPY reversed from key support level 158.40

- Likely to rise to resistance level 162.00

EURJPY currency pair recently reversed up from the key support level 158.40 (former resistance from last month, acting as the support after it was broken).

The support level 158.40 was strengthened by the 38.2% Fibonacci correction of the previous sharp upward impulse from December.

Given the strong daily uptrend and widespread euro optimism, EURJPY can be expected to rise further to the next resistance level 162.00.

SNB’s Jordan highlights challenges for Swiss firms due to Franc’s real appreciation

In an interview with Bloomberg TV, SNB President Thomas Jordan noted that for a prolonged period, the Swiss economy experienced primarily a nominal appreciation of its currency. He described that as "very helpful" as it helped shield Switzerland from external inflationary pressures, providing a buffer against global economic fluctuations.

However, the situation evolved in the latter part of the year with Swiss Franc experiencing real appreciation. "That makes the situation for some of our firms more difficult," Jordan added.

The SNB President also indicated that these recent currency movements would be a critical factor in the central bank's next quarterly decision. The shift from nominal to real appreciation in Swiss Franc will be a key consideration, as it alters the economic context within which SNB makes its policy decisions.

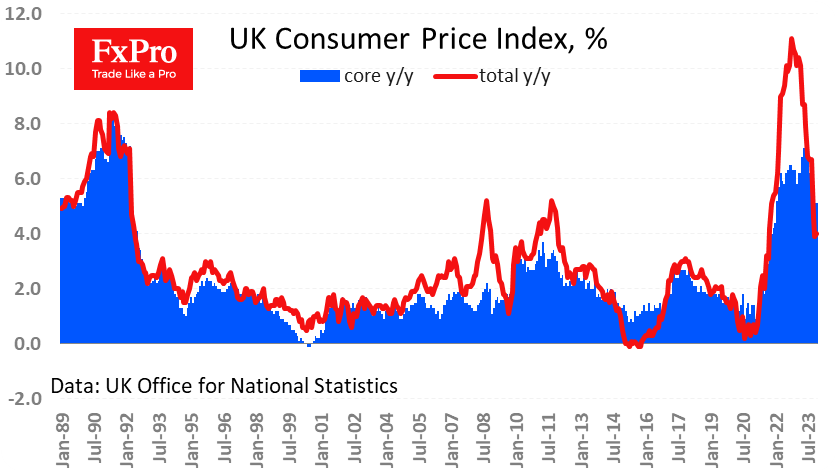

Pound Doesn’t Give Up Without a Fight, Thanks to CPI

UK inflation statistics sparked a 0.8% rally in the pound on Wednesday morning, supporting GBPUSD gains against a general pull from risk assets.

According to data released on Wednesday morning, the General Price Index rose by 0.4% for December against an expected 0.2%. Annual inflation accelerated to 4.0%, the first rise in 10 months.

The core consumer price index maintained the pace at 5.1% y/y vs. an expected slowdown to 4.9%.

The drivers of price increases were tobacco and alcohol due to one-off factors. Formally, this will make it harder for inflation to return to the target, but it is unlikely to be a factor that the Bank of England will struggle with.

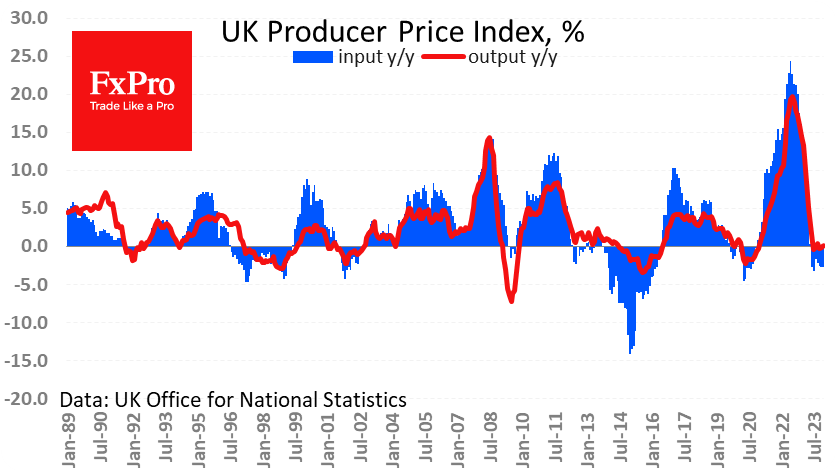

In contrast, producer prices are falling more strongly than expected, and we think this is the more important factor. Producer prices fell by 1.2% after falling 0.4% previously. The year-to-date decline is 2.8% and has fluctuated between 2% and 2.9% over the six months.

Producer prices lost 0.6% over December and are up 0.1% y/y, hovering around zero for the past six months.

A separate report noted a 2.1% y/y drop in housing prices in November, weaker than the 1.9% decline expected and the 1.3% decline a month earlier.

The inflation surprise caused traders to soften expectations of a key rate cut by the Bank of England. As a result, the GBPUSD pair is enjoying gains while the markets continue the risk-aversion bias. The news also added pressure on the UK equity market, where the FTSE100 lost around 1.3%, back to early December levels at 7460.

Looking ahead, we note the decline in annualised inflation in producer input prices and disinflation in producer output prices. The slowdown in wage growth also points to a reduction in domestic inflationary pressures. Technically, this opens the door for the Bank of England to start easing policy, but we should expect the central bank to take this step only after signs of a significant cooling of the economy.

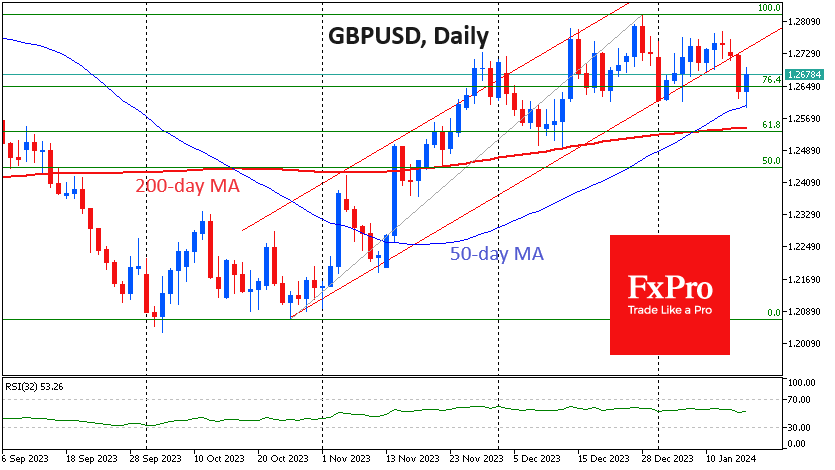

Technically, GBPUSD got support on touching the 50-day moving average. But yesterday’s decline has already effectively broken the upward trend, which has been in force since October. The pound may stabilise for a while in the 1.26-1.27 range, but there are still higher chances that the exit from consolidation will be down, not up.

Sunset Market Commentary

Markets

ECB president Lagarde immediately set the tone for trading in a Bloomberg interview at the World Economic Forum in Davos. She repeated that the ECB is watching wages, profit margins, energy prices and supply chains over the next months before firmly concluding that inflation is on a sustained path towards the central bank’s 2% inflation target. Short of any major shock, ECB policy rates have peaked with the next move being a rate cut. On the timing, she joined other ECB members who recently pushed back against aggressive market pricing on both rapid and plenty of policy rate decreases this year. Lagarde suggested that a first move lower is only likely by the Summer. This year’s two ECB Summer policy meetings are July 18 and September 12. A July rate cut would symbolically come exactly two years after the first policy rate increase while a September cut would mean that the ECB’s key rate was at its 4% peak for exactly one year. While investors reduced early easing bets, they still discount a cumulative 50 bps of rate cuts by the June 6 policy meeting completely ignoring recent guidance. By the first Summer meeting in July, this increases to a cumulative 75 bps! The Lagarde comments triggered a soft opening for German Bunds with the front end of the curve underperforming. German yields currently add up to 7.2 bps (2-yr).

And yet US Treasuries and UK Gilts sell off even more intensely today… US yields add 2 bps (30-yr) to 11.1 bps (2-yr). Apart from the echo of yesterday’s Fed Waller comments, markets were served consensus-beating December US retail sales. The headline figure rose by 0.6% M/M (vs 0.8% consensus) with the control group (used as a proxy for consumption in GDP calculations) even adding 0.8% M/M following an upwardly revised 0.5% M/M in November and rounding another good quarter. UK Gilt yields even surge 9 bps (30-yr) to 17.5 bps (3-yr) today following December UK inflation figures. Inflation accelerated by 0.4% M/M (vs 0.2% consensus), pushing the headline figure to 4% Y/Y (vs 3.8% expected). Both core inflation (unchanged at 5.1%) and services inflation (6.4% from 6.3%) beat consensus as well. Today’s inflation print significantly limits the Bank of England’s room to prioritize growth over the ongoing inflation battle. Sterling initially profited from the interest rate support (EUR/GBP 0.8575 from 0.8610) but can’t build on those gains. EUR/USD extends its move south (1.0860) with the Japanese yen back under huge selling pressure (USD/JPY 148). European stock markets cede over 1% with WS opening up to 1.2% lower (Nasdaq).

News & Views

The president of the Swiss National Bank told Bloomberg that the recent strengthening of the Swiss franc has been significant enough so that it affects the inflation outlook. The central bank will take that into account at the next policy meeting on March 21. At the latest December meeting, the SNB shifted to a more neutral approach by no longer keeping the door for rate hikes formally open and making the FX intervention threat bidirectional again instead of focusing on CHF sales. Its inflation forecast showed inflation not above 2% for the entire horizon and Jordan told Bloomberg at the time that “In three months, we will look very carefully at the new forecast” and that “Depending the situation, we will adapt monetary policy.” If the outlook now gets revised downward again in March because of the (real) CHF appreciation, the SNB may pivot further towards rate cuts. A first full rate cut is priced in for June but odds for a March move rose after Jordan’s speech. The Swiss franc loses ground as a result. EUR/CHF rises above 0.94 and, by doing so, recovers previously lost support.

When the deputy governor of the Hungarian central bank speaks, the forint listens. Virag in Q4 last year guided the market towards several 75 bps rate cuts through early 2024. In December they nevertheless already discussed the option of moving ahead with a 100 bps move before eventually sticking to the original pace. However, with inflation figures coming in more favourable than expected, the deputy governor today said room for a 100 bps cut has grown and they’ll consider the possibility again at the January 30 meeting. If that were to happen, it would be only temporary, say one to three months. By mid-2024, Virag said the key rate could drop to around 6-7% from 10.75% today. The Hungarian central bank meets on a monthly basis. The forint dropped on Virag’s comments. EUR/HUF topped 380 before moving further to 381.25 currently. Hungarian swap yields dropped 14 bps intraday at the front before recovering again, joining the trend in global core bond markets.

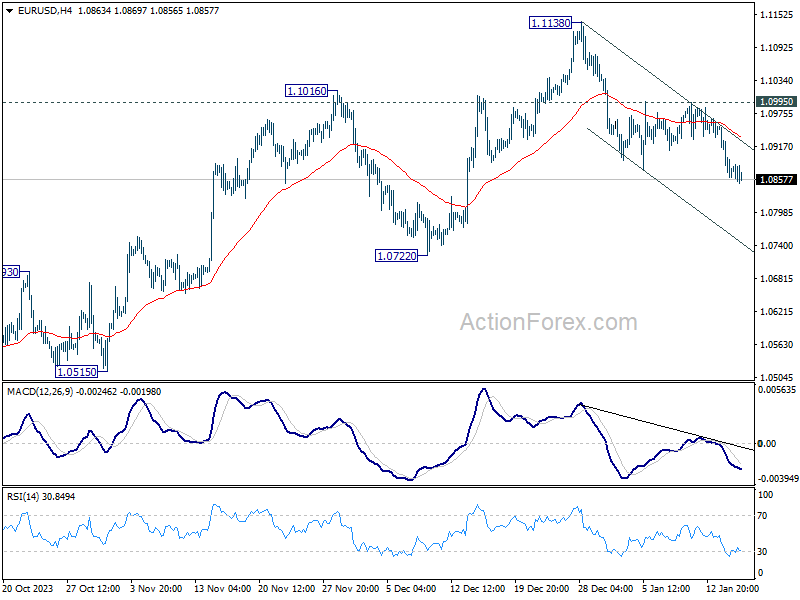

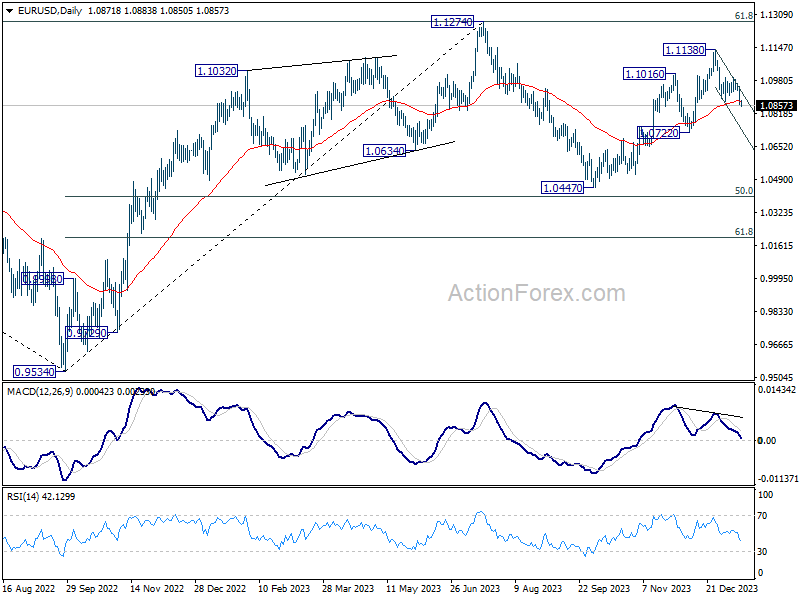

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0841; (P) 1.0897; (R1) 1.0933; More...

Intraday bias in EUR/USD remains on the downside at this point. Current decline from 1.1138 is in progress for 1.0722 support. Sustained break there will argue that whole rise from 1.0447 has completed, and target this low. For now, risk will stay on the downside as long as 1.0995 resistance holds, in case of recovery.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and below.

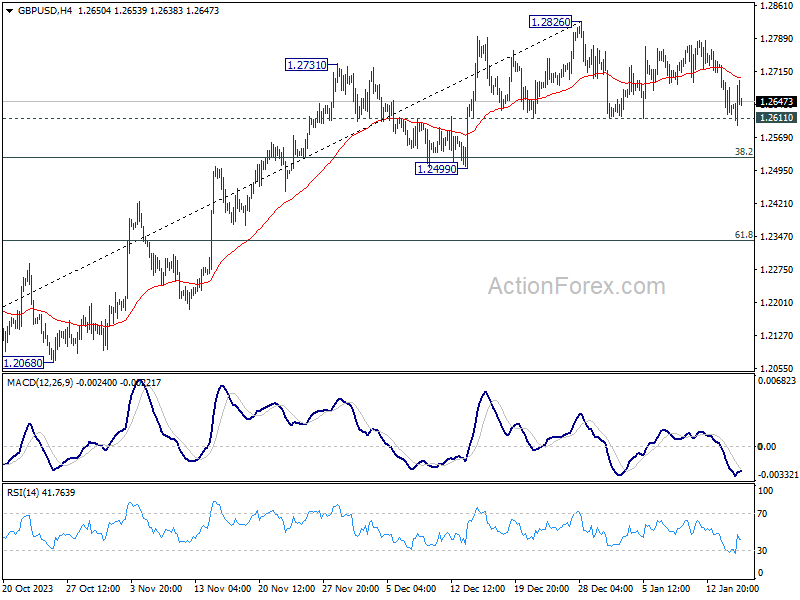

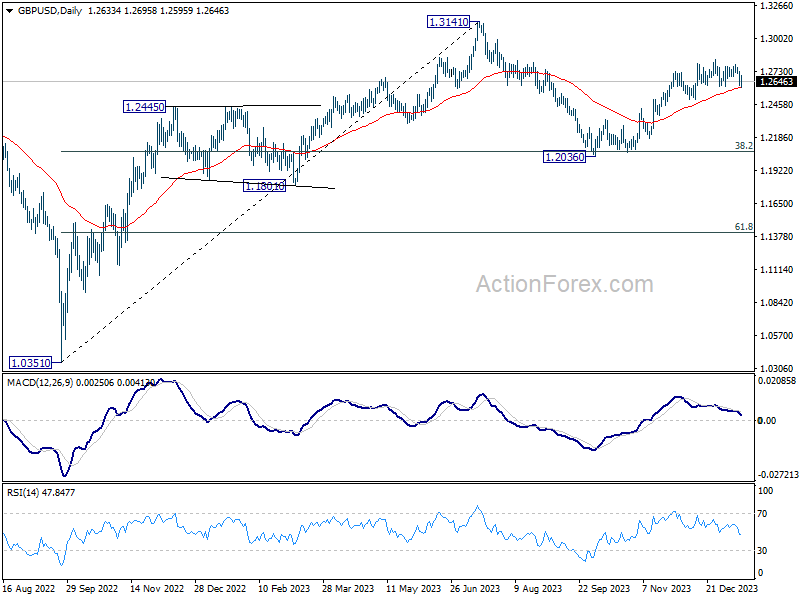

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2592; (P) 1.2664; (R1) 1.2709; More...

Intraday bias in GBP/USD remains neutral for the moment. On the downside, firm break of 1.2611 will resume the decline from 1.2826 to 1.2499 support. Nevertheless, strong rebound from current level will retain near term bullishness. Decisive break of 1.2826 will resume whole rally from 1.2036.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg that's in progress. Upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

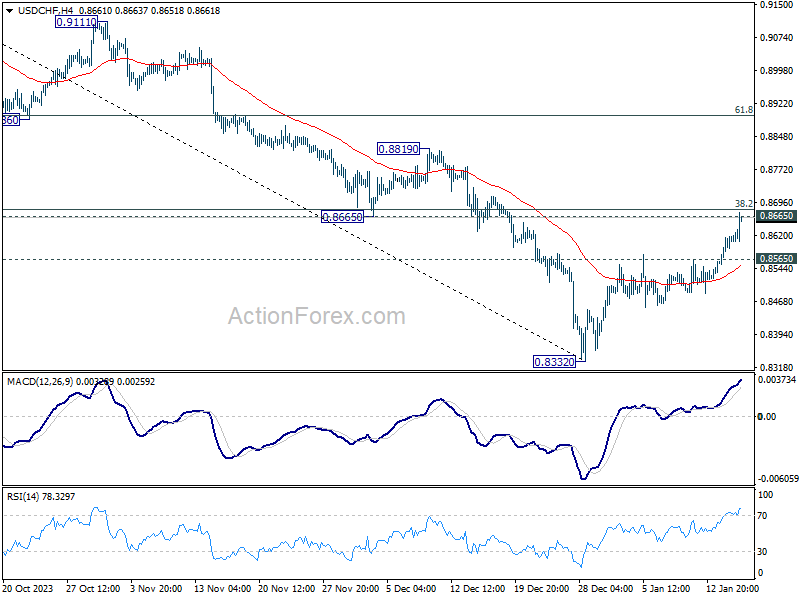

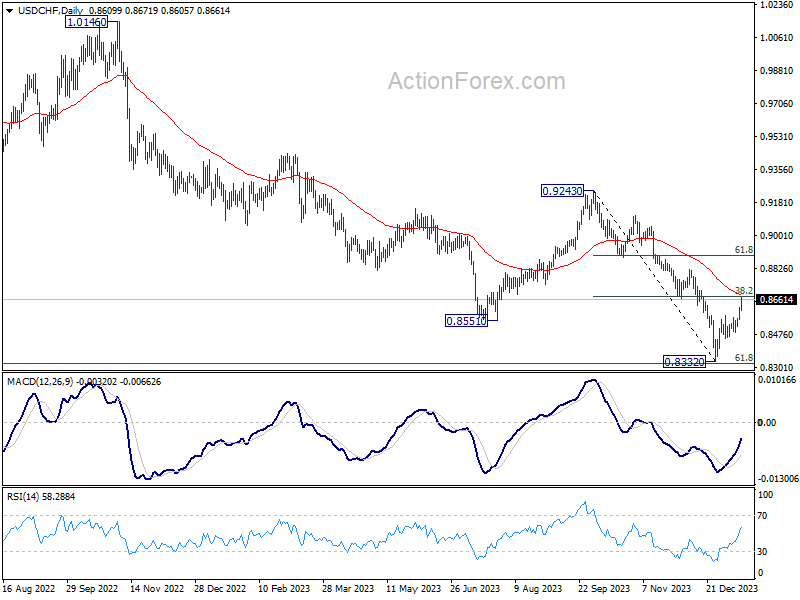

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8574; (P) 0.8597; (R1) 0.8639; More....

Immediate focus in now on 0.8665 support turned resistance as rebound from 0.8332 extends today. Decisive break there will turn near term outlook bullish for 61.8% retracement of 0.9243 to 0.8332 at 0.8995. Nevertheless, break of 0.8565 minor support will turn intraday bias back to the downside for retesting 0.8332 low.

In the bigger picture, outlook in USD/CHF will stay bearish as long as 0.9243 resistance holds. Larger down trend from 1.0146 (2022 high) should resume through 0.8332 low at a later stage.

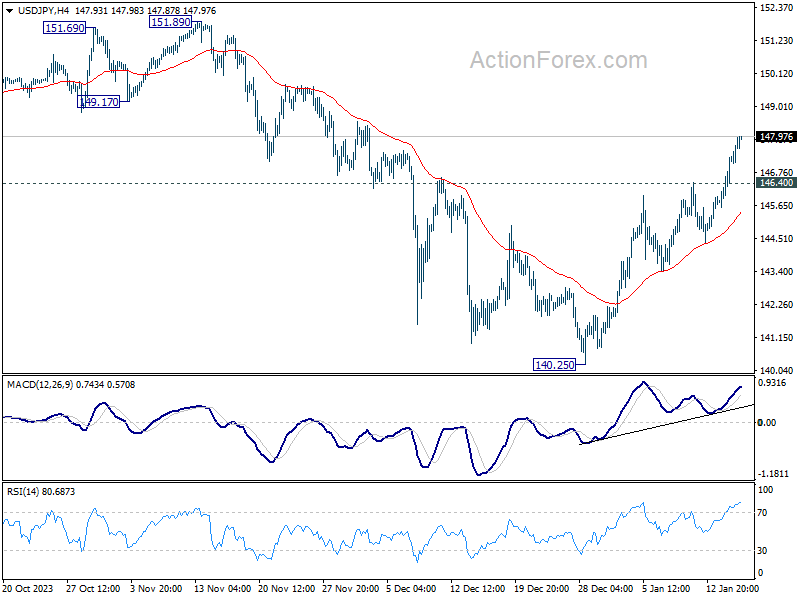

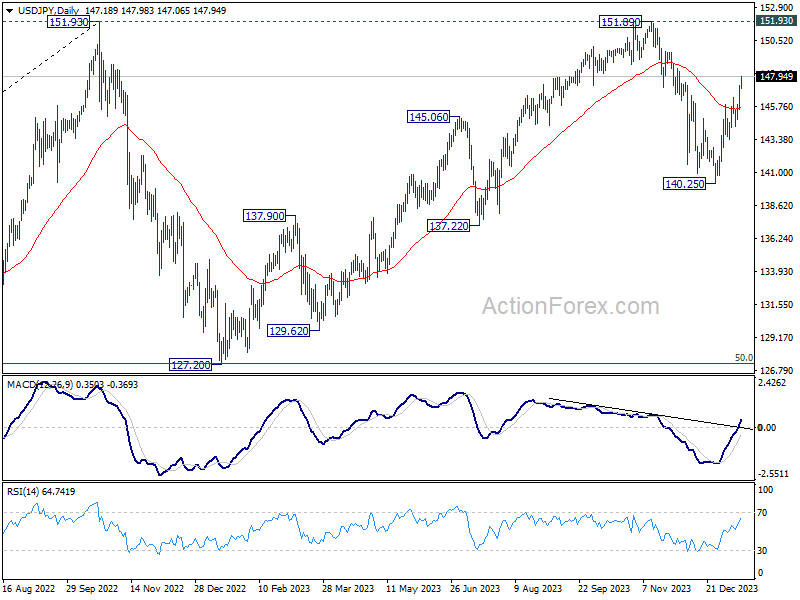

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 146.08; (P) 146.70; (R1) 147.80; More...

Intraday bias in USD/JPY remains on the upside at this point. Current rise from 140.25 should target 151.89/93 key resistance zone next. On the downside, below 146.40 minor support will turn intraday bias neutral first. But further rally will remain in favor as long as 55 D EMA (now at 145.67) holds.

In the bigger picture, stronger than expected rebound from 140.25 dampened the original bearish review. Strong support from 55 W EMA (now at 141.89) is also a medium term bullish sign. Fall from 151.89 could be a correction to rise from 127.20 only. Decisive break of 151.89/93 will confirm resumption of long term up trend. This will now be the favored case as long as 140.25 support holds.

U.S. Retail Sales Close 2023 on an Stellar Note

Retail sales rose by 0.6% month-on-month (m/m) in December, extending November's 0.3% gain. This was higher than consensus forecast calling for an increase of 0.4%.

Trade in the auto sector was up on the month rising by 1.1% m/m. This reflected an increase in sales at both motor vehicle dealers (up 1.2%) and automotive parts and accessory stores (up 0.7%).

Sales at gasoline stations continued to pull back, falling by -1.3% m/m extending last month's -3.4% decline. This largely reflected the reduction in gas prices. The building materials and equipment category rose by 0.4% m/m, overcoming the previous month's -0.1% decline.

Sales in the retail sales "control group", which excludes the above volatile components (autos, building materials and gas) and is used to estimate personal consumption expenditures (PCE) came in at a sizeable 0.8% m/m. November's figure was also revised up to 0.5% growth from the previously reported 0.4%.

- Among the control group, the largest contributions came from sales at non-store retailers (1.5% m/m), clothing and accessory stores (1.5% m/m) and department stores (1.3 % m/m).

- The only two categories posting declines were health and personal care stores (-1.4% m/m) and furniture and electronics stores (-0.7% m/m).

Food services & drinking places – the only services category in the retail sales report – was flat on the month after a upwardly revised growth of 1.7% m/m in November.

Key Implications

Once again U.S. consumers showed their resilience, boosting retail spending in December and closing out the year with a bang. Sales for the month rose at a relatively fast pace adding to decent gains in November. This was sufficient to overcome October's decline, causing retail sales to grow at a 3.9% annualized pace for the fourth quarter. While decent, this was still a step-down from 6.9% q/q annualized growth in Q3. With the holidays in the rear view mirror and consumer headwinds still firmly in play, spending is expected to continue slowing in the New Year.

While moderating, consumer spending is still resilient and remains a challenge to the Fed's disinflation objective. Given that this spending is largely being supported by a still robust labor market, the central bank will need to see more progress on this front (i.e. a more balanced labor market with reduced wage pressures) before pursuing rate cuts. This is unlikely to happen before summer.