Sample Category Title

Trimming

Investors continue to come back to their senses and the latter involves trimming the interest rate cut expectations that went ahead of themselves over the past few months. Yesterday, the Federal Reserve’s (Fed) Beige Book survey suggested that resilient consumer spending during the holiday season helped propel the US economy, and another solid rise in the US retail sales confirmed that spending in the US didn’t slow by the end of last year. On the contrary, the latest data printed its highest pace in three months. As such, robust economic data added to the thinking that, yes, maybe March is too early for the Fed to announce the first rate cut; there is no apparent reason for the Fed to rush to the rate cuts as early as in March. The Fed will likely start cutting in the H1 but March seems overly optimistic given the ongoing strength of the economic data. The probability of a March cut fell to around 60% from around 80% at the start of the year, the US 2-year yield advanced 25bp since the start of the week, the 10-year steadies above the 4%, the US dollar index is pushing higher, the S&P500 comes under fresh selling pressure near peak, and volatility is rising. Given how far the Fed doves and the market bulls pushed their rate cut bets over the past months, there is room for further downside correction in both stock and bond markets, and potential for a further recovery in the US dollar against most majors.

Davos vibes

Central bankers, bank CEOs and other influential figures continue to talk in Davos. They continue to push back on the interest rate cut expectations, they highlight the need to consider the upside risks for inflation due to the rising geopolitical tensions and they continue to warn that the market’s optimism regarding the rate cuts may have the opposite impact on rate policies: too much optimism could delay the rate cuts. European Central Bank (ECB) Chief Christine Lagarde warned in Davos yesterday that overly optimistic rate cut expectations don’t help the central banks’ fight against inflation – as they loosen the financial conditions prematurely. She, however, hinted that the ECB will likely cut rates by, or in summer. And this was the first time we heard the ECB Chief loudly considering rate cuts.

The market and the central bankers have started to move toward each other, but the time gap between when investors price in the first cuts and when central bankers contemplate rate reductions should continue narrowing to find an optimal balance and that should involve a deeper downside correction in stock and bonds, and a further recovery in the US dollar.

Markets

The EURUSD tested the 200-DMA to the downside yesterday and price rebounds could be interesting opportunities for building fresh shorts targeting the 1.0770/1.08 range. Cable is better bid above the 50-DMA after a surprise rebound in the UK’s December inflation numbers weakened the Bank of England (BoE) doves’ hands yesterday. Cable is testing the 1.27 offers, with a limited upside potential, however, given that the Fed rate cut expectations are being cut, and when the Fed is in play, the other central bank expectations must wait their turn to speak up. In Japan, the USDJPY advanced to 148.50, a move that no one saw coming by the end of last year when the Bank of Japan (BoJ) normalization bets started fueling long positions in the Japanese yen. Data released this morning showed that the Japanese core machinery orders fell 5% in November, calling for a supportive BoJ, rather than a rate hike.

Earlier this week, China printed a 5.2% growth for last year - not a major achievement, mind you, as the 5% rebound from the pandemic crash matched nothing better than a meagre 2% growth compared to a non-Covid year. Industrial production was better than expected in December while retail sales grew slower. Chinese equities barely reacted to the news of a trillion-yuan worth stimulus earlier this week. The selloff in the CSI 300 accelerates as the focus remains on developing deflation and worsening property crisis. The Aussie feels the pinch of soft China, soft jobs figures and stronger US dollar. The AUDUSD sank below the 200-DMA and is preparing to test the 100-DMA, at 0.6510, to the downside. The AUDUSD outlook turns neutral from positive, the only thing that could slow the Aussie’s selloff against the greenback is technical indicators hinting that the pair will soon step into the oversold conditions.

In energy, crude oil is better bid and the barrel of American crude is testing the $73pb – again this morning on the Red Sea tensions and on OPEC forecast that global oil demand will grow by a robust 1.8 mio barrels per day next year, exceed growth in supplies and keep the market in deficit. Of course, the OPEC forecasts should be taken with a pinch of salt as they have an interest in making the numbers look in favour of them. But what’s real is the sharp decline in shipping transits through the Red Sea region, which will continue to push the shipping costs higher, could squeeze the energy markets and throw a floor under the oil selloff near the $70pb level.

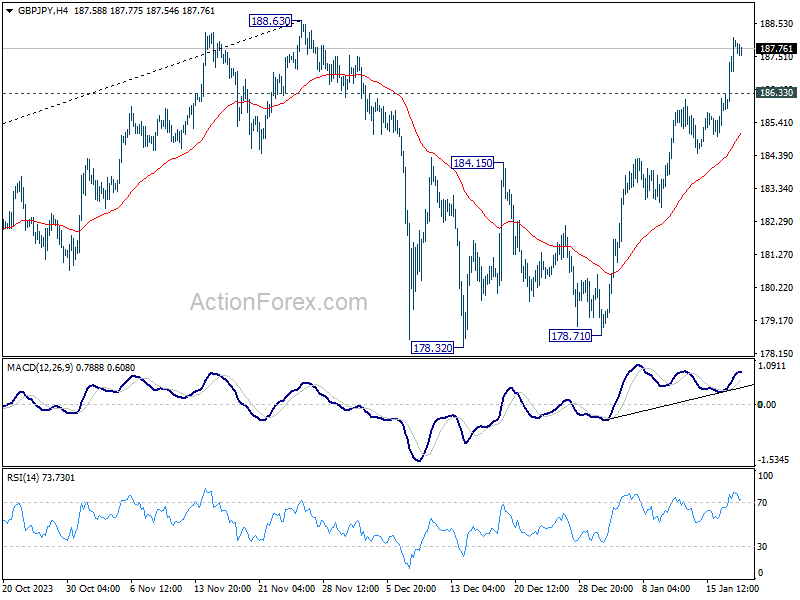

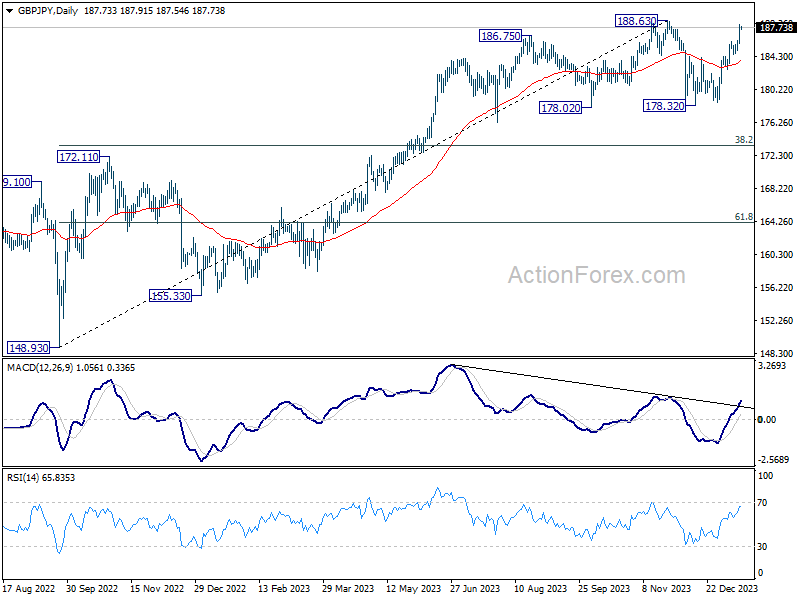

GBP/JPY Daily Outlook

Daily Pivots: (S1) 186.40; (P) 187.27; (R1) 188.65; More...

Intraday bias in GBP/JPY remains on the upside for retesting 188.63 high. Firm break there will confirm larger up trend resumption. On the downside, below 186.33 minor support will turn intraday bias neutral and bring consolidations first. But further rally is expected as long as 184.15 resistance turned support holds.

In the bigger picture, price actions from 188.63 medium term top are seen as a correction to the up trend from 148.93 (2022 low) only. As long as 172.11 resistance turned support holds, larger up trend from 123.94 (2020 low) is still in favor to resume through 188.63 at a later stage. Next target will be 195.86 long term resistance.

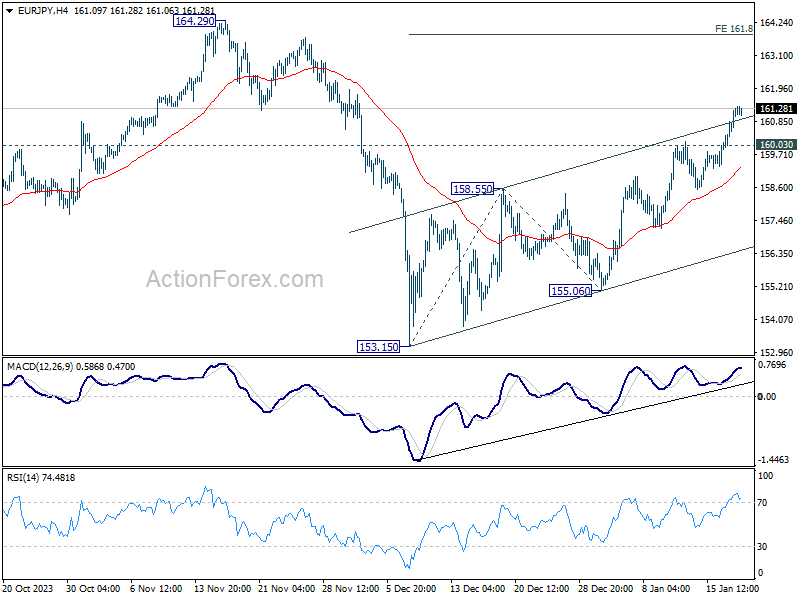

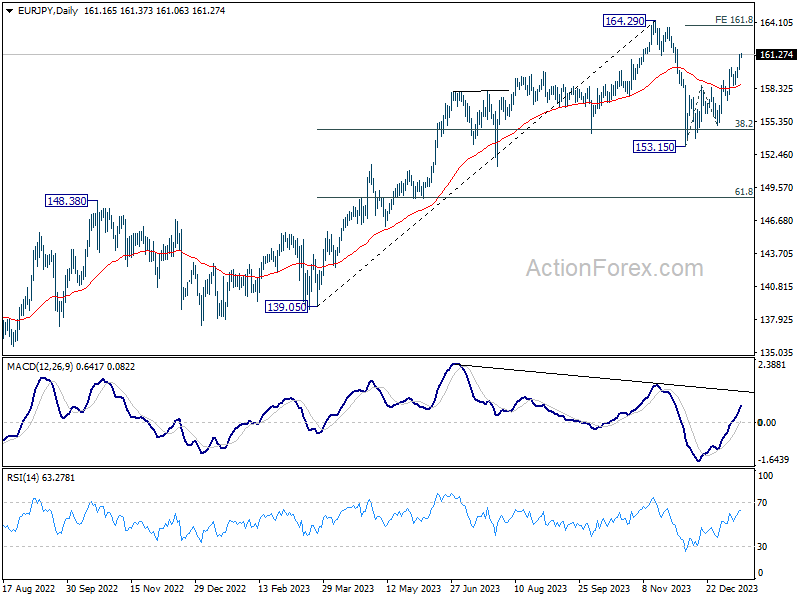

EUR/JPY Daily Outlook

Daily Pivots: (S1) 160.32; (P) 160.81; (R1) 161.71; More...

Intraday bias in EUR/JPY remains on the upside at this point. Current rise from 153.15 is in progress for 161.8% projection of 153.15 to 158.55 from 155.06 at 163.79, which is close to 164.29 high. On the downside, below 160.03 minor support will turn intraday bias neutral first. But further rally is expected as long as 158.55 resistance turned support holds.

In the bigger picture, price actions from 164.29 medium term top are tentatively seen as a correction to rise from 139.05 for now. As long as 148.48 resistance turned support holds (2022 high), larger up trend from 114.42 (2020 low) could still resume through 164.29 at a later stage.

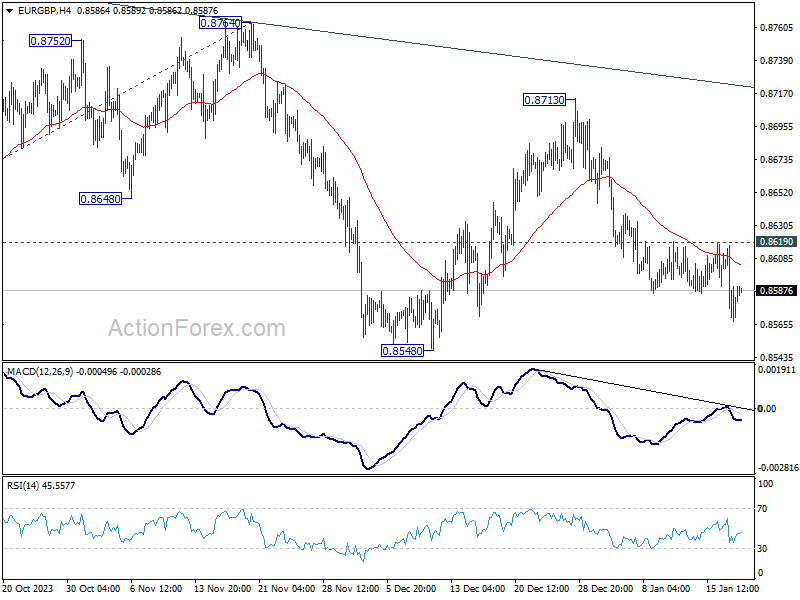

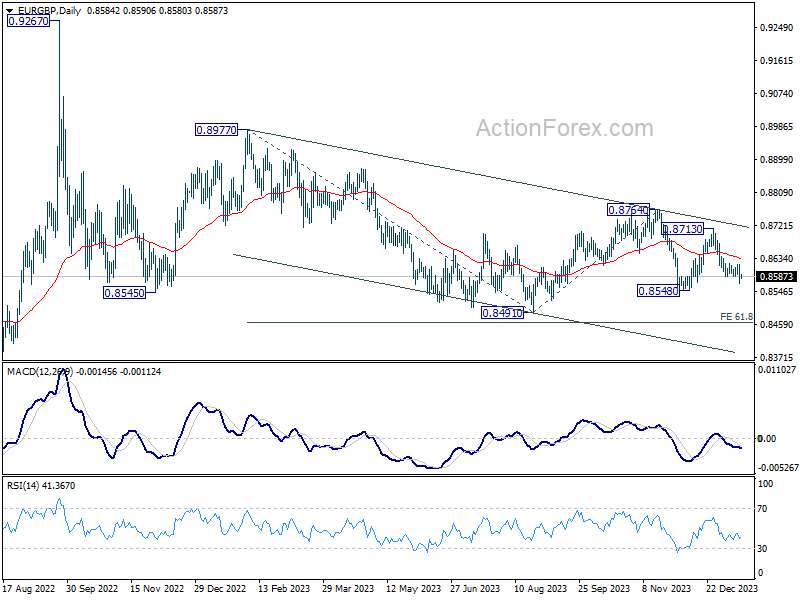

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8563; (P) 0.8590; (R1) 0.8613; More...

Intraday bias in EUR/GBP remains on the downside for 0.8548 support. Firm break there will argue that larger down trend is ready to resume through 0.8491 low. On the upside, break of 0.8619 resistance is needed to indicate short term bottoming. Otherwise, further fall is in favor in case of recovery.

In the bigger picture, fall from 0.8764 is seen as another leg in the whole down trend from 0.9267 (2022 high). Outlook will stay bearish as long as 0.8764 resistance holds. Break of 0.8491 will target 61.8% projection of 0.8977 to 0.8491 from 0.8764 at 0.8464.

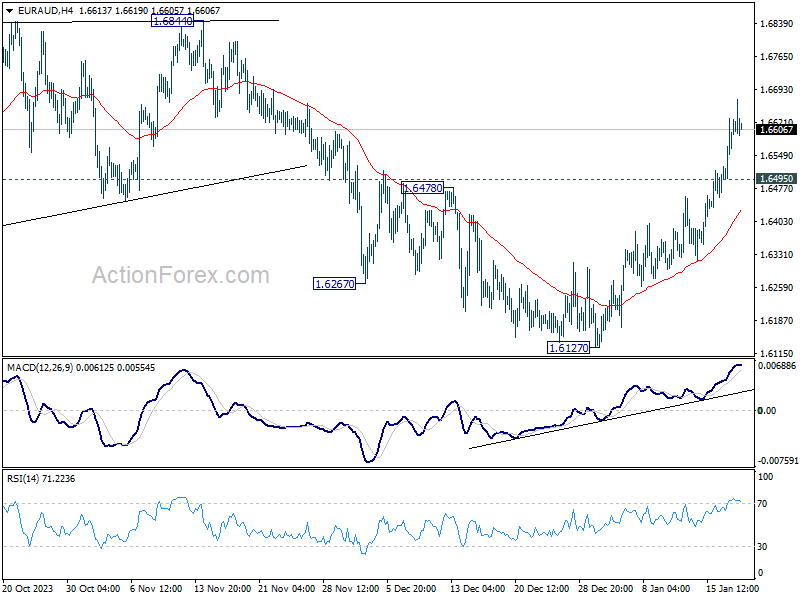

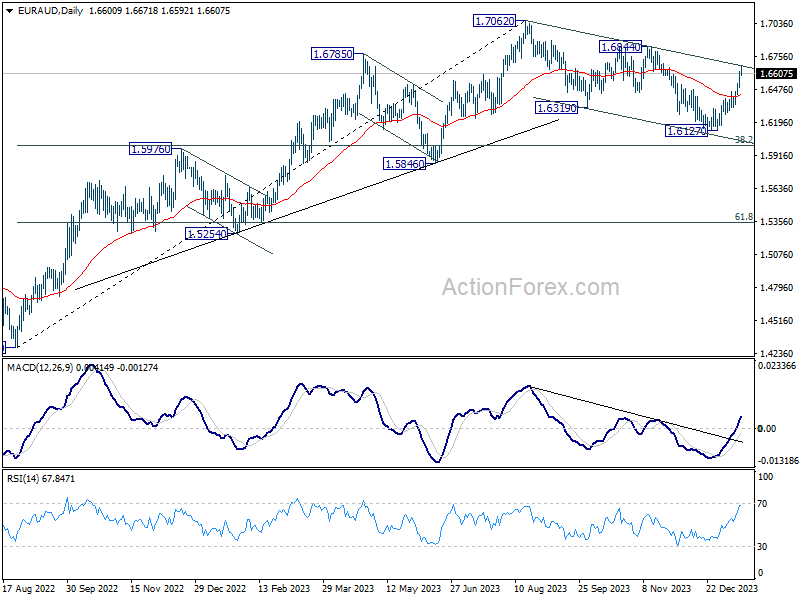

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6527; (P) 1.6579; (R1) 1.6662; More...

Intraday bias in EUR/AUD stays on the upside at this point. As noted before, Correction from 1.7062 should have completed with three waves down to 1.6127. Further rise should be seen to 1.6844 resistance for confirmation. On the downside, below 1.6495 minor support will turn intraday bias neutral and bring consolidations, before staging another rally.

In the bigger picture, fall from 1.7062 medium term top is seen as correction to the up trend from 1.4281 (2022 low). Break of 1.6844 resistance will argue that this up trend is ready to resume through 1.7062 high. In case of another fall, strong support should be seen around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 bring rebound.

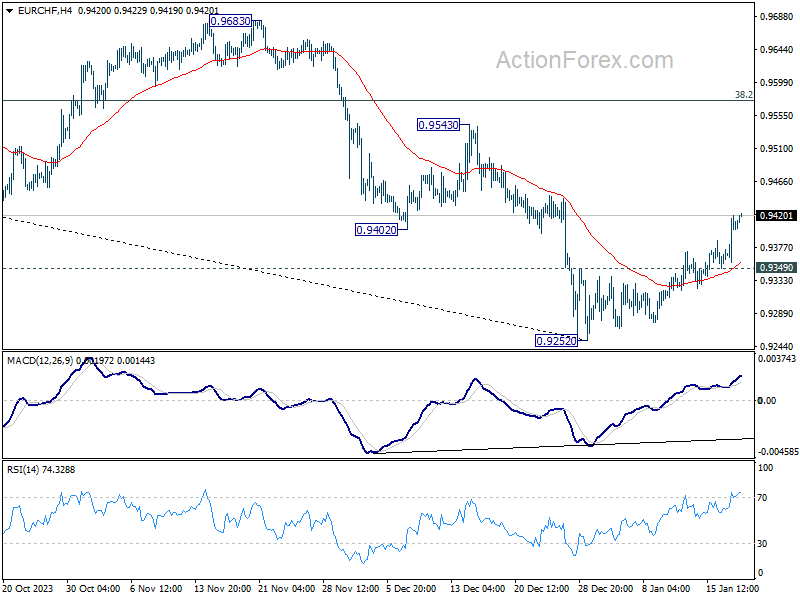

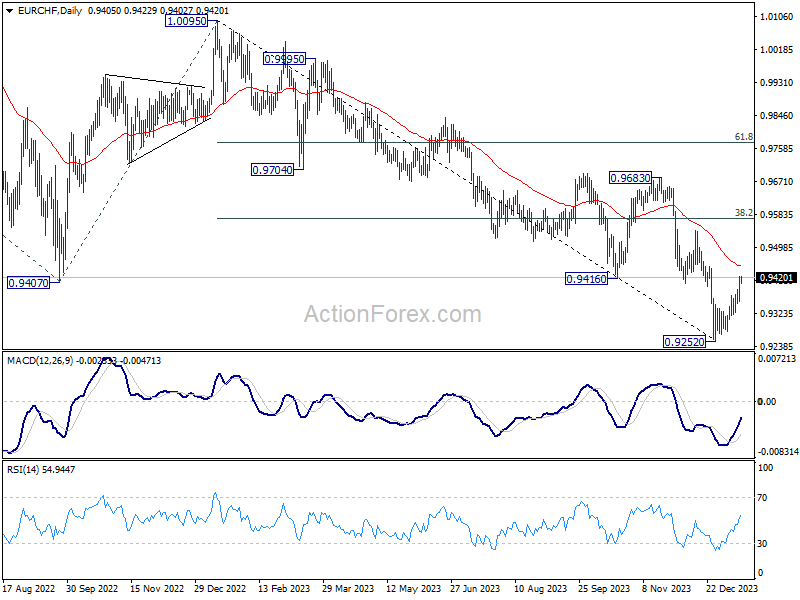

EUR/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9351; (P) 0.9370; (R1) 0.9389; More...

Intraday bias in EUR/CHF remains on the upside at this point. Rebound from 0.9252 short term bottom is in progress for 55 D EMA (now at 0.9448). Sustained break there will target 38.2% retracement of 1.0095 to 0.9252 at 0.9574. On the downside, though, break of 0.9349 minor support will turn bias back to the downside for retesting 0.9252 low instead.

In the bigger picture, medium term outlook remains bearish as long as 0.9683 resistance holds. Current fall from 1.2004 (2018 high) is part of the multi-decade down trend. Another decline is in favor after rebound from 0.9252 completes.

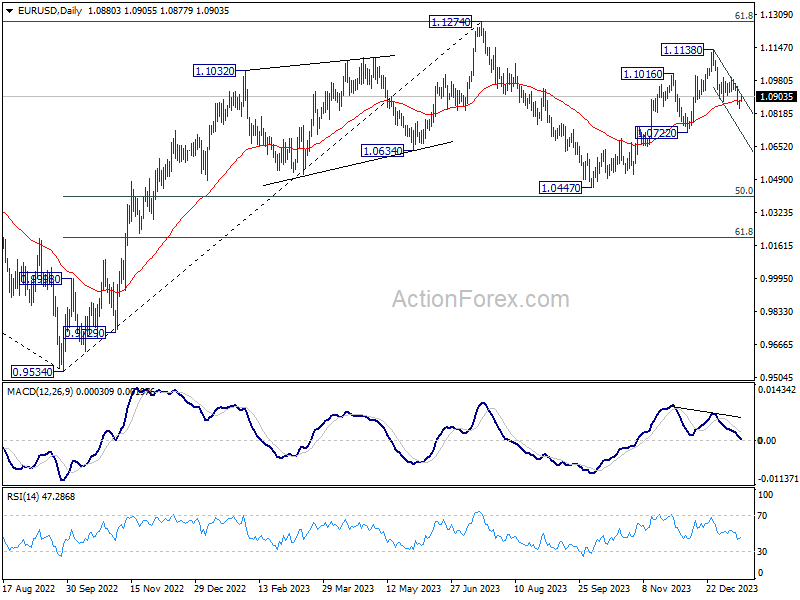

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0857; (P) 1.0870; (R1) 1.0896; More...

Intraday bias in EUR/USD is turned neutral with 4H MACD crossed above signal line. Some consolidations could be seen but further decline is expected with 1.0995 resistance intact. break of 1.0843 will resume the fall from 1.1138 to 1.0722 support. Sustained break there will argue that whole rise from 1.0447 has completed, and target this low.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and below.

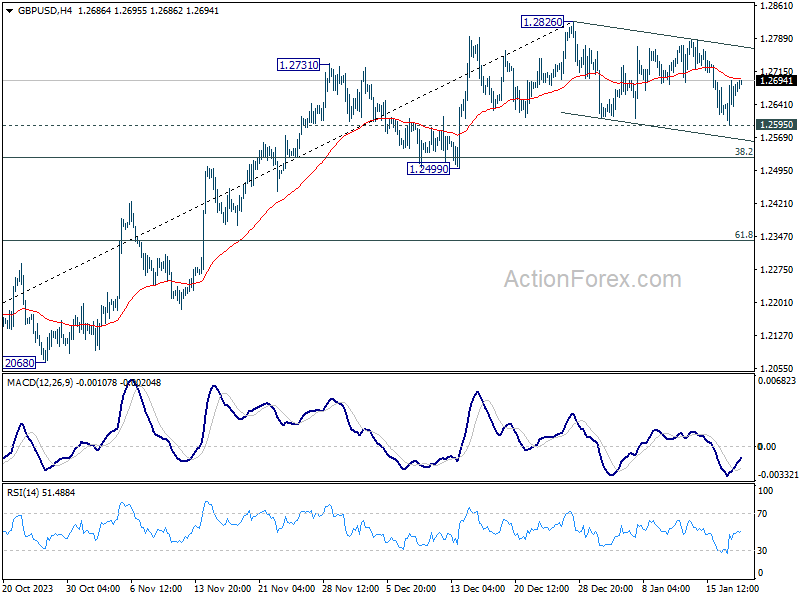

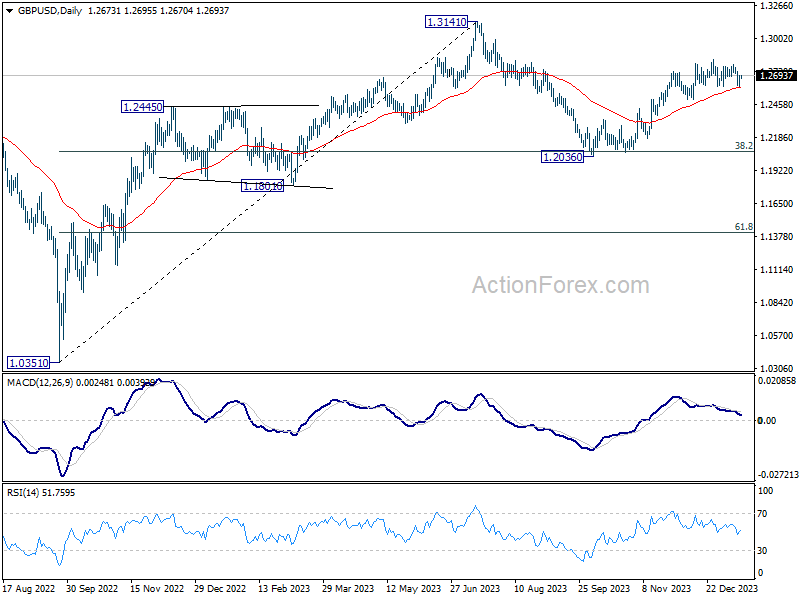

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2616; (P) 1.2656; (R1) 1.2715; More...

Intraday bias in GBP/USD remains neutral at this point. On the downside, firm break of 1.2595 support will resume the decline from 1.2826 to 1.2499 support. Nevertheless, strong rebound from current level will retain near term bullishness. Decisive break of 1.2826 will resume whole rally from 1.2036.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg that's in progress. Upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

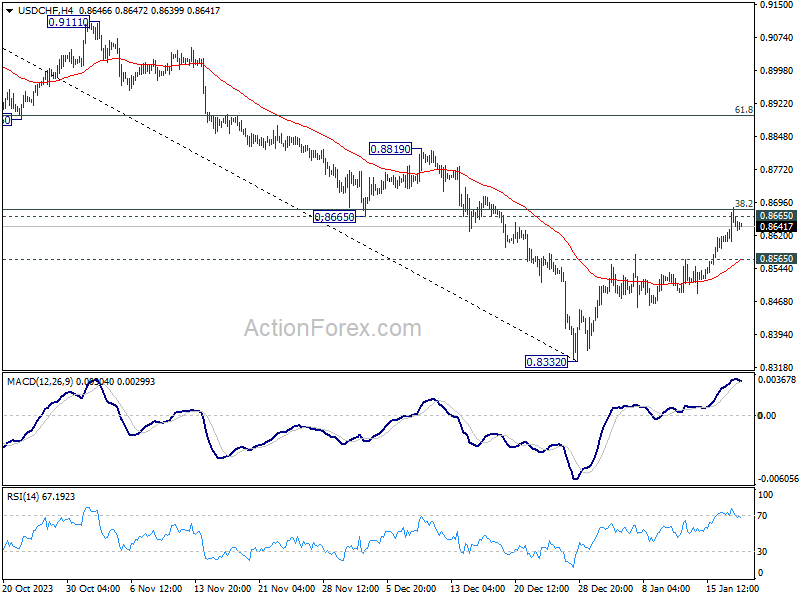

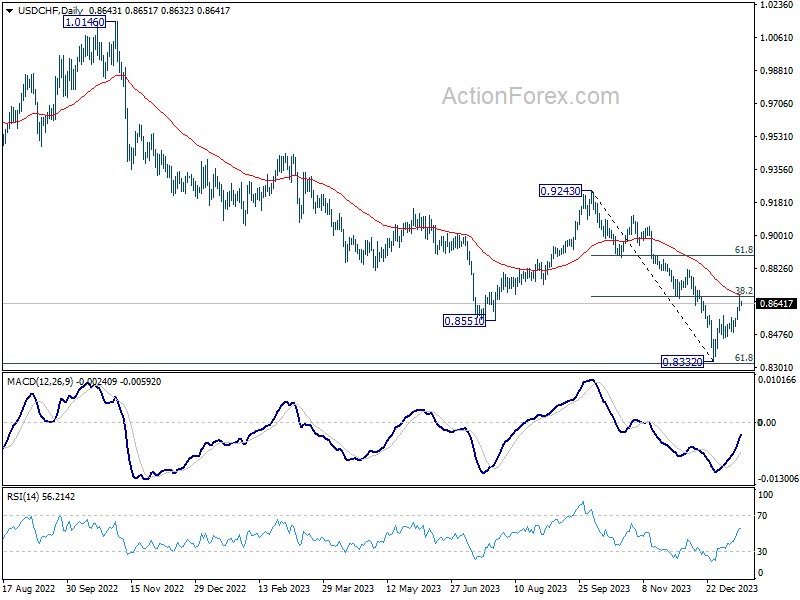

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8604; (P) 0.8645; (R1) 0.8684; More....

Focus stays on 0.8665 support turned resistance as rebound in USD/CHF. Decisive break there will turn near term outlook bullish for 61.8% retracement of 0.9243 to 0.8332 at 0.8995. Nevertheless, break of 0.8565 minor support will turn intraday bias back to the downside for retesting 0.8332 low.

In the bigger picture, outlook in USD/CHF will stay bearish as long as 0.9243 resistance holds. Larger down trend from 1.0146 (2022 high) should resume through 0.8332 low at a later stage.

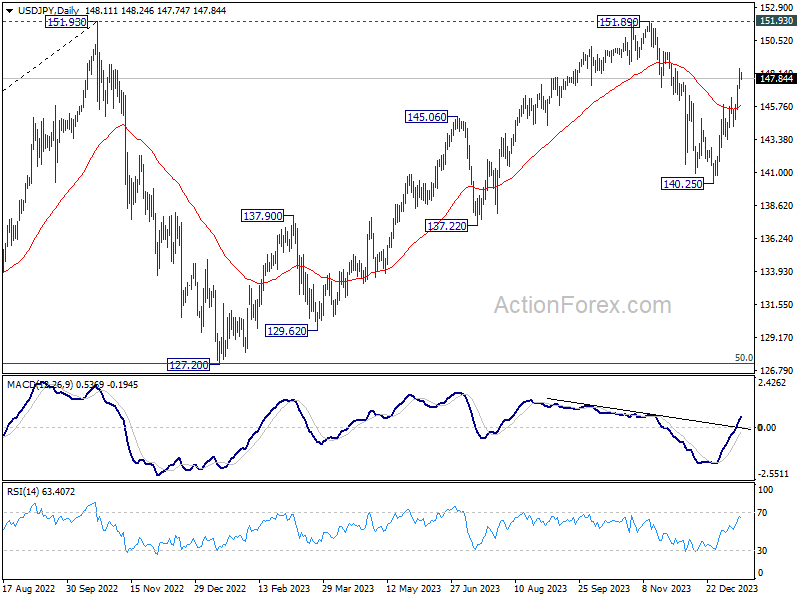

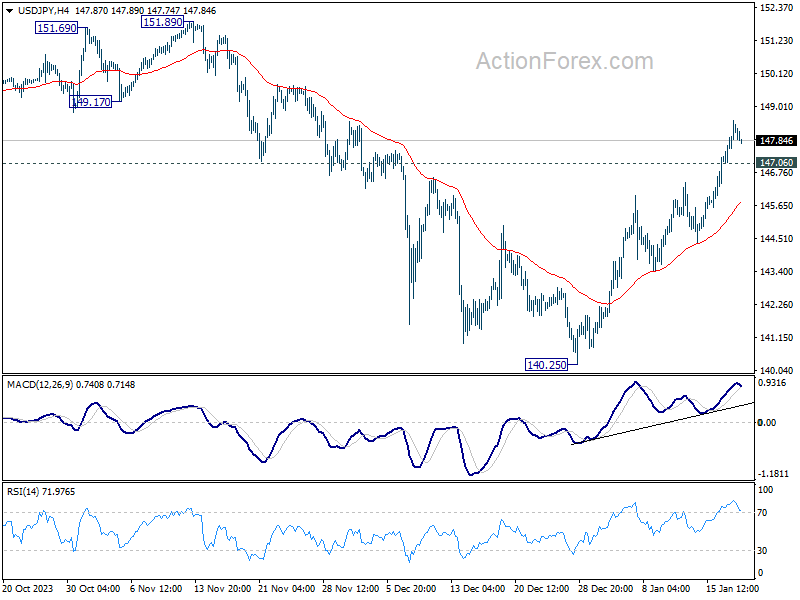

USD/JPY Daily Outlook

Daily Pivots: (S1) 147.33; (P) 147.92; (R1) 148.75; More...

Intraday bias in USD/JPY remains on the upside, as rise from 140.25 is in progress. Next target is 151.89/93 key resistance zone next. On the downside, below 147.06 minor support will turn intraday bias neutral and bring consolidations first. But further rally will remain in favor as long as 55 D EMA (now at 145.83) holds.

In the bigger picture, stronger than expected rebound from 140.25 dampened the original bearish review. Strong support from 55 W EMA (now at 141.89) is also a medium term bullish sign. Fall from 151.89 could be a correction to rise from 127.20 only. Decisive break of 151.89/93 will confirm resumption of long term up trend. This will now be the favored case as long as 140.25 support holds.