Sample Category Title

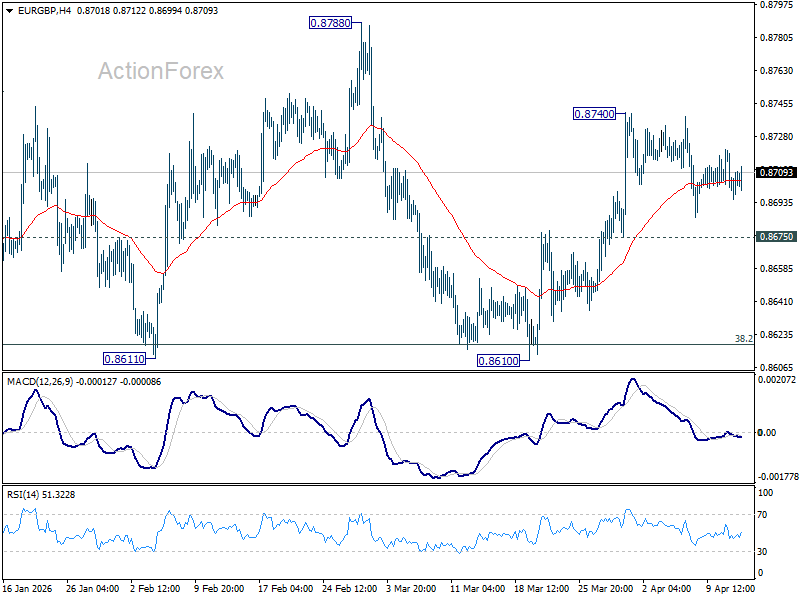

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8691; (P) 0.8711; (R1) 0.8725; More…

EUR/GBP is extending consolidation pattern from 0.8740 and intraday bias stays neutral. Further rise is mildly in favor as long as 0.8675 support holds. Break of 0.8740 will resume the rebound from 0.8610 to 0.8788 resistance. However, firm break of 0.8675 will turn bias back to the downside for retesting 0.8610 low instead.

In the bigger picture, strong support was seen again from 38.2% retracement of 0.8821 to 0.8863 at 0.8618. Break of 0.8788 resistance will argue that larger rise from 0.8221 might be ready to resume through 0.8863 (2025 high). Nevertheless, sustained trading below 0.8618 should confirm bearish reversal, and bring deeper fall to 61.8% retracement at 0.8466 at least.

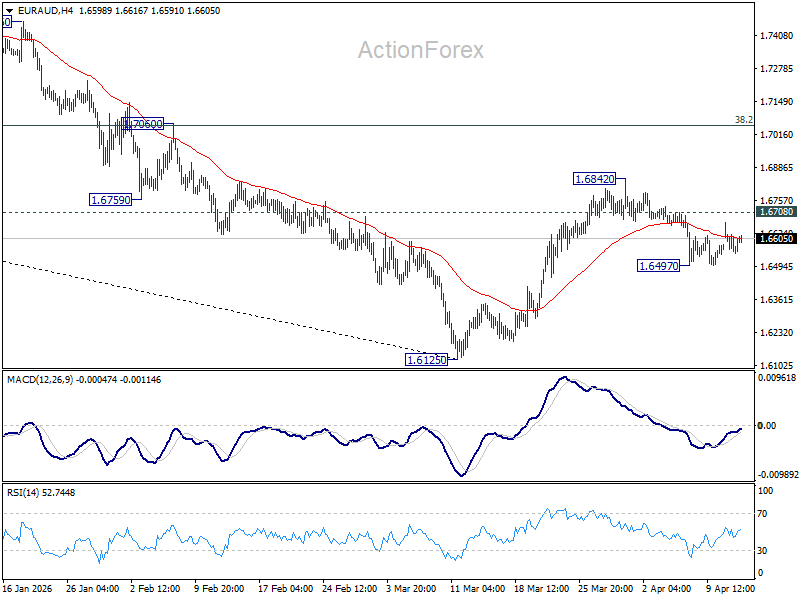

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6514; (P) 1.6607; (R1) 1.6666; More...

Intraday bias in EUR/AUD remains neutral. Outlook is unchanged that rebound from 1.6125 could have completed at 1.6842, after rejection by 55 D EMA (now at 1.6720). Below 1.6497 will bring retest of 1.6125 low first. Nevertheless, firm break of 1.6708 will should resume the rebound from 1.6125 through 1.6842 to 38.2% retracement of 1.8554 to 1.6125 at 1.7053.

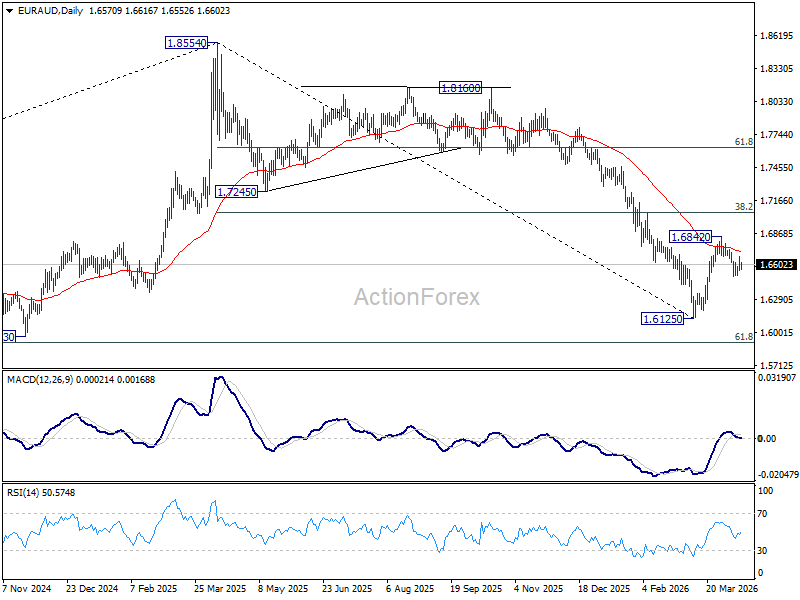

In the bigger picture, fall from 1.8554 (2025 high) is in progress and deeper decline should be seen to 61.8% retracement of 1.4281 to 1.8554 at 1.5913, which is slightly below 1.5963 structural support. Decisive break there will pave the way back to 1.4281 (2022 low). For now, risk will stay on the downside as long as 55 W EMA (now at 1.7163) holds, even in case of strong rebound.

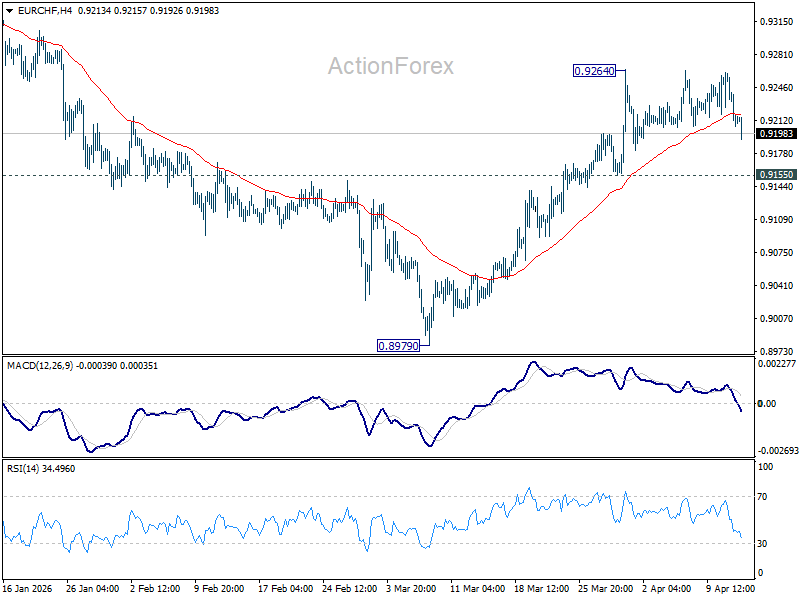

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9194; (P) 0.9231; (R1) 0.9254; More....

EUR/CHF is extending consolidation from 0.9264 with another fall, and intraday bias stays neutral. Further rise is expected with 0.9155 support intact. Firm break of 0.9264 will resume the rebound from 0.8979 to 0.9394 resistance next. However, break of 0.9155 will turn bias back to the downside for deeper pullback.

In the bigger picture, considering bullish convergence condition in W MACD, a medium term bottom should be in place at 0.8979. Sustained trading above 55 W EMA (now at 0.9281) will add more credence to this case. Further break of 0.9394 resistance will pave the way to 0.9660 resistance next. However rejection by the 55 W EMA will set up another fall through 0.8979 low at a later stage.

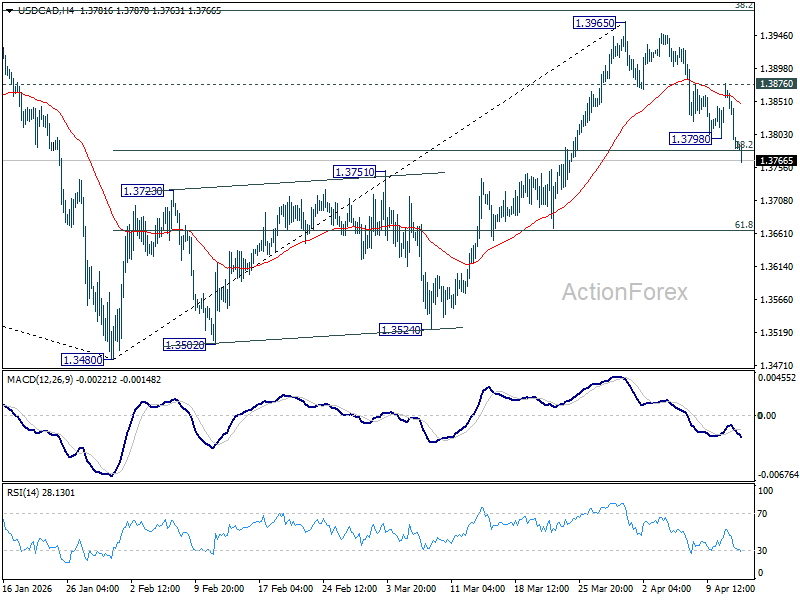

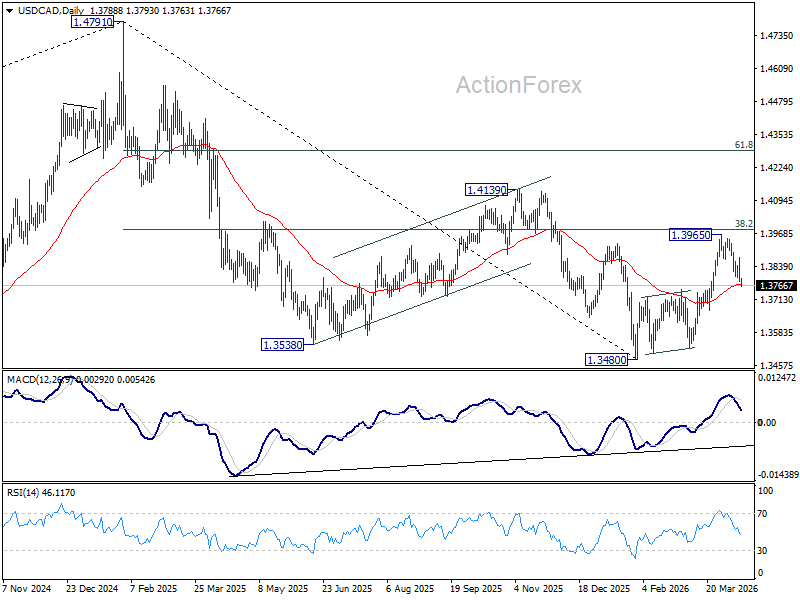

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3759; (P) 1.3819; (R1) 1.3851; More...

USD/CAD's fall from 1.3965 resumed by breaking through 1.3798 temporary low. Intraday bias is back on the downside. Sustained trading below 38.2% retracement of 1.3840 to 1.3965 at 1.3780 will argue that the rebound from 1.3840 has completed, and bring deeper decline to 61.8% retracement at 1.3665 and below. On the upside, above 1.3876 resistance will turn bias neutral again first.

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen, as the pattern extends, to 61.8% retracement of 1.2005 to 1.4791 at 1.3069. However, decisive break of 38.2% retracement of 1.4791 to 1.3480 at 1.3981 will argue that the correction has completed with three waves down to 1.3480 already. Further break of 1.4139 will confirm and bring retest of 1.4791 high.

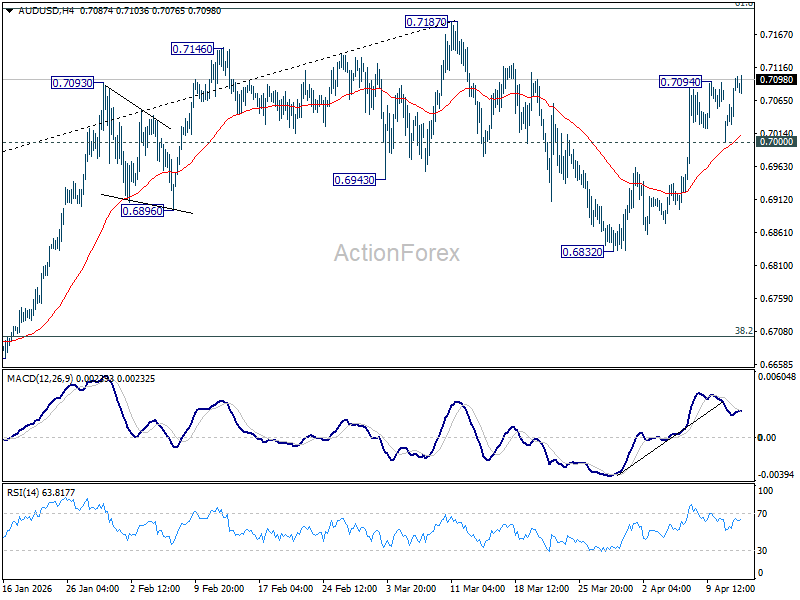

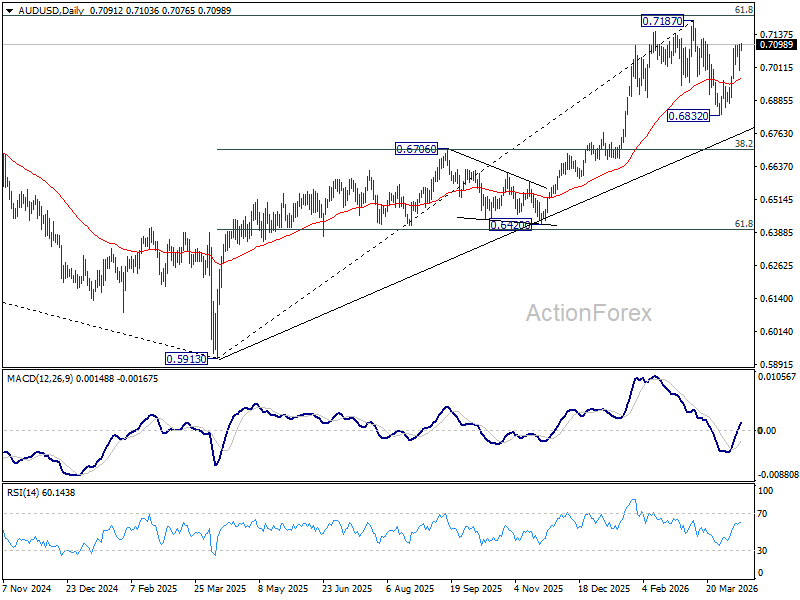

AUD/USD Daily Report

Daily Pivots: (S1) 0.7023; (P) 0.7062; (R1) 0.7136; More...

Intraday bias in AUD/USD is back on the upside with break of 0.7094 temporary top. Rebound from 0.6832 is resuming for 0.7187 high. Strong resistance could be seen there on first attempt. On the downside, below 0.7000 support will turn intraday bias neutral again first.

In the bigger picture, as long as 0.6706 cluster support holds, rise from 0.5913 (2024 low) should still be in progress. Decisive break of 61.8% retracement of 0.8006 to 0.5913 at 0.7206 will solidify the case that it's already reversing the down trend from 0.8006 (2021 high). However, firm break of 0.6706 will dampen this bullish case, and bring deeper fall back to 0.6420 support, and possibly below.

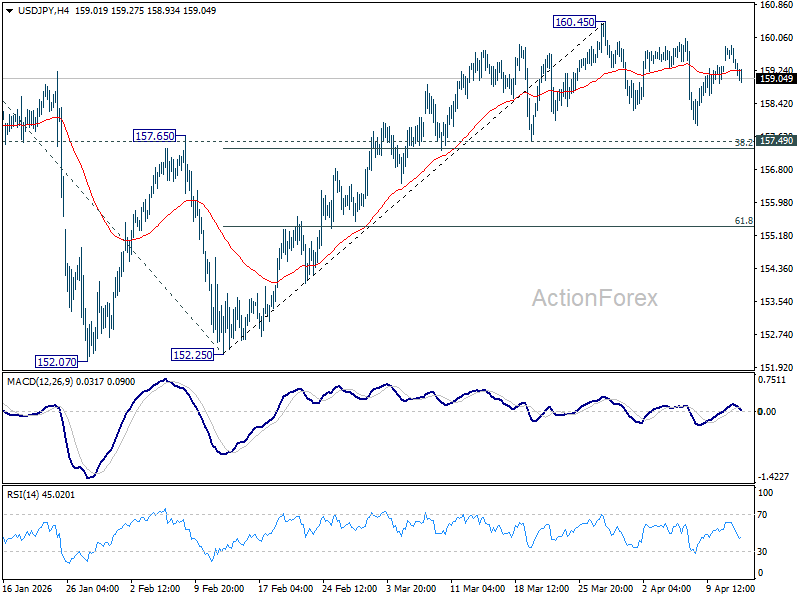

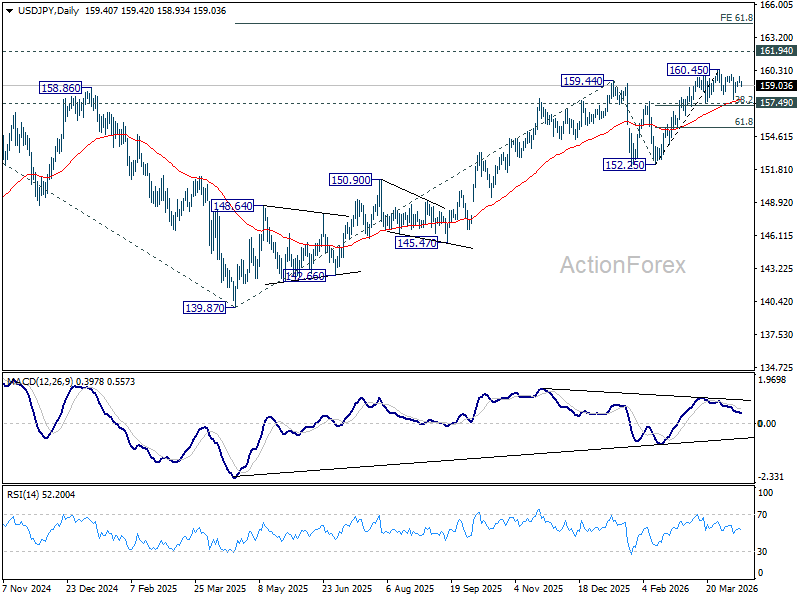

USD/JPY Daily Outlook

Daily Pivots: (S1) 159.21; (P) 159.53; (R1) 159.78; More...

USD/JPY is still extending consolidations from 160.45 and intraday bias remains neutral. Outlook will stay bullish as long as 157.49 cluster support (38.2% retracement of 152.25 to 160.45 at 157.31) holds. On the upside break of 160.45 will target a retest on 161.94 high. However, firm break of 157.31/49 will bring deeper fall back to 61.8% retracement at 155.38 next.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 155.24) holds. Firm break of 161.94 will pave the way to 61.8% projection of 102.58 to 161.94 from 139.87 at 176.75.

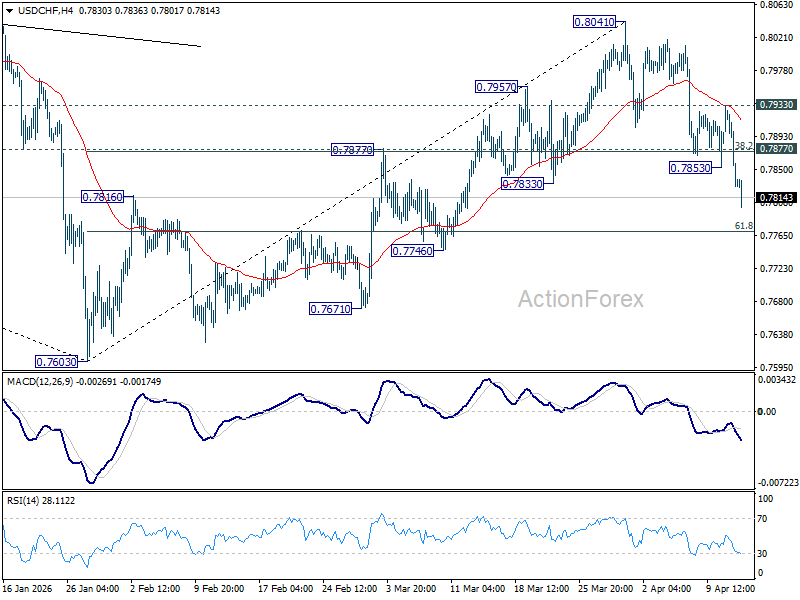

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7801; (P) 0.7867; (R1) 0.7906; More….

USD/CHF's fall from 0.8041 resumed by breaking through 0.7853 temporary low and intraday bias is back on the downside. Rebound from 0.7603 should have completed. Deeper decline should be seen to 61.8% retracement of 0.7603 to 0.8041 at 0.7770 . Firm break there will bring retest of 0.7603 low. For now, risk will stay on the downside as long as 0.7933 resistance holds, in case of recovery.

In the bigger picture, rebound from 0.7603 medium term bottom is seen as correcting the fall from 0.9200 only. Rejection by 55 W EMA (now at 0.8071) will affirm this bearish case, and setup down trend resumption to 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382 at a later stage. Though, sustained break of 55 W EMA will suggest that it's probably correcting the larger scale down trend from 1.0146 (2022 high).

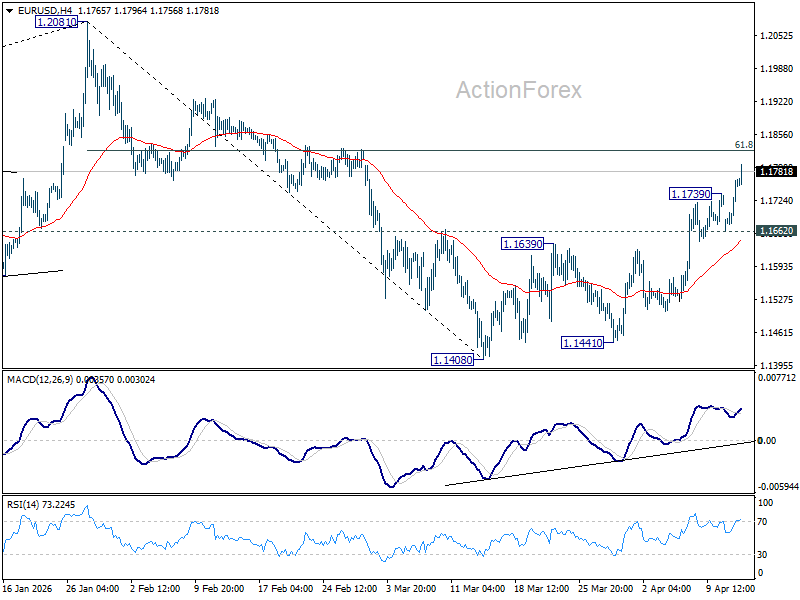

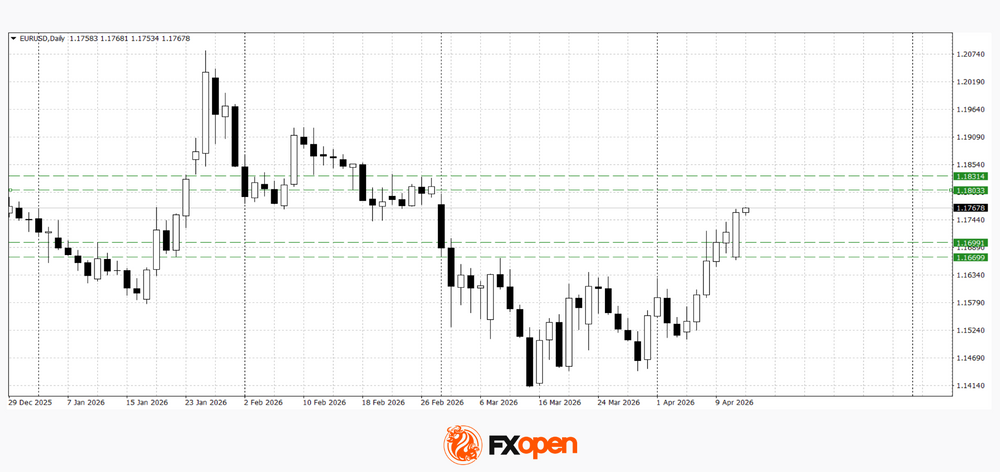

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1694; (P) 1.1729; (R1) 1.1795; More….

EUR/USD's rise from 1.1408 resumed after brief consolidations. Intraday bias is back on the upside for 61.8% retracement of 1.2081 to 1.1408 at 1.1824. Decisive break there will pave the way to retest 1.2081 high. For now, further rally will remain in favor as long as 1.1662 support holds, in case of retreat.

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1513). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.

European Currencies Advance Amid Shifting Geopolitical Outlook

The initial rise in EUR/USD and GBP/USD was driven by reports of a temporary ceasefire between the United States and Iran, which reduced demand for the US dollar as a safe-haven asset. However, over the weekend, reports emerged that negotiations had stalled, leading to a bearish gap at the start of the new trading week. Subsequently, rumours of a possible resumption of dialogue once again shifted market sentiment, restoring interest in risk-sensitive assets.

This supported a swift recovery in the euro and the pound, while also increasing pressure on the US dollar. Additional downside pressure on the dollar comes from declining Treasury yields and a reassessment of expectations regarding the Federal Reserve’s monetary policy, which continues to limit the upside potential of the US currency.

Market attention today will focus on upcoming macroeconomic releases from the euro area and the United States, including producer inflation (PPI), business activity data, and speeches from Federal Reserve officials. These factors may adjust current interest rate expectations and influence the dollar’s short-term trajectory.

EUR/USD

The pair continues to move higher following a breakout from last week’s consolidation range. The week opened with a price gap, but after a retest of support at 1.1660, the pair quickly recovered above 1.1700. Technical analysis suggests the potential for further gains towards the 1.1800–1.1830 area. However, any negative developments in US–Iran negotiations could trigger a sharp pullback towards 1.1700–1.1660.

Key events for EUR/USD:

- today at 10:00 (GMT+3): Spain HICP

- today at 15:30 (GMT+3): US Producer Price Index (PPI)

- today at 20:00 (GMT+3): speech by Bundesbank representative Balz

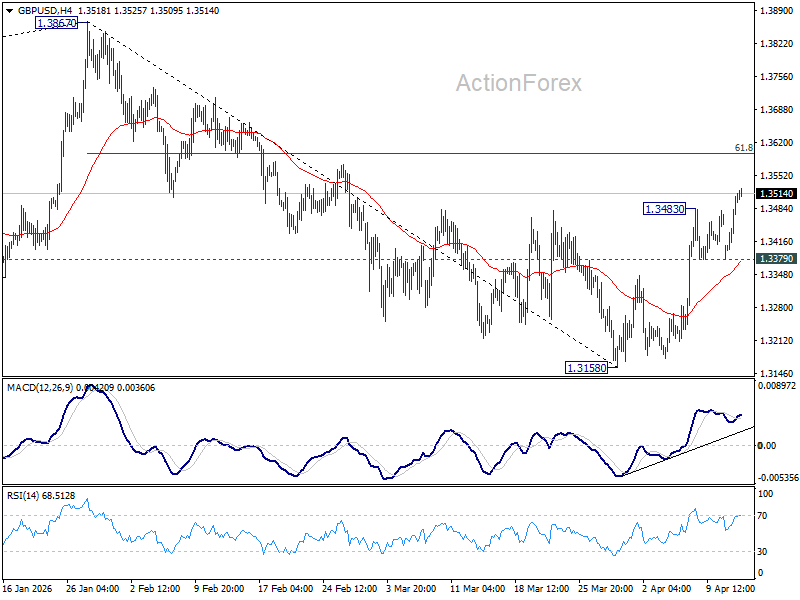

GBP/USD

The pair is showing a similar pattern, largely mirroring the euro’s dynamics. Following the overnight gap, the price managed to break above last week’s highs and test key resistance at 1.3500. Technical analysis points to a possible move towards 1.3570–1.3600. In case of a pullback, a retest of recent levels near 1.3450–1.3470 is possible.

Key events for GBP/USD:

- today at 11:50 (GMT+3): speech by Bank of England MPC member Mann

- today at 19:00 (GMT+3): speech by Bank of England Governor Bailey

- today at 19:45 (GMT+3): speech by Federal Reserve Vice Chair for Supervision Michael S. Barr

Overall, European currencies maintain an upward bias amid an unstable geopolitical environment and declining US yields. However, the current rally remains highly sensitive to developments in the negotiation process, increasing the likelihood of short-term volatility. The next directional move in EUR/USD and GBP/USD will depend on both geopolitical signals and incoming macroeconomic data.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips (additional fees may apply). Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

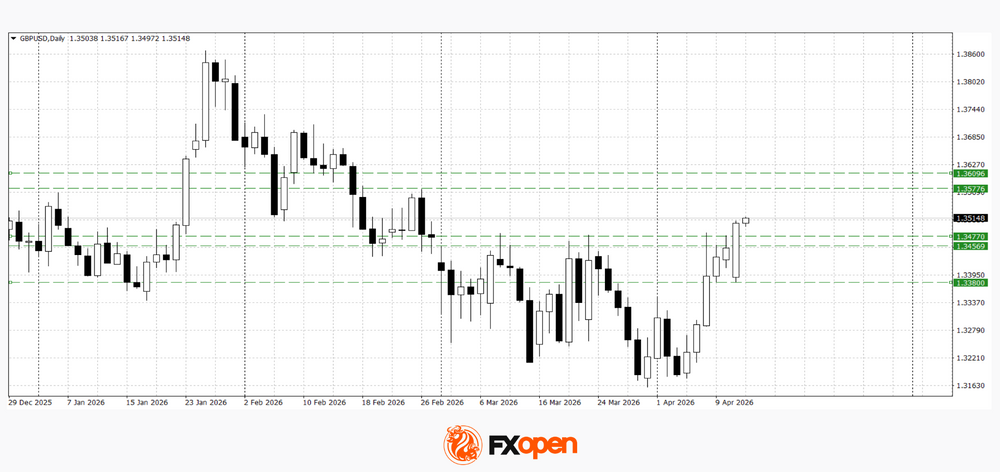

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3422; (P) 1.3466; (R1) 1.3551; More...

GBP/USD's rebound from 1.3158 resumed after brief consolidations. Intraday bias is back on the upside for 61.8% retracement of 1.3867 to 1.3158 at 1.3596. Firm break there will bring retest of 1.3867 high. For now, further rally will remain in favor as long as 1.3379 support holds, in case of retreat.

In the bigger picture, current development suggests that price actions from 1.3867 are merely a corrective pattern within the broader up trend from 1.0351 (2022 low). With 1.3008 support intact, medium term bullishness is maintained and break of 1.3867 is back in favor for a later stage, towards 1.4248 key resistance (2021 high).