Sample Category Title

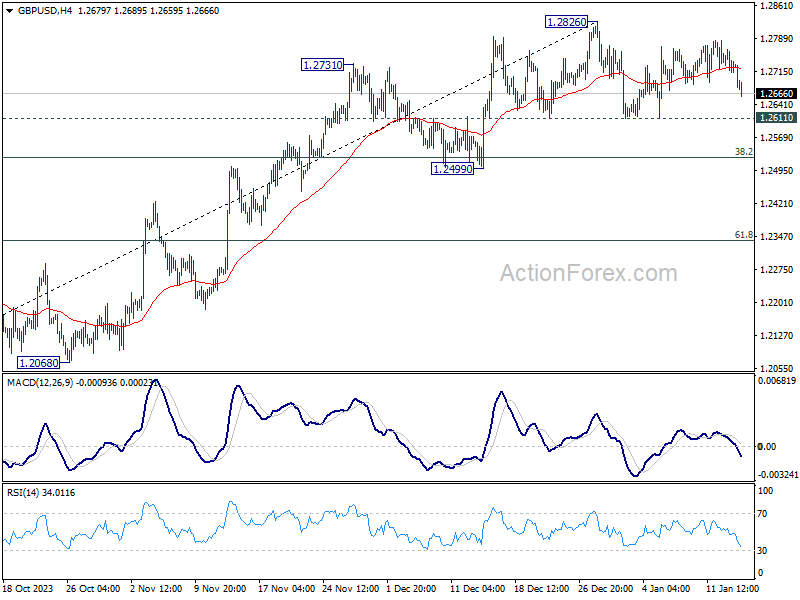

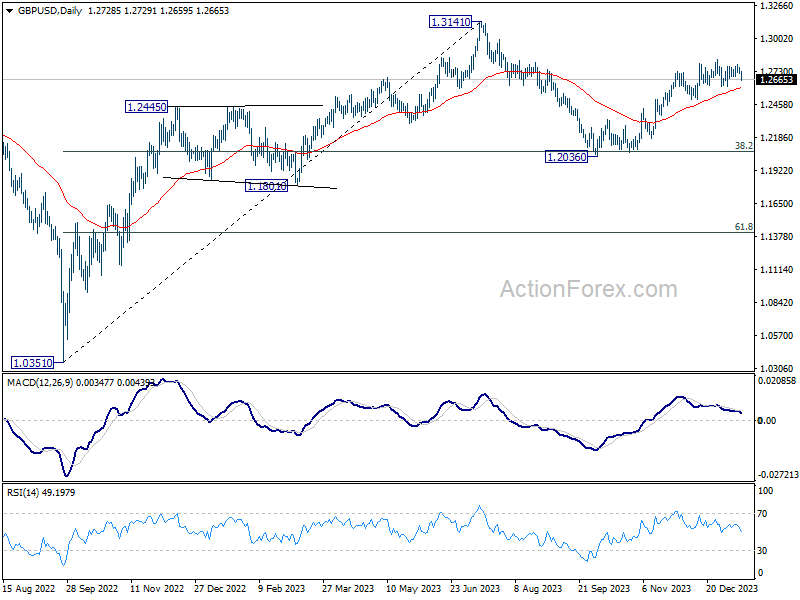

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2705; (P) 1.2735; (R1) 1.2758; More...

GBP/USD is staying in range of 1.2611/2826 despite today's decline. Intraday bias remains neutral first. On the upside, decisive break of 1.2826 will resume whole rally from 1.2036. Nevertheless, break of 1.2611 will bring deeper decline to 1.2499 support instead.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg that's in progress. Upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

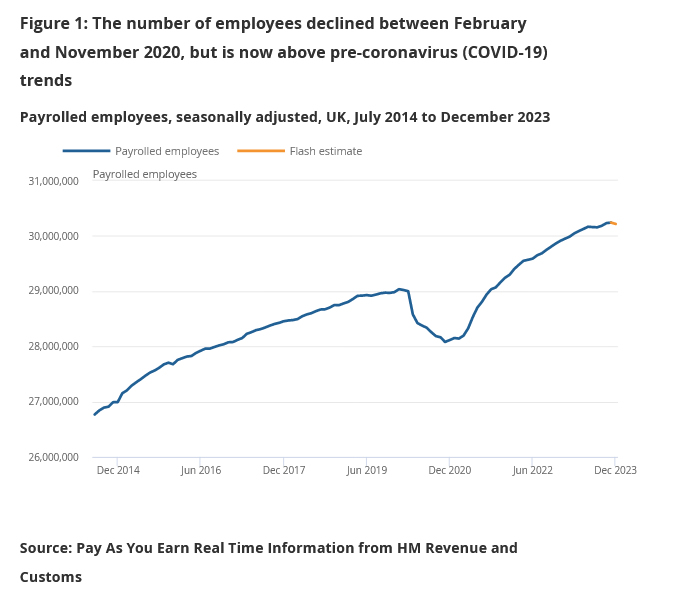

UK payrolled employment falls -24k in Dec, unemployment rate at 4.2% in Nov

UK payrolled employment fell -0.1% mom, or -24k in December. Annual growth in employees fell from 1.3% yoy to 1.0% yoy. Median monthly pay increased by 6.6% yoy, up from prior month's 6.5% yoy. Claimant count rose 11.7k, below expectation of 18.1k.

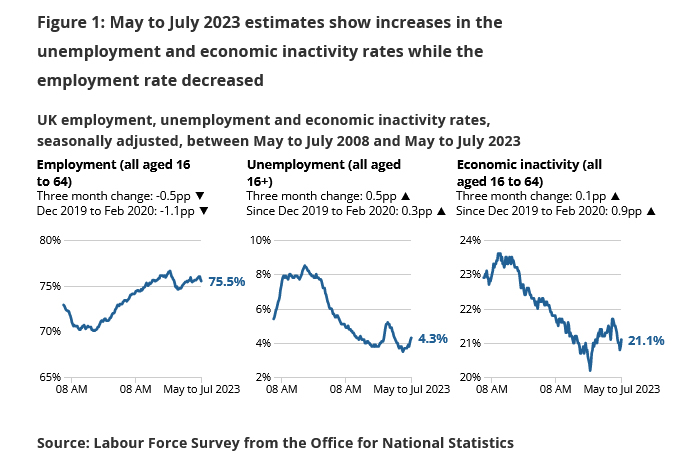

In three months to November, unemployment rate rose to 4.2%, up 0.5% from the previous three month period. Employment rate fell to 75.5%, down -0.5%. Total weekly hours also fell -18.5 to 1040. Average earnings excluding bonus slowed from 7.3% 3moy to 6.6%, matched expectations. Average earnings including bonus fell from 7.2% 3moy to 6.5%, below expectation of 6.8%.

WTI Oil Technical: Sideways Within a Potential Minor Bottoming Configuration

- Ongoing hostilities in the Middle East region and the Red Sea shipping route have put a potential “floor” in oil prices due to the increasing risk of supply disruptions.

- The demand side has remained weak as China’s top policymakers have signalled a less forceful approach in enacting stimulus measures after PBoC left its 1-year MLF rate unchanged at 2.50%.

- Sideways for now between US$76.05/78.40 and US$69.20 for WTI crude oil.

Since our last report, the price actions of West Texas Oil (a proxy of WTI crude oil futures) have managed to trade above its 13 December 2023 low of US$67.82/barrel and whipsawed around the 20-day moving average in the past two weeks.

Conflicting fundamental factors

There are no clear catalysts to determine whether the bulls or bears are leading the oil market as conflicting factors are at play, thus causing a flux situation at this juncture.

On the positive side that is supporting oil prices is the rising geopolitical risk premium in the Middle East region that could potentially disrupt the oil supplies. The odds are high for an increase in hostilities in the Red Sea shipping route where Yemen’s Houthi militants are showing no signs of backing down in attacking registered ships from Israel and its allies, primarily the US in the Red Sea despite the recent joint counter strikes from US and UK to neutralize these threats.

In addition, Iran, a key stakeholder in the Middle East has started to play a bigger military role in terms of showing its displeasure in the ongoing war between Israel and Hamas by mounting an attack yesterday on Israel’s spy HQ in Iraq as reported by various media outlets.

On the flipside, the demand side narrative for oil remains weak as China’s central bank, PBoC has disappointed market participants by keeping one of its key benchmark interest rates unchanged; the 1-year medium-term lending (MLF) rate was held at 2.5% since August 2023.

This latest monetary policy move from PBoC has signalled that Chinese top policymakers are in no rush to enact more “pronounced” stimulus measures to negate the deflationary risk spiral in China, thus dampening the mood of short-term bullish animal spirits in the oil market.

Potential minor bottoming for WTI crude

Fig 1: West Texas Oil medium-term trend as of 16 Jan 2024 (Source: TradingView, click to enlarge chart)

In the lens of technical analysis, the recent steep drop of -15% of WTI crude from 30 November 2023 to 13 December 2023 has managed to stall at the medium-term ascending trendline support in place since the 20 March 2023 swing low of US$64.21. In addition, it has formed a “higher low” in the past four weeks.

The key resistance of this potential minor bottoming formation stands at US$76.05/78.40 which confluences with 50-day and 200-day moving averages that are acting as price caps as well.

Therefore, in the short to medium term, WTI crude is likely to trade sideways between US$78.40 and US$69.20 (the ascending trendline from the 20 March 2023 low) due to conflicting fundamental factors. Only a clearance above US$78.40 may ignite a more impulsive upmove sequence to see the next medium-term resistances coming in at US$83.20 and US$93.80.

On the other hand, failure to hold at US$69.20 sees a slide to retest the first major support zone at US$67.55/66.35.

Calling a Spade, a Spade

I sense that the first quarter of this year will be marked by the realization that it’s too early for the central banks to cut the interest rates unless something really bad – like another bank crisis, or a real estate crisis, or another debt crisis hits the fan. Because March – where market prices reflect the first rate cuts from both the Federal Reserve (Fed) and the European Central Bank (ECB) - is about two months away, and things don’t look *that* bad.

In Europe, growth is slowing, Germany is struggling to reverse slow down, the slump in the Eurozone’s industrial production accelerated, and production fell 6.8% in November from a year earlier. Over the last 9 readings, only one came in positive, and it was a small 0.2% growth back in June. But economic slowdown is what the ECB needs to pull inflation lower. And unless there is a sharp slowdown in economic activity, the ECB won’t hurry up to cut rates. On the contrary, the bank is now focused on waning the pandemic era aid programs. And according to a recent Bloomberg survey, the ECB will make four 25bp cuts this year starting in June instead of six rate cuts starting from April – as priced in by the markets.

In the US, the resilient growth, healthy jobs market and sustained fiscal spending into the presidential election suggest no urge for a Fed cut in March.

The divergence between the reason and market pricing suggests that the rate cut expectations will be gently delayed and pricing will be revisited.

If that’s the case, stock and bond markets should correct to the downside, and the US dollar should recover.

Calling a spade, a spade

The US dollar kicked off this week on a positive note, as the EURUSD made a swift move to the downside following ECB Holzmann’s words in Davos yesterday. Holzmann warned that the threats from looming inflation will likely prevent the ECB from lowering the rates this year, even as a recession can no longer be ruled out. He pointed at the conflict in the Middle East as a risk for further disruption to supply chains and energy markets and cautioned that the latter developments will likely keep ECB alert regarding the price risks. The euro fell and the Stoxx 600 retreated.

One thing that prevents inflation worries from darkening the mood is the subdued reaction from oil markets. The escalation of the conflict in the Red Sea region no longer fuels oil prices. Despite news of further attacks and retaliation, US crude saw limited upside yesterday and closed the session slightly lower. Resistance remains intact into $75pb level.

But if inflation worries resurface, weak economic data will no longer fuel the central bank doves and act as good news.

The EURUSD has potential to fall further. The next natural target for the euro bears stands at 1.0875, the major 38.2% Fibonacci retracement on the latest rebound that started in October. Below this level, the EURUSD will step into the medium-term bearish consolidation zone. Cable could return below 1.25, and the USDJPY could make an attempt on the 100-DMA – near 147.40. But the consensus for the USDJPY remains bearish as the Bank of Japan (BoJ) should exit the negative rate policy. Japanese policymakers could be further encouraged to act in case of strong annual wage-negotiation results.

Trump Wins Iowa Caucus

In focus today

Today, focus is on German ZEW data for January and final inflation figures for December. The final HICP figures include details on inflation components that will provide important information about the underlying inflationary pressure in the largest euro area economy.

While the official labour force statistics continue to be postponed, today we get the experimental estimates for November/December at 8:00 CET. Key will be developments in wage growth, which is highly determining of service inflation. Other surveys point to a further easing in wage growth although the loosening of the labour market appears to lose steam.

In Norway November GDP numbers for the mainland is released at 08:00 CET. We expect the number to come in at -0.2% m/m.

Fed's Waller speaks at 17:00 CET.

In the US, markets will resume trading after being closed for Martin Luther King Day on Monday.

Early Wednesday morning (03:00 CET) China releases GDP on top of the monthly batch of data. GDP growth is expected to be 1.0% q/q down from 1.3% q/q in Q4 which would result in a rise in the annual growth rate from 4.9% to 5.2%. It would imply an average growth rate for the year at 5.2% and thus above the government's 5% target. More interesting will be Chinese data on home sales and retail sales. Home sales are still very depressed leaving no sign of a bottom in the housing crisis. Retail sales have been solid in November growing 10.1% y/y but expected by consensus to drop to around 8%. It is crucial that consumption growth stays afloat for China to continue a growth path around 5% in 2024.

Economic and market news

What happened overnight

In the US, former president Donald Trump expectedly won the Iowa caucus, thus bringing him one step closer to getting on the Republican ticket for the presidential election this November. The Trump victory was highly anticipated in prediction markets. Ron DeSantis came second narrowly ahead of Nikki Haley. Third runner-up Vivek Ramaswamy chose to withdraw from the primaries and endorse Trump, thus giving the former president even more support in his endeavours to secure the Republican nomination.

In Asia, Japanese wholesale inflation for December came out higher than expected at 0.3% m/m and 0.0% y/y. Consensus was expecting it to land at 0.0% m/m and -0.3% y/y. The surprise in the corporate goods inflation comes ahead of Friday's nationwide Japanese December CPI release.

Swedish unemployment increased from 6.5% in November to 6.7% in December according to new data released by the Swedish Public Employment Service (SPES) this morning. This number can be compared to an unemployment rate of 6.6% back in December 2022 and shows that the unemployment is remaining at stable and relatively low levels. Danske Bank expects a modest increase in Swedish unemployment during 2024.

What happened yesterday

In Sweden, inflation surprised to the upside with the nominal CPIF coming in at 2.3% and CPIF ex energy coming in at 5.3%, both y/y. Clothing and furniture appeared to be the primary causes behind the upside surprise, both rising much more than expected. Despite the higher than expected December print, inflation remains below the most recent Riksbank forecast.

German GDP numbers showed the economy shrank by 0.3% in 2023. The preliminary GDP numbers (official quarterly data are released in two weeks) for the Q4 came in at -0.3% q/q, whereas Q3 was revised up from -0.1% q/q to 0.0% q/q. The manufacturing sector has weighed increasingly heavy on the economy in Q4 according to IFO data and the construction sector has continued its increasingly steeper slide into recession.

Manufacturing recession: In the euro area, weak soft data also translates into weak hard data with industrial production down 0.3% m/m in November as expected. This compares to a decline in October of 0.7% m/m.

ECB: At the World Economic Forum in Davos, Robert Holzmann, hawkish member of the ECB Governing Council, made it clear he deemed it prematurely to speak of rate cuts, saying he "may even foresee no cut at all this year".

In energy markets the Dutch natural gas benchmark the TTF, widely recognised as the most prominent natural gas benchmark in Europe, dropped below €30/MWh due to EU natural gas storages sitting at around 80%. This storage level is close to a record-high for this time of year, albeit slightly lower than the corresponding level in 2023, hence market sentiment has begun leaning towards Europe making it rather comfortably through the winter despite cold weather. By session end the TTF stood at €30.5/MWh.

Red Sea: The on-going conflict between the Iran-backed Houthis and the US led naval contingent in the Red Sea is still at the centre of attention in crude markets. A US owned dry bulk carrier ship was hit by a missile off Yemen. The Houthi movement responsible for the attack followed up with a statement saying they would now target all American ships. Several oil tankers diverted routes to avoid the Red Sea. QatarEnergy announced they would also seize passing through the Red Sea. Despite the continued tension in the Red Sea oil retracted slightly in yesterday's trading session, with Brent settling at USD78.15/barrel.

Equities: Global equities were mostly lower yesterday with US closed for Martin Luther King Day. Sentiment kept sliding throughout the day and the appetite for risk continues to drop this morning in Asian and western futures. No big sector or style rotation but rather a broad-based sell-off with energy sector doing marginally better than the rest. Japan stood out yesterday as well and is 5% ahead of other markets year-to-date as yen has weakened on the back of a dovish turn in central bank expectations.

FI: Yields rose across the board on the first trading session of the week, reversing some of the decline last Friday. 10Y UST yields ended 6bp higher, while 10Y Bund yields rose 5bp. The pricing of rate cuts from the ECB in 2024 fell from 156bp to 150bp during the session. The Bund ASW-spread continued to tighten, while peripheral spreads were slightly wider. Overnight, oil prices have gained some tailwinds on the back of yesterday's Houthi attack on a US-owned commercial vessel in the Red Sea.

FX: The week has started relatively quietly in the G10 FX space with the US market closed yesterday. EUR/USD remains in the mid 1.09-1.10 range, while the JPY traded weak, driving USD/JPY above 145 and EUR/JPY closer to 160. EUR/GBP hovers around 0.86. In the Scandies space, both EUR/NOK and EUR/SEK drifted above 11.30.

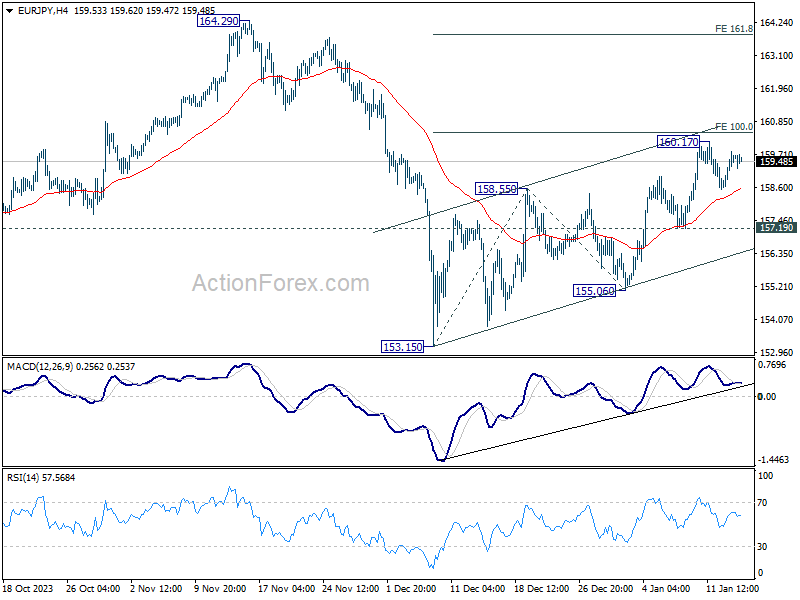

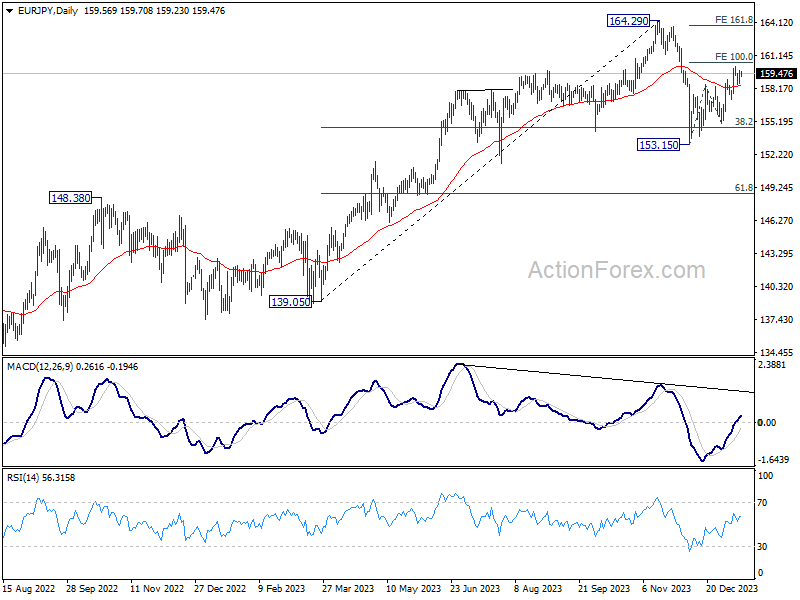

EUR/JPY Daily Outlook

Daily Pivots: (S1) 158.88; (P) 159.35; (R1) 160.10; More...

Range trading continues in EUR/JPY and intraday bias remains neutral. Further rise is mildly in favor as long as 157.19 minor support holds. Firm break of 100% projection of 153.15 to 158.55 from 155.06 at 160.46 will pave the way to 161.8% projection at 163.79. However, break of 157.19 support will argue that the rebound has completed, and turn bias back to the downside.

In the bigger picture, price actions from 164.29 medium term top are tentatively seen as a correction to rise from 139.05 for now. As long as 148.48 resistance turned support holds (2022 high), larger up trend from 114.42 (2020 low) could still resume through 164.29 at a later stage.

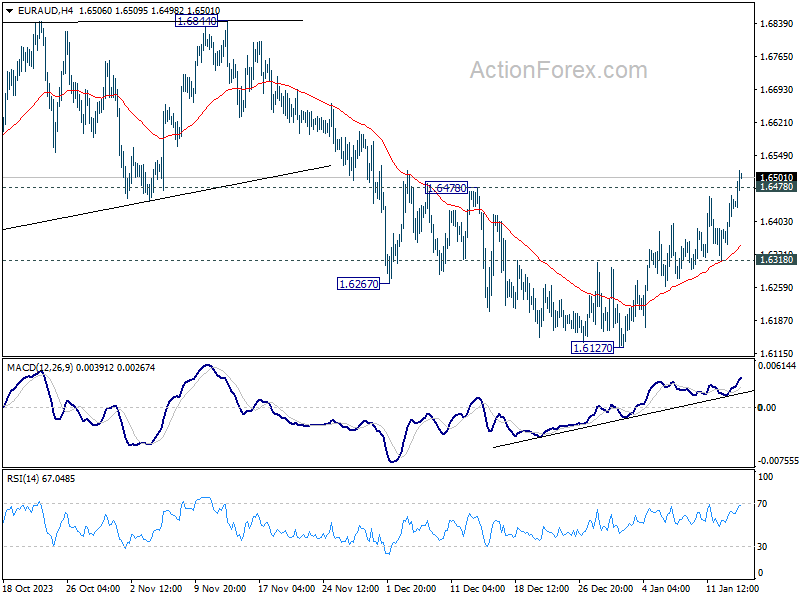

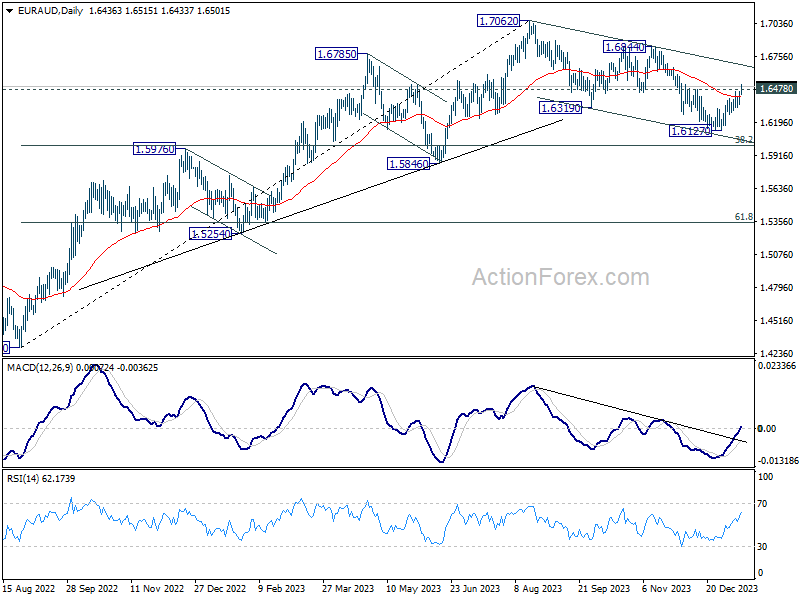

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6377; (P) 1.6421; (R1) 1.6486; More...

EUR/AUD's rebound from 1.6127 resumed and the break of 1.6478 resistance argues that whole correction from 1.7062 has completed. Intraday bias is back on the upside for 1.6844 resistance for confirmation. For now, further rally is expected as long as 1.6318 support holds, in case of retreat.

In the bigger picture, fall from 1.7062 medium term top is seen as correction to the up trend from 1.4281 (2022 low). Strong support should be seen around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 bring rebound. Break of 1.6844 will argue that this up trend is ready to resume through 1.7062 high.

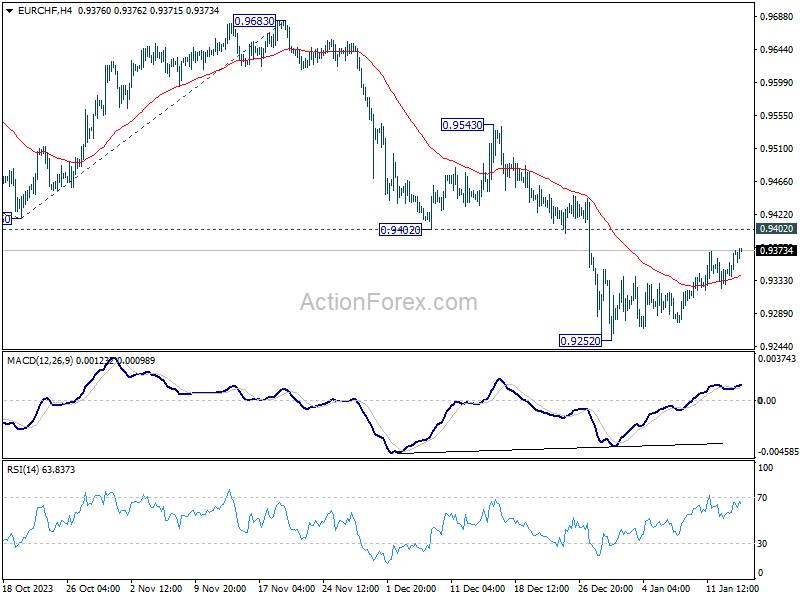

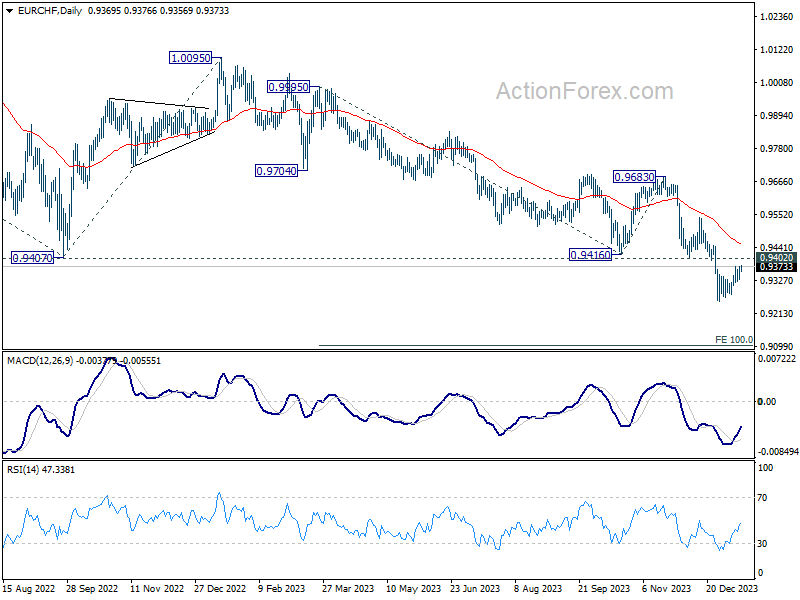

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9338; (P) 0.9359; (R1) 0.9391; More...

No change in EUR/CHF's outlook as price actions from 0.9252 are seen as a consolidation pattern only. Intraday bias remains neutral and outlook stays bearish with 0.9402 support turned resistance intact. On the downside, break of 0.9252 will resume larger down trend to 100% projection of 0.9995 to 0.9416 from 0.9683 at 0.9104 next. However, firm break of 0.9402 will dampen this view, and turn bias back to the upside for 0.9543 resistance instead.

In the bigger picture, medium term outlook remains bearish as long as 0.9683 resistance holds. Current fall from 1.2004 (2018 high) is part of the multi-decade down trend. Next target is 61.8% projection of 1.1149 (2020 high) to 0.9407 from 1.0095 at 0.9018.

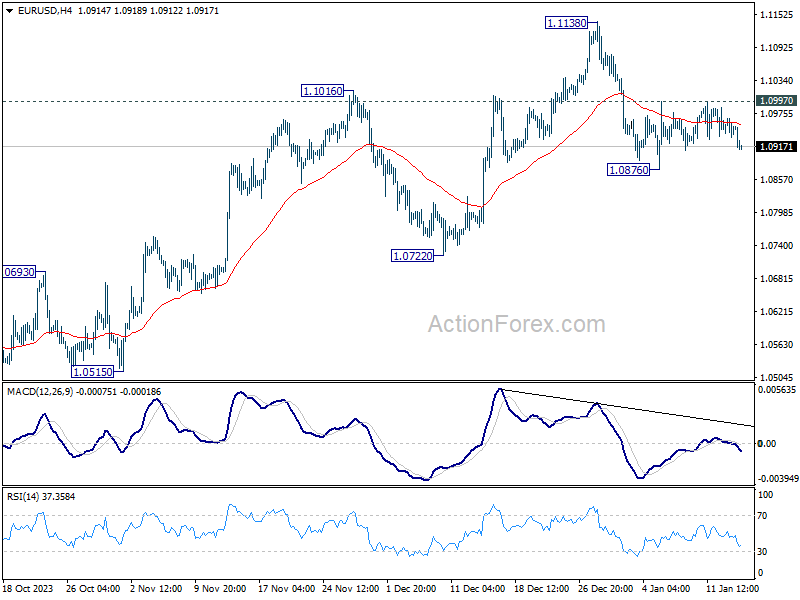

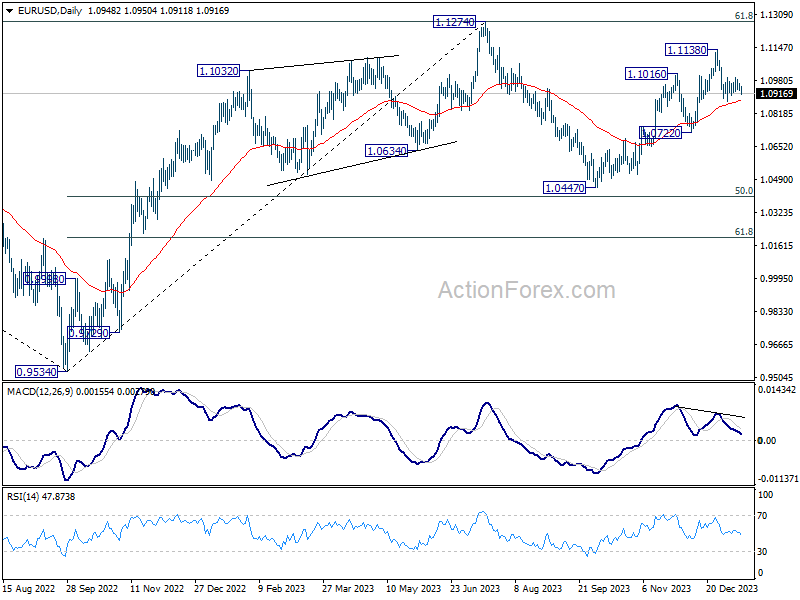

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0934; (P) 1.0951; (R1) 1.0968; More...

EUR/USD is still bounded in range above 1.0876 despite today's decline. Intraday bias stays neutral for the moment. Further fall is in favor as long as 1.0997 minor resistance intact. Break of 1.0876 will resume the fall from 1.1138 to 1.0722 support next. Nevertheless, firm break of 1.0997 will turn bias back to the upside for retesting 1.1138 high instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and below.

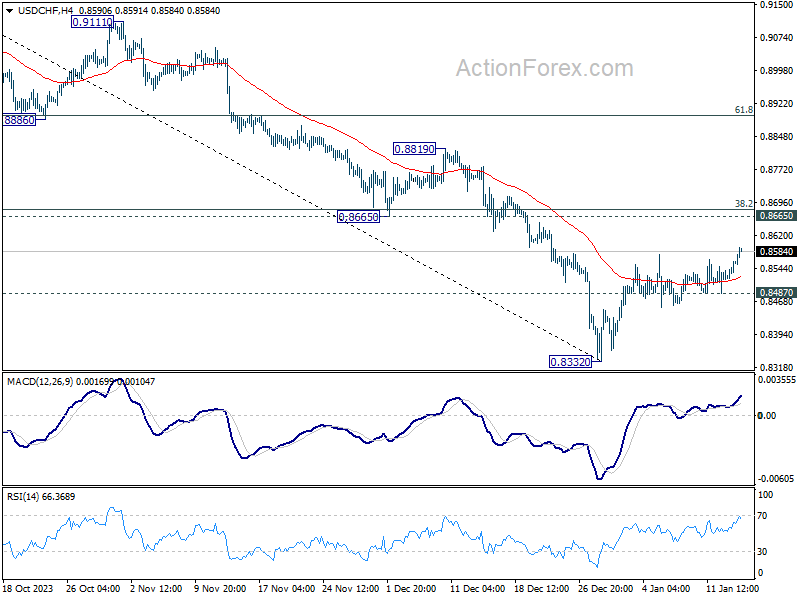

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8526; (P) 0.8547; (R1) 0.8579; More....

While USD/CHF's rebound could extend higher, overall outlook will stay bearish as long as 0.8665 support turned resistance holds. On the downside, break of 0.8487 minor support will bring retest of 0.8332 low first. However, decisive break of 0.8665 will rise the change of larger trend reversal and target 0.8819 resistance next.

In the bigger picture, outlook in USD/CHF will stay bearish as long as 0.9243 resistance holds. Larger down trend from 1.0146 (2022 high) should extend further to 61.8% retracement of 1.0146 to 0.8551 from 0.9243 at 0.8257.