Sample Category Title

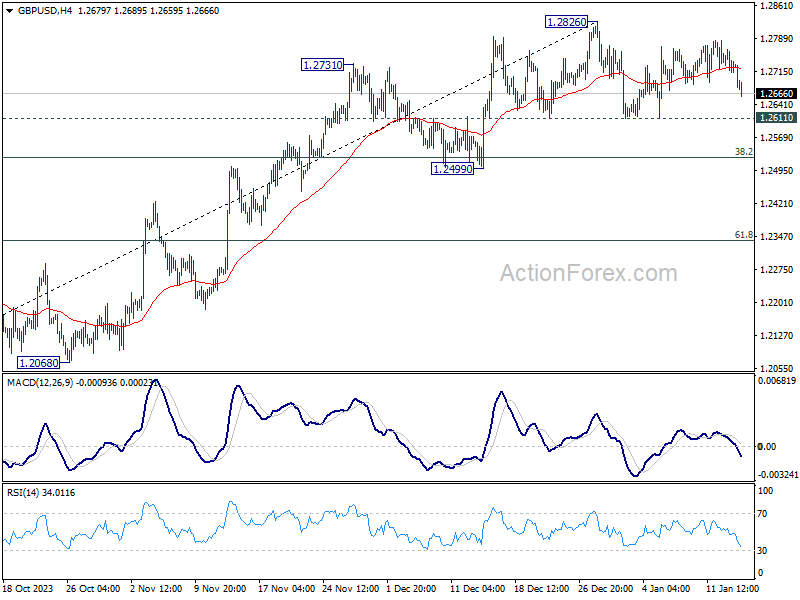

GBPUSD Slides But Remains Stuck in Rangebound Pattern

- GBPUSD experiences losses in the past couple of sessions

- But its short-term sideways structure holds

- Momentum indicators turn slightly negative

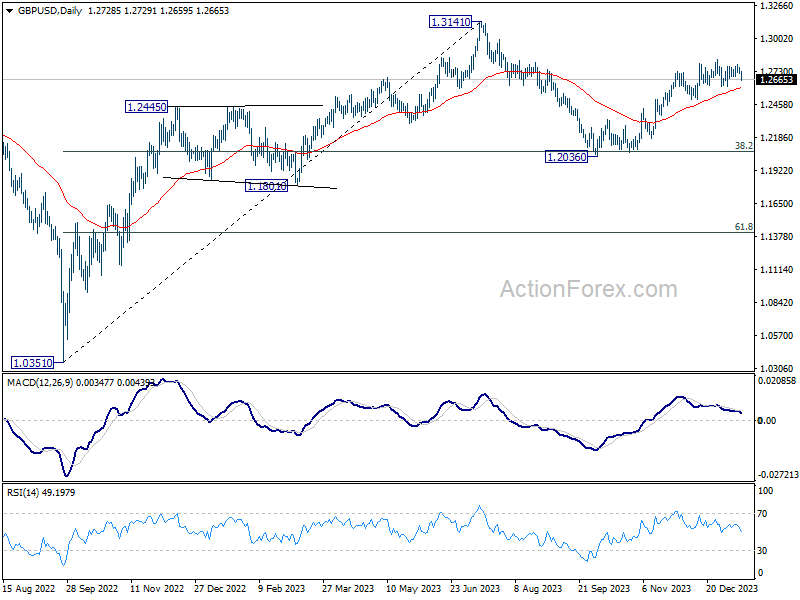

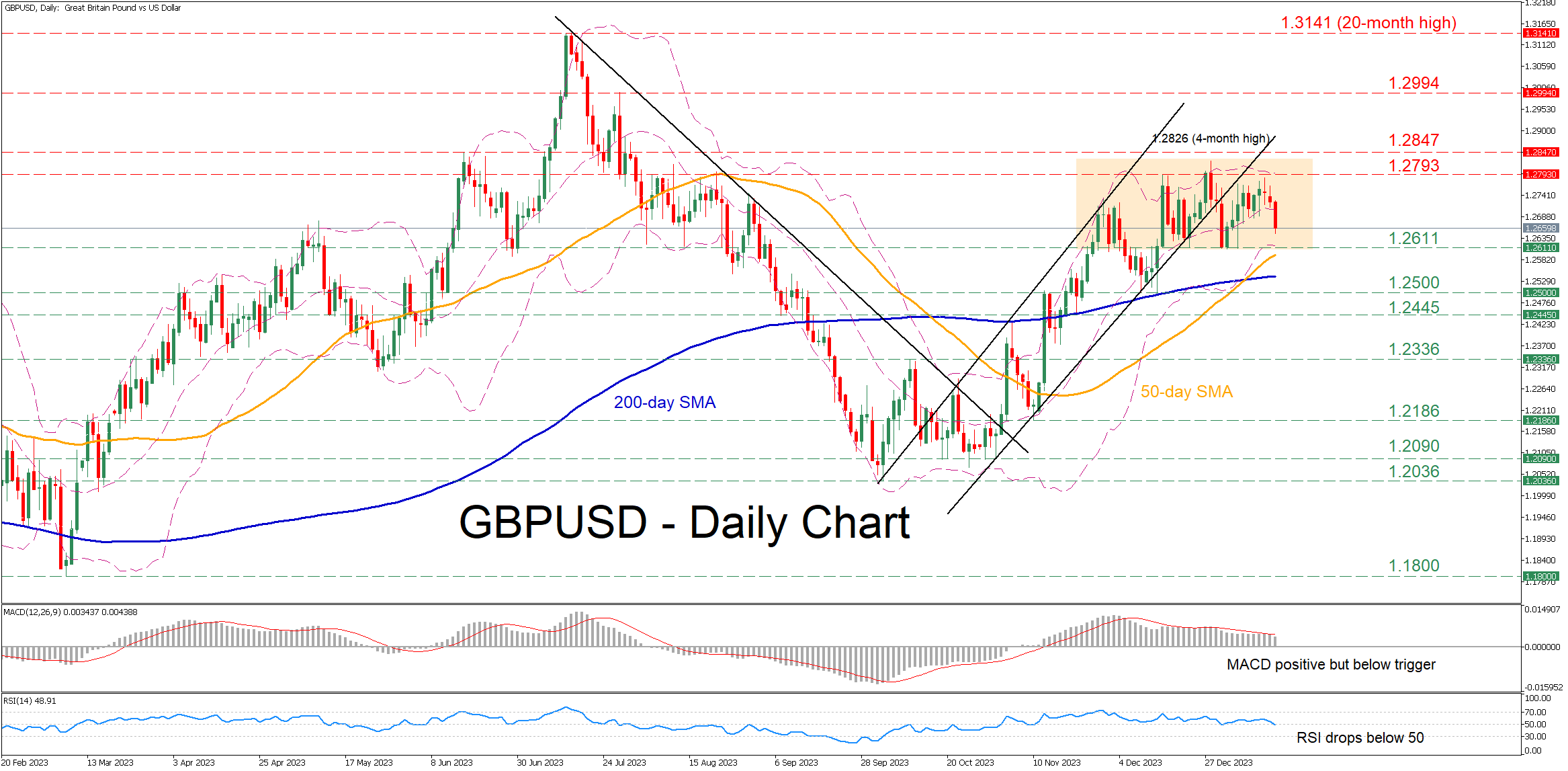

GBPUSD had been trending higher within an upward sloping channel, posting a fresh four-month peak of 1.2826 in late December. Nevertheless, the rally seems to have taken a breather, with the price trading without a clear direction since the beginning of the year.

Given that the short-term oscillators are providing cautiously negative signals, the bears could attempt to push the price below 1.2611, which is the lower end of the recent range. Piercing through that floor, the price may test the December bottom of 1.2500. A violation of that hurdle could pave the way for 1.2445, a region that provided both support and resistance throughout 2023.

Alternatively, if the pair storms back higher, the December resistance of 1.2793 could prove to be the first barricade for buyers to overcome. Breaching that area, the price might test the four-month peak of 1.2826 before it faces the June 2023 high of 1.2847. Further upside attempts could then stall at the July resistance of 1.2994.

In brief, GBPUSD remains a prisoner within its tight range, appearing unable to adopt strong directional impetus. However, negative pressures seem to be intensifying as the RSI has fallen below 50 for the first time since early November.

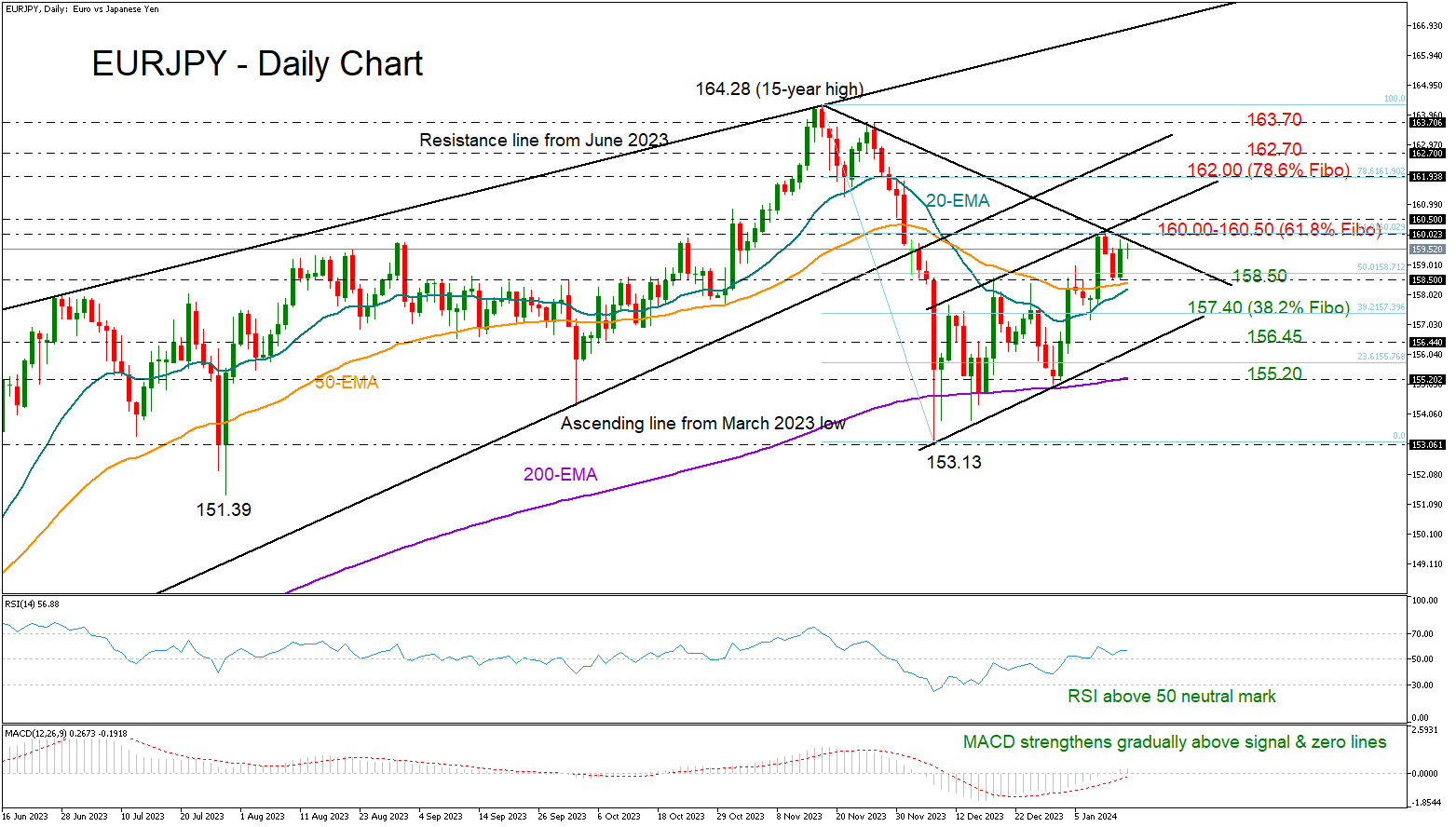

EURJPY Sustains Short-term Bullish Structure

- EURJPY takes a breather after one-month high

- A break above the 160 area is required

EURJPY has been moving back and forth within the 158.50-160.00 region following last week’s aggressive bounce to a one-month high of 160.17.

Technically, the short-term range is formed by the 50% and 61.8% Fibonacci retracement levels of the previous downfall, but the series of higher highs and higher lows that started from December’s trough are still promising.

Moreover, the RSI is still fluctuating above its 50 neutral mark and the MACD continues to strengthen, albeit marginally above its zero and signal lines, keeping the bias on the positive side.

Practically, the bulls will need a clear close above the 160.00-160.50 region to reach the 78.6% Fibonacci mark of 162.00 and the broken ascending trendline from March 2023 at 162.70. Additional gains from there could bring November’s ceiling of 163.70-164.28 under examination.

In the event the price tumbles below the 158.50 floor, some consolidation could develop around the 38.2% Fibonacci of 157.40 before the sellers target the lower band of the bullish channel at 156.45. A bearish breakout there might see an extension towards the 200-day exponential moving average (EMA) at 155.20.

Summing up, EURJPY has some bullish power in the tank, though only a durable move above the 16.00-160.50 region could create more upside.

ECB’s Valimaki addresses market uncertainty rate and inflation outlook

In a Reuters interview, ECB Governing Council Member Tuomas Valimaki addressed the disparity between market pricing, which suggests a 150 basis points rate cut this year, and the views of economists.

He pointed out that the expectations reflected in money markets do not always align with economists' projections, indicating a significant level of uncertainty among market participants. The wide distribution around market prices, as mentioned by Valimaki, underscores the existing ambiguity and varied interpretations of future monetary policy directions.

Valimaki further elaborated on the implications of market expectations versus the ECB's baseline forecasts. He pointed out that if market rates were to fall more rapidly than projected, and the ECB's forecasts prove more accurate, it could lead to higher inflation. This scenario, he explained, "could delay monetary easing."

ECB’s Centeno: Inflation trajectory is very positive

At the World Economic Forum in Davos, ECB Governing Council member Mario Centeno highlighted the positive direction of medium-term inflation, noting that its "trajectory is very positive right now." He further told CNBC that "we don't need to do more than is needed"

On the topic of rate cuts, Centeno noted "once inflation starts going down sustainably, with an economy … that is not growing, where the challenges are huge, we need to be open to get all data on board and decide upon that."

Meanwhile, another ECB Governing Council member, Francois Villeroy de Galhau, speaking at a panel in Davos, cautioned against premature declarations of victory over inflation. However, he admitted that "our next move will be a cut, probably this year" evenh though he refrained from commenting on the timing.

UK Wage Growth Cools Which Could Enable Earlier BoE Rate Cuts

Labour market figures this morning have kicked off a big week of economic data for the UK in a promising way, with wage growth a particular highlight from the report.

For a long time now, central banks have indicated that a significant amount of pressure from higher interest rates will need to be applied to cool the labour market - in turn, lifting unemployment and slowing wage growth - to return inflation sustainably to target. But recent evidence suggests that may not necessarily be the case.

Instead, inflation has been falling faster than anticipated, and now so is wage growth which has slowed significantly since the last peak four months ago. Average earnings growth including bonuses in the three months to November was 6.5% compared with 7.2% a month earlier and 8.5% four months ago.

Don't get me wrong, that's still far too high but it's a lot of progress in a very short period, and with inflation now running much lower, there's every chance we see much more over the coming months that enables the Bank of England to pivot towards cutting interest rates.

The pound did fall in the aftermath of the release but perhaps not quite as much as you'd expect from such an undershoot. That said, market positioning on rate cuts from the BoE was already far more aggressive than what many, especially at the central bank, have indicated is likely. Markets still see 125 basis points of cuts this year but there's a growing chance of 150 which is more in line with the US and euro area.

We'll hear from BoE Governor Andrew Bailey later in the day who may offer his views on the recent data and perhaps hint at a change in tone when the central bank meets in a couple of weeks. It's probably a little early to expect too big a pivot but it could lay the groundwork for a May cut as long as the data continues to comply.

Oil prices remain very choppy

Oil prices remain very choppy amid the uncertainty in the Middle East following the US and UK attacks on Houthi targets. We haven't seen a significant increase in the price of oil on the back of the attacks but the brief spikes we've seen have highlighted the sensitivity in the market to events around the Red Sea.

Gold struggling near previous record high

Gold is trading a little lower this morning after bouncing higher once again in recent sessions. The yellow metal remains buoyed by very aggressive rate-cutting expectations, particularly in the US, but at the same time, it is struggling to generate fresh momentum around the prior record highs, near $2,070. We obviously saw a spike in early December well above this but the timing of the move and the speed with which it reversed it suggests the market was never fully behind it, so the prior highs continue to look like a significant psychological threshold.

Could Bitcoin dip below $40,000 after ETF announcement?

Bitcoin is trading quite flat today but has come well off its highs since last Thursday. It's down around 13% in that time with some heat potentially coming out of the market in the aftermath of the spot bitcoin ETF announcement. We may be seeing another example of "buy the rumour, sell the fact" considering how highly anticipated the announcement was, it's just not clear whether that's now played out. A dip below $40,000 would be a big test.

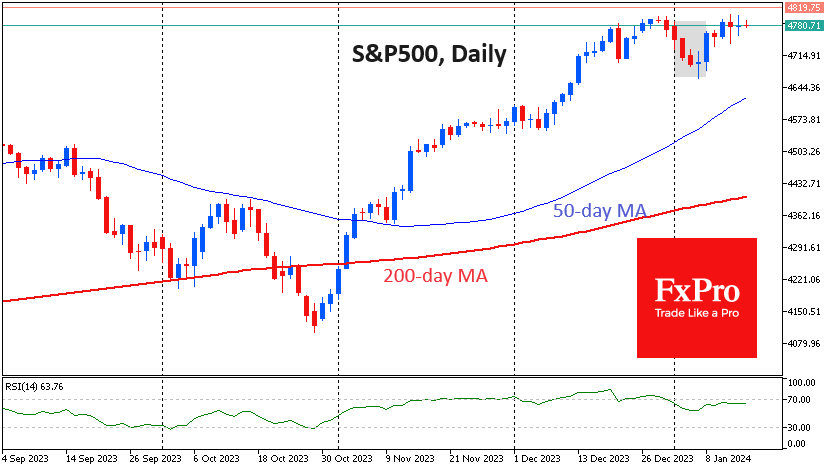

‘First Five Days’ Rule Points to a Challenging Year

US equity indices declined in the first five trading sessions of January. This dynamic promises a challenging year for the stock market, according to the old “first five days” rule.

Identifying a defining trend would have been an easy task if not for stabilisation on the day of the NFP release on January 5 and a strong rally on January 8.

The “first five days” rule was popularised by Jim O’Neil during his time working for investment banks. Don’t limit yourself to this rule for the entire year, but consider it as a sentiment for the year.

The last time this method misfired was in 2018, but after that, it correctly determined five times whether the S&P500 would end the year up or down. The indicator also predicted a decline in 2016, but that was a year of growth after the prolonged stagnation of 2015 and an 11% plunge in January.

We now tend to agree with the “first five days” sentiment. The S&P500 index broke the highs of late last week and was only 0.8% away from an all-time high.

The US stock market was near highs last week as markets strengthened on expectations of more aggressive rate cuts from the Fed. Currently, rate futures see a cut at every meeting since March as the main scenario. The driver has been weaker ISM services and producer price indices, but the usually weightier, stronger employment and consumer inflation data is ignored.

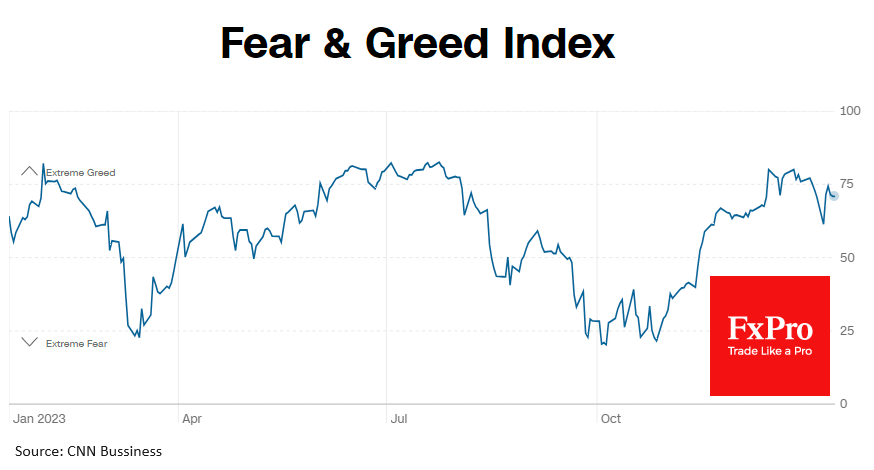

In addition, we are dismayed to see that the level of greed in the markets has bordered on extreme greed over the past month. Declines out of extreme greed often precede corrections and sometimes give rise to bear markets.

It may well be that the bulls squeezed everything they could out of the last rally, including abundant short-squeezes from recession-expecting bears and extremely dovish expectations from the Fed for this year.

The coming year may prove to be as challenging and clear-cut as the first five trading sessions have been, but still more indicators point to a correction than a continued rally, at least in the coming weeks.

Dollar Shows Broad Gains

Markets

With US markets closed for Martin Luther King Day, Europe was obliged to find its own intraday dynamics. After a sharp US driven (softer PPI’s) yield decline on Friday, German rates gapped higher at the open (+/-4 bps). Initially, there was little news to support a clear directional move. A preliminary estimate of the German Statistical office of the country’s 2023 GDP growth was set at -0.3% Y/Y, in line with expectations. The estimates/details in the report didn’t provide much of a reason for yields to rally further. Later in the session, the focus turned the ECB members speaking on the sidelines of the World Economic Forum in Davos. Buba’s Nagel repeated his assessment that it’s too early to talk about rate cuts as inflation still remains too high. He labelled markets’ pricing as too optimistic. Later, ECB’s Holzmann, admittedly a well-known hawk within the ECB MPC, even indicated that one should not bank on rate cuts in 2024 as geopolitical tensions still risk disrupting supply chains and energy markets, potentially keeping price increases at levels the ECB can’t ignore. Hawkish comments from Nagel and Holzmann shouldn’t come as a big surprise. Even so, German yields gained some further traction close higher between 8.1 bps (2-y) and 4.0 bps (30-y). Higher yields added to a risk-off sentiment with the EuroStoxx 50 ceding 0.57%. Despite ongoing tensions on Middle East supply, Brent oil held stable below the $80 p/b mark (close $78.15). Higher EMU yields and at the same time a risk-off sentiment kept the euro and the dollar in balance (EUR/USD close 1.095). Sterling lost modest ground against the euro as UK yields rose less than EMU/German ones (EUR/GBP close 0.8603).

This morning, US yields are joining yesterday’s rebound in Europe and gain about 5-6 bps across the curve. Asian markets are captured by a broad risk-off sentiment often ceding 1% (+). India outperforms. The dollar shows broad gains (DXY 102.87, EUR/USD 1.092, USD/JPY 146.1). The eco calendar today is again rather thin. ECB inflation expectations and the ZEW economic confidence might influence intraday trends but are no game changers. ECB’s Villeroy will speak in Davos. The US calendar only contains the Empire manufacturing survey. Fed’s Waller will speak on the economy. Even as US yields are gaining a few bps this morning, last week’s price action keeps the downtrend in place, especially at the short end of the curve. The US 2-y yield needs to regain the 4.40% area to call off the downside alert. On FX markets, first USD resistance/euro support is coming in at 1.0877.

UK labour market data this morning came in on the soft side of expectations. The number of payrolled employees declined a bigger than expected 24k. At the same time average weekly earnings growth (ex-bonus) slowed more than expected from 7.2% to 6.6%. In a first reaction, sterling is losing some further ground (EUR/GBP 0.8615).

News & Views

Former BoJ executive director as well as ex-chief economist Maeda said that he expects annual wage negotiations to result in a 4% rise, exceeding the 3.58% of last year and paving the way for the central bank to ditch its negative policy rate. According to Maeda, the “virtuous cycle between wages and inflation” that the Bank of Japan is seeking is already in place. Until now, current governor Ueda has defended the ultra-easy policy stance because policymakers aren’t so sure that is indeed the case. Maeda, who left the BoJ in 2020 after playing a major role in the central bank’s initial response to the pandemic, believes rate action could come in the spring (April) without ruling out an earlier move.

Hungary’s Finance Ministry State Secretary in an op-ed on a Hungarian financial news website called for a bigger consolidation effort. While the government does plan to reduce the deficit from 5.9% in 2023 to 2.9% of GDP this year, Péter Beno Banai warned for the probability of revenues missing estimates and expenditures exceeding plans due to base effects. With the current forecast being only just below the EU’s 3% threshold, risks are for Hungary to enter the bloc’s excessive-deficit procedure. That could ultimately end up in the suspension of EU funds at a time when many billions (including from the Resilience and Recovery Facility) are already held back over graft and rule-of-law concerns.

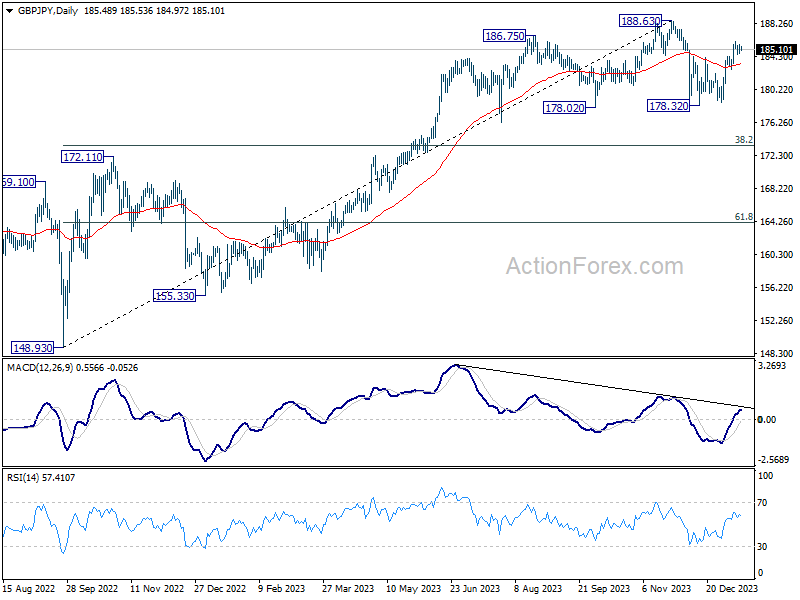

GBP/JPY Daily Outlook

Daily Pivots: (S1) 184.82; (P) 185.29; (R1) 185.98; More...

GBP/JPY is staying in tight range despite today's dip and intraday bias remains neutral. Further rally is in favor as long as 182.73 minor support holds. Corrective pull back from 188.63 should have completed. Above 186.14 will resume the rebound from 178.32 to retest 188.63.

In the bigger picture, price actions from 188.63 medium term top are seen as a correction to the up trend from 148.93 (2022 low) only. As long as 172.11 resistance turned support holds, larger up trend from 123.94 (2020 low) is still in favor to resume through 188.63 at a later stage.

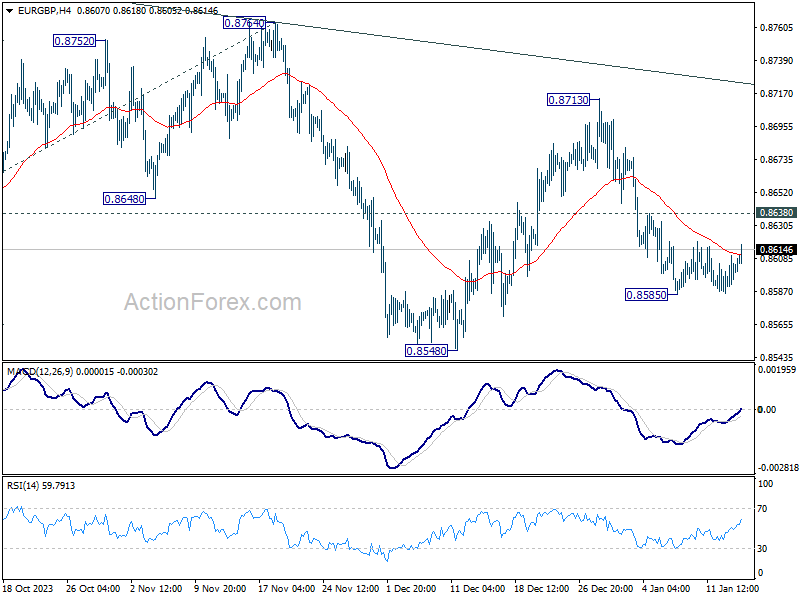

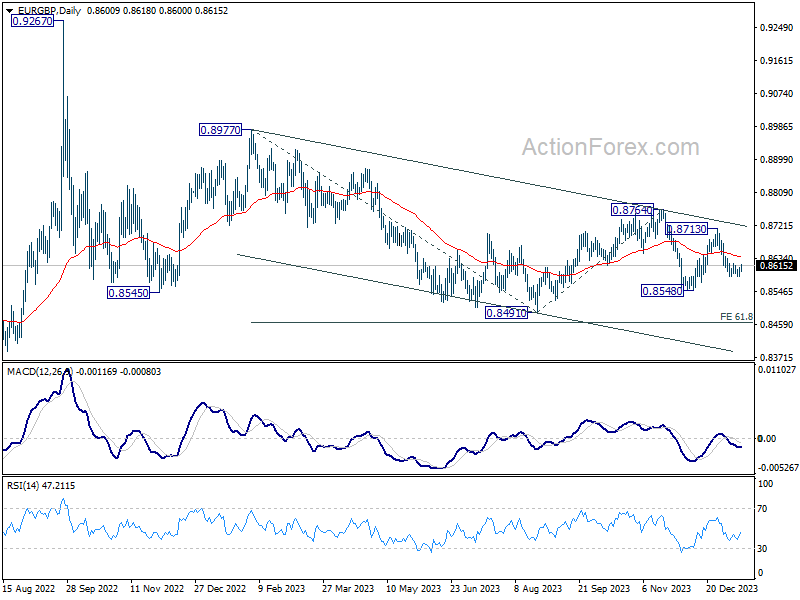

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8591; (P) 0.8601; (R1) 0.8616; More...

EUR/GBP is staying in tight range above 0.8585 and intraday bias remains neutral. Further decline is expected as long as 0.8638 minor resistance holds. On the downside, below 0.8585 will resume the fall from 0.8713 to 0.8548 support. Firm break there will target 0.8491 low next. Nevertheless, decisive break of 0.8638 will turn bias back to the upside for stronger rebound to 0.8713 instead.

In the bigger picture, fall from 0.8764 is seen as another leg in the whole down trend from 0.9267 (2022 high). Outlook will stay bearish as long as 0.8764 resistance holds. Break of 0.8491 will target 61.8% projection of 0.8977 to 0.8491 from 0.8764 at 0.8464.

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2705; (P) 1.2735; (R1) 1.2758; More...

GBP/USD is staying in range of 1.2611/2826 despite today's decline. Intraday bias remains neutral first. On the upside, decisive break of 1.2826 will resume whole rally from 1.2036. Nevertheless, break of 1.2611 will bring deeper decline to 1.2499 support instead.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg that's in progress. Upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.