Sample Category Title

GBP/USD Daily Outlook

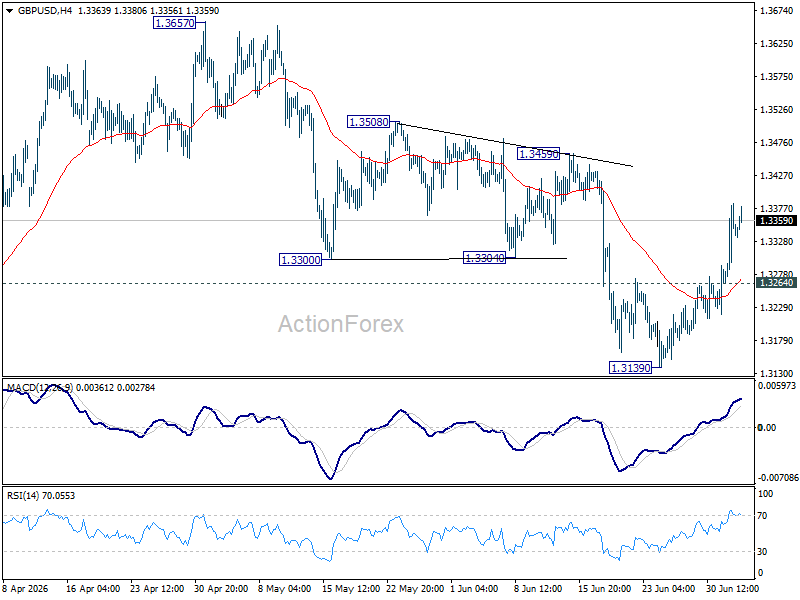

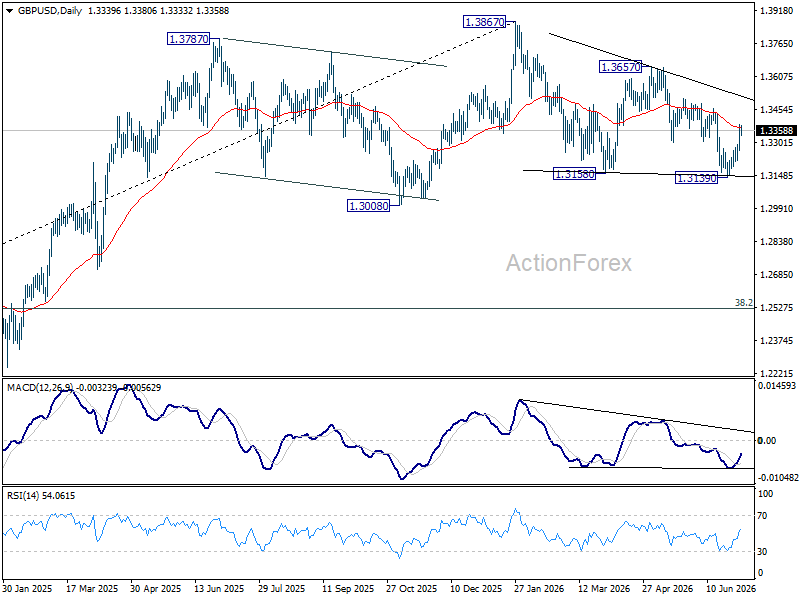

Intraday bias in GBP/USD remains on the upside for 1.3459 resistance. Firm break there will add to the case that correction from 1.3867 has completed at 1.3139. Next target is 1.3657 for confirmation. On the downside, below 1.3264 minor support will turn intraday bias neutral again first.

In the bigger picture, price actions from 1.3867 are a corrective pattern within the broader up trend from 1.0351 (2022 low). With 1.3008 support intact, medium term bullishness is maintained and break of 1.3867 is in favor for a later stage, towards 1.4248 key resistance (2021 high). However, firm break of 1.3008 will at least bring deeper fall to 38.2% retracement of 1.0351 to 1.3867 at 1.2524, with increased risk of bearish reversal.

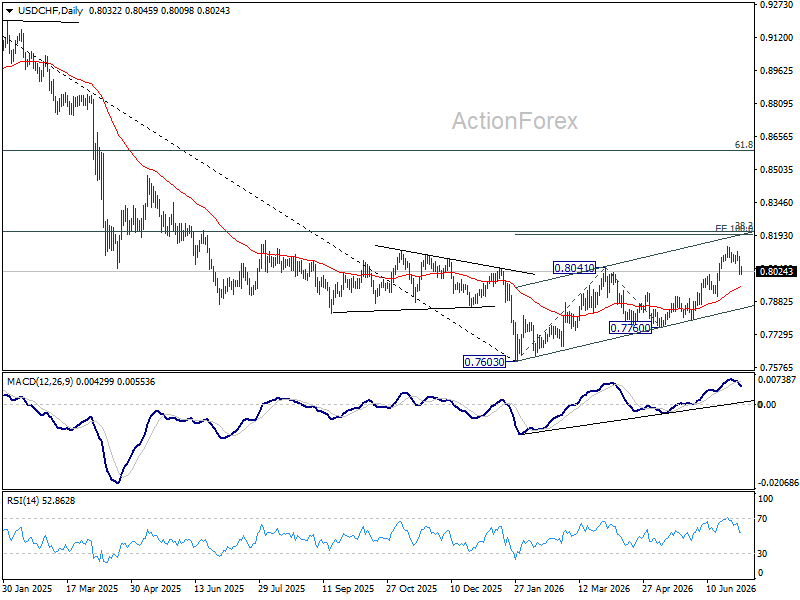

USD/CHF Daily Outlook

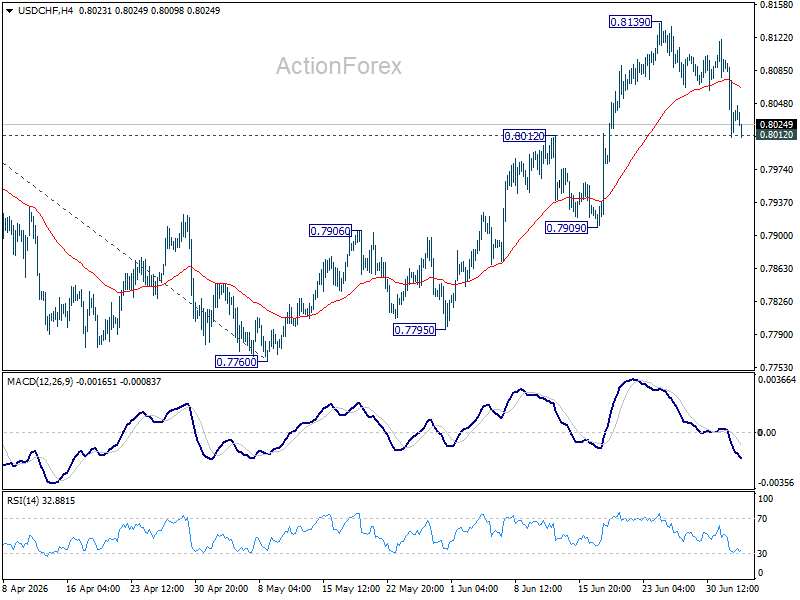

USD/CHF is still defending 0.8012 resistance turned support and intraday bias remains neutral first. On the upside, above 0.8139 will extend the larger rise from 0.7603 to 100% projection 0.7603 to 0.8041 from 0.7600 at 0.8198 next. However, sustained break of 0.8012 will bring deeper fall to 55 D EMA (now at 0.7951) and below.

In the bigger picture, while a medium term bottom was formed at 0.7603, it's still early to call for bullish trend reversal. As long as 38.2% retracement of 0.9200 (2025 high) to 0.7603 at 0.8213 holds, the larger down trend could still continue through 0.7603 at a later stage. However, firm break of 0.7603 will argue that the trend has reversed and turn focus to 0.8332 support turned resistance (2023 low) for confirmation.

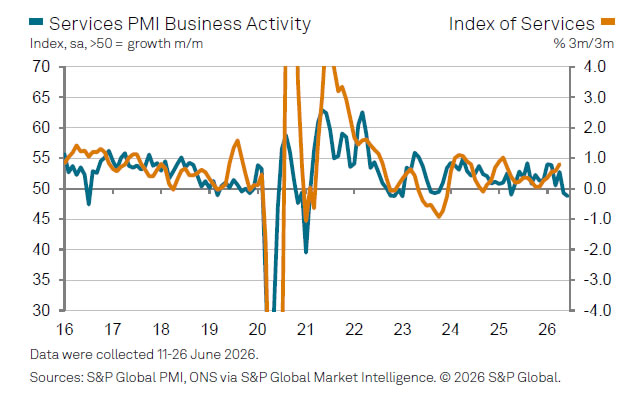

UK Services PMI Falls to Lowest Since 2023 as Demand Weakens Despite Cooling Cost Pressures

UK business activity weakened further in June as the services sector recorded its sharpest contraction in nearly three and a half years, highlighting a loss of economic momentum during the second quarter. The final S&P Global UK Services PMI Business Activity Index fell to 48.8 from 49.3 in May, its lowest reading since January 2023. The Composite PMI Output Index also slipped to 49.3 from 49.7, marking a second consecutive month below the 50.0 threshold and its weakest reading since April 2025.

The survey pointed to weakening demand as a key driver of the slowdown. New orders declined for a fourth straight month, with S&P Global describing the fall as the steepest in just over three and a half years. According to Economics Director Tim Moore, firms cited persistent cost pressures, subdued customer demand and uncertainty surrounding the Middle East conflict as the main factors weighing on activity. Businesses also reported fragile investment sentiment, greater client caution and pressure on household spending, all of which contributed to softer service-sector output.

There was, however, some encouragement on inflation. Input cost inflation eased to its lowest level since March, largely reflecting lower fuel prices following the decline in global oil prices. Although businesses continued to report higher transport, wage and raw material costs, the moderation in overall cost pressures should provide some relief. Business confidence also improved modestly on hopes that the US-Iran ceasefire will prove durable, but optimism remained well below levels seen at the start of the year as concerns over the broader UK economic outlook persisted.

| Indicator | Previous | Latest |

|---|---|---|

| Services PMI Business Activity | 49.3 | 48.8 |

| Composite PMI Output | 49.7 | 49.3 |

Ethereum: Has the Recovery Begun?

Ethereum has staged a notable rebound after once again testing the heavily watched psychological zone around 1500$. Since bouncing off this support, ETH/USD has climbed roughly 13%, now trading around the $1,700 mark.

This recovery is being driven by a combination of technical and fundamental factors. On the technical side, the aforementioned support zone has once again proven its relevance, attracting buyers at a historically significant level. On the fundamental side, the latest US Non-Farm Payrolls report added just 57,000 jobs in June, well below the 110K-115K consensus and a sharp slowdown from May's downwardly revised 129,000. Combined with a 74,000-job downward revision to the prior two months, the weaker print has weighed on the US Dollar, reducing the likelihood of near-term Fed rate hikes and boosting risk assets positioned as an alternative to the greenback — including cryptocurrencies.

Technical analysis of ETH/USD

After bouncing off the $1,500 support zone, Ethereum seems to be directed to a key test at the former support, turned resistance, around $1,800.

Bullish scenario

A confirmed break and hold above the $1,800 level would allow ETH to sustain bullish momentum and begin forming a structure of higher highs and higher lows after months of bearish price action. This potential recovery also finds support from a notable bullish divergence on the 4-hour RSI, where a sequence of rising lows on the indicator contrasts with the sequence of falling lows on price, a signal that downward momentum may be fading.

Bearish scenario

Alternatively, as price approaches the $1,800 resistance, ETH could reject the level and resume its broader downtrend, slipping back below the intermediate $1,680–$1,700 zone. Such a move would suggest the asset still lacks the strength needed to break through this crucial threshold.

Investors and traders remain focused on new Fed Chair Warsh's statements and their impact on the DXY. Will a weaker Dollar Index prove to be the real catalyst for a bullish return across the crypto market?

FXOpen offers the world's most popular cryptocurrency CFDs*, including Bitcoin and Ethereum. Floating spreads, 1:2 leverage — at your service (additional fees may apply). Open your trading account now or learn more about crypto CFD trading with FXOpen.

*Important: At FXOpen UK, Cryptocurrency trading via CFDs is only available to our Professional clients. They are not available for trading by Retail clients. To find out more information about how this may affect you, please get in touch with our team.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

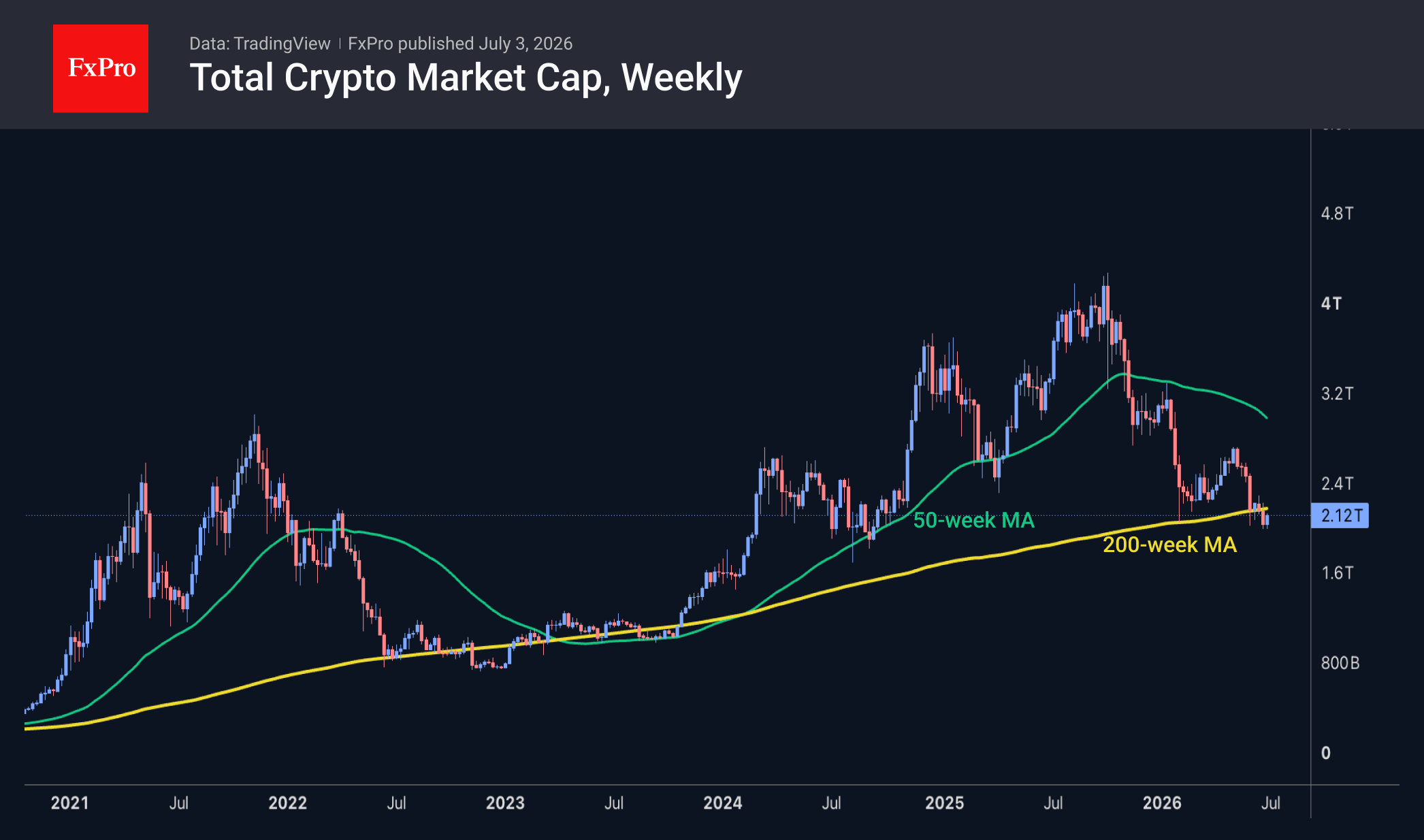

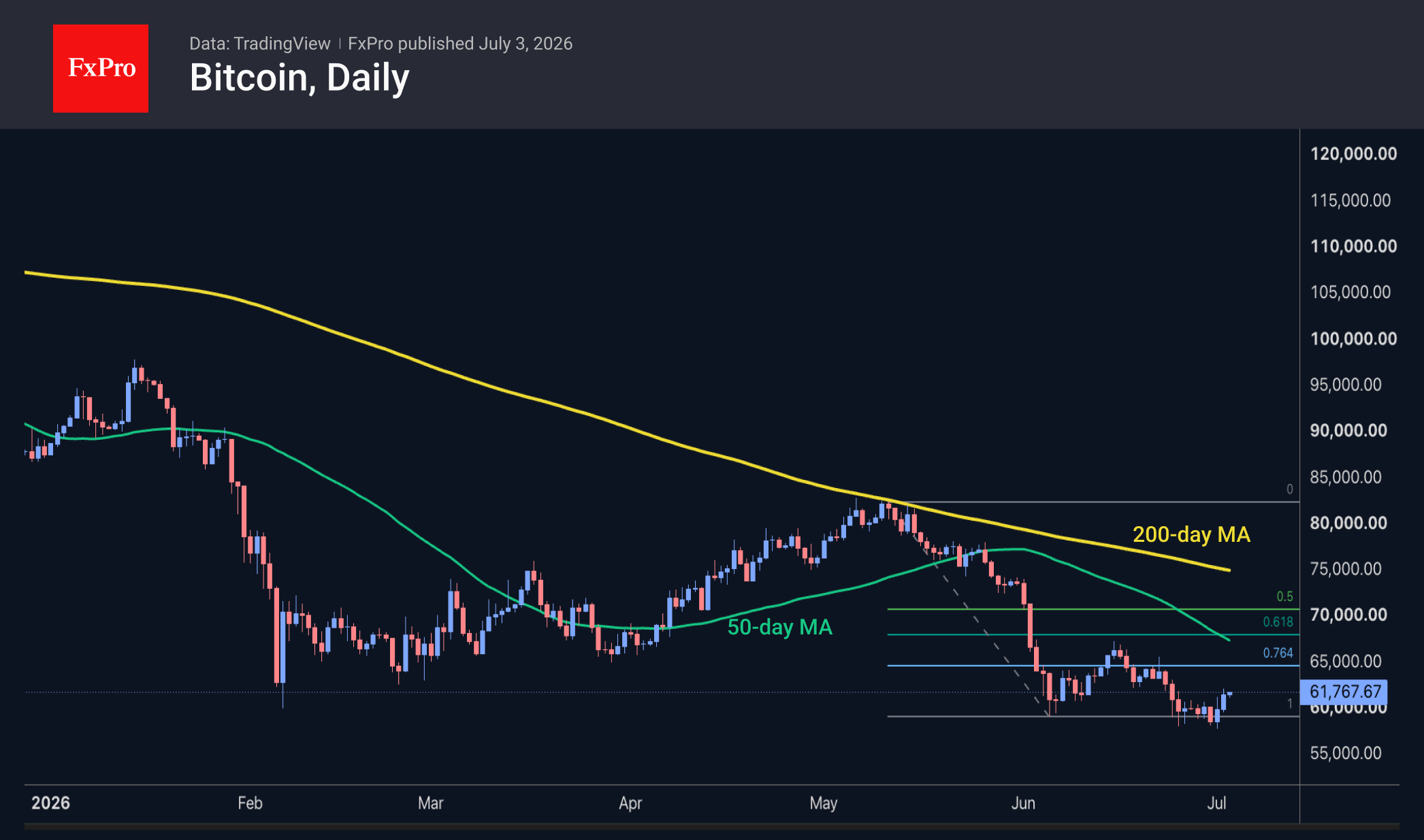

The Crypto Market Is Rebounding: BTC Needs $67K to Reverse Course

Market Overview

The crypto market is continuing its recovery, which coincided with the start of the calendar month. Market capitalisation has reached $2.14T, up from a low of $2.02T at the start of 1 July. Buying is taking place across the board. Amongst the individual performers over the last 24 hours, the leaders were Uniswap (+13.1%), SushiSwap (+6.8%) and Cardano (+6.5%), while Hedera (-1.9%) and IOTA (-1.7%) lost ground. The crypto market is edging up from below its 200-week moving average. However, we stand by our view that a dip below, or even an approach to, this line reflects a bearish sentiment in the cryptocurrency market, which often lasts for weeks or months. On the other hand, we have not seen any significant historical falls below this curve, so it would be overly pessimistic, in our view, to expect a pullback to $1T, the starting point of the last bull market in 2023.

Bitcoin rose above $62K at one point on Thursday but retreated to $61.6K amid low trading activity due to the US weekend. On daily timeframes, the RSI has moved out of oversold territory and formed a bullish divergence with the price, indicating that selling momentum is waning and laying the groundwork for a rebound. However, it would only be reasonable to speak of a fundamental reversal of the downtrend if the price consolidates above the $67–68K range, where the local highs from June, the 50-day moving average and the 61.8% retracement level of the May–June decline are concentrated.

News Background

CryptoQuant points to a growing proportion of investors in the red. Losses are reaching record levels, suggesting that the bottom is near.

The collapse in Strategy shares, although painful, is a necessary part of the market cycle, signalling that Bitcoin is approaching its bottom, said Matt Hougan, Chief Investment Officer at Bitwise. In his view, a new BTC bull market could begin this autumn.

Japanese investment firm Metaplanet purchased a further 2,823 bitcoins in the second quarter, according to its quarterly report. The company’s total holdings have reached 43,000 BTC, making it the third-largest corporate holder of the leading cryptocurrency.

According to Arkham Intelligence, brothers Cameron and Tyler Winklevoss transferred Bitcoin and Ethereum totalling around $67 million to hot wallets on their crypto exchange, Gemini. Previously, such transactions were followed by cryptocurrency sales.

The FxPro Analyst Team

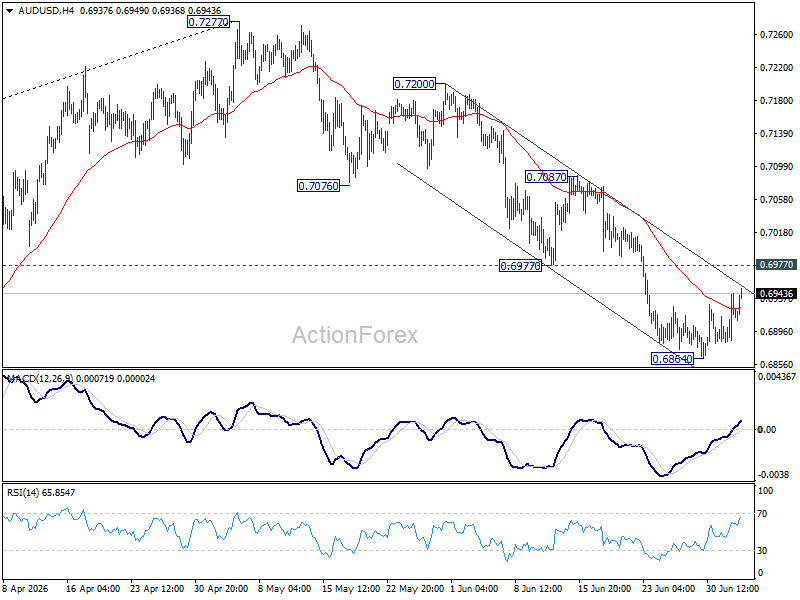

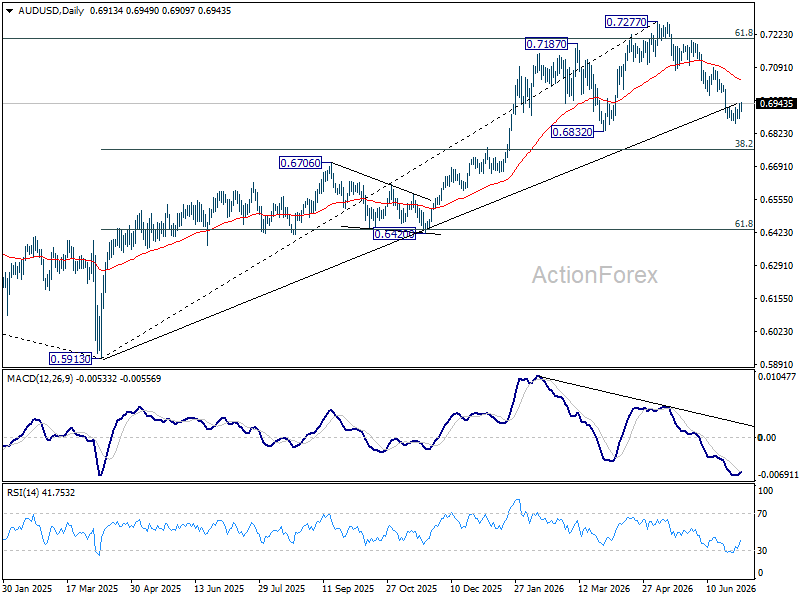

AUD/USD Daily Report

Intraday bias in AUD/USD remains neutral at this point. Further decline is expected as long as 0.6977 support turned resistance holds. Below 0.6864 will extend the fall from 0.7277 to 0.6832 support. Firm break there will target 0.6756 fibonacci level. However, sustained break of 0.6977 will bring stronger rebound to 0.7087 resistance instead.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top could be formed at 0.7277 after failing to sustain above 61.8% retracement of 0.8006 (2021 high) to 0.5913 (2024 low) at 0.7206. Deeper fall could be seen to 38.2% retracement of 0.5913 to 0.7277 at 0.6756 as a correction. But strong support should be seen there to bring rebound. Consolidations would continue below 0.7277 for a while.

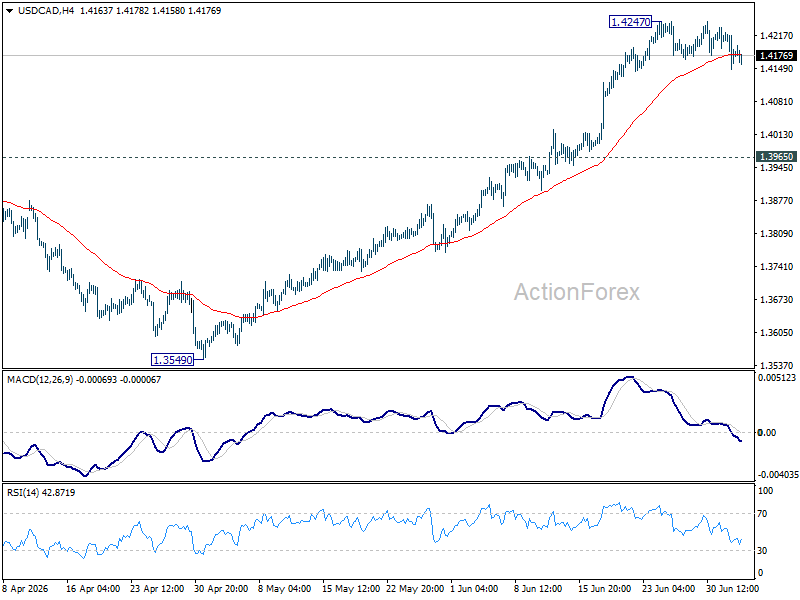

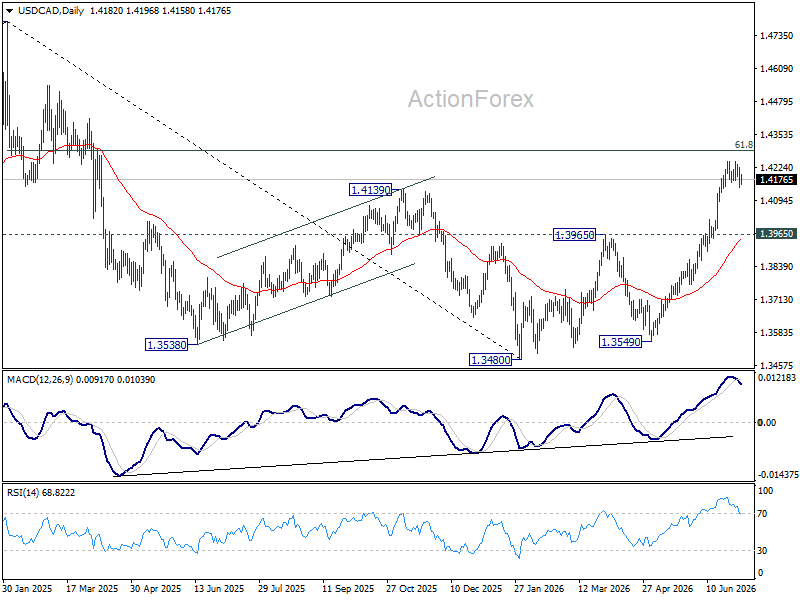

USD/CAD Daily Outlook

Intraday bias in USD/CAD remains neutral first. Consolidation form 1.4247 is extending and deeper pullback cannot be ruled out. But downside should be contained above 1.3965 resistance turned support. Above 1.4247 will resume the rally from 1.3480 to 61.8% retracement of 1.4791 to 1.3480 at 1.4290. Firm break there will pave the way back to 1.4791 high.

In the bigger picture, current development suggests that fall from 1.4791 has completed as a three wave correction to 1.3480. It's still early to judge if rise from there a corrective bounce, or resumption of the larger up trend from 1.2005 (2021 low). But in either case, retest of 1.4791 high should be seen next.

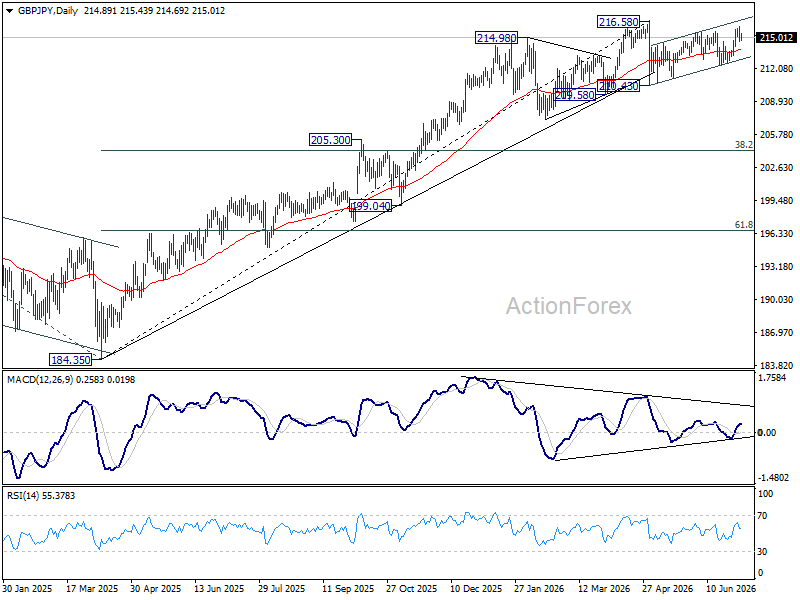

GBP/JPY Daily Outlook

Intraday bias in GBP/JPY remains neutral for the moment. On the upside, above 216.05 will extend the rebound from 210.43 to retest 216.58 high. For now, risk will stay on the upside as long as 212.36 support holds, in case of retreat.

In the bigger picture, there is no clear sign of trend reversal yet. The long term up trend could still extend to 61.8% projection of 148.93 (2022 low) to 208.09 (2024 high) from 184.35 at 220.90 on resumption. However, sustained break of 55 W EMA (now at 207.52) will argue that it's already in medium term down trend for 184.35 support.

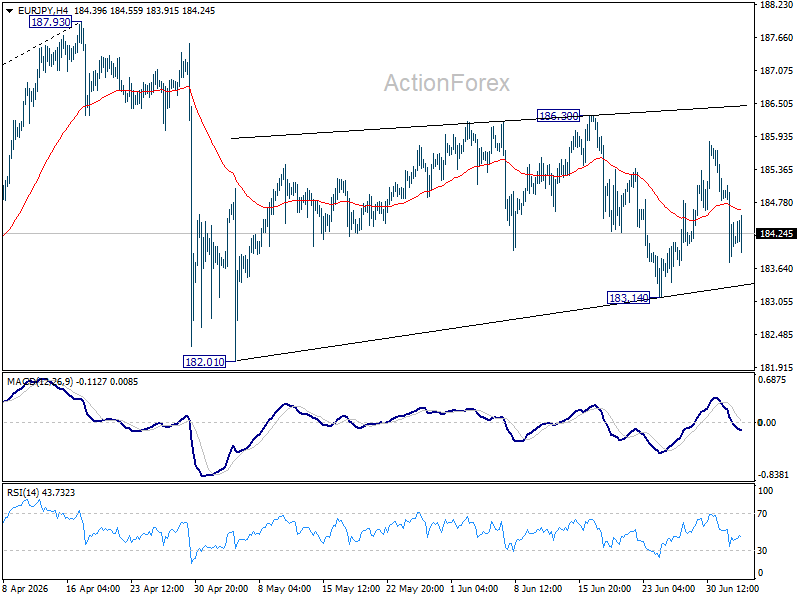

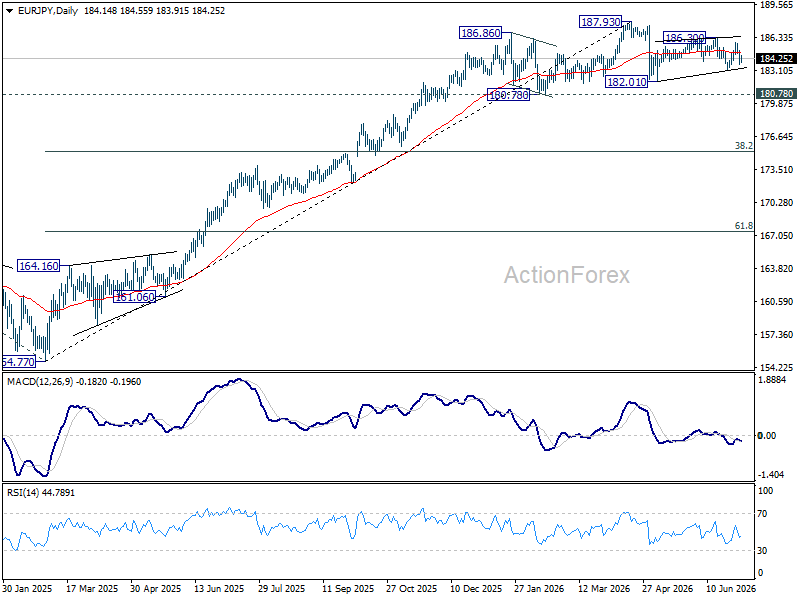

EUR/JPY Daily Outlook

Sideway trading continue in EUR/JPY and intraday bias stays neutral. Risk will remain mildly on the downside as long as 186.30 resistance holds. Below 183.14 will bring retest of 182.01 support first. However, firm break of 186.30 will resume the rebound from 182.01 to retest 187.93 high.

In the bigger picture, there is no sign of reversal yet. Uptrend from 114.42 (2020 low) is still expected to resume at a later stage to 78.6% projection of 124.37 (2022 low) to 175.41 (2025 high) from 154.77 at 194.88. However, sustained break of 55 W EMA (now at 179.37) will argue that it's already in a medium term down trend to 175.41 resistance turned support and below.

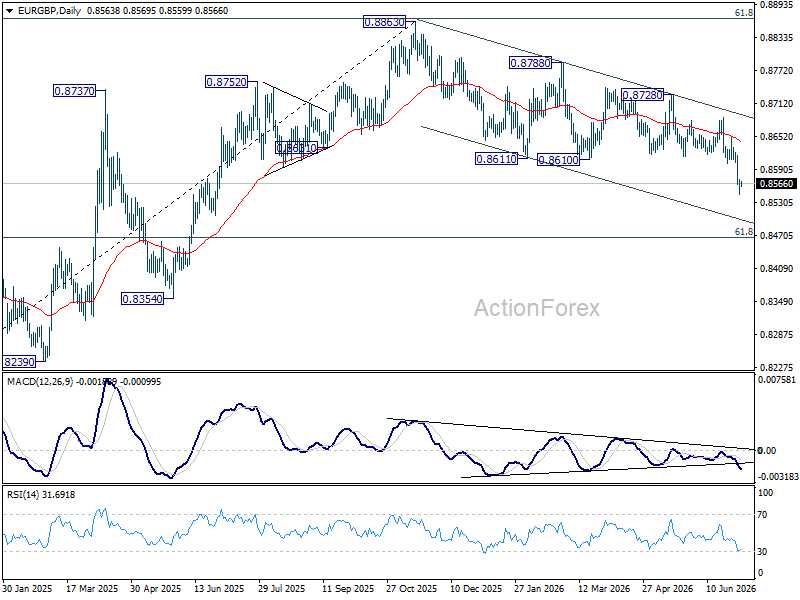

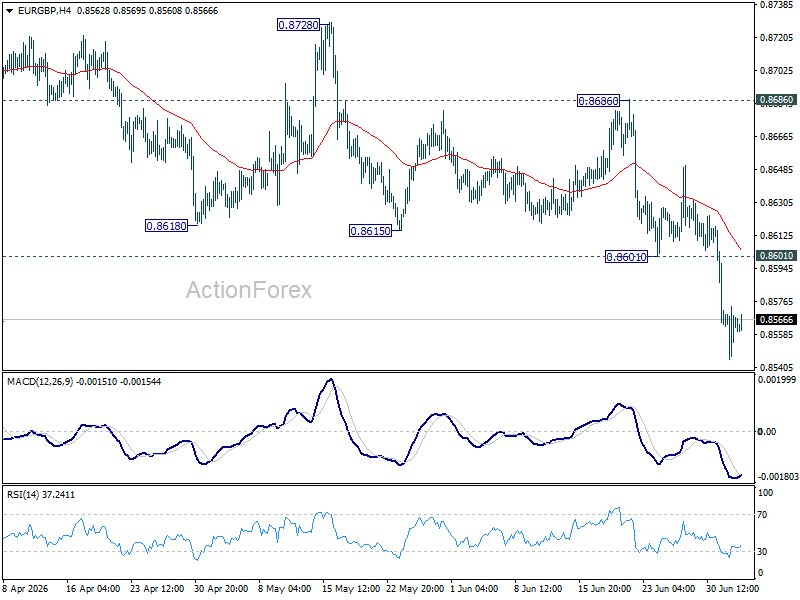

EUR/GBP Daily Outlook

Intraday bias in EUR/GBP stays on the downside at this point. Fall from 0.8863 should target 61.8% retracement of 0.8221 to 0.8863 at 0.8466 at next. On the upside, above 0.8601 minor resistance will turn bias neutral first. But risk will stay on the downside as long as 0.8686 resistance holds, in case of recovery.

In the bigger picture, current development suggests that rise from 0.8221 (2024 low) has completed at 0.8863, just ahead of 38.2% retracement of 0.8221 (2024 low) to 0.8863 (2025 high) at 0.8618. Deeper fall would be seen back to 0.8201 (2022 low). For now, outlook will be neutral at beast as long as 0.8863 hold.