Sample Category Title

Sunset Market Commentary

Markets

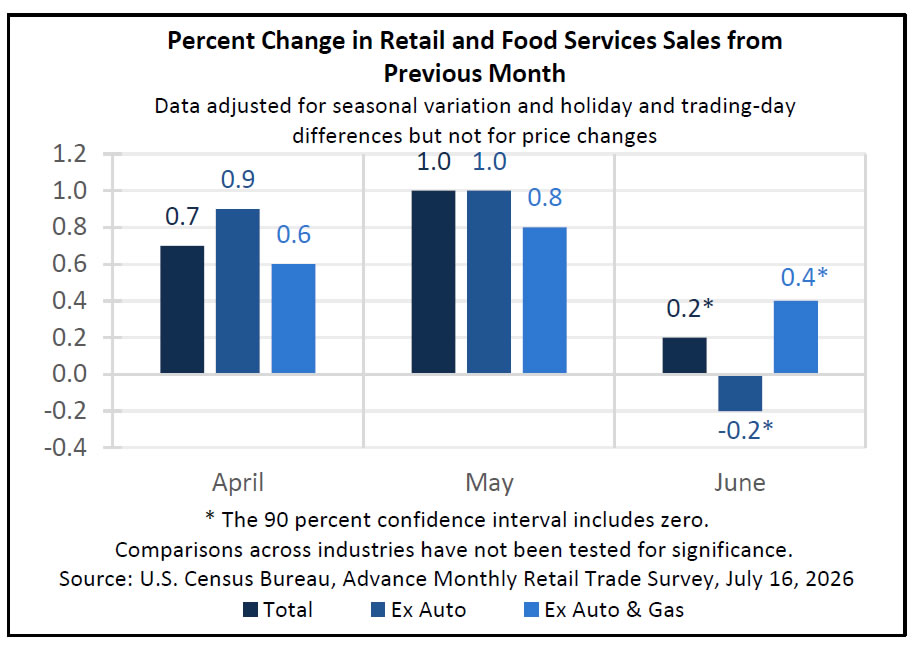

US retail sales were the headliner today. They printed slightly stronger than expected when considering the upward revisions to an already strong month of May. Headline turnover increased by 0.2%. That's actually not bad when taking into account the series aren't adjusted for price swings. Indeed, sales from gasoline stations weighed down on the overall number by dropping -5.3%, reflecting at least partially the significant drop in crude oil last month. A core gauge that excludes car and gas sales rose 0.4% after an upwardly revised 0.8% in May while the private consumption proxy used in GDP calculations (control group) added 0.5% (0.8% vs the month before). Seven out of the 13 categories rose with sporting goods, motor vehicles & parts and online sales increasing the most. Eating & drinking, the only services-related category, rose by just 0.1%.

While decent if not strong, it wasn't the retail sales triggering today's market moves. Geopolitics did. President Trump earlier warned Iran this week the US would start bombing civilian infrastructure including bridges and power stations if it doesn't get back to the negotiating table. Iran has now reportedly instructed its Houthi allies in Yemen to shut the Bab-al-Mandab strait if the US follows through. The Strait connects the Red Sea to the Indian Ocean through the Gulf of Aden and is a transit for an estimated 10% of global oil supply. That share since the Iran war probably even rose. The market reaction follows the well-known pattern. Oil prices rebounded from the intraday lows (Brent near $86), gas prices did the same to hit a new multi-month high (€55.3/MWh). Core bonds sell off. The front end of the curve repositions in function of increased central bank tightening bets. For the ECB, markets assume a cumulative 45 bps in additional hikes this year. The Fed is seen hiking by 28 bps and the Bank of England by 40 bps. 2-yr yields rise 3-3.5 bps in the US and Europe (where the 2026 highs remain under attack) and almost 5 bps in the UK. The long end takes a hit from rising inflation expectations and risk premia. The US 10-30-yr bucket adds 4 bps. European swap rates inch around 3 bps higher in the same segment. The 30-yr at some point was less than a basis point away from a new 15-year high. The US dollar kept a minor upper hand against most peers in the FX landscape. EUR/USD gives back some of yesterday's gains to trade around 1.145. DXY rises towards 100.6. Sterling's strong momentum yesterday dwindled today. The FT reported that Labour's fiscally more conservative Mahmood would be tapped as new chancellor instead of Miliband. That eased some concerns on UK fiscal sustainability, prompting a break of EUR/GBP below 0.85 towards support at 0.8468. The latter is doing its job for the time being. GBP/USD returned a two-month high at 1.354 to 1.351 currently. Blockbuster earnings and a solid outlook from semiconductor bellwether TSMC failed to inspire the AI/tech sector, on the contrary. Stock markets in the US open lower with the Nasdaq slipping about a percent as questions continue to linger on the profitability of massive capital investments.

News & Views

The National Bank of Poland published a set of underlying inflation numbers today. Core CPI excluding food and energy prices rose by 0.3% M/M with the Y/Y-change hovering around 3% for the third consecutive month. That's above the 2.5% mid-point of the 1.5%-3.5% tolerance band. Other core gauges which respectively exclude the most volatile prices or the 15% trimmed mean both slowed from 3.3% to 2.8% Y/Y. Inflation excluding administered prices fell by 0.6% M/M to 2.1% Y/Y (from 2.8%). Today's data printed near consensus, leaving no traces on markets. Polish money markets expect policy rate stability over the next 12 months amid mixed messaging from central bank members and awaiting the outcome of summer inflation readings given the expiry of fiscal measures capping energy bills.

Minutes of the June policy meeting by the Swiss National Bank confirmed that monetary policy (0% policy rate) is continuing to have an expansionary effect. Real interest rates are currently negative and below their long-term equilibrium. Money markets attach a 40% probability to a rate hike at this year's final (December) SNB meeting. Swiss inflation remains stuck in the lower half of the 0%-2% target range with the central bank labelling the impact of the energy shock as largely temporary. SNB Minutes also showed relief that a weaker franc is contributing to easier monetary conditions (EUR/CHF 0.9250 now vs 0.90 in March). In Q1, the SNB was still fighting CHF strength via FX purchases, part of which they were able to reverse in May.

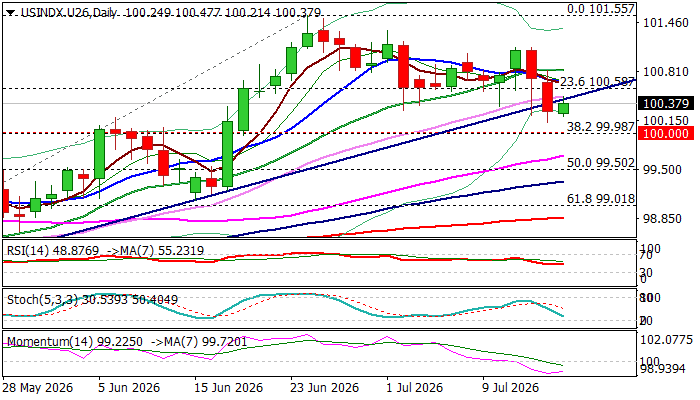

Dollar Index Weakened on Softer Than Expected Inflation Data but Larger Bulls Remain in Play While Key 100 Support...

The dollar index regains traction after suffering losses in past two days, sparked by softer than expected US inflation data for June (CPI, PPI) that cooled expectations for Fed rate hikes.

Wednesday’s break of trendline support (100.40) hit one-month low and generated bearish signal, though the price remained above pivotal 100 support (psychological / Fibo 38.2% of 97.44/101.55) keeping larger bulls alive.

Technical picture on daily chart is mixed (conflicting DMAs / negative momentum / neutral RSI) but fundamentals are still favorable for greenback.

The US economy is in much better condition than other western economies and less exposed to energy shocks that keeps the dollar as currently major safe-haven asset which would benefit from higher energy prices.

Also, upbeat inflation data in June were directly related to the ceasefire in the Middle East and seen as rather temporary phenomenon, as US – Iran conflict escalated again, resulting in closure of strategic Hormuz strait that is likely to fuel inflation again.

This partially offsets risk of dollar’s stronger weakness (especially while the price stays above 100 level), with return and close above broken trendline support, expected to strengthen near-term structure and signal a false break lower.

In such scenario, lift above the trendline would require extension above 20DMA (100.82) to validate positive signal and shift near-term focus higher.

Res: 100.48; 100.82; 101.12; 101.55

Sup: 100.12; 100.00; 99.50; 99.09

Markets Pause Ahead of Weekend as Traders Await Next US-Iran Move

Financial markets settled into a cautious holding mood today, with investors reluctant to extend positions ahead of a potentially pivotal weekend in the Middle East. Despite a sharp selloff across Asia, where the KOSPI plunged -6.37% and the Nikkei dropped -2.79%, the weakness failed to spill into Europe. Major European indexes traded only modestly lower, while US equity futures hovered around unchanged levels. The muted cross-asset response suggested markets were looking beyond day-to-day military headlines and instead waiting for signs of whether the conflict between the United States and Iran is about to return to a more dangerous phase.

That wait-and-see attitude was reflected across asset classes. Brent crude remained confined to a familiar USD 85-87 range after this week's rally stalled below USD 90. Gold slipped back below the USD 4,000 psychological level but attracted little follow-through selling, while the US 10-year Treasury yield edged higher without reclaiming the 4.6% level. Currency markets were equally subdued, with nearly all major pairs and crosses trapped within Wednesday's ranges. Rather than signaling complacency, the lack of movement appeared to reflect investors' reluctance to establish large directional positions before the geopolitical outlook becomes clearer.

One reason markets are hesitating is that recent US military operations increasingly resemble preparation for broader action rather than the decisive escalation itself. According to Reuters, citing US officials, the latest waves of strikes are targeting Iranian air defenses, coastal radar, missile and drone sites, and maritime assets not only to pressure Tehran over the Strait of Hormuz but also to degrade capabilities that Washington would seek to eliminate before undertaking more complex military operations. One official described the campaign as "shaping operations", suggesting the strikes are expanding President Donald Trump's military options should he choose to intensify the conflict. That interpretation helps explain why traders have become less reactive to individual headlines: markets are now focused less on the strikes already underway than on whether they evolve into a materially larger campaign over the coming days.

Currency performance this week also reflects evolving macro themes rather than a traditional flight to safety. New Zealand Dollar remains the strongest performer as markets continue to price additional RBNZ tightening. Canadian Dollar ranks second, supported by elevated oil prices and the Bank of Canada's more constructive assessment of the domestic economy. Sterling has benefited from optimism that incoming Prime Minister Andy Burnham's cabinet will pursue greater fiscal discipline. At the other end of the spectrum, Yen remains the weakest currency, followed by Dollar and Swiss Franc.

Brent Holds Below $90 as Markets Wait for the Next Escalation Trigger. Is $100 Next?

Brent crude has stalled below $90 despite escalating military conflict between the United States and Iran. The pause reflects two key factors: Washington is simultaneously escalating military operations while easing some commercial measures, and traders are waiting for a genuine supply shock before pricing another sustained leg higher in oil. Read More.

EUR/GBP and GBP/CHF Channel Breakouts as Burnham's Cabinet Choice Signals Fiscal Discipline

Sterling rallied after reports that Andy Burnham will appoint Shabana Mahmood as Chancellor, a move investors see as an early commitment to fiscal discipline. Rather than focusing on the change in prime minister alone, markets are now repricing the UK's fiscal outlook, helping EUR/GBP and GBP/CHF break through key technical channels. Read More.

US Retail Sales Rise 0.2% MoM in June as Consumer Spending Stays Resilient

US retail sales rose 0.2% in June, matching expectations and extending the expansion in consumer spending. Combined with an upward revision to May's 1.0% gain, the report suggests households continue to support economic growth despite elevated interest rates and geopolitical uncertainty. Read More.

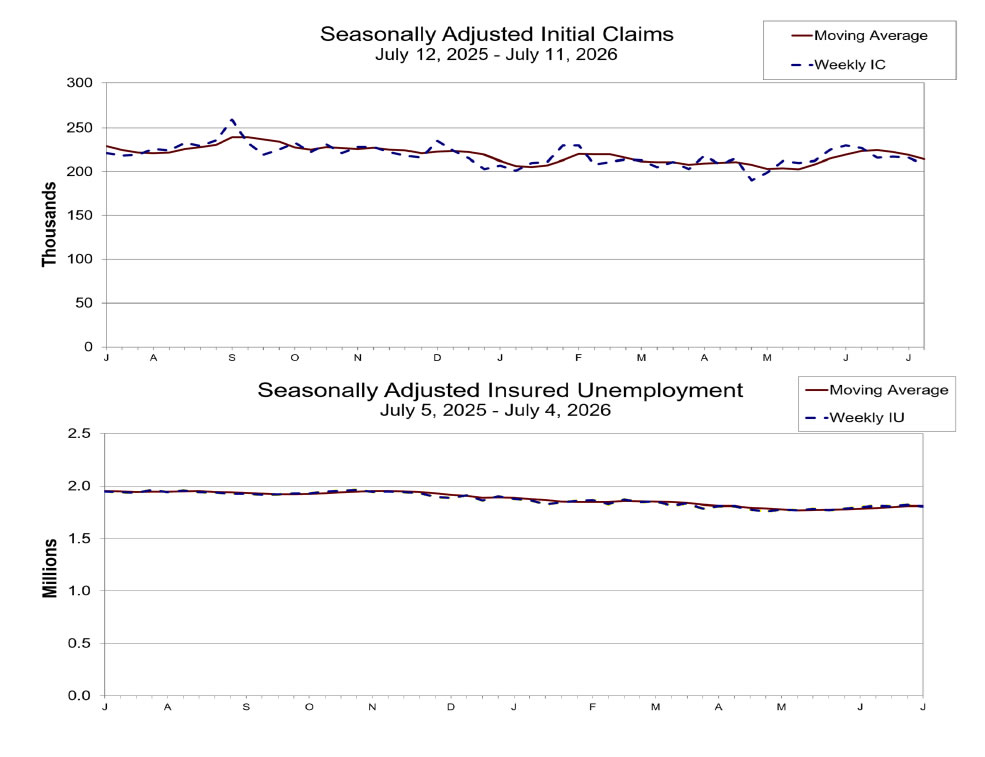

US Initial Jobless Claims Decline to 208k as Labor Market Holds Firm

The US labor market remained resilient in mid-July, with initial jobless claims falling to 208,000, below expectations. The decline, together with a lower four-week average, suggests layoffs remain limited despite broader signs that the economy and inflation are gradually cooling. Read More.

Eurozone Trade Swings to Deficit as Imports Surge Despite Stable Exports

The Eurozone's goods trade balance swung to a €7.8 billion deficit in May as imports surged 10.0% year-on-year, easily outpacing 0.1% export growth. The data suggest the deterioration was driven primarily by higher import costs and stronger import demand, rather than a collapse in exports. Read More.

SNB Minutes: Inflation Risks Rise, But 'No Immediate Need for Action'

The SNB's June policy minutes show policymakers becoming more concerned about inflation risks without seeing a need to tighten policy. While acknowledging that oil prices and geopolitical tensions have increased upside inflation risks, the Governing Board concluded there is "no immediate need for action" because "price stability is not jeopardised." Read More.

BoE's Breeden Says Soft Growth Reduces Need for Rate Hikes

BoE Deputy Governor Sarah Breeden argued that the UK's weak economic outlook and labour market slack should prevent the latest surge in oil prices from becoming persistent inflation. Her comments reinforce the view that the Bank of England can keep rates on hold unless higher energy costs begin feeding into wages and broader price-setting. Read More.

UK GDP Grows 0.1% MoM in May as Services Offset Weak Production and Construction

The UK economy grew 0.1% in May, slightly beating expectations after April's contraction. Growth was driven entirely by the services sector, while production (-0.5%) and construction (-0.8%) both declined, highlighting an expansion that remains resilient but uneven. Read More.

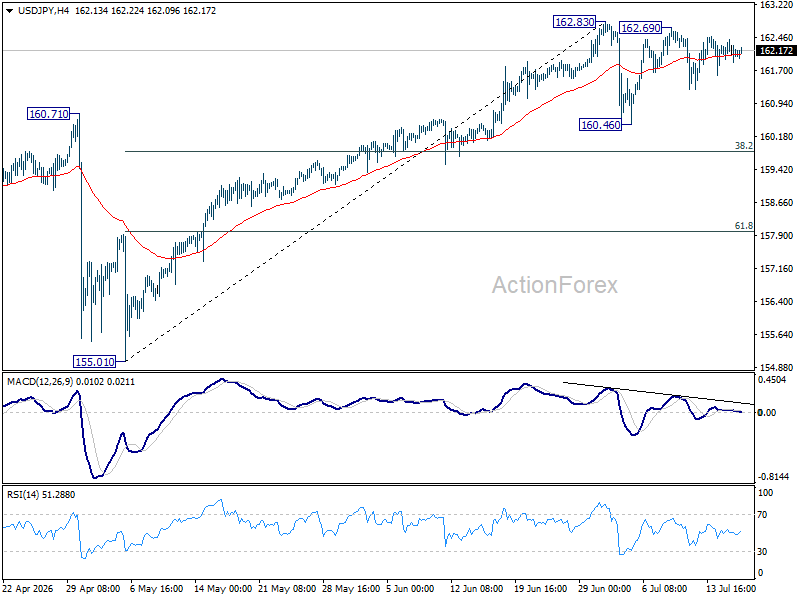

USD/JPY Daily Outlook

No change in USD/JPY's outlook as consolidations continue below 162.83. Intraday bias stays neutral at this point. In case of another fall, downside should be contained by 38.2% retracement of 155.01 to 162.83 at 159.84. On the upside, firm break of 162.83 will resume larger up trend to 164.34 projection level.

In the bigger picture, rise from 139.87 (2025 low) is seen as another rising leg of the long term up trend. Next target is 61.8% projection of 139.87 to 159.44 from 152.25 at 164.34. For now, outlook will remain bullish as long as 155.01 support holds, even in case of deep pullback.

U.S. Retail Sales Rise Modestly in June

- Retail and food services sales rose 0.2% month-over-month (m/m) in June, in line with expectations for a 0.3% gain. On an inflation-adjusted basis, retail sales rose by 0.6% on the month.

- Sales at gasoline stations (-5.3% m/m) were lower, but that was entirely due to a sharp drop in prices at the pump. Removing the price effects, real gasoline sales were higher by 4.9%. Meanwhile, sales of autos and parts remained robust, advancing by 1.9% m/m in June and were up 3% on the second quarter, a notable acceleration relative to the prior two quarters. Sales at building materials and garden retailers were little changed (+0.1% m/m).

- Within the “control group”—which excludes volatile sales of gasoline, autos and parts, and building materials and garden equipment—sales fared better than the headline, advancing by 0.5% m/m. There were notable gains at sporting goods stores (+1.3% m/m) and electronics and appliance retailers (+0.8% m/m). Sales at non-store retailers, continued to rise at a brisk pace (+1.9% m/m). Zooming out, non-store sales are up 14.2% from a year ago.

- Sales were little changed to lower in the remaining categories, such as food and beverage stores (+0.2%), general merchandise stores (+0.1%), and health and personal care stores (-0.8%).

- Spending at bars and restaurants—the only service category included in the report—remained flat in June and were up only 3.8% y/y, down from 6.8% y/y growth in June 2025.

Key Implications

- Retail sales posted a modest headline gain in June, as lower gasoline prices weighed on nominal gas station receipts and held back overall growth. However, the underlying details were more encouraging, with solid gains in control group sales and inflation-adjusted spending. With respect to inflation, the latest CPI report also showed that price pressures broadly eased in June, offering some reprieve to inflation-wary consumers.

- Overall, this was a solid report, suggesting that consumer spending remains on track to increase by about 2% annualized in Q2 – a notable pick up from Q1's 0.5% and consistent with our economic forecast. While some pockets of caution remain—such as modest growth in sales at bars and restaurants and grocery stores—consumer spending remained resilient through a second quarter, as elevated energy prices were partially offset by higher tax refund checks, rising equity market valuations, and some stabilization in the labor market.

US Retail Sales Rise 0.2% MoM in June as Consumer Spending Stays Resilient

US retail sales increased modestly in June, suggesting consumer spending continued to expand despite elevated interest rates and lingering uncertainty surrounding energy prices. Advance estimates from the Census Bureau showed retail and food services sales rose 0.2% mom to USD 768.6 billion, matching market expectations. The gain followed an upward revision to May's increase to 1.0% from 0.9%, indicating household spending entered the second quarter on a firmer footing than previously estimated.

The broader trend also remained solid. Retail sales were 6.7% higher than a year earlier, while total sales during the April-June period increased 6.4% from the same period in 2025. Although June's monthly increase represented a moderation from May's strong gain, it extended the run of positive consumer spending and suggested households continue to support economic growth despite tighter financial conditions.

Excluding motor vehicles and parts, sales slipped -0.2% mom, reflecting some moderation in discretionary purchases, while sales excluding gasoline stations rose 0.7%, indicating underlying consumer demand remained resilient even as fuel prices became more volatile.

Economic Data

| Indicator | Actual | Expected | Previous |

|---|---|---|---|

| Retail Sales MoM (Jun) | 0.2% | 0.2% | 1.0% |

| Retail Sales YoY (Jun) | 6.7% | — | — |

| Retail Sales (Apr-Jun) YoY | 6.4% | — | — |

| Retail Sales ex Autos MoM (Jun) | -0.2% | 0.0% | 1.0% |

| Retail Sales ex Gasoline MoM (Jun) | 0.7% | — | 0.9% |

Key Takeaways

- Headline retail sales rose 0.2% mom, matching expectations and extending consumer spending growth into June.

- May sales were revised higher to 1.0% from 0.9%, indicating stronger spending momentum entering the second quarter than previously estimated.

- Retail sales were 6.7% higher than a year earlier, while April-June sales increased 6.4% y/y, pointing to continued resilience in household demand.

- Sales excluding motor vehicles fell 0.2%, suggesting some moderation in discretionary spending after May's strong gain.

- Sales excluding gasoline stations rose 0.7%, indicating underlying consumer demand remained healthy despite volatility in fuel prices.

US Initial Jobless Claims Decline to 208k as Labor Market Holds Firm

Initial jobless claims fell more than expected last week, suggesting the US labor market remains resilient despite moderation in economic activity elsewhere. The Labor Department reported that seasonally adjusted initial claims declined by -8,000 to 208,000 in the week ended July 11, below market expectations of 218,000. The previous week's figure was revised up slightly to 216,000, while the four-week moving average fell by -4,750 to 214,250, indicating that layoffs remain historically subdued rather than reflecting week-to-week volatility.

Continuing claims also pointed to a broadly stable labor market. The number of Americans receiving unemployment benefits fell by -16,000 to 1.805 million in the week ended July 4, while the insured unemployment rate held steady at 1.2%. Although the four-week average of continuing claims edged up slightly to 1.811 million, the increase was marginal and continues to suggest that workers losing jobs are generally able to find new employment without a significant deterioration in labor market conditions.

Economic Data

| Indicator | Actual | Expected | Previous |

|---|---|---|---|

| Initial Jobless Claims | 208K | 218K | 216K |

| 4-Week Average (Initial Claims) | 214.25K | — | 219.00K |

| Continuing Claims | 1.805M | — | 1.821M |

| Insured Unemployment Rate | 1.2% | — | 1.2% |

| 4-Week Average (Continuing Claims) | 1.811M | — | 1.810M |

Key Takeaways

- Initial jobless claims fell to 208K, beating expectations of 218K and marking another sign that layoffs remain subdued.

- The four-week average declined to 214.25K, reinforcing that the improvement is broader than weekly volatility.

- Continuing claims fell by -16K to 1.805M, indicating unemployed workers are still finding new jobs without a material deterioration in hiring conditions.

- The insured unemployment rate held steady at 1.2%, consistent with a labor market that remains fundamentally healthy.

- Taken together, the data suggest the US labor market is cooling gradually rather than weakening sharply

BoE’s Breeden Says Soft Growth Reduces Need for Rate Hikes

Bank of England Deputy Governor Sarah Breeden suggested that the recent rebound in oil prices is unlikely to trigger persistent inflation, arguing that the UK's weak economic backdrop should prevent higher energy costs from feeding into wages and broader price-setting behaviour. Speaking to Bloomberg TV, Breeden acknowledged that renewed fighting between the United States and Iran has once again clouded the inflation outlook, but indicated that monetary policy does not need to respond unless there is evidence of second-round inflation effects becoming embedded.

"We have a softish economic outlook; we have slack in the labor market," Breeden said. "Those two things mean that that shock is less likely to become embedded and lead to inflationary dynamics that we might need to lean against." The remarks reinforce the Bank's current wait-and-see approach.

Breeden, one of the more dovish members of the Monetary Policy Committee, noted that she had expected inflation to return to the Bank's 2% target were it not for the renewed conflict in the Middle East. While acknowledging that energy prices remain highly uncertain, she stressed, "I said back in June that I expected the outlook for energy prices to be uncertain, and I think that has proved to be the case."

Even so, Breeden made clear that the BoE is not ruling out tighter policy if inflation proves more persistent. She said she would support higher interest rates should higher energy costs begin feeding into wages and corporate pricing decisions, creating a broader inflation feedback loop.

EUR/USD Daily Outlook

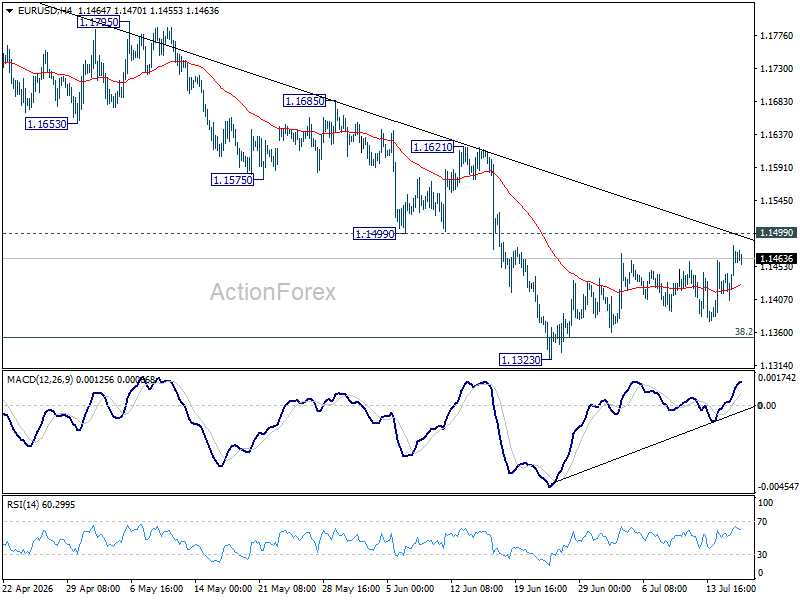

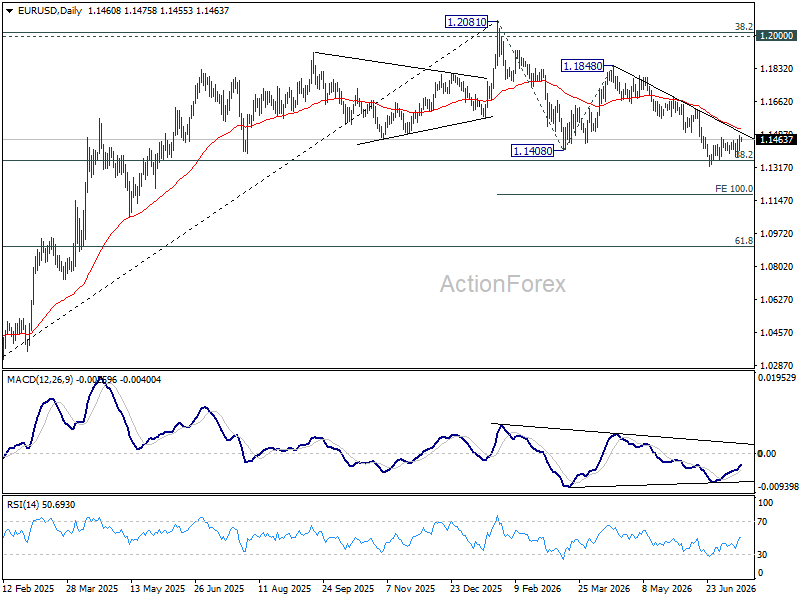

Intraday bias in EUR/USD stays neutral at this point, as consolidations continue above 1.1323. With 1.1499 support turned resistance intact, further decline is expected. On the downside, break of 1.1323 will resume the fall from 1.2081 to 100% projection of 1.2081 to 1.1408 from 1.1848 at 1.1175. However, decisive break of 1.1499 will turn bias back to the upside for 1.1621 resistance.

In the bigger picture, focus is back on 38.2% retracement of 1.0176 to 1.2081 at 1.1353. Decisive break there will revive the case of medium term bearish trend reversal after rejection by 1.2 key cluster resistance level. Further fall should be seen to 61.8% retracement at 1.0904. Nevertheless, strong rebound from 1.1353, followed by break of 1.1621 resistance, will retain medium term bullishness.

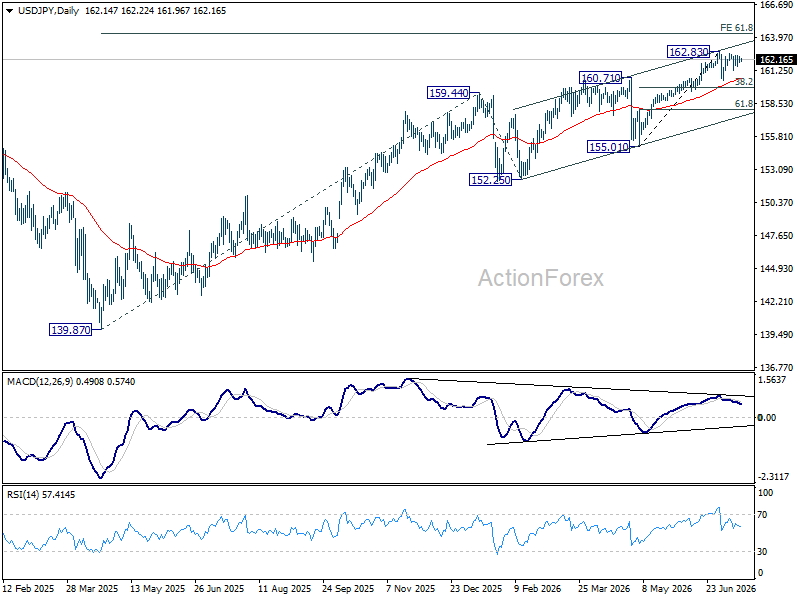

USD/JPY Daily Outlook

No change in USD/JPY's outlook as consolidations continue below 162.83. Intraday bias stays neutral at this point. In case of another fall, downside should be contained by 38.2% retracement of 155.01 to 162.83 at 159.84. On the upside, firm break of 162.83 will resume larger up trend to 164.34 projection level.

In the bigger picture, rise from 139.87 (2025 low) is seen as another rising leg of the long term up trend. Next target is 61.8% projection of 139.87 to 159.44 from 152.25 at 164.34. For now, outlook will remain bullish as long as 155.01 support holds, even in case of deep pullback.

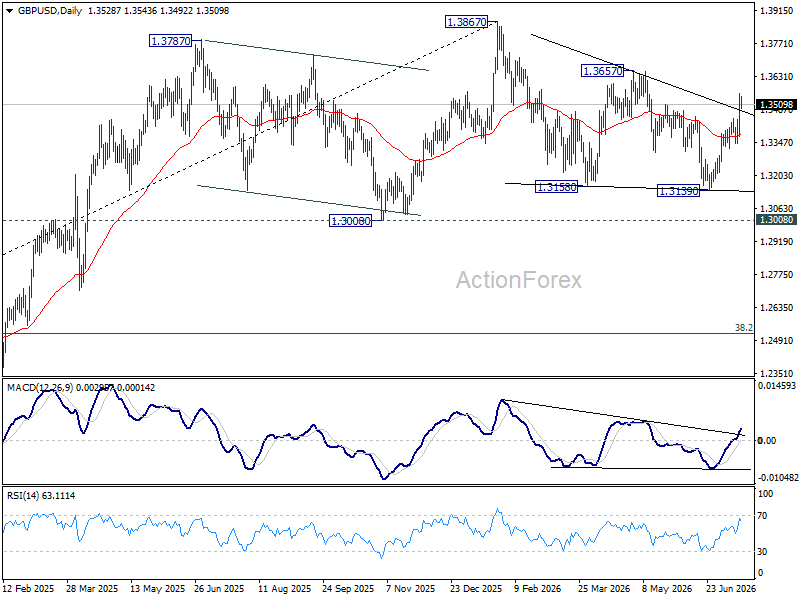

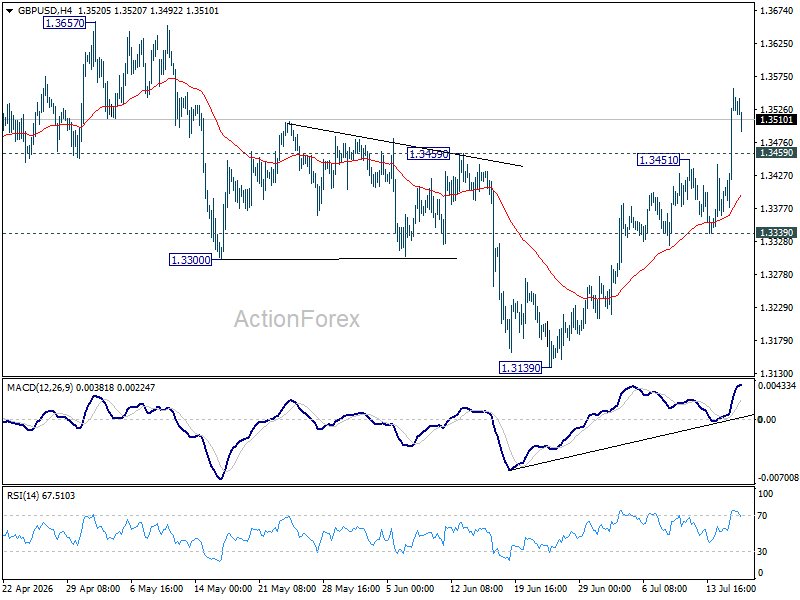

GBP/USD Daily Outlook

GBP/USD's rally resumed and the break of 1.3459 resistance argues that whole correction from 1.3867 has completed at 1.3139. Intraday bias is back on the upside for 1.3657 resistance for confirmation. For now, risk will stay on the upside as long as 1.3339 support holds, in case of retreat.

In the bigger picture, price actions from 1.3867 are a corrective pattern within the broader up trend from 1.0351 (2022 low). With 1.3008 support intact, medium term bullishness is maintained and break of 1.3867 is in favor for a later stage, towards 1.4248 key resistance (2021 high). However, firm break of 1.3008 will at least bring deeper fall to 38.2% retracement of 1.0351 to 1.3867 at 1.2524, with increased risk of bearish reversal.