Sample Category Title

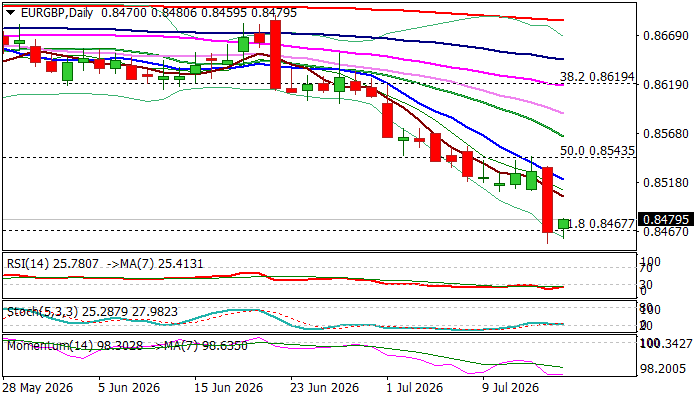

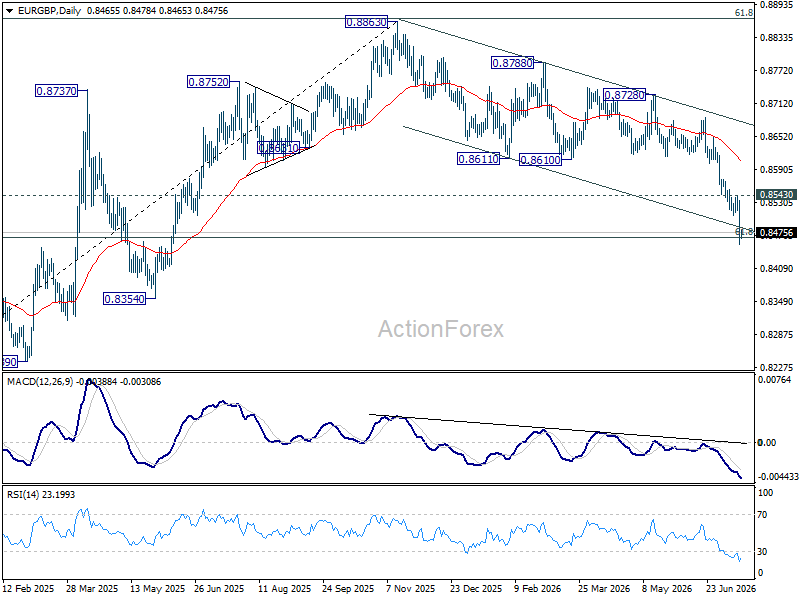

EURGBP – Bears Take a Breather Above 13-Month Low

EURGBP edges higher in early Thursday after hitting 13-month low following 0.8% drop on Wednesday (the biggest daily loss since June 22), when the pound was strongly lifted by signals that new PM Burnham will pick a fiscally conservative finance minister to be in charge of handling fragile public finances.

Oversold daily studies contributed to partial profit-taking after strong fall on Wednesday, with limited upticks seen rather as positioning for fresh push lower, as larger downtrend remains intact.

Technical picture on daily chart remains bearish, though with overstretched momentum studies that open way for some corrective action.

Falling 10DMA (0.8520) should ideally cap and guard upper breakpoints at 0.8550 zone (broken 50% retracement of 0.8222/0.8865 rally / 100WMA), violation of which may sideline larger bears for stronger bounce that would unmask next key barriers at 0.8600/10 zone (200WMA / former range floor and higher base).

Firm break of cracked Fibo support at 0.8467 (61.8% of 0.8222/0.8865) where bears faced strong headwinds on Wednesday / today, would signal continuation of larger downtrend and expose targets at 0.8373 (Fibo 76.4%) and 0.8355 (29 May 2025 low).

Res: 0.8500; 0.8520; 0.8550; 0.8600

Sup: 0.8467; 0.8449; 0.8373; 0.8355

Brent Holds Below $90 as Markets Wait for the Next Escalation Trigger. Is $100 Next?

Brent crude has delivered an interesting message this week. Prices briefly climbed to USD 87.55 as fighting between the United States and Iran intensified, yet the rally quickly lost momentum even as military operations continued across the Middle East. The hesitation should not be mistaken for complacency. Rather, it reflects a market that sees the conflict becoming more dangerous but is still waiting for the event that would fundamentally alter the outlook for global oil supply. Until then, the USD 89-90 region is likely to remain formidable resistance.

There are two reasons why the rally has stalled.

The first is that escalation and partial retreat are unfolding simultaneously—and from the same actor. The United States has expanded its military campaign for a fifth straight day, targeting Iranian missile sites and coastal defences while maintaining a naval blockade of Iranian ports. At the same time, however, Washington abandoned its proposed 20% Hormuz shipping fee after legal objections from the International Maritime Organization and strong opposition from the shipping industry. The military conflict has intensified, but one of the week's most disruptive commercial measures has quietly been removed. Those mixed signals have left traders reluctant to push prices aggressively higher.

The second reason is that traders appear to be waiting for a much higher threshold before pricing another sustained leg higher in oil. Military strikes on missile batteries, coastal defences and naval assets have so far had only a limited direct impact on oil production or exports. What the market is watching instead is whether the conflict expands into infrastructure that directly underpins global energy supply. US President Donald Trump may already have identified that trigger by warning that unless Tehran returns to negotiations, the United States could strike Iranian power plants, bridges and ultimately energy infrastructure next week. Such attacks would represent a fundamentally different category of escalation. On the other side, Iranian parliamentary speaker Mohammad Baqer Qalibaf declared the country was engaged in an "existential war" with the United States, argued Iran's security depends on controlling the Strait of Hormuz, and suggested Tehran has little reason to continue adhering to last month's memorandum of understanding. Those developments keep the risk of broader disruption to Gulf energy exports firmly alive.

If such an escalation occurs, the market may prove far more sensitive than earlier this year. IMF economists Azim Sadikov and Jean-Marc Natal warned this week that the global oil market's spare production capacity has been meaningfully depleted after months of increased output, inventory drawdowns and demand adjustment. Their assessment is that the world will enter the next supply shock from a much weaker position than it did in March. In other words, while Brent has struggled to extend gains above USD 87 this week, the market's ability to absorb a genuinely new disruption has become increasingly limited.

That backdrop leaves Brent at an important technical inflection point. The bounce from 70.14 short term bottom is, for now, seen as a corrective move only. While further rise cannot be ruled out, upside should be limited by 38.2% retracement of 119.50 to 70.14 at 89.00. Break of 80.59 resistance turned support will argue that the rebound has completed.

However, decisive break of 89.00 will raise the chance that it's actually reversing whole fall from 119.50 to 70.14. That would set up further rise to 61.8% retracement at 100.64, and possibly above.

The Pound: from Outsider to Favourite

- Rumours of a less profligate Treasury than expected have boosted GBPUSD.

- The US dollar is falling as the likelihood of monetary tightening by the Fed has diminished.

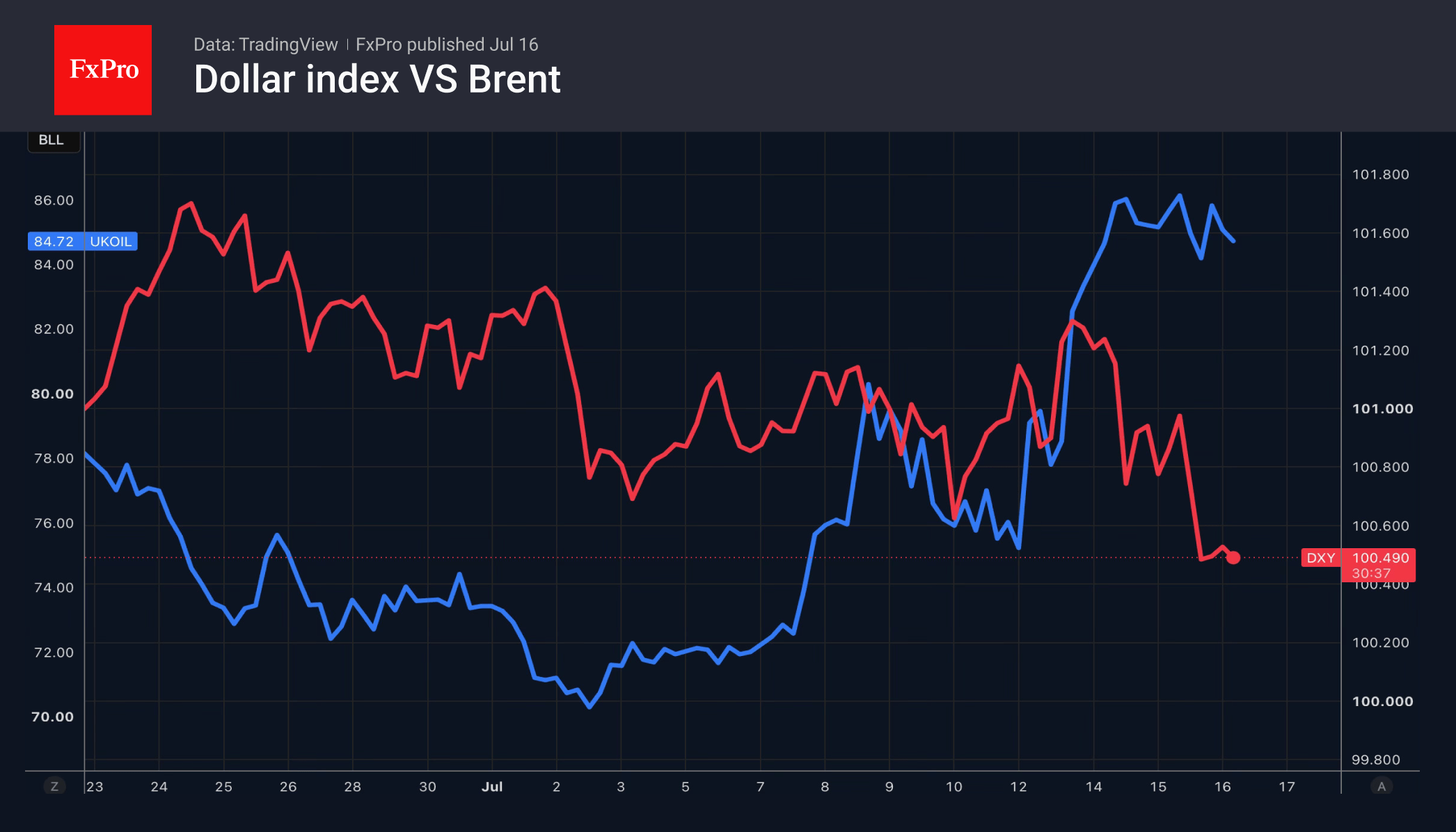

The US dollar is no longer finding support from oil. Brent is trading near monthly highs, while the USD index continues to fall. Investors are in no hurry to buy the greenback as a safe-haven ticket amid the escalation in the Middle East. The US President’s threats may well be part of his negotiating strategy. Instead, the markets are following the old playbook on geopolitics.

At the start of the US-Iran standoff, the dollar enjoyed increased demand as the rally in Brent crude accelerated inflation and raised the chance of a Fed Rate hike. Later, in April, the USD index fell as investors concluded that oil would be unable to reclaim its March highs. This implied that inflation would soon peak.

Something similar is happening in July. The month-on-month decline in consumer and producer prices is leading investors to believe that inflation peaked in May. If so, there is no need for the Fed to tighten monetary policy. This reduces the likelihood of a rate hike and causes the US dollar to retreat.

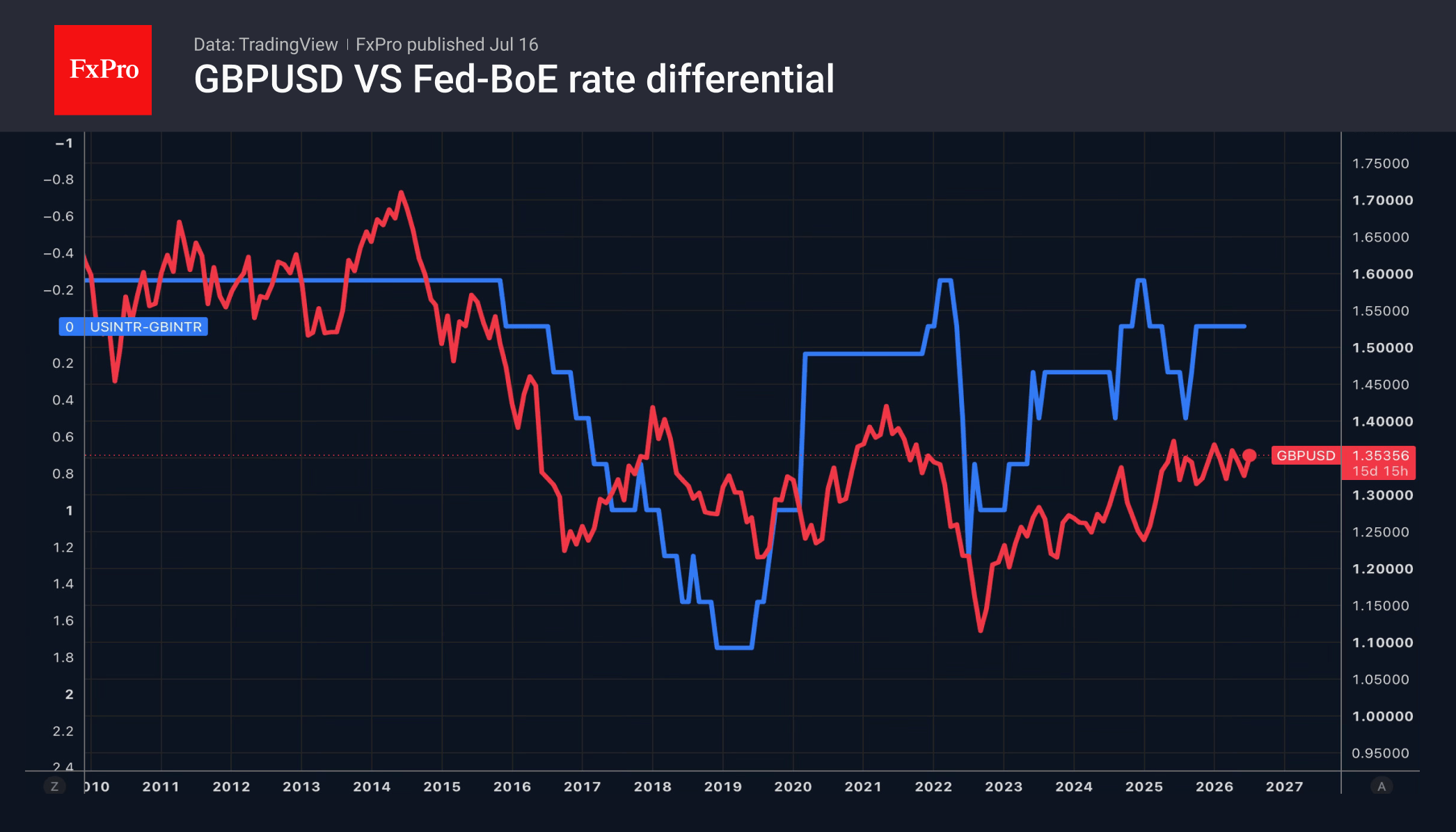

Other currencies are capitalising on its weakness. For instance, the British pound has been the best-performing G10 currency over the past month, thanks to reduced political risk. The incoming Prime Minister, Andy Burnham, is set to stick to the old rules of fiscal consolidation. Meanwhile, rumours that he will appoint a less spendthrift Chancellor than expected have driven GBPUSD to its highest level since early May.

Divergences in monetary policy are also supporting sterling. The futures market is pricing in a lower probability of aggressive monetary tightening by the Fed, simultaneously signalling confidence in two hikes by the Bank of England in 2026. The first of these could take place in September.

Meanwhile, Japan appears to have found a stronger hand for the yen than threats of currency intervention or rumours of a tightening of the BoJ’s monetary policy. USDJPY has remained range-bound following a statement by Satsuki Katayama. The finance minister announced that she would take measures to encourage the GPIF to purchase domestic assets.

The FxPro Analyst Team

Gold Is Rapidly Declining in Price: Statistics Hardly Help

Gold fell to 4,033 USD per ounce on Thursday, extending its losing streak. Pressure on the market is being exerted by a sharp rise in oil prices amid intensified attacks in the Middle East, which is once again heightening inflationary fears and expectations of tighter central bank policies.

On Wednesday, the United States launched new strikes on Iranian targets. At the same time, Donald Trump stated that Tehran had signalled its readiness to return to negotiations, which somewhat reduced the geopolitical temperature.

Some support for gold came from weaker-than-expected US inflation data. In June, producer prices unexpectedly fell for the first time in nearly a year, largely due to cheaper energy. Earlier, softer-than-forecast consumer inflation data were also released.

However, June's figures do not yet reflect the consequences of the renewed US-Iran conflict. The interim peace deal reached last month has effectively lapsed, meaning the risks of accelerating inflation and further pressure on gold remain firmly in place.

Technical Analysis

On the H4 XAU/USD chart, the market has formed a consolidation range around the 4,060 USD level. A downward wave to 4,015 USD and a growth leg to 4,080 USD have been completed. A continuation of the downward wave to 3,920 USD is expected, followed by a potential rise to 4,055 USD, with the prospect of the wave extending to 4,150 USD. The MACD indicator confirms the current downside momentum, with its signal line below the centre line and pointing strictly downwards.

On the H1 chart, the market has broken below the 4,060 USD level and is forming a downward wave structure towards 4,012 USD. A wide consolidation range is practically forming around 4,060 USD. The Stochastic oscillator confirms this scenario, with its signal line remaining below the 50 level and under pressure to decline to 20.

Conclusion

Gold continues its sharp decline as rising oil prices and heightened Middle East tensions reinforce inflationary fears and expectations of tighter monetary policy. While US inflation data for June came in softer than expected-with producer prices unexpectedly falling-these figures predate the collapse of the interim peace deal and the renewed US-Iran hostilities. As a result, the risks of accelerating inflation and further pressure on gold remain firmly intact. Technical indicators point to further downside towards 3,920 USD, with any recovery likely to be capped by persistent geopolitical and inflation concerns. The metal's safe-haven appeal is being overshadowed by the prospect of sustained central bank tightening.

SNB Minutes: Inflation Risks Rise, But ‘No Immediate Need for Action’

The Swiss National Bank's June policy minutes show policymakers becoming more concerned about inflation risks but not sufficiently alarmed to warrant tighter monetary policy. While the Governing Board acknowledged that higher energy prices and geopolitical tensions have increased upside risks to inflation, it concluded there was "no immediate need for action" and reaffirmed that "monetary conditions are appropriate and price stability is not jeopardised." Those assessments explain why the SNB left its policy rate unchanged at 0%.

The discussions repeatedly highlighted the Middle East as the principal source of uncertainty. Policymakers warned that a prolonged disruption to shipping through the Strait of Hormuz could further tighten energy markets, noting that "economic growth could be weaker and inflation higher than expected" if passage were impaired for an extended period. At the same time, the Governing Board judged that medium-term inflation dynamics had changed little, stating that "medium-term inflationary pressure is virtually unchanged compared with the monetary policy assessment in March." While members acknowledged that "inflation risks have increased in recent months and stronger second-round effects are possible," they also concluded that inflation is not expected to "rapidly rise above 2% or fall into negative territory."

Beyond inflation, the minutes portrayed an economy that continues to perform reasonably well. GDP growth in the first quarter was described as solid, with "numerous economic indicators" pointing to positive momentum, although labour market conditions remained subdued. The Governing Board also maintained a clear focus on the exchange rate, warning that the risk of excessive Swiss franc appreciation persists amid heightened geopolitical uncertainty. As a result, policymakers reiterated that the SNB's willingness to intervene in the foreign exchange market should "remain increased" if necessary to prevent an excessive appreciation that could threaten price stability. Together, the minutes reinforce an SNB that is comfortable remaining on hold while keeping both oil markets and the franc under close watch.

Market Takeaways

- The minutes reinforce that the SNB remains comfortable keeping the policy rate at 0%.

- Policymakers acknowledge higher oil-driven inflation risks but continue to view them as temporary rather than persistent.

- The SNB remains highly sensitive to excessive Swiss franc appreciation and reiterated its readiness to intervene in FX markets.

- Unless oil prices rise substantially further or second-round inflation effects emerge, the bar for another policy move remains high.

Dow Jones (DJIA): Consolidation Beyond the Trend

Federal Reserve Chair Kevin Warsh testified before Congress on 14–15 July, reaffirming the Fed's commitment to bringing inflation back to target while providing no clear guidance on the future path of interest rates. Meanwhile, June inflation data came in softer than expected, with annual consumer price growth slowing to 3.5% from 4.2% in May, temporarily supporting risk appetite. At the same time, the earnings season got underway, with Goldman Sachs reporting better-than-expected results on 14 July, providing additional support for the Dow Jones Industrial Average index (Wall Street 30 on FXOpen).

Technical Picture

The Dow Jones Index (WS30m on FXOpen) advanced along an ascending trendline from its 23 June low, reaching the 53,400 area on 7 July, marked by the red resistance level. A sharp decline then followed, breaking below the trendline, with prices subsequently consolidating within the range of the large bearish breakout candle. Since then, the index has been trading within the current market profile, compressed between the profile's upper boundary at 52,770 and the Point of Control (POC) at 52,550, awaiting a catalyst to break out of the current range.

If the bearish scenario unfolds and the price falls below both the trendline and the lower boundary of the market profile at 52,240, market participants might focus on the 51,750 area, where the index could potentially find support during a further decline. The RSI + MAs indicator currently shows readings of 55, 49, and 50 respectively, with all three remaining in neutral territory and providing no clear directional signal.

Summary

With the RSI lacking momentum and price remaining confined to a narrow range between the POC and the upper boundary of the market profile, the market appears to be in a pause following the failed trend breakout. A potential catalyst for a decisive move could come from the US June Retail Sales report, due later today, 16 July, while the Federal Reserve's policy meeting on 29 July may provide the next major directional trigger.

Trade global index CFDs with zero commission and tight spreads (additional fees may apply). Open your FXOpen account now or learn more about trading index CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

European Currencies Strengthen Ahead of Key Macroeconomic Releases

EUR/USD and GBP/USD continue to recover moderately following the recent weakening of the US dollar. European currencies have been supported by expectations that US inflationary pressures will continue to ease after softer-than-expected CPI and PPI data, reinforcing market hopes for a more accommodative Federal Reserve policy. However, the upside potential for both the euro and the pound remains limited amid persistent geopolitical tensions. The United States continues to carry out strikes against targets in Iran, supporting demand for defensive assets and periodically boosting the US dollar.

Today, traders will closely monitor a series of important economic releases from the United Kingdom, the eurozone, and the United States, which could determine the next direction for the major currency pairs.

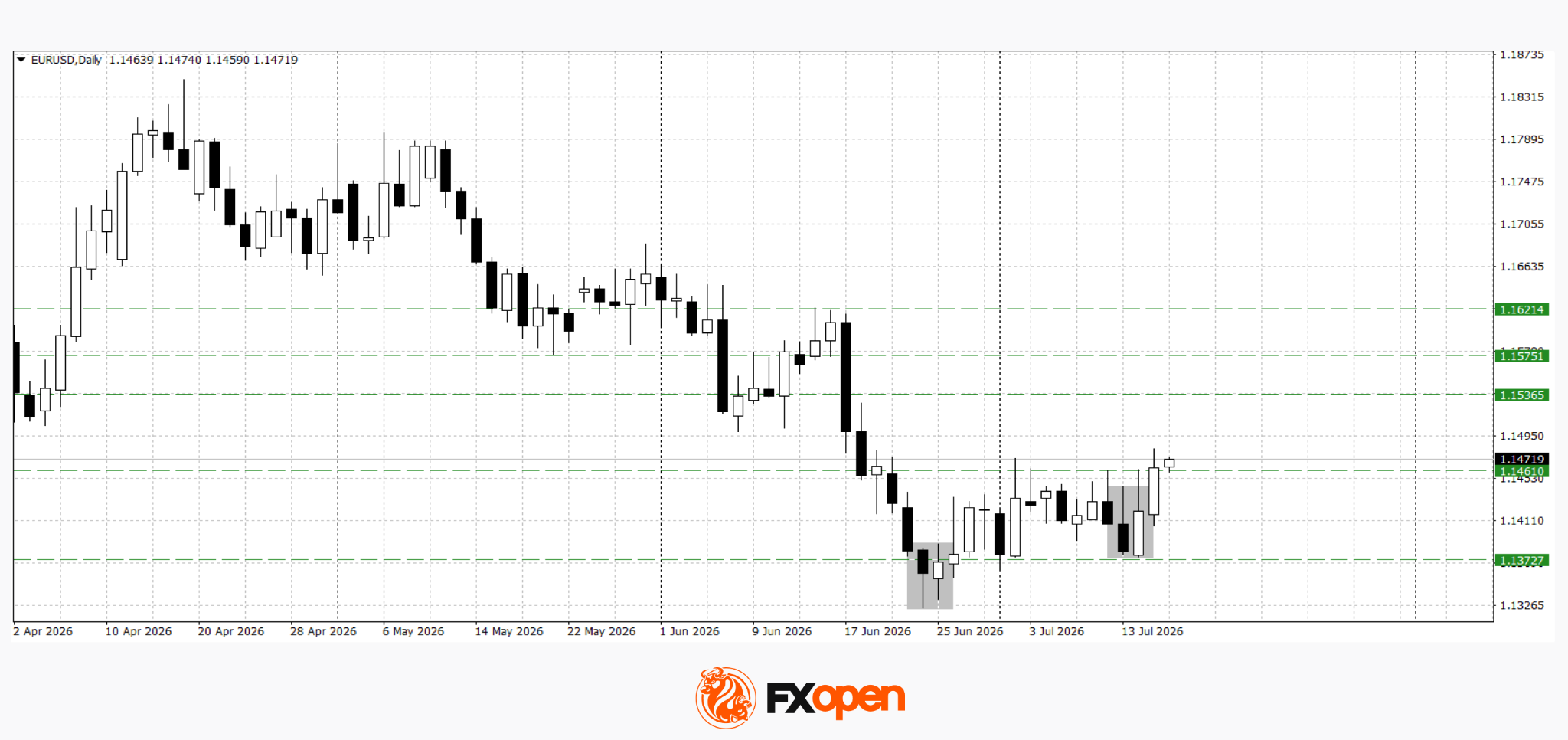

EUR/USD

EUR/USD continues to develop after a bullish engulfing reversal pattern while attempting to establish itself above the key resistance level at 1.1460. Technical analysis suggests the pair could extend its advance towards the 1.1540–1.1580 area. The bullish scenario would be invalidated by a decisive move below 1.1370.

Key events for EUR/USD:

- 11:40 (GMT+3): Spain 10-year government bond auction;

- 15:30 (GMT+3): US Core Retail Sales;

- 15:30 (GMT+3): US Philadelphia Fed Manufacturing Index.

GBP/USD

GBP/USD is recovering more strongly than EUR/USD. Buyers have managed to establish the pair above the important 1.3500 resistance level, and positive UK macroeconomic data could pave the way for a further advance towards the 1.3610–1.3680 region. At the same time, after such a rapid rally, a corrective pullback could see the pair retest the 1.3440–1.3480 area, this time as support.

Key events for GBP/USD:

- 09:00 (GMT+3): UK Gross Domestic Product (GDP);

- 14:00 (GMT+3): NIESR Monthly UK GDP Tracker;

- 18:30 (GMT+3): Atlanta Fed GDPNow estimate.

Overall, European currencies retain the potential to extend their recovery as markets continue to price in a more accommodative Federal Reserve. However, today's economic releases from the UK, the eurozone, and the US could significantly reshape market sentiment. If US data once again disappoint expectations, EUR/USD and GBP/USD may receive additional support. Conversely, stronger-than-expected US figures could revive demand for the dollar and limit further gains in European currencies.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips (additional fees may apply). Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Sunset Market Commentary

Markets

The US Treasury curve bull steepened for a second session straight. Markets mirrored Tuesday's post-CPI reaction after a more benign June PPI report. Headline producer price inflation fell by 0.3% M/M and slowed from 6% Y/Y to 5.5%. Core PPI rose by 0.2% M/M and ticked up from 4.6% Y/Y to 4.7%. Both were below consensus and further squeezed July rate hike bets towards 0%. Recall that they temporary hit 50% at the start of the week. Fed governor Cook stated that upside inflation risks are the priority now with all indicators pointing to a stable labour market. She's prepared to act in absence of disinflation signs (soon). Deprived of interest rate support, the dollar lost some more ground with EUR/USD closing at 1.1463 from a start at 1.1420. Clearing 1.1481/1.15 would make the short term technical picture again more neutral instead of USD-positive. Today's eco calendar contains US retail sales and more Fed speeches, but their market-moving potential is low after the past two days' repositioning. US President Trump holds a primetime address to the nation which serves as a wildcard for trading. He is expected to focus on elections and voting machines, but is notorious for going off-script and tackling a wider variety of topics. Energy prices remain elevated as the US keeps launching Iranian strikes.

Sterling had a good run yesterday. EUR/GBP fell below the 0.85 big figure for the first time since June last year and tested 0.8468 technical support (62% retracement on Dec24-Nov25 move). Losing that marker leaves little intermediate support towards full retracement (0.8223). At best, we're looking at 0.8372 (76% retracement) and 0.8330 (final target of multiple top formation with neckline at 0.86). Cable (GBP/USD) cleared the 1.34 mark and rallied to its best close (1.3540) since early May. Markets took comfort from an FT article indicating that incoming UK PM Burnham selected current Home Secretary Mahmood as next Chancellor. Mahmood is seen as more orthodox than Ed Miliband, Labour's left favorite to fill the job. With little capacity for expansionary fiscal policy, market focus will now be on delivering in the Autumn budget. On the UK data front, monthly labour market numbers and inflation figures are scheduled for next week. They'll help shape expectations for the Bank of England's reaction function. UK money markets currently discount a rate hike by the November meeting. BoE governor Bailey in a speech earlier this week kept a more balanced approach (than some of his colleagues), prioritizing supporting growth over an activist monetary policy response given inflation risks.

News & Views

South Korea's central bank raised interest rates from 2.5% to 2.75% today. The first hike in three years caps an increasingly hawkish rhetoric over the last couple of months and won't be the last. Governor Shin Hyun Song just last week before parliament warned rates would have to be raised at an appropriate time. Above-target inflation, an AI/semiconductor led economic boom, a weak exchange rate and increasing financial stability risks have eventually culminated in today's move. "It is judged that it will be necessary to continue a policy stance consistent with further rate hikes, and the Board will determine the timing and pace of further increases in the Base Rate while assessing the extent of inflationary pressure, the improvement trend in the domestic economy, and financial stability," the statement reads. The South Korean won benefits from the strong language and appreciates to the best levels since mid-May around USD/KRW 1480.6.

The US administration slaps Brazil with a 25% tariff levy, effective July 22. The import tariffs won't affect US imports of coffee, beef and certain ethanol products. They are the result of an investigation pursued under Section 301 of the Trade Act of 1974 which "found a number of Brazil's practices to be unreasonable and discriminatory, restricting the competitive position of American farmers, workers, innovators, and exporters." The US is Brazil's second-largest trading partner and one of the few major economies with which it runs a trade deficit. US President Trump last year imposed 50% tariffs on a wide range of products to pressure Brazilian authorities over the prosecution of former President Bolsonaro. Most of them were rolled back following negotiations between current president Lula and Trump. New presidential elections are due in October with Lula's main challenger being the son of Bolsonaro.

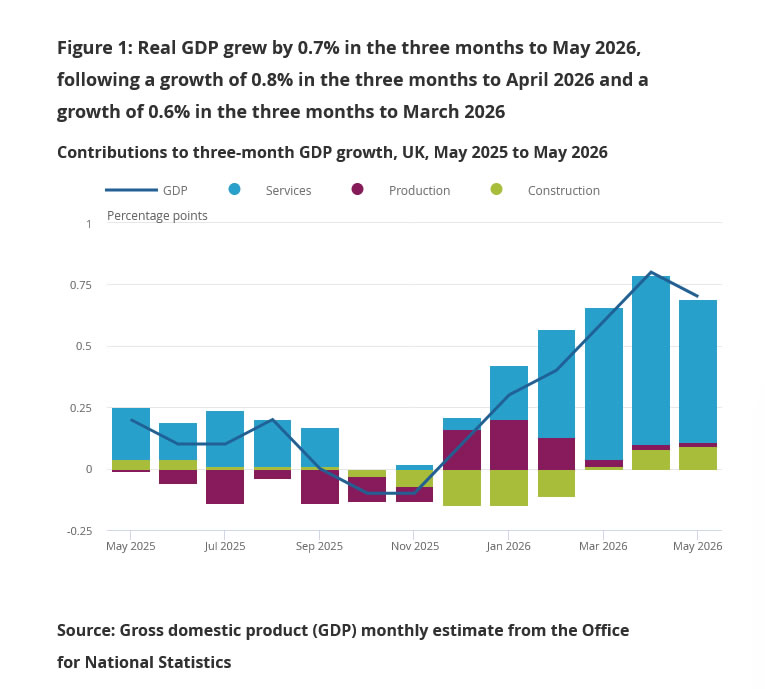

UK GDP Grows 0.1% MoM in May as Services Offset Weak Production and Construction

The UK economy returned to modest growth in May, with GDP rising 0.1% month-on-month after a -0.1% contraction in April, slightly exceeding expectations for a flat reading. The data suggest the economy regained some momentum after a soft start to the second quarter, although the recovery remains uneven beneath the headline. Growth was driven almost entirely by the services sector, while both production and construction continued to weigh on overall activity.

Services output rose 0.3% mom in May, reversing April's modest decline, with seven of the fourteen subsectors expanding during the month. The sector continues to provide the principal source of support for the economy, highlighting the resilience of consumer-facing and business services despite a backdrop of elevated interest rates and global uncertainty.

In contrast, production fell -0.5% mom, led by a sharp -4.6% decline in mining and quarrying alongside weakness in utilities and waste management. Manufacturing provided a rare bright spot, edging up 0.1% and preventing an even steeper decline in industrial output. Construction activity also weakened, falling -0.8% mom after a revised 0.1% decline in April, suggesting higher borrowing costs continue to restrain investment and building activity.

The broader trend nevertheless remains constructive. Over the three months to May, GDP expanded 0.7%, following growth of 0.8% in the previous three-month period. Services remained the primary growth engine with a 0.7% increase, while construction posted a solid 1.6% rise despite recent monthly weakness. Production also managed a modest 0.1% gain over the period.

Taken together, the figures point to an economy that continues to grow, albeit at a moderate pace and with an increasingly uneven sectoral mix. The resilience of services is helping offset ongoing weakness in more cyclical industries, suggesting the UK expansion remains intact but far from broad-based.

Economic Data

| Indicator | Actual | Expected | Previous |

|---|---|---|---|

| GDP (May MoM) | 0.1% | 0.0% | -0.1% |

| Services Output (MoM) | 0.3% | — | -0.1% |

| Production Output (MoM) | -0.5% | — | 0.2% |

| Manufacturing Output (MoM) | 0.1% | — | 0.0% |

| Construction Output (MoM) | -0.8% | — | -0.1% |

| GDP (3M/3M) | 0.7% | — | 0.8% |

| Services Output (3M/3M) | 0.7% | — | 0.9% |

| Production Output (3M/3M) | 0.1% | — | 0.1% |

| Construction Output (3M/3M) | 1.6% | — | 1.3% |

Key Takeaways

- UK GDP returned to growth in May, rising 0.1% mom after April's 0.1% contraction, modestly beating expectations.

- The recovery was entirely service-led, with services output rising 0.3%, while production and construction both contracted.

- Production fell -0.5%, largely due to sharp declines in mining & quarrying (-4.6%) and utilities. Manufacturing edged up just 0.1%.

- Construction declined -0.8%, marking a second consecutive monthly fall and pointing to continued weakness in investment-related activity.

- Despite softer monthly readings in production and construction, the broader trend remains positive, with GDP expanding 0.7% over the three months to May.

- The data suggest the UK economy continues to grow at a modest pace, but the expansion remains narrowly driven by services rather than broad-based across sectors.

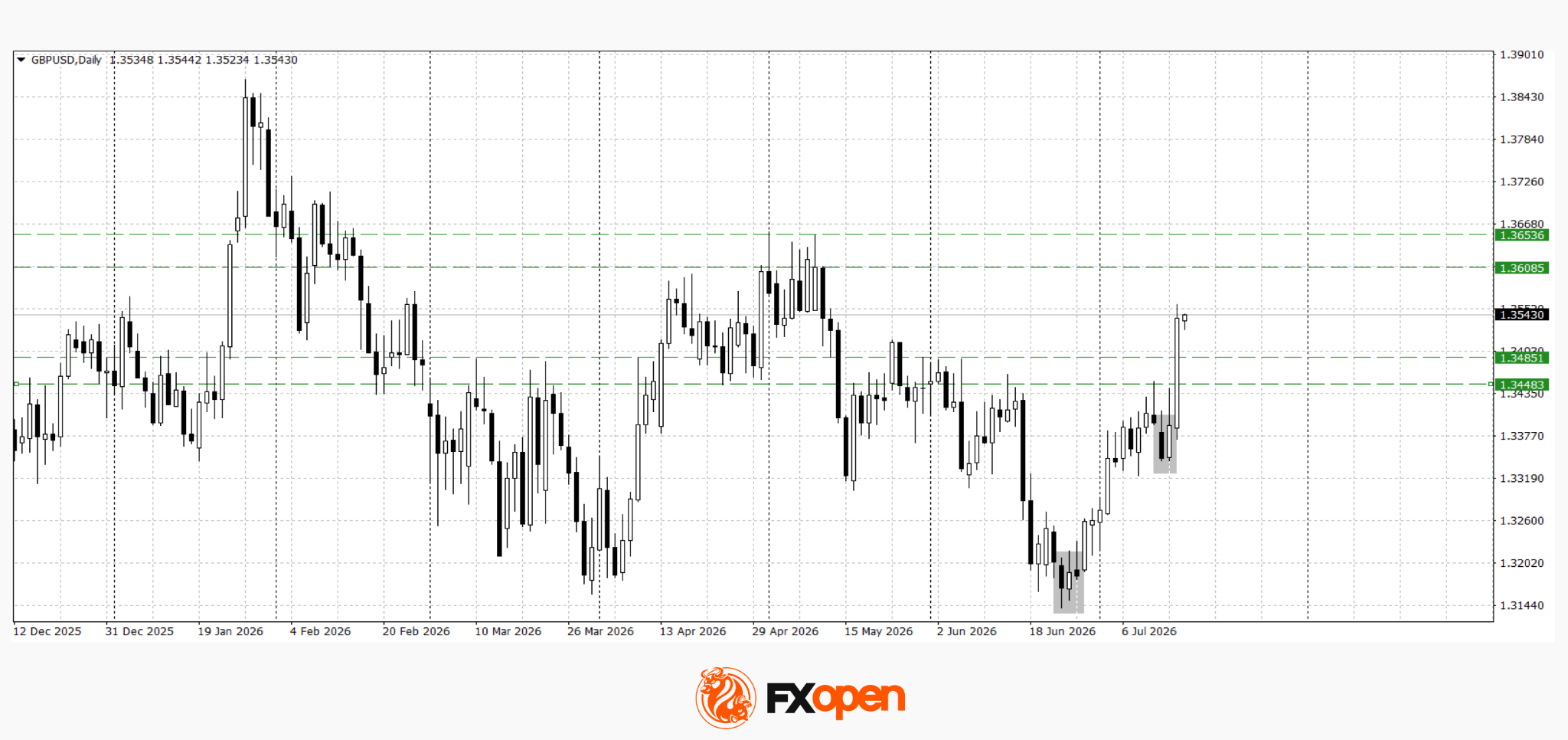

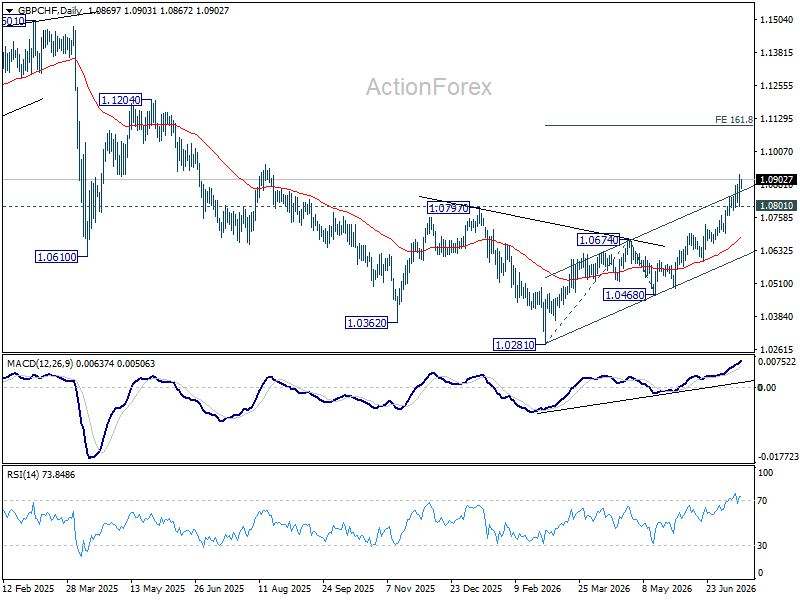

EUR/GBP and GBP/CHF Channel Breakouts as Burnham’s Cabinet Choice Signals Fiscal Discipline

Sterling extended its rally after reports that incoming Prime Minister Andy Burnham has decided on a fiscally conservative Chancellor. The Pound outperformed broadly, with the strongest gains seen against the Euro and Swiss Franc as both EUR/GBP and GBP/CHF broke out of established technical channels, suggesting investors are beginning to price a more durable revaluation of UK assets rather than merely covering short positions.

The catalyst was a Financial Times report, later corroborated by Reuters, that Burnham has settled on Home Secretary Shabana Mahmood as Chancellor of the Exchequer, with one source describing the appointment as "nailed down." Formal cabinet appointments are expected on Monday when Burnham succeeds Keir Starmer as Prime Minister. Although Mahmood has built her political profile primarily on domestic issues rather than economic policymaking, markets appear to be focusing less on her experience than on what her appointment signals about Burnham's governing philosophy.

Until recently, investors had worried that Burnham, whose political roots lie in Labour's soft-left tradition and mayoral politics, might pursue a looser fiscal agenda once in office. Those concerns had supported a modest political risk premium in Sterling during the leadership contest. The Makerfield by-election largely removed uncertainty over who would become Prime Minister, but it did not resolve uncertainty over how the new government would govern.

The expected choice of Mahmood appears to answer that question. Compared with Ed Miliband, who had long been viewed as the frontrunner for Chancellor and whose association with expansive industrial and net-zero policies had unsettled parts of the business community, Mahmood is regarded as representing a more centrist and fiscally disciplined approach. Investors are therefore interpreting the appointment as an early indication that fiscal credibility will remain a cornerstone of the new government.

That distinction matters because currency markets generally respond more to expected fiscal settings than political personalities. Expectations of tighter control over public finances improve confidence in the outlook for government borrowing, gilt issuance and longer-term debt sustainability. In that sense, the Chancellor announcement would represent a more concrete market signal than Burnham's leadership victory itself.

The technical picture reinforces that fundamental shift. EUR/GBP resumed its decline from 0.8863 and broke below its near-term falling channel, indicating that downside momentum is accelerating. The cross is now testing the key 61.8% retracement of 0.8221 (2024 low) to 0.8863 (2025 high) at 0.8466. A sustained break there would strengthen the case for a medium-term move back toward the 2024 low at 0.8221.On the upside, above 0.8543 resistance will bring consolidations first. But recovery should be limited below 0.8610 support turned resistance to bring another fall.

GBP/CHF is delivering a similarly constructive signal. The cross has broken above the upper boundary of its rising channel, suggesting that the uptrend is entering a stronger acceleration phase. The next objective lies at 161.8% projection of 1.0281 to 1.0674 from 1.0468 at 1.1104. On the downside, below 1.0801 support will bring consolidations first. But pullback should be contained above 1.0674 resistance turned support to bring another rise.

Together, the technical breakouts across both crosses suggest Sterling's rally is evolving from a simple unwinding of political uncertainty into a broader repricing of UK fiscal credibility that could extend through the third quarter as Burnham's cabinet and policy agenda become clearer.