Sample Category Title

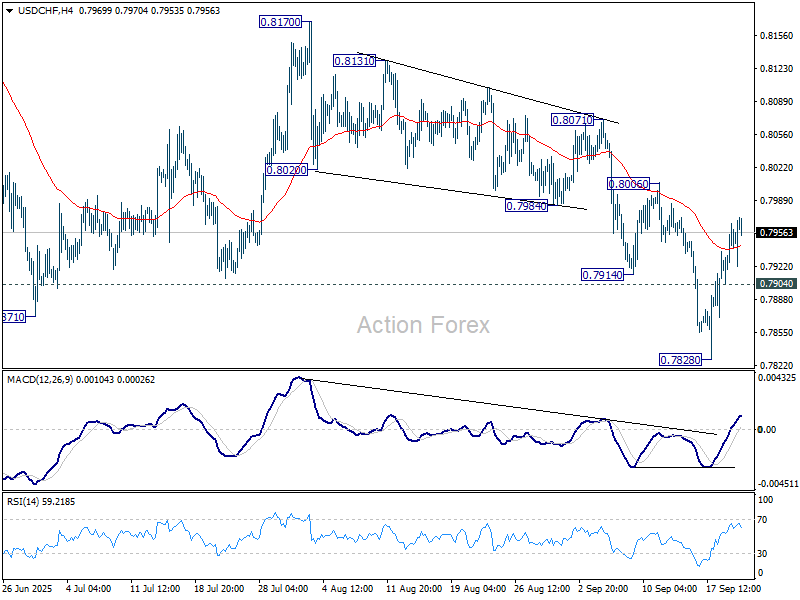

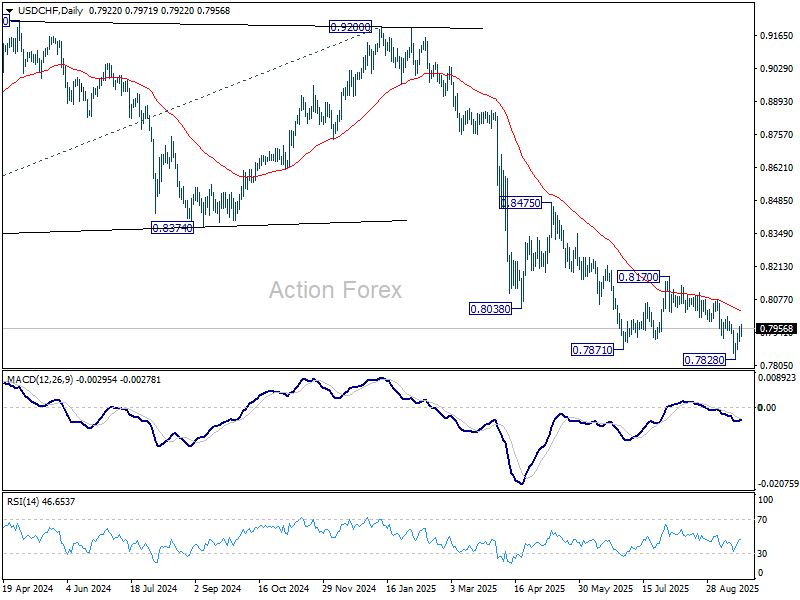

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7917; (P) 0.7942; (R1) 0.7978; More….

Intraday bias in USD/CHF remains on the upside for the moment. Rebound from 0.7828 short term bottom is in progress for 0.8006 resistance. Firm break there will bring stronger rise back to 0.8170. On the downside though, below 0.7904 minor support will bring retest of 0.7828 low instead.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).

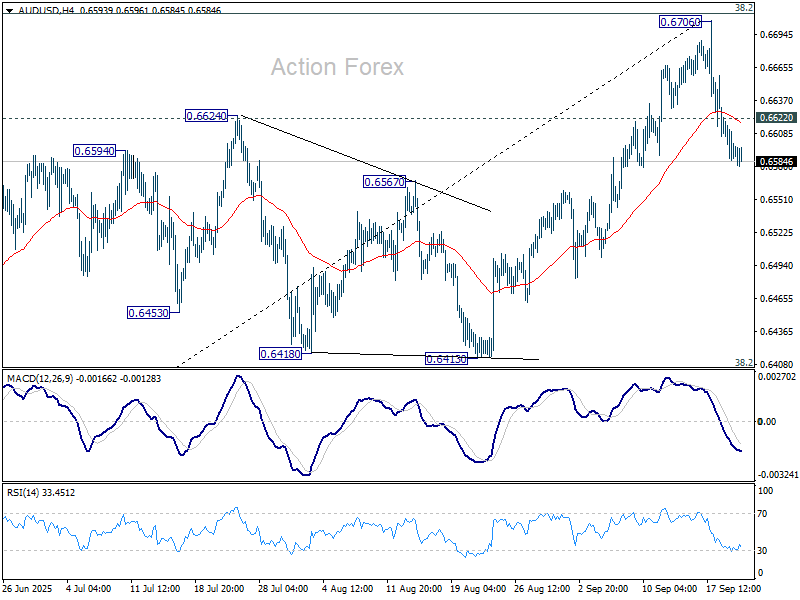

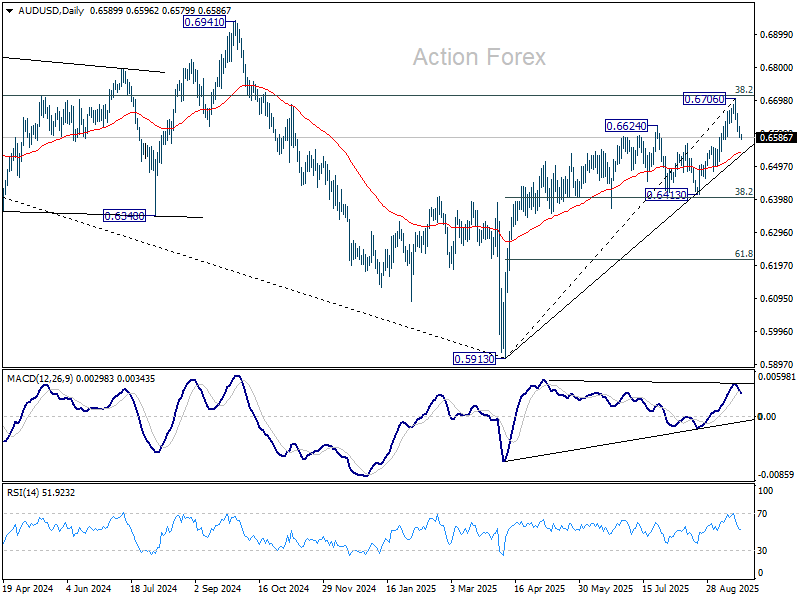

AUD/USD Daily Report

Daily Pivots: (S1) 0.6580; (P) 0.6600; (R1) 0.6614; More...

Intraday bias in AUD/USD remains on the downside for the moment. Fall from 0.6706 short term top should target 55 D EMA (now at 0.6540). Firm break there will target 0.6413 support. On the upside, though above 0.6622 minor resistance will bring retest of 0.6706 high.

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. Outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, sustained break of 0.6713 will be a strong sign of bullish trend reversal, and path the way to 0.6941 structural resistance for confirmation.

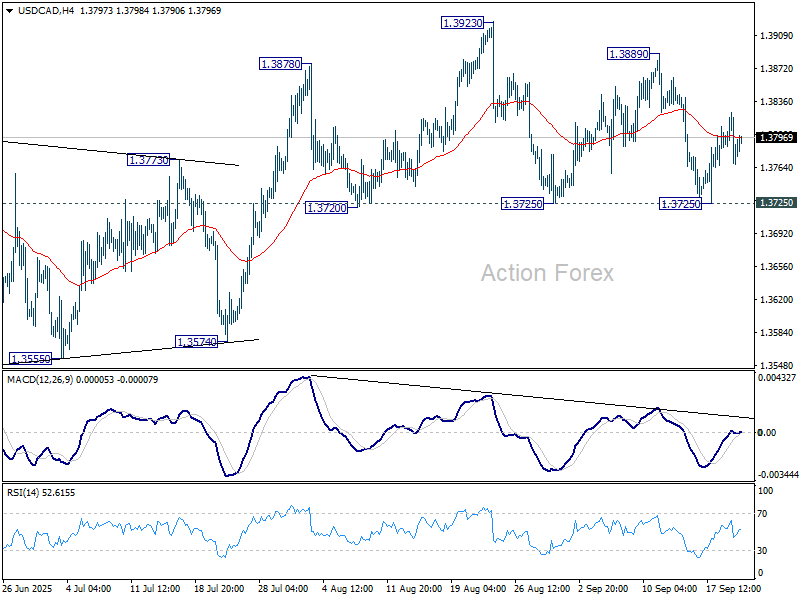

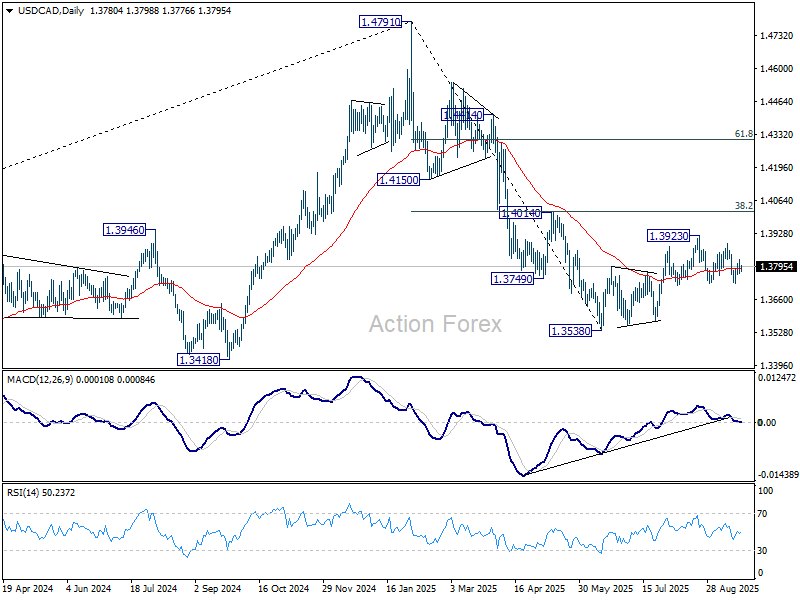

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3758; (P) 1.3791; (R1) 1.3814; More...

Intraday bias in USD/CAD stays neutral and more consolidations would be seen first. On the upside, break of 1.3889 resistance will suggest that the corrective rebound from 1.3538 is resuming, and further rise should be seen through 1.3923 high towards 1.4014 cluster resistance. However, decisive break of 1.3725 will indicate that the corrective rebound has completed, and turn near term outlook bearish.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 cluster resistance (38.2% retracement of 1.4791 to 1.3538 at 1.4017) holds. Next target is 61.8% retracement of 1.2005 (2021 low) to 1.4791 (2025 high) at 1.3069.

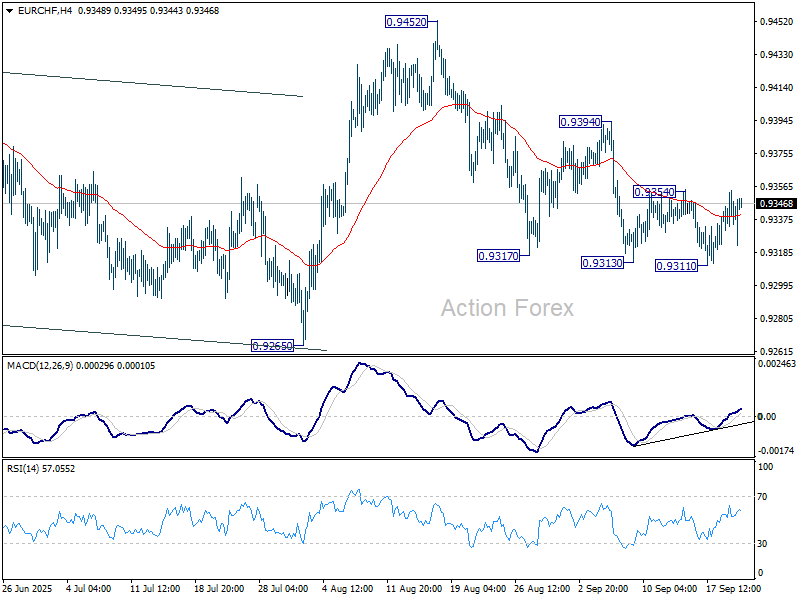

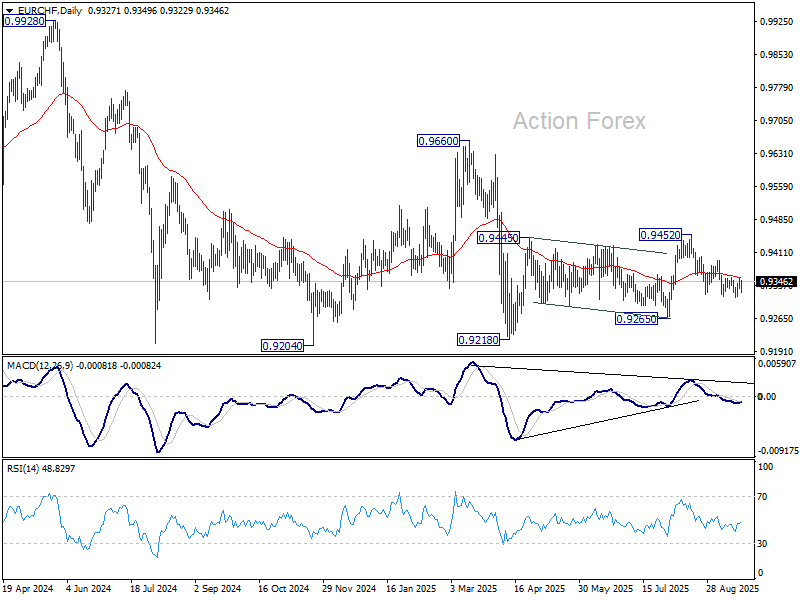

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9335; (P) 0.9346; (R1) 0.9356; More...

Intraday bias in EUR/CHF remains neutral for the moment. Considering bullish convergence condition in 4H MACD, firm break of 0.9354 resistance will confirm short term bottoming, and bring stronger rebound to 0.9394 resistance. On the downside, break of 0.9311 will resume the fall from 0.9452 to 0.9265 support.

In the bigger picture, the down trend from 0.9204 (2018 high) might still be in progress considering that EUR/CHF is staying well inside the long term falling channel. However, with bullish convergence condition in W MACD, downside potential should be limited in case of another fall. Instead, firm break of 0.9660 resistance will be an important sign of medium term bullish trend reversal.

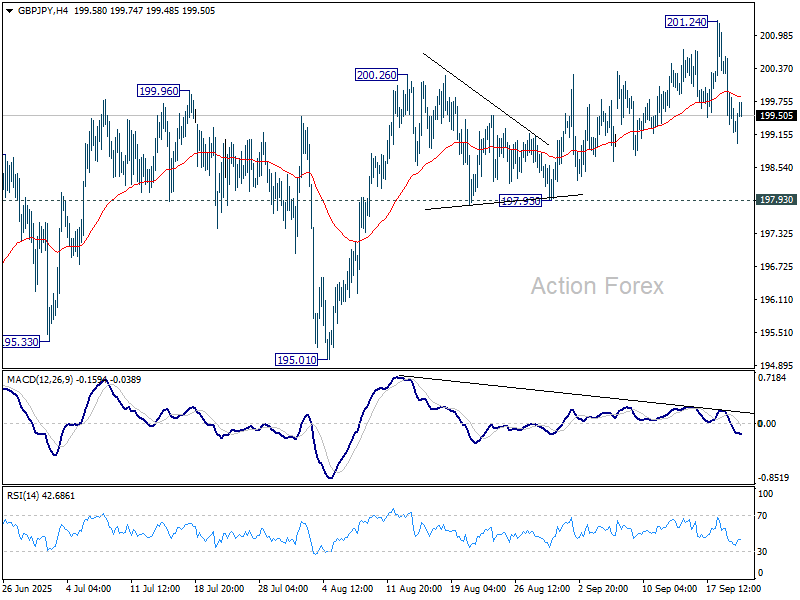

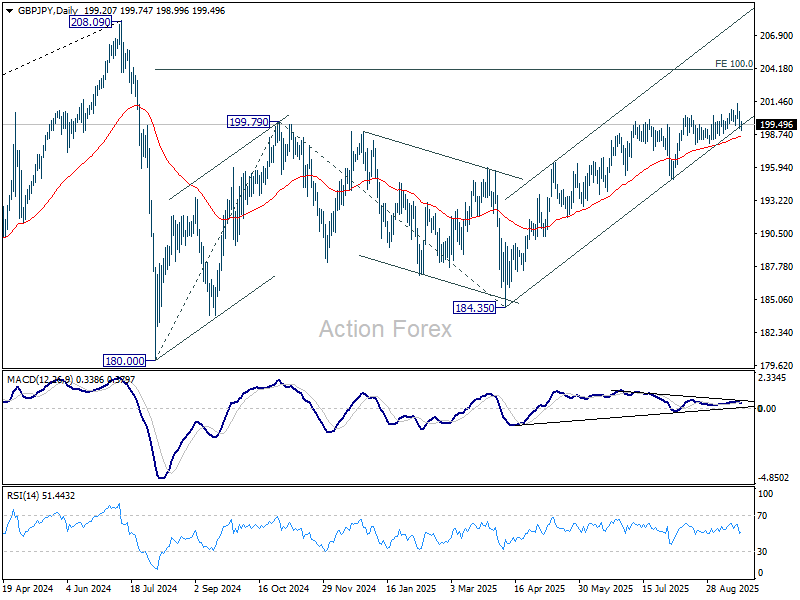

GBP/JPY Daily Outlook

Daily Pivots: (S1) 198.80; (P) 199.72; (R1) 200.24; More...

Intraday bias in GBP/JPY remains neutral and more consolidations could be seen first. Further rise is expected as long as 197.93 support holds. Firm break of 201.24 will target 100% projection of 180.00 to 199.79 from 184.35 at 204.14. However, considering bearish divergence condition in both D and 4H MACD, firm break of 197.93 will indicate bearish reversal and bring deeper fall back to 195.01 support first.

In the bigger picture, price actions from 208.09 (2024 high) are seen as a correction to rally from 123.94 (2020 low). The pattern might still extend with another falling leg. But in that case, strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. Meanwhile, decisive break of 208.09 will confirm long term up trend resumption.

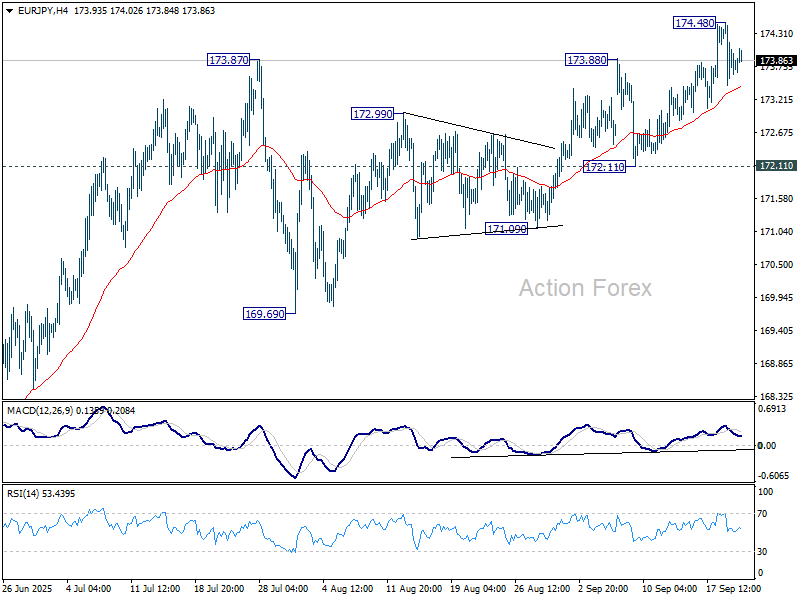

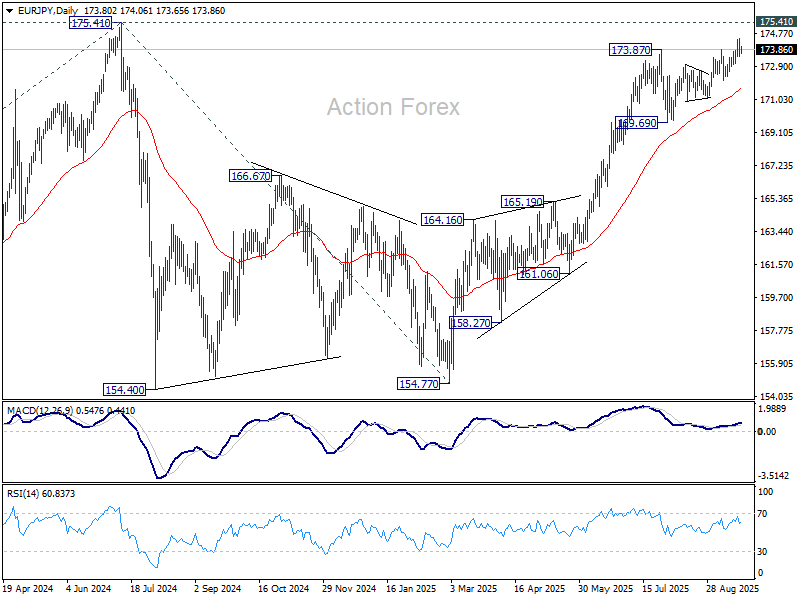

EUR/JPY Daily Outlook

Daily Pivots: (S1) 173.33; (P) 173.92; (R1) 174.36; More...

Intraday bias in EUR/JPY remains neutral and more consolidations could be seen below 174.48. But outlook will stay bullish as long as 172.11 support holds. Above 174.48 will target a retest on 175.41 high. However, firm break of 172.11 support will confirm short term topping, and turn bias back to the downside for deeper pullback.

In the bigger picture, current rally from 154.77 is still tentatively seen as resuming the larger up trend. Firm break of 175.41 (2024 high) will confirm and target 61.8% projection of 124.37 (2022 low) to 175.41 from 154.77 (2025 low) at 186.31. However, sustained break of 169.69 support will delay this bullish case, and probably extend the correction from 175.41 with another fall.

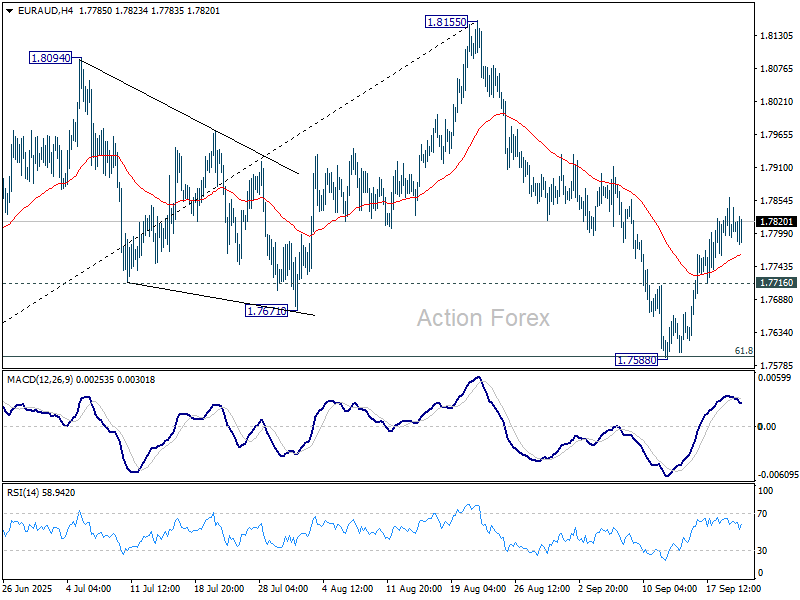

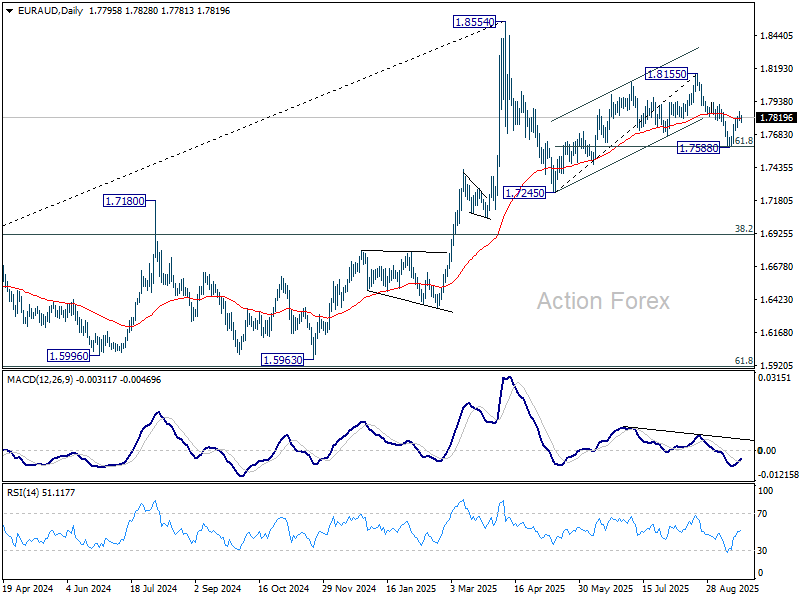

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7787; (P) 1.7824; (R1) 1.7853; More...

Intraday bias in EUR/AUD stays mildly on the upside at this point. Pullback from 1.8155 could have completed at 1.7588, after defending 61.8% retracement of 1.7245 to 1.8155 at 1.7593. Further rise would be seen to retest 1.8155. On the downside, however, break of 1.7716 will bring deeper fall to retest 1.7588 instead.

In the bigger picture, price actions from 1.8554 medium term top are seen as a corrective pattern. Deeper fall could be seen as the pattern extends, but downside should be contained by 38.2% retracement of 1.4281 (2022 low) to 1.8554 at 1.6922 to bring rebound. Uptrend from 1.4281 is expected to resume at a later stage.

New Trading Weeks Kicks Off Today With a Series of Central Bank Speeches

Markets

A phone call between US president Trump and his Chinese counterpart Xi Jinping supported the bulls on Friday. The sale of TikTok’s US operations to an American company was the main point but Trump said both made progress on a variety of issues including “Trade, Fentanyl, the need to bring the War between Russia and Ukraine to an end”. The US president added that he would meet Xi in person on the sidelines of the upcoming Asia-Pacific Economic Cooperation summit. The main indices on Wall Street all hit new records. The US dollar extended its post-Fed rebound into a third day. DXY rose to 97.64, EUR/USD drifted gradually but steadily towards the mid 1.17-1.18 area. The dollar’s (for now still) minor comeback comes along with some short-term bottoming out of the 2-year yield. Net daily changes in US rates on Friday varied between 0.8-2.2 bps. German bonds slightly underperformed. Intra-EMU spreads narrowed. France’s 10-yr yield (and therefore spread as well) finished the week the way it started: slightly higher than Italy. The remarkable swap has been years in the making. Italy’s rating upgrade (see below), along with southern peers including Portugal and Spain, are testament to the changing fiscal pecking order. Gilts were the laggards. The long end of the UK curve was particularly vulnerable (30-yr +5.2 bps). August budget deficit figures came in much higher than the Office of Budget Responsibility expected. This independent budget watchdog assesses the government performance against its self-imposed fiscal rules so Friday’s numbers are yet another blow for UK finance minister Reeves going into November’s Autumn Budget. Sterling was among the weaker performers with EUR/GBP closing north of 0.87 for the first time since early August. Cable (GBP/USD) forfeited the 1.35 handle.

The new trading weeks kicks off today with a series of central bank speeches, ranging from Bailey and chief economist Pill in the UK over ECB’s Lane and Nagel in the euro area to several Fed members (NY’s Williams, board member Miran) that are to address the economy and monetary policy. PMI’s are scheduled for release tomorrow along with Fed’s Powell offering his view on the economic outlook. PCE deflators, the Fed’s preferred inflation gauge, are printed on Friday. A slew of central bank meetings are scattered across the week with Hungary and Sweden on tap Tuesday, the Czech Republic Wednesday and Switzerland the day after.

News & Views

Rating agency Fitch raised Italy’s credit rating from BBB to BBB+ with a stable outlook. The upgrade reflects increased confidence in Italy’s fiscal trajectory, a stable political environment, ongoing reform momentum and reduced external imbalances. Fitch expects a continued gradual deficit reduction in 2025-2027, supported by structural improvements on the revenue side and strict expenditure control. They expect a deficit ratio of 3.1% of GDP, below the official 3.3% target. The government’s aim is bring it down to 2.6% in 2027 and under 2% by 2029. The primary surplus is expected to rise from 0.7% of GDP this year to 2.4% in 2029, supported by reform implementation. Fitch forecasts the debt ratio to increase modestly from 135.3% of GDP to 137.5% in 2026, before falling back towards 134% by 2030. One of Italy’s weaker points remains its low growth potential. The rating agency estimates growth of 0.6% this year and an average of 0.8% in 2026-2027. Domestic demand, particularly investment, will be a key driver of short-term growth, offsetting weakness in the external sector. Italian BTP’s have been performing strongly this year with the 10y swapspread narrowing from a YtD top at 130 bps to 83 bps currently and trading more and more in line with semi-core peers.

RBA governor Bullock sounded slightly more hawkish this morning in a testimony to the House of Representatives Standing Committee on Economics. Inflation has fallen substantially since the peak of 7.8% in 2022 and is now within the 2-3% target range. Labour market conditions are close to full employment. Since the August meeting, domestic data have been broadly in line with the Australian central bank’s expectations or if anything slightly stronger. The Board will discuss this and other developments at their meeting next week. Markets expect a stable policy rate (3.6%), but slightly reduced bets on a final rate cut at the November meeting (75% from 95%). Australian bond yields add 3-4 bps across the curve this morning while AUD/USD treads water.

Mixed Sentiment

The week kicks off on a mixed note. Last week’s Federal Reserve (Fed) rate cut gave markets a boost, but news that the Bank of Japan (BoJ) will begin reducing its ETF holdings unsettled global risk sentiment on Friday. The Nikkei came under notable selling pressure, the Stoxx 600 and FTSE 100 traded slightly bearish, but Wall Street shrugged it off: the S&P 500 and Nasdaq both advanced to fresh record highs as the US 2-year yield consolidated just below 3.60% and the 10-year rose to 4.41%.

On the geopolitical front, Trump and Xi reportedly held a constructive call. Details remain scarce, but progress was reported on TikTok, and the two leaders will revisit trade and tariffs in the coming weeks. Meanwhile, Australia, Canada and UK recognized the state of Palestine that could revive geopolitical tensions as the move didn’t please Israel and the US...

On the monetary policy front, the People’s Bank of China (PBoC) left its key rate unchanged at record lows for the fourth consecutive month, aiming to cushion the impact of US tariffs. But Chinese equities opened the week on a muted note, as investors were left wanting more clarity on trade from the Xi-Trump dialogue. By contrast, the Nikkei is better bid thanks to a softer yen, Asian gauges are broadly firmer, while Indian tech stocks face pressure after Trump proposed raising H-1B visa fees to $100,000 up from a few thousand dollars. The steep increase would make hiring foreign talent far more expensive; an analyst at Jefferies estimates this could raise corporate costs by 4–13%, weighing on jobs and growth in the near term, while potentially accelerating AI adoption longer term.

On the goods side, a North American freight index shows shipments have steadily declined this year, falling to their lowest levels since the pandemic. Yet weaker imports haven’t yet fueled consumer price pressures, and US growth likely improved last quarter after a sharp hit in Q1. This Thursday’s US Q2 GDP update is expected to show 3.3% growth with inflation near 2%, while Friday’s core PCE print is also unlikely to suggest building pressures.

Several Fed officials are scheduled to speak this week following last week’s decision to cut rates. They are expected to stress the need to support a weakening labour market as long as inflation remains under control. For now, equity bulls see little to fear: lower rates, an improving earnings outlook, dollar softness boosting overseas revenues and the AI theme remain supportive. Oracle jumped 4% Friday on reports it is in talks with Meta on a ~$20bn cloud deal, while Samsung rose 4% in Korea after winning Nvidia approval to supply high-bandwidth memory chips.

In FX, the dollar is broadly firmer since the FOMC, which proved less dovish than markets hoped. The EURUSD looks toppish, with scope for a retreat toward the 50- and 100-DMA levels. Cable has already slipped below its 100-DMA and is testing 50-DMA support. Dollar strength looks set to keep both pairs under pressure in the near term.

In commodities, gold opened the week higher on renewed Middle East tensions, while silver hit its highest level since 2011. Oil gained as Europe considers tightening sanctions against Russia after fresh airspace violations over NATO countries. European defense and aerospace names remain well bid.

But the standout move was in uranium: the Global X Uranium ETF surged 8% Friday to its highest since 2011 after Trump signed executive orders to quadruple U.S. nuclear power capacity by 2050 and unveiled a cross-Atlantic Technology Prosperity Deal with the UK. The news underscores nuclear’s growing role alongside clean energy, as data-center demand from AI surges. While clean energy ETFs lagged Friday, nuclear’s revival doesn’t necessarily derail the broader green transition — both sources are needed to meet intensifying power needs.

Week ahead: This week brings flash PMIs for a global read on activity, US growth and inflation data, and the Swiss National Bank’s (SNB) policy meeting on Thursday, where rates are expected to remain unchanged.

TikTok Deal Edges Forward With Planned US-China Meeting

In focus today

In the euro area, focus turns to the consumer confidence indicator for September. Confidence has been stuck at a low level for the last four months, which limits growth in private consumption. As the tariff uncertainty has been reduced and inflation returned to the 2% target, we expect gradual improvements in confidence.

Economic and market news

What happened over the weekend

In tech and tariffs, discussions between the US and China on TikTok's US operations appear to have advanced, with White House officials saying China's ByteDance would retain one board seat while Americans hold six. The White House also claims that a deal "signed in the coming days" will put the algorithm in US hands, clashing with Beijing's recent claims that the algorithm will remain in Chinese hands.

Donald Trump and Xi Jinping spoke over the phone on Friday, agreeing to meet in person at the Asia-Pacific Economic Cooperation (APEC) forum starting 31 October in South Korea. While the tone of the call was reportedly positive, and Trump said they had made progress in advancing the TikTok deal, the call yielded little concrete news on the state of tariff discussions. Trump also said he would visit China in early 2026, which could suggest that the trade negotiations will be extended even further beyond the current 10 November deadline. We will discuss the outlook for the trade war, how it is impacting US and Chinese economies and its implications for CNY and USD in a webinar this Thursday.

In the US, President Trump hailed Charlie Kirk as a "martyr for American freedom" at his memorial service on Sunday, using the platform to blame the "radical left" for his murder while vowing to carry on Kirk's conservative legacy. Critics warn Trump's rhetoric risks deepening partisan divides and escalating political tensions.

Furthermore, Trump appointed his former attorney Lindsey Halligan as US Attorney for the Eastern District of Virginia, replacing Erik Siebert. The appointment comes amid Trump's criticism of Attorney General Pam Bondi and calls for more aggressive investigations into political rivals, including James Comey and Letitia James.

In geopolitics, Britain, Canada, Australia, and Portugal formally recognised the State of Palestine on Sunday, in a move intended to promote a two-state solution amidst the ongoing Gaza war. While Palestinian leaders welcomed the decision as a step towards independence, the Israeli PM Netanyahu condemned the move. The recognition is expected to heighten tensions with Israel and its ally, the US, as similar announcements are anticipated during the UN General Assembly this week.

Recent Russian airspace violations in Estonia, Poland, and most recently the Baltic Sea, drew a muted US response. This comes after Pentagon officials in August said that under Trump, the US military would be shifting its attention to other priorities, like defence of the homeland. Analysts warn that US disengagement risks emboldening Russia and straining NATO unity, as European diplomats' express frustration over Trump's inconsistent stance.

In the UK, retail sales data released on Friday surprised to the upside, rising 0.7% y/y in August (cons: 0.6% y/y), despite a downward revision to July's growth to 0.8% y/y.

In China, the PBoC kept the 1Y and 5Y loan prime rates (LPR) unchanged, in line with market expectations. While there is pressure for more stimulus, broad-based rate cuts may not be the preferred tool for China as they are also concerned about fuelling a liquidity-driven equity bubble. We expect more targeted stimulus measures coming soon.

Equities: US equities rose yet again on Friday cementing the strong end to the week, following the FOMC decision on Wednesday, and setting new highs. S&P500 was up 0.5%, with Nasdaq up 0.7% on Friday. Stoxx600 was a touch lower. The tech sector was yet again the driver for the higher equities amid higher US yields as well. Inflation expectations moderated somewhat towards the end of the week, contributing to the cyclical outperformance vs. defensives stocks by almost 1.5% in the final two trading sessions. Overnight, futures are slightly lower.

FI and FX: It is going to be an eventful week with central bank meetings (Sweden - no change, and SNB - no change) as well as key economic data such as the Flash PMIs from Europe and US, US PCE data, inflation data from Japan.