Sample Category Title

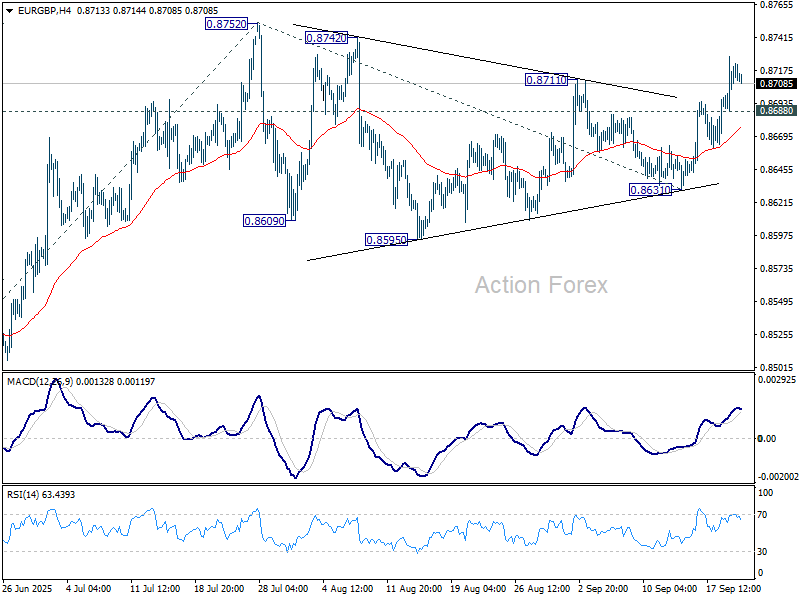

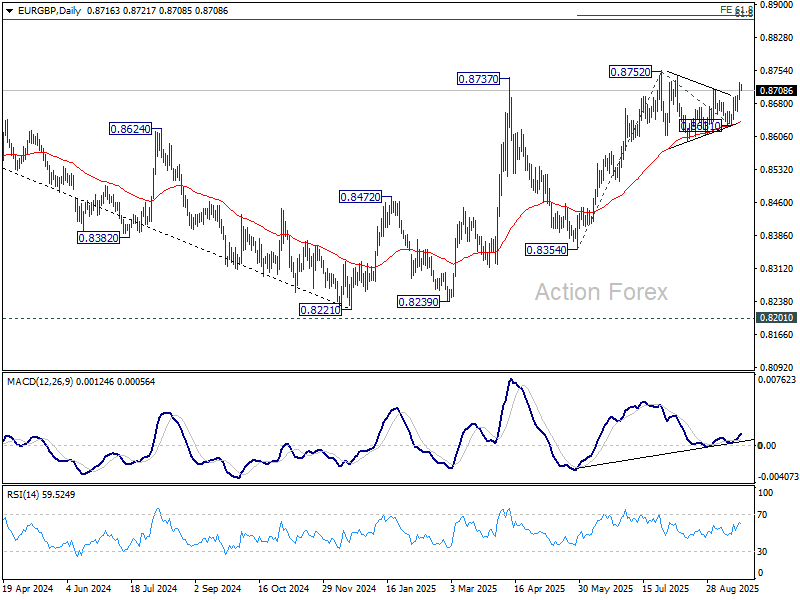

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8698; (P) 0.8714; (R1) 0.8737; More...

Intraday bias in EUR/GBP remains on the upside for retesting 0.8752 resistance. Firm break there will resume larger rally to 61.8% projection of 0.8354 to 0.8752 from 0.8631 at 0.8877, which is close to 0.8867 fibonacci level. On the downside, though, below 0.8688 minor support will dampen this view and turn bias neutral first.

In the bigger picture, the structure from 0.8221 medium term bottom are not impulsive enough to suggest that it's reversing the down trend from 0.9267 (2022 high). But even if it's a correction, further rise could still be seen to 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Nevertheless, sustained trading below 55 W EMA (now at 0.8518) will argue that the pattern has completed and bring retest of 0.8221 low.

Quiet Markets Look to Fed and BoE Commentary

Forex markets started the week on a subdued note, with Asian trading showing little momentum. With no top-tier data scheduled, activity is likely to stay muted until later in the week, leaving traders watching central bank commentary for direction.

Several Fed officials are set to deliver remarks today, their first since last week’s rate cut. Their speeches may shed light on how individual members view inflation risks and labor market resilience after the latest policy move. But collectively, there should be broad alignment around the outlook for two more cuts this year.

The BoE, on the other hand, is a bigger source of uncertainty. Chief Economist Huw Pill will speak today, and his comments could sway expectations ahead of the November meeting, where markets still see the chances of a cut as a coin toss.

Elsewhere, Asian equities diverged. Japan’s Nikkei advanced strongly, building on Wall Street’s rally from Friday, while Hong Kong’s Hang Seng came under pressure. Sentiment in Hong Kong was dampened by Beijing’s reluctance to roll out fresh stimulus despite mounting evidence of domestic fatigue.

In commodities, gold remained range-bound while silver outperformed, breaking higher as traders looked for alternative momentum plays. Cryptocurrencies, by contrast, were under renewed selling pressure, with Bitcoin and Ethereum slipping further in their ongoing consolidations.

On the geopolitical front, U.S. President Donald Trump said progress had been made in negotiations over TikTok’s U.S. operations. The expected deal would see the app’s American assets transferred to domestic ownership under a board with national security credentials. Trump named business leaders Lachlan Murdoch, Larry Ellison, and Michael Dell as potential backers, a move that could give his allies greater influence over a platform central to U.S. political and cultural discourse.

In Asia, at the time of writing, Nikkei is up 1.09%. Hong Kong HSI is down -1.02%. China Shanghai SSE is down -0.09%. Singapore Strait Times is down -0.11%. Japan 10-year JGB yield is up 0.02 at 1.661.

RBA's Bullock: Economy may prove weaker or stronger than forecasts

RBA Governor Michele Bullock told a parliamentary committee today that the central bank expects underlying inflation to moderate toward the midpoint of its 2–3% target range, with forecasts conditioned on the market’s assumption of modest further easing. Recent rate cuts are seen supporting household and business spending, while real income growth should help sustain consumption in the year ahead.

She noted that domestic data since the August meeting have been “broadly in line with expectations, or slightly stronger,” giving the Board some confidence heading into next week’s policy meeting. But Bullock stressed that forecasts remain only estimates, and the outlook is highly uncertain, particularly given the unpredictable global environment.

She highlighted risks on both sides: growth momentum may fade, or it could prove “materially stronger” than anticipated. Bullock warned that "excess demand" in the economy and labour market could persist, particularly that "productivity growth has not picked up and growth in unit labour costs remains high".

PBoC holds fire, China stays patient on stimulus as economy shows strain

The People’s Bank of China left its one-year loan prime rate at 3.0% and the five-year at 3.5% today, extending a steady policy stance for the fourth month running. The unchanged setting came in line with forecasts and follows the central bank’s last 10bps trim in May, part of earlier efforts to shore up growth.

Policymakers opted for patience as the recent strong rally in domestic equities reduced pressure for immediate support, even as official data continue to point to uneven demand and fading momentum in industry and property.

Still, most expect modest easing steps before year-end as Beijing works to lock in its 5% growth target, also as policy focus shifted from deflation management to reflation

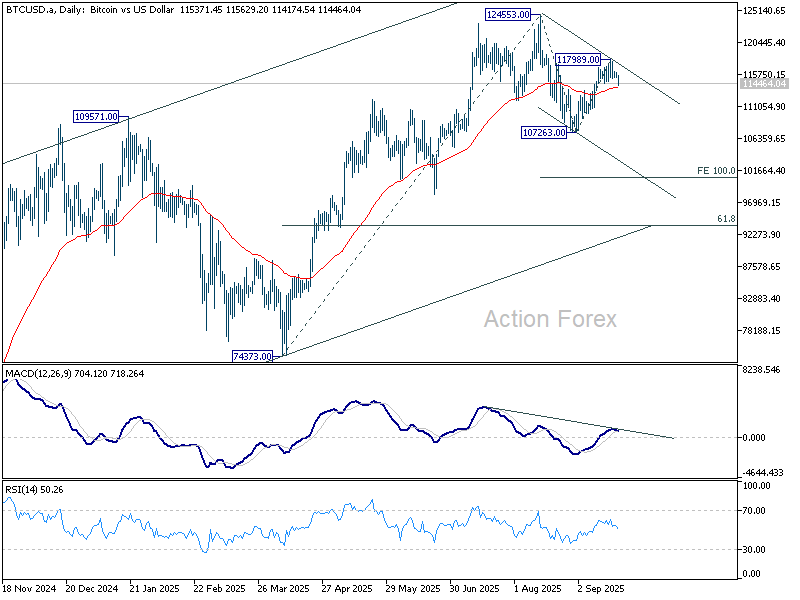

Bitcoin risks drop toward 100k correlation with tech stocks breaks

Bitcoin and Ethereum lost ground over the past week as stronger Dollar weighed, breaking their recent correlation with the NASDAQ. While tech stocks surged to fresh records, the two largest cryptocurrencies failed to follow. The price action suggests that the consolidation phase in both Bitcoin and Ethereum, in place since August, is set to extend with another downward leg.

For Bitcoin, sustained break of 55 D EMA (now at 113,835) would confirm that the correction from 124,553 has entered its third leg. That would open the way for a retest of the 107,263 support. Firm break there would target a deeper fall toward 100% projection of 124,553 to 107,263 from 117,989 at 100,699, which is close to 100k psychological level.

Ethereum’s structure looks slightly less fragile, but risks are also tilting lower. The current move from 4,956.08 is seen as correcting only the rise from 2,110.58, not the larger trend from 1,382.55. Still, decisive break of 4,211.04, which aligns closely with 55 D EMA (now at 4,207.58) would signal scope for a deeper correction. The next technical target for Ethereum would be 38.2% retracement of 2,110.58 to 4,956.08 at 3,869.09.

SNB set to hold, Fed officials to shape post-cut outlook

The SNB takes center stage this week, with its policy decision as the only major central bank highlights. Consensus strongly points to no change, with the policy rate remaining at 0.00%. A Bloomberg survey showed only two out of 21 economists anticipate a return to negative rates, reflecting the broad belief that the hurdle for such a move is exceptionally high.

SNB Chair Martin Schlegel has reiterated several times that reintroducing negative rates would require extraordinary circumstances. Even with Switzerland now facing sweeping 39% U.S. tariffs on exports, inflation has remained stable above 0%, providing the Bank room to stay patient. The message is clear: no urgency to deploy policy “mega-bullets” at this stage.

Attention in the U.S. will turn to August PCE inflation due Friday. Both headline and core are projected to hold steady at 2.7% and 2.9%, respectively. Markets are unlikely to be shaken even by a mild upside surprise, as last week’s FOMC meeting signaled two more cuts this year as part of a gradual risk-management strategy.

Fed officials have struck a more confident tone on inflation since tariffs were adjusted away from worst-case scenarios. Minneapolis Fed President Neel Kashkari said last week that while inflation may stay near 3%, it is unlikely to accelerate to 4–5%. That aligns with the Fed’s view that the balance of risks still tilts toward guarding against labor market deterioration.

The focus this week will be less on data surprises and more on Fed officials’ remarks following the latest rate cut. With two more reductions penciled in for 2025, investors will parse comments for insight into how comfortable policymakers are with maintaining a steady easing path. Diverging views within the Committee could start to shape expectations for timing and magnitude.

Europe will also provide important signals through Germany’s Ifo business climate index. Markets are worried that the early recovery momentum in Europe’s largest economy is losing steam, and the survey results will either validate or challenge those concerns. A downside print could weigh on Euro sentiment, especially after last week’s failure of the currency to hold gains versus Dollar.

In Canada, July GDP will be closely watched. Optimism for a rebound in Q3 is high after upbeat retail sales, but the print will be a critical test of whether growth momentum is truly returning. The Loonie’s outperformance last week, despite the BoC’s rate cut, highlights how data surprises can swing sentiment in either direction.

Beyond these highlights, Australia’s monthly CPI, Japan’s Tokyo CPI, and global flash PMI readings round out the calendar.

Here are some highlights for the week:

- Monday: Canada IPPI, RMPI; Eurozone consumer confidence.

- Tuesday: Australia PMIs; Eurozone PMIs; UK PMIs; US PMIs.

- Wednesday: Japan PMIs; Australia monthly CPI; Germany Ifo business climate; US new homes sales.

- Thursday: BoJ minutes, corporate service prices; Germany Gfk consumer climate; SNB rate decision; Eurozone M3 money supply; US Q2 GDP final, jobless claims, durable goods orders, goods trade balance, existing home sales.

- Friday: Japan Tokyo CPI; Canada GDP; US personal income and spending, PCE inflation.

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8698; (P) 0.8714; (R1) 0.8737; More...

Intraday bias in EUR/GBP remains on the upside for retesting 0.8752 resistance. Firm break there will resume larger rally to 61.8% projection of 0.8354 to 0.8752 from 0.8631 at 0.8877, which is close to 0.8867 fibonacci level. On the downside, though, below 0.8688 minor support will dampen this view and turn bias neutral first.

In the bigger picture, the structure from 0.8221 medium term bottom are not impulsive enough to suggest that it's reversing the down trend from 0.9267 (2022 high). But even if it's a correction, further rise could still be seen to 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Nevertheless, sustained trading below 55 W EMA (now at 0.8518) will argue that the pattern has completed and bring retest of 0.8221 low.

Bitcoin risks drop toward 100k correlation with tech stocks breaks

Bitcoin and Ethereum lost ground over the past week as stronger Dollar weighed, breaking their recent correlation with the NASDAQ. While tech stocks surged to fresh records, the two largest cryptocurrencies failed to follow. The price action suggests that the consolidation phase in both Bitcoin and Ethereum, in place since August, is set to extend with another downward leg.

For Bitcoin, sustained break of 55 D EMA (now at 113,835) would confirm that the correction from 124,553 has entered its third leg. That would open the way for a retest of the 107,263 support. Firm break there would target a deeper fall toward 100% projection of 124,553 to 107,263 from 117,989 at 100,699, which is close to 100k psychological level.

Ethereum’s structure looks slightly less fragile, but risks are also tilting lower. The current move from 4,956.08 is seen as correcting only the rise from 2,110.58, not the larger trend from 1,382.55. Still, decisive break of 4,211.04, which aligns closely with 55 D EMA (now at 4,207.58) would signal scope for a deeper correction. The next technical target for Ethereum would be 38.2% retracement of 2,110.58 to 4,956.08 at 3,869.09.

PBoC holds fire, China stays patient on stimulus as economy shows strain

The People’s Bank of China left its one-year loan prime rate at 3.0% and the five-year at 3.5% today, extending a steady policy stance for the fourth month running. The unchanged setting came in line with forecasts and follows the central bank’s last 10bps trim in May, part of earlier efforts to shore up growth.

Policymakers opted for patience as the recent strong rally in domestic equities reduced pressure for immediate support, even as official data continue to point to uneven demand and fading momentum in industry and property.

Still, most expect modest easing steps before year-end as Beijing works to lock in its 5% growth target, also as policy focus shifted from deflation management to reflation

RBA’s Bullock: Economy may prove weaker or stronger than forecasts

RBA Governor Michele Bullock told a parliamentary committee today that the central bank expects underlying inflation to moderate toward the midpoint of its 2–3% target range, with forecasts conditioned on the market’s assumption of modest further easing. Recent rate cuts are seen supporting household and business spending, while real income growth should help sustain consumption in the year ahead.

She noted that domestic data since the August meeting have been “broadly in line with expectations, or slightly stronger,” giving the Board some confidence heading into next week’s policy meeting. But Bullock stressed that forecasts remain only estimates, and the outlook is highly uncertain, particularly given the unpredictable global environment.

She highlighted risks on both sides: growth momentum may fade, or it could prove “materially stronger” than anticipated. Bullock warned that "excess demand" in the economy and labour market could persist, particularly that "productivity growth has not picked up and growth in unit labour costs remains high".

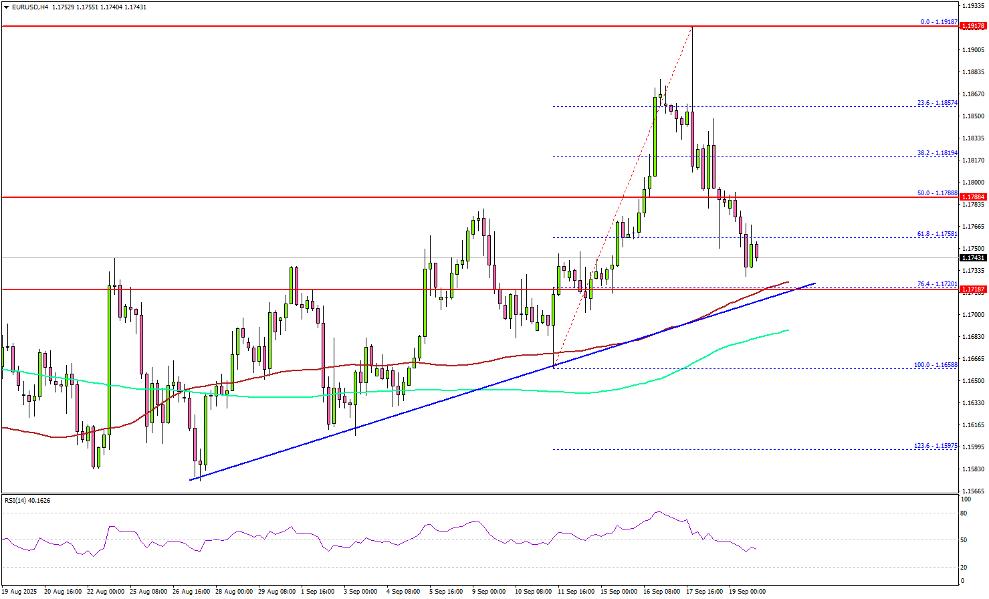

EUR/USD Pullback Deepens – All Eyes on This Make-or-Break Support

Key Highlights

- EUR/USD started a sharp downside correction from 1.1920.

- A major bullish trend line is in place with support at 1.1720 on the 4-hour chart.

- GBP/USD declined heavily below 1.3600 and 1.3550.

- Gold prices remained elevated above the $3,620 level.

EUR/USD Technical Analysis

The Euro struggled above 1.1900 against the US Dollar. The Fed rate cut sparked bearish moves in EUR/USD, and the pair tumbled below 1.1850.

Looking at the 4-hour chart, the pair traded below the 1.1820 and 1.1800 support levels. There was a drop below the 50% Fib retracement level of the upward move from the 1.1658 swing low to the 1.1918 high.

The pair is now consolidating losses below 1.1780. On the downside, there is a key support at 1.1720 and the 100 simple moving average (red, 4-hour).

There is also a major bullish trend line in place with support at 1.1720 on the same chart. It is close to the 76.4% Fib retracement level of the upward move from the 1.1658 swing low to the 1.1918 high. The next key area of interest might be near 1.1680 and the 200 simple moving average (green, 4-hour).

The main support could be 1.1650. Any more losses might increase selling pressure and send EUR/USD toward 1.1565. On the upside, the pair could face resistance near the 1.1780 level.

The first major hurdle for the bulls could be 1.1800. A close above 1.1800 could set the pace for a steady recovery wave. In the stated case, the pair could rise toward 1.1840, above which the bulls could aim for a move toward 1.1880. Any more upsides could send the pair toward 1.1920. s

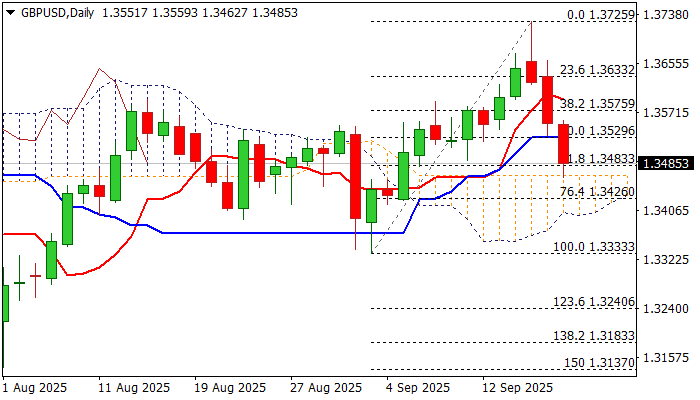

Looking at GBP/USD, the pair failed to continue higher above 1.3720 and recently started a major downside correction.

Upcoming Key Economic Events:

- ECB's Lane speech.

- Fed's Williams speech.

- Fed's Musalem speech.

Fed Cuts 0.25%, BoJ ETF Sale Shocks Market, U.S. Stocks Hit Records

Markets moved sideways early in the week as traders waited for key central bank decisions. U.S. retail sales were stronger than expected, while U.K. inflation stayed high at 3.8%. The Bank of England met first, kept rates unchanged as expected, and said any future cuts would depend on clear signs that inflation is falling steadily.

The U.S. Federal Reserve then cut interest rates by 0.25% and suggested there could be two more cuts before the end of 2025. The Fed noted slower job growth and a weaker labor market but also said inflation is still somewhat high. The U.S. dollar dipped at first but soon recovered, finishing the week strong. U.S. stock markets hit new record highs, helped by the rate cut and strong gains in technology shares.

The Bank of Japan also kept rates unchanged but surprised markets by saying it will slowly start selling some of its large holdings of exchange-traded funds (ETFs) and real estate trusts (J-REITs). The Nikkei index fell briefly but rebounded after the BoJ promised the sales would be very gradual. Two board members voted for a 0.25% rate hike, and Governor Kazuo Ueda said gradual tightening is possible if the economy and inflation stay on track, leading markets to expect a possible rate increase later this year.

Markets This Week

U.S. Stocks

U.S. equities saw profit-taking early last week ahead of the FOMC announcement, but the selling was brief as buyers stepped in near the 10-day moving average. The Dow then climbed to fresh record highs after the Fed’s 0.25% rate cut and guidance for two more cuts in 2026. With the FOMC maintaining a bullish tone, the uptrend has resumed, making buying on dips toward the 10-day moving average the preferred strategy. Key resistance is now at 46,500, 47,000, and 48,000, while support lies at 45,700, 45,000, 44,000, and 43,000.

Japanese Stocks

The Nikkei 225 surged after the FOMC announcement, extending its recent strong gains. However, the Bank of Japan’s surprise plan to begin selling its ETF and J-REIT holdings caused a sharp drop on Friday before the market recovered into the close. With the BoJ moving closer to a possible rate hike and starting asset sales, further gains may be harder to achieve, so a sideways-to-lower move is expected this week. Resistance is at 46,000円 and 47,000円, while support is at 45,500円, 45,000円, and 44,000円.

USD/JPY

USD/JPY again tested the lower end of its recent range last week after the U.S. rate cut and dovish comments from Fed Chair Powell. Surprisingly, strong support held near 146, and the pair finished the week firmly as the market had been positioned for deeper losses. The rebound is notable and could attract more buying this week, but range trading between 146 and 149 remains the preferred strategy. Key resistance is at 148, 149, and 150, with support at 146 and 145.

Gold

Gold had a volatile week, posting new record highs again after the U.S. interest rate cut. The uptrend remains very strong, with prices holding above the 10-day moving average as buyers stay aggressive. In the short term, following the uptrend can be profitable, but waiting for a break below the 10-day moving average to sell may offer the best near-term trading opportunity given how far the market has already climbed. Resistance is at $3,700 and $3,800, while support stands at $3,600, $3,500, and $3,450.

Crude Oil

WTI crude stayed under pressure last week, failing to hold above the key $65 level after an early rise. Concerns about a slowing U.S. economy and the potential for weaker demand kept sellers in control, limiting any upward momentum. For short- and medium-term traders, selling into strength or waiting for a decisive break below $60 remains the preferred strategy as the market struggles to find support. Key resistance is at $65, $70, and $75, while support is at $60 and $55.

Bitcoin

Bitcoin had a quiet week, consolidating earlier gains and briefly rising on the U.S. interest rate cut before sellers pushed prices back below the 10-day moving average, signaling an end to September’s uptrend. The market is now expected to test lower and provide range-trading opportunities between $112,000 and $120,000 in the near term. Key levels remain unchanged, with resistance at $120,000, $125,000, and $150,000, and support at $112,000, $105,000, and $100,000.

This Week’s Focus

- Monday: U.K. BoE Gov Bailey Speaks

- Tuesday: E.U. HCOB Eurozone Manufacturing PMI, U.K. S&P Global Manufacturing PMI, U.S. Current Account and S&P Global Manufacturing PMI

- Wednesday: Japan au Jibun Bank Services PMI and BoJ Core, U.S. Building Permits and New Home Sales

- Thursday: Japan Monetary Policy Meeting Minutes, U.S.Initial Jobless Claims, Durable Goods Orders, GDP and Existing Home Sales

- Friday: Japan Tokyo Core CPI, U.S. Core PCE Price Index and Michigan Consumer Sentiment

This week the market will continue to forecast the next moves in U.S. and Japanese interest rates as traders digest last week’s central bank meetings. A busy economic calendar includes manufacturing data from Europe, the U.K., and the U.S., with Thursday’s U.S. durable goods orders and GDP, and Friday’s U.S. Core PCE Price Index and Michigan Consumer Sentiment all likely to create volatility and trading opportunities. FX markets remain range-bound but look ready for a breakout, while traders will watch closely to see if equities and gold can extend their strong uptrends.

GBP/USD: Cable Bears Face Headwinds from Daily Cloud Top

Cable remains in a step fall from last Wednesday’s 2 ½ month peak (1.3725) which has so far retraced over 61.8% of recent 1.3333/1.3725 rally and cracked next significant support at 1.3465 (daily cloud top).

Pound was initially hit by stronger dollar after Fed disappointed expectations for keeping very dovish stance, with signals from BoE Governor for possible further rate reductions, boosting bears on Thursday, while Friday’s unexpectedly high rise in UK borrowing sparked fresh acceleration lower.

Technical studies weakened on daily chart, with the pair being on track for weekly close in red (potential formation of bearish engulfing and long upper shadow on weekly candle add to negative signals).

On the other hand, daily cloud top offers solid support, which may hold bears for some time, with limited upticks to be capped under 1.3530 (daily Kijun-sen / broken Fibo 50%) to offer better selling levels and keep bears in play.

Res: 1.3500; 1.3530; 1.3559; 1.3575

Sup: 1.3465; 1.3426; 1.3397; 1.3333

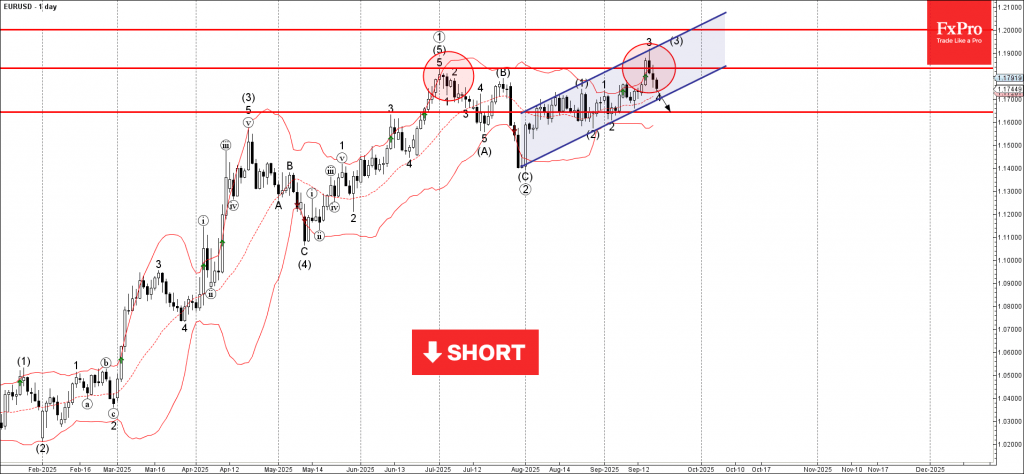

EURUSD Wave Analysis

EURUSD: ⬇️ Sell

- EURUSD reversed from resistance zone

- Likely to fall to support level 1.1640

EURUSD currency pair recently reversed down from the resistance zone between the resistance level 1.1835 (former multi-month high from June), upper daily Bollinger Band and the resistance trendline of the daily up channel from July.

The downward reversal from this resistance zone started the active minor correction 4.

Given the strongly bullish US dollar sentiment seen across the FX markets, EURUSD currency pair can be expected to fall to the next round support level 1.1640.