Sample Category Title

Sunset Market Commentary

Markets

Dire public finances suddenly turned the spotlights back on the UK today. The monthly August deficit, a once only second tier number for markets, came in at £18bn. That was way bigger than both markets but more importantly, the Office of Budget Responsibility had predicted (£12.5bn). Total deficit in the running fiscal year (starting in April) now mounted to £83.8bn, again well above OBR forecasts. It’s another blow to UK chancellor Reeves and ups the ante for the November 26 annual budget. Reeves needs to strike a balance between her pledge not to raise taxes any further and stick to the government’s promised investment plans while abiding to her self-imposed fiscal rules (ie. simply borrowing your way out is not an option). Today’s setback comes days after news that the OBR is expected to lower its productivity forecast, meaning less economic growth and therefore less tax revenue. UK gilts underperform. The 30-yr yield adds 4 bps currently. The Bank of England yesterday announced that it would sell less long-term bonds as part of its QT programme (which has been lowered in scale as well, to £70bn from £100bn). But that seems to be a drop on a hot plate. Yields in other core areas rise too, be it to a lesser extent. US rates add 1.2-2.7 bps, leaving further behind the recent lows in the wake of the Fed’s rate cut on Wednesday. We’re closely watching the inflation expectations component, which is nearing the recent highs around 2.5%. There’s some buzz again around the Fed’s 2% target. Fed’s Kashkari said today the central bank is not ok with 3% inflation but some say Wednesday’s precautionary move (to support the labour market even though inflation is still too high and not expected to drop below target) is a sign the Fed is willing to tolerate higher inflation. European rates add a few bps as well with Bunds slightly underperforming vs. swap. Between euro area countries, the French spread has been trading higher than Italy’s every day all week in what is nothing less than a historical shift. The US dollar has a slight upper hand. DXY rises to 97.7 in a three-day win streak. EUR/USD drifts south to 1.175. Sterling loses ground as well with EUR/GBP pushing beyond 0.87(1). The Japanese yen pared early gains to trade flat around 148. The BoJ stood pat this morning but in a 7-2 split. The dissenters wanted to hike to 0.75%, saying that the 2% price target has been achieved.

News & Views

Previewing next week’s policy decision, it is widely expected that the MNB will leave its policy rate unchanged at 6.5%. Headline inflation (4.3% in August) has eased toward 4%, but underlying measures such as core inflation and inflation expectations remain uncomfortably high, leaving no room for a premature move. At the same time, the economic activity offers no strong support for policy tightening. Retail sales and underlining domestic demand is fragile. Growth remains subdued overall (0.4% Q/Q in Q2, but only 0.1% higher activity compared to the same period last year). Despite weak growth, MNB has no choice but to keep its focus on inflation. Positive news for policy makers: the forint performed rather well of late with EUR/USD moving toward 390. This should help to ease second round inflation effects. However, the forint remains vulnerable, amongst others as market position is quite strongly skewed HUF-long leaving the currency exposed to external shocks. In a somewhat longer term perspective, KBC assesses that a chances on a MNB rate cut are slim this year. A narrow window for a symbolic 25 bps cut in December could open if three conditions are met: 1. Rating agencies in their autumn reviews have to leave the Hungarian Credit rating unchanged; 2.The Fed has to continue policy easing global yields spreads; 3. The forint strengthening toward EUR/HUF 385 would give the MNB some room of maneuver. Even so, such a move won’t mark the beginning of a new easing cycle, but serve as a signal of flexibility, an acknowledgment that domestic and external conditions had aligned sufficiently to justify a modest step.

According to the German IFO institute, sentiment in residential construction in Germany clouded over again in August, with the index falling from minus 24.2 to minus 26.3 points. Both companies’ expectations for the coming months and their assessments of the current situation worsened. “The cautious upturn in sentiment of recent months is on hold,” said Klaus Wohlrabe, Head of Ifo Surveys. He assesses that it will take time before the increase in building permits is reflected in the order books. In a broader perspective, Ifo still sees companies struggling with weak demand. The share of companies with a lack of orders eased slightly but at 45.7% remains at a high level.

Canada’s Retail Sales Slips, Canadian Dollar Edges Higher

The Canadian dollar is in negative territory for a third straight day. In the North American session, USD/CAD is trading at 1.3820, up 0.18% on the day.

Canada's retail sales slide

Canada's retail sales declined by 0.8% m/m in July, a sharp dowrturn from the 1.6% gain in June. The volatility in retail sales reflects uncertainty over the US tariffs, which has affected consumer spending. August is expected to show a rebound, with a preliminary estimate of a 1% gain, which would make up for the July decline.

US unemployment claims slip

There are no US releases today but there was positive news from the employment front on Thursday. Unemployment claims fell to 231 thouand last week, down from 264 thousand a week earlier, which was the highest reading since October 2021. The sharp spike in claims, together with soft nonfarm payrolls, had elevated concerns about the health of the US labor market.

The latest unemployment claims release indicates that layoff are low, but hiring remains weak as the demand for workers has slowed. The Federal Reserve is keeping a close eye on the labor market and Fed Chair Powell cited the downside risk to employment as the reason for the rate cut, the first since December 2024.

- USDCAD is testing resistance at 1.3808. Next, there is resistance at 1.3821

- 1.3796 and 1.3783 are providing support

USDCAD 4-Hour Chart, September 19, 2025

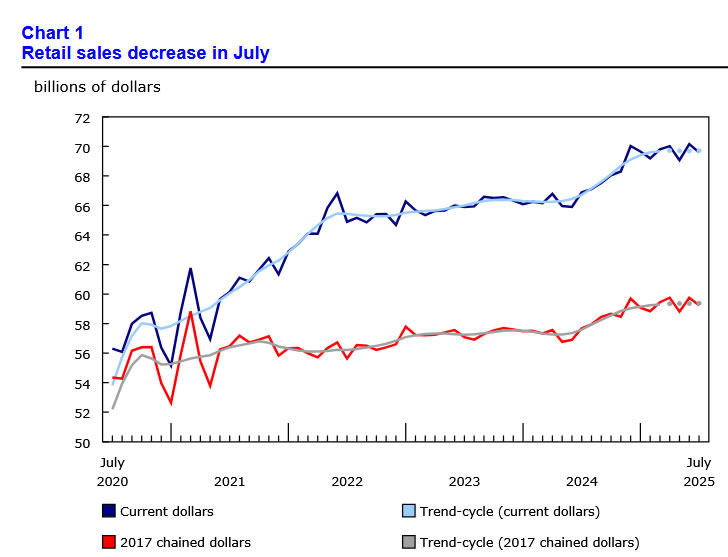

Canada: Retail Sales Falter in July, But Rebound in August

Retail sales contracted by 0.8% month-on-month (m/m) in July, matching Statistics Canada's advanced estimate.

After adjusting for inflation, the volume of retail sales declined 0.8% m/m.

Auto sales continued to grow at a modest pace, rising 0.2% m/m and providing a small offset to the headline decline.

Receipts at gas stations and fuel vendors fell 0.9%, as gasoline prices continued to decline in July. In volumes terms, however, sales rose 0.2% m/m.

Core sales – excluding auto sales and receipts at gas stations – fell 1.2% m/m in July. Food and beverage stores led the decline (-2.5% m/m) despite ongoing price inflation. Sales at clothing and clothing accessories stores also retreated (-2.9% m/m), giving back some of the strong gains recorded in June.

The only categories to record gains were furniture and home furnishings stores (+1.0% m/m) and miscellaneous store retailers (+0.5% m/m), though neither added meaningfully to the headline.

E-commerce sales rose by 2.2% m/m in July.

Statistics Canada's advanced estimate points suggests that sales recovered in August, rising 1.0% m/m.

Key Implications

Volatility in the data remains exceptionally high, however nominal sales in Q3 are now tracking 1.1% annualized growth despite July's outsized weakness.

Cooling employment and softer wage gains are likely to catch up with consumers in Q3, reinforcing a more frugal mindset. While wealth effects could continue to buoy services spending among higher-income households, another leg up in domestic tourism and related spending appears unlikely. Goods demand, meanwhile, looks set for a sizeable contraction, with vehicle sales likely to pull back in in the third quarter.

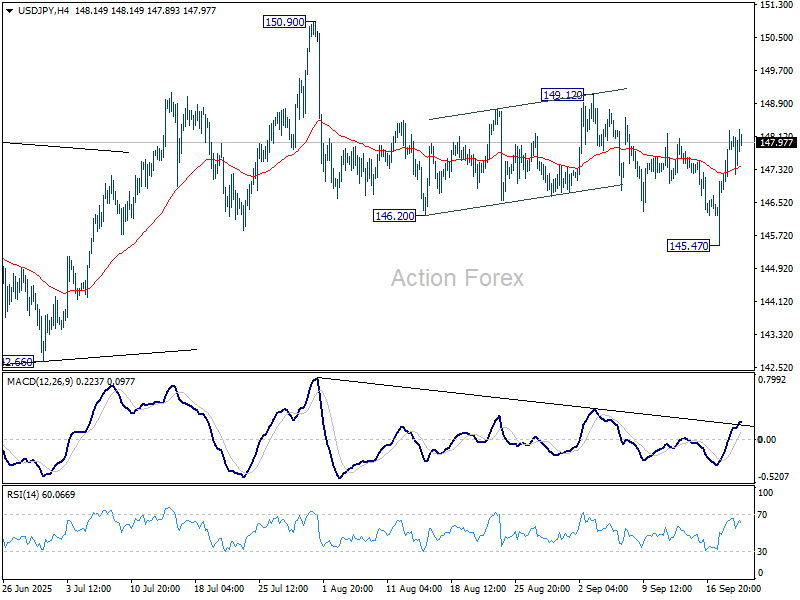

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 147.09; (P) 147.68; (R1) 148.59; More...

Outlook in USD/JPY is unchanged and intraday bias remains neutral. On the upside, break of 149.12 resistance will suggest that pullback from 150.90 has completed as a correction, and rise from 139.87 is still in progress. Further rise should then be seen back to retest 150.90 next. On the downside, below 145.47 will resume the fall to 142.66 support next.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 will argue that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. In case the corrective pattern extends with another fall, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.

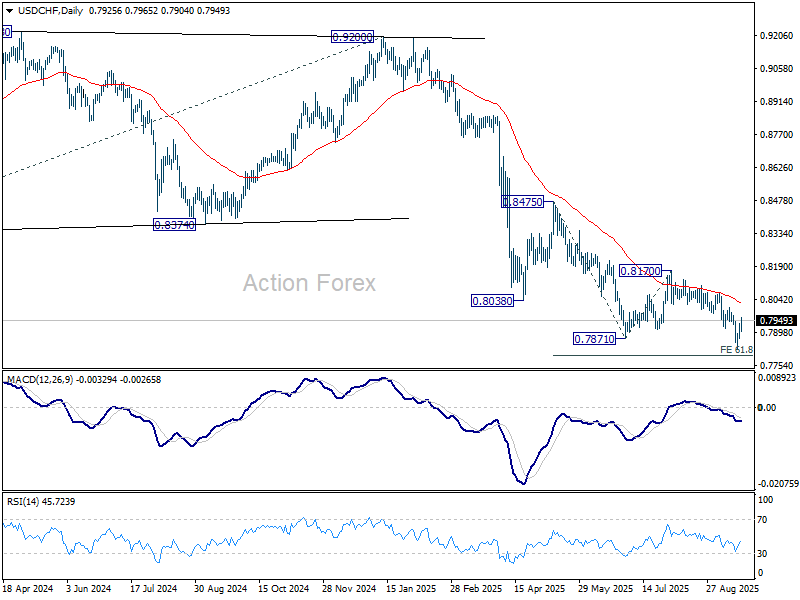

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7885; (P) 0.7912; (R1) 0.7951; More….

No change in USD/CHF's outlook and intraday bias stays neutral. While rebound from 0.7828 might extend higher, outlook will stay bearish as long as 0.8006 resistance holds. On the downside, break of 0.7828 will resume larger down trend to 61.8% projection of 0.8475 to 0.7871 from 0.8170 at 0.7797.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds.

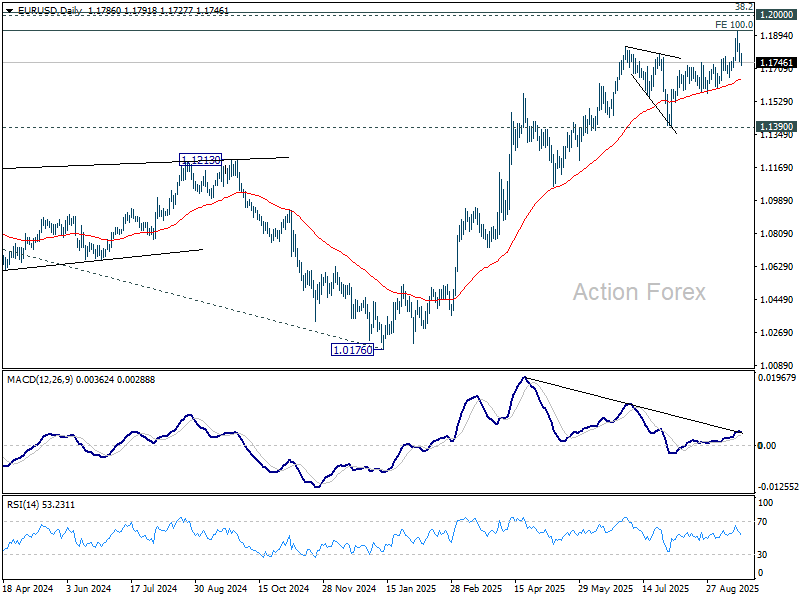

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1743; (P) 1.1795; (R1) 1.1841; More...

EUR/USD's break of 1.1741 resistance turned support indicates short term topping at 1.1917, after rejection by 1.1916 projection level. Intraday bias is back on the downside. Deeper fall should be seen to 1.1573 support next. For now, risk will stay on the downside as long as 1.1917 resistance holds, in case of recovery.

In the bigger picture, rise from 0.9534 (2022 low) long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. Further rise could still be seen as long as 1.1390 support holds. Break of 1.1917 will target 1.2 psychological level. Decisive break there will carry larger bullish implications. However, considering bearish divergence condition in D MACD, firm break of 1.1390 will indicate medium term topping.

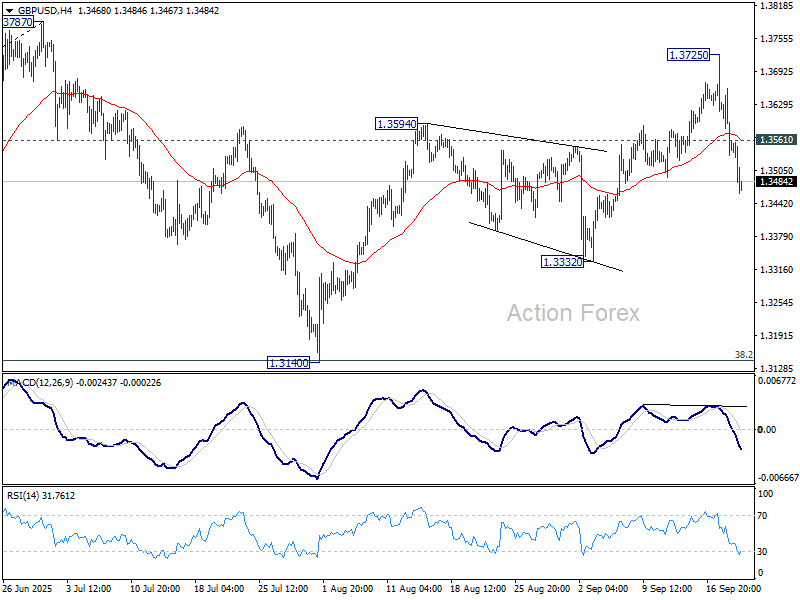

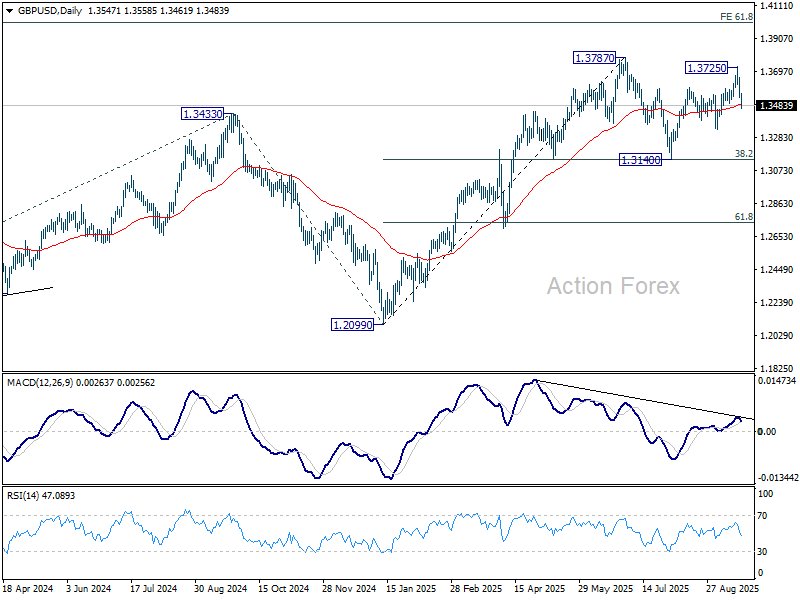

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3505; (P) 1.3583; (R1) 1.3631; More...

GBP/USD's break of 55 D EMA (now at 1.3486) suggests that rebound from 1.3140 has completed at 1.3725. Fall from there is seen as the third leg of the corrective pattern from 1.3787. Intraday bias is back on the downside for 1.3332 support first. Break there will target 1.3140 support next. On the upside, above 1.3561 minor resistance will turn intraday bias neutral again first.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.3151) holds, even in case of deep pullback.

Dollar Gains Momentum, Outpaces Peers as 10-Year Nears 4.15%

Dollar’s rebound is gathering strong momentum today, surging broadly across the board as markets continue to realign with the Fed’s message from midweek. After being under pressure earlier in the week, the greenback is now positioned to potentially end as one of the strongest performers. Supporting the move, U.S. Treasury yields have extended higher, with the 10-year looking set to break through 4.15% mark. That is notable considering the benchmark yield briefly dipped below 4% twice earlier in the week.

The resilience in Dollar and yields underscores investor confidence that the Fed remains in control of the easing process rather than being pushed into aggressive action by market forces. Indeed, traders appear to have taken comfort in the Fed’s framing of its rate cut as “risk management” rather than a response to imminent economic weakness. Policymakers still project two more cuts this year, but with the overall policy rate just 25bps below June’s projections and the terminal rate expected to stay above the long-run neutral. The message is that the Fed is easing with caution, not capitulation.

Meanwhile, Yen was briefly buoyed by a slightly more hawkish than expected BoJ vote, which saw two dissenters calling for a rate hike. The move triggered a sharp intraday jump in Yen crosses. But that strength quickly faded as Governor Kazuo Ueda’s press conference highlighted the board’s more cautious stance. Ueda stressed that in his personal view, “underlying inflation is still somewhat below 2% but approaching that level.” He added that while upside price risks identified by board member Naoki Tamura deserved attention, downside risks tied to the intensifying impact of U.S. tariffs on Japan’s economy could not be ignored. His balanced tone signaled that the hawkish dissent remains a minority position.

For the week so far, Swiss Franc and Loonie still lead the performance table, followed closely by Dollar. If current momentum persists into the close, the greenback could overtake both. At the other end, Kiwi and Aussie remain pinned to the bottom, with Sterling also soft. Euro and Yen are stuck in the middle of the pack.

In Europe, at the time of writing, FTSE is up 0.03%. DAX is down -0.16%. CAC is up 0.15%. UK 10-year yield is up 0.043 at 4.723. Germany 10-year yield is up 0.025 at 2.750. Earlier in Asia, Nikkei fell -0.57%. Hong Kong HSI closed flat. China Shanghai SSE fell -0.30%. Singapore Strait Times fell -0.23%. Japan 10-year JGB yield rose 0.04 to 1.641.

Canada's retail sales drop -0.8% mom in July, but advance data signal August rebound

Canadian retail sales declined -0.8% mom to CAD 69.6B in July, worse than expectations of a -0.6% drop. Core sales, which exclude motor vehicles, parts, and fuel, fell even more sharply by -1.2%.

The downturn was broad-based, with eight of nine subsectors posting declines, led by food and beverage retailers. The figures point to cooling consumer demand as households remain squeezed by high borrowing costs and lingering price pressures.

Still, Statistics Canada’s advance estimate suggested a brighter picture ahead, with retail sales projected to rebound by 1.0% mom in August.

Fed’s Kashkari sees two more cuts this year, labor market risks more pressing

Minneapolis Fed President Neel Kashkari said the balance of risks facing the U.S. economy tilted toward the labor market rather than inflation. In an essay, he argued that given the “large concurrent changes” in trade, immigration, and tax policies, and the mixed signals in the economy, the more pressing danger is “rapid further weakening” in employment rather than a major inflation overshoot.

Kashkari noted that labor markets historically can deteriorate “quickly and non-linearly,” making preemptive action necessary. By contrast, he said tariff-related uncertainty implies a risk of inflation persistence near 3% rather than a sharp surge to 4–5%.

That backdrop led him to support this week’s rate cut, raising his own projection from two to three cuts this year in the Fed’s Summary of Economic Projections.

Still, Kashkari stressed that policy is not on a preset course. If the labor market proves more resilient or inflation surprises on the upside, the Fed should pause, or even consider raising rates again. Conversely, if jobs weaken more rapidly than expected, he said policymakers should be ready to act more aggressively to support growth.

UK retail sales rise 0.5% mom in August, third monthly gain

UK retail sales rose 0.5% mom in August, slightly above expectations of 0.4%, marking a third consecutive month of growth. Still, volumes remain shy of their March 2025 peak, highlighting that the rebound is steady but incomplete.

The broader three-month trend still points to weakness, with sales down -0.1% compared to the three months to May. However, this marks an improvement from July’s -0.6% decline, indicating the downturn in spending is losing intensity.

BoJ holds with two members calling for hike, starts selling ETFs and J-REITs

The BoJ kept rates steady at 0.50% in September, but the 7–2 vote revealed a growing hawkish bias. Naoki Tamura and Hajime Takata broke ranks to support a rate increase, citing upside risks to inflation and progress toward achieving the 2% price stability target. Takata said that Japan has more or less achieved its inflation goal, while Tamura argued that the key rate should move closer to neutral given skewed risks to the upside.

Alongside the decision, the BoJ unveiled plans to shrink its massive balance sheet by selling assets. The Bank will sell ETFs at a pace of JPY 330B annually and J-REITs at JPY 5B, with the principle of minimizing market disruption. With its balance sheet at 125% of GDP—far larger than other major central banks—the BoJ’s move marks a notable shift toward normalization, even as rates remain unchanged for now.

Japan core CPI Slows to 2.7%, lowest since late 2024

Japan’s consumer inflation eased notably in August, with both headline CPI and core CPI (excluding fresh food) falling to 2.7% yoy from 3.1% in July, the lowest since November 2024. Despite the slowdown, inflation has remained above the BoJ’s 2% target for over three years.

Core-core CPI, which strips out both fresh food and energy and is seen as a key gauge of underlying price dynamics, ticked down to 3.3% yoy from 3.4%. The moderation suggests a gradual cooling in inflationary pressures, though price growth remains elevated relative to historical norms.

Food prices continued to drive the cost-of-living squeeze, with processed food up 8.0% yoy, though slower than July’s 8.3%. Rice inflation also eased to 69.7% yoy from an eye-watering 90.7%. Energy prices provided some relief, falling -3.3% yoy after a -0.3% drop in July.

NZ exports jump 23% in August, imports flat, deficit at NZD -1.2B

New Zealand recorded a goods trade deficit of NZD 1.2B in August as imports outpaced a sharp rise in exports. Goods exports climbed NZD 1.1B, or 23% yoy, to NZD 5.9B, supported by strong shipments to major partners. Imports slipped slightly, falling NZD 30m (-0.4% yoy) to NZD 7.1B, but remained elevated enough to keep the monthly balance in deficit.

Export growth was broad-based, with China (+35% yoy, the EU (+52%), Australia (+17%), and the U.S. (+14%) all showing strong gains. Japan was the notable exception, where exports fell -11% yoy, driven by a NZD 28m decline in milk powder, butter, and cheese.

On the import side, flows from China rose 6.2% yoy, while purchases from the EU fell -6.0% and from the U.S. declined -1.3%. The largest pullback came from South Korea, where imports dropped -32% yoy.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3505; (P) 1.3583; (R1) 1.3631; More...

GBP/USD's break of 55 D EMA (now at 1.3486) suggests that rebound from 1.3140 has completed at 1.3725. Fall from there is seen as the third leg of the corrective pattern from 1.3787. Intraday bias is back on the downside for 1.3332 support first. Break there will target 1.3140 support next. On the upside, above 1.3561 minor resistance will turn intraday bias neutral again first.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.3151) holds, even in case of deep pullback.

Canada’s retail sales drop -0.8% mom in July, but advance data signal August rebound

Canadian retail sales declined -0.8% mom to CAD 69.6B in July, worse than expectations of a -0.6% drop. Core sales, which exclude motor vehicles, parts, and fuel, fell even more sharply by -1.2%.

The downturn was broad-based, with eight of nine subsectors posting declines, led by food and beverage retailers. The figures point to cooling consumer demand as households remain squeezed by high borrowing costs and lingering price pressures.

Still, Statistics Canada’s advance estimate suggested a brighter picture ahead, with retail sales projected to rebound by 1.0% mom in August.

Fed’s Kashkari sees two more cuts this year, labor market risks more pressing

Minneapolis Fed President Neel Kashkari said the balance of risks facing the U.S. economy tilted toward the labor market rather than inflation. In an essay, he argued that given the “large concurrent changes” in trade, immigration, and tax policies, and the mixed signals in the economy, the more pressing danger is “rapid further weakening” in employment rather than a major inflation overshoot.

Kashkari noted that labor markets historically can deteriorate “quickly and non-linearly,” making preemptive action necessary. By contrast, he said tariff-related uncertainty implies a risk of inflation persistence near 3% rather than a sharp surge to 4–5%.

That backdrop led him to support this week’s rate cut, raising his own projection from two to three cuts this year in the Fed’s Summary of Economic Projections.

Still, Kashkari stressed that policy is not on a preset course. If the labor market proves more resilient or inflation surprises on the upside, the Fed should pause, or even consider raising rates again. Conversely, if jobs weaken more rapidly than expected, he said policymakers should be ready to act more aggressively to support growth.