Sample Category Title

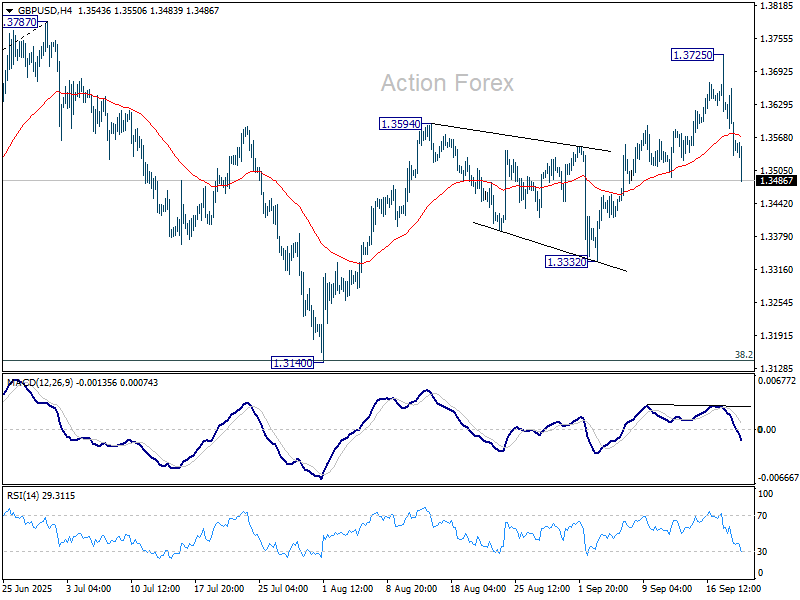

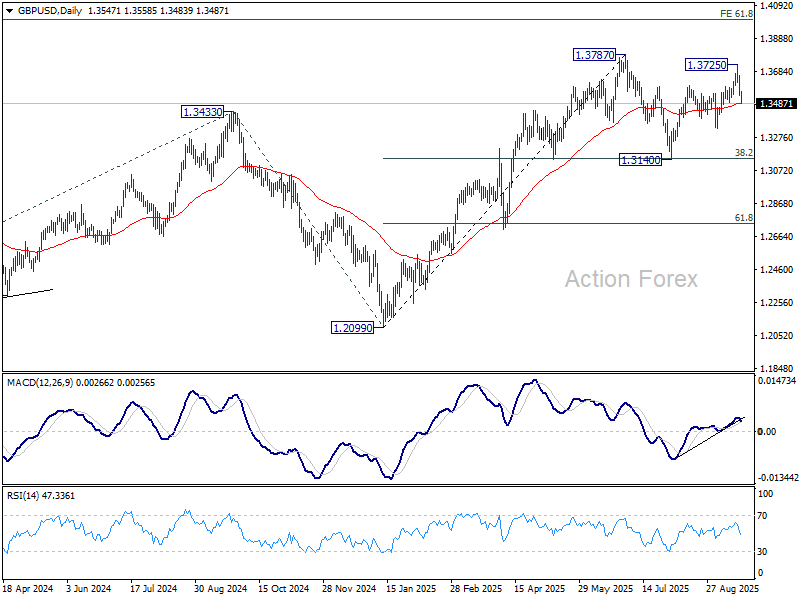

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3505; (P) 1.3583; (R1) 1.3631; More...

GBP/USD's fall from 1.3725 accelerates lower today, and immediate focus is now on 55 D EMA (now at 1.3488). Sustained break there will suggest that rebound from 1.3140 has completed as the second leg of the corrective pattern from 1.3787 high. The third leg has already started. Deeper fall should then be seen to 1.3332 support first. Break will target 1.3140 next. On the upside, break of 1.3725 will bring retest of 1.3787 high.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.3151) holds, even in case of deep pullback.

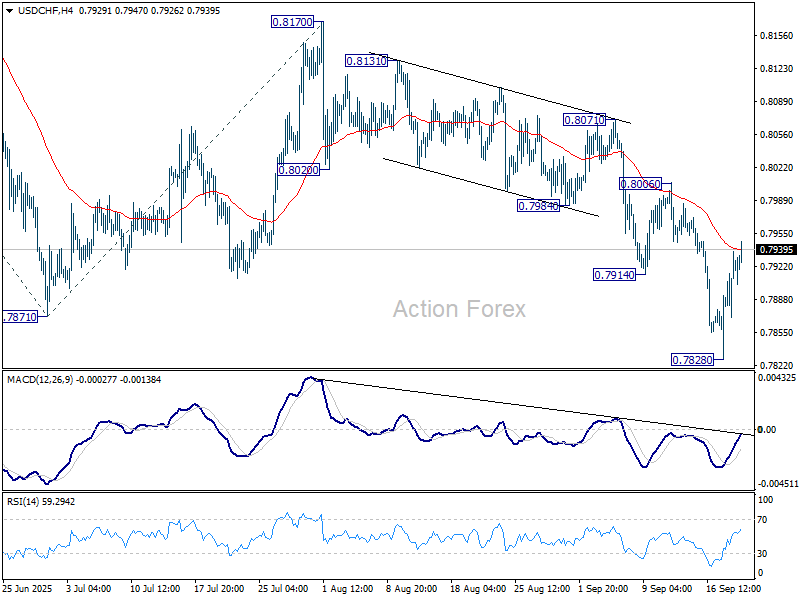

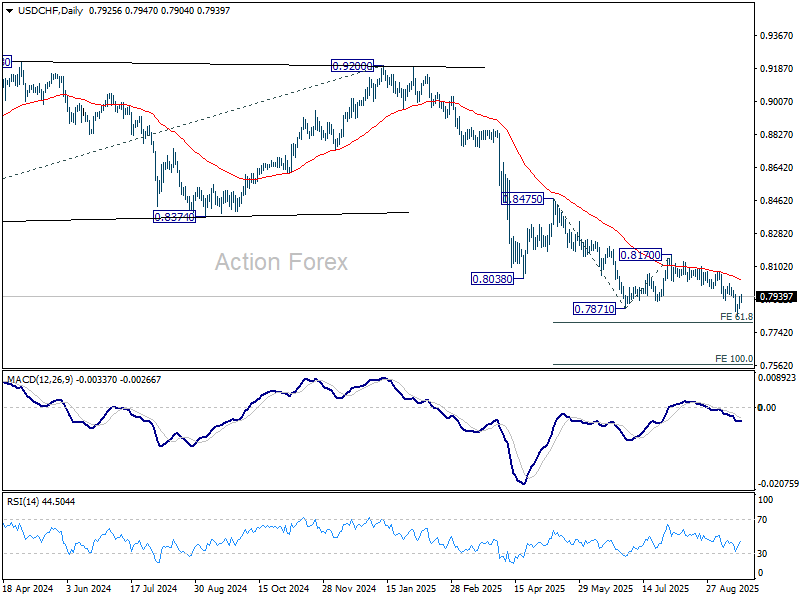

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7885; (P) 0.7912; (R1) 0.7951; More….

Intraday bias in USD/CHF remains neutral at this point. While rebound from 0.7828 might extend higher, outlook will stay bearish as long as 0.8006 resistance holds. On the downside, break of 0.7828 will resume larger down trend to 61.8% projection of 0.8475 to 0.7871 from 0.8170 at 0.7797.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds.

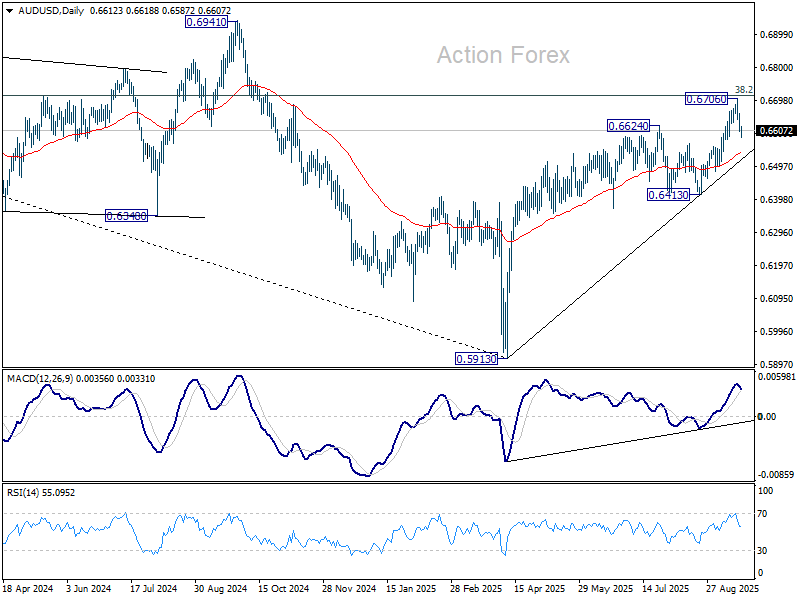

AUD/USD Daily Report

Daily Pivots: (S1) 0.6593; (P) 0.6626; (R1) 0.6646; More...

Intraday bias in AUD/USD remains neutral for the moment. Some more consolidations would be seen, but further rally is expected as long as 55 D EMA (now at 0.6541) holds. Decisive break of 0.6713 fibonacci level will carry larger bullish implications. However, sustained break of 55 D EMA will confirm short term topping and rejection by 0.6713. Deeper fall should then be seen back to 0.6413 support.

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. While stronger rally cannot be ruled out, outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, sustained break of 0.6713 will be a strong sign of bullish trend reversal, and path the way to 0.6941 structural resistance for confirmation.

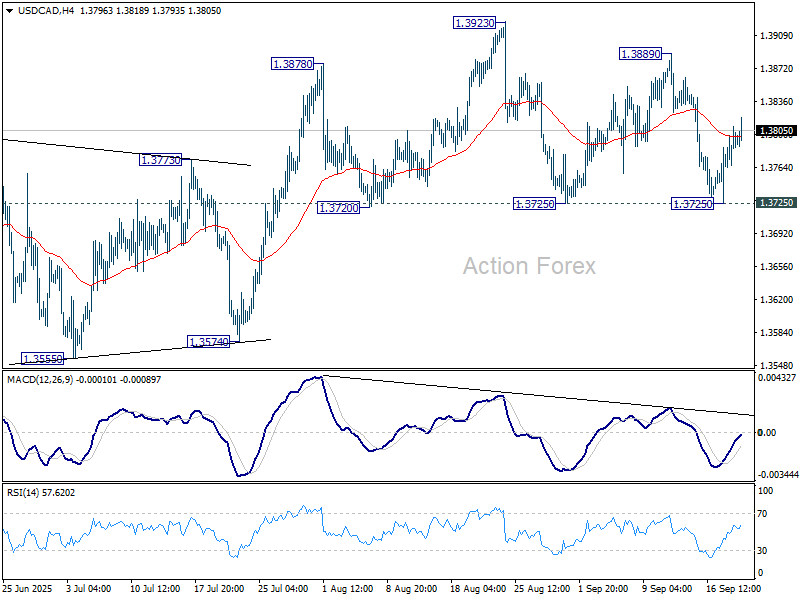

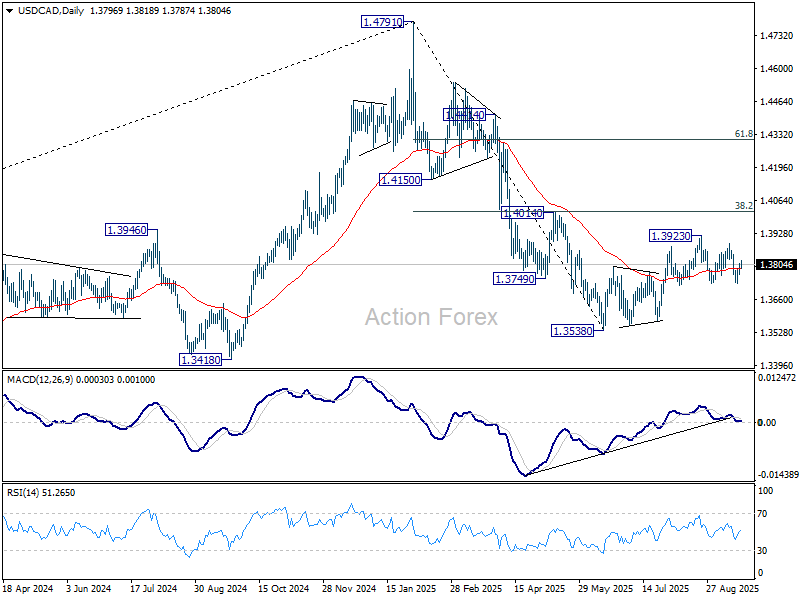

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3772; (P) 1.3791; (R1) 1.3816; More...

Intraday bias in USD/CAD remains neutral, and with 1.3725 support intact, rise from 1.3538 could still extend higher. ON the upside, break of of 1.3889 should resume the corrective rise through 1.3923 to 1.4014 cluster resistance. On the downside, though, firm break of 1.3725 will indicate that the corrective rebound has completed, and bring deeper fall back to 1.3574 support.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 cluster resistance (38.2% retracement of 1.4791 to 1.3538 at 1.4017) holds. Next target is 61.8% retracement of 1.2005 (2021 low) to 1.4791 at 1.3069.

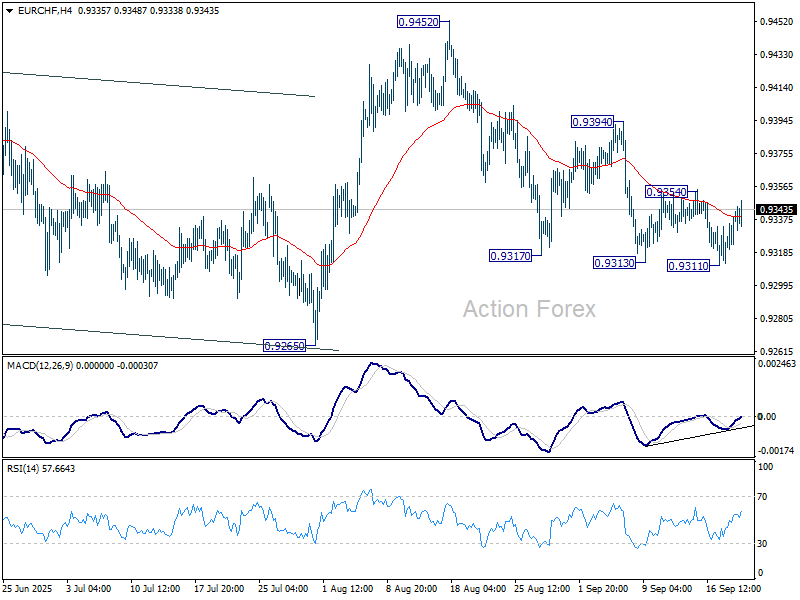

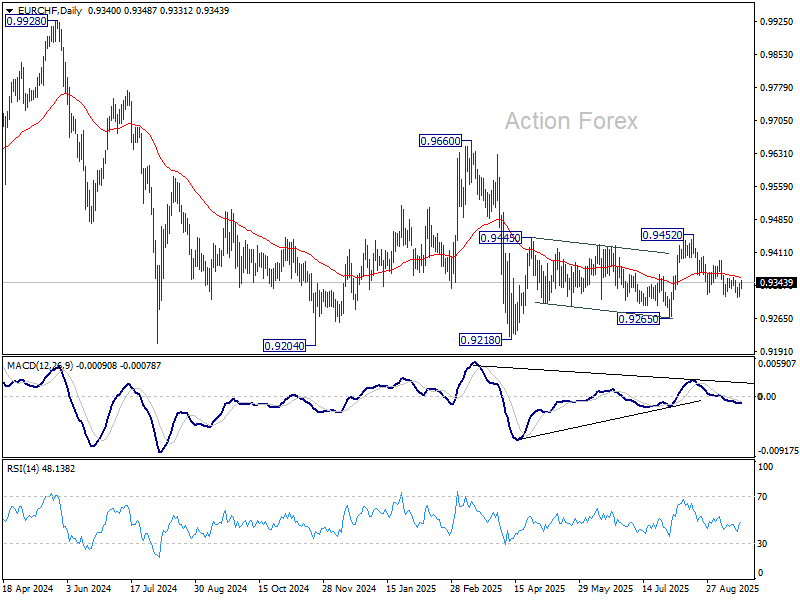

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9318; (P) 0.9331; (R1) 0.9354; More...

EUR/CHF is staying in range of 0.9311/9354 and intraday bias stays neutral. Further decline will remain in favor as long as 0.9354 resistance holds. Firm break of 0.9311 will extend the fall from 0.9452 to retest 0.9218 low. Nevertheless, considering bullish convergence condition in 4H MACD, firm break of 0.9354 will confirm short term bottoming, and turn bias back to the upside for 0.9394 resistance next.

In the bigger picture, the down trend from 0.9204 (2018 high) might still be in progress considering that EUR/CHF is staying well inside the long term falling channel. However, with bullish convergence condition in W MACD, downside potential should be limited in case of another fall. Instead, firm break of 0.9660 resistance will be an important sign of medium term bullish trend reversal.

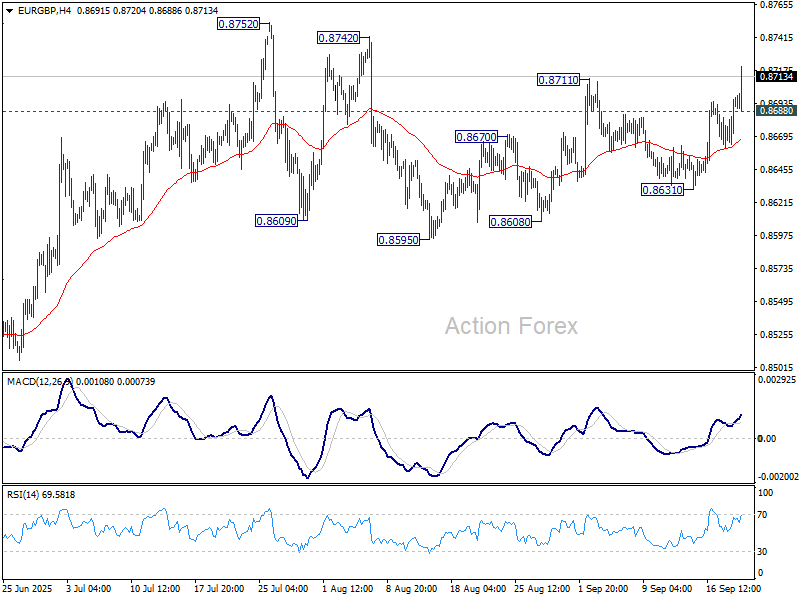

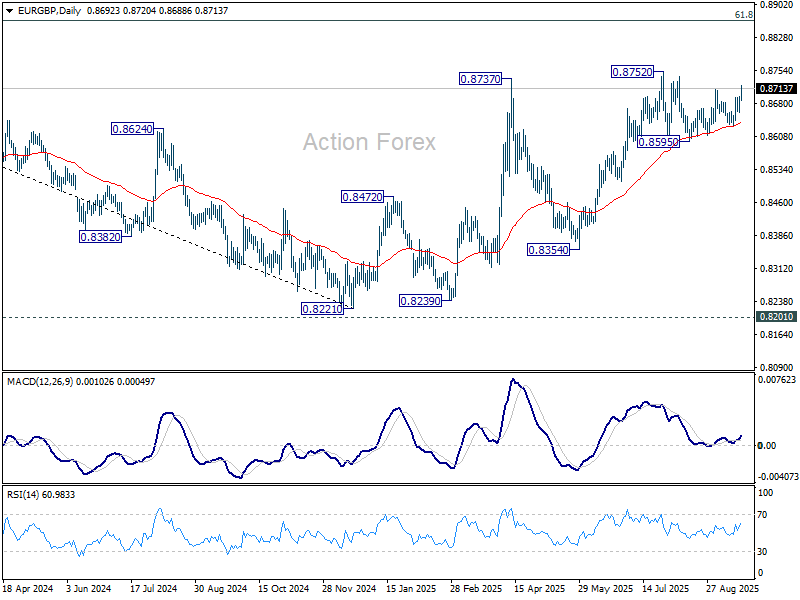

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8671; (P) 0.8685; (R1) 0.8710; More...

EUR/GBP's rally continues today and intraday bias stays on the upside. The rebound from 0.8595 is in progress for retesting 0.8752 high. Firm break there will extend the rise from 0.8221 to 0.8867 fibonacci level. On the downside, below 0.8688 minor support will turn intraday bias neutral again first. But further rise is expected as long as 0.8631 support holds, in case of retreat.

In the bigger picture, the structure from 0.8221 medium term bottom are not impulsive enough to suggest that it's reversing the down trend from 0.9267 (2022 high). But even if it's a correction, further rise could still be seen to 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Nevertheless, sustained trading below 55 W EMA (now at 0.8518) will argue that the pattern has completed and bring retest of 0.8221 low.

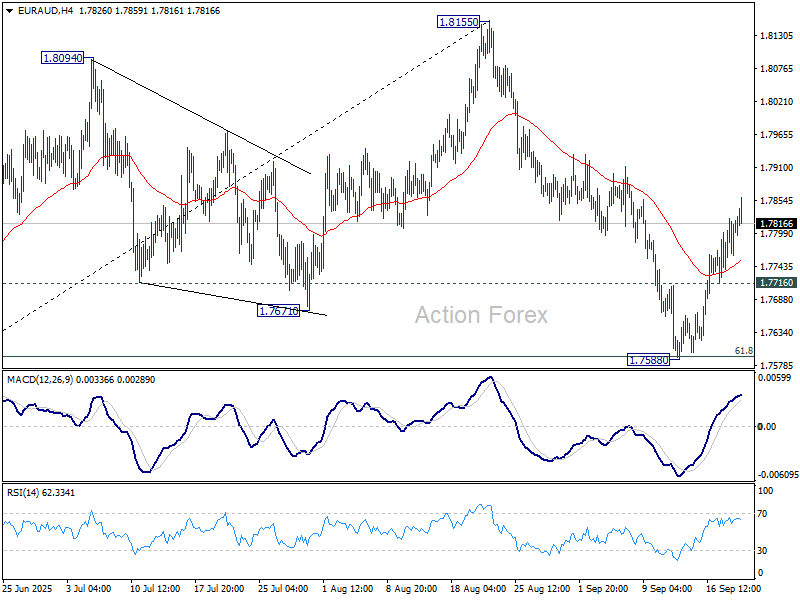

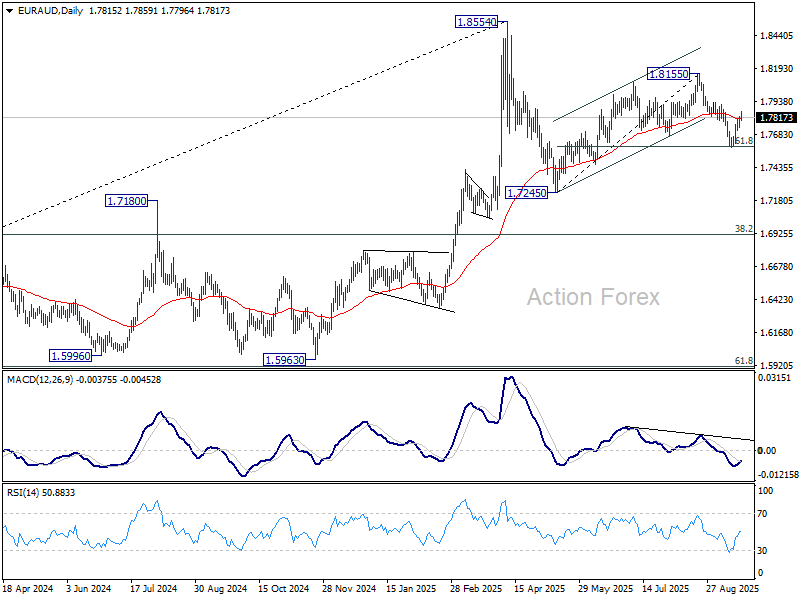

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7775; (P) 1.7801; (R1) 1.7854; More...

EUR/AUD's rebound from 1.7588 extended higher today and the breach of 55 D EMA (now at 1.7809) suggests that pullback from 1.8155 has completed, after defending 61.8% retracement of 1.7245 to 1.8155 at 1.7593. Intraday bias on the upside for retesting 1.8155 resistance. On the downside, though, below 1.7716 minor support will turn bias back to the downside for 1.7588 again.

In the bigger picture, price actions from 1.8554 medium term top are seen as a corrective pattern. Deeper fall could be seen as the pattern extends, but downside should be contained by 38.2% retracement of 1.4281 (2022 low) to 1.8554 at 1.6922 to bring rebound. Uptrend from 1.4281 is expected to resume at a later stage.

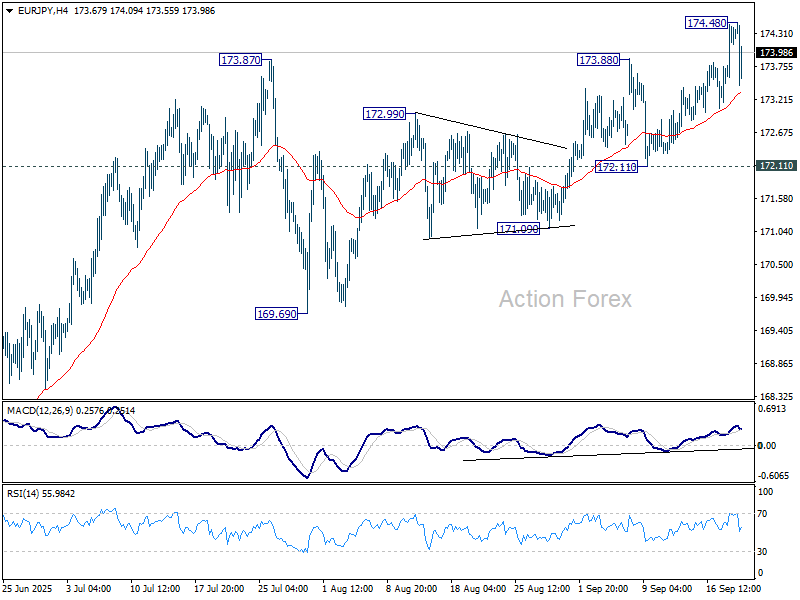

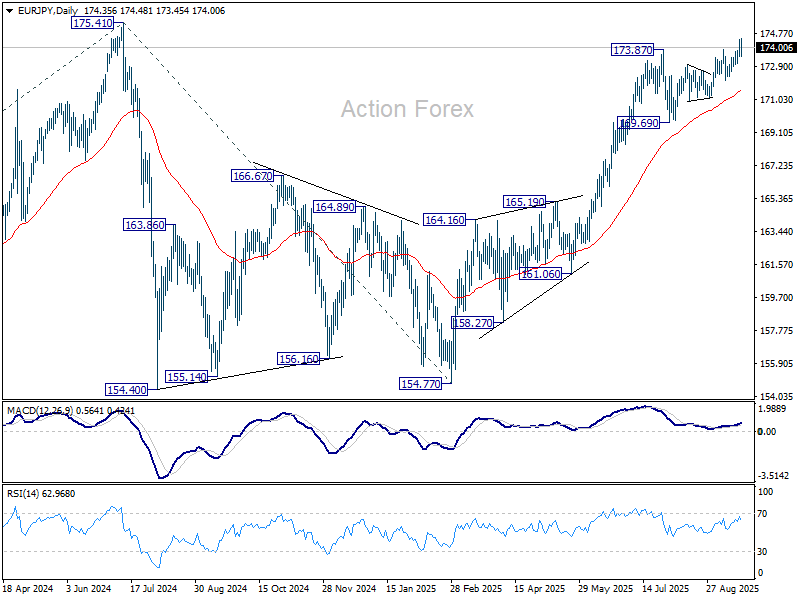

EUR/JPY Daily Outlook

Daily Pivots: (S1) 173.76; (P) 174.11; (R1) 174.80; More...

Intraday bias in EUR/JPY is turned neutral with current retreat, and some consolidations would be seen below 174.48. Further rise is expected as long as 172.11 support holds. Above 174.48 will resume larger rise from 154.77 to retest 175.41 high. However, firm break of 172.11 support will confirm short term topping, and turn bias back to the downside for deeper pullback.

In the bigger picture, current rally from 154.77 is still tentatively seen as resuming the larger up trend. Firm break of 175.41 (2024 high) will confirm and target 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. However, sustained break of 169.69 support will delay this bullish case, and probably extend the correction from 175.41 with another fall.

Pretty Calm End of the Week

Markets

The Bank of England’s policy meeting won’t exactly go down as one of the more important ones in history. The key message on policy rates remains the same as before: stubborn inflation limits the room for rate cuts from the current 4%. CPI is expected to hit 4% in September and until clearer disinflation signs emerge, the policy rate isn’t going anywhere anytime soon. The annual quantitative tightening target for the period October ’25 through September ’26 was cut to £70bn from £100bn with an overweight in selling short (40%) and medium-term (40%) bonds. That move was broadly expected as well since the BoE doesn’t want to be the one adding even pressure to already vulnerable long-term gilts. Sterling slipped to around EUR/GBP 0.87 and the UK gilt yield curve bear steepened, be it in a move that had little to do with the outcome. We saw similar curve shifts in the US (+1 to 3.4 bps, but masking an intraday 10 bps+ move) and especially in Europe. German rates shot up 8 bps in the 30-yr tenor. The steepening is a bit odd in timing, particularly in the US as the bulk happened following a huge drop in US jobless claims (231k from 264k). Did Wednesday’s first of probably several Fed rate cuts in a labour market environment that’s seemingly not completely derailing trigger fear for renewed inflation momentum? Market-based inflation expectations have been trending higher towards their recent highs in any case the last couple of weeks, diverging from real yields. If it’s indeed the inflation component supporting yields higher it helps explain the decent stock performance (WS +1% in the Nasdaq). The dollar gained for a second day straight, pushing EUR/USD back below the 1.18 big figure. DXY rose to 97.4. The Japanese yen struggled ahead of the Bank of Japan decision (see below) but is in better shape since. USD/JPY trades around 147.47. The pair hasn’t gone anywhere in a tight 146-149 trading range ever since the start of summer.

We’re looking at a pretty calm end of the week if the economic calendar is of any guide, offering a chance to let underlying market dynamics play after a heavy central bank week. UK retail sales are among the final noteworthy data for today. They came in slightly better than expected (0.5% m/m headline, 0.8% core) but leave no marks on GBP. US President Trump and his Chinese counterpart Xi are expected to hold a call today to discuss the fate of TikTok but possible the broader trade topic as well. Fed’s Miran double television appearance is worth watching. Miran dissented on Wednesday by voting for a 50 bps cut instead of the delivered 25 bps.

News & Views

The UK GFK consumer confidence index dropped from -17 in Augst to -19 September. All measures of the index were down. UK consumers turned less confident both on their personal financial during the last year (-7 from -4) as well on expectations for their finances for the next 12 months (4 from 5), but both levels were still higher y/y. This also applies for the index or major purchases (-16 from -13, vs -23 last year). Consumers turned less confident on the general economic situation over the past year (-45 from -42) and the next 12 months (-32 from -30). The savings index dropped 8 points (22), to slightly below last year’s level. GFK analyses that ‘there’s an autumnal chill in the air this month’ and that ‘The August 7th decrease in interest rates does not appear to have provided any obvious boost to the financial mood of consumers or drawn attention away from day-to-day cost issues’. GFK fears that with tax rises expected in the November budget, the risk is that confidence inevitably falls.

Japanese August CPI excluding fresh food eased from 3.1% to 2.7%, due to utility subsidies. The core measure additionally excludes energy dropped only slightly from 3.4% to 3.3%, still firmly above the BoJ’s 2% target. The publication came as the BoJ debated its policy decision. The BoJ as expected left its policy rate unchanged at 0.5%, supported by a vote of 7-2, with two members voting for a 25 bps rate hike. The Bank of Japan also announced that it will start to sell ETFs and real estate investment trusts (J-REITs) meeting three principles including that it should avoid inducing destabilizing effects on financial markets. It will sell ETFs to the market at a pace of about 330 bln yen per year and J-REITs at about 5 bln yen per year. The 2-y Japanese yield (0.915%) jumped to the highest level since 2008 as expectations on frontloading a potential further rate hike rose. The yen strengthened from the USD/JPY 148 area to currently trade near 147.5. After opening higher, the Nikkei briefly dropped more than 2% off the intraday top levels after the announcement of ETF selling, but reversed a part soon (-0.4%).

Trump and Xi to Discuss TikTok Deal Amid Ongoing Trade War

In focus over the weekend

US President Trump plans to speak with Chinese President Xi today, as the two sides appear to be making ground on a TikTok deal. A deal for the social media app might act as a catalyst for improving the relationship between the two largest economies amid an ongoing trade war.

The data side is fairly quiet, with UK retail sales as the main print we will be watching.

Early Monday, China announces the Loan Prime Rates (LPR), which is widely expected to be unchanged. The LPRs are normally adjusted following changes to the 1-week reverse repo rate, which is the rate China uses to signal policy changes. This rate has not been changed since May, though. While there is pressure for more stimulus, broad based rate cuts may not be the preferred tool for China as they are also concerned about fuelling a liquidity driven equity bubble. We expect more targeted stimulus measures coming soon.

Economic and market news

What happened overnight

In Japan, the Bank of Japan stayed on hold and kept interest rates unchanged at 0.50%. The decision was in line with expectations, and no outlook report followed as it was a 'small' meeting. With a solid growth picture and real wage growth back in positive territory, we think conditions are lining up for a rate hike at the October meeting, where the decision can also be supported by an updated growth and inflation outlook. A potential snap election in the wake of the LDP-leadership election 4 October could also end up postponing a potential rate hike to December.

Prior to the decision, August CPI data was released and matched expectations. CPI inflation excluding fresh food, Bank of Japan's favourite measure) was at 2.7% y/y, staying above the Bank of Japan's target. However, the measure is largely driven by food, as core inflation (CPI excluding food and energy) remained at a more modest 1.6%.

What happened yesterday

In the US, President Trump made another move targeting the Federal Reserve Governor Lisa Cook. An application was sent to the Supreme Court, asking for permission to fire the Fed Governor. The ongoing battle is jeopardizing the Fed's independence as Trump seeks to gain influence on key rate decisions.

In Norway, Norges Bank cut policy rates by 25bp to 4.00% in a unanimous decision. The guidance that accompanied the decision was on the cautious side and excludes the probability of rate cuts for the next three meetings (Nov, Dec and Jan). Due to this, we modify our Norges Bank call and no longer pencil in a December 2025 rate cut. Given our economic projections we now pencil in four 25bp rate cuts in 2026 (Mar, Jun, Sep and Dec), which would bring the policy rate to 3.0% by the end of 2026.

In the UK, the Bank of England (BoE) held the Bank Rate at 4.00% in a 7-2 vote split (7 for hold, 2 for cut). The BoE maintained their guidance of a "gradual and careful approach to the further withdrawal of monetary policy restraint remains appropriate". They slowed the pace of quantitative tightening to GBP 70bn annually from GBP 100bn - close to expectations. We think a November rate cut remains alive, although 22 October CPI data will be crucial. See more in our Bank of England Review - Near term rate cuts remain an option, 18 September.

In Germany, the Bundestag approved the government's delayed 2025 budget. The government has a majority so it was expected, but some members could have diverged from the party line, as seen previously when Merz was sworn in as Chancellor. The approval shows that the government is working together and pushing through the planned draft budgets, with the new 2026 budget also likely to be passed.

Equities: Equities rose yesterday as markets digested the Fed's dovish stance. Interestingly, gains occurred alongside rising yields - a notable shift from the pattern seen since summer, when lower yields had primarily fuelled US growth stocks. This dynamic aligns with the "run it hot" narrative we discussed yesterday. Small caps stood out, in particular with the Russell 2000 gaining 2.5% compared to 0.5% for the S&P 500 and 0.8% for the Stoxx 600. The rally in small caps finally pushed the index above its previous record close from 2021.

That said, this was far from a broad-based rally. Sector dispersion was significant, with strength concentrated in technology and industrials. Semiconductor stocks were especially strong, supported by news of Nvidia taking a stake in Intel and an upbeat earnings report and guidance from Renishaw. Futures are slightly higher this morning while tech-heavy Asian markets are taking a breather after the 10% rise (Shenzhen, Kospi) the last month.

FI and FX: Global yield curve bear steepened yesterday, with European government bonds leading the way whereas moves were more contained in US treasuries. The global FX market radiated a rather calm, post-FOMC vibe with light flows and mostly contained volatility. The USD continued to strengthen broadly, with EUR/USD breaking below 1.18. Norges Bank combined their rate cut with a hawkish adjustment of the forward-looking rate path, but although NOK-EUR spreads widened significantly we saw EUR/NOK edging higher, emphasizing the importance of the global investment environment when trading the NOK. The Norges Bank cut had seemingly no spillover to market pricing on the Riksbank next week, but we did see Swedish government bonds and the SEK both underperform peers. Overnight, Bank of Japan kept the key rate steady at 0.50% and USD/JPY is currently sitting at 147.50.