Sample Category Title

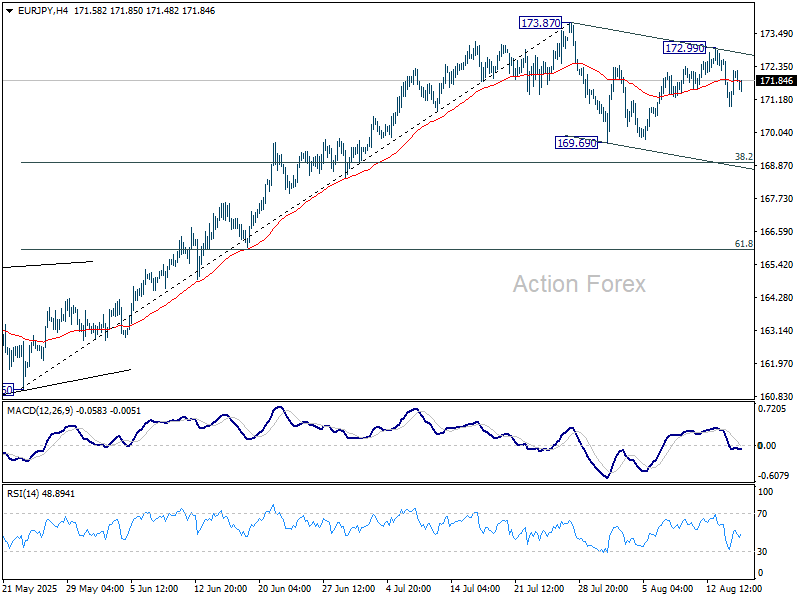

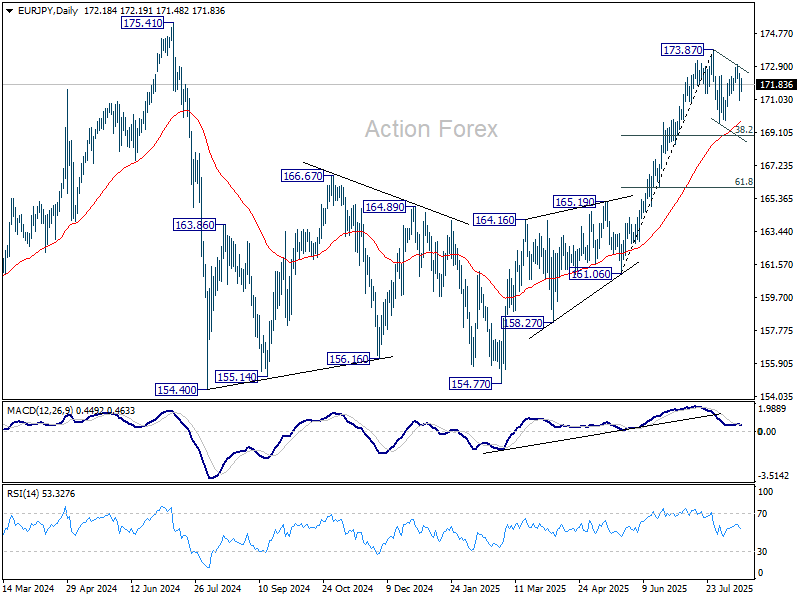

EUR/JPY Daily Outlook

Daily Pivots: (S1) 171.17; (P) 171.91; (R1) 172.85; More...

Intraday bias in EUR/JPY is turned neutral first with current recovery. Overall, corrective pattern from 173.87 is extending and deeper fall might be seen. But downside should be contained by 38.2% retracement of 161.06 to 173.87 at 168.97 to complete the pattern. On the upside, above 172.99 will bring retest of 173.87.

In the bigger picture, considering current strong momentum as seen in the rally from 154.77, corrective pattern from 175.41 could have already completed. Decisive break of 154.77 will confirm long term up trend resumption. Next target is 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. However, rejection by 175.41, followed by firm break of 55 D EMA (now at 169.64) will delay this bullish case.

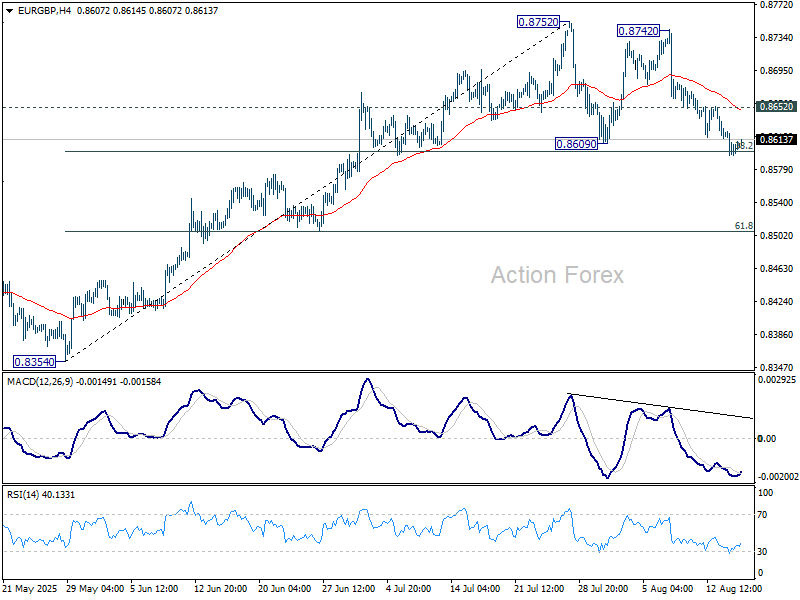

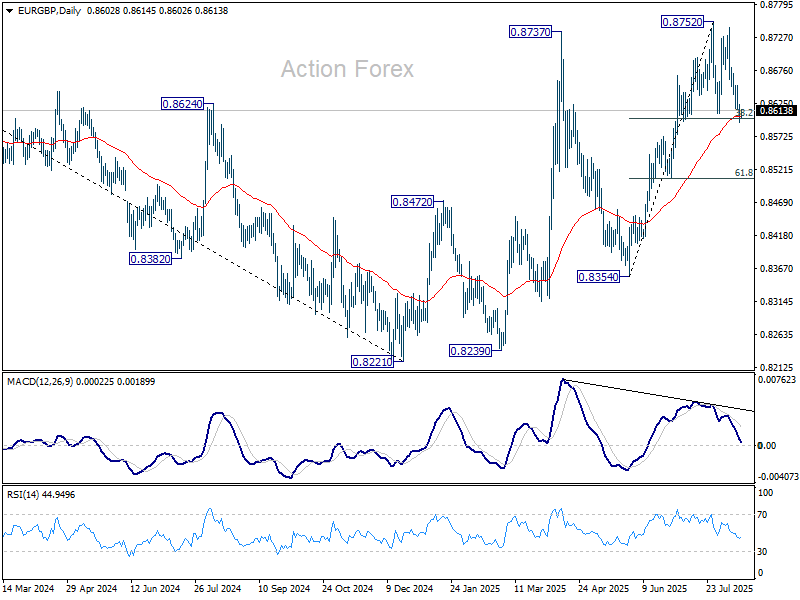

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8594; (P) 0.8612; (R1) 0.8627; More...

Focus stays on 38.2% retracement of 0.8354 to 0.8752 at 0.8600 in EUR/GBP. Sustained break there indicate near term bearish reversal and target 61.8% retracement at 0.8506. Strong rebound from current level will maintain bullishness for another rise through 0.8752 at a later stage.

In the bigger picture, the structure from 0.8221 medium term bottom are not impulsive enough to suggest that it's reversing the down trend from 0.9267 (2022 high). But even if it's a correction, further rise is expected to 61.8% retracement of 0.9267 to 0.8221 at 0.8867. This will remain the favored case as long as 55 W EMA (now at 0.8497) holds.

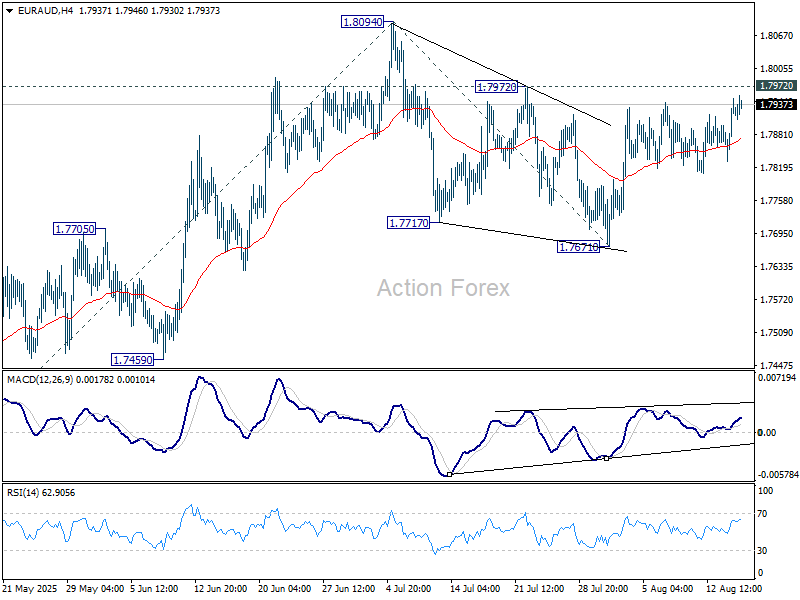

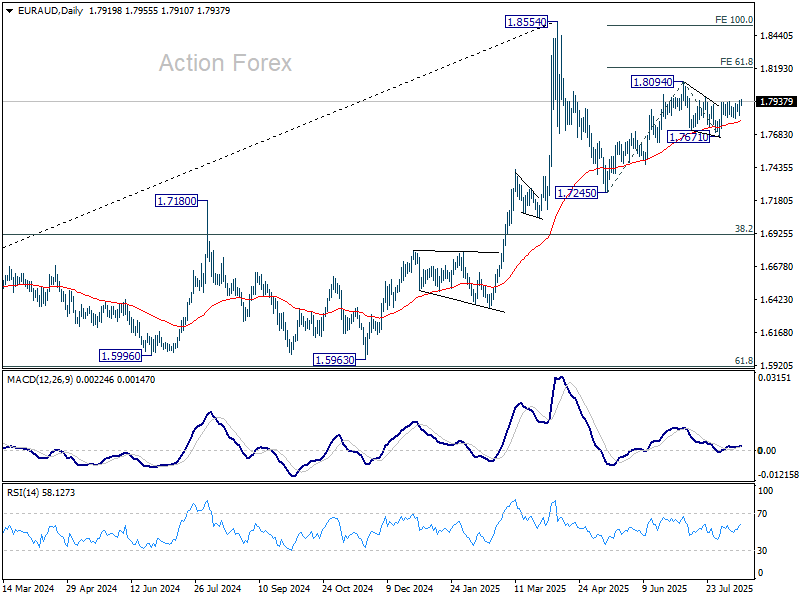

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7860; (P) 1.7905; (R1) 1.7977; More...

EUR/AUD recovers mildly today but stays below 1.7972 resistance, and intraday bias stays neutral. Decisive break of 1.7972 should confirm that corrective pattern from 1.8094 has completed at 1.7671. Further rise should then be seen through 1.8094, to resume the rebound from 1.7245. Next target is 61.8% projection of 1.7245 to 1.8094 from 1.7671 at 1.8196. On the downside, below 1.7671 will bring deeper fall back to 1.7459 support instead.

In the bigger picture, price actions from 1.8554 medium term top are seen as a corrective pattern. Such pattern could extend further with another falling leg. But even in that case, downside should be contained by 38.2% retracement of 1.4281 (2022 low) to 1.8554 at 1.6922 to bring rebound. Uptrend from 1.4281 is expected to resume at a later stage.

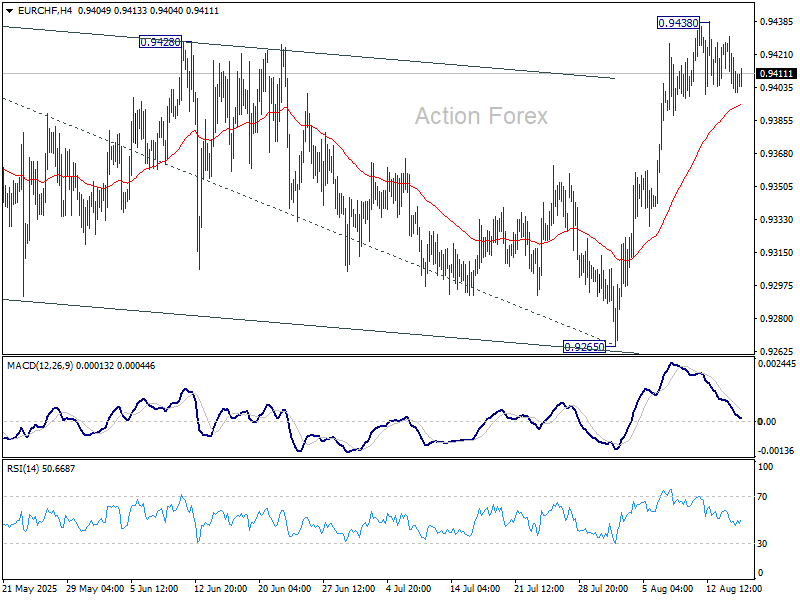

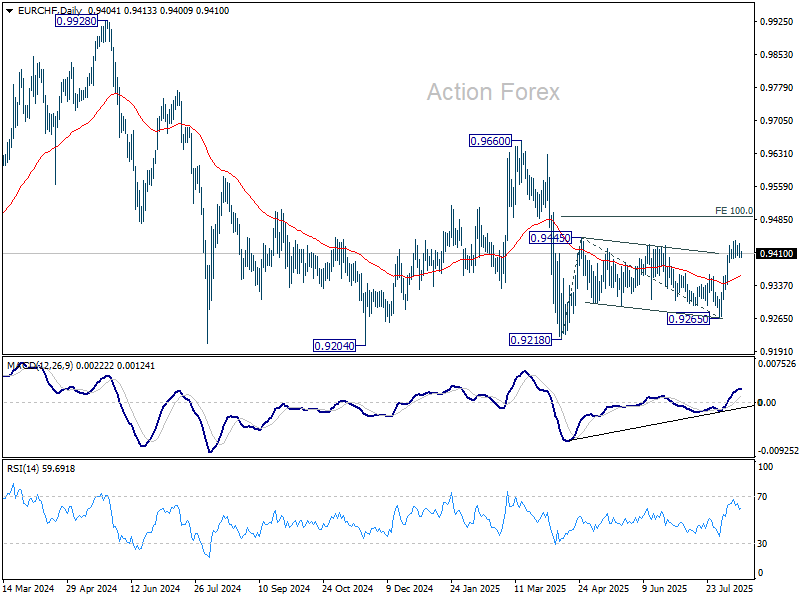

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9397; (P) 0.9414; (R1) 0.9425; More....

EUR/CHF is staying in consolidations below 0.9438 temporary top and intraday bias remains neutral first. On the upside, decisive break of 0.9445 resistance will resume the whole rebound from 0.9218. Next target is 100% projection of 0.9218 to 0.9445 from 0.9265 at 0.9492. However, sustained trading below 55 4H EMA (now at 0.9394) will extend the corrective pattern from 0.9445 with another falling leg.

In the bigger picture, the down trend from 0.9204 (2018 high) might still be in progress considering that EUR/CHF is staying well inside the long term falling channel. However, with bullish convergence condition in W MACD, downside position should be limited in case of another fall. Instead, firm break of 0.9660 resistance will be an important sign of medium term bullish trend reversal.

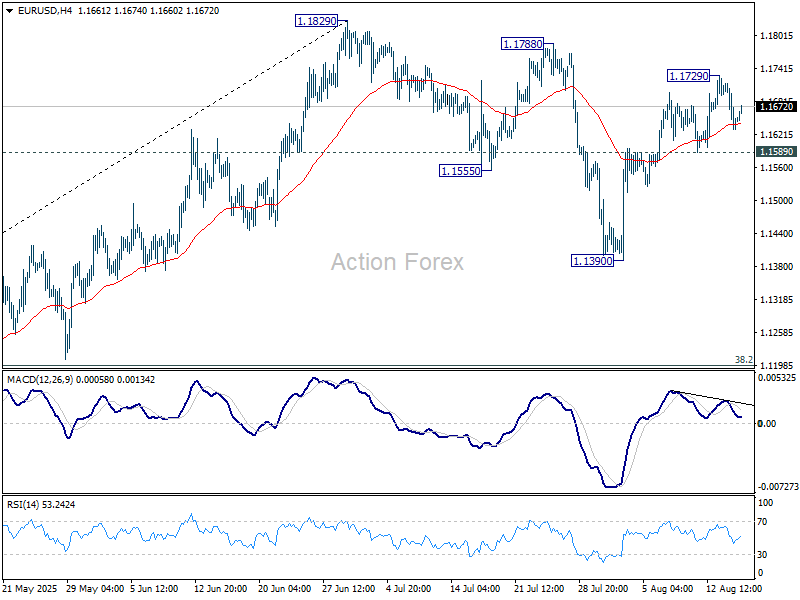

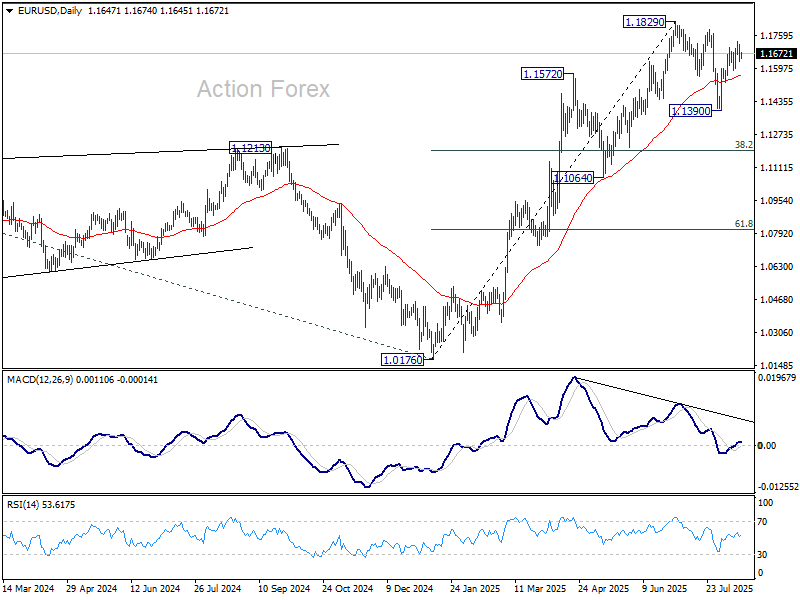

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1615; (P) 1.1665; (R1) 1.1700; More...

Intraday bias in EUR/USD remains neutral and more consolidations could be seen below 1.1729 temporary top. Further rise is expected as long as 1.1589 support holds. Above 1.1729 will target a retest on 1.1829 high. Firm break there will resume larger up trend to 1.1916 projection level. On the downside, however, break of 1.1589 support will delay the bullish case and extend the corrective pattern from 1.1829 with another falling leg.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will remain the favored case as long as 1.1604 support holds.

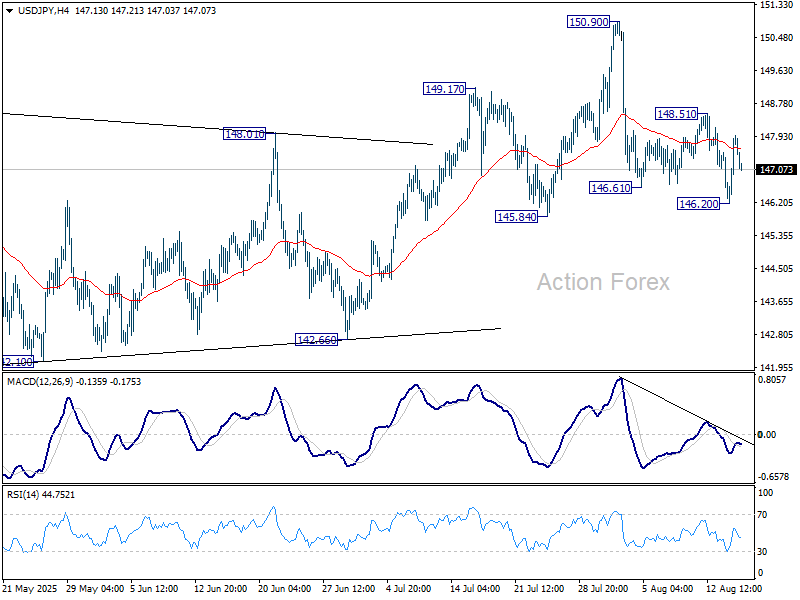

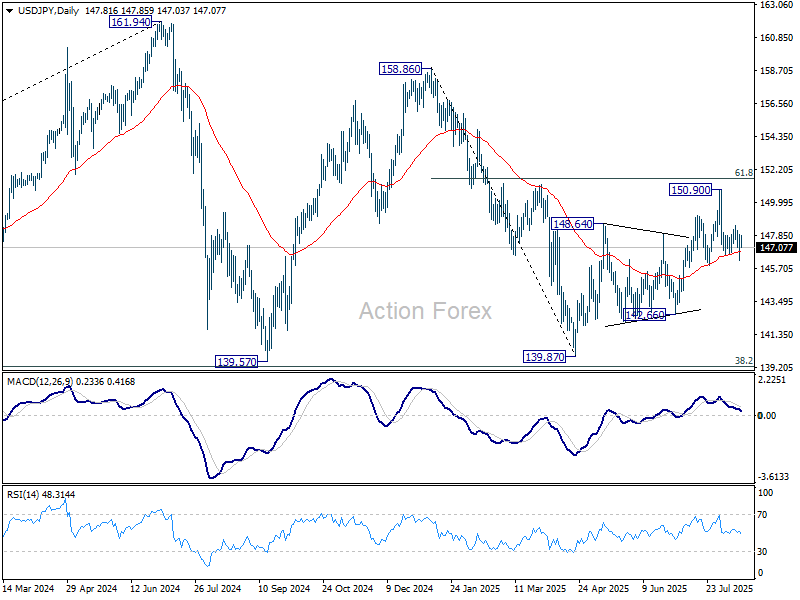

USD/JPY Daily Outlook

Daily Pivots: (S1) 146.66; (P) 147.31; (R1) 148.40; More...

Intraday bias in USD/JPY stays neutral for the moment. Further decline is mildly in favor as long as 148.51 resistance holds. On the downside, firm break of 146.85 support will suggest that whole rebound from 139.87 has completed at 150.90, and turn outlook bearish. Next target is 142.66 support. On the upside, above 148.51 will bring retest of 150.90 instead.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 will argue that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. In case the corrective pattern extends with another fall, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.

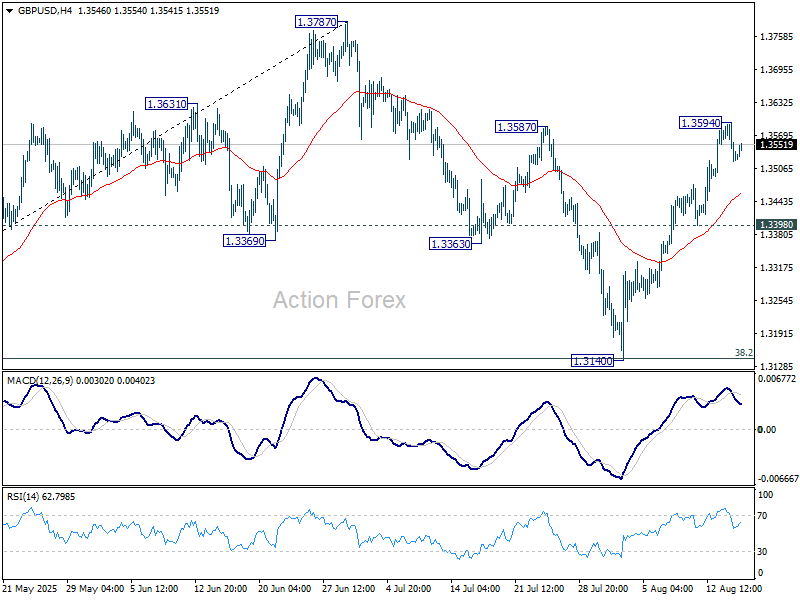

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3502; (P) 1.3549; (R1) 1.3576; More...

Intraday bias in GBP/USD remains neutral for consolidations below 1.3594 temporary top. Further rally is expected as long as 1.3398 support holds. Above 1.3594 will extend the rise from 1.3140 to retest 1.3787 high.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.3068) holds, even in case of deep pullback.

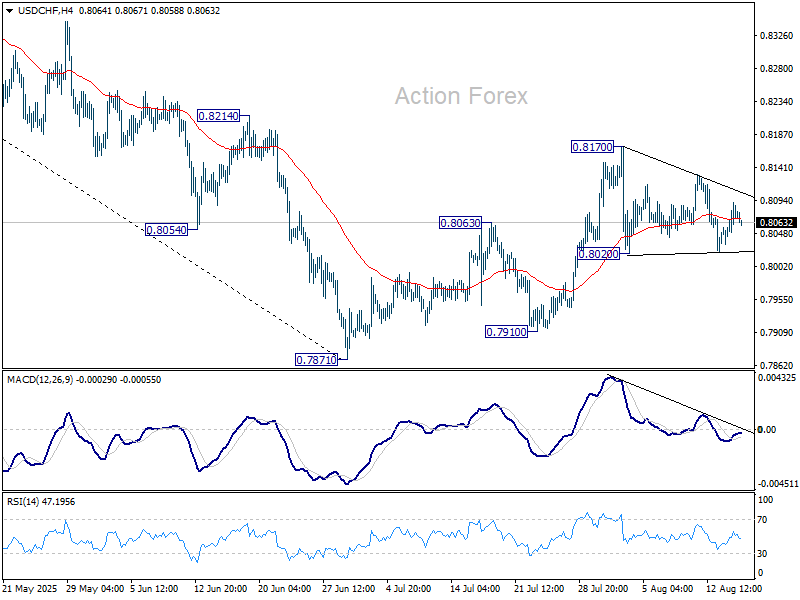

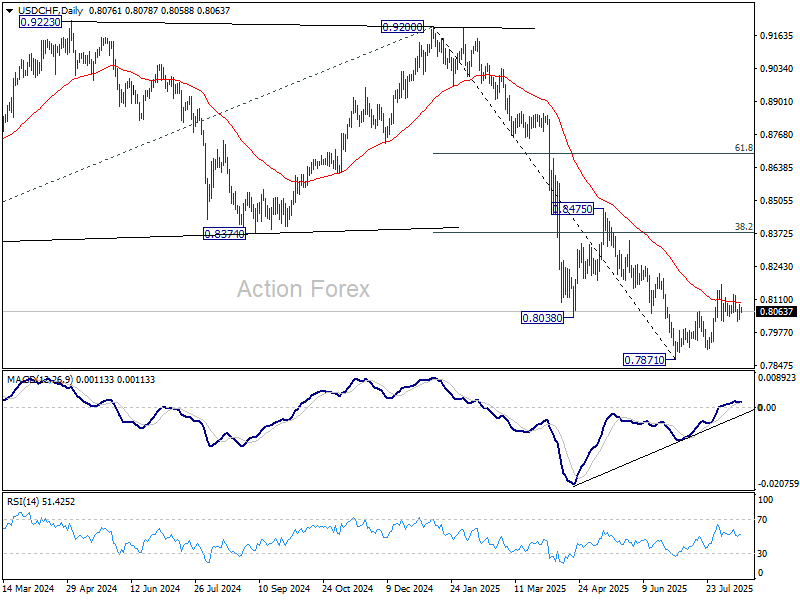

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8044; (P) 0.8069; (R1) 0.8099; More….

Intraday bias in USD/CHF remains neutral for the moment. On the downside, break of 0.8020 will revive that case that the corrective pattern from 0.7871 has completed, and target a retest on 0.7871 low. On the upside, firm break of 0.8710 will resume the corrective from 0.7871. Intraday bias will be back on the upside for 38.2% retracement of 0.9200 to 0.7871 at 0.8379.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8475 resistance holds.

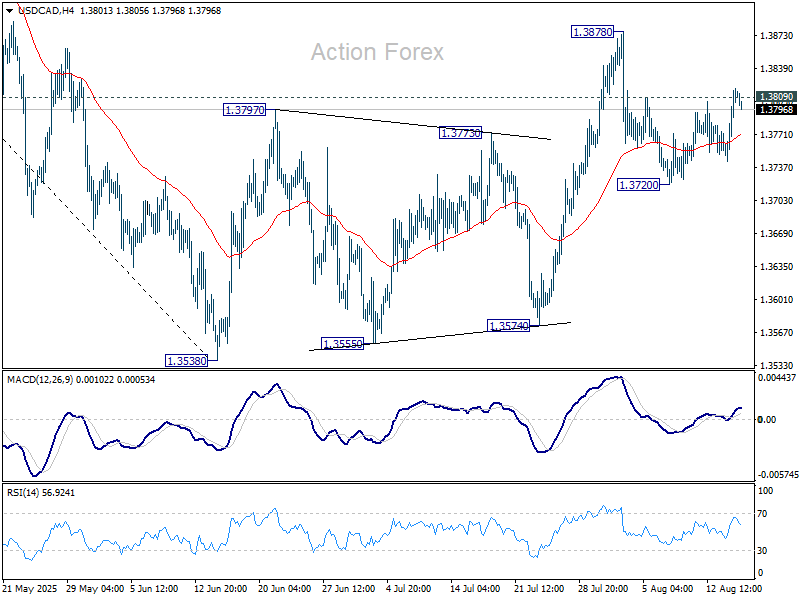

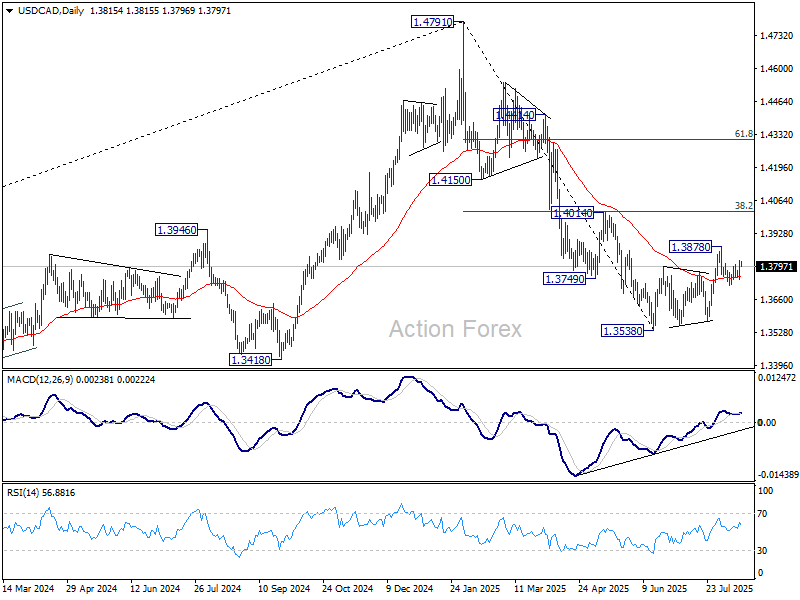

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3768; (P) 1.3795; (R1) 1.3844; More...

USD/CAD breached 1.3809 resistance but failed to sustain above there. Intraday bias stays neutral first. Firm break of 13809 will bring retest of 1.3878. Further break there will extend the corrective rebound from 1.3538 with another rising leg. On the downside, break of 1.3720 will reaffirm the case that corrective pattern from 1.3538 has completed at 1.3878. Further decline should then be seen back to retest 1.3538 low.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 resistance holds. Next target is 61.8% retracement of 1.2005 (2021 low) to 1.4791 at 1.3069.

A Bad ‘Good Idea’

The Fed doves hit a wall yesterday after US PPI data came in far hotter than analysts pencilled in, raising doubts that consumer prices will remain immune to tariff effects and that the Federal Reserve (Fed) can fully deliver the cuts the government wants. Headline PPI jumped from 2.4% to 3.3% (vs. 2.5% expected) while core inflation surged from 2.6% to 3.7% (vs. 2.9% expected) — the biggest leap in three years. The surprise leaves the Fed doves rattled.

This week’s CPI and PPI prints suggest companies have mostly swallowed the tariff costs so far, but that could change, with higher prices soon passed on to consumers. In normal times, such numbers would make a rate cut highly unlikely — let alone a jumbo cut that risks stoking inflation and eroding the Fed’s future policy room. But these are not normal times. The White House pressure is mounting, and the September rate cut looks inevitable — come hell or high water. Markets now see a 93% probability of a 25bp cut in September. A 50bp cut, despite political noise, is hopefully off the table. I believe that 25bp cut will be the only one this year. The US 2-year yield jumped on the data, the dollar rebounded but still hovers near its 50-DMA, while the S&P 500 inexplicably shrugged off worries. Firms are absorbing tariffs — for now — but that will likely bite into margins when earnings season arrives.

In the corporate spotlight, Intel jumped 7% yesterday after the US government said that they could build a stake in the once-iconic US company. But this time last week, Trump was calling for the resignation of the company’s new CEO, Lip-Bu Tan, for having a track record for investing in China. The two men than met at the White House and now, all is well. If we put the pieces together, the US government will get a 15% cut from Nvidia and AMD, and invest in Intel – which was originally not willing to expand production plans before confirmation from clients. While the Ohio plant would be the biggest chip factory in the world, churning out chips clients don’t want isn’t exactly a solid foundation for capital markets. In short, Trump looks ready to play Santa for America’s chip industry… but mixing up the pieces on this board could be a game that spooks investors.

Across the Atlantic, UK GDP surprised to the upside, easing pressure on Chancellor Rachel Reeves but complicating the Bank of England’s (BoE) November decision. Growth is slowing, but not alarmingly; inflation is rising, strengthening the case against another cut. Still, tight fiscal policy and possible tax hikes in the Autumn Budget could weigh on growth — though the BoE can’t act on speculation. Cable touched 1.36 before easing on a firmer dollar, while the EURGBP slipped below its 50-DMA on stronger-than-expected UK and softer-than-expected European growth data. The eurozone expanded just 0.1% in Q2, with weak industrial output and employment holding European Central Bank (ECB) doves in check. The EURUSD remains supported near its 50-DMA, its direction still driven more by US dollar moves than by the euro itself. Rising US inflation concerns should temper dovish Fed bets, but with the US economy slowing, the greenback’s broader downtrend is unlikely to reverse.

Elsewhere, Japan’s GDP beat forecasts, while Chinese industrial production, investment, and retail sales all disappointed.

In energy, US crude consolidates after a nearly 2% bounce on Thursday on geopolitical jitters. Trump warned of ‘severe consequences’ — including sanctions — if Ukraine peace talks stall, raising the risk of tensions with Russia. The upcoming meeting looks more likely to sour than succeed, with oil flows potentially caught in the crossfire. US crude recently breached the $65 support and is consolidating in a medium-term bearish zone, where ample supply and cloudy demand argue for further downside — though a softer dollar is cushioning the slide.