Sample Category Title

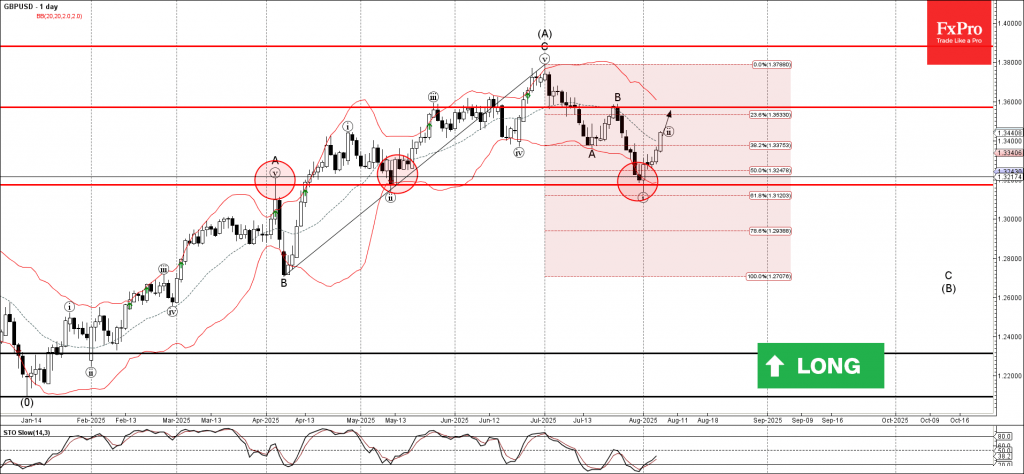

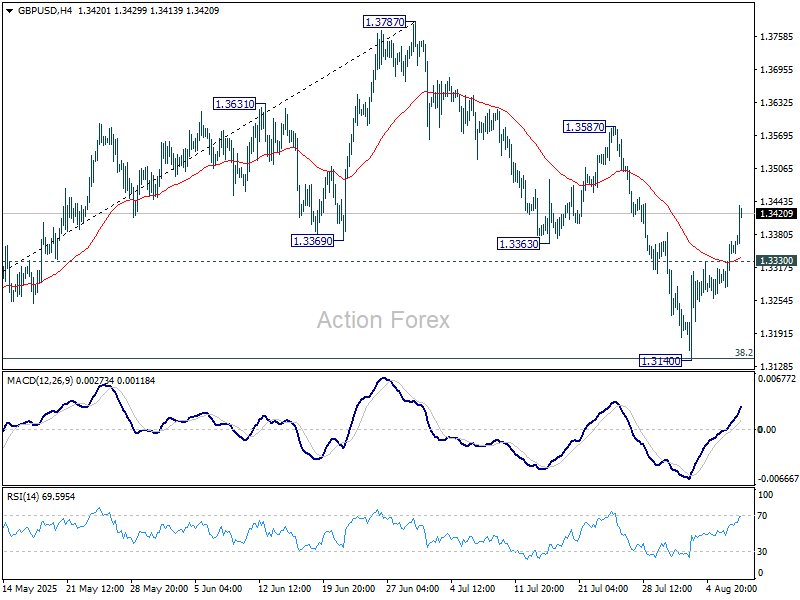

GBPUSD Wave Analysis

GBPUSD: ⬆️ Buy

- GBPUSD reversed from the support area

- Likely to rise to resistance level 1.3600

GBPUSD currency pair recently reversed from the support area between the strong support level of 1.3175 (former resistance from April) and the lower daily Bollinger Band.

This support area was further strengthened by the 61.8% Fibonacci correction of the upward impulse from April.

Given the clear daily uptrend, GBPUSD currency pair can be expected to rise to the next resistance level 1.3600 (which stopped wave B in July).

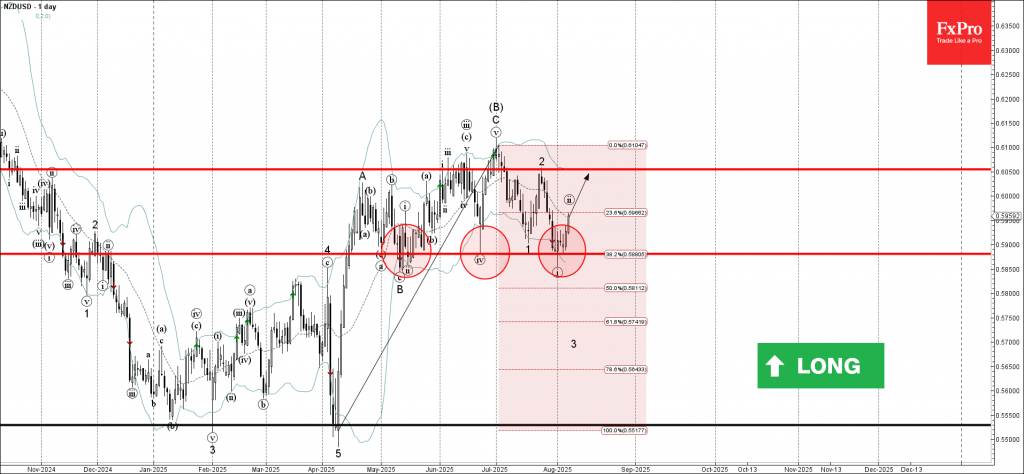

NZDUSD Wave Analysis

NZDUSD: ⬆️ Buy

- NZDUSD reversed from the support area

- Likely to test resistance level 0.6050

NZDUSD currency pair recently reversed from the support area between the strong support level of 0.5880 (which has been reversing the price from May) and the lower daily Bollinger Band.

The upward reversal from this support area created a clear daily Japanese candlestick reversal pattern, the Hammer, which initiated active correction ii.

Given the strongly bearish US dollar sentiment seen today, NZDUSD currency pair can be expected to rise to the next resistance level 0.6050 (top of wave 2 from July).

Bank of England Review – A 25bp Cut With a Hawkish Twist

- The Bank of England cut the Bank Rate by 25bp to 4.00% as widely expected.

- The vote split was more hawkish than expected, with four members voting for an unchanged decision.

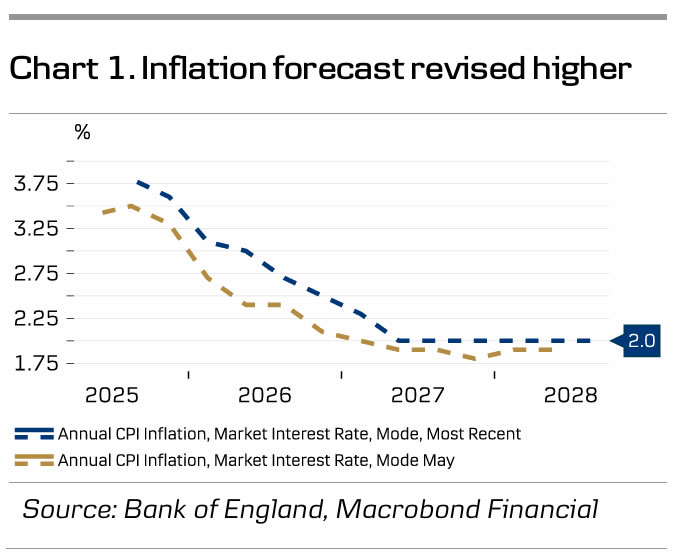

- The guidance included a hawkish twist and forecasts for inflation were revised significantly higher.

- The market reacted by trading Gilt yields a bit higher and sending EUR/GBP below the 0.87 mark.

The Bank of England (BoE) cut the Bank Rate to 4.00% as widely expected. The vote split delivered a hawkish surprise, with five members voting for a cut and four members voting for an unchanged decision. Alan Taylor favoured a larger 50bp cut but joined the 25bp camp to secure a majority for a cut. Thus, the balance of the MPC was indeed skewed towards cutting the Bank Rate.

The overall guidance was unchanged, as the BoE noted that "a gradual and careful approach to the further withdrawal of monetary policy restraint remains appropriate". However, a hawkish twist was added to the wording, as they also note that the monetary policy stance has become less restrictive and future cuts will depend on the perspectives for further disinflation. To us, this indicates that the cutting cycle is nearing its end. Additionally, the MPC revised its inflation forecast significantly higher in the new monetary policy report (MPR). with Q4 inflation forecasts now at 3.8, 2.7 and 2% for years 2025, 2026 and 2027 vs. 3.5, 2.4 and 1.9% back in May (see chart 1). GDP forecasts were largely unchanged at very modest growth rates.

BoE call. We continue to expect the BoE to deliver the next cut in the Bank Rate in November, followed by quarterly rate cuts next year leaving the Bank Rate at 2.75% by end-2026. After today's somewhat hawkish surprise, we think the risk is that the cutting cycle will come to an end earlier than previously thought, which is also what markets price. That said, recent increasingly negative employment growth and lower wage growth suggest further cuts will be necessary.

Market reaction. Gilt yields traded a couple of basis points higher and EUR/GBP dropped below the 0.87 mark on the hawkish twist, particularly in the short-end as markets now price 20bp for the remainder of the year against 25bp ahead of the meeting. We expect EUR/GBP to move higher towards 0.89 on a 6-12-month horizon on a weakening of the UK growth outlook and a positive correlation to a USD negative environment.

US Dollar Tries to Find Stable Ground

Since last Friday's Non-Farm Payrolls number, the Greenback has been getting obliterated, retreating from the 100.00 landmark in the DXY to touching high 97.00 levels.

Markets are quickly moving towards a heavy pricing of FED cuts which is hurting the Dollar and supporting strongly Equities in their ongoing rebound.

It will be essential to see how US indices open today but the trading has been green for other global indices, particularly the DAX up 1.70% on the session, and the Nasdaq (CFD and Futures) is about 200 points from its all-time highs.

In the meantime, the US Dollar follows through with another beginning of NA session where it lags other majors and even bringing back USDCAD back into its past months' range, despite an also underperforming Loonie (which you can check out right here)

To continue yesterday's Mid-Week analysis, we'll review the Dollar Index in detail and a few pairs.

Will the USD downfall continue?

Dollar Index Multi-Timeframe Analysis

Dollar Index Daily Chart

US Dollar Index Daily Chart, August 7, 2025 – Source: TradingView

The outlook for the US Dollar is neither bullish or bearish looking at the daily chart.

The swift End-July rebound could have brought the greenback towards a more tenace Bull outlook but the strong NFP retracement corrected that thesis.

This is another proof of how stong psychological levels (100.00 Level resistance) can be – despite them overshooting slightly on some occasions – and how influential data like Non-Farm Payrolls can be.

The Daily RSI flattening at the middle line indicates higher probability of rangebound action for Major FX pairs as Markets await for more key data.

The Dollar is trading right at its 50-Day MA so watch where Markets take the index from here.

Dollar Index 4H Chart

US Dollar Index 4H Chart, August 7, 2025 – Source: TradingView

Looking closer, we see that the overnight selloff in the Dollar has found support at just below the 98.00 handle, just below its support zone (overnight lows: 97.45).

The swift retreat downwards found supporting buyers at the 4H MA 200 which will be a key mark to follow for upcoming trading.

After this morning's Bank of England Cut, markets may be realizing that the US Main rates are still high (currently 4.50%) which could lead to some consolidation in the Index int he waiting of further data.

Levels to watch for the Index:

Support Levels:

- 98.00 Pivot turned Support

- 4H MA 200 97.60

- Last Main low Pivot 97.15

Resistance Levels:

- 98.50 Intermediate Pivot Zone

- Resistance turned Pivot 99.20 to 99.40

- 100.00 to 101.00 Main Resistance

Dollar Index intraday – 30m Chart

US Dollar Index 30m Chart, August 7, 2025 – Source: TradingView

For immediate Bull/Bear strength analysis, watch the overnight lows (97.95) and the current swing highs (98.30) – If markets close above on strong candles, expect continuation.

If the DXY gets choppy from here, look at individual pairs which may offer decent rangebound setups.

Safe Trades!

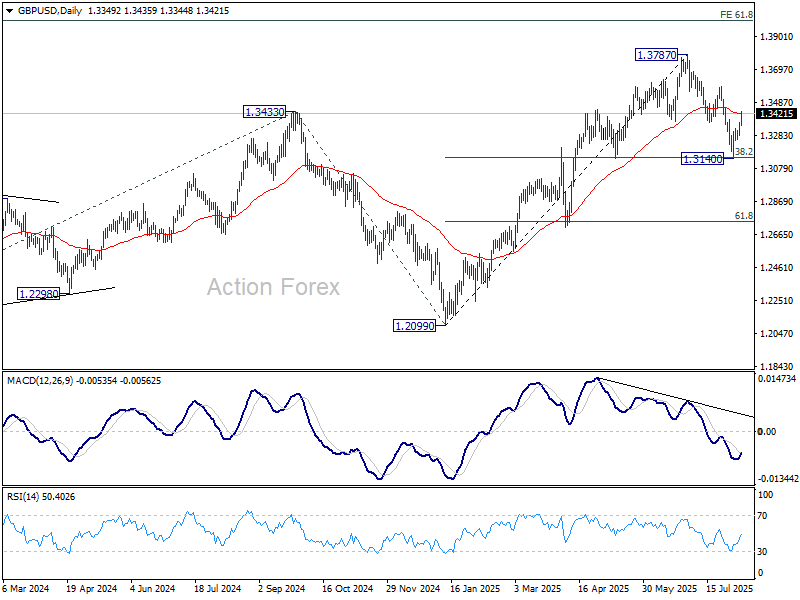

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3303; (P) 1.3336; (R1) 1.3389; More...

GBP/USD's rebound from 1.3140 continues today and intraday bias stays on the upside. As noted before, correction from 1.3787 should have completed with three waves down to 1.3140. Further rise should be seen to 1.3587 resistance. Firm break there will target 1.3787 high. On the downside, below 1.3330 minor support will turn intraday bias neutral again first.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.3049) holds, even in case of deep pullback.

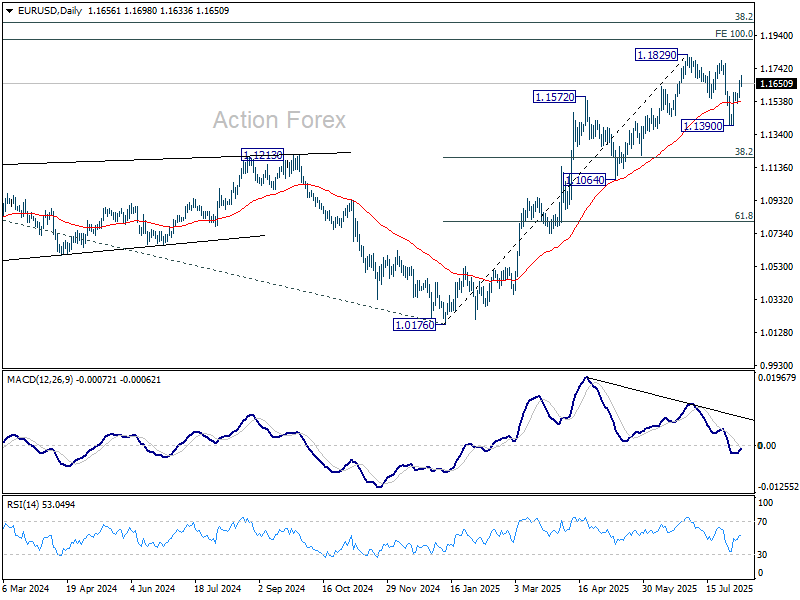

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1593; (P) 1.1631; (R1) 1.1697; More...

Intraday bias in EUR/USD stays on the upside at this point. As noted before, correction from 1.1829 should have completed with three waves down to 1.1390. Further rally should be seen to retest 1.1788/1820 resistance zone. On the downside, however, break of 1.1526 minor support will dampen this view and bring retest of 1.1390 instead.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will remain the favored case as long as 1.1604 support holds.

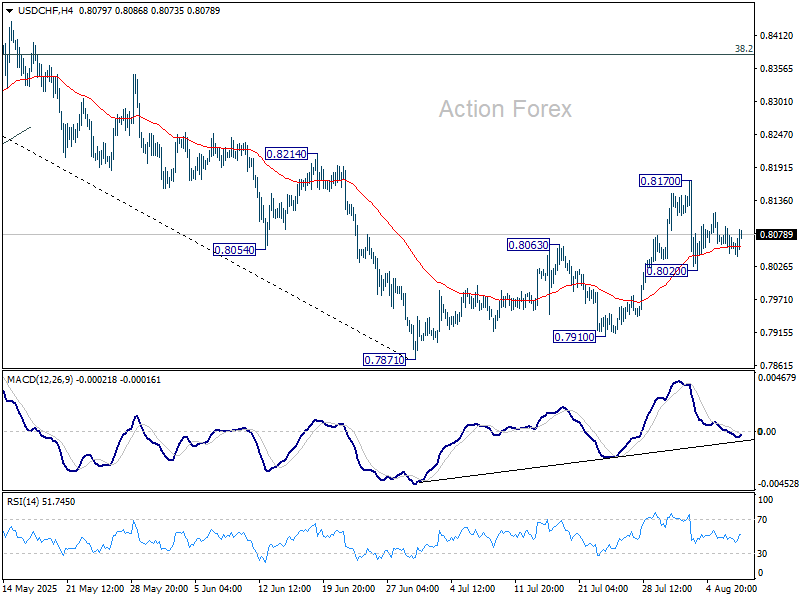

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8044; (P) 0.8069; (R1) 0.8089; More….

No change in USD/CHF's outlook and intraday bias remains neutral. On the downside, below 0.8020 will affirm that case that corrective bounce from 0.7871 has completed at 0.8170. Bias will be back on the downside for 07871/7910 support zone. On the upside, though, break of 0.8170 will resume the rise from 0.7871 to 38.2% retracement of 0.9200 to 0.7871 at 0.8379 instead.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8475 resistance holds.

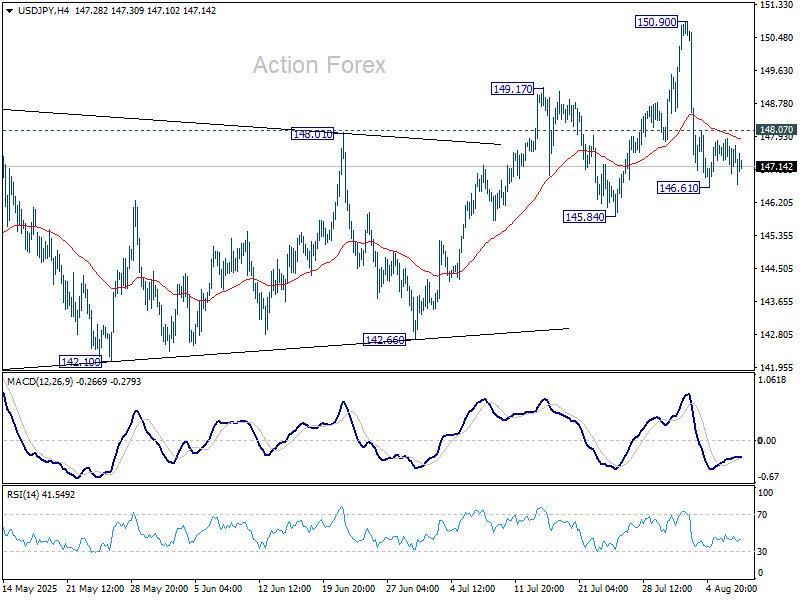

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 146.93; (P) 147.41; (R1) 147.83; More...

Intraday bias in USD/JPY stays neutral as range trading continues. As long as 145.84 support holds, larger rebound from 139.87 is still in favor to continue. On the upside, above 148.07 minor resistance will bring stronger rebound back to retest 150.90. However, on the downside, firm break of 145.84 support will argue that whole rise from 139.87 might have already completed. Deeper fall should then be seen to 142.66 support for confirmation.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 will argue that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. In case the corrective pattern extends with another fall, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.

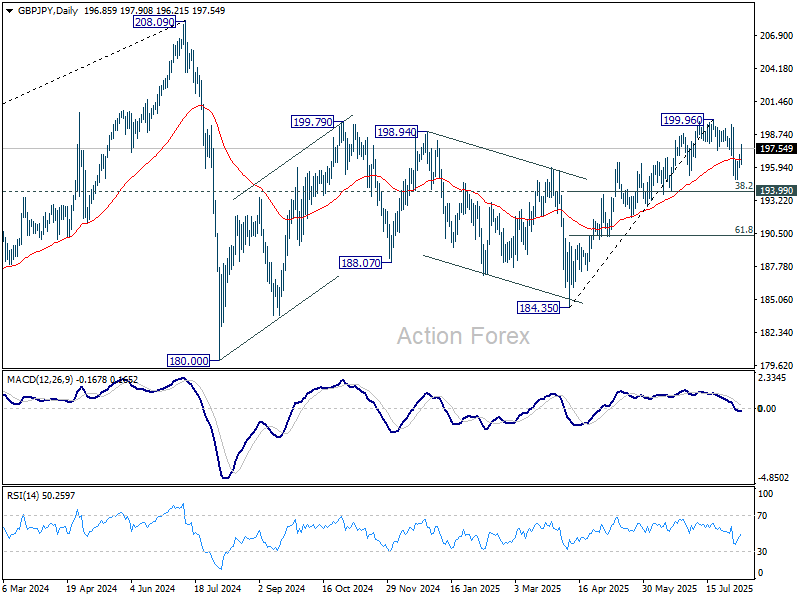

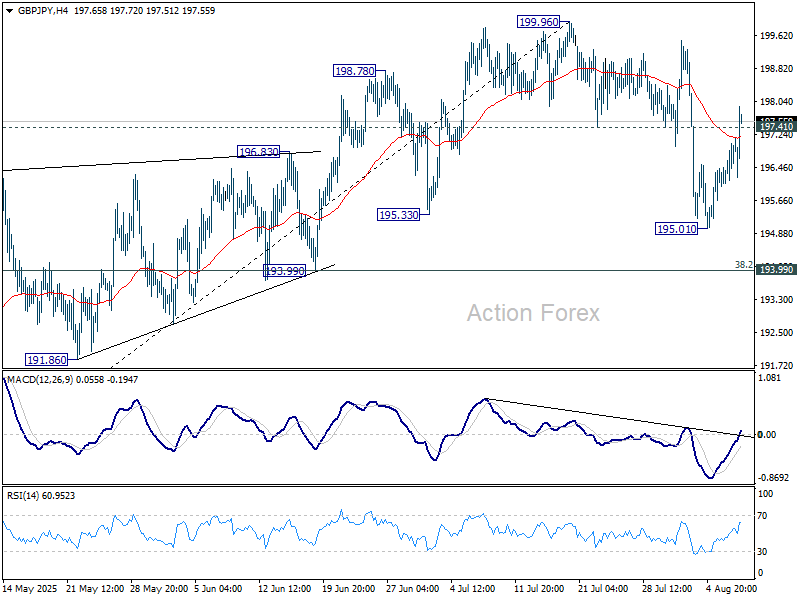

GBP/JPY Mid-Day Outlook

Daily Pivots: (S1) 196.25; (P) 196.67; (R1) 197.25; More...

GBP/JPY's break of 197.41 support turned resistance suggests that corrective pullback from 199.96 has already completed at 195.01. Intraday bias in back on the upside for retesting 199.96 high. Firm break there will resume the rally from 184.35. In case of another fall, strong support is expected from 193.99 cluster support (38.2% retracement of 184.35 to 199.96 at 193.99) to bring rebound.

In the bigger picture, price actions from 208.09 (2024 high) are seen as a correction to rally from 123.94 (2020 low). The pattern might still extend with another falling leg. But in that case, strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. Meanwhile, decisive break of 208.09 will confirm long term up trend resumption.