Sample Category Title

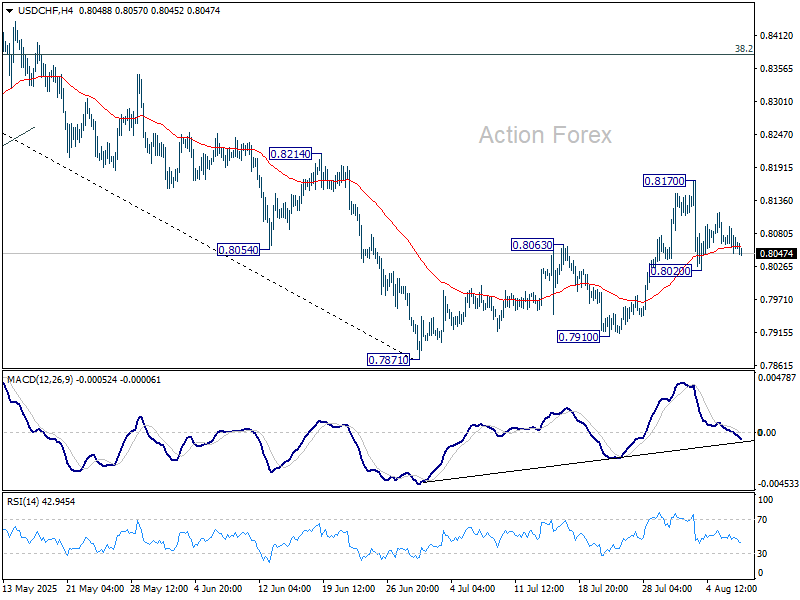

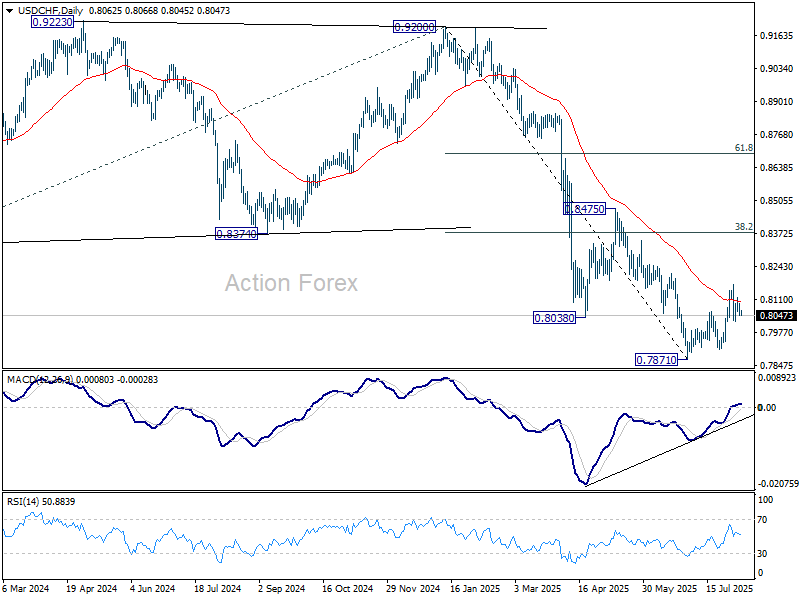

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8044; (P) 0.8069; (R1) 0.8089; More….

Intraday bias in USD/CHF remains neutral and outlook is unchanged. On the downside, below 0.8020 will affirm that case that corrective bounce from 0.7871 has completed at 0.8170. Bias will be back on the downside for 07871/7910 support zone. On the upside, though, break of 0.8170 will resume the rise from 0.7871 to 38.2% retracement of 0.9200 to 0.7871 at 0.8379 instead.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8475 resistance holds.

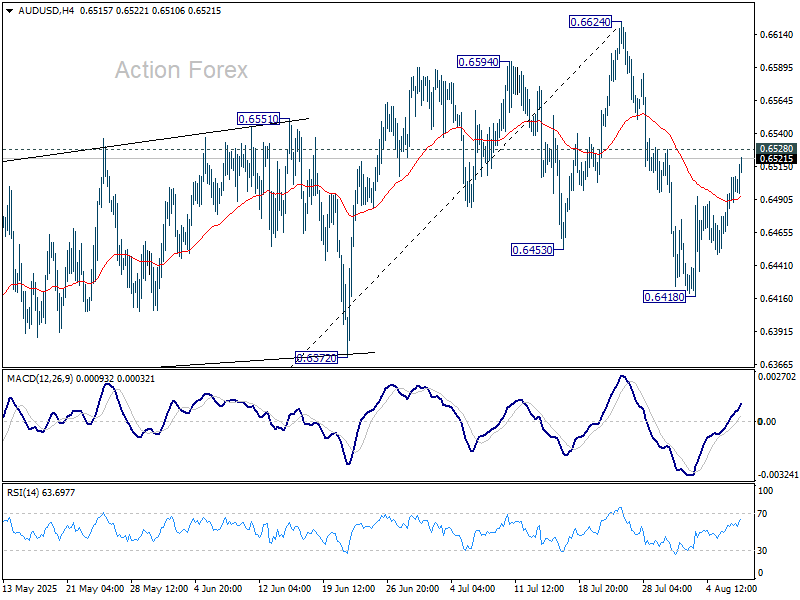

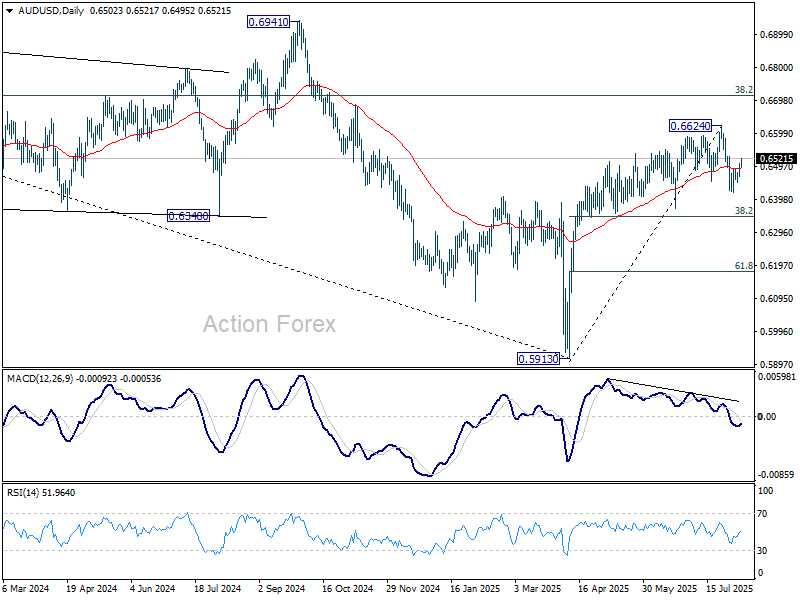

AUD/USD Daily Report

Daily Pivots: (S1) 0.6474; (P) 0.6491; (R1) 0.6521; More...

AUD/USD is still staying below 0.6528 resistance and intraday bias remains neutral. On the upside, firm break of 0.6528 will indicate that corrective pullback from 0.6624 has completed at 0.6418. Intraday bias will be back on the upside for retesting 0.6624. On the downside, break of 0.6418 will resume the fall to 38.2% retracement of 0.5913 to 0.6624 at 0.6352.

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. While stronger rally cannot be ruled out, outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, even in case of another fall through 0.5913, downside should be contained above 0.5506 (2020 low).

The Trump Order

Mr. Trump continues to shape the world to his taste: he has doubled tariffs on Indian imports to 50% because he doesn’t want them to buy oil from Russia. Mr. Rubio, from his negotiation team, gently met with the Swiss delegation — and when I say delegation, I mean two Federal Councillors, including the President herself — to leave the tariffs unchanged at 39%. But hey, the meeting was nice and open to further talks.

Further talks, however, won’t ease worries about the 150–250% tariffs that Trump wants to impose on pharmaceutical imports, and both India and Switzerland are highly concerned. Looking at the car industry — another big victim of the Trump administration — tariffs eventually settled at more reasonable levels, so the hope here is that the same will happen with drugmakers. But of course, because one man decides everything as he wishes — and no one can stop him — uncertainty and lack of visibility will remain on the menu for years to come.

Then, Apple agreed to invest an extra $100bn in US production facilities to please Mr. Trump and ease his rage — because he doesn’t want iPhones produced in China... nor in India! This brings Apple’s total investment promise to a whopping $600bn. Apple shares reacted to the news with a 5% rebound yesterday, showing investors were more relieved to see Tim Cook stay friends with the White House than worried about the company’s margins being smashed by the inevitably higher cost of producing iPhones in the US — note that labour and assembly costs for an iPhone would be at least 10 times higher on US soil.

So, what will probably happen — and I think this is the catch — is that Apple will invest hundreds of billions into US factories, and make sure they are highly automated to require ever less labour. That’s great for AI enablers, of course, but maybe not so great for jobs, which are already taking a hit from the combined impact of AI and trade chaos.

Speaking of AI, the US remains a few years ahead of its closest rival — China — and AI remains one safe space for investors, as Jensen Huang managed to woo the White House over chip exports to China. Jensen says that if the US stops exporting chips to China — and they’re not even exporting the best — the Chinese will just speed up their innovation. Trump has now announced 100% tariffs on chip imports but TSMC, which builds Nvidia chips, will be exempt, because they’re investing in the US. And any other firm investing in the US will also be exempt from the big tariffs. What a world. TSMC just rallied more than 4% to a fresh record high today in Taiwan.

Zooming out to a broader perspective, the US 10-year bond auction saw weak demand yesterday, following a soft 3-year auction the day before. The 10-year yield briefly spiked to 4.28%, but has eased since, while the 2-year yield remains under pressure from rising dovish Federal Reserve (Fed) expectations. The Fed is now expected to deliver its next rate cut as early as September, and with the changes Trump is preparing at the heart of the FOMC, the Fed may be cutting rates despite rising inflation.

And the rising inflation problem is an easy fix — if you just tweak the numbers to make inflation look cooler than it really is. Yet, if investors start believing that US inflation numbers are no longer credible, the $2 trillion TIPS market — Treasuries that track US inflation — could crack. That, in turn, would likely weigh on the US dollar and boost demand for alternative inflation-protection assets like gold, and for some, Bitcoin. Although there’s no statistical evidence that Bitcoin is a good inflation hedge. In fact, the correlation between Bitcoin and US inflation was near flat from 2021 to 2023 — Bitcoin behaves more like a risk asset.

That said, Bitcoin will likely continue to do well alongside tech stocks, regardless of inflation.

Elsewhere, the US dollar is weakening on the back of trade news and dovish Fed expectations. The dollar Index slipped below the 38.2% Fibonacci retracement of its summer rally, marking the end of the summer’s upward trend. It’s pushing below the 50-DMA this morning and could extend losses given the dovish divergence between the Fed and other central banks — where dovishness remains, but is already priced in.

The Bank of England, for example, is expected to announce a 25bp rate cut today, but the vote split will be the major talking point — with rising risks to both inflation and the labour market amid Trump tariffs and Reeve’s tax hikes. Seven out of nine MPC members are expected to vote for a cut, one will likely push for a larger cut, and one is expected to stay put. Another 25bp cut is expected in November, but it will be interesting to see if inflation risks threaten that move.

Any hawkish surprise – that will play around the language about ‘gradual and careful rate cuts’ - could help support cable, which is rising above its 100-DMA this morning on US dollar weakness. But sterling’s weakness is more obvious against the euro, where the EURGBP is pushing toward its highest level since end-2023, driven by the UK’s deteriorating economic outlook and rising inflation risks, with little room for more fiscal support, and likely more tax hikes in a country already struggling with the recent fiscal squeeze.

BoE Expected to Cut Rates to 4.00%

In focus today

Today we get Swedish flash estimates for inflation in July, where we expect that CPIF will rise to 3.17% (RB 2.50%) and that CPIFxE will decline to 3.06% (RB 2.84%). A 'low' core number would support expectations of an H2 rate cut given that real activity data continues to underdeliver. A 'high core number' would fortify the Riksbank's stagflation dilemma, and while it could send rates and the SEK higher it would probably not fully erase expectations of later cuts. Our base case is that the policy rate will not go below 2.0%, although we have argued that the risk is clearly skewed to the downside.

The Bank of England is expected to lower the Bank Rate by 25bp to 4.00%, aligning with market and consensus expectations. Recent data has been a mixed, with labour market showing more pronounced signs of cooling, weaker than expected growth but inflation surprising to the topside. For more on our take see Bank of England Preview - On track with easing, 4 August.

Economic and market news

What happened overnight

In China, July trade data outperformed forecasts, with exports rising 7.2% y/y, surpassing expectations of a 5.4% increase. Imports also surprised, growing 4.1% y/y against expectations of a 1.0% decline. This led to a narrower trade surplus of USD 98bn, down from USD 115bn in June. The export surge was driven by a rush to ship goods ahead of the 12 August US tariff deadline, while stronger imports suggest tentative improvements in domestic demand.

What happened yesterday

In the euro area, retail sales rose by 3.1% y/y in June, surpassing the expected 2.6% y/y, driven by a continued rebound in domestic consumption. Monthly retail trade volume increased by 0.3% m/m, slightly below the expected 0.4%, though this follows upward revisions to previous months' weak figures. The annual growth was primarily supported by a 4.3% rise in non-food product sales and a 4.0% increase in car fuel sales, reflecting the bloc's resilience to trade uncertainty.

Trump announced an additional 25% tariff on Indian imports, raising the total tariff rate to 50%. The announcement followed a meeting between Putin and US's Witkoff, which Russian official described as productive. This move underscores Trump's ongoing efforts to target countries engaged in direct or indirect imports of Russian oil, where he has accused India of financing Russia's war in Ukraine via its oil imports. The additional tariffs are scheduled to take effect on 27 August.

Equities: Equity markets rallied yesterday in a session light on macro headlines but rich on micro developments, including another Trump-related twist that is becoming a near-daily fixture for market participants.

Equities advanced across the board, but what stood out was the relative performance within sectors. Healthcare notably lagged, despite (or rather, because of) the noise surrounding it.

While Novo Nordisk reported results, the broader driver was renewed unease about sector-specific tariffs - particularly given lingering uncertainty around pharma trade between the US and EU, despite the recent broader trade agreement. The moves were not just Europe-specific or earnings-driven. In the US, healthcare was the worst-performing sector on the day. The divergence was particularly striking when comparing healthcare with consumer staples both typically considered defensive. Yesterday alone, healthcare underperformed staples by nearly 3%, a rare daily spread of that magnitude within defensives. Asian markets are trading higher this morning, and the tone remains positive in US and European equity futures.

FI and FX: Yesterday, the US yield curve steepened from the long end as 30Y yield rose some 4bp, while 2Y yields declined 2-3bp. This was driven by a weak 10Y US Treasury auction and that the US will sell USD 25bn in the 30Y segment today.

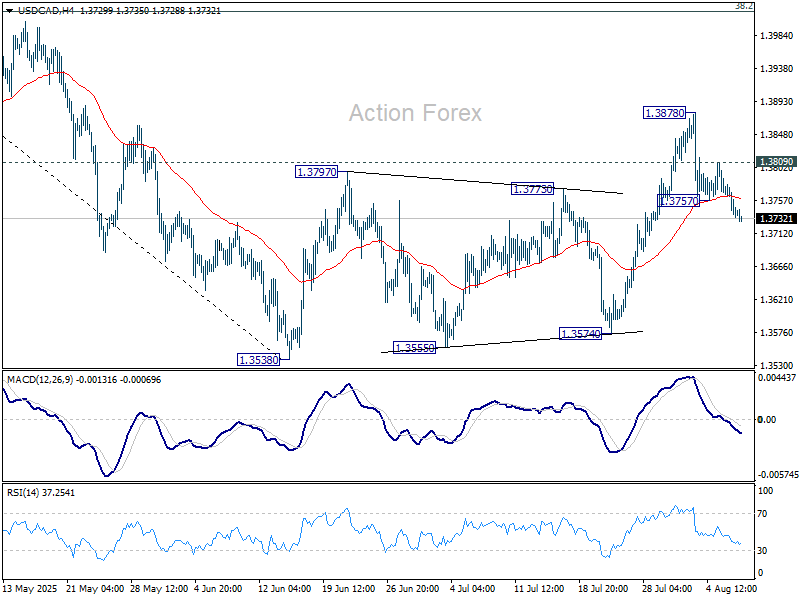

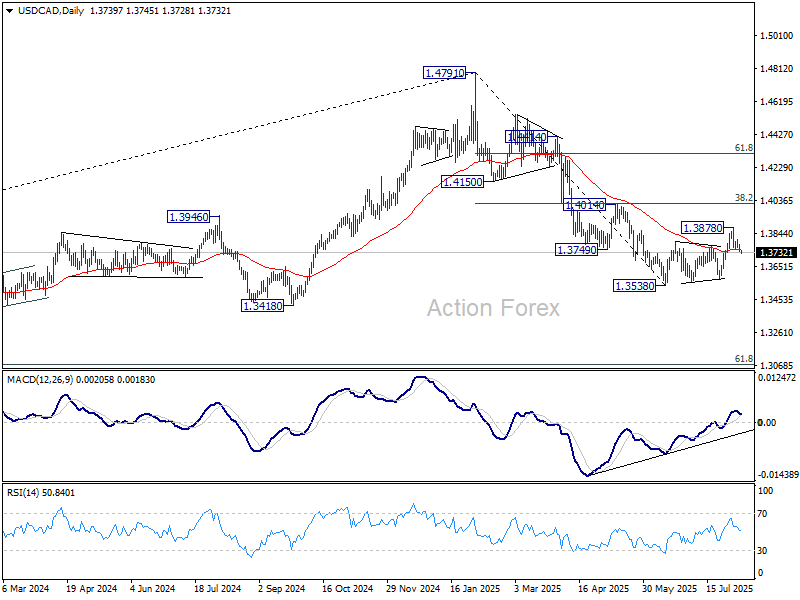

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3724; (P) 1.3752; (R1) 1.3769; More...

USD/CAD's fall from 1.3878 resumed by breaking through 1.3757 temporary low and intraday bias is back on the downside. Current development suggests that corrective rebound from 1.3538 has completed with three waves up to 1.3878. Deeper fall should be seen to retest 1.3538 low. On the upside, however, above 1.3809 will dampen this view and turn bias neutral again.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 resistance holds. Next target is 61.8% retracement of 1.2005 (2021 low) to 1.4791 at 1.3069.

Tariffs and Doves Drive Dollar Lower, Split BoE to Cut

Dollar came under pressure again in Asian session, deepening this week’s selloff as traders digested a flood of tariff developments and dovish commentary from Fed officials. While Asian equity markets held steady with modest gains, the currency markets showed clearer directional bias, with the greenback slipping alongside Swiss Franc and Yen. Euro, Aussie and Kiwi firmed up, while risk sentiment in equities remained somewhat cautious but resilient.

Overnight, multiple Fed speakers leaned toward affirming a rate cut in September. While they avoided endorsing a faster pace of easing, the tone shift was clear: concern is growing about labor market softness, and inflation—while still elevated—is no longer the primary fear. That aligns with the Fed’s June dot plot, which already signaled two cuts in H2 2025. Additional dovish commentary in coming days may not shift pricing much unless it opens the door to three cuts.

Meanwhile, the macro backdrop was quickly overtaken by a fresh round of US tariff moves. President Donald Trump surprised markets by announcing a second 25% tariff on Indian imports, citing continued oil purchases from Russia. The latest round comes on top of duties scheduled to begin Thursday and reflects a dramatic escalation in secondary sanctions enforcement.

In parallel, Trump raised the possibility of targeting China next, depending on what unfolds in coming days. He said "It may happen" when asked if similar tariffs could be imposed on Beijing, after citing dissatisfaction with China’s handling of Russian trade ties. That adds extra uncertainty ahead of the August 12 deadline to finalize a long-term truce following the US-China framework agreement struck in May and updated in June.

In a signal of shifting geopolitical alignment, Indian Prime Minister Narendra Modi is reportedly planning a visit to China for the August 31 Shanghai Cooperation Organisation summit. It would be his first trip to Beijing in over seven years, and comes at a time when New Delhi's ties with Washington are rapidly fraying. The move may indicate India is hedging its bets diplomatically amid escalating US trade threats.

Japan also found itself blindsided. According to a Kyodo report, contrary to earlier assumptions, the 15% US country-specific tariff on Japanese imports will not replace existing duties, but will stack on top of them. A White House official clarified that Tokyo had misunderstood the bilateral deal's terms. That gives the EU preferential treatment over Japan and adds to Tokyo's frustration. Japanese officials have not yet announced a response, but the development adds strain to what was seen as a stable alliance.

Switzerland, meanwhile, failed in its last-ditch effort to avert crippling 39% tariffs. President Karin Keller-Sutter returned from Washington without meeting Trump or any top trade official. With over 60% of Swiss exports affected, the government has called an emergency meeting to formulate a response.

The tech space is now at the center of the tariff war. Trump confirmed a 100% tariff on chip imports unless companies build in the US. While the criteria remain vague, this marks the most aggressive sector-specific measure yet. Apple’s new USD 100B investment pledge in the US was cited as validation of the policy. Major global chipmakers, including TSMC and Nvidia, are already expanding US production, but the tariff scope remains uncertain.

In Asia, at the time of writing, Nikkei is up 0.43%. Hong Kong HSI is up 0.50%. China Shanghai SSE is up 0.12%. Singapore Strait Times is up 0.81%. Japan 10-year JGB yield is down -0.009 at 1.492. Overnight, DOW rose 0.18%. S&P 500 rose 0.73%. NASDAQ rose 1.21%. 10-year yield rose 0.024 to 4.220.

Fed doves gain ground as Cook, Collins highlight drag from uncertainty

In a panel discussion overnight, Fed Governor Lisa Cook described July’s weaker-than-expected jobs report as “concerning” and noted that the pattern of downward revisions to payroll figures was “somewhat typical of turning points.”

Cook warned that uncertainty is now acting like a tax on businesses, with executives spending more time managing ambiguity than making forward-looking decisions. “This is deadweight loss,” she said.

Boston Fed President Susan Collins supported that view, stating the uncertainty burden is “top of mind” for firms across sectors. She pointed out that the effects extend beyond capital spending, with many businesses now hesitant to adjust pricing strategies due to a lack of visibility. “There’s still a wait-and-see,” Collins said.

The shared emphasis from two Fed officials underscores how economic ambiguity is increasingly viewed as a constraint on both employment and inflation dynamics. While neither Cook nor Collins offered direct policy guidance, their comments will reinforce expectations that the Fed is growing more open to easing, particularly if labor and business activity remain sluggish into the fall.

Fed's Daly: Rate cut likely soon as labor market risks mount

San Francisco Fed President Mary Daly said overnight that she expects the central bank will need to cut interest rates “in the coming months,” citing a gradually cooling economy and persistent downside risks in the labor market. “I would see additional slowing as unwelcome,” Daly warned, adding that the labor market tends to “fall quickly and hard” once momentum is lost.

Daly also downplayed the inflationary impact of US tariffs, saying they pose only a short-term threat. Excluding tariff effects, she noted, inflation has been “gradually trending down,” and should continue to ease given restrictive policy and moderating demand.

Fed’s Kashkari reaffirms case for two cuts, says economy slowing

Minneapolis Fed President Neel Kashkari reiterated his view that two rate cuts in 2025 remain a reasonable base case, telling CNBC overnight that “the economy is slowing — and that means, in the near term, it may become appropriate to start adjusting the federal-funds rate.” The comment aligns with growing expectations for a September cut, especially after last week’s soft jobs data.

However, Kashkari’s remarks are broadly consistent with the position he laid out in June, when he wrote in an essay that tariff impacts may be more muted than feared due to corporate adaptations and exemptions. At the time, he argued that these offsetting forces would allow inflation to ease gradually, supporting a measured policy adjustment.

In both June and today’s comments, Kashkari has signaled a preference for patience but also preparedness. Barring any surprises, his base case still assumes a September move, followed by another later in the year.

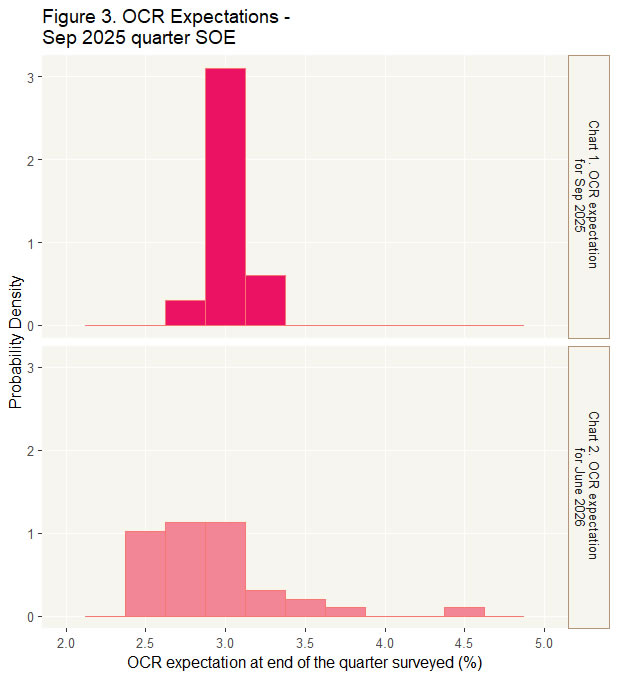

RBNZ survey signals one more cut, then long pause ahead

RBNZ’s August Survey of Expectations suggests the central bank will likely cut rates only once more in 2025, but the outlook beyond that remains cautious. The OCR is forecast to decline from 3.25% to 3.02% by September 2025 — consistent with a single 25bps move, likely in this month's meeting. By June 2026, it’s seen at 2.86%, implying a second cut is possible in H1 2026, but far from assured.

Inflation expectations continue to ease gradually. One-year-ahead CPI forecasts slipped from 2.41% to 2.37%, while two-year-ahead projections fell marginally from 2.29% to 2.28%. Wage inflation expectations were mixed, with one-year views dropping to 2.61% while two-year expectations rose to 2.88%, implying confidence that wage pressures will not reignite inflation risks over the medium term.

The unemployment outlook also improved slightly, with expectations for joblessness falling across all time horizons. Despite soft growth conditions, respondents see GDP rising 1.66% over the next year and 2.16% the year after. Taken together, the survey points to a slow-moving easing cycle ahead, starting with one cut likely later this year, followed by a potentially long pause.

Strong oil, soybean demand drives China import spike, cuts surplus

China’s July trade data surprised to the upside, with exports rising 7.2% yoy and imports jumping 4.1% yoy — the largest annual gain in over a year. Strong commodity demand underpinned the figures, as soybean imports surged 18.5% yoy and crude oil shipments rose 11.5% yoy.

The trade surplus came in at USD 98.2 B, narrower than the expected USD 107.9B, suggesting stronger domestic demand helped balance trade flows.

While the numbers offer a positive signal for global demand, investors remain focused on the looming August 12 deadline to finalize a lasting trade agreement with the US. The strong data may give Beijing some negotiating leverage, but uncertainty remains high.

BoE to cut as doves, hawks, and moderates collide, EUR/GBP set for wild swings

BoE is set to cut interest rates by 25bps to 4.00% today, continuing its steady easing cycle that began a year ago. The decision would mark the fifth rate cut since last August. Crucially, today’s announcement will also include updated economic forecasts that could shed light on how far the BoE is willing—or able—to go with further easing.

With UK GDP shrinking in both April and May, the need for additional support is evident. The IMF recently warned that UK economic growth could stall at just 0.1% for both Q3 and Q4, setting the stage for stagflation.

However, inflation remains a concern. Headline CPI rose 3.6% in June—well above the 2% target—and any upward revision in today's CPI forecasts could tighten the BoE’s policy space. If projections inch toward 4%, it would significantly complicate any aggressive easing path.

The decision is also likely to see a notable division within the Monetary Policy Committee. Hawks like Huw Pill and Catherine Mann may vote to hold rates, while doves such as Swati Dhingra and Alan Taylor could push for a deeper 50bps cut. Even Deputy Governor Dave Ramsden is seen as a potential dovish swing vote. Any unexpected alignment or dissent could shift market pricing for future BoE moves.

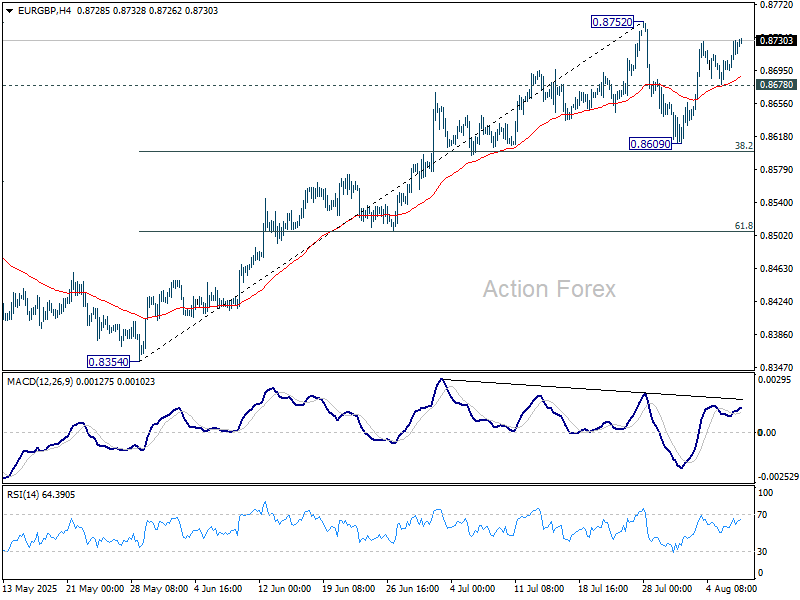

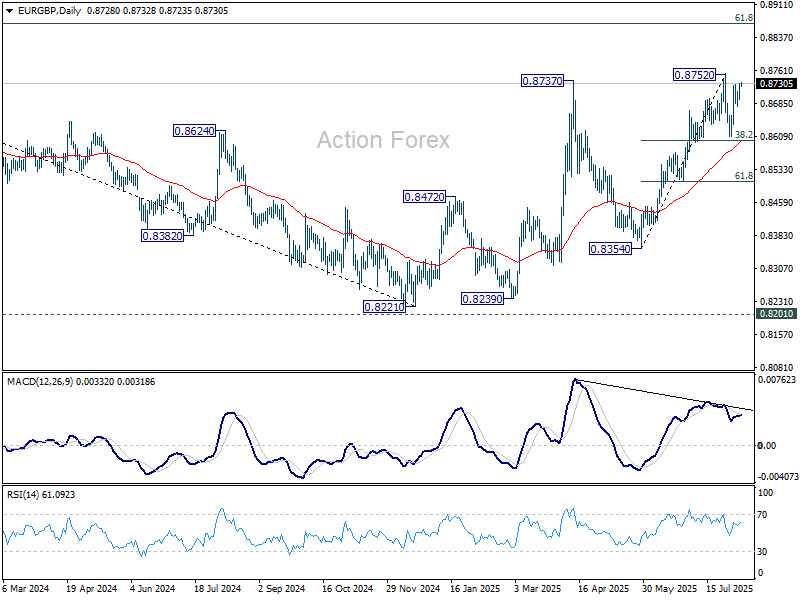

Volatility in EUR/GBP is expected with the rate decision. Technically, it is currently extending the rebound from 0.8609 towards 0.8752 resistance. Strong break there will confirm resumption of whole rally from 0.8221 towards 0.8867 fibonacci level. However, break of 0.8678 support will extend the corrective pattern from 0.8752 towards 0.8609 support again.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3724; (P) 1.3752; (R1) 1.3769; More...

USD/CAD's fall from 1.3878 resumed by breaking through 1.3757 temporary low and intraday bias is back on the downside. Current development suggests that corrective rebound from 1.3538 has completed with three waves up to 1.3878. Deeper fall should be seen to retest 1.3538 low. On the upside, however, above 1.3809 will dampen this view and turn bias neutral again.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 resistance holds. Next target is 61.8% retracement of 1.2005 (2021 low) to 1.4791 at 1.3069.

BoE to cut as doves, hawks, and moderates collide, EUR/GBP set for wild swings

BoE is set to cut interest rates by 25bps to 4.00% today, continuing its steady easing cycle that began a year ago. The decision would mark the fifth rate cut since last August. Crucially, today’s announcement will also include updated economic forecasts that could shed light on how far the BoE is willing—or able—to go with further easing.

With UK GDP shrinking in both April and May, the need for additional support is evident. The IMF recently warned that UK economic growth could stall at just 0.1% for both Q3 and Q4, setting the stage for stagflation.

However, inflation remains a concern. Headline CPI rose 3.6% in June—well above the 2% target—and any upward revision in today's CPI forecasts could tighten the BoE’s policy space. If projections inch toward 4%, it would significantly complicate any aggressive easing path.

The decision is also likely to see a notable division within the Monetary Policy Committee. Hawks like Huw Pill and Catherine Mann may vote to hold rates, while doves such as Swati Dhingra and Alan Taylor could push for a deeper 50bps cut. Even Deputy Governor Dave Ramsden is seen as a potential dovish swing vote. Any unexpected alignment or dissent could shift market pricing for future BoE moves.

Volatility in EUR/GBP is expected with the rate decision. Technically, it is currently extending the rebound from 0.8609 towards 0.8752 resistance. Strong break there will confirm resumption of whole rally from 0.8221 towards 0.8867 fibonacci level. However, break of 0.8678 support will extend the corrective pattern from 0.8752 towards 0.8609 support again.

Strong oil, soybean demand drives China import spike, cuts surplus

China’s July trade data surprised to the upside, with exports rising 7.2% yoy and imports jumping 4.1% yoy — the largest annual gain in over a year. Strong commodity demand underpinned the figures, as soybean imports surged 18.5% yoy and crude oil shipments rose 11.5% yoy.

The trade surplus came in at USD 98.2 B, narrower than the expected USD 107.9B, suggesting stronger domestic demand helped balance trade flows.

While the numbers offer a positive signal for global demand, investors remain focused on the looming August 12 deadline to finalize a lasting trade agreement with the US. The strong data may give Beijing some negotiating leverage, but uncertainty remains high.

RBNZ survey signals one more cut, then long pause ahead

RBNZ’s August Survey of Expectations suggests the central bank will likely cut rates only once more in 2025, but the outlook beyond that remains cautious. The OCR is forecast to decline from 3.25% to 3.02% by September 2025 — consistent with a single 25bps move, likely in this month's meeting. By June 2026, it’s seen at 2.86%, implying a second cut is possible in H1 2026, but far from assured.

Inflation expectations continue to ease gradually. One-year-ahead CPI forecasts slipped from 2.41% to 2.37%, while two-year-ahead projections fell marginally from 2.29% to 2.28%. Wage inflation expectations were mixed, with one-year views dropping to 2.61% while two-year expectations rose to 2.88%, implying confidence that wage pressures will not reignite inflation risks over the medium term.

The unemployment outlook also improved slightly, with expectations for joblessness falling across all time horizons. Despite soft growth conditions, respondents see GDP rising 1.66% over the next year and 2.16% the year after. Taken together, the survey points to a slow-moving easing cycle ahead, starting with one cut likely later this year, followed by a potentially long pause.

Fed’s Daly: Rate cut likely soon as labor market risks mount

San Francisco Fed President Mary Daly said overnight that she expects the central bank will need to cut interest rates “in the coming months,” citing a gradually cooling economy and persistent downside risks in the labor market. “I would see additional slowing as unwelcome,” Daly warned, adding that the labor market tends to “fall quickly and hard” once momentum is lost.

Daly also downplayed the inflationary impact of US tariffs, saying they pose only a short-term threat. Excluding tariff effects, she noted, inflation has been “gradually trending down,” and should continue to ease given restrictive policy and moderating demand.