Sample Category Title

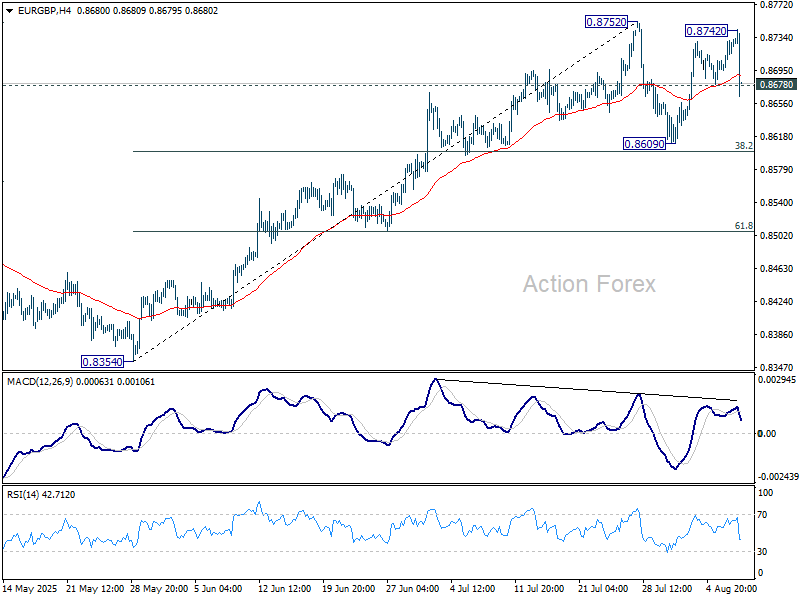

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8707; (P) 0.8720; (R1) 0.8742; More...

EUR/GBP's steep decline and break of 0.8678 support suggests that consolidation pattern from 0.8752 is extending with another falling leg. Deeper decline might be seen but downside should be contained by 38.2% retracement of 0.8354 to 0.8752 at 0.8600. On the upside, firm break of 0.8752 will resume the rise from 0.8354 towards 0.8867 fibonacci level.

In the bigger picture, the structure from 0.8221 medium term bottom are not impulsive enough to suggest that it's reversing the down trend from 0.9267 (2022 high). But even if it's a correction, further rise is expected to 61.8% retracement of 0.9267 to 0.8221 at 0.8867. This will remain the favored case as long as 55 W EMA (now at 0.8493) holds.

BoE’s Hawkish Cut Sparks Sterling Rally

Sterling surged across the board after the BoE delivered a widely expected rate cut to 4.00%, but with a much tighter vote split than markets anticipated. Four of the nine Monetary Policy Committee members voted to keep rates unchanged, signaling persistent concerns about upside inflation risks. This hawkish undercurrent, paired with Governor Andrew Bailey’s cautious tone, undercut expectations for an accelerated easing cycle and helped Sterling lead currency gains on the day.

The hawkish composition of the vote suggests that a follow-up cut in September can be basically ruled out. Odds for a November reduction remain slightly in play, but confidence has diminished. Much will hinge on whether inflation indeed peaks at 4% in September as projected, and if it visibly starts to retreat in October. Until then, investors may treat incoming inflation and wage data as binary catalysts for the next policy move.

Bailey reiterated in the press conference that while the policy path remains downward, it is now clouded by uncertainty. “We do not cut too quickly or by too much,” he warned, highlighting energy and food prices as short-term distortions. His response to questions about the policy direction was telling: while still confident about the eventual path, the Governor acknowledged that the timing and scale of future moves are more uncertain than before.

In the currency markets, Sterling is currently the day’s top performer. Kiwi and Aussie followed in strength, reflecting an underlying risk-on tilt in sentiment. At the other end, Swiss Franc lagged broadly, followed by Euro and Loonie. Dollar and Yen were mixed as they consolidated recent losses.

In Japan, the government downgraded its GDP growth outlook for the fiscal year to 0.7% from 1.2%, citing US tariffs’ drag on capital spending and inflation’s toll on private consumption. Despite the downgrade, the government maintained hope that wage growth would overtake inflation in 2026, supporting a modest recovery in domestic demand-led growth.

In India, Prime Minister Narendra Modi responded forcefully to President Trump’s imposition of a 50% tariff on Indian goods, insisting that his government would not compromise on the welfare of farmers. The message came as Indian and Russian officials met in Moscow to reaffirm their strategic partnership, a sign that geopolitical alignment may further complicate the tariff dispute.

In Europe, at the time of writing, FTSE is down -0.75%. DAX is up 1.65%. CAC is up 1.13%. UK 10-year yield is up 0.027 at 4.56. Germany 10-year yield is down -0.001 at 2.649. Earlier in Asia, Nikkei rose 0.65%. Hong Kong HSI rose 0.69%. China Shanghai SSE rose 0.16%. Singapore Strait Times rose 0.72%. Japan 10-year JGB Yield fell -0.016 to 1.486.

US initial jobless claims rise to 226k, continuing claims highest since late 2021

US initial jobless claims rose 7k to 226k in the week ending August 2, above expectation of 220k. Four-week moving average of initial claims fell -500 to 221k.

Continuing claims rose 38k to 1974k in the week ending July 26, highest since November 6 2021. Four-week moving average of continuing claims rose 5k to 1952k.

BoE cuts to 4.00%, hawkish 5-4 vote lifts Sterling

BoE delivered a widely expected 25 basis point rate cut, lowering the Bank Rate to 4.00% and continuing its cautious easing cycle. However, a hawkish four-member minority, including Chief Economist Huw Pill, Megan Greene, Clare Lombardelli, and Catherine Mann voted to hold rates steady, reflecting continued concern over lingering inflation pressures.

Governor Andrew Bailey led the five-member majority in favor of the reduction, and no member supported a larger reduction (Alan Taylor voted to cut bank rate by 50 bps in first round but changed to 25 bps in second round to avoid hold).. This signals that while easing continues, the BoE is far from embracing a more aggressive cutting path.

The BoE's updated projections show inflation expected to rise temporarily, peaking around 4.0% in September before falling back toward the 2% target. However, the MPC noted that upside risks to medium-term inflation "have moved slightly higher" since May, citing concerns that temporary price increases could entrench wage and pricing behaviors. This inflation vigilance likely explains the hawkish vote split and continued pushback against front-loading cuts.

On the growth side, the MPC noted that underlying GDP "remains subdued", with slack emerging in the labor market. While domestic and global uncertainties persist, the committee acknowledged that trade policy risk has “diminished somewhat”—a nod to easing tensions after recent UK-U.S. tariff agreements.

Even with economic momentum fading, the MPC maintained that policy is “not on a pre-set path,” emphasizing a “gradual and careful approach” to further easing.

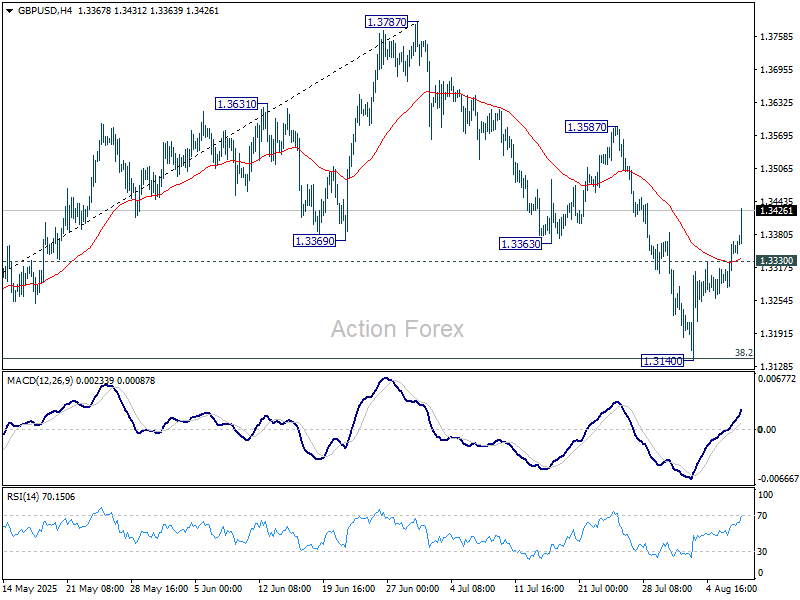

Sterling responded positively to the rate cut and the hawkish tilt in the vote. GBP/USD's rally from 1.3140 accelerates after the announcement. Current development further affirms the case that correction from 1.3787 has completed with three waves down to 1.3140. Further rise should be seen to 1.3587 resistance first. Firm break there will target a retest on 1.3787 high.

RBNZ survey signals one more cut, then long pause ahead

RBNZ’s August Survey of Expectations suggests the central bank will likely cut rates only once more in 2025, but the outlook beyond that remains cautious. The OCR is forecast to decline from 3.25% to 3.02% by September 2025 — consistent with a single 25bps move, likely in this month's meeting. By June 2026, it’s seen at 2.86%, implying a second cut is possible in H1 2026, but far from assured.

Inflation expectations continue to ease gradually. One-year-ahead CPI forecasts slipped from 2.41% to 2.37%, while two-year-ahead projections fell marginally from 2.29% to 2.28%. Wage inflation expectations were mixed, with one-year views dropping to 2.61% while two-year expectations rose to 2.88%, implying confidence that wage pressures will not reignite inflation risks over the medium term.

The unemployment outlook also improved slightly, with expectations for joblessness falling across all time horizons. Despite soft growth conditions, respondents see GDP rising 1.66% over the next year and 2.16% the year after. Taken together, the survey points to a slow-moving easing cycle ahead, starting with one cut likely later this year, followed by a potentially long pause.

Strong oil, soybean demand drives China import spike, cuts surplus

China’s July trade data surprised to the upside, with exports rising 7.2% yoy and imports jumping 4.1% yoy — the largest annual gain in over a year. Strong commodity demand underpinned the figures, as soybean imports surged 18.5% yoy and crude oil shipments rose 11.5% yoy.

The trade surplus came in at USD 98.2 B, narrower than the expected USD 107.9B, suggesting stronger domestic demand helped balance trade flows.

While the numbers offer a positive signal for global demand, investors remain focused on the looming August 12 deadline to finalize a lasting trade agreement with the US. The strong data may give Beijing some negotiating leverage, but uncertainty remains high.

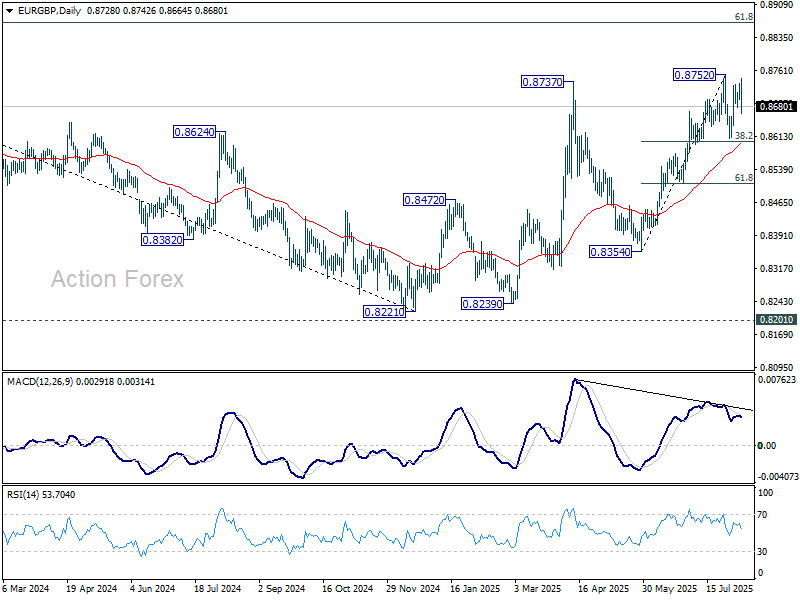

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8707; (P) 0.8720; (R1) 0.8742; More...

EUR/GBP's steep decline and break of 0.8678 support suggests that consolidation pattern from 0.8752 is extending with another falling leg. Deeper decline might be seen but downside should be contained by 38.2% retracement of 0.8354 to 0.8752 at 0.8600. On the upside, firm break of 0.8752 will resume the rise from 0.8354 towards 0.8867 fibonacci level.

In the bigger picture, the structure from 0.8221 medium term bottom are not impulsive enough to suggest that it's reversing the down trend from 0.9267 (2022 high). But even if it's a correction, further rise is expected to 61.8% retracement of 0.9267 to 0.8221 at 0.8867. This will remain the favored case as long as 55 W EMA (now at 0.8493) holds.

US initial jobless claims rise to 226k, continuing claims highest since late 2021

US initial jobless claims rose 7k to 226k in the week ending August 2, above expectation of 220k. Four-week moving average of initial claims fell -500 to 221k.

Continuing claims rose 38k to 1974k in the week ending July 26, highest since November 6 2021. Four-week moving average of continuing claims rose 5k to 1952k.

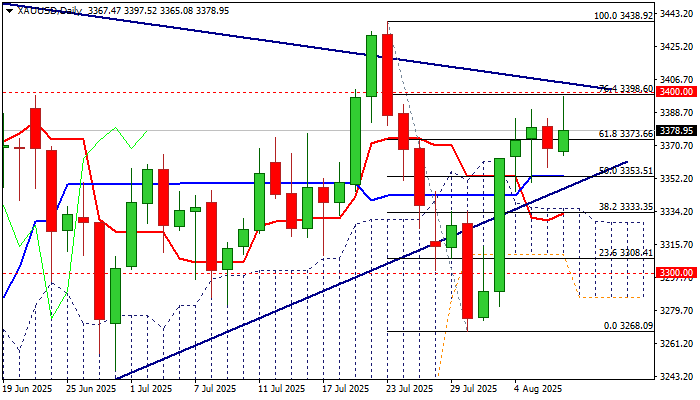

XAU/USD: Gold Cracks Key Resistance Zone on Fresh Wave of Safe Haven Demand

Gold price rose on Thursday morning as new packages of increased US import tariffs took effect, adding to high global uncertainty and prompting investors into safety.

Fresh rise cracked strong resistances at $3400 zone (Fibo 76.4% of $3438/$3268 / psychological /upper triangle boundary) but failed to break higher on first attempt.

As expected, bulls faced headwinds and metal’s price eased to the mid-point of congestion that extends into third straight day.

Technical picture on daily chart has improved, but flat momentum (slightly above the centreline) and overbought stochastic warning, after gold faced a double false break below and above triangle recently.

However, triangle is narrowing, and eventual clear break is likely to be seen in coming sessions that would generate fresh direction signal.

Current favorable fundamentals contribute to bullish scenario, with sustained break above $3400 zone to signal bullish continuation and expose targets at $3438 and $3452 (tops of July 23 / June 16) guarding key barrier at $3500 (new record high, posted on Apr 22).

Conversely, violation of triangle support line ($3347) would weaken near-term structure, but extension below daily cloud top ($3335) will be required to verify fresh negative signal and shift focus towards key supports at $3300 / $3286 / $3268 (psychological /daily cloud base / July 30 multi-week low).

Res: 3400; 3405; 3414; 3438.

Sup: 3365; 3353; 3347; 3335.

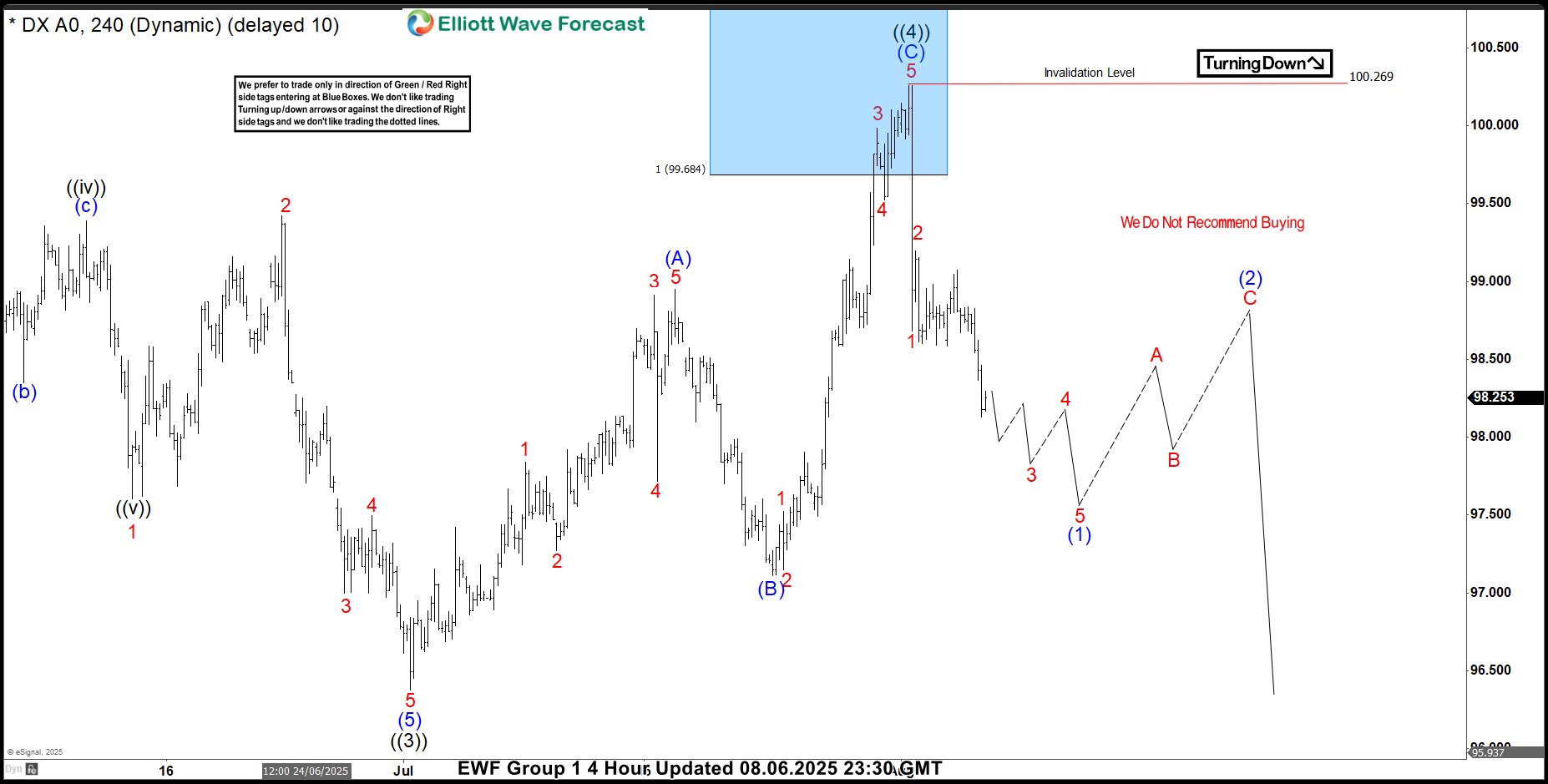

Dollar Index (DXY) Elliott Wave: Selling Rallies at the Blue Box

Hello traders. In this article, we are going to present another Elliott Wave trading setup we got in Dollar Index . As our members know DXY index remains bearish against the 101.936 pivot. Recently Dollar made a clear 3 waves recovery completed precisely at the Equal Legs zone, referred to as the Blue Box Area. In the following sections, we are going to explain Elliott Wave pattern and discuss the trading setup.

DXY Elliott Wave 4 Hour Chart 07.28.2025

Dollar is doing recovery against the 101.936 peak. The price action suggest that recovery is still incomplete at the moment , suggesting potentially more short term strength. This correction can see another leg up toward the Blue Box zone at 99.68-101.28 area, where we are looking to re-enter as sellers. We recommend members to avoid buying Dollar. As the main trend remains bearish, we expect at least a 3-wave pull back from this Blue Box area. Once the price touches the 50 fibs against the ((x)) black connector, we’ll make positions risk-free and set the stop loss at breakeven and book partial profits. On other hand, breaking above the 101.281 peak would invalidate the trade.

Quick reminder on how to trade our charts :

Red bearish stamp+ blue box = Selling Setup

Green bullish stamp+ blue box = Buying Setup

Charts with Black stamps are not tradable. 🚫

DXY Elliott Wave 4 Hour Chart 07.28.2025

Dollar reached the Blue Box area between 99.68-101.28 and, as expected, found sellers. DXY has made a solid decline from our Selling Zone. As a result, any short positions taken from the Blue Box should now be risk-free, with partial profits already booked. At this point, we would like to see a further decline and a break below the July 1st low to confirm that the next leg down is in progress.

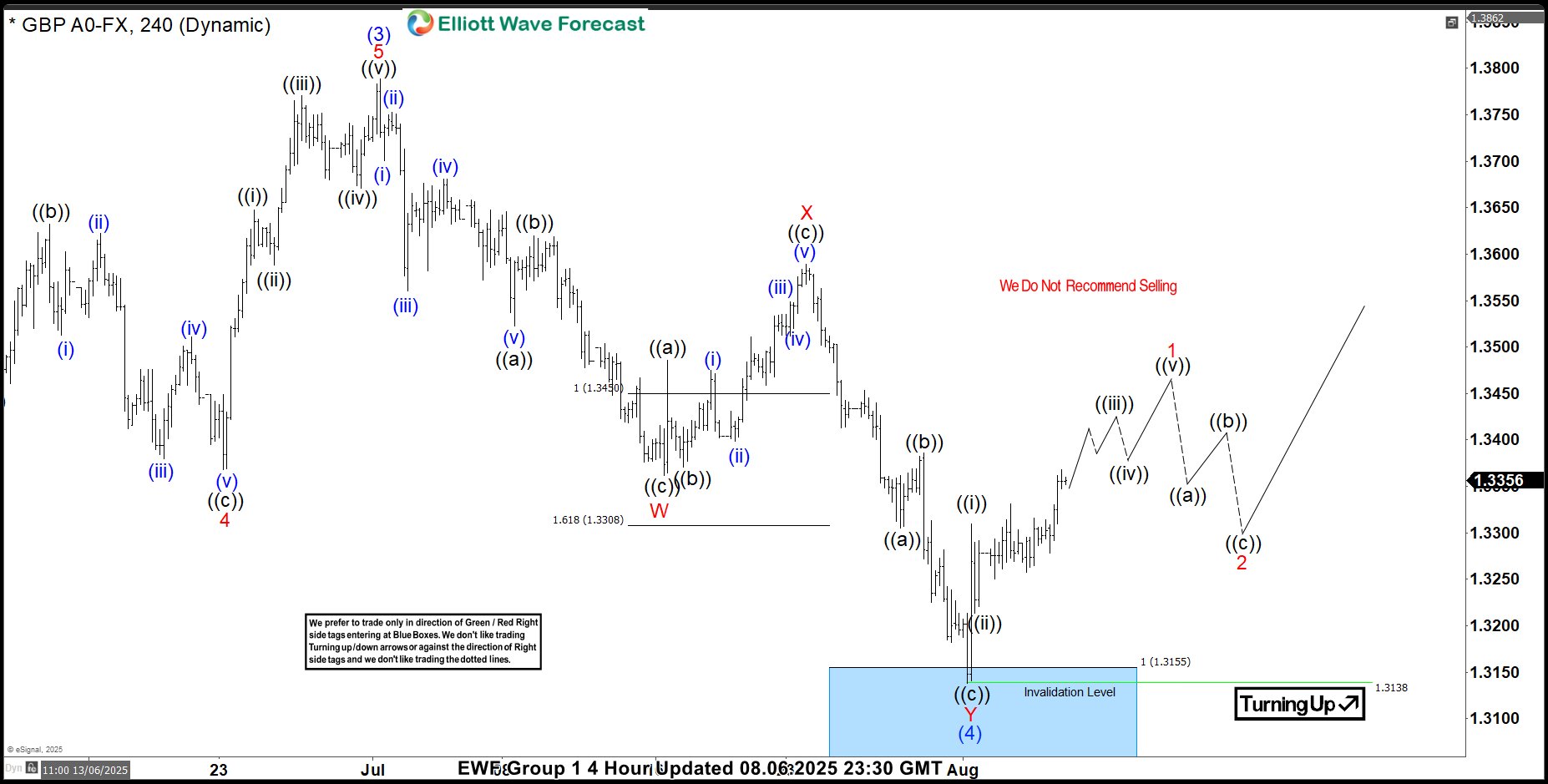

GBPUSD Elliott Wave Forecast: Buying the Dips in the Blue Box

As our members know we have had many profitable trading setups recently. In this technical article, we are going to talk about another Elliott Wave trading setup we got in GBPUSD. The pair has completed its correction exactly at the Equal Legs zone, also known as the Blue Box Area. In this article, we’ll break down the Elliott Wave forecast, explain the trading setup in detail, and provide the upside target.

GBPUSD Elliott Wave 4 Hour Chart 07.26.2025

The price action suggests that GBPUSD is forming a pullback in the form of a double three (WXY) structure. While price remains below the red X connector, we believe the correction is still in progress and expect another leg lower toward the 1.3156 area , where we are looking to re-enter as buyers. We recommend that members avoid selling GBPUSD, as the main trend remains bullish. We anticipate at least a three-wave bounce from the Blue Box area.Once the price reaches the 50% Fibonacci retracement against the red X connector, we will make the position risk-free by moving the stop loss to breakeven and booking partial profits.

GBPUSD Elliott Wave 4 Hour Chart 08.06.2025

The pair has made another wave down and completed 7 swings pattern at the Blue Box area. The pair found buyers as expected, making decent bounce. Reaction from the buying zone has reached 50 fibs against the X red connector. Consequently, any long positions from the Blue Box should now be risk-free. We’ve set our stop loss at breakeven and have already secured partial profits. While price holds above 1.3138, we consider the wave (4) correction complete and see potential for wave (5) to be in progress toward the 1.3936 area.

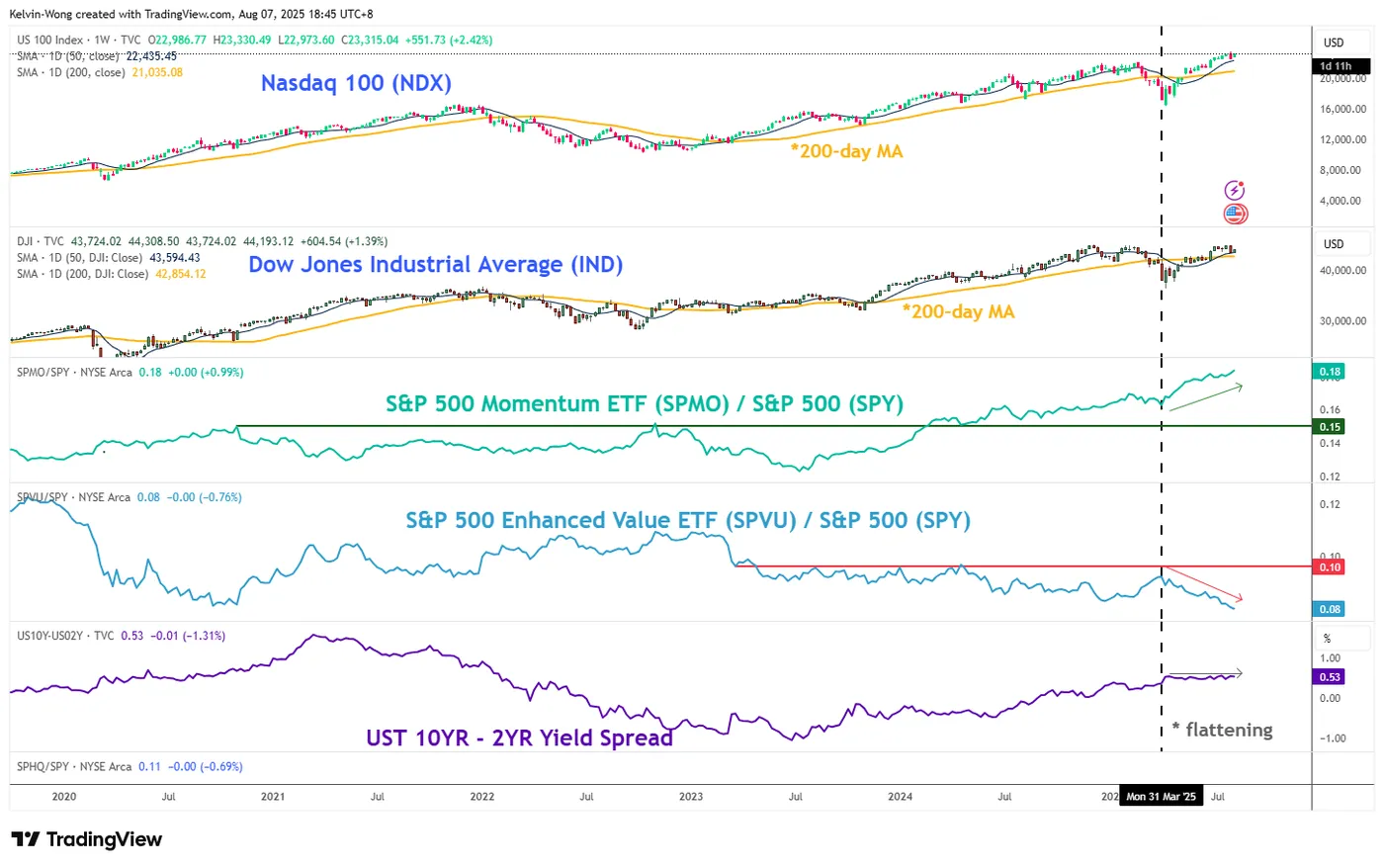

Nasdaq 100 Technical: Eyeing a New Fresh All-Time High, Supported by Momentum and Flattening US Treasury Yield Curve

Risk-on sentiment was on full display since the start of this week, as optimism around the US technology boom driven by Artificial Intelligence (AI) once again overshadowed more worrisome global developments on tariffs and growth.

AI optimism triggered another bullish impulsive move on US equities

On Wednesday, 6 August, U.S. equities rallied on news that OpenAI—the creator of ChatGPT and a leading force in the ongoing AI boom—is considering a stock sale that could value the company at $500 billion, a significant leap from its current $300 billion valuation.

Meanwhile, President Trump’s announcement of a proposed 100% tariff on semiconductor imports was largely shrugged off by investors. The impact was softened by incentives: U.S. corporations could be exempt from the levy if they commit to reshoring production. Apple Inc. was cited as a model example.

The S&P 500 and Nasdaq 100 extended their short-term bullish momentum that began on Monday, 4 August, posting intraday gains of 0.7% and 1.3%, respectively. The Dow Jones Industrial Average underperformed slightly with a modest 0.2% gain.

Asian markets followed the positive sentiment today, with bullish momentum persisting. S&P 500 and Nasdaq 100 E-mini futures advanced a further 0.7% by the end of the Asia trading session.

Let’s now decipher the US Nasdaq 100 CFD Index from a technical analysis perspective and construct a medium-term (multi-week) trading set-up.

Fig. 1: US Nasdaq 100 CFD Index medium-term trend as of 7 Aug 2025 (Source: TradingView)

Fig. 2: Nasdaq 100 major trend with S&P 500 momentum/S&P 500 relative strength & US Treasury yield curve as of 6 Aug 2025 (Source: TradingView)

Preferred trend bias (1-3 weeks)

The minor corrective decline of -4.4% from 31 July 2025 high to 1 August 2025 low is likely to have ended. The US Nasdaq 100 CFD Index is now in the process of shaping a potential bullish impulsive up move sequence within its medium-term uptrend phase.

Bullish bias with key medium-term pivotal support at 22,945 for the next medium-term resistances to come in at 23,820 and 24,164/24,220 (Fibonacci extension cluster and upper boundary of a medium-term ascending channel in place since 19 June 2025 low) (see Fig. 1).

Key elements

- Price actions of the US Nasdaq 100 CFD Index have reintegrated above and retested the 20-day moving average on Wednesday, 6 August 2025, indicating the potential start of another bullish impulsive up move sequence.

- The 4-hour MACD trend indicator of the US Nasdaq 100 has just trended upwards above its centreline, which suggests the potential start of a new medium-term (multi-week) uptrend phase.

- The S&P 500 Momentum factor exchange-traded fund (ETF) has continued to outperform the S&P 500 ETF since the end of March 2025. Based on past observations, this momentum outperformance has supported the medium-term and major uptrend phases of the US Nasdaq 100 CFD Index (see Fig. 2).

- The US Treasury yield curve (10-year yield of the US Treasury note minus the 2-year yield of the US Treasury note) has flattened since early April 2025. This observation suggests falling US interest rates, which directly increase bond prices and returns in the short run. However, higher bond prices mean lower yields and lower returns for bonds in the future, which in turn, drive investors into the US stock market. An indirect medium-term positive driver to support further potential upside in the US Nasdaq 100 CFD Index (see Fig. 2).

Alternative trend bias (1 to 3 weeks)

Failure to hold the 22,945 key support invalidates the bullish tone to open scope for another corrective decline to expose the next medium-term supports at 22,670 and 22,410 (also close to the 50-day moving average).

FTSE 100 Technical Outlook: Range Holds Firm as BOE Meeting Approaches

The FTSE 100 edged higher this morning ahead of the highly anticipated Bank of England (BoE) interest rate meeting.

Markets are expecting a rate cut from the BoE today which could help propel the FTSE 100 to fresh all-time highs,

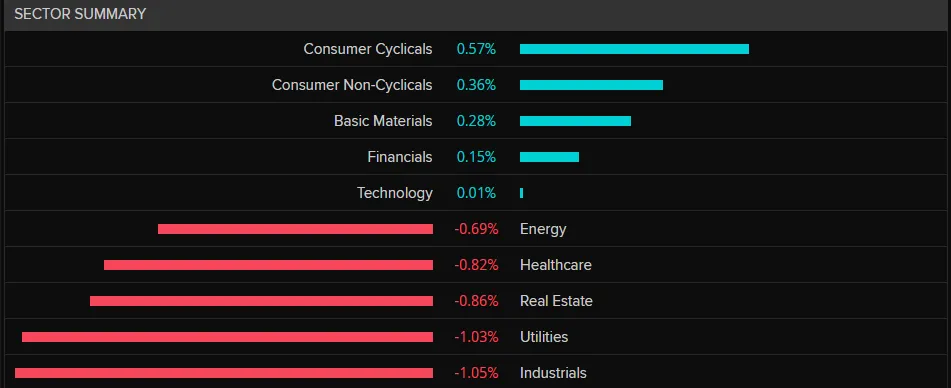

Looking at a sector breakdown for the FTSE and consumer non-cyclicals leads the way with gains of 0.23% with only consumer cyclicals, financials,and technology (marginal) in the green as well. All other sectors are in the red at the time of writing.

Source: LSEG

Looking at companies, BAE Systems and Hikma Pharmaceuticals are weighing on the index with losses of 4.1% and 7.1% respectively. This was however offset thanks to significant gains from the Intercontinental Hotel Group which is trading around 7.% higher on the day.

In other news, Halifax data was released this morning and showed UK house prices went up by 0.4% in July, the biggest monthly increase this year, helped by lower mortgage rates making homes more affordable.

Technical Analysis - FTSE 100

From a technical standpoint, the FTSE has been rangebound since July 23.

Having broken above crucial resistance at 9048 the index has held above this level with previous attempts to break lower met with significant buying pressure.

Such an example occurred on Friday last week and saw the index find support at the 200-day MA on the H2 chart.

Price is currently reston on the 100-day MA and attempts to push higher have thus far stalled.

Immediate resistance is at 9144 before the 9157 and 8183 handles come into focus.

Looking at the downside picture, support may be found at 9120 before 9082 and 9048 come into view.

FTSE 100 (UK100) H2 Chart, August 7, 2025

Source: TradingView (click to enlarge)

BoE cuts to 4.00%, hawkish 5-4 vote lifts Sterling

BoE delivered a widely expected 25 basis point rate cut, lowering the Bank Rate to 4.00% and continuing its cautious easing cycle. However, a hawkish four-member minority, including Chief Economist Huw Pill, Megan Greene, Clare Lombardelli, and Catherine Mann voted to hold rates steady, reflecting continued concern over lingering inflation pressures.

Governor Andrew Bailey led the five-member majority in favor of the reduction, and no member supported a larger reduction (Alan Taylor voted to cut bank rate by 50 bps in first round but changed to 25 bps in second round to avoid hold).. This signals that while easing continues, the BoE is far from embracing a more aggressive cutting path.

The BoE's updated projections show inflation expected to rise temporarily, peaking around 4.0% in September before falling back toward the 2% target. However, the MPC noted that upside risks to medium-term inflation "have moved slightly higher" since May, citing concerns that temporary price increases could entrench wage and pricing behaviors. This inflation vigilance likely explains the hawkish vote split and continued pushback against front-loading cuts.

On the growth side, the MPC noted that underlying GDP "remains subdued", with slack emerging in the labor market. While domestic and global uncertainties persist, the committee acknowledged that trade policy risk has “diminished somewhat”—a nod to easing tensions after recent UK-U.S. tariff agreements.

Even with economic momentum fading, the MPC maintained that policy is “not on a pre-set path,” emphasizing a “gradual and careful approach” to further easing.

Sterling responded positively to the rate cut and the hawkish tilt in the vote. GBP/USD's rally from 1.3140 accelerates after the announcement. Current development further affirms the case that correction from 1.3787 has completed with three waves down to 1.3140. Further rise should be seen to 1.3587 resistance first. Firm break there will target a retest on 1.3787 high.

(BOE) Bank Rate reduced to 4%

Monetary Policy Summary, August 2025

The Monetary Policy Committee (MPC) sets monetary policy to meet the 2% inflation target, and in a way that helps to sustain growth and employment. The MPC adopts a medium-term and forward-looking approach to determine the monetary stance required to achieve the inflation target sustainably.

At its meeting ending on 6 August 2025, the MPC voted by a majority of 5–4 to reduce Bank Rate by 0.25 percentage points, to 4%, rather than maintaining it at 4.25%.

There has been substantial disinflation over the past two and a half years, following previous external shocks, supported by the restrictive stance of monetary policy. That progress has allowed for reductions in Bank Rate over the past year. The Committee remains focused on squeezing out any existing or emerging persistent inflationary pressures, to return inflation sustainably to its 2% target in the medium term.

The path of disinflation in underlying domestic price and wage pressures has generally continued, albeit to different degrees. Twelve-month CPI inflation increased to 3.5% in 2025 Q2, owing to developments in energy, food and administered prices. Pay growth remains elevated, but has declined further recently, and is still expected to slow significantly over the rest of the year. Services consumer price inflation has been broadly flat over recent months. The Committee continues to be vigilant about the extent to which easing pay pressures will feed through to consumer price inflation.

CPI inflation is forecast to increase slightly further to peak at 4.0% in September. Inflation is expected to fall back thereafter towards the 2% target, although the Committee remains alert to the risk that this temporary increase in inflation could put additional upward pressure on the wage and price-setting process. Overall, the MPC judges that the upside risks around medium-term inflationary pressures have moved slightly higher since May.

Underlying UK GDP growth has remained subdued, consistent with a continued, gradual loosening in the labour market. A margin of slack is judged to have emerged in the economy. Downside domestic and geopolitical risks around economic activity remain, although trade policy uncertainty has diminished somewhat.

At this meeting, the Committee voted to reduce Bank Rate to 4%. A gradual and careful approach to the further withdrawal of monetary policy restraint remains appropriate. The restrictiveness of monetary policy has fallen as Bank Rate has been reduced. The timing and pace of future reductions in the restrictiveness of policy will depend on the extent to which underlying disinflationary pressures continue to ease. Monetary policy is not on a pre-set path, and the Committee will remain responsive to the accumulation of evidence.

Minutes of the Monetary Policy Committee meeting ending on 6 August 2025

1: Before turning to its immediate policy decision, the Committee discussed: the international economy; monetary and financial conditions; demand and output; and supply, costs and prices. The latest data on these topics were set out in the accompanying August 2025 Monetary Policy Report.

2: The Committee discussed recent developments in international trade policies and their implications for the UK. US tariff rates had remained at higher levels than in the period preceding the initial announcements by the US administration in April. However, uncertainty around trade had reduced since the May Monetary Policy Report as the US had reached trade agreements with some countries. The reduction in tariff rates relative to those assumed in the May Report implied that global demand would be slightly stronger in the baseline projection. Global developments had, nevertheless, not played a large role in the policy discussions at this MPC meeting.

3: Developments in international trade policies had also generally supported sentiment in financial markets, such that financial conditions had loosened a little since the MPC’s June meeting. Measures of financial market volatility had either remained stable or fallen somewhat. UK and US equity prices had increased, with estimates of equity risk premia across advanced economies falling. Spreads on investment grade corporate bonds had tightened.

4: The near-term market-implied path for Bank Rate was relatively little changed since the Committee’s June meeting but was a little higher than the path assumed in the May Report. Almost all respondents to the Bank’s latest Market Participants Survey (MaPS) expected a reduction in Bank Rate at this meeting, similar to market pricing. The median profile in the August MaPS implied a cumulative 50 basis point reduction in Bank Rate by the end of this year, broadly in line with market pricing.

5: Monthly UK GDP growth in April and May had been -0.3% and -0.1% respectively. These outturns suggested that stronger GDP growth earlier in the year had, in part, been driven by international tariff or domestic tax-related front-loading. The S&P Global UK PMI future output index had risen over past months, and the output index had also risen but by less. Bank staff estimated that GDP growth had been 0.1% in 2025 Q2, in line with the projection in the May Report, and growth was expected to pick up to 0.3% in Q3.

6: The Committee discussed the extent to which developments in activity had fed through to spare capacity in the economy. There had continued to be a gradual loosening in the labour market. Weak underlying employment growth in recent quarters had largely been ascribed to weakness in underlying demand and, more recently, an increase in firms’ costs. The LFS unemployment rate had increased further in the three months to May, as expected. Vacancies had remained below their estimated equilibrium levels, with other indicators and statistical models pointing to further increases in spare capacity.

7: The evidence from a range of sources and Bank staff analysis suggested that disinflation in underlying price and wage pressures had generally continued, albeit to different degrees. Annual private sector regular AWE growth had declined further in the most recent data, to just below 5%. This was weaker than expected in the May Report, but consistent with a range of other indicators. AWE growth nevertheless remained above what Bank models could explain. Developments in pay settlements, the latest DMP Survey and Agents’ intelligence suggested a further weakening in pay growth in coming quarters, to around 3¾% by the end of the year.

8: Twelve-month CPI inflation had increased to 3.6% in June, slightly above expectations at the time of both the May Report and the Committee’s June meeting, reflecting upside news in food, energy and services prices. Services price inflation had remained unchanged at 4.7% in June. Underlying services price inflation had continued to moderate, but at a slower pace than last year based on some measures.

9: CPI inflation was expected to rise a little further, to just over 3¾% in 2025 Q3, before falling back towards the 2% target. The return of inflation towards target would be supported by an expected gradual reduction in food price inflation next year. Box E in the August Report discussed the risks related to food price inflation, including the potential for it to have an outsized influence on households’ formation of inflation expectations. The Committee discussed the extent to which the lag from wage growth through to services price inflation was operating in line with historical trends. Looking beyond the temporary factors putting upward pressure on prices this year, wage and services price disinflation would be key drivers of CPI inflation settling sustainably at the target.

The immediate policy decision

10: The MPC sets monetary policy to meet the 2% inflation target, and in a way that helps to sustain growth and employment. The MPC adopts a medium-term and forward-looking approach to determine the monetary stance required to achieve the inflation target sustainably.

11: The Committee’s policy deliberations at this meeting had focused on a number of factors, including the extent to which disinflation was continuing, the degree of slack building in the economy, and the current and future restrictiveness of the monetary policy stance.

12: Disinflation in underlying domestic price and wage pressures had generally continued, albeit to different degrees. Core CPI and services price inflation had been broadly unchanged in recent months. Continued moderation in wage growth was likely to feed through to lower services price inflation, although this process could take time and Committee members varied in their confidence in it. Headline inflation had risen and was projected to rise slightly further in the near term, although in the baseline projection this was not expected to lead to additional second-round effects on underlying domestic inflationary pressures. The increase in headline inflation was explicable by factors such as supply issues in certain food items and changes in administered prices. However, increases in food and energy price inflation might prove salient for households’ formation of inflation expectations. As illustrated in the inflation persistence scenario set out in the May Monetary Policy Report, this could place upward pressure on the wage and price-setting process. Overall, the MPC judged that the upside risks around medium-term inflationary pressures had moved slightly higher since May.

13: UK economic activity had remained subdued. A margin of spare capacity was estimated to have opened up, which was expected to act against some continuing inflationary persistence. There was a range of views around the extent to which it had opened and would continue to build. The labour market was continuing to loosen gradually. For some members, weak employment growth pointed to further spare capacity building. For others, potential structural changes in the labour market meant that sufficient slack might not have emerged and might not build further to weigh on inflation. Members concurred that there were generally downside risks around consumption growth in the baseline forecast and upside risks around the path of the saving ratio, including from the risk of greater precautionary saving behaviour by households.

14: The Committee considered Bank staff’s latest assessment of monetary policy restrictiveness, as set out in Box A in the accompanying August Report. Reflecting the usual lags of policy, past restrictiveness was estimated to be weighing on the current level of demand, which would contribute to the disinflationary process. For those members placing greater weight on downside risks to inflation, the impact of past and current restrictiveness was likely to be sufficient to lean against inflationary pressures and less restrictiveness was probably required going forward. Those members who were more concerned about inflationary pressures persisting judged that a more prolonged period of policy restrictiveness was likely to be warranted.

15: In considering the approach to removing remaining policy restraint at this meeting and beyond, all members were balancing various considerations. This included risks in different directions to growth and inflation, the degree of continued impact from past tightening in policy, the costs of loosening policy too quickly or too slowly, and whether and how long to wait and observe further incoming evidence before reducing Bank Rate further.

16: Five members preferred a reduction in Bank Rate at this meeting.

17: Four of these five members preferred a 0.25 percentage point reduction in Bank Rate at this meeting. There had been sufficient progress in underlying disinflation albeit, for some of these members, with a risk that this momentum could slow. There remained greater signs of disinflation from labour market quantities and wages, than from developments in domestic prices. Activity remained weak. The pace of disinflation from here would help inform these members’ views on how quickly to remove remaining policy restraint. On the one hand, higher food prices could raise inflation expectations and generate greater inflation persistence. On the other hand, signs of weaker demand, for example as a result of the impact of continued high saving on consumption, could lead to a more rapid opening up of slack in the labour market.

18: One of these five members preferred a 0.5 percentage point reduction in Bank Rate at this meeting. Underlying disinflation continued. Absent external shocks, domestic inflation, especially in services, was tightly linked to wages. The labour market had slack and was deteriorating further. Wage settlements had fallen to around 3.5% in the first half of 2025 and were expected to fall further in the second half. The inflation hump was expected to normalise, being dominated by one-off changes in tax and administered prices, and food inflation in a limited set of items, neither related to demand pressure. Energy futures curves were flat. With a US average tariff rate near 20%, trade diversion would slowly permeate, pushing down on inflation. UK sentiment was weak, with subdued consumption and investment. This picture was one of downside risks in coming years, namely: inflation below forecast, and activity weak or an increased risk of recession. For insurance against this balance of risks, a less restrictive policy was warranted.

19: Four members preferred to hold Bank Rate at 4.25% at this meeting. The disinflationary process had slowed and the risk of inflation expectations feeding through to second-round effects had risen. Business and household inflation expectations remained elevated, inflation was expected to peak at 4% and much of the recent near-term upside news in inflation had been driven by highly salient food and energy prices. Firms’ own-price expectations remained more sensitive to upside inflation surprises as well. These members would continue to assess the pace of disinflation, being alert to downside pressures on pricing power from domestic demand and global forces, alongside the risk of greater inflation persistence from structural changes in goods and labour markets. A slower loosening of policy would reduce the risk of inflation not meeting the target sustainably.

20: The Committee judged that a gradual and careful approach to the further withdrawal of monetary policy restraint remained appropriate. The restrictiveness of monetary policy had fallen as Bank Rate had been reduced. The timing and pace of future reductions in the restrictiveness of policy would depend on the extent to which underlying disinflationary pressures would continue to ease. Monetary policy was not on a pre-set path, and the Committee would remain responsive to the accumulation of evidence.

21: The Chair invited the Committee to vote on the proposition that:

- Bank Rate should be reduced by 0.25 percentage points, to 4%.

22: Four members voted in favour of the proposition (Andrew Bailey, Sarah Breeden, Swati Dhingra and Dave Ramsden). Four members (Megan Greene, Clare Lombardelli, Catherine L Mann and Huw Pill) preferred to maintain Bank Rate at 4.25%. One member (Alan Taylor) preferred to reduce Bank Rate by 0.5 percentage points, to 3.75%.

23: In order to secure a majority decision on Bank Rate, the Chair invited the Committee to vote on whether:

- Bank Rate should be reduced by 0.25 percentage points, to 4%, or Bank Rate should be maintained at 4.25%.

24: Five members (Andrew Bailey, Sarah Breeden, Swati Dhingra, Dave Ramsden and Alan Taylor) voted to reduce Bank Rate by 0.25 percentage points, to 4%. One of these members (Alan Taylor), who would otherwise have preferred to reduce Bank Rate by 0.5 percentage points, voted for a 0.25 percentage points reduction rather than maintaining Bank Rate. Four members (Megan Greene, Clare Lombardelli, Catherine L Mann and Huw Pill) voted to maintain Bank Rate at 4.25%.

25: On this basis, the MPC voted by a majority of 5–4 to reduce Bank Rate by 0.25 percentage points, to 4%, rather than maintaining it at 4.25%.

Operational considerations

26: On 6 August, the stock of UK government bonds held for monetary policy purposes was £586 billion.

27: The following members of the Committee were present:

- Andrew Bailey, Chair

- Sarah Breeden

- Swati Dhingra

- Megan Greene

- Clare Lombardelli

- Catherine L Mann

- Huw Pill

- Dave Ramsden

- Alan Taylor

Sam Beckett was present as the Treasury representative.

David Roberts was present on 30 July and 4 August, as an observer for the purpose of exercising oversight functions in his role as a member of the Bank’s Court of Directors.