Sample Category Title

USDCAD Rises from a Weak Canadian Employment Data

USDCAD rises from a disappointing Canadian Employment number.

The data which came at -40.8K vs 13.5K expected , takes out half of the past month's upwards surprise (+83K) and looking at the detail, full-time employment saw the most regression (-51K) while part-time employment rose by a small margin.

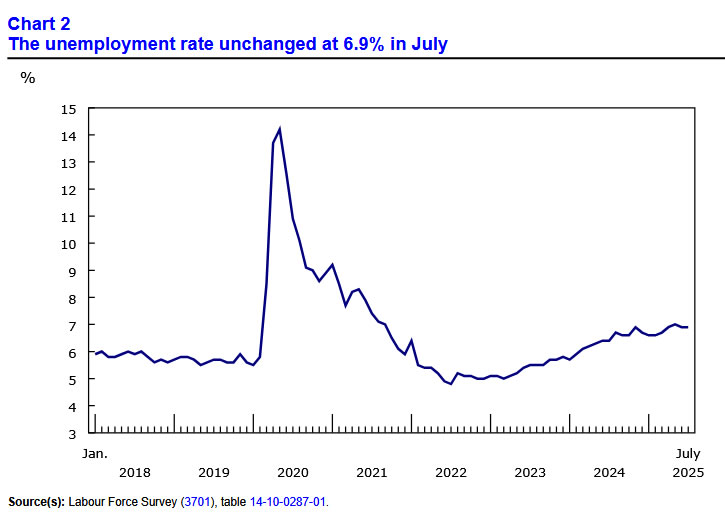

Overall, the unemployment rate came as expected (6.9% vs 6.9% exp) but overall, Canada has been struggling with job creation for a while now.

Canadian Employment data tends to be pretty volatile, especially during summer.

In the meantime, the Loonie had appreciated a bit against the US Dollar in the past few days. With not many factors prompting participants to buy the CAD, it was more a selloff in the Greenback which took the pair to retest the highs of the past month range.

Let's take a detailed look at USDCAD.

USDCAD Multi-timeframe analysis

USDCAD Daily Chart

USDCAD Daily Chart, August 8, 2025, Source: TradingView

Despite the strong rally at the end of July, the pair holds within its 2025 downwards channel.

RSI Momentum saw a deceleration of bullish momentum after last Friday's US Jobs data that also disappointed, but stays above the neutral line.

Holding the channel will be the element to look at on higher timeframes for the pair.

Let's take a closer look to spot how the miss impacted the Loonie.

USDCAD 4H Chart

USDCAD 4H Chart, August 8, 2025, Source: TradingView

The pair rose about 200 pips after this morning's data, but buyers are stepping against a downwards intermediate trendline (blue).

Bullish momentum is gathering and the rest is to see if the 1.37630 highs can be broken

A lack of more conviction from buyers could leave the pair ranging for the day – For future outlooks, keep an eye on the action being constrained within the 4H MA 200 (as support – 1.3699) and the 4H MA 50 as resistance (1.3783)

Breaking below the pivot zone would also mean a re-entry of the June/July range between 1.3550 to 1.3750.

Key levels for the pair

Support Levels:

- range highs turned pivot 1.3750

- Intermediate support Zone 1.3660

- 1.3550 (2025 Lows, Main Support)

Resistance Levels:

- 1.3850 Main Resistance

- 1.38 intermediate Resistance

- 1.3783 4H MA 50

USDCAD 1H Chart

USDCAD 1H Chart, August 8, 2025, Source: TradingView

Buyers are stepping in strong – For the rest of the price action, the element to track is whether buyers break the imminent downwrads trendline that is just getting tested.

Daily highs: 1.3773

Daily lows: 1.3722

Safe Trades!

Canada’s Economy Sheds Jobs in July, Unemployment Rate Steady as Labour Force Shrinks

Canada's economy lost 41k jobs on net in July (-0.2% month/month), weaker than consensus expectations. The details were similarly weak, with job losses concentrated in full-time positions (-51k) and in the private sector (-39K).

The unemployment rate held steady at 6.9% in June, as the labour force shrunk (-33k). Despite the flat headline, the share of people who have been unemployed long term (>27 weeks) was the highest since 1998 at 23.8%.

Youth bore the brunt of a cooler labour market on the month (-34k, -1.2% m/m). Younger Canadians continue to face a tough job market, with the unemployment rate at 14.6%, the highest since 2010 (ex-pandemic).

Job losses were broad-based across goods and services sectors. The biggest losses were seen in information, culture and recreation (-29k, -3.3% m/m), construction (-22k, -1.3% m/m), business building and other support services (-19k, -2.8% m/m) and health care and social assistance (-17k, +0.6% m/m). Notable job gains were seen in transportation and warehousing (+26k, +2.4% m/m).

Wage growth was steady in July. Average hourly wages rose 3.3% versus a year ago, up slightly from 3.2% in June.

Key Implications

Canada's labour market gave back half of June's outsized job gains in July. Employment tallies have always been volatile in the Labour Force Survey, with the unemployment rate being the key metric to watch. The unemployment rate did hold steady, but given it was due to declining labour force participation, is not a very positive sign. We expect the stagnation in labour force growth to continue, which will keep the unemployment rate from rising too high, despite weak labour demand.

The Bank of Canada has a fair bit of time before it's next rate setting date on September 17th. Today's jobs report likely won't move the needle much on the Bank's thinking on the economy relative to its recent monetary policy report. We think a strong argument for further rate cuts remains in Canada, we'll see if the BoC agrees.

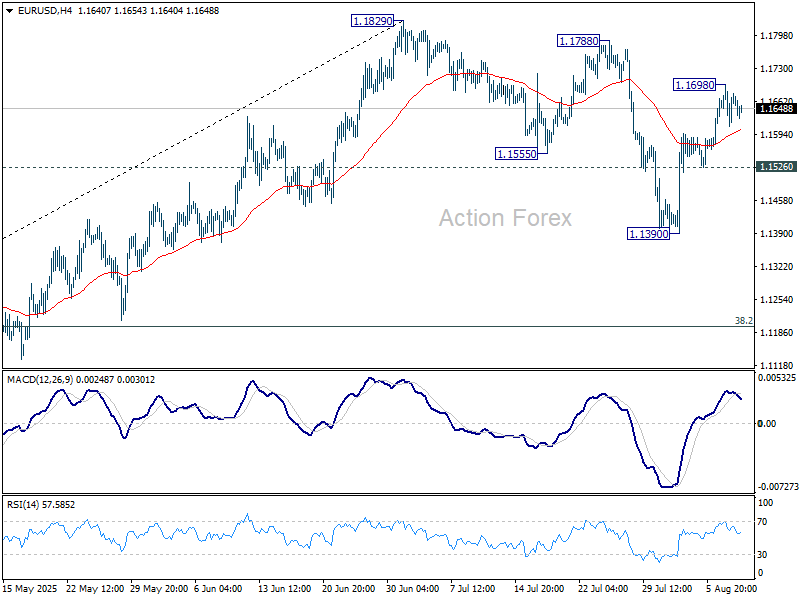

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1617; (P) 1.1658; (R1) 1.1705; More...

Intraday bias in EUR/USD is turned neutral first with 4H MACD crossed below signal line. Further rise is expected as long as 1.1526 support holds. As noted before, correction from 1.1829 should have completed with three waves down to 1.1390. Above 1.1698 will target 1.1788/1820 resistance zone. On the downside, however, break of 1.1526 minor support will dampen this view and bring retest of 1.1390 instead.

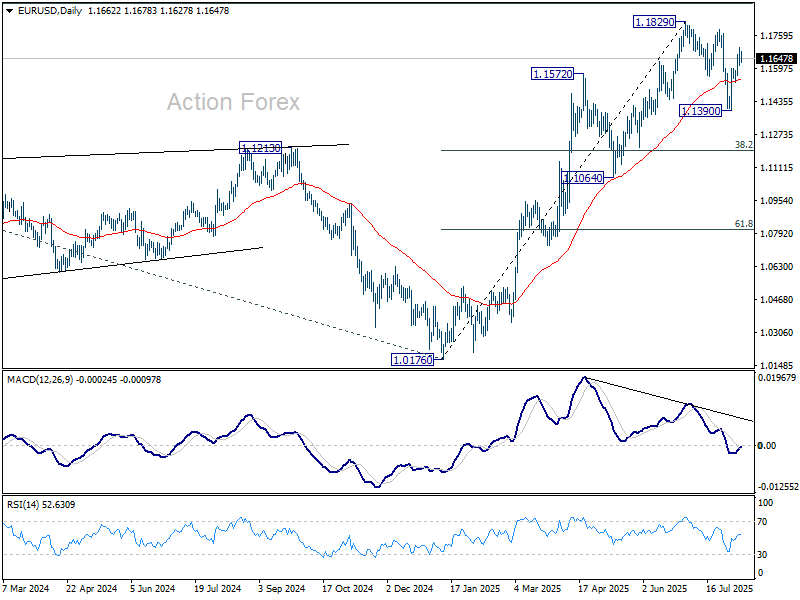

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will remain the favored case as long as 1.1604 support holds.

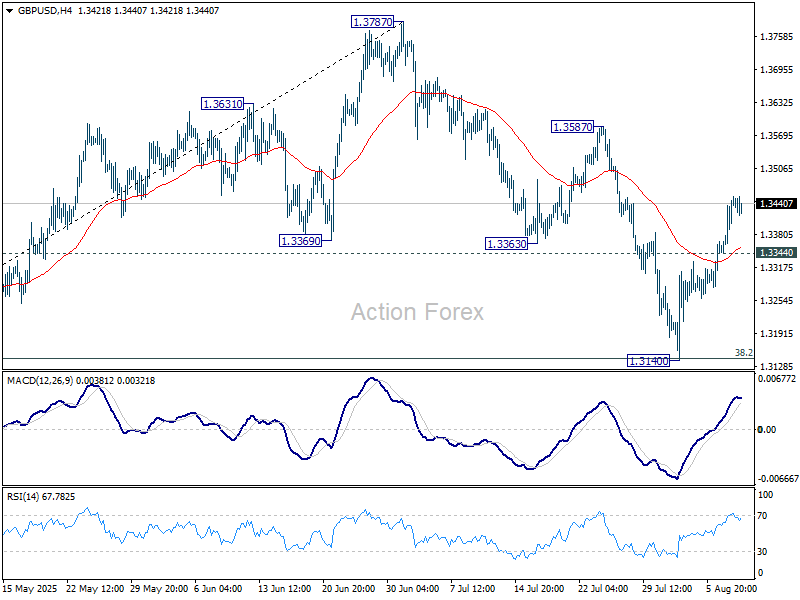

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3371; (P) 1.3410; (R1) 1.3484; More...

GBP/USD's rise from 1.3140 is in progress and intraday bias stays on the upside. As noted before, correction from 1.3787 should have completed with three waves down to 1.3140. Further rise should be seen to 1.3587 resistance. Firm break there will target 1.3787 high. On the downside, below 1.3344 minor support will turn intraday bias neutral again first.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.3049) holds, even in case of deep pullback.

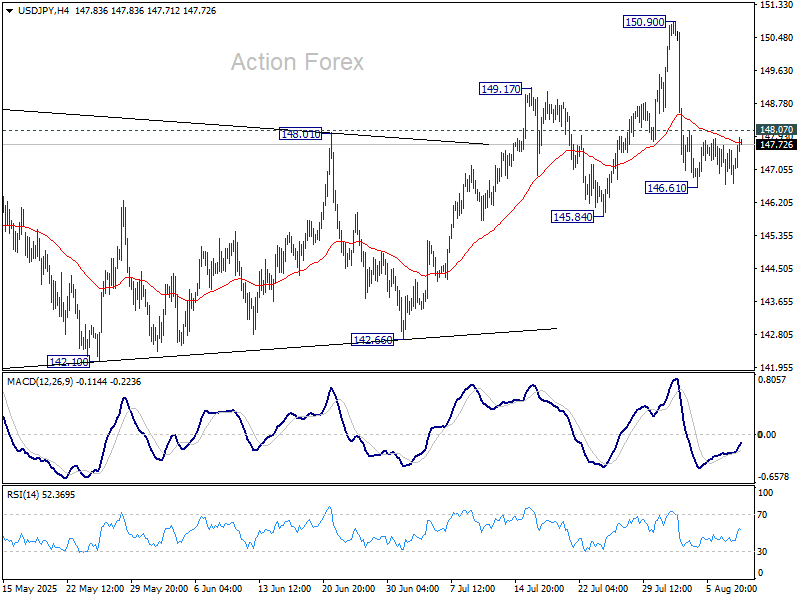

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 146.66; (P) 147.18; (R1) 147.68; More...

Sideway trading continues in USD/JPY and intraday bias remains neutral. As long as 145.84 support holds, larger rebound from 139.87 is still in favor to continue. On the upside, above 148.07 minor resistance will bring stronger rebound back to retest 150.90. However, on the downside, firm break of 145.84 support will argue that whole rise from 139.87 might have already completed. Deeper fall should then be seen to 142.66 support for confirmation.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 will argue that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. In case the corrective pattern extends with another fall, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.

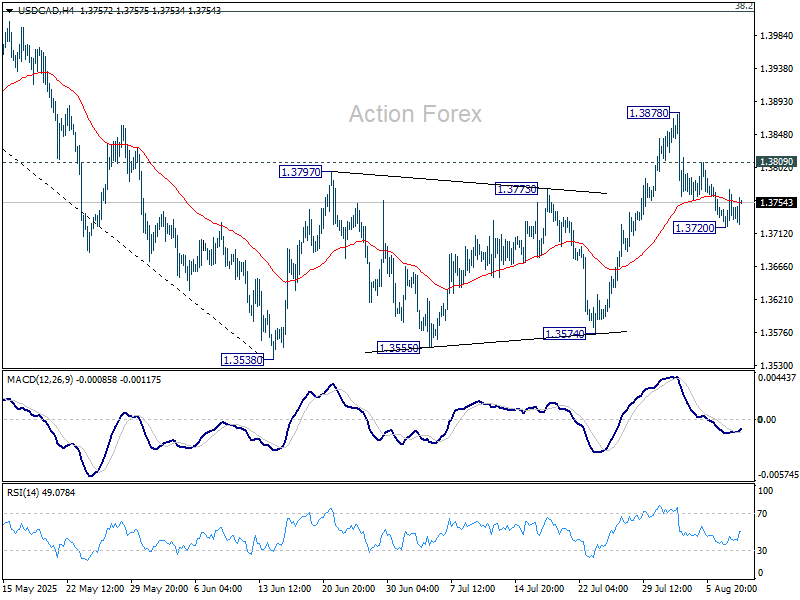

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3723; (P) 1.3748; (R1) 1.3775; More...

Intraday bias in USD/CAD is turned neutral first with 4H MACD crossed above signal line. On the downside, below 1.3720 will affirm the case that corrective rebound from 1.3538 has completed at 1.3878. Deeper fall should then be seen to retest 1.3538 low. On the upside, however, above 1.3809 will dampen this view, and turn bias back to the upside for retesting 1.3878 instead.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 resistance holds. Next target is 61.8% retracement of 1.2005 (2021 low) to 1.4791 at 1.3069.

Loonie Dips After Mixed Jobs Data, Loss Limited as BoC Caution Still in Play

Canadian Dollar edged lower in early US trading Friday following a mixed labor market report that offered little clarity on the BoC’s next move. The set of data suggests that slack is building, but not yet enough to trigger a policy response.

BoC left its benchmark rate unchanged at 2.75% last week for the third straight meeting, stating that a cut could be warranted if economic weakness deepens and inflationary pressures from global trade disruptions remain contained. Today’s report will add weight to those arguments, but with no surge in unemployment and wage pressures still evident, the central bank is expected to stay cautious.

Markets may start pricing in a higher probability of a rate cut in Q4, but an immediate policy shift remains unlikely. Loonie traders appear to be taking the data in stride, with USD/CAD holding within tight range, reflecting a wait-and-see stance.

Broader market moves were subdued heading into the weekend. Yen came under fresh pressure and is now the second worst performer on the week, trailing only Swiss Franc. Dollar is slightly firmer today but remains the third weakest major, still digesting recent dovish shifts in Fed expectations.

On the stronger side, Sterling continues to outperform, buoyed by the Bank of England’s hawkish rate cut this week. Aussie and Kiwi also remain firm. Euro and Loonie are trading in the middle of the pack, showing no strong directional bias.

Meanwhile, tensions between India and the US are escalating. In a rare public signal of protest, New Delhi has reportedly frozen plans to purchase US weapons and aircraft following US President Donald Trump’s decision to hike tariffs on Indian exports to 50%. A planned visit by Indian Defence Minister Rajnath Singh to Washington has also been scrapped according to media reports.

Canada’s jobs shrink -40.8k in July, wages growth pick up

Canada’s labor market surprised to the downside in July, shedding -40.8k jobs versus expectations of a 15.3k gain. The drop was led by a sharp decline in full-time employment (-51k), and offsetting some of June’s strong 83k rise. Overall job growth has stagnated, with employment up just 27k since January. However, the unemployment rate held steady at 6.9%, slightly better than the expected 7.0%.

Despite the headline job loss, average hourly wages rose 3.3% yoy in July, slightly up from June’s 3.2% yoy. Total hours worked dipped marginally by -0.2% mom, indicating flat momentum in overall labor output. The mixed signals—a steep fall in full-time jobs alongside rising wages—paint a complex picture for policymakers.

BoE's Pill questions cut pace, says inflation risks may delay easing

BoE Chief Economist Huw Pill signaled that the central bank may need to reconsider its steady pace of easing if shifts in longer-term inflation dynamics persist. In a briefing to business leaders, Pill acknowledged that inflation pressures are likely to keep easing, but warned that price- and wage-setting behavior" may delay further policy easing.

“That might lead us to... question whether the pace at which we're reducing Bank Rate... is sustainable,” he said, referencing the quarterly 25bps cut rhythm the BoE has maintained over the past year.

Pill's comments help clarify the reasoning behind Thursday’s unexpectedly tight 5–4 policy vote, where he and three other members dissented against the 25bps cut to 4.00%. The majority, including Governor Andrew Bailey, favored continuing the easing path. But the split exposed growing concern within the Monetary Policy Committee over stickier inflation risks. Pill said the more hawkish voters are focused on upside risks driven by behavioral shifts rather than headline inflation itself.

Traders are now pushing back expectations for the next cut, with futures no longer fully pricing a 25bps move before February. Pill's remarks reinforce the message that while policy is still on a downward path, the pace may slow if inflation proves more persistent beneath the surface.

BoJ Opinions: 2–3 months needed to Gauge Tariff impacts, year-end hike possible

BoJ’s July 30–31 Summary of Opinions revealed a broadly cautious stance on future policy moves, with members emphasizing the need for more data before shifting course.

Despite the recent US–Japan tariff agreement, board members reaffirmed that Japan’s baseline outlook has not improved. "Japan's economic growth will moderate and the improvement in underlying CPI inflation will be sluggish temporarily,” one policymaker said. Accordingly, the consensus was to maintain current interest rates and financial accommodation, while monitoring trade risks and external demand.

“At least two to three more months are needed to assess the impact of US tariff policy,” one member stated, noting that the direction of US monetary policy and exchange rates could also shift materially depending on inflation and labor conditions.

Still, the door is now open for rate hikes later this year. The Summary suggests that if incoming data shows resilience in the US economy—and Japan avoids major trade fallout—the BoJ could resume policy normalization as soon as year-end.

“It may be possible for the Bank to exit from its current wait-and-see stance, perhaps as early as the end of this year,” one policymaker said. That prospect keeps the door open to further hikes in late 2025 if inflation and growth align.

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3723; (P) 1.3748; (R1) 1.3775; More...

Intraday bias in USD/CAD is turned neutral first with 4H MACD crossed above signal line. On the downside, below 1.3720 will affirm the case that corrective rebound from 1.3538 has completed at 1.3878. Deeper fall should then be seen to retest 1.3538 low. On the upside, however, above 1.3809 will dampen this view, and turn bias back to the upside for retesting 1.3878 instead.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 resistance holds. Next target is 61.8% retracement of 1.2005 (2021 low) to 1.4791 at 1.3069.

Canada’s jobs shrink -40.8k in July, wages growth pick up

Canada’s labor market surprised to the downside in July, shedding -40.8k jobs versus expectations of a 15.3k gain. The drop was led by a sharp decline in full-time employment (-51k), and offsetting some of June’s strong 83k rise. Overall job growth has stagnated, with employment up just 27k since January. However, the unemployment rate held steady at 6.9%, slightly better than the expected 7.0%.

Despite the headline job loss, average hourly wages rose 3.3% yoy in July, slightly up from June’s 3.2% yoy. Total hours worked dipped marginally by -0.2% mom, indicating flat momentum in overall labor output. The mixed signals—a steep fall in full-time jobs alongside rising wages—paint a complex picture for policymakers.

BoE’s Pill questions cut pace, says inflation risks may delay easing

BoE Chief Economist Huw Pill signaled that the central bank may need to reconsider its steady pace of easing if shifts in longer-term inflation dynamics persist. In a briefing to business leaders, Pill acknowledged that inflation pressures are likely to keep easing, but warned that price- and wage-setting behavior" may delay further policy easing.

“That might lead us to... question whether the pace at which we're reducing Bank Rate... is sustainable,” he said, referencing the quarterly 25bps cut rhythm the BoE has maintained over the past year.

Pill's comments help clarify the reasoning behind Thursday’s unexpectedly tight 5–4 policy vote, where he and three other members dissented against the 25bps cut to 4.00%. The majority, including Governor Andrew Bailey, favored continuing the easing path. But the split exposed growing concern within the Monetary Policy Committee over stickier inflation risks. Pill said the more hawkish voters are focused on upside risks driven by behavioral shifts rather than headline inflation itself.

Traders are now pushing back expectations for the next cut, with futures no longer fully pricing a 25bps move before February. Pill's remarks reinforce the message that while policy is still on a downward path, the pace may slow if inflation proves more persistent beneath the surface.

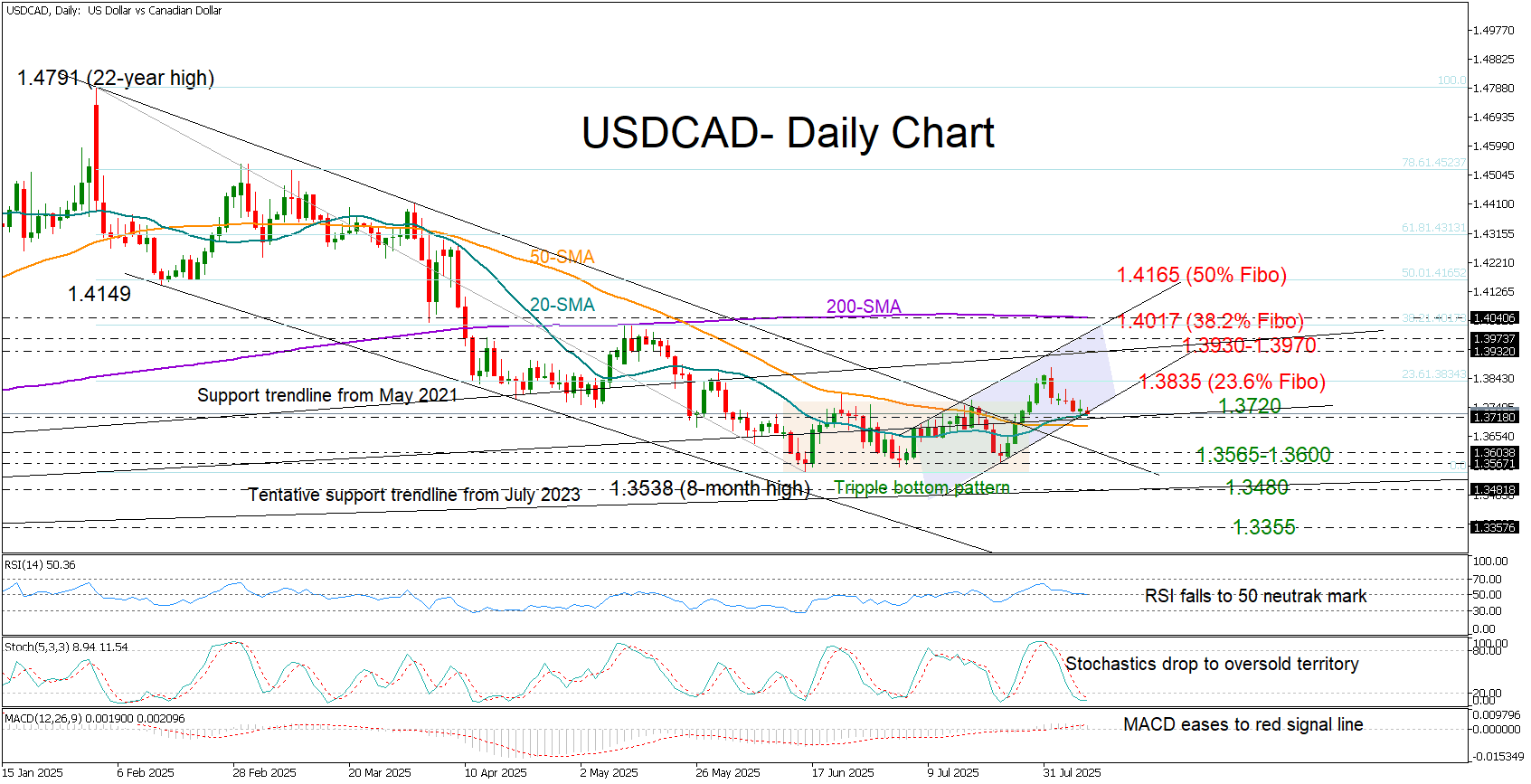

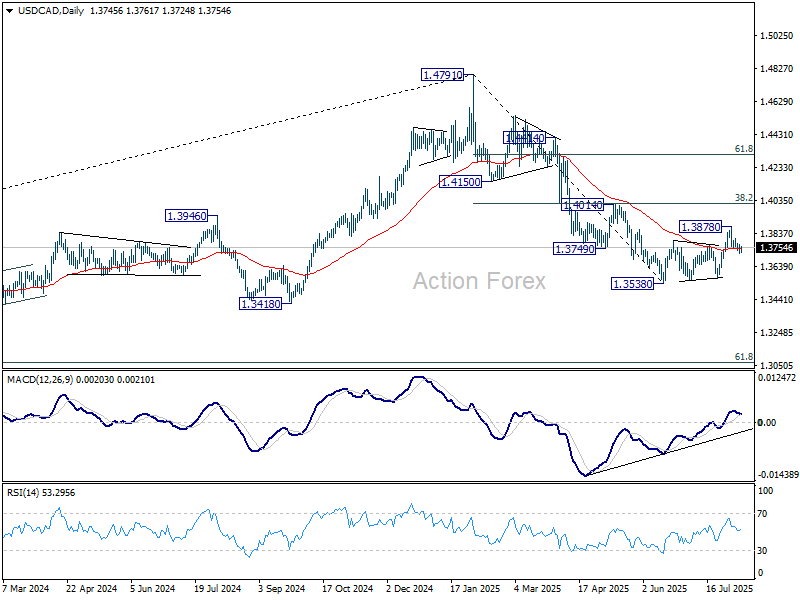

Has USD/CAD Found the Next Bull Trigger?

- USDCAD lacks momentum but maintains hopes for a positive reversal.

- Market action tests a make-or-break point near 1.3720.

USD/CAD has traded quietly this week, slipping from 1.3800 to 1.3720 despite steep US import tariffs of 10–40% kicking in against countries without trade deals. Canadian employment data due today could still inject volatility before the weekend, with the unemployment rate expected to rise to 7.0% for the first time in four years.

Although bullish momentum has been lacking lately, the pair appears to have laid the groundwork for a potential positive trend reversal. Having confirmed a bullish triple-bottom pattern, the price posted a new higher high near 1.3877 before upside pressures were capped by the 23.6% Fibonacci retracement level of the 2025 downtrend near 1.3835. The bullish crossover between the 20- and 50-day SMAs is adding to the constructive signals, with the price now seeking fresh buying interest near the protective 20-day SMA and the constraining trendline from July 2023 at 1.3720.

The stochastic oscillator suggests that the latest decline is overdone and that a pivot higher could be imminent. However, the downward slope in both the RSI and MACD indicates that momentum could stay weak.

If the pair manages to break above the 1.3835 barrier, the next hurdle could appear within the April–May range of 1.3930–1.3970. Slightly higher, the 200-day SMA and the 38.2% Fibonacci level at 1.4017 could challenge any attempt at a full bullish trend reversal above May’s high.

On the downside, a close below the 50-day SMA at 1.3685 could trigger another critical test near the 1.3600 level and the triple-bottom area of 1.3565. If this floor gives way, the tentative support trendline from July 2023 at 1.3480 could prevent a deeper fall towards the January 2024 base near 1.3355.

In summary, USD/CAD bulls have not yet surrendered to the bears. The 1.3720 zone could still serve as a springboard for a renewed positive trajectory.