Sample Category Title

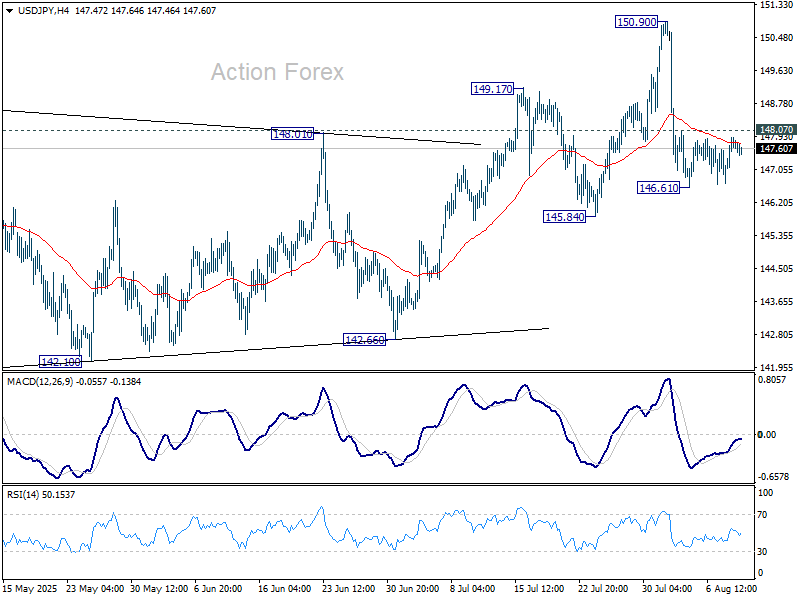

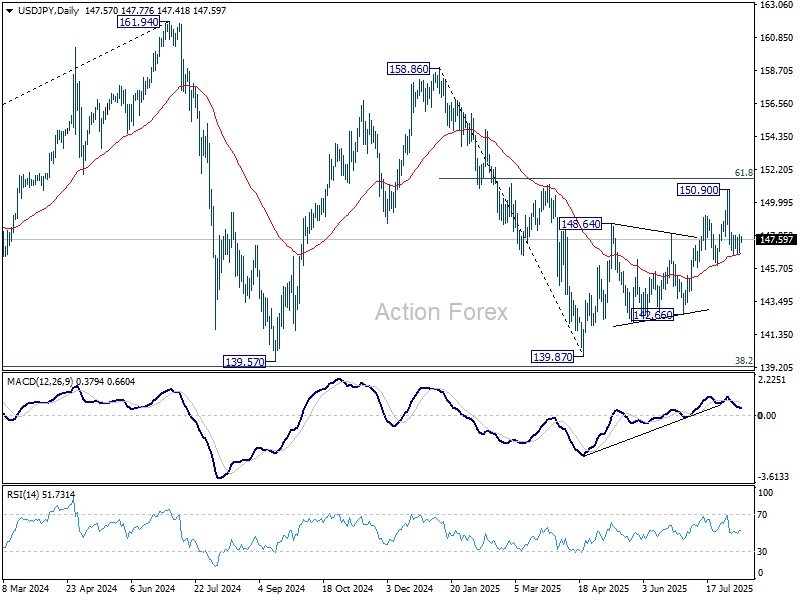

USD/JPY Daily Outlook

Daily Pivots: (S1) 147.00; (P) 147.45; (R1) 148.18; More...

Intraday bias in USD/JPY stays neutral and outlook is unchanged. As long as 145.84 support holds, larger rebound from 139.87 is still expected to continue. On the upside, above 148.07 minor resistance will bring retest of 150.90 high first. However, decisive break of 145.84 will indicate near term bearish reversal and target 142.66 support next.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 will argue that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. In case the corrective pattern extends with another fall, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.

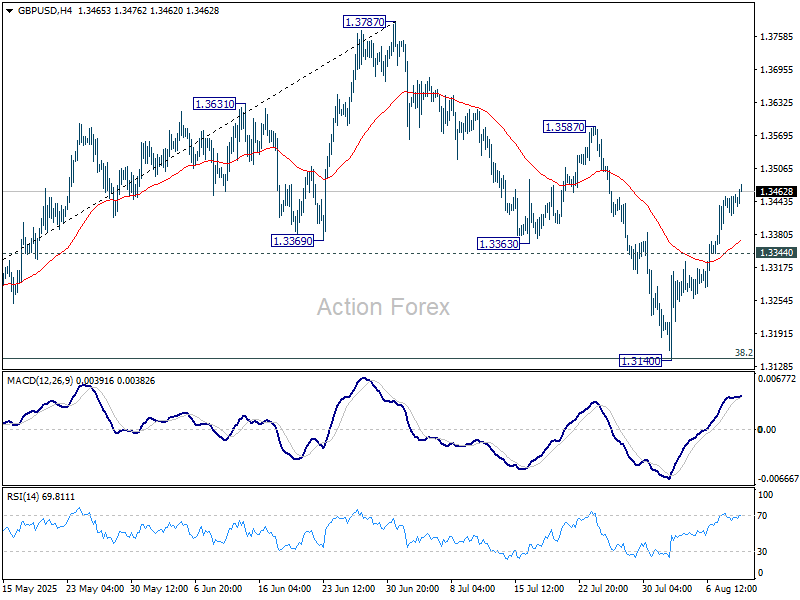

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3426; (P) 1.3442; (R1) 1.3467; More...

Intraday bias in GBP/USD stays on the upside this point. Correction from 1.3787 should have completed with three waves down to 1.3140. Further rally should be seen to 1.3587 resistance first. Firm break there will pave the way to retest 1.3787 high. However, break of 1.3344 minor support will dampen this bullish case and turn bias neutral again first.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.3055) holds, even in case of deep pullback.

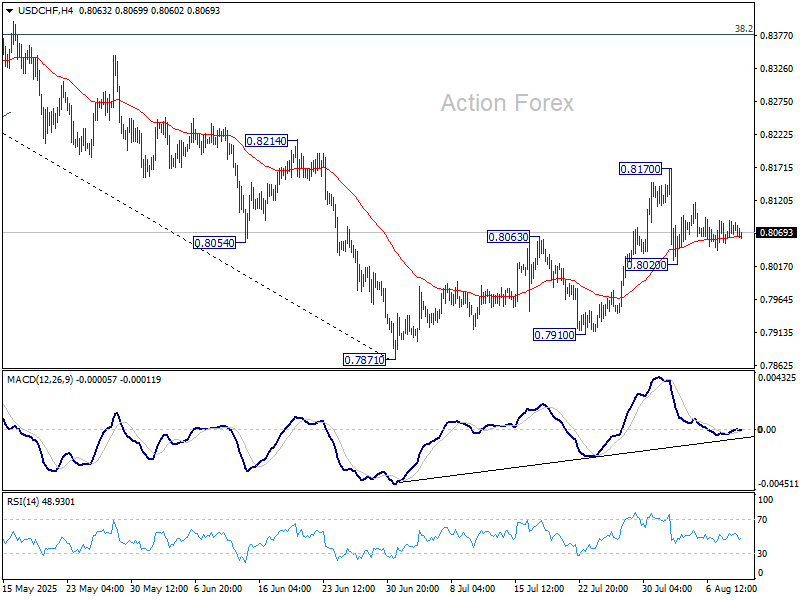

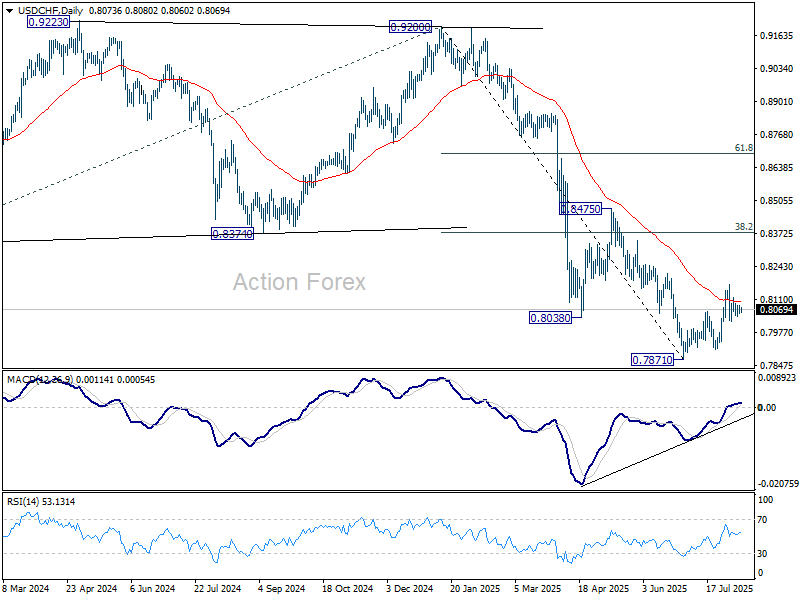

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8061; (P) 0.8075; (R1) 0.8098; More….

Intraday bias in USD/CHF stays neutral for the moment. On the downside, break of 0.8020 will solidify the case that corrective pattern from 0.7871 has completed at 0.8170. Further fall should be seen back to retest 0.7871 low. However, break of 0.8710 will resume the corrective rise towards 38.2% retracement of 0.9200 to 0.7871 at 0.8379.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8475 resistance holds.

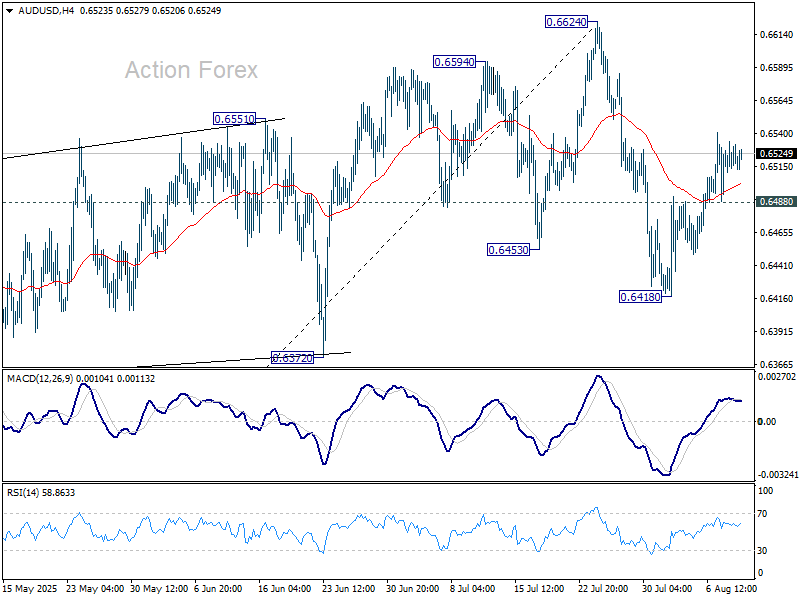

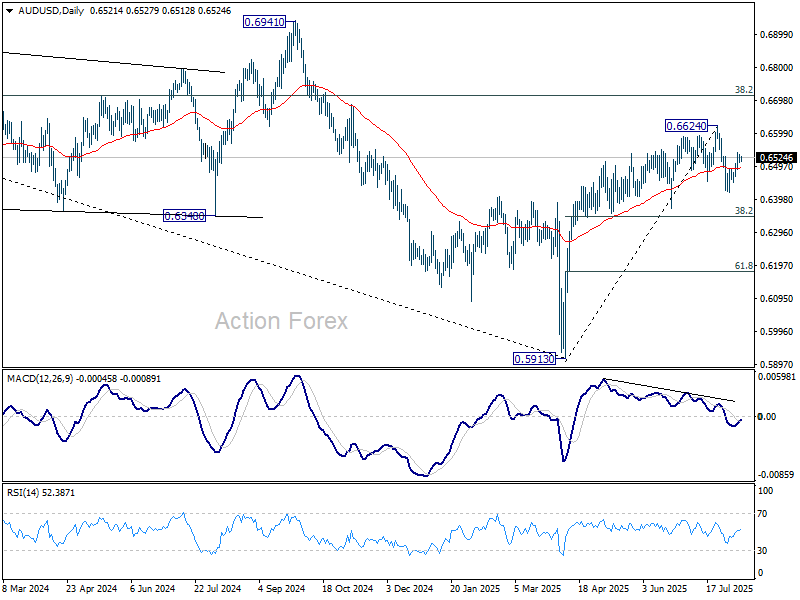

AUD/USD Daily Report

Daily Pivots: (S1) 0.6508; (P) 0.6522; (R1) 0.6536; More...

Intraday bias in AUD/USD remains mildly on the upside at this point. Corrective fall from 0.6624 could have completed at 0.6418 already. Further rise would be seen to retest this high. On the downside, however, firm break of 0.6449 will argue that the pattern from 0.6624 is extending with another falling leg. Break of 0.6418 will target 38.2% retracement of 0.5913 to 0.6624 at 0.6352.

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. While stronger rally cannot be ruled out, outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, even in case of another fall through 0.5913, downside should be contained above 0.5506 (2020 low).

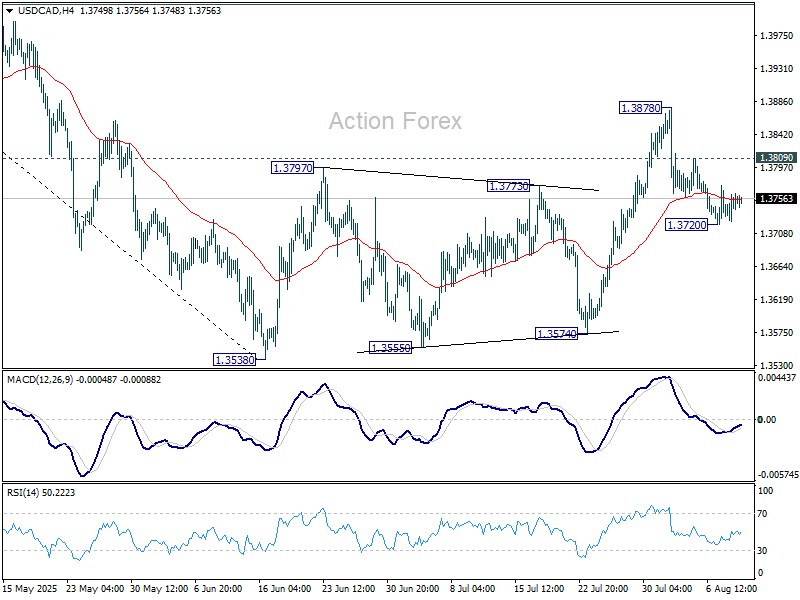

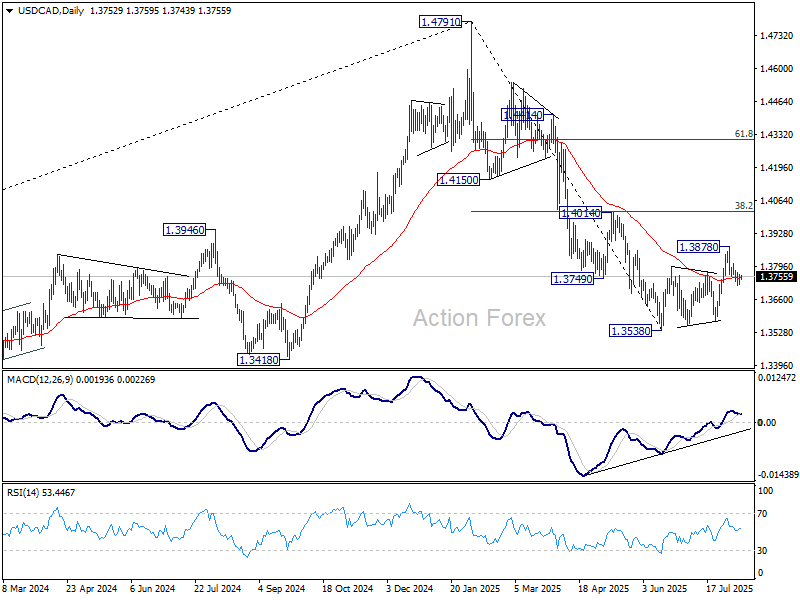

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3733; (P) 1.3748; (R1) 1.3771; More...

Intraday bias in USD/CAD remains neutral at this point. On the downside, break of 1.3720 will reaffirm the case that corrective pattern from 1.3538 has completed at 1.3878. Further decline should then be seen back to retest 1.3538 low. However, break of 1.3809 will bring retest of 1.3878. Further break there will extend the corrective rebound from 1.3538 with another rising leg.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 resistance holds. Next target is 61.8% retracement of 1.2005 (2021 low) to 1.4791 at 1.3069.

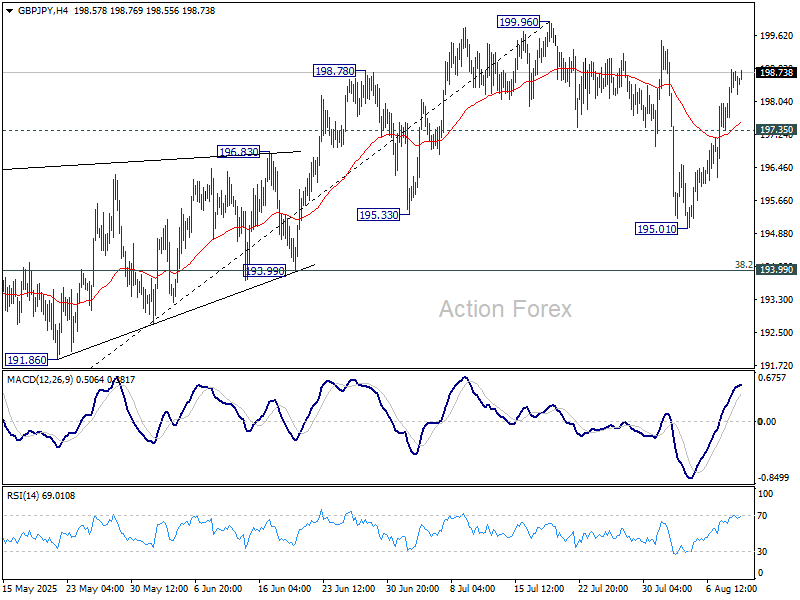

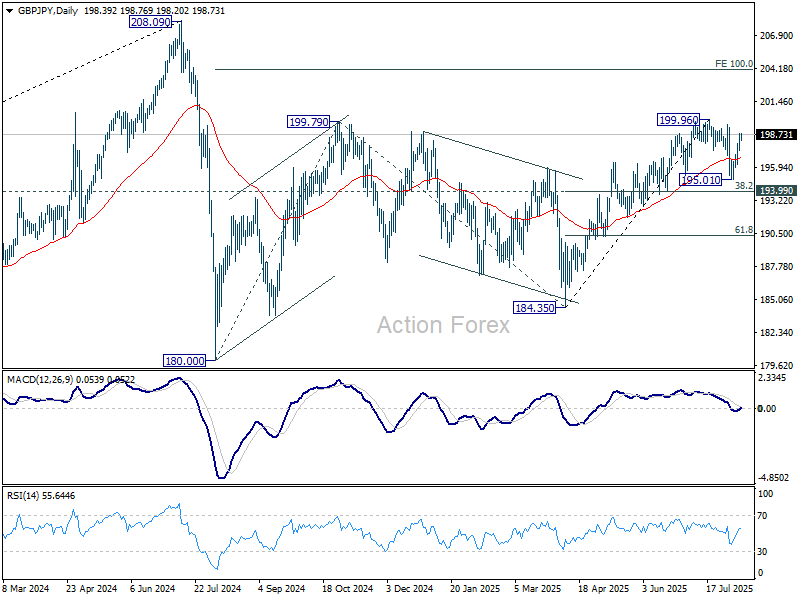

GBP/JPY Daily Outlook

Daily Pivots: (S1) 197.75; (P) 198.29; (R1) 199.20; More...

Intraday bias in GBP/JPY stays on the upside for retesting 199.96 resistance first. Decisive break there resume whole rise from 184.35. Next target is 100% projection of 180.00 to 199.79 from 184.35 at 204.14. On the downside, below 197.35 minor support will delay the bullish case and turn intraday bias neutral again. In this case, corrective pattern from 199.96 would extend with another falling leg.

In the bigger picture, price actions from 208.09 (2024 high) are seen as a correction to rally from 123.94 (2020 low). The pattern might still extend with another falling leg. But in that case, strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. Meanwhile, decisive break of 208.09 will confirm long term up trend resumption.

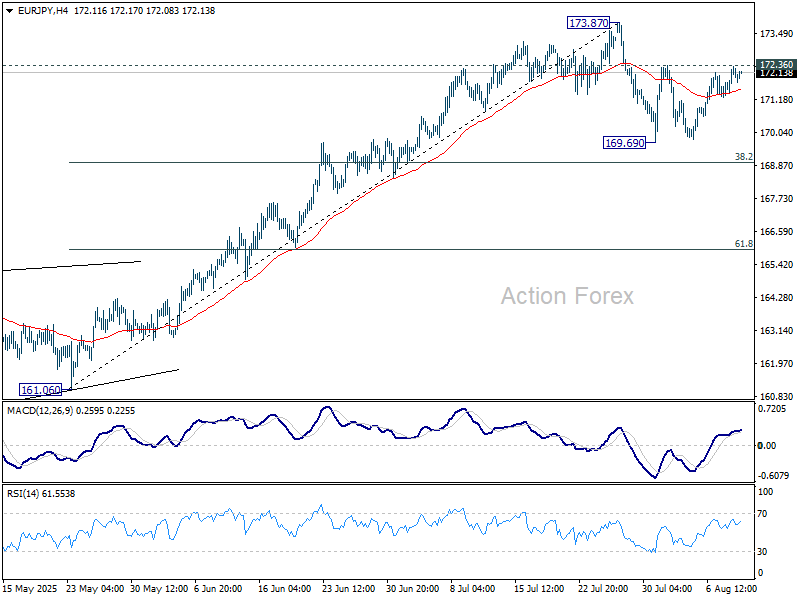

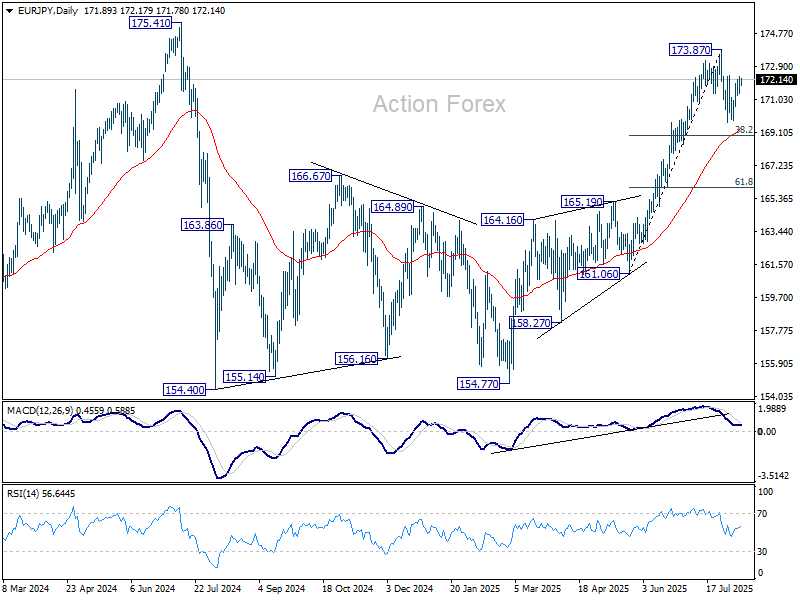

EUR/JPY Daily Outlook

Daily Pivots: (S1) 171.46; (P) 171.91; (R1) 172.44; More...

Intraday bias in EUR/JPY stays neutral as range trading continues. Corrective pattern from 173.87 could extend lower. But downside should be contained by 38.2% retracement of 161.06 to 173.87 at 168.97 to bring rebound. On the upside, above 172.36 will bring retest of 173.87 first. Firm break there will resume larger rally from 154.77 to retest 175.41 high.

In the bigger picture, considering current strong momentum as seen in the rally from 154.77, corrective pattern from 175.41 could have already completed. Decisive break of 154.77 will confirm long term up trend resumption. Next target is 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. However, rejection by 175.41, followed by firm break of 55 D EMA (now at 169.27) will delay this bullish case.

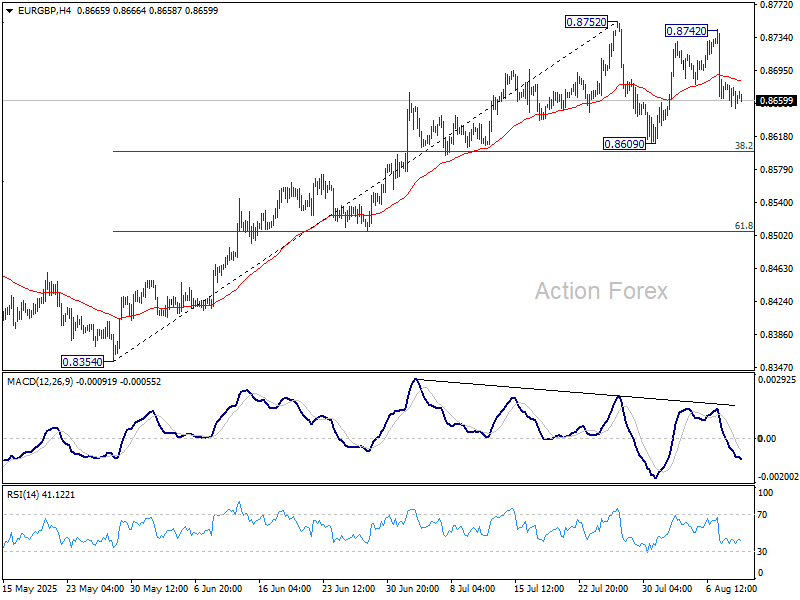

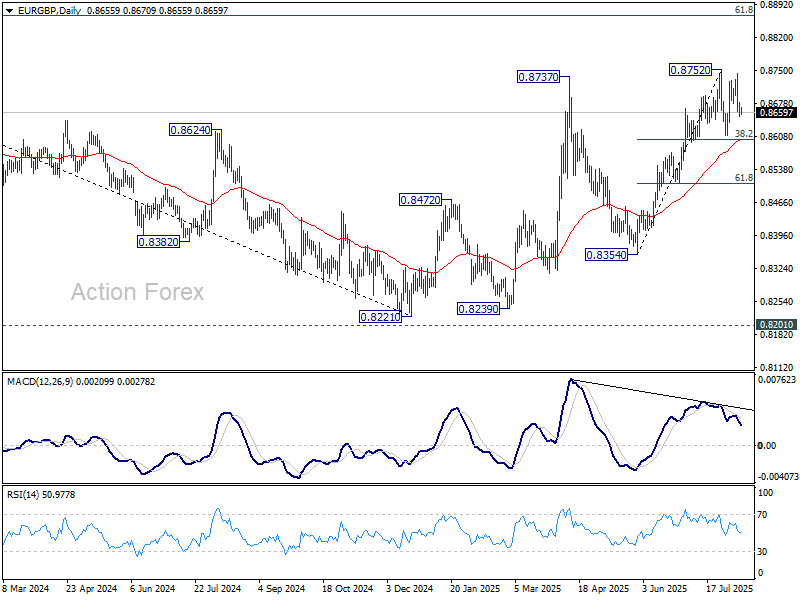

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8645; (P) 0.8664; (R1) 0.8675; More...

Consolidation from 0.8752 short term top is still extending and intraday bias in EUR/GBP remains neutral. Downside should be contained by 38.2% retracement of 0.8354 to 0.8752 at 0.8600. On the upside, firm break of 0.8752 will resume the rise from 0.8354 towards 0.8867 fibonacci level.

In the bigger picture, the structure from 0.8221 medium term bottom are not impulsive enough to suggest that it's reversing the down trend from 0.9267 (2022 high). But even if it's a correction, further rise is expected to 61.8% retracement of 0.9267 to 0.8221 at 0.8867. This will remain the favored case as long as 55 W EMA (now at 0.8497) holds.

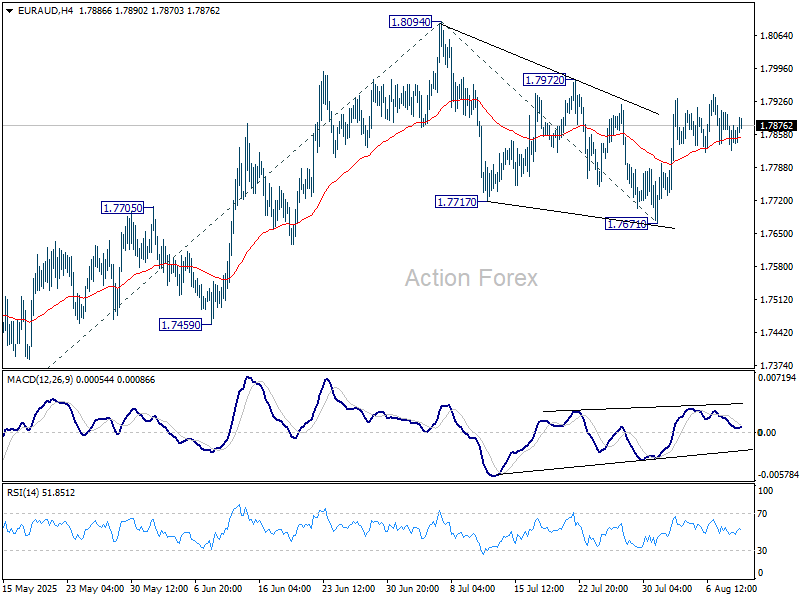

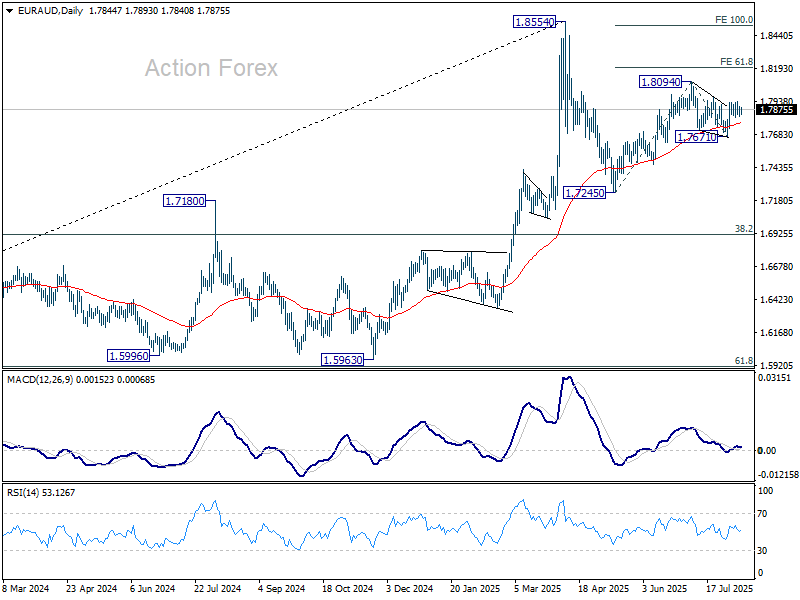

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7813; (P) 1.7863; (R1) 1.7900; More...

Range trading continues in EUR/AUD and intraday bias remains neutral. On the upside, firm break of 1.7972 resistance should confirm that corrective pattern from 1.8094 has completed at 1.7671. Further rise should then be seen through 1.8094, to resume the rebound from 1.7245. Next target is 61.8% projection of 1.7245 to 1.8094 from 1.7671 at 1.8196. On the downside, below 1.7671 will bring deeper fall back to 1.7459 support instead.

In the bigger picture, price actions from 1.8554 medium term top are seen as a corrective pattern. Such pattern could extend further with another falling leg. But even in that case, downside should be contained by 38.2% retracement of 1.4281 (2022 low) to 1.8554 at 1.6922 to bring rebound. Uptrend from 1.4281 is expected to resume at a later stage.

Pay to Play

The week starts with gains in most Asian indices, and futures are in the positive in the early hours of the trading week. The S&P 500 posted its strongest week since late June on the back of robust earnings, further appetite for technology stocks, and hopes of progress in the Ukrainian war. Trade and tariff chaos have been, for now, left behind – which has translated into improved sentiment in the Stoxx 600, although the concrete implications will come to investors’ attention in waves as data flows in and shows the damage.

But this Monday morning, attention is on Ukraine and optimism that there could be progress. Gold is trading lower, and crude oil is under pressure. The price of a barrel finally cleared a critical Fibonacci support last week, near the $65.20pb level, and is now in a medium-term bearish consolidation zone with trend and momentum indicators suggesting room for a deeper slide, while the RSI indicator is not yet near the oversold level. The ample supply and cloudy demand outlook support the bearish camp, yet any disappointment on the Ukraine front could rapidly reverse the latest decline and send the price of a barrel back above the $65pb level.

Falling energy prices is good news for inflation watchers: they should help keep inflation in check, and that’s important for those expecting the Federal Reserve (Fed) to cut interest rates as early as next month. This week, the US will reveal its most-watched CPI figures. Both headline and core CPI are expected to have risen in July; core inflation remains sticky near the 3% level – above the Fed’s 2% policy target – which in normal times should justify a ‘no cut’ from the Fed next month. But alas, times are not normal, and the increasing pressure from the White House – along with the replacement of outgoing members by dovish, White House-friendly members – suggests that rate cuts will come, no matter what. Whether they could ease borrowing costs is yet to be seen.

If inflation is higher than expected, investors will likely scale back September cut expectations and send the US 2-year yield higher. If the data points to lower-than-expected numbers, investor reaction could be two-sided: either they believe the numbers are accurate and top up dovish Fed expectations – which would result in lower short-term yields – or they will question the accuracy of the government data after the BLS chief was fired two Fridays ago for having announced unpleasant revisions to US jobs data. For now, the US 2-year yield is recovering the post-NFP decline, the US dollar remains under pressure from dovish Fed expectations, the majors including the EURUSD and Cable extend gains, while the USDJPY continues to see resistance near the 148 level.

In individual news, the big story of the day is that Nvidia and AMD will pay 15% of their Chinese chip sales to the US government, according to the FT — an effort to reduce export-restriction risks toward China and increase visibility on their Chinese revenues. The idea of paying the US government to soften export policies — originally designed to control national-security risks — is an unusual move. If the US government is willing to exchange national-security risks for money, that would be good news for Nvidia and AMD. However, this arrangement will hardly guarantee the end of export restrictions, as the US government is not primarily driven by financial considerations — especially when it comes to national security issues.

TSMC shares – seen this morning as a proxy for market reaction to the news – are up by more than 1%, hinting that investors fully back the companies’ tolerance for lower margins on their Chinese business if it means more stability on the business front.

Now that we’re in the tech space, AI investors will be watching CoreWeave earnings this week – an AI-cloud company backed by Nvidia that recently went public and had a rough summer. The company is expected to announce around $1bn in revenue, a loss of roughly $0.20, and a high concentration of clients – as 77% of its revenue came from Microsoft and OpenAI last quarter. But the data-center business, energy, and cybersecurity are the backbones of AI adoption. If you like AI, you should also have exposure to these essential side sectors. Note that cybersecurity stocks have been under pressure this summer, partly due to macro and rate risks, but also due to seasonal weakness and because they’re in the middle of a firewall refresh cycle. Price pullbacks could be an interesting opportunity to strengthen exposure.