Sample Category Title

US CPI Release: Bullish Chance for Dollar

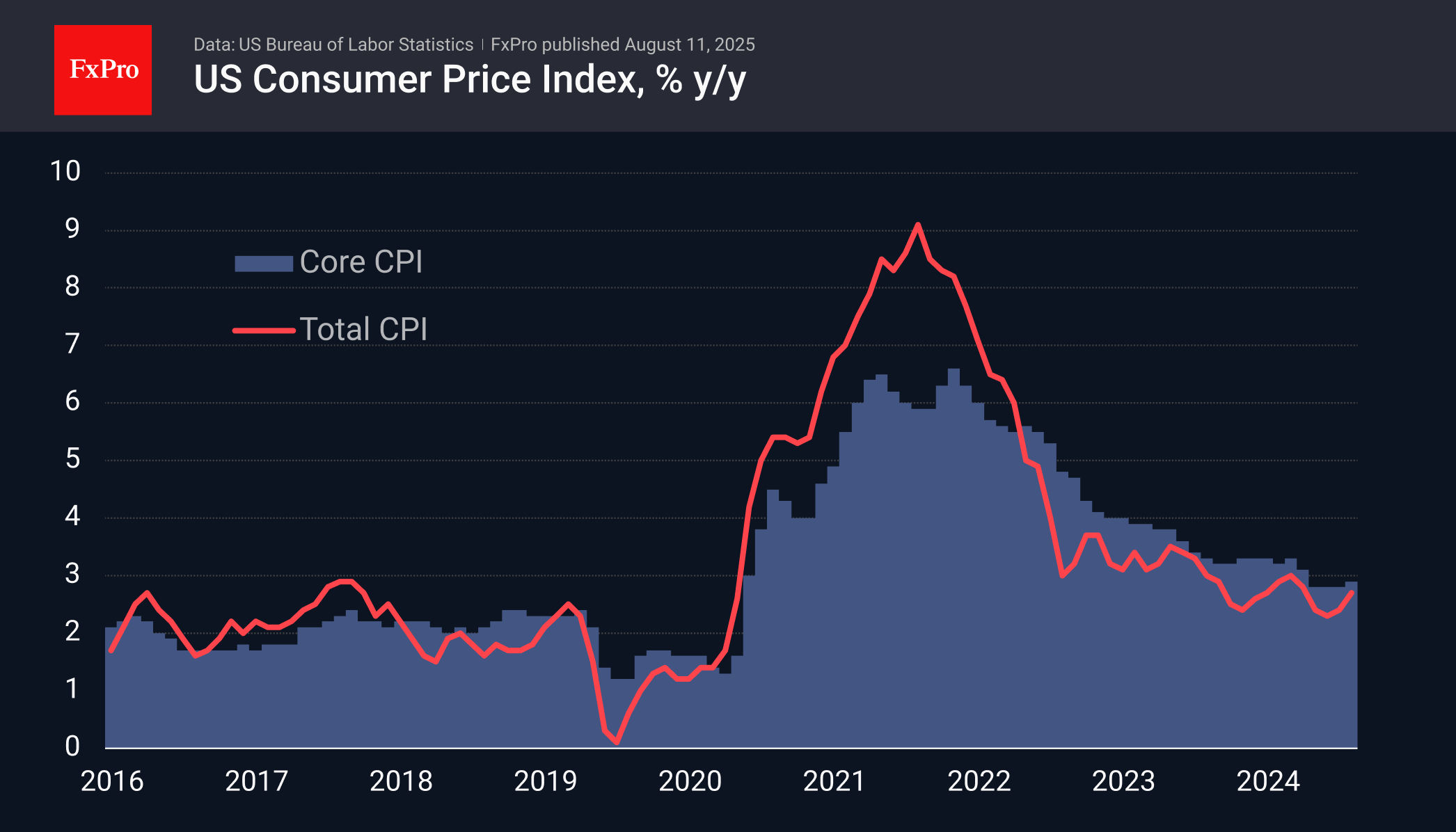

On Tuesday, US consumer inflation data for July will be released, which will largely determine the fate of the key rate cut in September.

The overall consumer price index in the US accelerated its annual growth from 2.3% to 2.7% in June, and analysts expect it to accelerate to 2.8%. Excluding food and energy prices, it is anticipated to accelerate to 3.0% y/y. In both cases, this will be the highest rate since February.

Since the beginning of the year, inflation reports have been below expectations, which could potentially negatively affect the dollar if this trend continues.

But it is also worth considering Powell’s warning at the end of July that the tariff-induced surge in prices has only just begun to gain momentum. An acceleration above expectations could bring back trading on the markets based on expectations of a rate cut in September.

Interest rate futures are pricing in an 86% chance of easing in September (up from over 90% a week ago). Still, an acceleration in headline CPI to 3% could well reduce that chance to 50%, providing a foundation for a dollar recovery.

US Dollar Finds Support Ahead of US CPI

The US Dollar is starting the week on a steadier footing after lagging through much of last week, weighed down by a string of underwhelming US data releases.

Traders now turn their attention to a pivotal stretch for inflation figures, with CPI due Tuesday (consensus: +0.2% m/m, +2.8% y/y) and PPI on Thursday (consensus: +0.3% m/m, +2.5% y/y) and expectations are for high volatility: Markets and central banks all want to know more on the US Economy as the infamous Trump tariffs are finally in place.

Major pairs like EUR/USD and GBP/USD have seen sharp appreciation on the back of recent USD weakness, but that rally now faces a test.

With key data looming, uncertainty is creeping back in and imposes to have a look on the Dollar Index as the week gets underway.

Dollar Index Multi-timeframe checkup ahead of tomorrow's CPI release

Dollar Index Daily Chart

Dollar Index Daily Chart, August 11, 2025 – Source: TradingView

After last week's trough in the DXY, sold off due to the consecutive NFP and PMI misses, buyers started to step in mean-reversion style.

Forming a low around the 98.00 handle with the 50-Day MA acting as immediate support, the buying is still a bit superficial as markets will want to see how inflation data lands.

A stronger than expected CPI will take out some of the pricing for a September cut.

Anything above 0.3% should strengthen the USD strongly which should have a negative effect on equities.

A miss on the other hand will turn the concerns to employment.

FED speak had expressed that US companies are for now absorbing the higher costs but we should see this effect spreading to consumer prices progressively as profit margins get squeezed.

Dollar Index 4H Chart

Dollar Index 4H Chart, August 11, 2025 – Source: TradingView

The US Dollar has formed an intermediate upwards channel confirmed after the most recent 97.95 Friday bottom.

USD Bulls will have to hold above the Friday lows to avoid a more bearish outlook which should see other majors rallying strongly against it – Everything will depend on tomorrow's data.

In the meantime, the Greenback is held between the 200-period MA and the 50-MA, monitor both for breakouts.

RSI momentum is back to neutral, allowing more potential volatility.

Dollar Index 1H Chart

Dollar Index 1H Chart, August 11, 2025 – Source: TradingView

After a bullish NA weekly open for the USD, buyers are facing the 98.50 Pivot Zone leading to some ongoing consolidation.

Expect a balanced price action in the waiting of the key data, particularly as RSI is coming close to overbought in the shorter timeframes.

The 50-H MA is acting as support at 98.20 while the 200-H MA acts as the next resistance at 98.85 – the rest of the action will have to be weighted depending on the potential USD Sellers at the current pivot zone.

If they do show up, expect rangebound action between this morning's 98.510 highs and the 50-H MA.

Safe Trades and successful trading week!

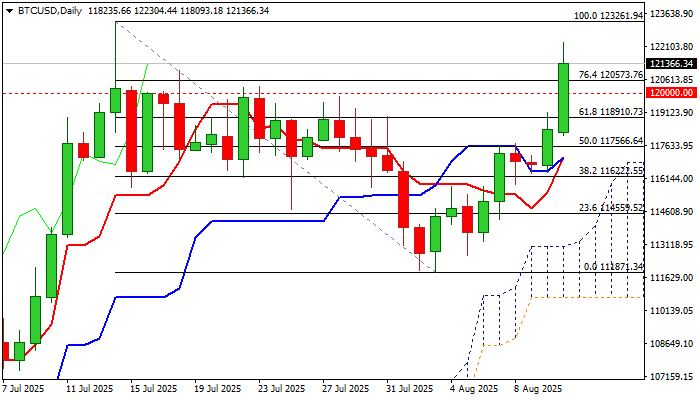

BTCUSD – Bulls Accelerate Through 120K and Near All-Time High

BTCUSD surged through psychological 120K barrier and hit the highest in almost one month (122300) on Monday.

Recovery leg from 112K zone (higher base / the bottom of pullback from new record high) has strongly accelerated in past two sessions and retraced over 76.4% of 123261/111871 pullback), generating signal that corrective phase might be over soon.

The recent rally was driven by fresh institutional purchases, growing expectations of Fed rate cuts (following the latest disappointing numbers from US labor sector) as lower rates and weaker dollar are supportive factors, with broader support provided by significant positive changes in the US legislation of crypto markets.

Return above 120K added to positive technical picture (the price action remains underpinned by ascending and thickening daily cloud / converged daily Tenkan/Kijun-sen about to for a bull-cross and strong positive momentum) however, overbought stochastic warns that bulls may face headwinds on approach to key resistance (new record high).

This is already visible on hourly chart as the price eased from session high, with corrective action expected to stay above broken 120K level (reverted to solid support) to keep larger bulls intact for fresh push higher and potential attack at 123261 top.

Break higher will confirm strong bullish stance and push the price into uncharted territory, with Fibo projections (126000, 127600) and psychological 130K barrier, marking next targets.

Res: 122300; 123261; 126000; 127600

Sup: 120573; 120000; 118910; 118000

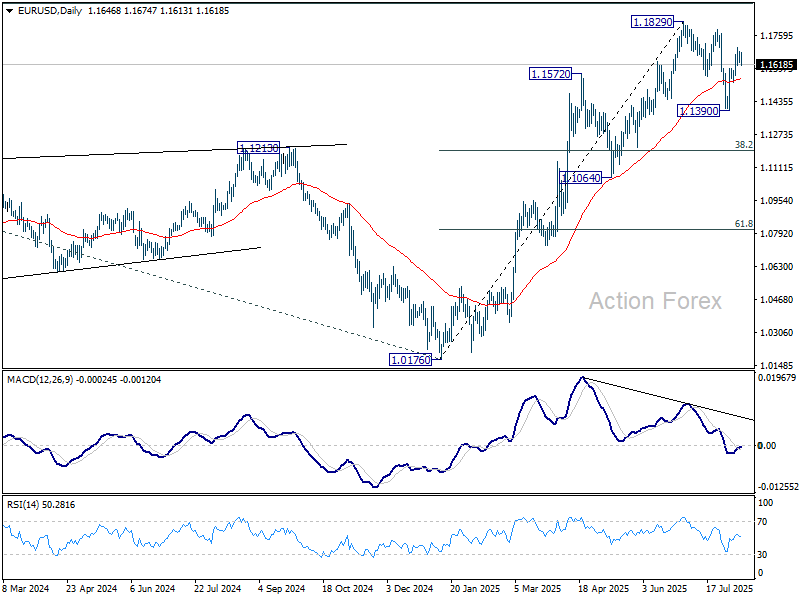

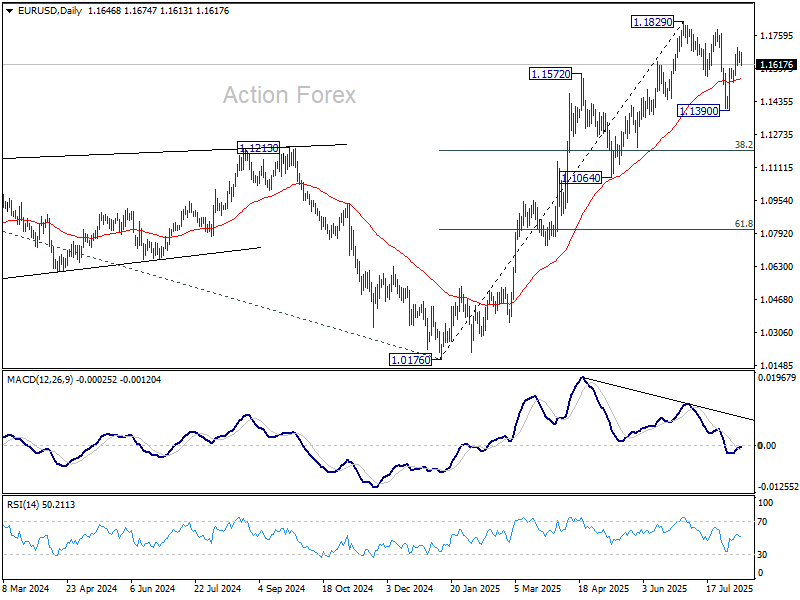

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1621; (P) 1.1650; (R1) 1.1671; More...

Intraday bias in EUR/USD remains neutral and more consolidations would be seen below 1.1698 temporary top. Outlook is unchanged that correction from 1.1829 should have completed with three waves down to 1.1390. Above 1.1698 will bring retest of 1.1829. However, break of 1.1526 support will dampen this bullish view and bring deeper fall back to 1.1390 instead.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will remain the favored case as long as 1.1604 support holds.

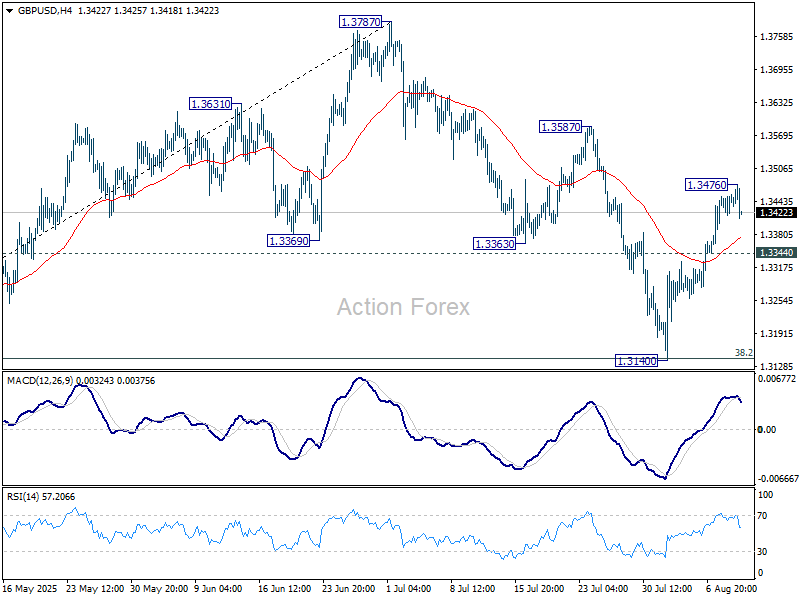

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3426; (P) 1.3442; (R1) 1.3467; More...

Intraday bias in GBP/USD is turned neutral first with current retreat. Some consolidations would be seen but further rally is expected as long as 1.3344 minor support holds. Correction from 1.3787 should have completed with three waves down to 1.3140. Above 1.3476 will target 1.3587 resistance first. However, break of 1.3344 minor support will dampen this bullish case, and turn bias to the downside for deeper fall.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.3068) holds, even in case of deep pullback.

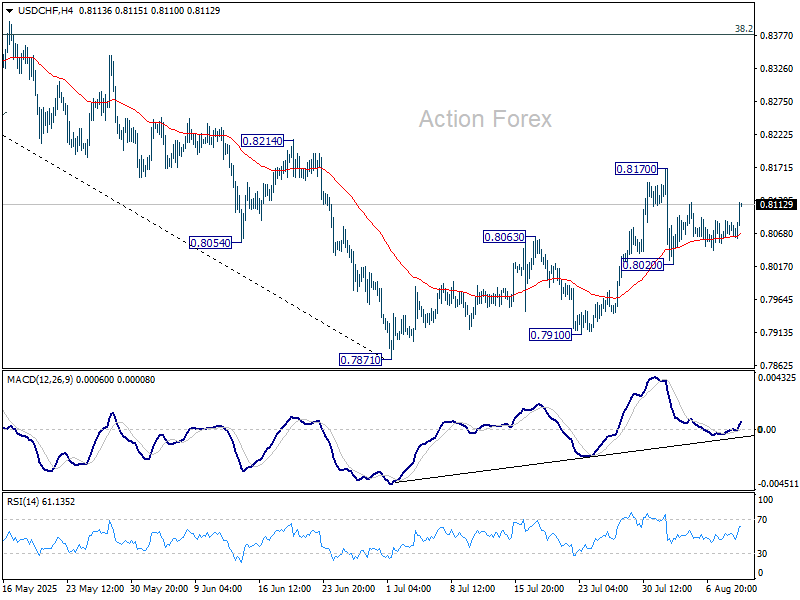

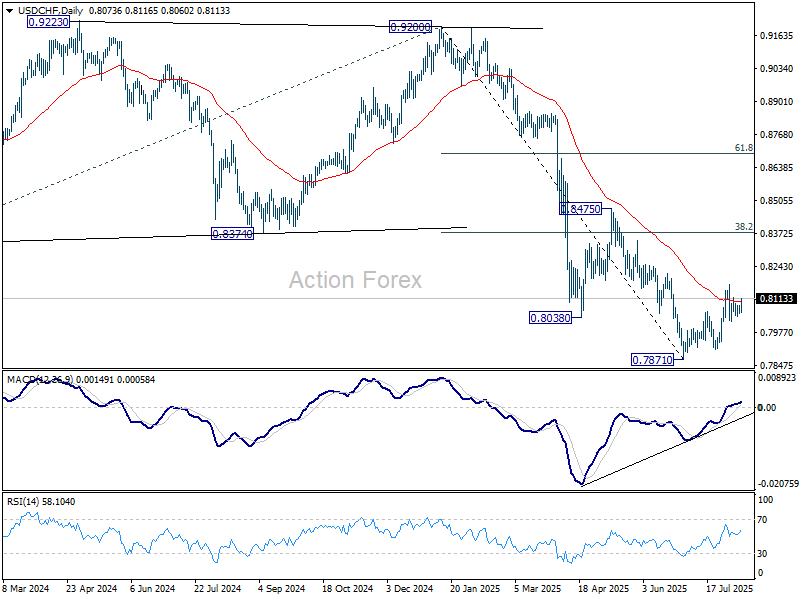

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8061; (P) 0.8075; (R1) 0.8098; More….

USD/CHF is still bounded in range of 0.8020/8170, and intraday bias remains neutral. On the downside, break of 0.8020 will solidify the case that corrective pattern from 0.7871 has completed at 0.8170. Further fall should be seen back to retest 0.7871 low. However, break of 0.8710 will resume the corrective rise towards 38.2% retracement of 0.9200 to 0.7871 at 0.8379.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8475 resistance holds.

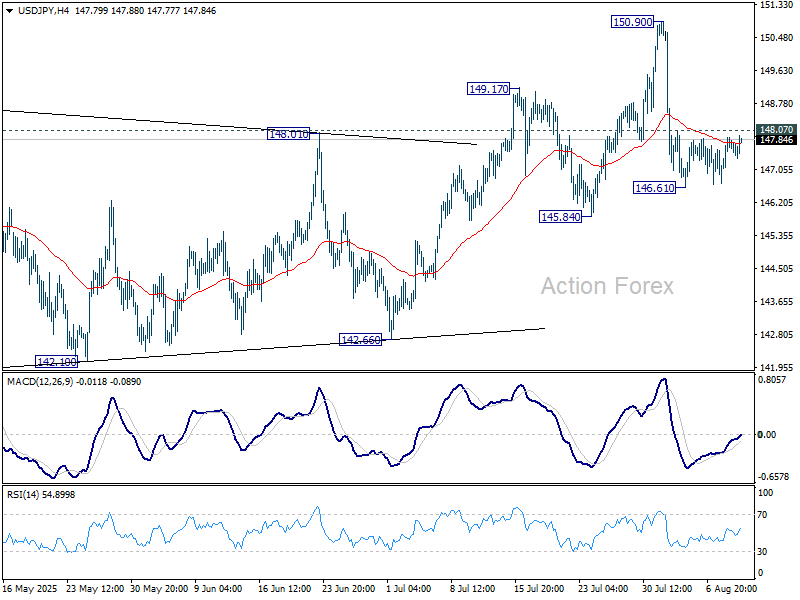

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 147.00; (P) 147.45; (R1) 148.18; More...

USD/JPY recovers mildly today but stays below 148.07 minor resistance. Intraday bias remains neutral at this point. Intraday bias in USD/JPY stays neutral and outlook is unchanged. As long as 145.84 support holds, larger rebound from 139.87 is still expected to continue. On the upside, above 148.07 minor resistance will bring retest of 150.90 high first. However, decisive break of 145.84 will indicate near term bearish reversal and target 142.66 support next.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 will argue that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. In case the corrective pattern extends with another fall, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.

Greenback Leads Ahead of Trump’s China Tariff Call, RBA Cut in Focus

Dollar rebounded strongly as US session begins, despite a day largely devoid of fresh headlines or major data. Traders are looking ahead to a week dominated by trade, geopolitical, and central bank risks, particular with the August 12 US–China tariff deadline now in sharp focus.

So far, US President Donald Trump has offered little clarity on whether he will extend the current truce. Following the latest bilateral meeting in Stockholm in July, Beijing struck an optimistic tone, signalling that both sides were working toward a 90-day extension. US negotiators, however, have left the decision squarely in Trump’s hands.

A potential deal could see China committing to increase purchases of US goods — particularly energy, agricultural products, and, if permitted, semiconductors and chipmaking equipment. Trump, in a Sunday post, pressed for China to “quickly quadruple its soybean orders.”

One sticking point remains China’s purchases of Russian oil, which Trump has threatened to punish with additional tariffs. Whether he acts on that threat may hinge on the outcome of his summit with Russian President Vladimir Putin in Alaska later this week, where a possible Russia–Ukraine ceasefire is the main focus.

Attention is also on the widely expected RBA rate cut in the upcoming Asian session. The central bank left rates unchanged last month, with Governor Michele Bullock framing the decision as a matter of “timing rather than direction,” pending more evidence that inflation was falling.

The latest quarterly data from the ABS showed headline inflation easing to 2.1% from 2.4%, and trimmed mean inflation slipping to 2.7% from 2.9% — both within the 2–3% target band. The conditions should be well set for RBA to resume policy easing.

Yet policy calls are complicated by the RBA’s restructured Monetary Policy Board, which since April has comprised nine members: three internal (Bullock, Deputy Governor Andrew Hauser, and Treasury Secretary Steve Kennedy) and six external members.

With external members holding the majority and few making public remarks, consensus-building is opaque. That lack of visibility contributed to last month’s surprise 6–3 vote to hold rates steady. While inflation data now give the RBA room to cut, the internal–external split adds an element of uncertainty to Tuesday’s decision.

For the day so far, Dollar leads the major currency pack, followed by Yen and Euro. Kiwi is the weakest performer, ahead of the Swiss Franc and Aussie. Sterling and Loonie are trading in the middle.

In Europe, at the time of writing, FTSE is up 0.36%. DAX is down -0.17%. CAC is down -0.24%. UK 10-year yield is down -0.039 at 4.565. Germany 10-year yield is up 0.004 at 2.693. Earlier in Asia, Japan was on holiday. Hong Kong HSI rose 0.19%. China Shanghai SSE rose 0.34%. Singapore Strait Times fell -0.17%.

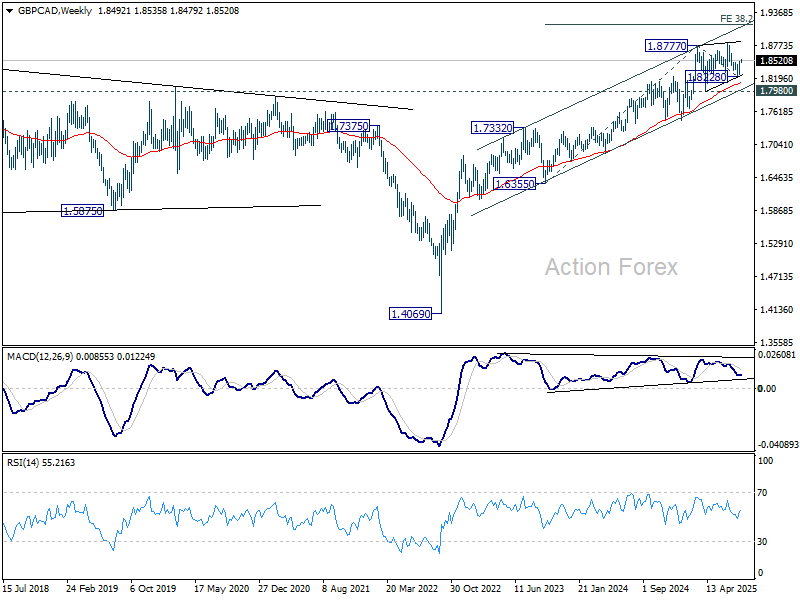

GBP/CAD rising towards 1.8830 as UK jobs and GDP awaited

GBP/CAD built on last week’s strong rebound as trading opened this week, with technical signals pointing to a retest of the recent high at 1.8830 as next step. The near-term direction will hinge partly on UK data, with employment figures due Tuesday and June GDP on Thursday.

Last week’s narrow 5–4 BoE vote to cut the Bank Rate to 4.00% highlighted the divide within the MPC, and the interplay between economic resilience and sticky inflation will remain the key driver.

Market consensus still favors a gradual “one cut per quarter” easing path from the BoE. A solid GDP print combined with firm labor market data — especially upside surprises in wage growth — could strengthen the hawkish camp’s argument to keep the pace steady, if not slower.

Technically, GBP/CAD’s break of 1.8484 resistance confirms that the fall from 1.8830 bottomed at 1.8228. The corrective pattern from 1.8777 also appears to have completed a three-wave correction at that low. Further rise should be seen to retest 1.8830 next. Firm break there will resume larger up trend to 38.2% projection of 1.6355 to 1.1877 from 1.8228 at 1.9153.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 147.00; (P) 147.45; (R1) 148.18; More...

USD/JPY recovers mildly today but stays below 148.07 minor resistance. Intraday bias remains neutral at this point. Intraday bias in USD/JPY stays neutral and outlook is unchanged. As long as 145.84 support holds, larger rebound from 139.87 is still expected to continue. On the upside, above 148.07 minor resistance will bring retest of 150.90 high first. However, decisive break of 145.84 will indicate near term bearish reversal and target 142.66 support next.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 will argue that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. In case the corrective pattern extends with another fall, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.

UK Wage Growth Expected to Ease, Pound Steady

The British pound is showing limited movement on Monday. In the European session, GBP/USD is trading at 1.3455, up 0.05% on the day.

The Bank of England is keeping a close eye on two key fronts as it charts a rate path - inflation and employment. The BoE lowered rates last week in a decision that raised a lot of eyebrows since it took an unprecedented two rounds of voting to reach the decision. The close 5-4 vote points to dissension among MPC members as how best to proceed.

Four members voted to hold rates and they can defend their case by pointing to rising inflation. The five members who voted in favor of cutting rates were more focused on the weakening labor market, especially slowing pay growth.

UK wage growth expected to ease

Wage growth will again be in focus on Tuesday, with the release of the employment report. Wages including bonuses is expected to drop to 4.7% in the three months to June, down from 5.0% in the previous release. The unemployment rate is expected to remain steady at 4.7%, the highest level in almost four years.

The BoE meets next on September 18 but the three-way split in the August decision will make it difficult to predict what will happen at the September meeting. Inflation has been moving higher but most members still voted in favor of a rate cut, focusing more on the weakening labor market than on rising inflation.

In the US, it's a very light calendar with no tier-1 events. On Tuesday, the US releases CPI for July, which is expected to tick up to 2.8% from 2.7% in June.

GBP/USD Technical

- GBP/USD has pushed above resistance at 1.3434 and is testing 1.3450. Next, there is resistance at 1.3463

- 1.3421 is providing resistance

GBPUSD 4-Hour Chart, Aug. 11, 2025