Sample Category Title

US core PCE holds at 2.8%, income and spending rebound

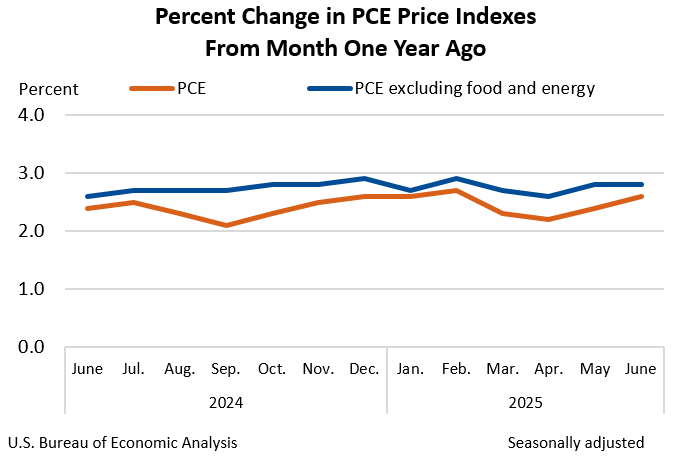

Fed’s preferred inflation gauge offered little relief in June, with the core PCE index holding at 2.8% yoy, above market expectations of 2.7% yoy. Headline PCE inflation also rose more than expected from 2.4% yoy to 2.6% yoy. Both monthly readings stood at 0.3% mom, reinforcing the message that price pressures are proving sticky and raising questions about the timing of any Fed rate cuts.

On the household front, income and spending showed modest improvement. Personal income climbed 0.3% mom, rebounding from a surprise decline in May. Personal spending rose by the same margin, albeit slightly below the 0.4% mom forecast. The recovery suggests consumers remain active, but the slight miss in spending hints at growing sensitivity to price levels and borrowing costs.

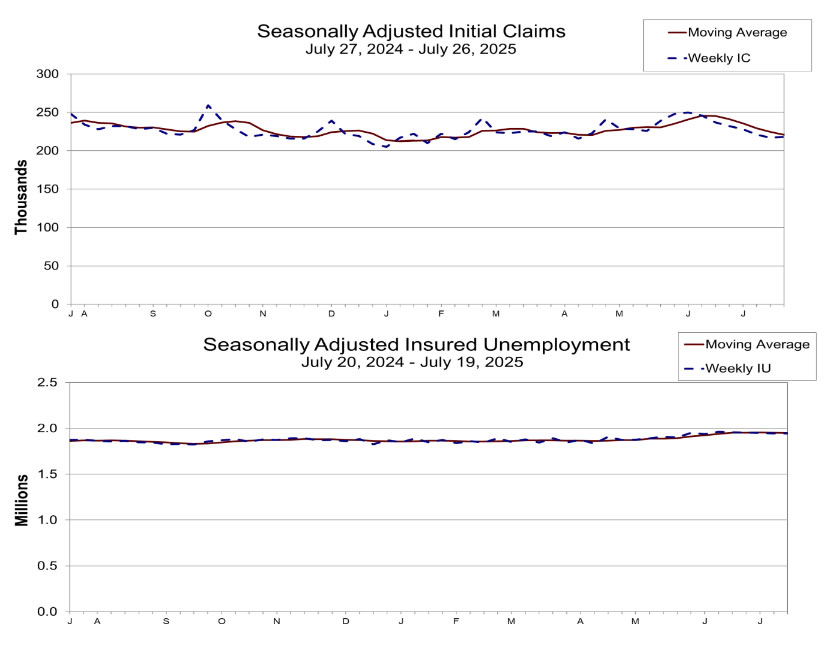

Labor data, however, remained steady: initial jobless claims edged up by 1 to 218k and continuing claims were flat at 1.946 million—consistent with a still-solid employment backdrop.

Altogether, the mixed bag of sticky inflation, resilient income, and cautious consumption leaves the Fed on hold, with markets still uncertain about the case for a September rate cut.

European data wrap: German CPI and Swiss retail surprise to upside

European data released today pointed to continued labor market resilience and upside surprises on inflation.

Eurozone unemployment rate held steady at 6.2% in June, defying expectations of a slight uptick to 6.3%. Across the broader EU, the jobless rate was unchanged at 5.9%, underscoring continued employment strength despite trade disruptions and slowing manufacturing activity.

In Germany, inflation pressures were firmer than expected. Headline CPI rose 0.3% mom in July, outpacing consensus for a 0.2% rise. Annual inflation held at 2.0% yoy, above the expected 1.8% yoy, suggesting steady underlying pressures even amid weaker growth. Import prices were flat on the month, beating forecasts for a modest decline of -0.2% mom, potentially limiting some disinflation via exchange rate channels.

Separately, Switzerland surprised to the upside with a 3.8% yoy surge in June retail sales, well above the 0.2% yoy consensus. The data offers a counterpoint to concerns about weakening domestic demand in the region and may reinforce the case for a patient SNB as it weighs the need to bring back negative rate.

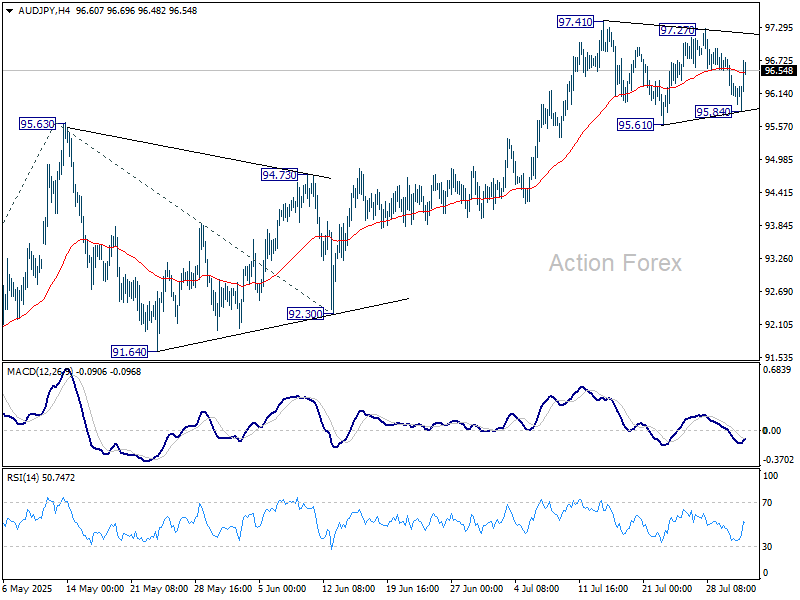

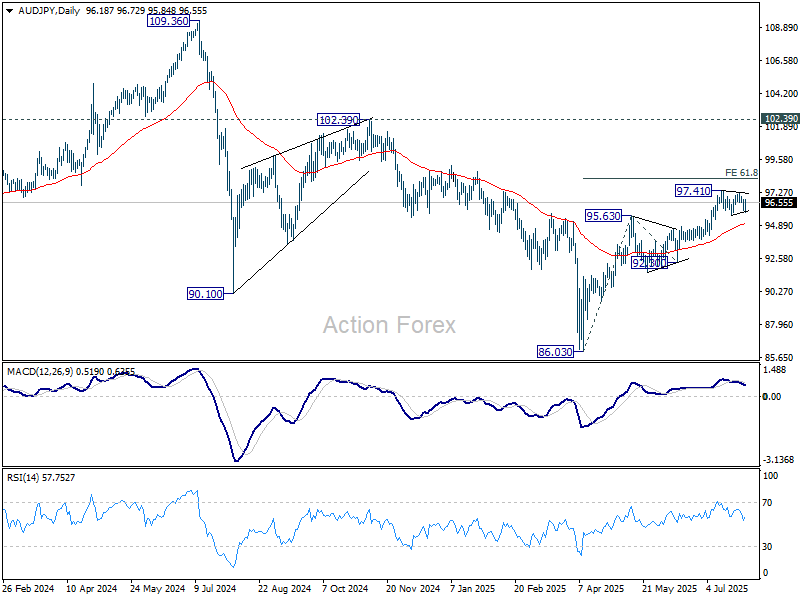

AUD/JPY reasserts bullish bias, as BoJ seen in no rush to hike again

Yen reversed earlier gains in the European session as traders reassessed the Bank of Japan's latest economic projections and policy stance. While BoJ maintained its upbeat tone on inflation eventually aligning with the 2% target, near-term commentary and projections have dampened rate hike expectations.

The central bank sharply upgraded core CPI forecasts for fiscal 2025 to 2.7%, but emphasized that the jump was mainly die to food prices. It sees inflation quickly falling back, with underlying price growth remaining subdued.

Even though core CPI is now expected to hit 1.8% in fiscal 2026 and reach 2.0% in 2027, the market appears to be focusing on BoJ’s cautious tone and lack of urgency to tighten further. The reaction suggests that traders may now be dialing back expectations for any near-term policy action.

Technically, AUD/JPY's bounce solidifies the case that price actions from 97.41 are merely forming a sideway consolidation pattern. Thus, near term bullish outlook is maintained. Firm break of 97.41 will target 61.8% projection of 86.03 to 95.63 from 92.30 at 98.23 next.

Bitcoin Rebounded from Support But Cannot Find Reasons to Break Through Resistance

Market Overview

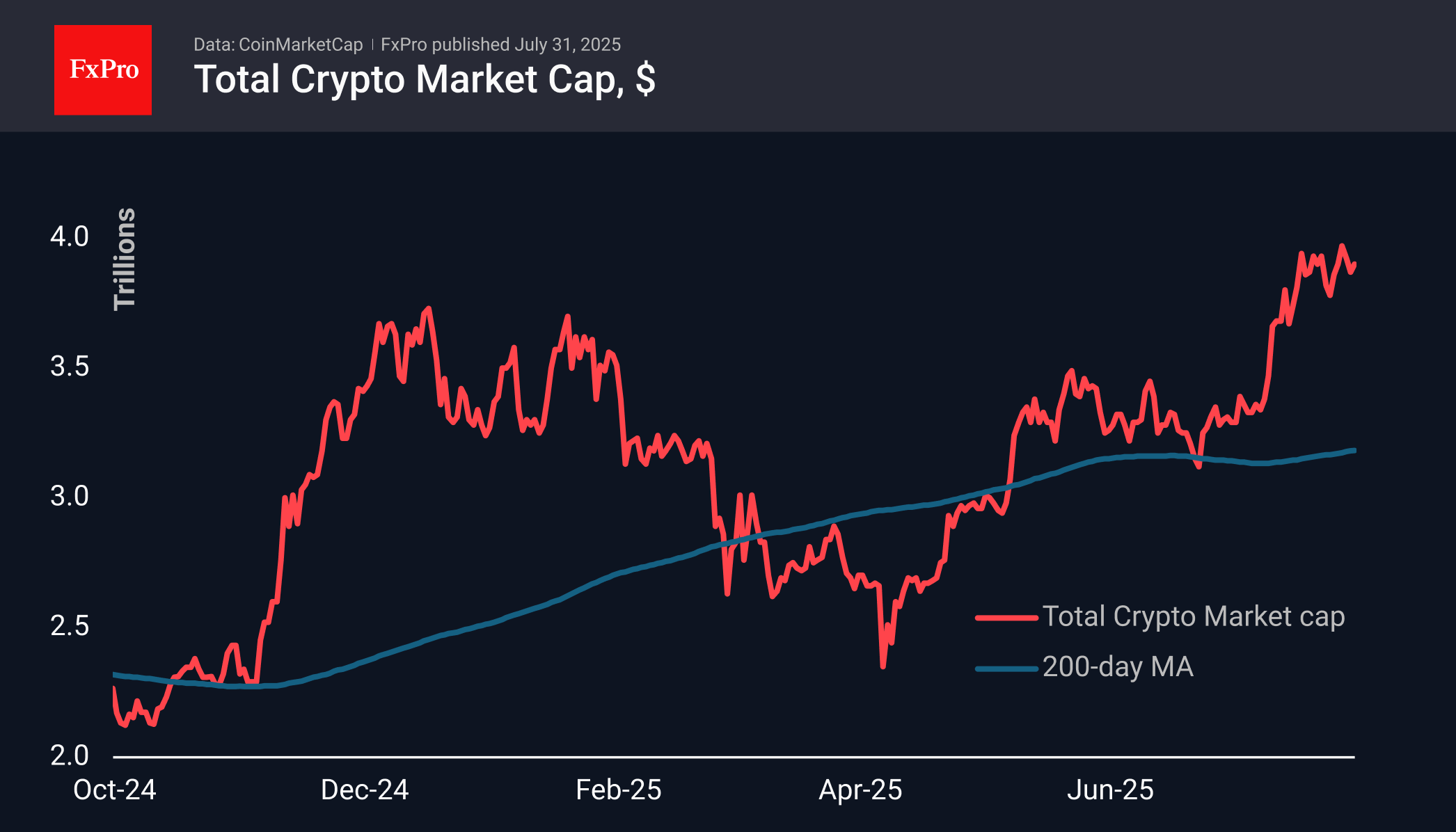

The crypto market capitalisation rose 0.5% during the day to $3.90T, following the reversal of the stock markets and Bitcoin at the end of the day on Wednesday, after falling to $3.79T immediately after the Fed’s announcement on the key rate. The influence of macroeconomic factors on cryptocurrencies continues to grow, even in the absence of major industry developments — a trend that can also be seen as part of the market’s maturation.

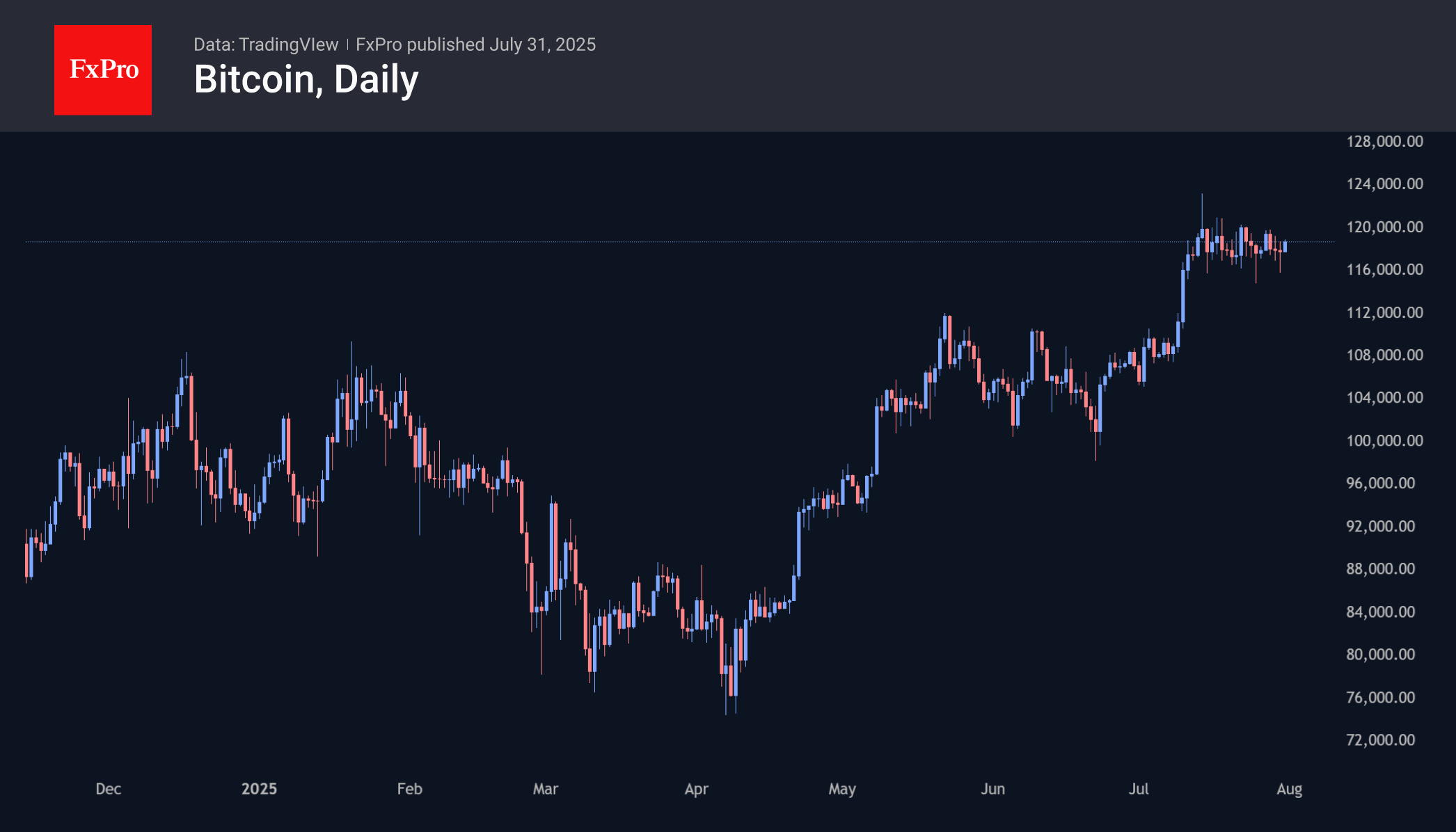

Bitcoin bulls once again defended the lower boundary of the range, which has been holding for almost three weeks, preventing the price from settling below $116K on Wednesday evening. A powerful buying momentum brought the price back to the $118.6K area. But the market still needs drivers to storm $120K. The US White House report on the development of digital assets did not contain any details that could inspire new buyers, making the crypto market follow the trends of macroeconomics and traditional finance.

News Background

According to Glassnode, for the first time since April 2023, Ethereum has reached 40% open interest in the derivatives market, while Bitcoin’s dominance is showing a decline.

Bernstein believes that large companies are increasingly choosing Ethereum over the first cryptocurrency as an investment vehicle, as ETH offers an income-generating tool such as staking.

The US SEC has begun reviewing an application from BlackRock, the world’s largest investment company, to stake Ethereum held in its ETH ETF.

Asian countries are tightening crypto regulations. The Bank of South Korea (BoK) has created a new division to monitor the crypto market. Indonesia has announced tax increases on cryptocurrency transactions, and Hong Kong has finalised rules for stablecoins.

Algeria has banned all cryptocurrency transactions, including exchange, storage, and mining. Violators of the new rules face fines and imprisonment.

Crypto lender Abra has suddenly suspended withdrawals for international customers. The crypto community fears that the platform may repeat the fate of the bankrupt Celsius and BlockFi.

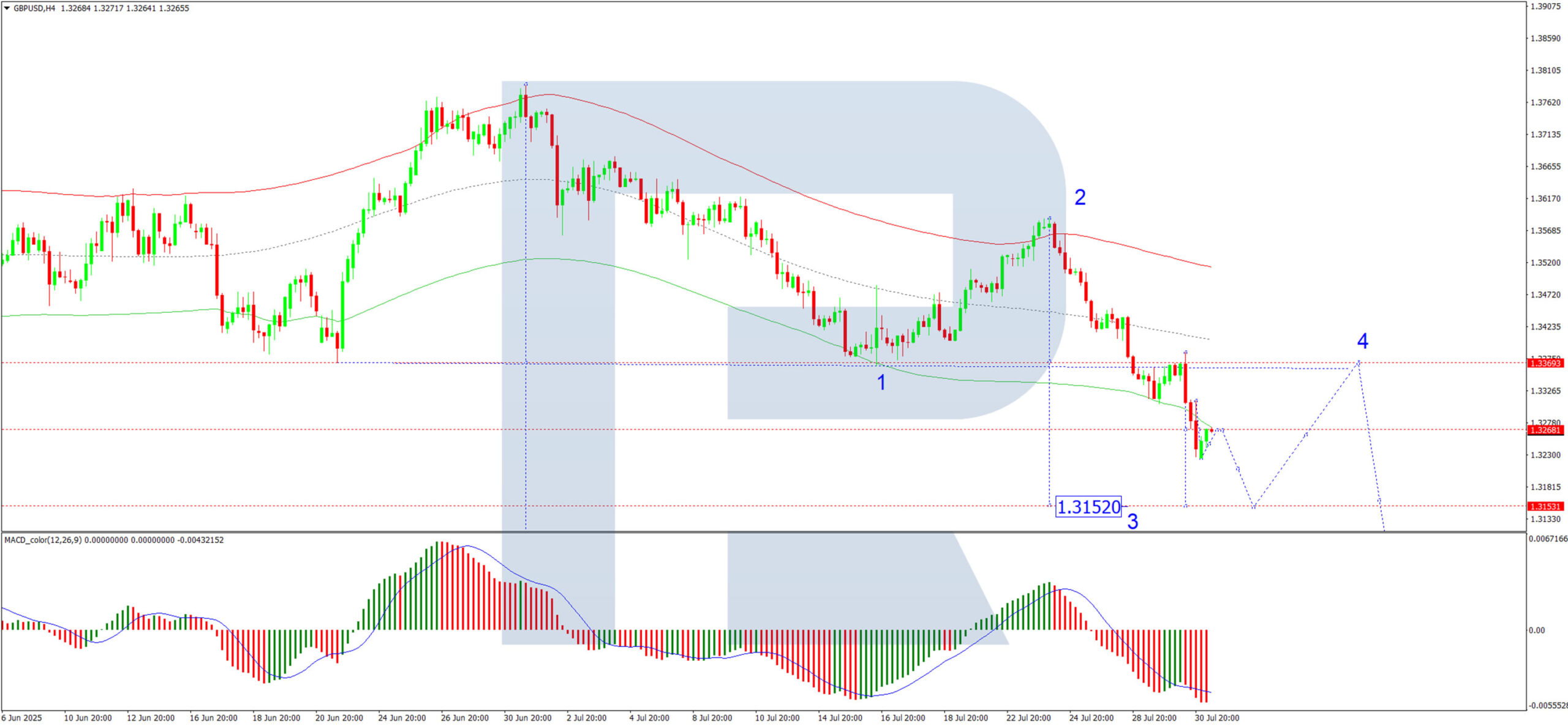

GBP/USD Hits Lows: Weak UK Data and a Strong Dollar Weigh on the Pound

The GBP/USD pair dropped to 1.3252, its lowest level since 11 May 2025, as a resurgent US dollar and disappointing UK economic data weighed on the pound.

Market sentiment has shifted from concerns about inflation to fears of an economic slowdown, while optimism surrounding new trade agreements has bolstered the dollar.

Although warmer weather boosted food sales, the broader economic outlook remains fragile after worse-than-expected PMI figures. This has reinforced expectations that the Bank of England (BoE) could cut interest rates by 25 basis points as early as August, with another potential reduction before year-end to stimulate growth.

Meanwhile, the dollar gained strength following the announcement of a US-EU trade deal, which imposes 15% tariffs on most European exports, including cars. The agreement has averted a further escalation in trade tensions, providing additional support for the greenback.

However, not all European leaders view the deal as favourable. Many argue that the terms disproportionately disadvantage the EU. While the UK maintains its separate agreements, the broader economic ripple effects are still being felt, given the interconnected nature of global markets.

Technical Analysis: GBP/USD

H4 Chart:

On the 4-hour chart, GBP/USD continues its downward trajectory towards 1.3152, with a consolidation range currently forming around 1.3268. A downside breakout from this range could see the pair extend losses towards 1.3152, followed by a potential corrective rebound to 1.3370. This scenario is supported by the MACD indicator, where the signal line remains below zero and points sharply downward.

H1 Chart:

On the hourly chart, the pair declined to 1.3225 before correcting to 1.3270. Further downside movement towards 1.3152 is anticipated today, with the Stochastic oscillator confirming this outlook: its signal line has crossed below 80 and is trending downward towards 20.

Conclusion

The pound remains under pressure amid a stronger dollar and a lacklustre UK economic performance. With rate cut expectations mounting and global trade dynamics shifting, further volatility in GBP/USD is likely. Traders will be watching key technical levels for confirmation of the next directional move.

Elliott Wave Perspective: USDJPY Targets Completion of 7 Swing Rally

The USDJPY pair exhibits an incomplete bullish sequence originating from the April 22, 2025 low, signaling potential for further upside. We can project the extreme target area for this rally can be projected using using the 100% to 161.8% Fibonacci extension from the April 22 low. This places the target range between 150.88 and 156.33. The ongoing rally from the May 27, 2025 low is unfolding as a double three Elliott Wave structure. This structure has two zigzag corrective structure driving the upward momentum.

From the May 27 low, wave W concluded at 148.03. A corrective pullback in wave X then followed, which bottomed at 142.67. Currently, wave Y is in progress, with internal subdivision as a zigzag pattern. From the wave X low, wave ((a)) peaked at 149.18, followed by a corrective wave ((b)) that unfolded as a zigzag. Within this structure, wave (a) ended at 147.81 and wave (b) reached 149.08. Wave (c) completed at 145.87, finalizing wave ((b)) in the higher degree. The pair has since resumed its ascent in wave ((c)), developing as a five-wave impulse.

From wave ((b)), wave (i) concluded at 148.71, with a minor pullback in wave (ii) at 147.79. In the near term, as long as the pivot low at 145.87 holds, dips are expected to attract buyers in a 3, 7, or 11-swing corrective pattern, supporting further upside toward the Fibonacci extension targets.

USDJPY – 60-Minute Elliott Wave Technical Chart:

USDJPY – Elliott Wave Technical Video:

https://www.youtube.com/watch?v=QK2AErXqDKk

Dollar Extended a Three-Day Jump Against Euro

Markets

The Fed’s policy rate stayed at 4.25-4.5% yesterday. It wasn’t a unanimous decision though. Two governors favoured of a 25 bps cut. Waller has repeatedly called for a July cut, citing a weaker economy and labour market than headline numbers suggest. For Bowman it was a matter of tariff inflation not realizing as much as initially feared. But for the FOMC majority it all remains to be seen and want to wait out a couple of months. The statement contained only some marginal changes. The growth assessment was downgraded from “expanding at a solid pace” to “moderating in the first half of the year”, with Powell during the press conference referring to a slowdown in consumer spending. With the July status quo, the Fed is buying time to wait and see future data rolling in. That seems to be both possible with a labour market and economy in a solid position and necessary: Powell said they are “still a ways away from seeing where things [ie tariffs impact] settle”. The Fed chair didn’t bite the bait when asked if the central bank would cut rates in September, as suggested earlier by US president Trump. US rates rallied between 4.3 and 7.3 bps in a bear flattening move. This suggests markets were at least expecting some kind of concrete clue for near-term easing. Bets for a September move fell from around 70% to <50%. All eyes are now turning to the “Labor Markets in Transition: Demographics, Productivity, and Macroeconomic Policy"-themed Jackson Holy symposium taking place August 21-23. This served in the past multiple times as an occasion to announce policy changes. The dollar extended a three-day jump against the euro and pushing the EUR/USD pair towards the 1.1431-support. The trade-weighted index tested but closed below the 100 barrier.

In overnight news, South Korea became the latest country in securing a trade deal with the US ahead of the August 1 deadline. They agreed to a 15% import levy and a Japan-like $350bn SK fund for US investments. While talks with India are ongoing, they will have a 25% rate plus a penalty for buying Russian energy starting Friday. The economic calendar for later today takes a step back after yesterday’s data flurry that included US and European GDP. The first EU member states inflation prints were also released on Wednesday with Italy, France and Germany joining the streak today. June PCE inflation in the US is up for publication too but could already be extracted from yesterday’s Q2 reading. In addition, Powell during the press conference already said (core) PCE would be 2.7%. We’re now looking at Friday’s payrolls report to validate the central bank’s relatively optimistic view and to determine (front-end) rates short-term trajectory. That will be the case for the USD as well. We are looking for EUR/USD to bottom out somewhat now but it’s the labour market report that’ll have the last say. EUR/USD 1.1431 survives for now.

News & Views

The Bank of Japan kept the policy rate unchanged at 0.5% this morning. It slightly upgraded the growth outlook for fiscal year 2025 (through March 2026) to 0.6% while keeping the forecasts for the two years after unchanged. Core inflation (ex. fresh food) for FY 2025 got a significant bump to 2.7% from 2.2%. Inflation forecasts for 2026 and 2027 were lifted to 1.8% and 2%. Risks for growth remain tilted to the downside but uncertainty diminished from being “extremely high” to “high”. Price risks meanwhile are seen as generally balanced, to be compared to the downside risks for 2025 and 2026 it cited in the previous outlook report. This suggests the central bank is moving closer to another rate hike. Money market pricing didn’t budge a lot with a 25 bps increase priced in for about 80% by the end of the year. The Japanese yen creeps higher against an overall weaker USD. USD/JPY trades near 148.9.

The Banco do Brasil held rates steady at 15% at yesterday’s policy meeting. The first and widely expected hold interrupted a sequence of seven hikes that raised the Selic rate a cumulative 4.5 ppts. The BdB said it’ll remain at 15% for the foreseeable future amid above-target inflation (5.3% in June vs a 3% +/- 1.5 ppt target) due to public spending and a near record-low unemployment rate. Inflation is expected to remain too high at least through 2027Q1. Tariff-related uncertainty over trade strengthens the central bank’s cautious stance. US President Trump on Wednesday delayed the implementation of a 50% levy by seven days (beyond the August 1 deadline). He also listed hundreds of products to be exempted from tariffs. The Brazilian real welcomed that by erasing much of the earlier losses. USD/BRL closed at 5.57 and has yet to react to the BdB’s policy decision.

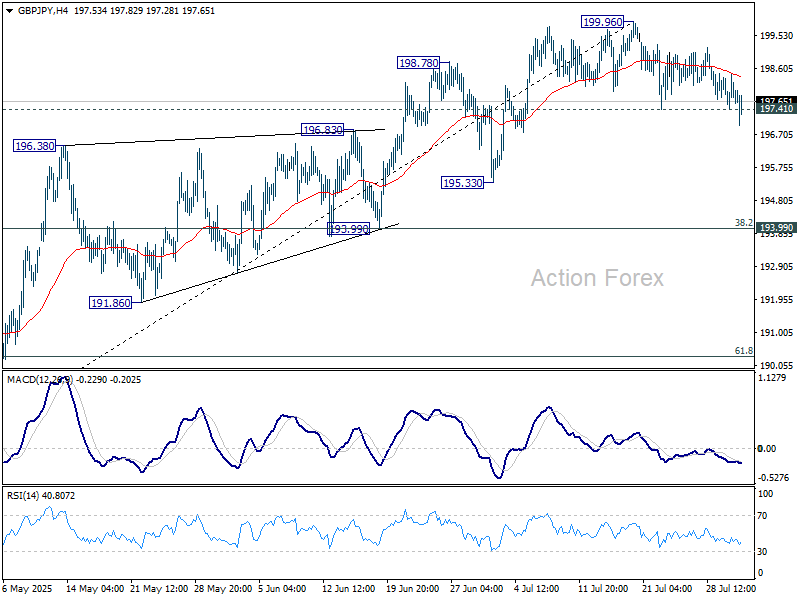

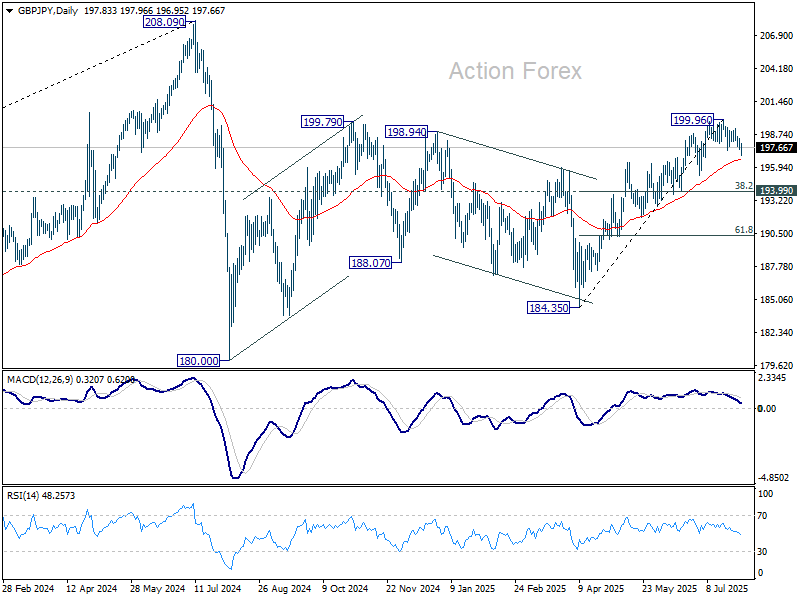

GBP/JPY Daily Outlook

Daily Pivots: (S1) 197.48; (P) 197.96; (R1) 198.46; More...

The breach of 197.41 support suggests that GBP/JPY's fall from 199.967 short term top is already correcting the rally from 184.53. Intraday bias is mildly on the downside for 193.99 cluster support (38.2% retracement of 184.35 to 199.96 at 193.99). For now, risk will stay on the downside as long as 199.96 resistance holds, in case of recovery.

In the bigger picture, price actions from 208.09 (2024 high) are seen as a correction to rally from 123.94 (2020 low). The pattern might still extend with another falling leg. But in that case, strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. Meanwhile, decisive break of 208.09 will confirm long term up trend resumption.

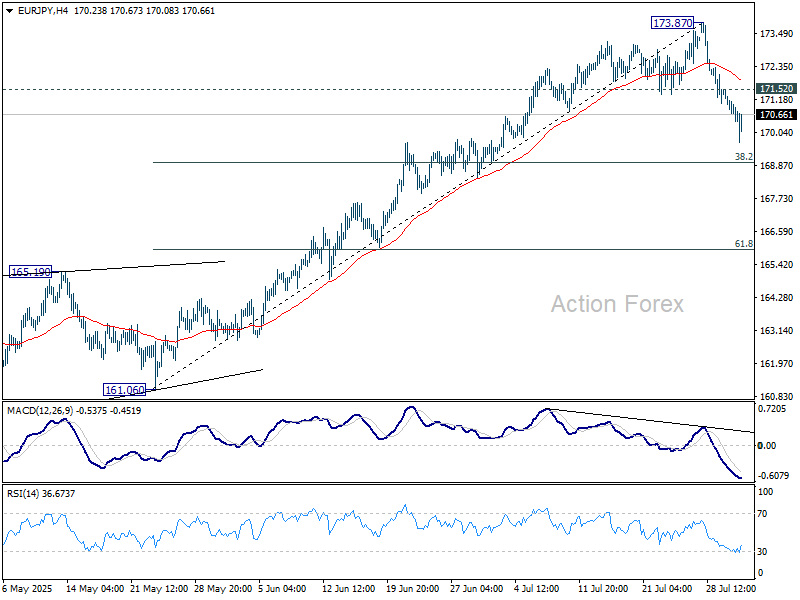

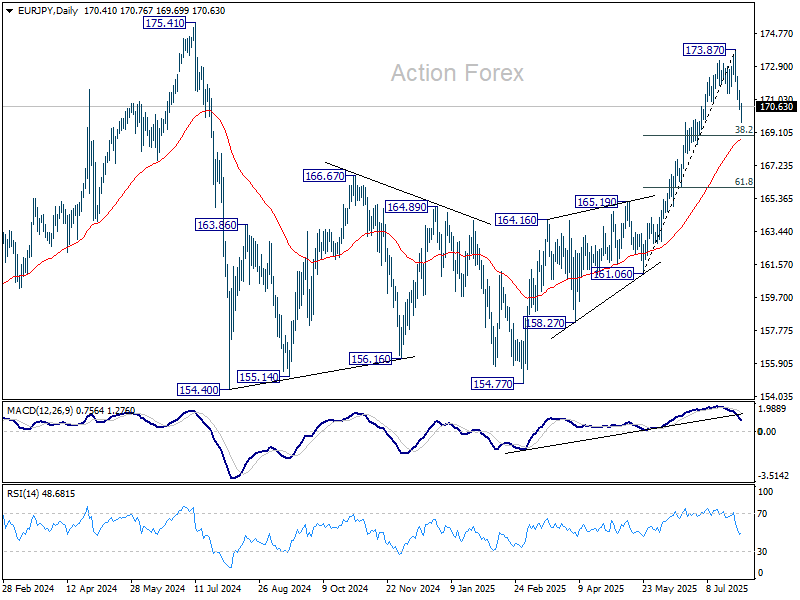

EUR/JPY Daily Outlook

Daily Pivots: (S1) 170.13; (P) 170.85; (R1) 171.24; More...

Intraday bias in EUR/JPY stays on the downside at this point. Fall from 173.87, as a correction to rally form 161.06, is in progress for 38.2% retracement of 161.06 to 173.87 at 168.97. Strong support should emerge from 55 D EMA (now at 168.68) to contain downside and bring rebound. On the upside, above 171.52 minor resistance will turn intraday bias neutral first.

In the bigger picture, considering current strong momentum as seen in the rally from 154.77, corrective pattern from 175.41 could have already completed. Decisive break there will confirm long term up trend resumption. Next target is 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. However, rejection by 175.41, followed by firm break of 55 D EMA (now at 168.69) will delay this bullish case.

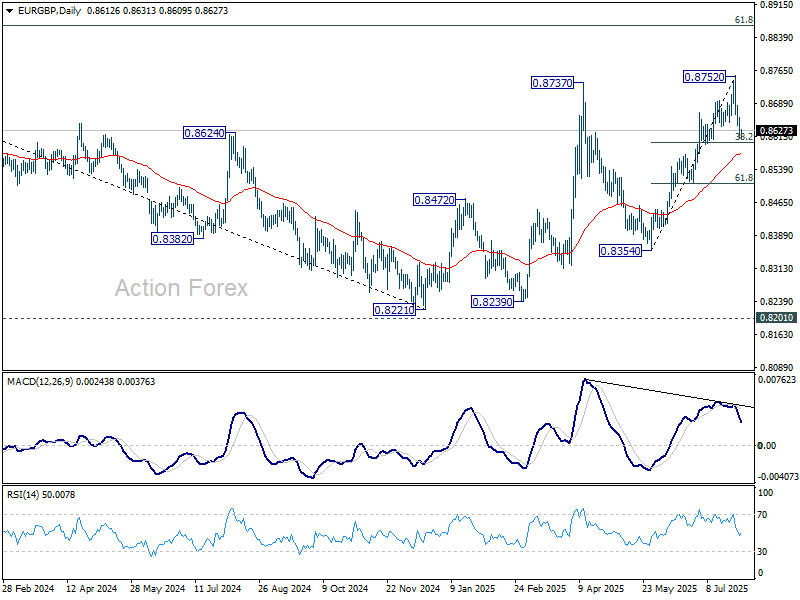

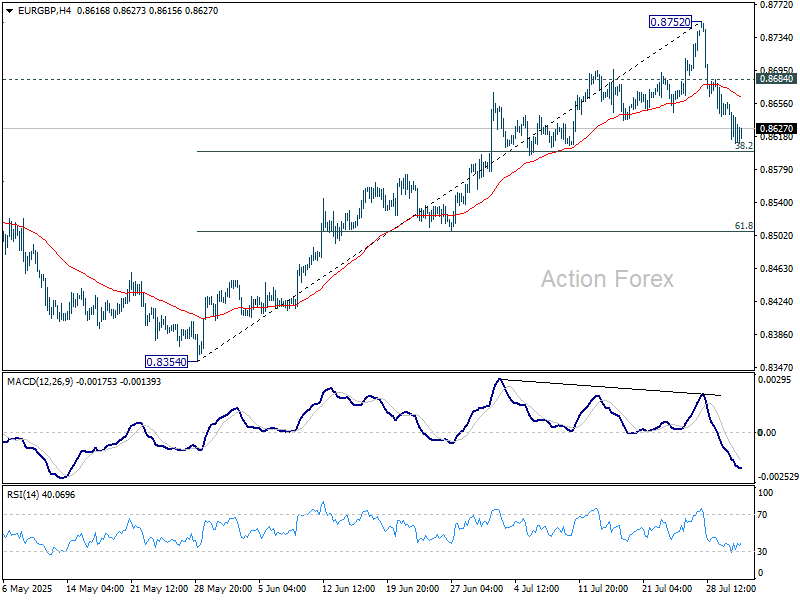

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8598; (P) 0.8628; (R1) 0.8645; More...

Intraday bias in EUR/GBP remains on the downside at this point. Fall from 0.8752 is seen as correcting the rise form 0.8354 for now. Deeper decline could be seen through 38.2% retracement of 0.8354 to 0.8752 at 0.8600. But strong support might emerge from 55 D EMA (now at 0.8576) to bring rebound. On the upside, above 0.8684 minor resistance will turn intraday bias neutral first. However, sustained trading below 55 D EMA will raise the chance of near term bearish reversal.

In the bigger picture, the structure from 0.8221 medium term bottom are not impulsive enough to suggest that it's reversing the down trend from 0.9267 (2022 high). But even if it's a correction, further rise is expected to 61.8% retracement of 0.9267 to 0.8221 at 0.8867. This will remain the favored case as long as 55 W EMA (now at 0.8486) holds.