Sample Category Title

Asia data wrap: Japan and Australia outperform but China falters

Asian economies delivered mixed signals as fresh data highlighted strength in Japan and Australia while exposing continued softness in China.

Japan’s industrial production rose 1.7% mom in June, defying forecasts for a -0.7% mom decline. The surge was driven by a 14.8% mom jump in transport equipment excluding autos and strength in electronics, a positive surprise despite ongoing US tariffs. Retail sales also rose 2.0% yoy, slightly beating forecasts of 1.8% yoy.

Australian retail sales posted an impressive 1.2% monthly gain in June, sharply above the 0.4% mom consensus. The ABS attributed the spike to widespread discounting and new product launches.

Meanwhile, China's July PMIs disappointed. The NBS Manufacturing PMI dipped from 49.7 to 49.3, remaining in contraction for the fourth straight month. The export component showed no signs of recovery, marking 15 months of sub-50 readings at 47.1 Non-Manufacturing PMI also weakened from 50.5 to 50.1, its lowest since November.

BoJ holds at 0.50%, lifts 2025 inflation projections sharply on food costs

The BoJ kept its short-term policy rate unchanged at 0.50% as expected, reaffirming its cautious stance in the face of growing external risks. While the central bank reiterated its intention to continue normalizing policy in light of improving economic and price conditions, it also cited heightened uncertainty around global trade and policy developments as justification for a steady hand.

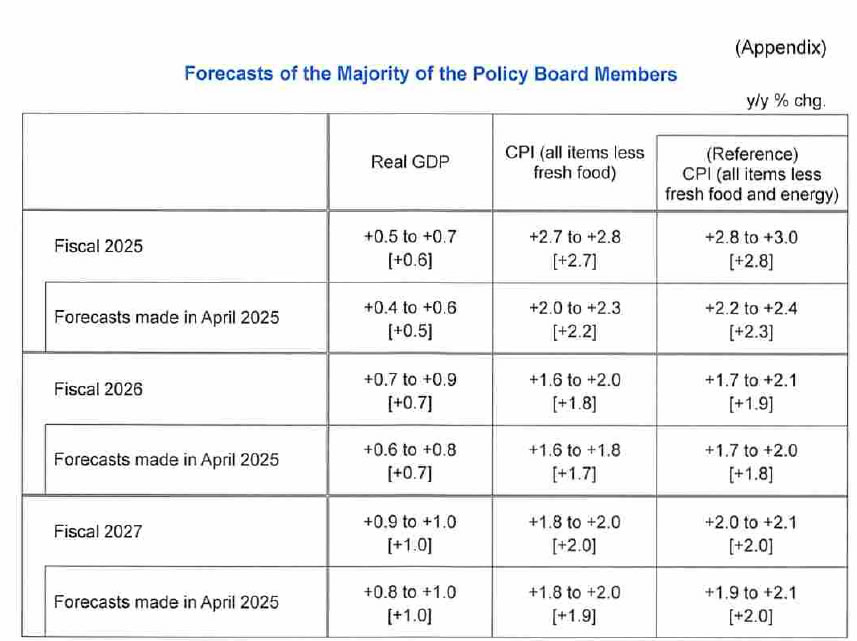

In its latest quarterly outlook, the BoJ sharply raised its inflation forecasts. Core CPI for fiscal 2025 was lifted from 2.2% to 2.7%. Core-core CPI, which excludes both fresh food and energy, jumped from 2.3% to 2.8%. The upward revisions were largely attributed to food price increases, though the BoJ still sees underlying inflation remaining subdued in the first half of the forecast horizon.

For fiscal 2026, core CPI was revised slightly higher from 1.7% to 1.8%, and core-core CPI from 1.8% to 1.9%. Projections for fiscal 2027 remained unchanged at 2.0% for both measures. The Bank noted that inflation will pick up toward levels “generally consistent” with the price stability target in the second half of the projection period.

Growth outlooks were little changed. The fiscal 2025 GDP forecast was lifted modestly to 0.6% from 0.5%, while estimates for fiscal 2026 and 2027 were held at 0.7% and 1.0%, respectively. The Bank continues to expect a slow but steady recovery, supported by resilient domestic demand and improvements in global conditions.

BoJ emphasized that the risk balance for growth remains tilted to the downside for 2025 and 2026, though price risks are now broadly balanced.

Fed Powell’s caution cools September cut bets, stocks end mixed

U.S. stocks ended mixed overnight after the Fed held its policy rate steady at 4.25–4.50%, in line with market expectations. The dissenting votes from Governors Christopher Waller and Michelle Bowman in favor of a cut came as little surprise, reflecting known dovish leanings. However, Chair Jerome Powell’s tone in the press conference struck a more cautious chord than markets had anticipated.

Powell pushed back against speculation of a near-term pivot, stating firmly, “We have made no decisions about September.” That effectively left the door open, but offered little for those hoping for imminent easing. Powell also warned that while tariff-driven inflation may be transitory, “more persistent” effects couldn’t be ruled out.

Between now and the next FOMC meeting, two additional rounds of jobs and inflation reports will be released—giving the Fed a wider lens to assess policy needs.

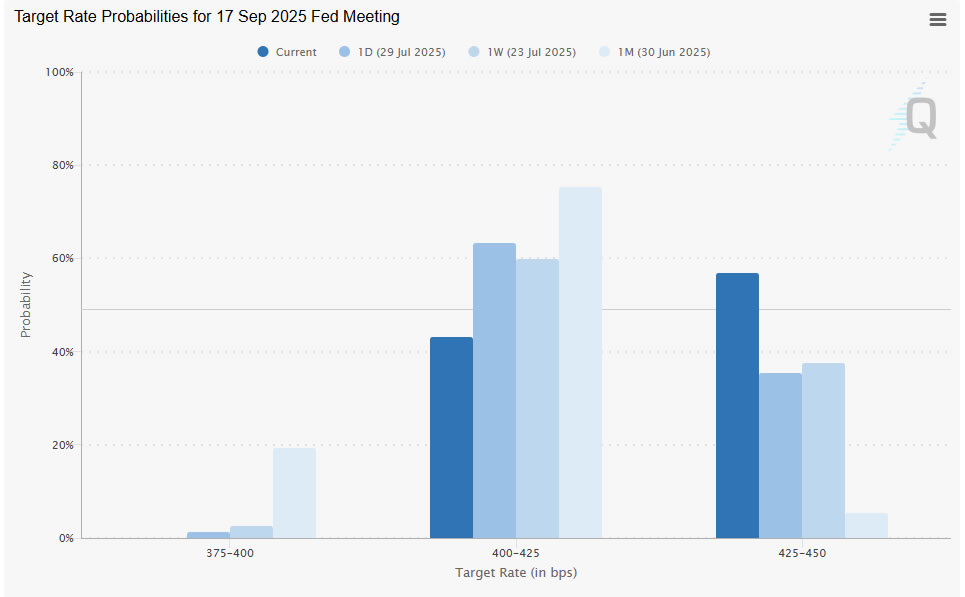

Traders responded by paring back bets for a September cut. Market pricing now sees just a 43% chance of easing at the next meeting, down from 65% a day earlier. The message: the Fed may be approaching the end of its pause, but it’s not ready to blink just yet.

Technically, while S&P 500's up trend continued this week, it's clearly continuing to lose upward momentum as seen in bearish divergence condition in D MACD. 6500 psychological level is likely to cap upside and bring consolidations. That's slightly above a major fibonacci level of 61.8% projection of 3491.58 to 6147.43 from 4835.04 at 6476.35. Break of 6281.71 support will indicate that a near term correction has already started towards 55 D EMA (now at 6110.15).

July FOMC: Optionality Maintained

Summary

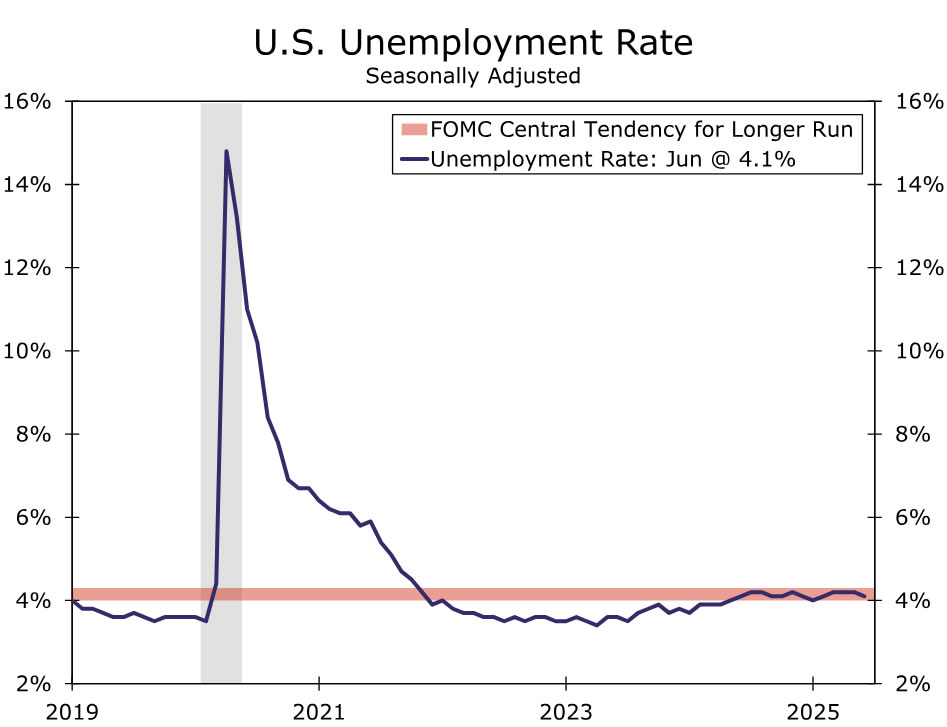

- The FOMC left the federal funds rate unchanged for the fifth consecutive meeting. The post-meeting policy statement had minimal changes and continued to characterize inflation as "somewhat elevated," the unemployment rate as "low" and labor market conditions as "solid." The pace of balance sheet runoff, also known as quantitative tightening, was left unchanged.

- Governors Waller and Bowman dissented against the decision to hold rates steady, preferring instead to cut the fed funds rate by 25 bps. This marked the first time multiple governors formally dissented since December 1993.

- To some extent these dissents reflect political jockeying, as Jerome Powell's term as Chair comes to an end next spring. But, we suspect the dissents reflect at least some genuine disagreement among Committee participants as they grapple with the appropriate stance of monetary policy amid the stagflationary impulse from higher tariffs.

- In the post-meeting press conference, Chair Powell was very careful to play his cards close to the chest regarding the outlook for a rate cut at the September meeting. Chair Powell cited easing financial conditions, a low unemployment rate and still-above target inflation as reasons to keep rates on hold. But, he highlighted potential downside risks to the labor market as a key reason to remain nimble when thinking about the path forward for the fed funds rate.

- Economic and policy developments between now and the next FOMC meeting on September 16-17 will be critical to determining the path forward for monetary policy. The FOMC will receive two more employment reports (including Friday's jobs data) and two more months of inflation data between now and then. Furthermore, although we doubt full clarity on tariffs is coming anytime soon, we should know more about the administration's tariff intentions and the economy-wide average effective tariff rate come mid-September.

- As we go to print, markets are pricing roughly a 49% chance of a 25 bps rate cut at the September FOMC meeting. Our current forecast looks for the FOMC to cut the fed funds rate by 25 bps at its September, October and December meetings, with risks skewed toward pushing back the timing of those cuts. We intend to adjust our fed funds forecast, if necessary, after the dust has settled following Friday's employment report.

The Center Holds

As was widely expected, the FOMC left the fed funds target range unchanged at the conclusion of its meeting today (Figure 1). The Committee has held the policy rate steady at 4.25%-4.50% this year as the economy's resilience has afforded the FOMC time to see how inflation and the labor market fare in the face of higher tariffs. However, Committee members are no longer all on board with this wait-and-see approach. Governors Waller and Bowman dissented in favor of reducing the fed funds rate by 25 bps at today's meeting.

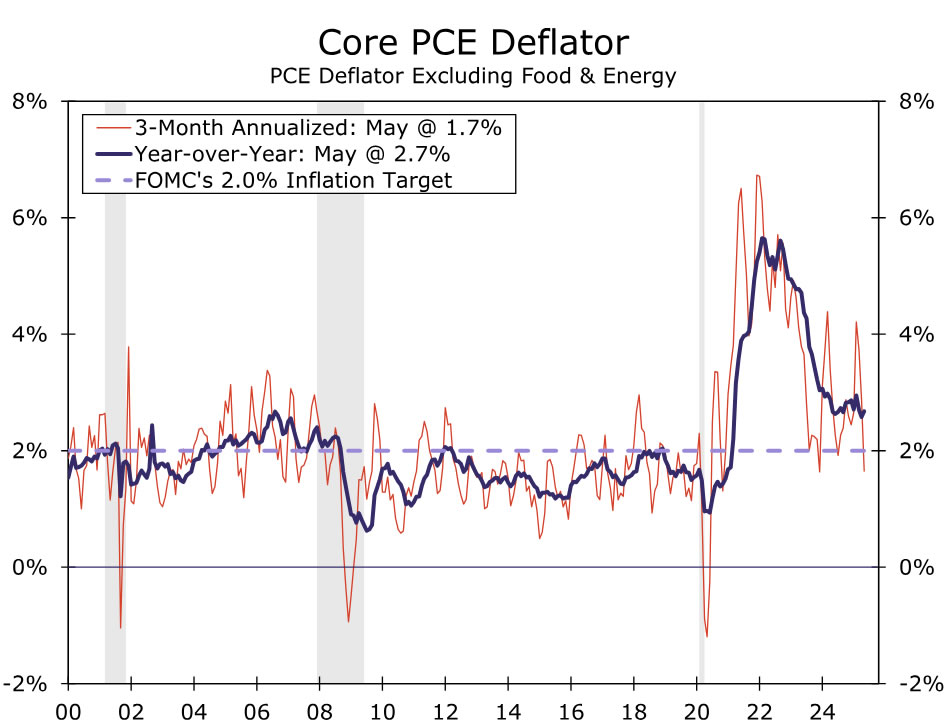

Yet, there were no hints in the statement that other Committee members may soon be ready to follow their lead. The majority of voters still see policy as appropriately positioned to support the Committee's inflation and employment objectives. The statement continued to characterize inflation as "somewhat elevated," as the core PCE deflator has been running above the FOMC's 2% target for four years and counting (Figure 2). At the same time, labor market conditions remain "solid." The Committee did note some loss of momentum in economic growth recently, which was evident in the details of second quarter GDP. That said, the statement does not seem overly worried about current activity, noting it has moderated, rather than expanded at a "solid" pace recently. The only other change to the statement was the removal of uncertainty as "having diminished;" it now simply states that uncertainty remains elevated.

The dissents of Governors Waller and Bowman were telegraphed ahead of today's meeting and thus do not come as a surprising development. As the only two governors appointed by President Trump, the breaking of ranks could be viewed as jockeying for position in the race for the next Fed chair given that the administration has made no secret in its preference for lower rates. After all, a double dissent by governors has become extraordinarily rare, with the last one occurring in 1993.

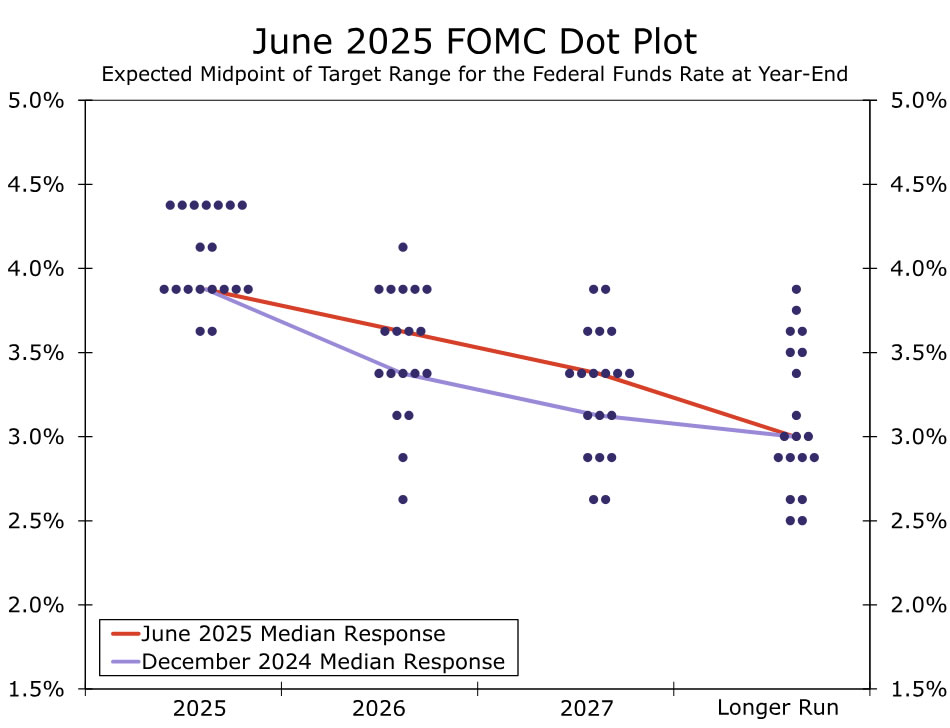

That said, dissents are not uncommon around policy turning points. A directional bias among Committee members to lower rates has been in place since the last rate reduction in December, even as there remains disagreement over the precise timing and magnitude (Figure 3). The more formal, vocal support by Waller and Bowman could slightly hasten the timing to which the Committee decides to next move rates lower, especially as Governor Waller has served as a bellwether for the Committee the past few years.

Committee members will not have to wait long for the picture to be filled in. Friday will bring the July employment report. Last year's July job report also was released just days after the FOMC's meeting, and it showed more pronounced softness in the labor market that started the FOMC down the path of eventually cutting the fed funds rate by 50 bps at its subsequent meeting in September. While Friday's jobs report will not be the only major data release before the FOMC's next meeting on September 17 (there will be one additional employment report and two more months of inflation data), we view a weaker employment report as a necessary condition for the FOMC to cut rates as soon as its next gathering (Figure 4). Our current forecast looks for the FOMC to cut the fed funds rate by 25 bps at its September, October and December meetings, with risks skewed toward pushing back the timing of those cuts. We intend to adjust our fed funds forecast, if necessary, after the dust has settled following Friday's employment report.

GBPJPY Rejects the Highs of Its Range as Traders Prepare for Bank of Japan

July was a rough month for both the GBP and the JPY which were the worst performing currencies in the Major FX space against the Greenback (which also sparked a market-shaking comeback).

The past week however did see the return of some strength for the Yen after observing a lot of bad talk around the Nippon currency– As if bearish positioning for the Yen was at an extreme.

Positioning now seems more balanced as players have reduced their positions to prepare for tonight's Bank of Japan Rate Decision.

No hike is expected but the BoJ tends to surprise markets so always stay ready, this one would shock the Trading World.

Markets are expecting a 25 bps rate cut from the upcoming Bank of England meeting on August 7.

The meeting will also see the release of the Quarterly Monetary Policy Report which will provide more details on the views from the UK Central Bank amid their ongoing Cut cycle – Cuts are currently priced in for one out of two meetings.

Taking a look at the GBPJPY Technicals

GBPJPY Daily

GBPJPY Daily Chart, July 30, 2025 – Source: TradingView

The most volatile FX pair has started to show some signs of retraction from its Range Extremes, right after reaching 199.976 (the pair did not breach the 200.00 level).

Momentum is actually starting to confirm a potential reversal around here with the RSI going towards bearish (still at a neutral level for now).

Expect whipsawing volatility between tonight's BoJ Rate Decision and next week's Bank of England meeting.

The most important aspect to spot is actually the confirmation of the range after bulls tried to break higher and saw some consequent sharp reversals.

Support Levels:

- 50 4H-MA 197.75 immediate support

- Intermediate Range Resistance Zone turned pivot near 196.00

- Range Intermediate Support Zone around the 190.00 level

Resistance Levels:

- Resistance Zone extremes 199.00 to 200.00

- Weekly highs 199.220

- 20 4H-MA 198.25

GBPJPY 4H

GBPJPY 4H Chart, July 30, 2025 – Source: TradingView

Looking closer to the 4H timeframe, we are spotting a trendline break-retest pattern.

This would be a decent sign of reversal if it wasn't for the 4H 200-period MA holding prices – Therefore, keep this one closely in check to get a better idea of the immediate strength for bulls and bears.

With the MA 20 also passing as resistance, it will be interesting to see how the action reacts in the waiting of tonight's BoJ Meeting.

GBPJPY 1H Chart

GBPJPY 1H Chart, July 30, 2025 – Source: TradingView

Looking even closer, we are seeing that the ongoing action is evolving within a downwards channel formed since the July 8th pivot.

The lower bound of the Channel is currently below 197.40 to 197.50 and its higher bound is around 198.90 – It would be uncommon to see any major breakout before tonight's BoJ Meeting.

The pair will be extremely important to watch as European currencies start to show signs of weakness – Stay ready for the key Rate Decisions coming up soon.

Safe Trades and good luck for tonight's Bank of Japan Meeting!

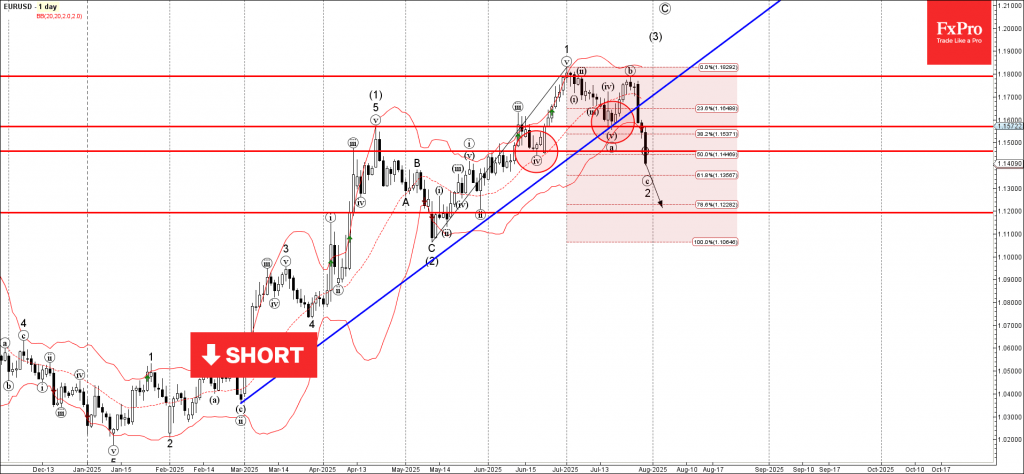

EURUSD Wave Analysis

EURUSD: ⬇️ Sell

- EURUSD falling inside accelerated impulse wave c

- Likely fall to support level 1.1200

EURUSD currency pair recently broke the support trendline from February, coinciding with the 38.2% Fibonacci correction of the upward impulse 1 from May.

The breakout of these support levels accelerated the active impulse wave c, which then broke the support at 1.1460.

EURUSD currency pair can be expected to fall further to the next support level 1.1200 (former strong support from May).

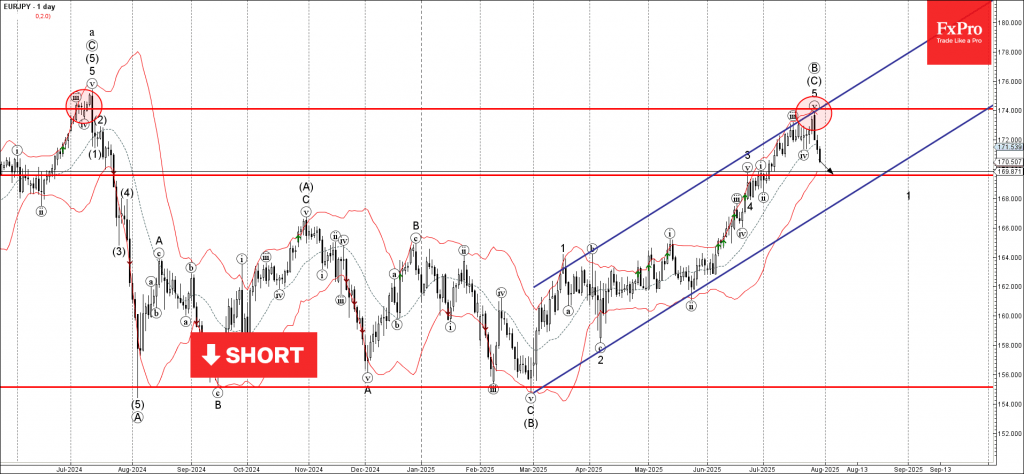

EURJPY Wave Analysis

EURJPY: ⬇️ Sell

- EURJPY reversed from the resistance zone

- Likely fall to support level 169.60

EURJPY currency pair recently reversed down from the resistance zone between the resistance level 174.00, the upper daily Bollinger Band and the resistance trendline of the daily up channel from February.

The downward reversal from this resistance zone created the daily Japanese candlesticks reversal pattern, Bearish Engulfing.

EURJPY currency pair can be expected to fall further to the next round support level 169.60 (former resistance from the end of June).

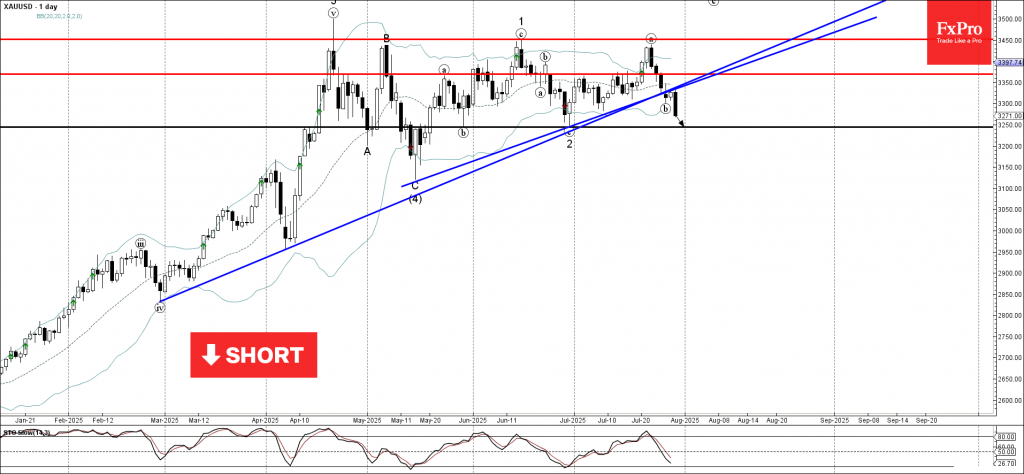

Gold Wave Analysis

Gold: ⬇️ Sell

- Gold falling inside wave b

- Likely fall to support level 3250.00

Gold is under bearish pressure after the price broke the two upward-sloping support trendlines from May and February.

The breakout of these support trendlines accelerated the active short-term correction b – which belongs to the impulse wave 3 from June.

Gold can be expected to fall further to the next round support level 3250.00 (former low of waves 2 and (b) from May and June).

Fed holds steady, dissenters Waller and Bowman call for cut

Fed held interest rates unchanged at 4.25–4.50% as widely expected, but a rare split emerged within the Committee. Governors Michelle Bowman and Christopher Waller dissented, voting in favor of a 25bps cut. Their push to begin easing suggests that internal debate is intensifying, even as the broader Committee maintains a cautious stance.

The statement offered few surprises, characterizing economic activity as having “moderated” in the first half of the year. Labor market conditions remain "solid" with "low" unemployment, while inflation remains “somewhat elevated.”

Fed reiterated its vigilance toward risks on "both sides of its dual mandate", but stopped short of signaling a policy shift.