Sample Category Title

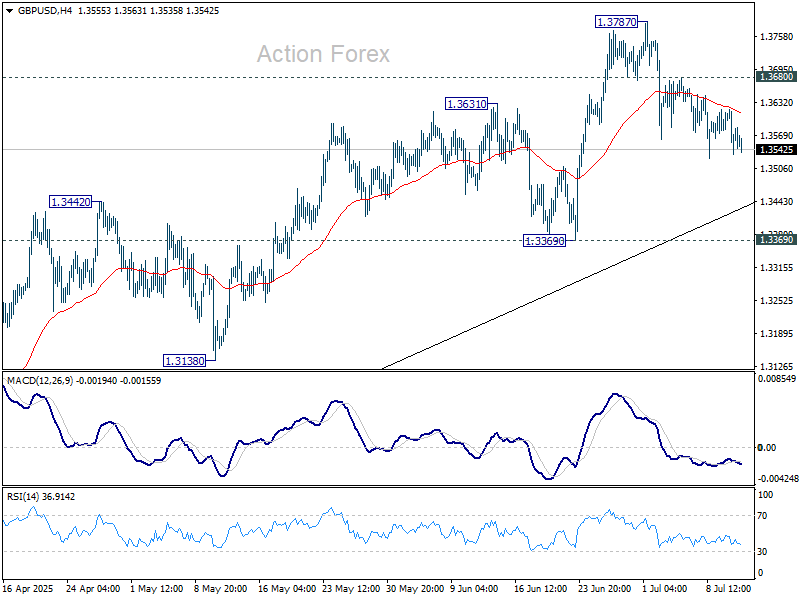

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3534; (P) 1.3577; (R1) 1.3620; More...

Intraday bias in GBP/USD stays neutral at this point. Corrective pullback from 1.3787 could extend lower. But downside is expected to be contained by 1.3369 support to bring rebound. On the upside, above 1.3680 minor resistance will bring retest of 1.3787. Firm break of 1.3787 will resume larger up trend to 100% projection of 1.2099 to 1.3206 from 1.3138 at 1.3813.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.2985) holds, even in case of deep pullback.

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7930; (P) 0.7959; (R1) 0.7998; More….

Intraday bias in USD/CHF remains neutral for the moment. Corrective pattern from 0.7871 could extend higher. But upside should be limited by 0.8054 support turned resistance to bring another fall. Below 0.7871 will extend the larger down trend to 61.8% projection of 0.9200 to 0.8038 from 0.8475 at 0.7757. Firm break there will pave the way to 100% projection at 0.7313 next.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8475 resistance holds.

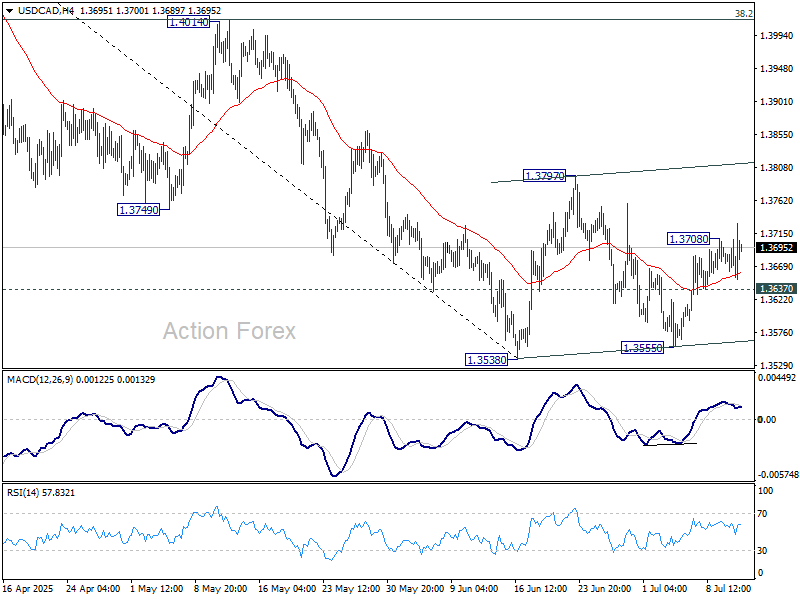

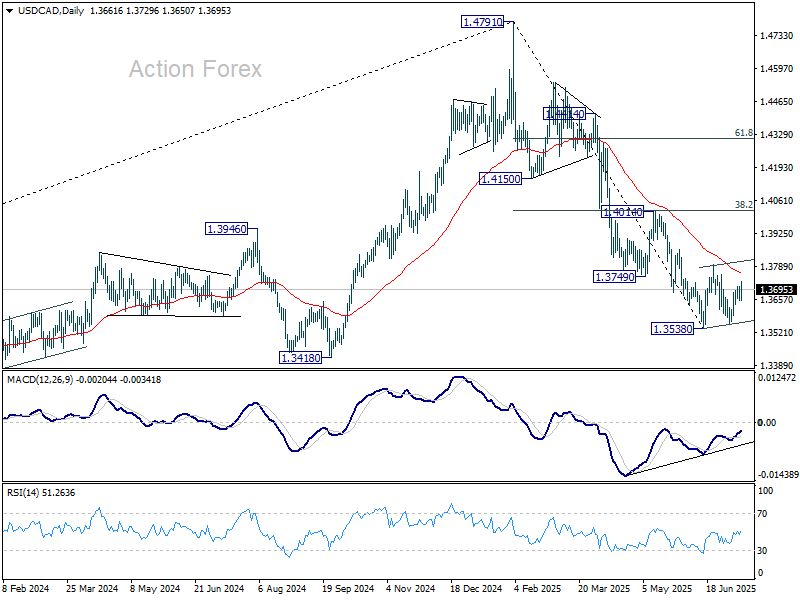

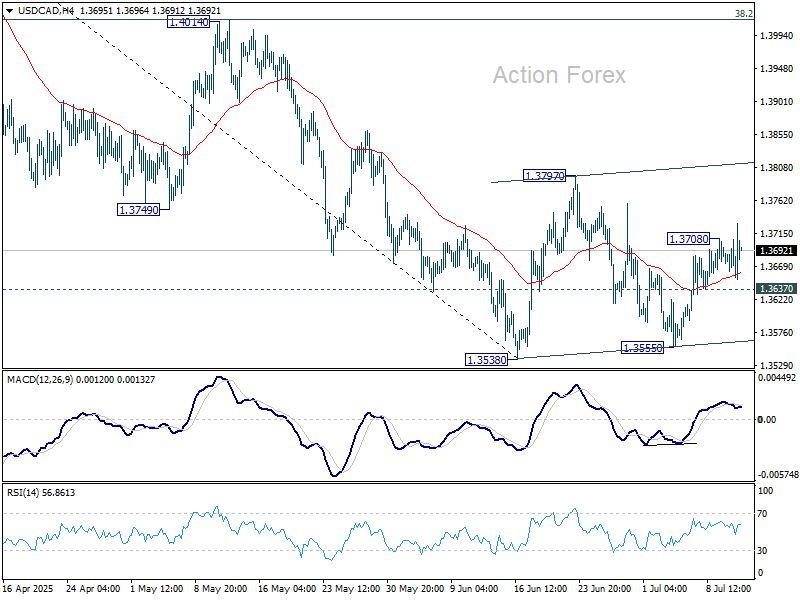

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3636; (P) 1.3666; (R1) 1.3692; More...

USD/CAD's rebound from 1.3555 resumed after brief retreat and intraday bias is back on the upside. Consolidative pattern from 1.3538 is in its third leg and further rise should be seen to 1.3797 and possibly above. On the downside, however, break of 1.3637 minor support will bring retest of 1.3538/55 support zone instead.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 resistance holds. Next target is 61.8% retracement of 1.2005 (2021 low) to 1.4791 at 1.3069.

Tariffs, Debt Worries Absorbed, Equities March On

Sentiment across major US indices was surprisingly positive this week – considering an avalanche of relatively high tariff rates announced throughout the week – some of which were quite shocking, like the 50% tariffs on copper and Brazil, between 25% to 40% on Asian nations, and possibly 35% on Canadian goods imports.

But investors took the news with no apparent stress. They could’ve worried that the tariffs would lead to significant spikes in inflation, potential disruption in supply chains, and unnecessary economic slowdown – a combination that could result in possible stagflation and a hands-tied Federal Reserve (Fed). But no. We haven’t seen any of those risks being priced into equity markets. On the contrary, the S&P500 claimed its second all-time high on Thursday, as Nvidia helped boost appetite in AI stocks. Strong earnings and a positive outlook from Delta Airlines sent airline shares rallying, with Delta adding as much as 12%. United Airlines jumped 14%, while American and Southwest rose nearly 13% and 8%, respectively. Improved demand for travel hinted at stronger consumer sentiment – which had recently taken a hit due to tariff fears – and supported the hope that US consumer spending will defy the tariff hikes. We hope it will.

In the sovereign space, strong sales of US Treasuries throughout the week also supported the bullish sentiment – global investors signalled that they are ready to keep financing Trump’s ‘big, beautiful’ tax bill and the exploding US debt.

Across the Atlantic, the lack of news about a trade deal between the US and the EU kept investors in a sweet wait-and-hope mode and sent the Stoxx 600 to its highest levels in a month.

Elsewhere, the closely watched Japanese 20-year bond auction went relatively smoothly. Demand came in below the long-term average, but it was the strongest since March. As such, Japanese long-maturity yields are lower this morning: the 20-year yield is down to 2.50%, while the 30-year yield is testing the 3% mark to the downside.

As such, risks continue to be ignored by the market: good news grabs all the attention, while bad news is brushed under the rug. You don’t need CNN’s Fear and Greed Index to see that there is extreme greed in the markets these days – which also helps push Bitcoin, for example, to fresh all-time highs with eyes now set on the $120K per coin mark.

So it’s in this atmosphere of fragile optimism that the earnings season will kick off next week – fragile because earnings growth expectations have been revised down, from nearly 10% to around 5–7%, while S&P 500 stocks have been busy climbing the Everest.

While lower expectations are easier to beat and the softer US dollar should help sweeten revenues, the impact of trade uncertainties remains highly uncertain.

Anyway, you know what? Big bank analysts continue to raise their year-end forecasts for the S&P 500 and Nasdaq 100 – and pessimistic ones, like JP Morgan’s Marko Kolanovic, are being pushed out of their jobs. So it’s hard to call for a correction. Up we go, and we hope tariffs won’t hurt much.

In FX, the US dollar is better bid on reduced stress around tariffs and a softer perception of exploding US debt (while the reality HASN’T changed). The EURUSD consolidates below the 1.17 mark, Cable is preparing to test the 1.35 support – which also matches the 50-DMA – and the USDJPY remains bid, trading near 147 at the time of writing.

Given the strong bearish positioning in the dollar, we could see the greenback’s rebound gain momentum in the coming weeks and drag major peers lower. But the EURUSD should remain in its year-to-date bullish consolidation zone above 1.12 – the major 38.2% Fibonacci retracement of this year’s rally. Cable should maintain its positive outlook above 1.3140, while the margin for the yen is tighter: the USDJPY is already stepping back into the bullish consolidation zone above 147.50.

The upcoming Upper House elections in Japan and doubts about the LDP’s ability to maintain a majority are weighing on appetite for Japanese assets, including the yen. Trade tensions with the US aren’t helping either. So, the Nikkei remains under pressure despite some relief in JGBs and the cheaper yen. Politics could be a key driver of sentiment in Japan over the next few weeks.

Elsewhere, in energy, US crude failed to clear the 200-DMA yesterday and fell more than 2% – despite news that OPEC will stop adding extra barrels to the market after unwinding the last chunk of the 2.2mbpd cuts in September, fearing that too much oil would send prices to undesirably low levels.

Meanwhile, there’s chatter of stronger sanctions against Russia: Europe wants to cut the price cap on Russian oil from $60 to $45 per barrel, and a new bipartisan US bill proposes slapping 500% tariffs on goods from countries buying Russian oil. That would hit China and India – which together buy around 70% of Russian supply. Depending on how these EM giants react, demand for US and Brent crude could spike, pushing WTI and Brent prices higher. Alas, oil bulls are nowhere to be found this morning. Even news that the Red Sea is boiling again hasn’t helped. Key support for US crude remains at $65 per barrel, and for Brent at $67. Below those levels, oil will likely return to the first-half’s bearish trend.

UK GDP shrinks -0.1% mom in May, but underlying momentum still holds

UK GDP unexpectedly contracted by -0.1% mom in May, missing expectations for 0.1% mom growth. The weakness was driven by a sharp -0.9% mom drop in industrial production and a -0.6% mom fall in construction output, partially offset by a modest 0.1% mom gain in services—the largest sector of the economy.

Still, broader momentum remains positive. Real GDP rose 0.5% in the three months to May, thanks to steady growth in services (+0.4%) and solid gains in construction (+1.2%). Production also rose 0.2%.

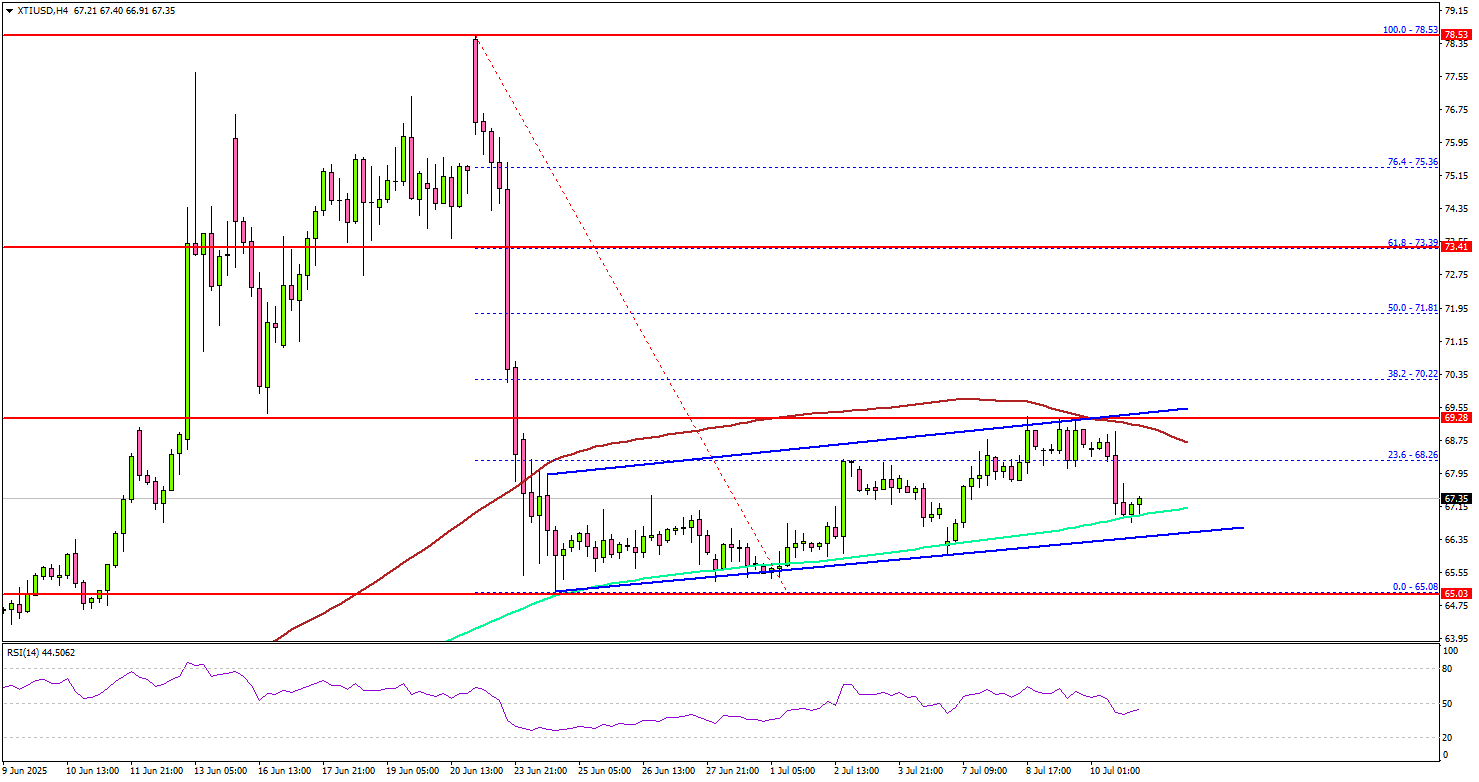

WTI Crude Oil at Risk — More Downside Could Be Coming

Key Highlights

- WTI Crude Oil prices started a fresh decline below the $70.00 zone.

- A rising channel is forming with support at $66.50 on the 4-hour chart.

- Gold bulls are struggling to clear the $3,350 resistance.

- EUR/USD extended losses and corrected below the 1.1720 zone.

WTI Crude Oil Price Technical Analysis

WTI Crude Oil price failed to continue higher above $72.50 against the US Dollar. There was a strong bearish reaction below the $70.00 and $68.00 levels.

Looking at the 4-hour chart of XTI/USD, the price settled below the $70.00 level and the 100 simple moving average (red, 4-hour). A low was formed at $65.00, and the price recently started a consolidation phase.

There was a move above the $68.00 level, but the bears remained active near the 100 simple moving average (red, 4-hour). On the upside, immediate resistance is near the $68.0 level. The first key resistance sits near the $70.00 level.

The main hurdle is now near the $71.80 zone, above which the price may perhaps accelerate higher. In the stated case, it could even visit the $73.50 resistance. Any more gains might call for a test of the $75.00 resistance zone in the near term.

On the downside, the first major support sits near the $66.20 zone. The next support could be $65.00. A daily close below $65.00 could open the doors for a larger decline. The next major support is $63.40. Any more losses might send oil prices toward $62.00 in the coming days.

Looking at Gold, the bears are active below the $3,650 level, and they might aim for a drop toward the $3,260 level.

Economic Releases to Watch Today

- USDA WASDE Report.

- Baker Hughes US Oil Rig Count.

- Monthly Budget Statement (Jun).

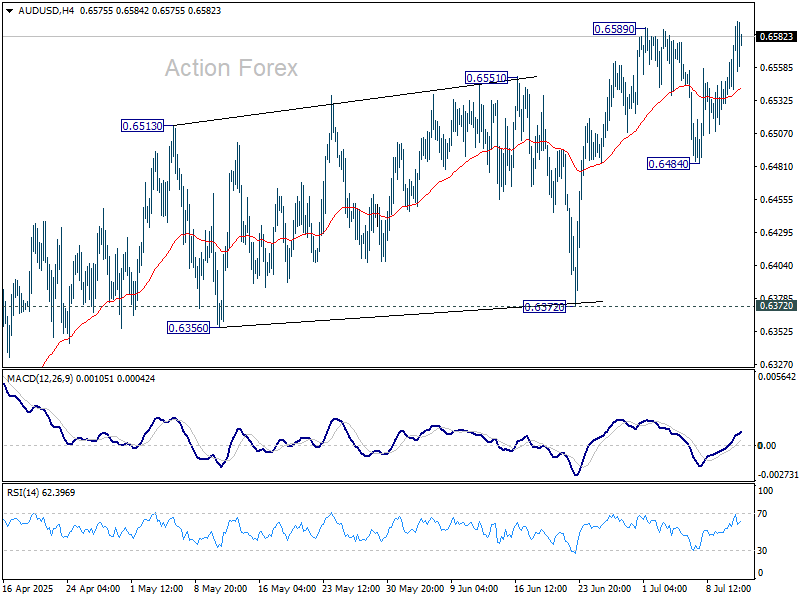

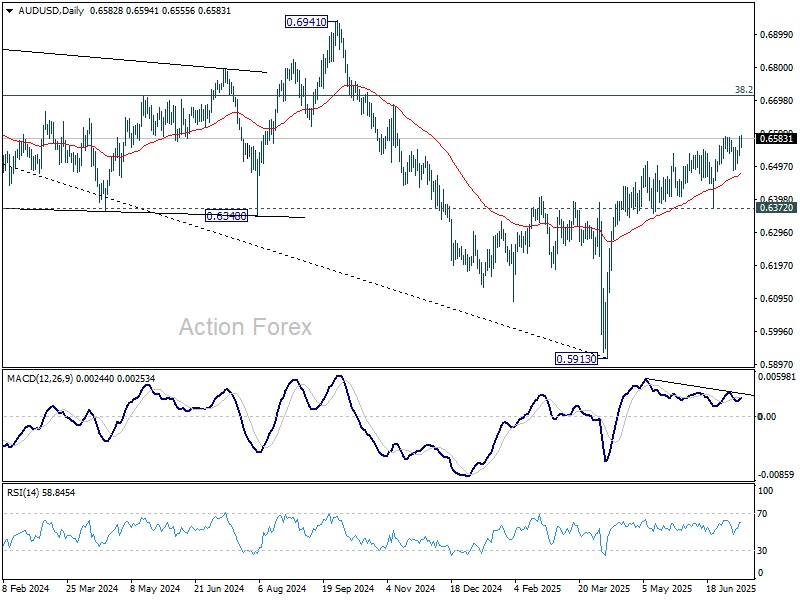

AUD/USD Daily Report

Daily Pivots: (S1) 0.6548; (P) 0.6570; (R1) 0.6611; More...

AUD/USD's rally resumed by breaching 0.6589 and intraday bias is back on the upside. Rise from 0.5913 should target 0.6713 fibonacci level next. ON the downside, however, firm break of 0.6484 support will now indicate short term topping, and turn bias back to the downside for 0.6372 support.

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. While stronger rally cannot be ruled out, outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, even in case of another fall through 0.5913, downside should be contained above 0.5506 (2020 low).

Dollar Climbs as Trump Targets Canada, But Aussie Outshines

Dollar advanced broadly after US President Donald Trump escalated trade war again with a fresh 35% tariff on Canadian imports. The announcement cited Canadian retaliation and the fentanyl crisis as justification, while threatening even steeper duties if Ottawa imposes further countermeasures.

Trump’s sweeping tone extended beyond Canada. While 22 countries have received formal letters setting tariffs between 20% and 50%, Trump said countries not on that list could face “blanket” tariffs of 15% to 20%.

Despite Dollar’s strength, FX traders showed limited urgency, with USD/CAD drifting higher but lacking strong follow-through. It’s Aussie that overtook the spot of top-performing currency of the week, hitting a nine-month high against the greenback.

Aussie's rally reflects strong risk appetite as seen in record breaking stocks in the US and Europe. Expectations that Australia will fall on the lower end of Trump’s sweeping tariff measures are also lifting the Aussie. Additionally, RBA's cautiousness, which defied market expectations for a rate cut and opted for a hold this week, also provides some support.

RBA is likely to resume rate reduction in August, after getting the quarterly CPI report due July 30. Yet, given the complexity for US tariffs to ripple through the global supply chains, RBA would tread cautious ahead, and only ease policy in a measured pace.

On the broader performance chart, Yen continues to lag as the weakest currency this week, followed by Euro and Kiwi. The Swiss franc is quietly firm, ranking third behind Aussie and Dollar. Sterling and the Canadian Dollar are in the middle of the pack.

USD/CAD edged higher after the tariff nears but there is no clear follow through momentum. Technically, price actions from 1.3538 are seen as a corrective pattern, with rise from 1.3555 as the third leg. Further rally could be seen to 1.3797 and possibly above. However, break of 1.3637 will turn bias back to the downside for retesting 1.3538/3555 support zone instead.

In Asia, at the time of writing, Nikkei is up 0.02%. Hong Kong HSI is up 1.66%. China Shanghai SSE is up 0.87%. Singapore Strait Times is up 0.53%. Japan 10-year JGB yield is up 0.001 at 1.498. Overnight, DOW rose 0.43%. S&P 500 rose 0.27%. NASDAQ rose 0.09%. 10-year yield rose 0.004 to 4.346.

Fed's Waller backs July cut, rejects political motive in push for easing

Fed Governor Christopher Waller made a rare call for immediate easing, stating that inflation has fallen far enough to support a rate cut as early as this month. Speaking in Dallas overnight, Waller said the policy rate is "too tight" given current inflation dynamics and that July presents a viable window for action. “I just made the argument… we could consider cutting,” he said, while acknowledging he’s "kind of in the minority on this".

Waller dismissed concerns that recent tariffs should delay easing, noting that their impact has so far been narrow and contained. He emphasized that the Fed’s job is to respond to broad inflation trends, not isolated price spikes. “If inflation is coming down, you don’t need to be as restrictive anymore,” he said.

He also emphasized "it's not political", saying his position was grounded in economics. With inflation easing, a steady labor market, and the Fed’s rate still well above its long-run neutral level, Waller said a July move would be justified based on data alone.

Fed’s Daly sees two cuts in 2025, says tariff-driven inflation may not materialize

San Francisco Fed President Mary Daly said overnight that the time has come to seriously consider lowering interest rates, citing the need to preserve the current strength of the US economy. “I really am of the view that it’s time,” she said, adding that two rate cuts this year now look like a “likely outcome.” Nevertheless, Daly noted that her preferred timing points to a potential move in the fall, aligning her with the broader consensus on the FOMC, even if some colleagues are advocating for action as early as July.

Daly downplayed concerns that the latest wave of tariffs would necessarily spark inflation, arguing that companies are increasingly absorbing costs or adapting rather than fully passing them on. “It’s possible it just doesn’t materialize,” she said, referring to fears of lasting inflation driven by trade policy.

Cautioning against excessive delay, Daly warned that waiting for persistent inflation before acting could result in a policy mistake. “It’s useful now to sort of recognize that waiting for inflation to rise or become persistent could leave us behind,” she said, emphasizing her desire to stay ahead of the curve.

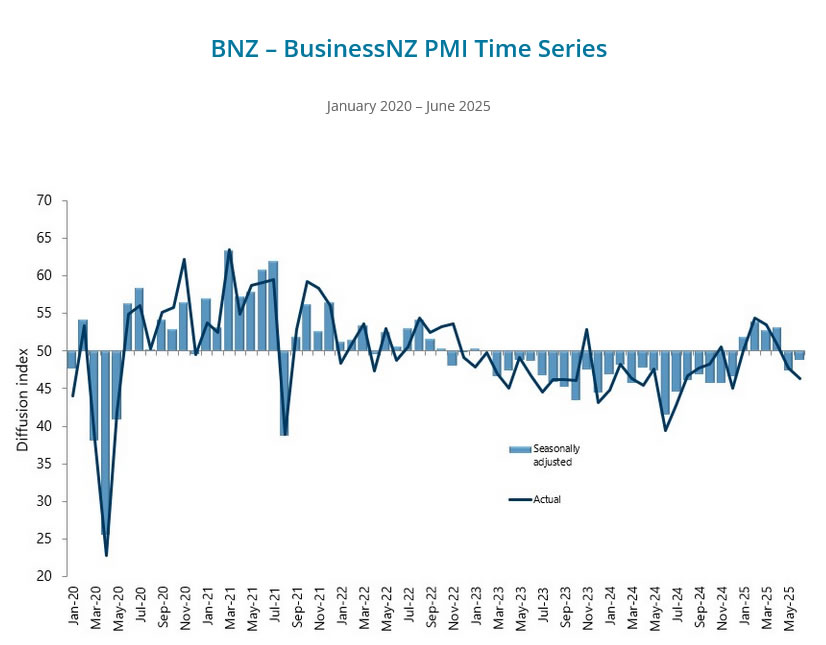

New Zealand BNZ manufacturing rises to 48.8, conditions still very tough

New Zealand’s manufacturing sector showed modest signs of stabilization in June, with the BusinessNZ Performance of Manufacturing Index rising from 47.4 to 48.8. While still signaling contraction, the gain was underpinned by an encouraging rebound in new orders, which jumped from 45.4 to 51.2—breaking back into expansion. Employment (47.9) and production (48.6) also improved slightly, though both remained under the 50 threshold. The headline PMI remains well below the historical average of 52.5.

The proportion of negative comments from respondents held steady at 65.5% (May 64.5), with widespread concerns over weak consumer demand, high living costs, and a murky economic outlook. Input cost pressures and a drop in construction activity also continue to weigh on manufacturing sentiment.

BNZ Senior Economist Doug Steel said that despite hopes of recovery, "conditions are still very tough." All key sub-indices remain below their long-run averages, highlighting that while some green shoots are emerging, the overall manufacturing environment is still struggling to gain traction.

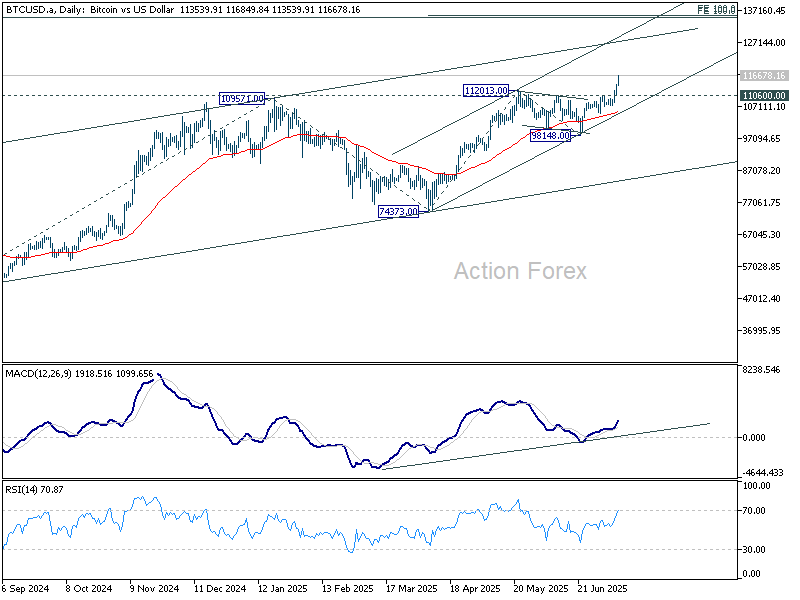

Bitcoin blasts to record ahead of House Crypto Week, 135k next

Bitcoin has broken decisively to a new all-time high with upside acceleration, confirming a bullish breakout from its recent consolidation range and setting sights on 135k level. The rally gained additional momentum as bullish sentiment grows ahead of “Crypto Week” in the US Congress, where the House Committee on Financial Services, led by the Republicans, plans to advance crypto-friendly legislation. The committee said the measures are designed to help position the US as the “crypto capital of the world.”

Behind the scenes, the rally continues to be supported by a trifecta of macro forces: rising institutional interest, increasing fiscal strain in the US, and a broadly dovish Fed outlook that is keeping real yields contained. Combined, these drivers are encouraging investors to seek alternatives and store-of-value assets like Bitcoin, with the added appeal of regulatory clarity possibly on the horizon.

Technically, near term outlook will now stay bullish as long as 11060 resistance turned support holds. Two major projection levels mark the next target zone at 135k, 100% projection of 49008 to 109571 from 74373 at 134946 and 100% projection of 74373 to 112013 from 98148 at 135788.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6548; (P) 0.6570; (R1) 0.6611; More...

AUD/USD's rally resumed by breaching 0.6589 and intraday bias is back on the upside. Rise from 0.5913 should target 0.6713 fibonacci level next. ON the downside, however, firm break of 0.6484 support will now indicate short term topping, and turn bias back to the downside for 0.6372 support.

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. While stronger rally cannot be ruled out, outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, even in case of another fall through 0.5913, downside should be contained above 0.5506 (2020 low).

Bitcoin blasts to record ahead of House Crypto Week, 135k next

Bitcoin has broken decisively to a new all-time high with upside acceleration, confirming a bullish breakout from its recent consolidation range and setting sights on 135k level. The rally gained additional momentum as bullish sentiment grows ahead of “Crypto Week” in the US Congress, where the House Committee on Financial Services, led by the Republicans, plans to advance crypto-friendly legislation. The committee said the measures are designed to help position the US as the “crypto capital of the world.”

Behind the scenes, the rally continues to be supported by a trifecta of macro forces: rising institutional interest, increasing fiscal strain in the US, and a broadly dovish Fed outlook that is keeping real yields contained. Combined, these drivers are encouraging investors to seek alternatives and store-of-value assets like Bitcoin, with the added appeal of regulatory clarity possibly on the horizon.

Technically, near term outlook will now stay bullish as long as 11060 resistance turned support holds. Two major projection levels mark the next target zone at 135k, 100% projection of 49008 to 109571 from 74373 at 134946 and 100% projection of 74373 to 112013 from 98148 at 135788.

New Zealand BNZ manufacturing rises to 48.8, conditions still very tough

New Zealand’s manufacturing sector showed modest signs of stabilization in June, with the BusinessNZ Performance of Manufacturing Index rising from 47.4 to 48.8. While still signaling contraction, the gain was underpinned by an encouraging rebound in new orders, which jumped from 45.4 to 51.2—breaking back into expansion. Employment (47.9) and production (48.6) also improved slightly, though both remained under the 50 threshold. The headline PMI remains well below the historical average of 52.5.

The proportion of negative comments from respondents held steady at 65.5% (May 64.5), with widespread concerns over weak consumer demand, high living costs, and a murky economic outlook. Input cost pressures and a drop in construction activity also continue to weigh on manufacturing sentiment.

BNZ Senior Economist Doug Steel said that despite hopes of recovery, "conditions are still very tough." All key sub-indices remain below their long-run averages, highlighting that while some green shoots are emerging, the overall manufacturing environment is still struggling to gain traction.