Sample Category Title

AUD/USD Daily Report

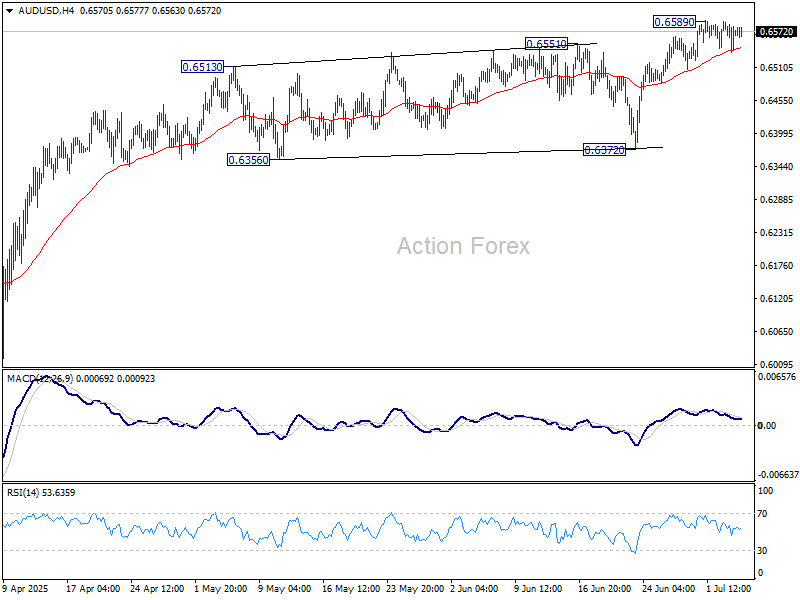

Daily Pivots: (S1) 0.6542; (P) 0.6566; (R1) 0.6594; More...

Intraday bias in AUD/USD remains neutral and consolidations from 0.6589 extends. Deeper retreat might be seen but outlook will remain bullish as long as 0.6372 support holds. Above 0.6589 will resume the rise from 0.5913 to 0.6713 fibonacci level.

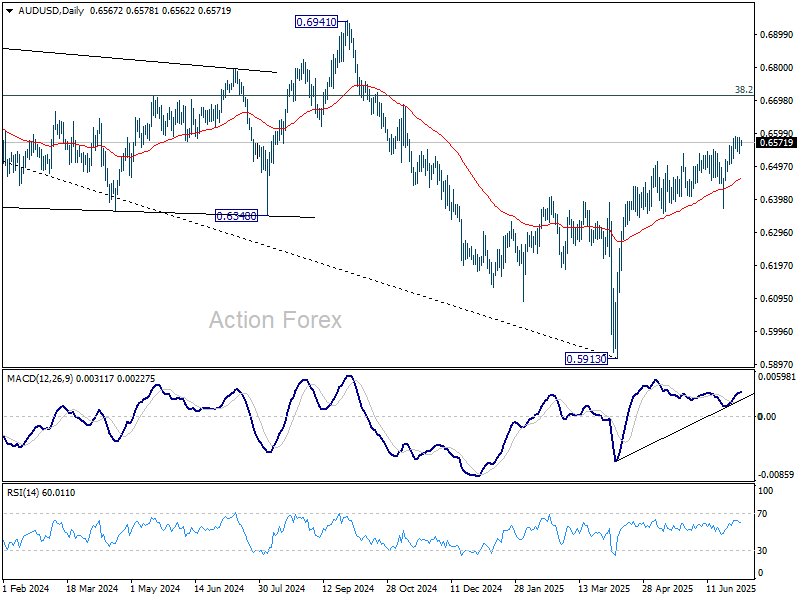

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. While stronger rally cannot be ruled out, outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, even in case of another fall through 0.5913, downside should be contained above 0.5506 (2020 low).

USD/JPY Daily Outlook

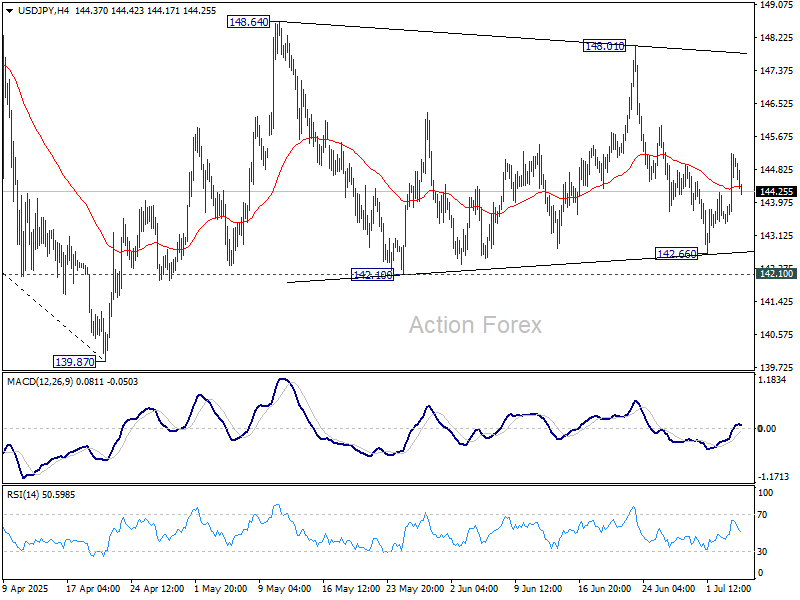

Daily Pivots: (S1) 143.84; (P) 144.53; (R1) 145.62; More...

Range trading continues in USD/JPY and intraday bias remains neutral. On the upside, firm break of 148.01 resistance will resume the rise from 139.87 to 61.8% retracement of 158.86 to 139.87 at 151.22. However, break of 142.10 will bring deeper fall back to retest 139.87 low.

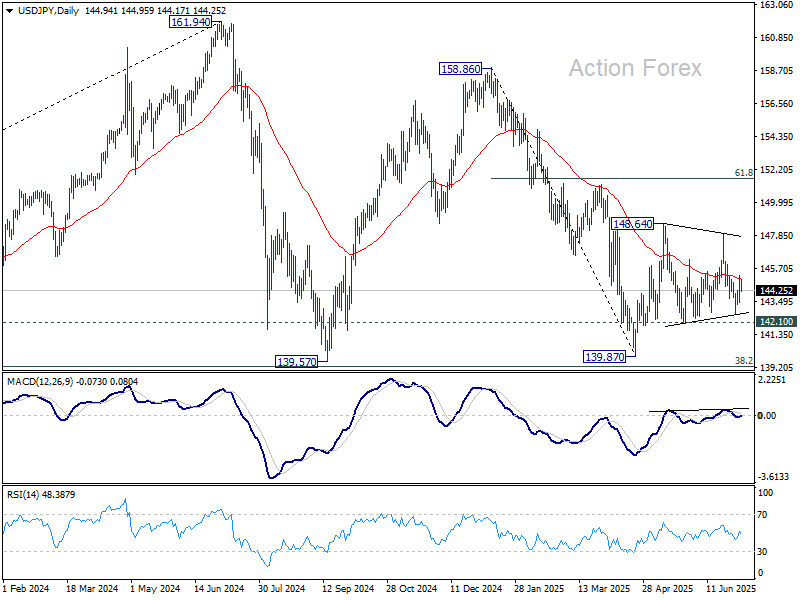

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

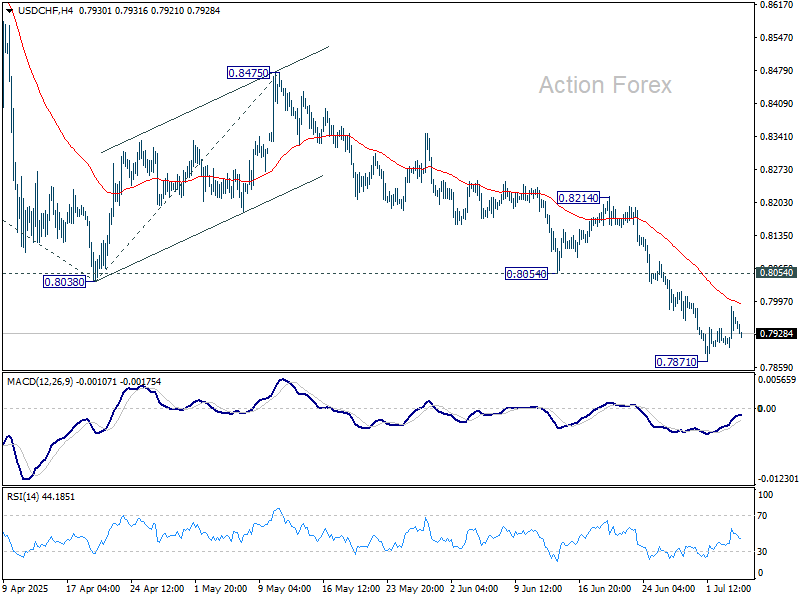

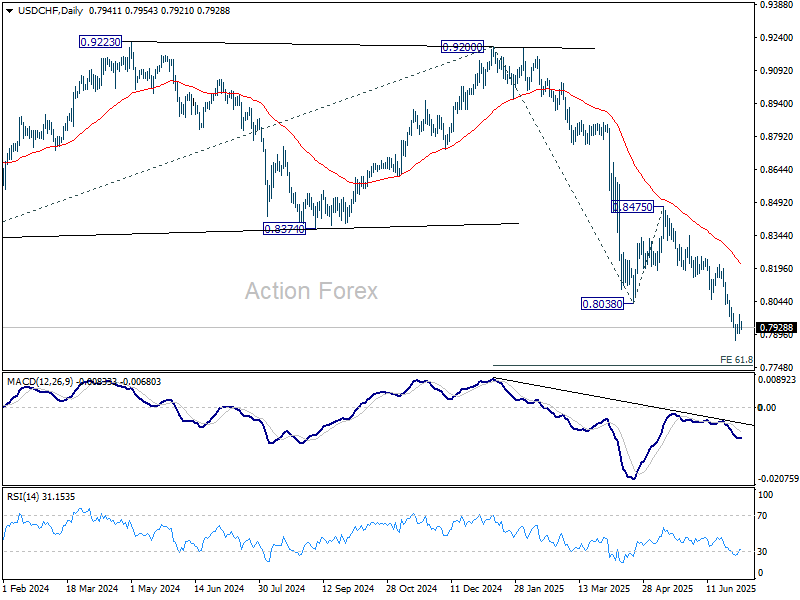

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7907; (P) 0.7947; (R1) 0.7993; More….

Intraday bias in USD/CHF remains neutral for the moment as consolidations continue above 0.7871. Stronger recovery cannot be ruled out, but upside should be limited by 0.8054 support turned resistance to bring another fall. Below 0.7871 will extend the larger down trend to 61.8% projection of 0.9200 to 0.8038 from 0.8475 at 0.7757. Firm break there will pave the way to 100% projection at 0.7313 next.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8475 resistance holds.

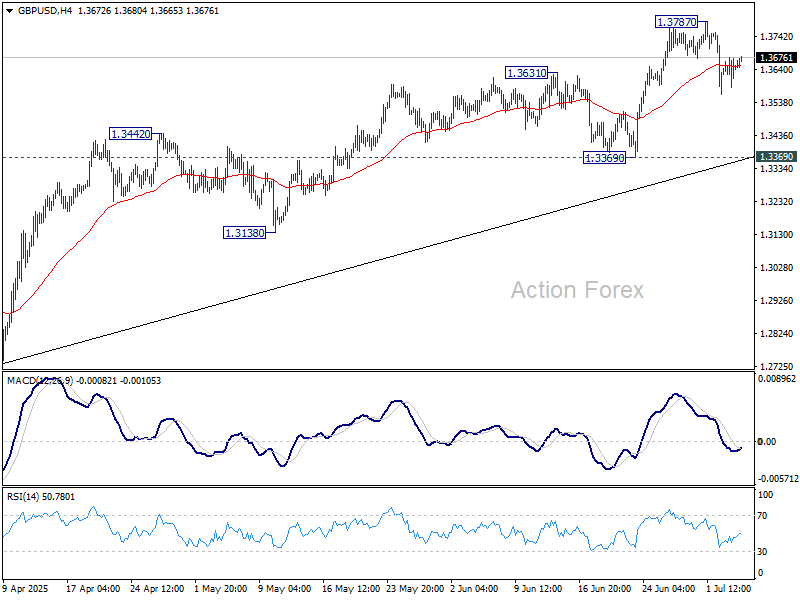

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3602; (P) 1.3639; (R1) 1.3692; More...

Intraday bias in GBP/USD stays neutral for the moment, and more consolidations could be seen below 1.3787. Deeper retreat cannot be ruled out, but downside should be contained above 1.3369 support to bring another rally. Firm break of 1.3787 will resume larger rise to 1.4004 projection level next.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.2983) holds, even in case of deep pullback.

Trade Narrative Back in Full Swing Now Trump’s Bill Got Approved

Markets

Hate him or love him, but US president Trump often gets things done. He wanted the OBBBA on his desk to be signed into law by July 4th, and he’s going to get it. The US House of Representatives greenlighted the Senate-amended version in a 218-214 vote after some arm-twisting (and probably backdoor sweeteners) yesterday. The price tag is huge: $3.4tn in additional federal deficits through 2034. This compares to a $1.8tn deficit, or well over 6% of GDP, in 2024. The debt ceiling will be raised by a whopping $5tn, which according to USTS Bessent “should get us well into 2027”. The House passage came after US trading hours (early close ahead of Independence Day) so a first real market reaction isn’t due until Monday. US rates nevertheless finished the day higher with net daily changes varying between 6 (30-yr) and almost 10 bps (2-yr). The bear flattening came in the wake of the payrolls report. Job growth and the unemployment rate came in better than expected but not for reasons tied to a strong economy per se. Local and state government jobs contributed to half of the net growth while people dropping out of the labour market resulted in the lower unemployment rate. The headline print nevertheless wrongfooted a more softly positioned market. The US non-manufacturing ISM released afterwards marginally topped consensus estimates as well and kept rates near the intraday highs. The headline number rose from 49.9 to 50.8 (50.5 expected) thanks to a rebound in new orders (51.3), general business activity (54.2). Employment was the weak link. The subindex dropped from 50.7 to 47.2. The US job report only temporarily interrupted the grind lower in European yield markets. Swap rates closed up to 4 bps lower, the belly of the curve outperforming the wings. The greenback’s performance given the rates divergence was poor. EUR/USD eased from 1.18 to 1.176 while DXY (97.18) continues to struggle near the lows. Part of the dollar gains are already being undone during the Asian session. The pound recovered somewhat of Wednesday’s hit along with long-term gilts but we’re wary for a sustained comeback. The fiscal debate is casting a shadow over UK assets.

The trade narrative is back in full swing now Trump’s bill got approved. The US president said he’ll start sending letters today in which he’ll set the tariff level unilaterally going into the July 9 deadline. Trump floated a rate between 10 and 70%. Countries that dodge the bullet with a trade deal so far are the UK and Vietnam. The US-Sino trade truce runs through mid-August. Talks with Japan have been frustrating Trump lately while those with the EU are running in the background and scheduled to continue over the weekend. An extension to the deadline is not being considered, Trump said, so the stakes are high. We could therefore see markets err to the side of caution, be it in thinned volumes due to the absence of US investors.

News & Views

National Bank of Poland President Glapinski yesterday labeled Wednesday’s unexpected 25 bps rate cut from 5.25% to 5% as a “cautious adjustment” and not the start of an easing cycle. The NBP lowered its policy rate with the backing of lower CPI projections, especially for this year, with inflation expected to fall within the 1%-point tolerance band around the 2.5% inflation target in coming months. The tone of the policy statement opened the door for a sequence of rate cut, but Glapinski closed that with his hawkish comments. He highlighted inflation risks coming from loose fiscal spending, energy prices and trade tensions. The zloty profited from the conflicting U-turn and erased all of Wednesday’s losses, ending the day at EUR/PLN 4.24 from 4.2650. A rebound in Polish swap rates was short-lived as Glapinski nevertheless offered a path to a September rate cut. The curve bull steepened again with daily losses of up to 8 bps at the front end of the curve (19 bps 2-day cumulative).

UK Chancellor Reeves is expected to announce a shake-up of UK pensions in her Mansion House speech on July 15 including plans to look at the amount companies and their staff set aside for retirement, according to reporting by the Financial Times. The review was initially expected by the end of 2024 but delayed after an angry backlash over the £25bn increase in National Insurance contributions announced in last year’s autumn Budget.

Big, Fat Bill

It’s another day, another record for the S&P 500 and Nasdaq 100, while the Dow Jones hovers just a few points shy of its own all-time high. Small- and mid-cap stocks are also better bid—though still well below their post-election highs. Remarkably, all this optimism comes despite stronger-than-expected employment data that crushed any near-term hopes of a July Federal Reserve (Fed) rate cut. The odds of such a move dropped from around 27% to just 5% following the data.

The US 2-year Treasury yield—often seen as a proxy for Fed expectations—jumped more than 10 basis points to 3.90%, while the 10-year yield rose above 4.35%. The US dollar rebounded.

If the post-data rally surprised you, you weren’t alone.

Looking under the hood, the data wasn’t quite as impressive as the headline numbers suggested. The US economy added 147,000 nonfarm jobs, but a large portion came from public education—not typically viewed as a barometer of sustained economic momentum. Meanwhile, the unemployment rate unexpectedly fell from 4.2% to 4.1% (vs. expectations of a rise to 4.3%), but this was largely due to around 130,000 workers leaving the labour force.

So while the initial numbers looked robust, the details told a more mixed story.

On the other hand—as flagged earlier this week—the revisions to previous months' data surprised to the upside, and wage growth slowed more than expected. Average hourly earnings declined on both a monthly and yearly basis, marking the slowest pace since last summer—a welcome sign for the Fed in its battle against inflation.

But this time, it's not wage pressures that threaten to reignite US inflation—it's tariffs.

The US-Vietnam trade agreement announced this week includes 20% tariffs on Vietnamese goods and 40% if those goods are transshipped through Vietnam, offering a strong signal that upcoming tariffs won’t hover near the universal 10% mark, they will be higher. These higher tariffs are expected to be inflationary, unless companies choose to absorb the costs—a strategy some may adopt to protect market share, but likely not a sustainable one.

Realistically, trump is redrawing global trade dynamics, and they are likely to add upward pressure on US inflation.

A big, fat bill

In parallel, Trump has just secured passage of his signature $3.3 trillion tax package last night. The bill narrowly passed and is expected to be signed later today—Independence Day—adding political theatre to fiscal policy.

This tax package is projected to push the US national debt past $40 trillion in the coming years, a looming concern for global investors. Should foreign appetite for US debt fade—as the UK’s recent experience has shown—it could raise long-term borrowing costs and put pressure on US Treasuries. That, in turn, could dampen risk appetite and increase the likelihood of a market correction, particularly given current lofty valuations.

While US bond markets are closed today, gold has reclaimed its 50-day moving average this week and is trending higher on the back of trade tensions and debt concerns. US and European equity futures are pointing lower, suggesting the week will end on a cautious note, with investors awaiting the final US tariff announcements—which are unlikely to please.

Whether that matters for risk assets remains to be seen. In recent months, markets have increasingly defied textbook reactions, raising fresh concerns about how sustainable this rally really is.

FX and Energy

The US dollar is giving back some of Thursday’s gains amid trade and fiscal uncertainty. The EURUSD is consolidating just below 1.18 and Cable is better bid following confirmation that Rachel Reeves will stay on as Chancellor, easing fears of a more aggressive fiscal push. While the mini-gilt stress was swiftly contained, the 10-year gilt yield remains near levels seen during the Truss-era budget turmoil, and high borrowing costs could constrain UK’s growth prospects, hence limit sterling’s upside.

In Japan, the USDJPY is trading lower after annual wage negotiations concluded with a 5.25% average wage increase—the highest in 34 years. Household spending also jumped significantly last month, reinforcing expectations for a hawkish Bank of Japan (BoJ). The Nikkei is down on tighter policy bets and growing trade concerns with the US.

Elsewhere, US crude is consolidating near the $67 per barrel mark. Bears are back in control this morning following reports that US–Iran nuclear talks are resuming and that OPEC+ is expected to announce a production increase of 411K barrels/day this weekend. While rising supply and softening demand suggest a move back below $65/bbl, the strong support seen this week near that level hints that any downside might take longer to materialize.

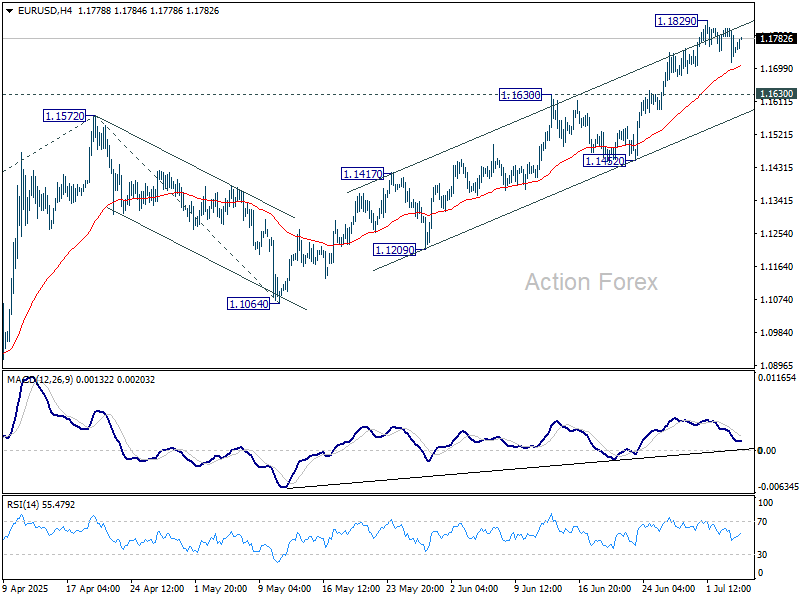

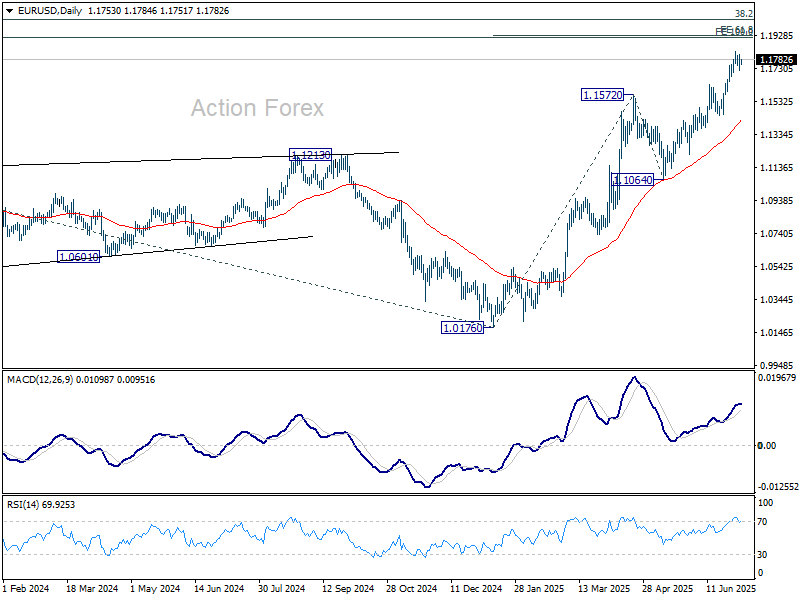

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1713; (P) 1.1762; (R1) 1.1805; More...

EUR/USD is staying below 1.1829 despite today's recovery. Intraday bias remains neutral and more consolidations could be seen. Deeper retreat cannot be ruled out, but downside should be contained by 1.1630 resistance turned support to bring another rally. On the upside, break of 1.1829 will target 61.8% projection of 1.0176 to 1.1572 from 1.1064 at 1.1927.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 1.1604 support holds.

Dollar Bounce Short-Lived as Eyes Turn to Trump’s Trade Salvo

Dollar’s rebound on upbeat US jobs and services data proved short-lived, as the greenback faded again in early Friday trading. The greenback failed to hold gains amid a broader risk-on tone with both S&P 500 and NASDAQ closed at fresh record highs.

Strong employment data gave policymakers room to wait, especially as they assess the fallout from tariffs following the July 9 truce deadline. Futures markets now assign a 95% probability Fed will hold rates steady at this month’s meeting. Meanwhile, expectations for aggressive easing are also fading. Markets now price in less than a 40% chance of three cuts in 2025, compared to higher odds earlier this month. Even so, reduced Fed cut expectations haven’t translated into Dollar strength.

The greenback also found no lift from Washington. The House narrowly passed President Donald Trump’s tax-and-spending bill, marking a major political win but also reviving deficit concerns. The IMF flagged the bill’s likely impact on worsening the fiscal outlook, noting in its press briefing that fiscal consolidation remains a priority the US has yet to address. The Fund will update its growth projections in late July to reflect the bill’s effects.

On trade, Trump escalated his tactics by announcing that tariff letters will be sent out to individual countries starting today. This would mark a clear pivot from deal-based diplomacy toward flat-rate enforcement. Each country will reportedly be told what tariff rates — typically between 20% and 30%. Trump called the unilateral approach “easier” and “more efficient.”

For the week so far, Sterling is still the weakest major currency. Dollar ranks second from the bottom, just ahead of Yen. Loonie leads the performance board, followed by Swiss Franc and Aussie. Euro and Kiwi are holding middle ground as the week winds down.

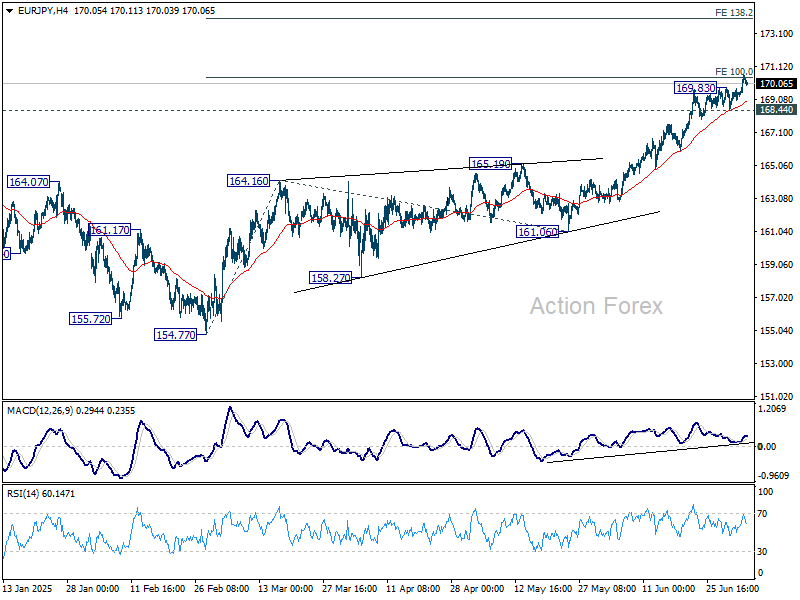

Technically, EUR/JPY's rally resumed after brief consolidations and met 100% projection of 154.77 to 164.16 from 161.06 at 170.45. Further rally is expected as long as 168.44 support holds. Firm break of 170.45 will pave the way to 138.2% projection at 174.03.

In Asia, at the time of writing, Nikkei is up 0.12%. Hong Kong HSI is down -0.20%. China Shanghai SSE is up 0.87%. Singapore Strait Times is down -0.25%. Japan 10-year JGB yield is up 0.014 at 1.457. Overnight, DOW rose 0.77%. S&P 500 rose 0.83%. NASDAQ rose 1.02%. 10-year yield rose 0.055 to 4.348.

Japan household spending surges 4.7% yoy in May, fastest in bearly three years

Japan’s household spending rose 4.7% yoy in May, sharply above expectations of 1.2% yoy and marking the fastest pace of growth since August 2022. Seasonally adjusted monthly spending also surged 4.6% mom, well ahead of the 0.4% mom consensus and the strongest gain since March 2021. The internal affairs ministry attributed the jump to robust demand for cars, dining out, and summer-related appliances.

By category, transportation and communications spending soared 25.3% yoy, while recreation and leisure climbed 11.1% yoy. Furniture and home appliance purchases rose 9.3% yoy as households prepared for a hot summer. Food spending, which accounts for nearly a third of total consumption, rose 1.0% yoy as price pressures eased and dining out increased.

Officials highlighted that the three-month moving average of household spending has remained positive since December 2024, suggesting a durable recovery in consumer demand.

Fed's Bostic sees prolonged inflation from tariff impact

Fed’s Raphael Bostic signaled strong resistance to near-term rate cuts, citing uncertainty around trade policy and a still-resilient US economy. “This is no time for significant shifts in monetary policy,” he said, emphasizing that the FOMC should avoid decisions it may be forced to "quickly reverse". With macro conditions steady, Bostic sees “space for patience” while waiting for greater clarity.

The Atlanta Fed chief pushed back on assumptions that the economic impact of Trump administration’s tariff and fiscal policies would be "a short and simple one-time shift in prices". Instead, he argued that the adjustment process will likely take a year or more, and that both prices and growth may respond in drawn-out, non-linear ways. The implication is that the economy may undergo a “longer period of elevated inflation readings” as it digests structural shifts.

Bostic remains at the cautious end of the FOMC, projecting just one rate cut this year—compared to the median forecast of two.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1713; (P) 1.1762; (R1) 1.1805; More...

EUR/USD is staying below 1.1829 despite today's recovery. Intraday bias remains neutral and more consolidations could be seen. Deeper retreat cannot be ruled out, but downside should be contained by 1.1630 resistance turned support to bring another rally. On the upside, break of 1.1829 will target 61.8% projection of 1.0176 to 1.1572 from 1.1064 at 1.1927.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 1.1604 support holds.

Elliott Wave Outlook: S&P 500 ($SPX) Nests Upward in Strong Rally

Since bottoming out on April 7, 2025, following the tariff war selloff, the S&P 500 (SPX) has sustained a robust rally. The Index is reaching new all-time highs in a clear Elliott Wave impulsive structure. Technical analysis, particularly momentum indicators like the Relative Strength Index (RSI), shows no divergence at the latest peak. This indicates sustained bullish momentum and suggests the rally remains within the third wave of the Elliott Wave sequence. From the April 7 low, wave 1 concluded at 5968.6. A corrective wave 2 followed which ended at 5767.41. The index has since nested higher within wave 3, demonstrating strong upward momentum.

Breaking down the substructure of wave 3, the hourly chart below reveals that wave ((i)) peaked at 6059.4. The subsequent pullback in wave ((ii)) unfolded as a zigzag pattern. Wave (a) declined to 5963.21, and wave (b) rebounded to 6050.83. Wave (c) concluded at 5941.4, completing wave ((ii)) in the higher degree. The index has since resumed its ascent in wave ((iii)). Up from wave ((ii)), wave (i) reached 215.08 and a minor pullback in wave (ii) ended at 6177.97.

The SPX is expected to continue its upward trajectory, with potential pullbacks finding support in a 3, 7, or 11 swing against the 5941.4 level, setting the stage for further gains. This analysis underscores the index’s bullish outlook, supported by technical indicators and Elliott Wave structure, as it navigates higher within this impulsive cycle.

S&P 500 (SPX) 60-Minute Elliott Wave Technical Chart

SPX Elliott Wave Technical Video

https://www.youtube.com/watch?v=5IJ9fBrfNdo

Japan household spending surges 4.7% yoy in May, fastest in nearly three years

Japan’s household spending rose 4.7% yoy in May, sharply above expectations of 1.2% yoy and marking the fastest pace of growth since August 2022. Seasonally adjusted monthly spending also surged 4.6% mom, well ahead of the 0.4% mom consensus and the strongest gain since March 2021. The internal affairs ministry attributed the jump to robust demand for cars, dining out, and summer-related appliances.

By category, transportation and communications spending soared 25.3% yoy, while recreation and leisure climbed 11.1% yoy. Furniture and home appliance purchases rose 9.3% yoy as households prepared for a hot summer. Food spending, which accounts for nearly a third of total consumption, rose 1.0% yoy as price pressures eased and dining out increased.

Officials highlighted that the three-month moving average of household spending has remained positive since December 2024, suggesting a durable recovery in consumer demand.