Sample Category Title

Fed’s Bostic sees prolonged inflation from tariff impact

Fed’s Raphael Bostic signaled strong resistance to near-term rate cuts, citing uncertainty around trade policy and a still-resilient US economy. “This is no time for significant shifts in monetary policy,” he said, emphasizing that the FOMC should avoid decisions it may be forced to "quickly reverse". With macro conditions steady, Bostic sees “space for patience” while waiting for greater clarity.

The Atlanta Fed chief pushed back on assumptions that the economic impact of Trump administration’s tariff and fiscal policies would be "a short and simple one-time shift in prices". Instead, he argued that the adjustment process will likely take a year or more, and that both prices and growth may respond in drawn-out, non-linear ways. The implication is that the economy may undergo a “longer period of elevated inflation readings” as it digests structural shifts.

Bostic remains at the cautious end of the FOMC, projecting just one rate cut this year—compared to the median forecast of two.

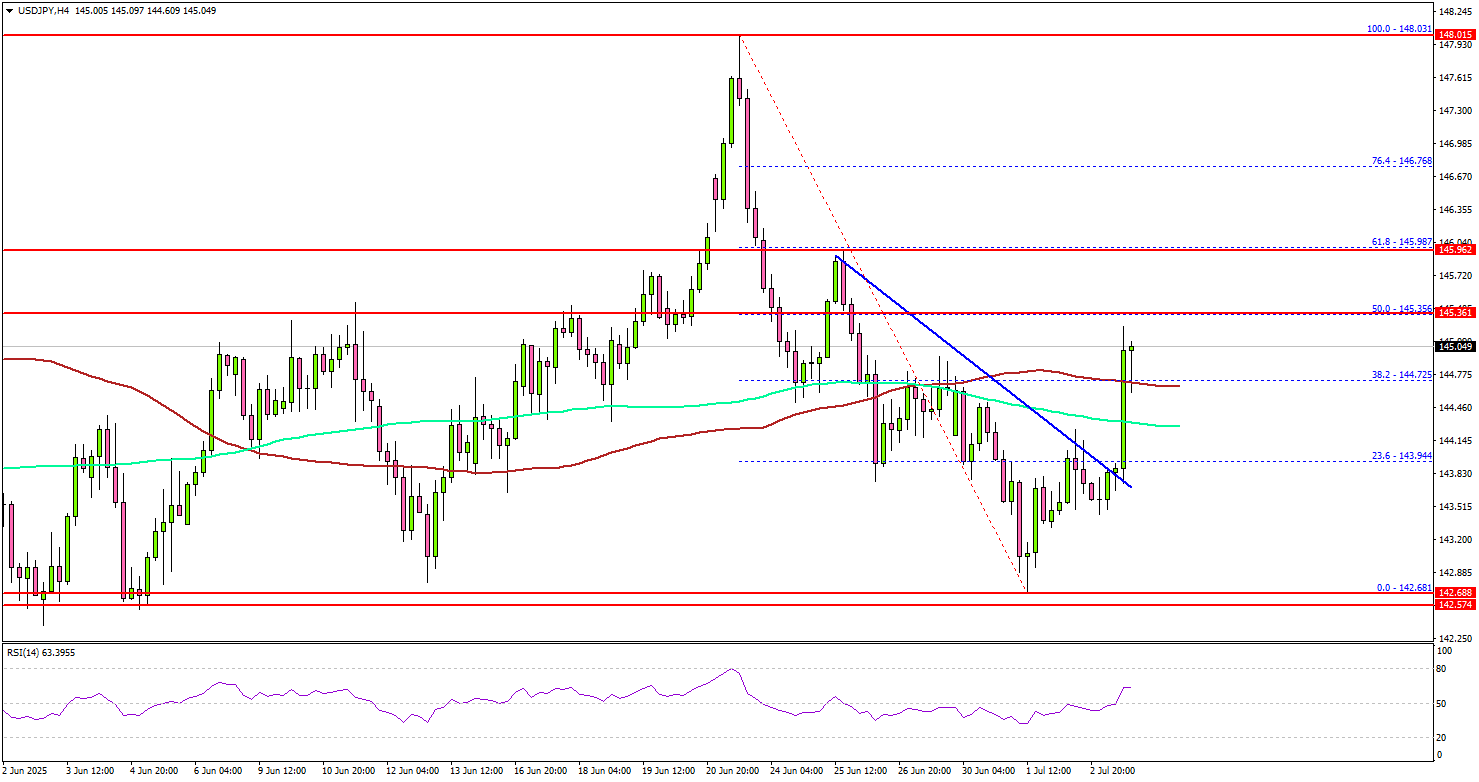

USD/JPY Regains Strength, Path Clear for More Gains?

Key Highlights

- USD/JPY started a fresh increase above the 144.00 resistance.

- It cleared a key bearish trend line with resistance at 143.80 on the 4-hour chart.

- EUR/USD started a downside correction from the 1.1820 zone.

- GBP/USD also corrected some gains and dipped below 1.3650.

USD/JPY Technical Analysis

The US Dollar found support near 142.65 and started a fresh increase against the Japanese Yen. USD/JPY climbed above the 143.50 and 144.00 levels.

Looking at the 4-hour chart, the pair cleared a key bearish trend line with resistance at 143.80. There was a move above the 38.2% Fib retracement level of the downward move from the 148.03 swing high to the 142.68 low.

The pair settled above the 100 simple moving average (red, 4-hour) and the 200 simple moving average (green, 4-hour). On the upside, the pair could face resistance near the 145.35 level. The next key resistance sits near the 146.00 level and the 61.8% Fib retracement level of the downward move from the 148.03 swing high to the 142.68 low.

A close above the 136.00 level could set the pace for another increase. In the stated case, the pair could even clear the 146.75 resistance. The next major stop for the bulls could be near the 147.50 resistance.

On the downside, immediate support is near the 144.40 level and the 200 simple moving average (green, 4-hour). The next key support sits near 143.80. Any more losses could send the pair toward the 143.20 support zone.

Looking at EUR/USD, the pair failed to extend gains above the 1.1820 resistance and recently started a consolidation and correction phase.

Upcoming Economic Events:

- ECB's Elderson speech.

- BoE's Taylor speech.

The Weekly Bottom Line: Signs of Waning Economic Resilience

Canadian Highlights

- This Canada Day week brought renewed trade drama, as the federal government dropped the Digital Services Tax, helping ease tensions and restart negotiations with the U.S.

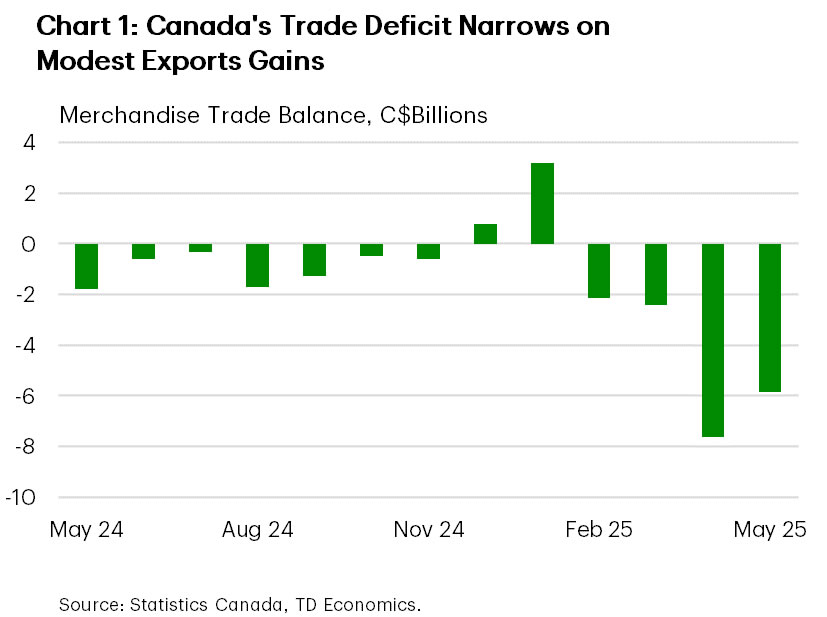

- Relief was limited in May’s trade data. While the merchandise trade balance improved modestly, it remains weak, reinforcing our forecast for a Q2 GDP contraction.

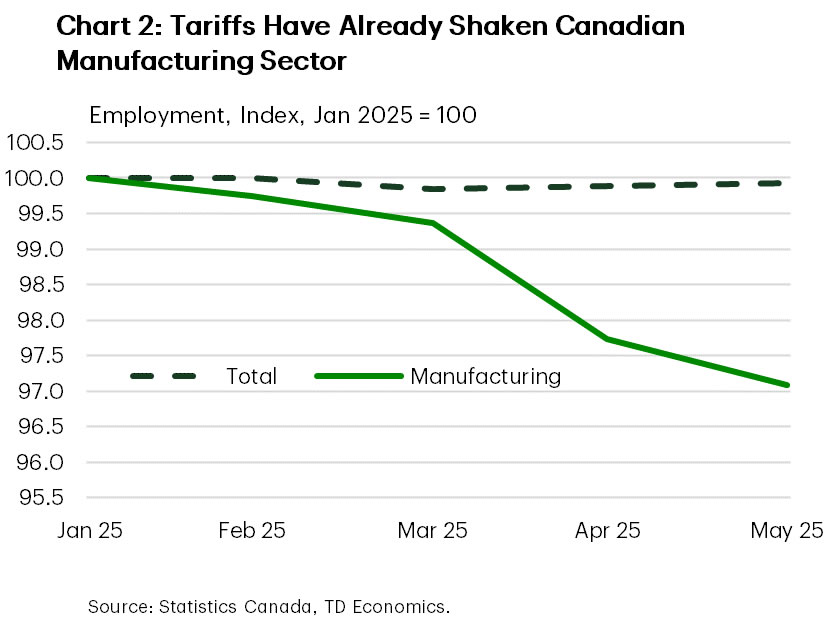

- Next week’s jobs report will offer another perspective into how deep the economic damage from tariffs runs. We expect enough evidence to support further Bank of Canada cuts in the third quarter.

U.S. Highlights

- Auto sales declined for the third consecutive month in June, as purchases continued to pull back following the pre-tariff rush to buy.

- Both manufacturing and non-manufacturing ISM sentiment indexes improved in June, but remained at low levels amid lingering trade uncertainty. Hiring intentions remained subdued, and prices stayed elevated.

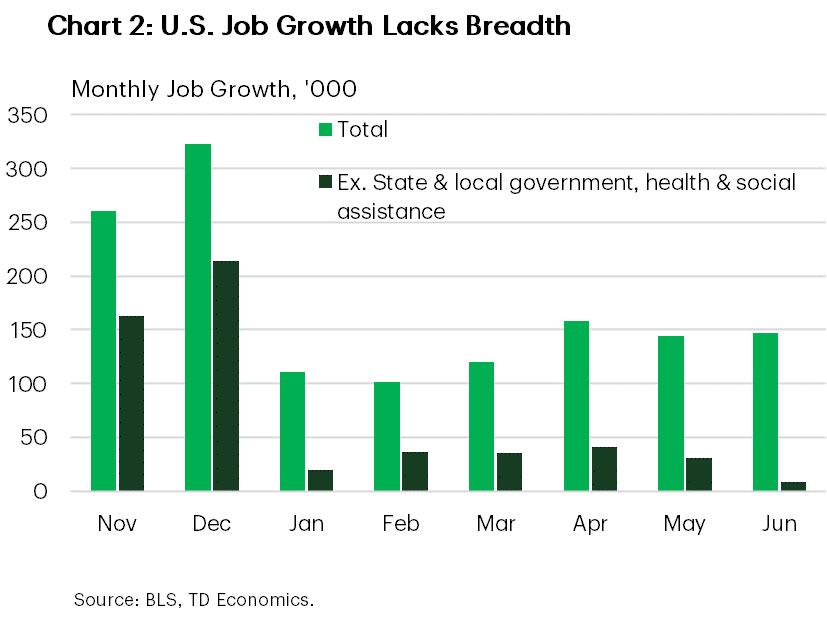

- The labor market continued to add jobs in June. Payrolls rose by 147k—well-above the 110k consensus—but gains were heavily concentrated in state & local government and healthcare & social assistance.

Canada – Trade Moves Back into the Spotlight

This Canada Day week may have been light on data, but surely didn’t lack the drama. It began with the federal government’s eleventh-hour decision to cancel the Digital Services Tax (DST), originally set to take effect on Monday, and to rescind the legislation once Parliament resumes. The move thawed tensions with the Trump administration. Markets responded positively, with the S&P/TSX Index resuming its climb and ending the week up almost 1%. The Canadian dollar also popped on the news but has since edged back.

The DST might have served as a future bargaining chip, but its withdrawal was a no-brainer. The tax – retroactive to January 2022 – was projected to raise $7.2 billion, but scrapping it adds less than two-tenths of a percentage point to the debt-to-GDP ratio, a negligible shift in the grand scheme. For trade talks, however, it was a thorn that had to be removed. Moreover, the DST risked backfiring on domestic firms and consumers. Tech giants were almost certain to pass on the cost, and some – like Amazon – may have already implemented Canada-specific surcharges.

The decision is widely seen as a compromise to restore momentum in trade negotiations with the U.S. and ease tensions between the two nations, with a goal of reaching a trade deal by July 21st. But signs of relief were scant in the May trade data. The merchandise trade balance improved modestly, with exports rebounding slightly and imports falling for the fourth consecutive month. As a result, the deficit narrowed to $5.9 billion from $7.1 billion in April (Chart 1). This net trade component is expected to subtract substantially from GDP in the second quarter, reinforcing our view of a Q2 contraction.

From an industry perspective, the rebound in exports was driven by higher sales of metal and non-metallic mineral products, particularly shipments of unwrought gold to the UK. Exports of consumer goods also made a notable contribution. On the import side, the weakness was concentrated in metals and mineral products, as well as in passenger cars and light trucks, imports of which fell to their lowest level in over two years.

Meanwhile, Canada’s merchandise trade surplus with the U.S. widened slightly, as imports declined more than exports. Gains in sales to non-U.S. markets were encouraging and have helped cushion the blow in recent months, but not enough to fully offset the drop with our largest trading partner.

The damage from fraying trade relations will continue unfolding. Next week’s jobs report will offer another perspective into how deep that damage runs. So far, total employment has moved sideways rather than down, but under the surface, cracks are evident. Employment in trade-intensive sectors like manufacturing is down nearly 3% since January (Chart 2). Should this weakness spread, the Bank of Canada is likely to respond – with two additional rate cuts before the end of Q3.

U.S. – Signs of Waning Economic Resilience

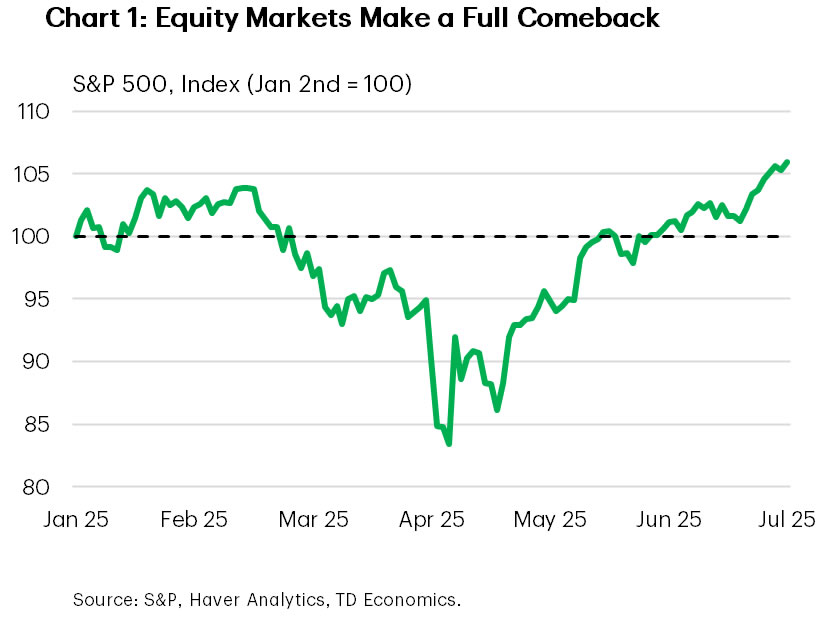

Monday marked the end of a volatile quarter in financial markets. After a 25% peak-to-trough decline from February to April, the S&P 500 has fully recovered, reaching new record highs (Chart 1). The 90-day pause on “Liberation Day” tariffs, a tentative truce with China, signs of economic resilience, and limited tariff pass-through to consumer prices thus far have helped to fuel the recovery.

However, uncertainty looms with the pause on the “Liberation Day” tariffs set to expire next week. President Trump has signalled a firm stance on the July 9th deadline, and recently threatened higher tariffs on Japanese imports. Lingering uncertainty on Section 232 tariffs — affecting lumber, copper, pharmaceuticals, and critical minerals — will further complicate matters. Trump recently halted trade talks with Canada, before resuming them when Canada canceled its Digital Service Tax. President Trump did announce a framework trade deal with Vietnam on social media. The U.S. will impose 20% tariffs on imports from the Vietnam and a 40% levy on any goods that are “transshipped” via this country in order to prevent Chinese goods from entering the U.S. via backdoor routes. So far, the UK and Vietnam are the only countries to get deals ahead of the deadline.

Domestically, the U.S. economy has shown resilience, but recent data revisions suggest it may not be as robust as initially believed. Q1 consumer spending growth was downgraded to 0.5% annualized, down from 1.2%. Spending is tracking weaker than forecast for the second quarter. Consumer spending slowed in April and declined in May, with much of the softness stemming from goods, which saw front-loaded demand ahead of tariffs. Auto sales declined for the third straight month in June, adding downside risk to activity. Services spending has also been lackluster, rising just 0.1% in April and remaining flat in May.

The labor market has been a relative bright spot, but is also showing signs of strain. Slowing immigration and weak population growth may be encouraging employers to hold onto workers, limiting layoffs — the unemployment rate remained little changed. June payrolls rose by 147k—above the 110k consensus—but gains were heavily concentrated in state and local government (+74k) and healthcare & social assistance (+60k). Excluding these two non-cyclical sectors, employment was nearly flat, suggesting continued private-sector hesitation (Chart 2).

ISM survey data also points to modest economic activity. Both the manufacturing and services indices improved slightly in June, but remained at low levels. Manufacturing remained in contraction, while services returned to expansion after a brief dip in May. Price pressures persisted in both sectors, especially for manufacturers, where input costs continue to rise. Employment subcomponents fell further into contraction, signaling reluctance to expand payrolls.

Overall, this week’s data is unlikely to shift the Fed from its patient stance. Activity is softening, but not collapsing. We share the market’s view that the Fed will likely keep monitoring inflation developments before making any policy moves, with September remaining the most likely decision point.

Weekly Economic & Financial Commentary: The One Big Beautiful Bill Endgame

Summary

- United States: Perhaps the Key to Economic Happiness Is Low Expectations

A better-than-expected jobs report owes much to big gains in just a few categories, while the trend ascent in continuing jobless claims still points to slowing momentum in the labor market. Meanwhile, tariff impact continues to weigh on trade activity and is top of mind for purchasing managers.

- Next week: NFIB (Tue.), Initial Jobless Claims (Thu.)

International: From Asia to Europe: Business Sentiment, Inflation Trends and Policy Shifts

- This week’s business sentiment surveys showed modest improvement in China PMIs, while Japan’s Tankan survey beat expectations, supporting the case for a Bank of Japan rate hike later this year. On the price front, Eurozone inflation was in line with consensus expectations, while Switzerland’s CPI surprised to the upside. Meanwhile, Poland’s central bank unexpectedly cut rates, citing easing inflation and softening growth momentum.

- Next week: Reserve Bank of Australia Policy Rate (Tue.), Mexico CPI (Wed.), Norway CPI (Thu.)

Credit Market Insights: Bank Lending Remains Tight Amid Softer Demand

- The first quarter SLOOS revealed banks tightened lending standards across most business categories, while demand for credit generally weakened. While lending standards remain tight, particularly for commercial sectors, the decline in demand suggests that both businesses and consumers may be wary of economic uncertainty and high interest rates.

Topic of the Week: The One Big Beautiful Bill Endgame

- Republicans in Congress are on track to advance the Senate-version reconciliation bill to the president's desk for signature ahead of a self-imposed July 4 deadline. While the Senate bill made a variety of modifications to the version that passed the House of Representatives in late May, from a macro perspective, the key implications have not changed materially: bigger budget deficits and faster economic growth over the next couple of years partially offset by higher tariffs, and a somewhat more ambiguous longer-term impact.

Cliff Notes: Budget Constraints

Key insights from the week that was.

The Cotality home value index rose another 0.6% in June, leaving prices up 2.3% since mid-February 2025, when the RBA delivered the first rate cut for this cycle. Gains by city were tightly bunched, from 0.5% in Melbourne and Adelaide to 0.8% in Perth. RBA rate cuts have clearly provided significant support over the period, daily data showing 1ppt of the gains have occurred in the two weeks immediately after each RBA rate cut. Importantly, the uptrend in prices and auction clearance rates is continuing as turnover lifts, pointing to robust demand and confidence. Private credit data implies demand is coming from both owner-occupiers and investors, credit for each subset up 0.5% in May and respectively 5.7% and 6.1% over the year. Westpac expects further price gains as the RBA returns the cash rate to a neutral setting by May 2026.

Bolstering expectations for a sustained uptrend in prices, the near-term supply of new housing remains limited. Total dwelling approvals rose 3.2% in May. However, this result follows a 12% decline January to April and a 23% gain in the prior 12 months, leaving the level of approvals just 6.5% higher than a year ago and well below our estimate of underlying demand. Through the first half of 2025, approvals have lacked direction across the states, though affordability favours greater momentum in SA, WA and Qld. For further detail on the outlook for housing, see Westpac’s June Housing Pulse. And, on the broader outlook for Australia’s state economies, our latest edition of Coast-to-Coast.

While the outlook has firmed, discretionary consumer demand remains weak, retail sales were up just 0.2% in the month, slowing annual growth to 3.3%. A rebound in clothing & footwear and department store sales drove May’s increase, partly offset by a second-consecutive decline in food retailing. The broader household spending indicator is due later today.

Offshore, US nonfarm payrolls beat expectations at the margin, with 147k new jobs reported in the month and 16k added to the count for the prior two months. Nonfarm payrolls 3-month change is little changed at 150k, consistent with balance between labour demand and supply. Household employment is weaker, rising just 93k in June and averaging -47k over the past 3 months. However, another 0.1ppt decline in participation in June (after a 0.2ppt reduction in May) edged the unemployment rate down to 4.1%. An unchanged participation rate over May and June would have instead left the unemployment rate near 4.4%.

The ISM surveys continue to point to downside risks for the US labour market through the remainder of the year. In June, the ISM manufacturing employment index fell back near its recent lows to 45.0 even with production broadly unchanged. The ISM services employment index was also well below its 5-year average at 47.2 in June. Thankfully for the US economy, initial claims holding near historic lows suggests downside risks are limited to reduced to job creation not outright jobless.

Chair Powell consequently remains in wait-and-see mode with monetary policy, continuing to believe the US economy remains in robust health and the inflationary impact of tariffs are yet to be seen. This was a key takeaway from the ECB’s Sintra Conference policy panel which also included representation from the leaders of the European Central Bank, Bank of England, Bank of Japan and Bank of Korea.

Fiscal policy developments over the past week are unlikely to sway the FOMC’s views. President Trump's 'Big Beautiful Bill' passed the House 218-214 overnight after being approved by the Senate earlier in the week 51-50 and will now be signed into law. Supporting household discretionary income, the bill extends Trump's tax cuts from his first term beyond the current year-end expiry. The final version of the bill also includes a temporary 5-year increase in the state and local tax deduction to $40,000 after which it will revert to $10,000. However, lower taxes over future years are to be partly funded by reductions to Medicaid, food stamp and college loan funding as well as the end of clean energy tax breaks introduced by the Biden administration, including the $7,500 consumer tax credit for electric vehicles. The bill is therefore likely to have little-to-no net impact on aggregate consumer spending.

Regarding tariffs, a deal was agreed with Vietnam this week following successful conclusions to negotiations with the UK and China over the past month. Still, the agreed 20% tariff on US imports from Vietnam (40% for transhipped goods, i.e. where goods are transited through Vietnam’s ports to avoid a higher tariff) is a step up from the 10% placeholder tariff instituted by President Trump for 90 days until 9 July. Of more concern though is the limited headway achieved by other nations in negotiations, particularly for key trading partners including Canada, Japan and South Korea. By September, we should have a clearer view of the scale and persistence of the tariffs’ inflationary impact, allowing the FOMC to ease cautiously into year end. But in July, they are set to remain on hold and noncommittal. As an aside, amid global trade uncertainty, Australian trade flows remain highly volatile month-to-month, the trade surplus narrowing sharply from $4.9bn in April to $2.2bn in May, its lowest level in nearly five years.

For China, the terms of Vietnam’s deal with the US are inconsequential. While some Chinese firms have been transiting shipments through Vietnam, this is only a temporary strategy while the China/US deal was agreed and, more importantly, strategic investment in Vietnam and other emerging Asian economies is undertaken. Over the long run, Chinese firms are intent on diversifying their production base across the region to minimise their cost-of-production and maximise export opportunities and political linkages throughout the world. This means Chinese firms operating in neighbouring nations will increasingly seek to add meaningful economic value there and consequently the US tariff for these nations will apply to the output. Profit will then be repatriated back to China and production there limited to high-value-add goods. As attested to by China’s trade surplus over the past few years and the current official NBS PMI readings, which are historically consistent with GDP growth circa 5-6%, this strategy of mutual economic development has already shown considerable success and will continue to compound. The primary risk for China is instead that these trade gains do not filter through to the average consumer, and the hoped-for recovery in consumer spending and housing does not eventuate. External and domestic growth drivers are necessary for China to achieve its development ambitions in the medium-to-long term.

Lastly, Japan’s Tankan survey this week highlighted the lingering threat Japanese manufacturers face from US trade policy, the diffusion index for medium and small manufacturers forecast to fall 4 and 3 points respectively in the September quarter, having edged down 1pt between March and June. Large manufacturers greater flexibility is arguably behind their neutral expectation for the current period. Interestingly, Japan’s services sector is more concerned over the outlook than manufacturers, a 6-8 point fall forecast across small-to-large enterprises by September following broadly unchanged conditions March to June.

While investment intentions are up amongst large and medium-sized enterprises, growth in investment by small firms is subdued. Profitability for FY2025 (ending March 2026) is expected to decline by 5.7%, led by manufacturing. Output prices, an indicator of domestic inflation, meanwhile held steady at around 3.0%, remaining aligned with the Bank of Japan’s 2.0% target. Firms anticipate ongoing labour shortages; but, with uncertainty clouding the outlook, still plan to increase their intake of new graduates by 4.3% this year after FY2024’s 14% rise. This points more towards a persistent skills mismatch than an outright labour shortfall. Domestic economic conditions may therefore become less supportive of further rate hikes, a risk the BoJ is attentive to.

Timing and Tactics

Nothing the RBA will learn in the next five weeks makes it worth waiting until the August meeting to cut the cash rate. Beyond the next move, things are less clear-cut and – as for other economies – increasingly driven by domestic considerations not global common shocks.

- Boiled down to its essence, the RBA’s near-term policy decision rests on whether the five weeks after next week’s meeting would change anything. If not, just get on with it next week. This was the rationale for our change of call last week.

- The story is less clear-cut further out. Front-loading further rate cuts would imply a fundamentally different view of the economy than the RBA has recently articulated.

- The Australian situation is part of a broader shift whereby domestic variation now dominates global common shocks as a determinant of monetary policy setting. This implies that short-run shifts in bond pricing and exchange rates can be expected, sometimes running counter to expected longer-run trends.

One of my longstanding bosses at the RBA (he knows who he is) had a superlative ability to get to the essence of an issue. When all those around him were debating the minutiae, he would bring it all together, often with a pithy question.

Monetary policy is complicated. The world is complex and uncertain. In the end, though, all that complexity needs to be boiled down to a decision about what to do with the cash rate. Sometimes it helps to channel my old boss and frame the issue as a pithy question. Back in May, the question was: could you really write a Board paper with a compelling case to hold? Having written a few in my time, it was clear that the answer to this question is “no”. That judgement solidified the call for a rate cut in May.

This time around, the question boils down to, “could you front a media conference and explain why you decided to wait another five weeks to cut rates, when it was just a choice between now and August?” Again, the answer is likely to be “no”. To be fair, there are arguments to wait (for quarterly CPI, new forecasts and so on). That is why we do not regard a cut in July as a shoo-in. Given how sensitive the RBA has been to arguments about lingering inflation pressures, it could be that the case to wait wins the day in the Board room.

The arguments to wait are not compelling, though, so we do not think that case should win the day. Nothing the RBA will learn in the subsequent five weeks will change the decision to cut. And explaining to the assembled mainstream media that you hesitated because (in essence) unemployment is “too low” and employment growth is “too strong” to do so will not land well with that audience.

Inflation is in the target range, with downwards momentum now evident. Ordinarily, the monthly CPI indicator should not tip the balance; the RBA’s own language does suggest they put far more weight on the full suite of quarterly data. As highlighted last week, though, a large enough downside surprise in one month can still tell you enough about the quarterly result that even a small upward surprise to the month-three data will not change. Sometimes, as it did with the May data, it can confirm the suspected downwards momentum. Key components of domestic inflation – rents, home-building, insurance and personal services – all surprised on the downside. Some of these components are still only measured quarterly and so are locked in for the June quarter read.

Likewise, another monthly labour force release and the last-ever retail sales number will not change the current view on the economy. More information is usually better, but not always by enough to be worth waiting for.

A decision to cut in July is one of timing and tactics, not whether to cut at all. The RBA has shown itself willing to “surprise the market” when the question is whether to move or not. The May 2023 hike was a good example of this. But if the question is now or in five weeks’ time, the juice is not worth the squeeze. Just get on with it.

Tactics versus strategy

The story changes when we consider the path after the next cut. Backing up a July cut with another in August seems like more of a stretch than shifting an obvious August cut to an almost-as-obvious July cut. To do so would require a qualitatively different view of the economy and the inflation outlook than the RBA has recently articulated.

This is why we suggested last week that the RBA’s post-meeting communication will be quite circumspect. One possible way to frame their message might be that, having now cut three times, it is prudent to wait a few months see how lower rates are flowing through the economy before deciding how much more is needed. This would leave open the possibility of further cuts but push back on an August timing. Given current market pricing, some would regard such messaging as “hawkish”.

There is a tension here, though. With inflation now clearly inside the target range and the forward view still heading down, it is questionable why monetary policy needs to be restrictive at all now. Given monetary policy affects the economy with a lag, leaving policy restrictive when inflation is already so close to target risks pushing it below the target midpoint and perhaps below the target range altogether.

The RBA’s read of the labour market is important here. The offset to the risk of an inflation undershoot is its view that the labour market is still tighter than is consistent with full employment.

Documents released under Freedom of Information showed that, early this year, the RBA was clearly considering whether this assessment was too pessimistic, and a lower unemployment rate was sustainable. However, the work was clearly unfinished at the time of release and was pushing back on alternative hypotheses. The careful, evidence-based approach the RBA staff bring to their work means that the RBA does not come to a view lightly. Nor does it change its view lightly – or quickly. (This is not a criticism!)

For this reason, while we expect further rate cuts from here, their timing will depend on the RBA’s evolving view of the economy. Until we hear more about how the RBA’s view of the inflation outlook is shifting, we see little reason to move the timing of those subsequent rate cuts forward. (That means we currently expect the next cut later this year, in November, and two more in the first half of 2026). Such a shift could still be needed down the track, however.

And we all (don’t) go down together

The Australian situation is part of a broader shift in strategies for monetary policy setting. In recent years, the story has all been about the common global inflation shock following the pandemic and then Russia’s invasion of Ukraine. Different countries were exposed to different extents; consider the inflation differential between Germany and Switzerland in recent years because of their differing exposures to hydrocarbon-based energy prices. By and large, though, most countries faced the same challenge: first, to get inflation down; and second, to remove the restrictive stance of monetary policy once it was clear that inflation would turn to target and stay there. The story is no longer so uniform, though. Even the supposedly common shock of the Trump administration’s tariff policy is playing out differently in different regions.

As Westpac Economics colleague Illiana Jain highlighted in her write-up of the Sintra Panel this week, as circumstances diverge across economies, so too do the strategies of monetary policymakers. This implies that short-run shifts in bond pricing and exchange rates can be expected. In some cases, this could run counter to expected longer-run trends.

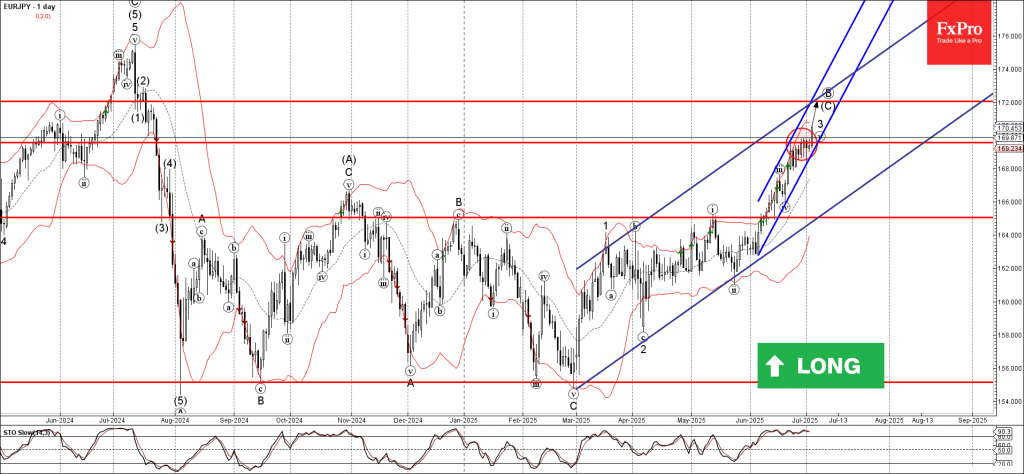

EURJPY Wave Analysis

EURJPY: ⬆️ Buy

- EURJPY broke resistance level of 169.55

- Likely to rise to resistance level 72.00

EURJPY currency pair recently broke above the key resistance level 169.55 (which reversed the price multiple times at the end of June, as can be seen from the daily EURJPY chart below).

The breakout of the resistance level 169.55 accelerated the active short-term impulse wave 3 of the intermediate impulse wave (C) from February.

Given the clear daily uptrend, EURJPY currency pair can be expected to rise further to the next resistance level 172.00, target price for the completion of the active impulse wave (C) lying at the intersection of the 2 up channels from June and March.

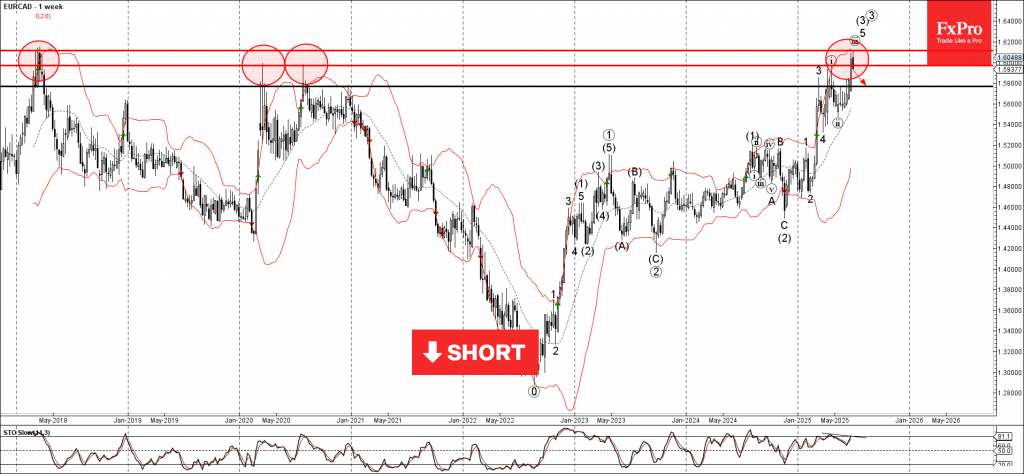

EURCAD Wave Analysis

EURCAD: ⬇️ Sell

- EURCAD reversed from resistance zone

- Likely to fall to support level 1.5800

EURCAD currency pair recently reversed down from the major resistance zone located between the strong resistance level 1.6150 (former yearly high from 2018) and the resistance level 1.5965 (former Double Top from 2020).

The downward reversal from this resistance zone stopped the previous impulse waves 5 and (3).

Given the strength of the resistance level 1.6150 and the bearish divergence on the weekly Stochastic indicator, EURCAD currency pair can be expected to fall further to the next support level 1.5800.

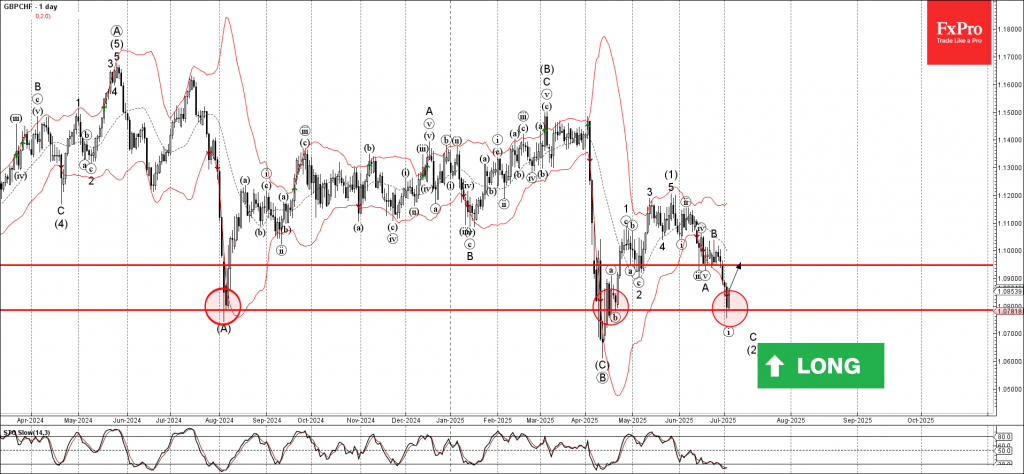

GBPCHF Wave Analysis

GBPCHF: ⬆️ Buy

- GBPCHF reversed from strong support level 1.0785

- Likely to rise to resistance level 1.0950

GBPCHF currency pair recently reversed up from the strong support level 1.0785 (which has been steadily reversing the price from last August as can be seen below).

The upward reversal from the support level 1.0785 created the daily Japanese candlesticks reversal pattern Bullish Engulfing.

Given the strength of the support level 1.0785 and the oversold daily Stochastic, GBPCHF currency pair can be expected to rise to the next round resistance level 1.0950.

USDJPY Accelerates Within Range After Back-to-Back Positive US Data Surprises

The United States continues to demonstrate why it remains the largest and most powerful economy in the world, consistently surprising markets with its resilience in the past few data releases.

While market participants have been eager to question US strength—especially under President Trump’s “US Exceptionalism” policy, which many feared could backfire—recent economic data continues to challenge that narrative.

Despite ongoing concerns over diplomatic volatility and declining business confidence, the US economy once again delivered upside surprises. The Non-Farm Payrolls (NFP) report, expected at 110K, surprised with a +37K beat, and the more influential ISM Services PMI came in strong—reaffirming underlying economic momentum.

As a result, the US Dollar is regaining its footing. The Dollar Index (DXY) is up approximately 0.35% on the session, and even with an early close ahead of Independence Day, USDJPY surged 1300 pips on the heels of the release.

USDJPY Technical Analysis from the Daily to 1H Charts

USDJPY Daily Chart

USDJPY Daily Chart, July 3, 2025 – Source: TradingView

Overnight, markets perceived some hawkish comments from Bank of Japan's Takata, who mentioned that the BoJ would still look to resume hikes after a pause – such comments did not do much to add strength to the Yen.

Nonetheless, the longer-term range 142.00 to 146.50 range remains intact, with the pair up 1,350 pips on the session.

It remains notable that 146.00 served many times as the higher resistance level within the range, but two occasions of USD dominance (Potential tariff removals in beginning of May and Iran-Israel War) led to what seemed like breakouts before rejecting the Extreme of Range 147.50 to 148.

Broader USD strength following this morning's data could bring the pair to such extremes again if the Greenback keeps rebounding from its lows.

USDJPY 4H Chart

USDJPY 4H Chart, July 3, 2025 – Source: TradingView

The latest round trip within the range led to a wick on the Main Range support (last swing low 142.68), followed by a swift rebound, particularly as markets retested the Intermediate Support at 143.55.

Key Moving Averages are still flat on the 4H timeframe, confirming again the strength of the range, which may only lead to actual breakouts when markets start to price in new fundamental change – mostly expected when respective US and Japanese Central Bank policies diverge further.

The RSI moved quite aggressively higher in this morning's up-move but still had some space before becoming overbought, leaving some margin for manoeuvre for bulls – Let's take a look closer to spot more zones of interest.

USDJPY 1H Chart

USDJPY 1H Chart, July 3, 2025 – Source: TradingView

On this shorter timeframe, we can observe with more details how volatile but rangebound the price action is in the pair. Although there has been many catalysts for breakouts, the action is still contained.

This morning's Hourly bar from the data release did close at its highs and has consolidated at its top, a sign of strength for the USD as seen in other currency pairs.

Look at 144.50 as immediate pivot – a break below would retest the lower parts of the range explored in higher timeframes. Sellers will have to show some strength at the current Lower timeframe Resistance 145.00 to regain some edge.

Staying above here leaves the bulls in control, and a failure of sellers to correct prices will hint at a re-entry within the 146.00 to 146.70 Main Resistance Zone

Safe Trades!