Sample Category Title

Fed’s Schmid backs wait-and-see stance amid uncertainty

Speaking overnight, Kansas City Fed President Jeff Schmid called Fed’s “wait-and-see” stance appropriate, especially given that inflation remains above target and the effects of rising tariffs are still filtering through the economy. "The resilience of the economy gives us the time to observe how prices and the economy develop," he added

Schmid noted that business contacts “almost uniformly” expect tariffs to drive prices higher and weigh on activity, putting Fed’s inflation and employment mandates at odds. But "there is far less clarity on when and by how much," said Schmid, who argued there’s little justification for near-term rate adjustments until the economic picture becomes clearer.

Fed’s Barr: Tariffs to push inflation higher, but policy can wait

Fed Governor Michael Barr warned that the recent wave of tariffs is likely to drive inflation higher, citing the potential "Higher short-term inflation expectations, supply chain adjustments, and second-round effects". Speaking overnight, Barr acknowledged that this could add to inflation persistence even as the broader economy slows and unemployment, currently at 4.2%, edges higher.

Despite these headwinds, Barr said the Fed is in a good position to “wait and see” how economic conditions evolve before adjusting policy. He noted the "considerable uncertainty about tariff policies and their effects," stressing that monetary policy requires balancing "tradeoffs" between supporting growth and containing inflation.

Fed’s Williams sees growth slowing to 1%, tariffs to push inflation to 3%

New York Fed President John Williams warned overnight that the combination of policy uncertainty, restrictive trade measures, and declining immigration will drag significantly on the US economy this year. He projects growth will decelerate to just 1%, with unemployment rising to 4.5% by the end of 2025. Williams also anticipates a near-term spike in inflation to 3%, driven by tariffs, though he expects that to slowly subside back toward 2% over the next two years.

While Williams described the hard economic data as still solid, he acknowledged a growing disconnect with softer indicators that point to rising concerns among consumers and businesses. Nonetheless, he welcomed signs that inflation expectations remain anchored despite recent price shocks.

Looking ahead, Williams emphasized that monetary policy will be guided by data due “over the next few months,” which will inform whether and when Fed should adjust interest rates. Though he reiterated that “interest rates eventually need to get back to more normal levels”, his comments suggest a wait-and-see approach remains the most likely course for now.

Fed’s Kashkari: Staying patient amid tariff uncertainty, sees strong economy

Minneapolis Fed President Neel Kashkari reiterated Fed's cautious stance overnight, emphasizing that policymakers remain in “wait and see mode” as they monitor the economic fallout from tariff policy. He noted that while officials are hesitant to make any "dramatic changes" to the policy outlook just yet, their priority is to gain clarity on how tariffs will impact inflation and broader growth dynamics.

Kashkari struck a generally optimistic tone on the domestic economy, saying the fundamentals remain “quite strong” and that inflation appears to be trending back toward the 2% target. He pointed to recent data suggesting underlying inflation is running near 2.5%, which—while still above target—is showing a welcome moderation.

However, the lingering uncertainty around tariffs continues to cloud the outlook. Kashkari warned that "nervousness" around trade is leading some firms to pause investment and may amplify inflation risks. While ongoing negotiations offer a path forward, he made clear that "ultimately we need to see what actually happens and then adjust our analysis of the economy."

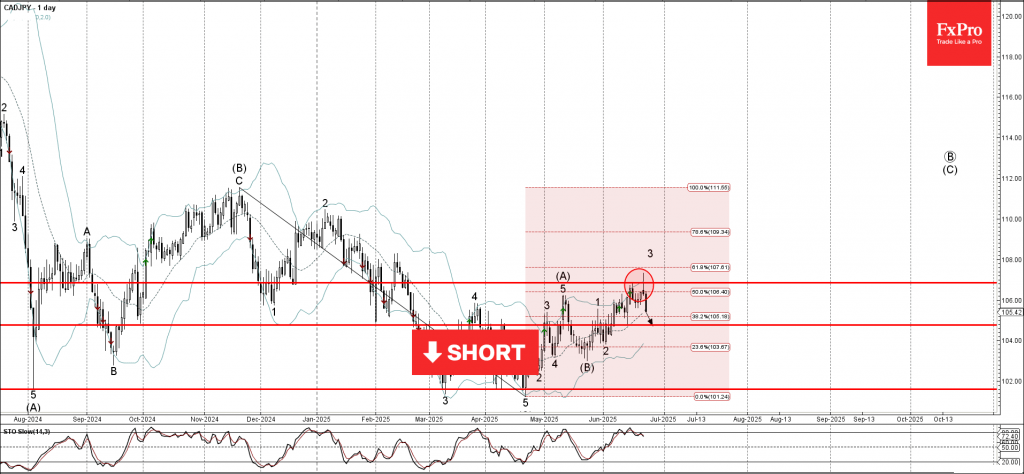

CADJPY Wave Analysis

CADJPY: ⬇️ Sell

- CADJPY reversed from the resistance area

- Likely to fall to support level 104.75

CADJPY currency pair recently reversed down from the resistance area between the resistance level 106.85, the upper daily Bollinger Band and the 50% Fibonacci correction of the extended downward impulse from November.

The downward reversal from this resistance area created the daily Japanese candlesticks reversal pattern Shooting Star, which stopped the previous minor impulse wave 3.

Given the strength of the resistance level 106.85, CADJPY currency pair can be expected to fall to the next support level 104.75 (which reversed the pair earlier this month).

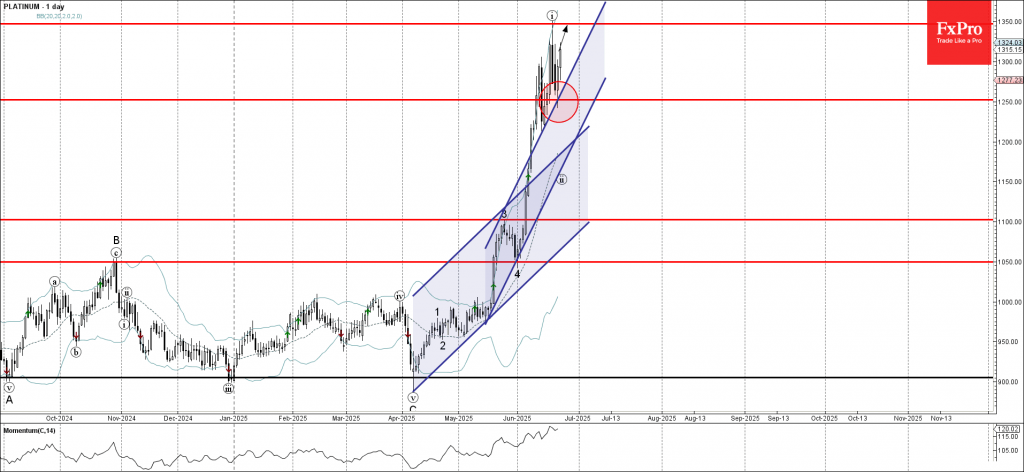

Platinum Wave Analysis

Platinum: ⬆️ Buy

- Platinum reversed from the support area

- Likely to rise to resistance level 1350.00

Platinum recently reversed up from the support area between the upper trendline of the recently broken up channel from May (acting as the support after it was broken) and the support level 1250.00.

The upward reversal from this support area continues the active minor impulse wave 5 from the end of May.

Given the strong daily uptrend, Platinum can be expected to rise to the next resistance level 1350.00 (which stopped the previous impulse wave i).

Nasdaq Reaches ATH, Equities Around the Globe from Fear to Greed

Global equity indices are rallying over 1% on the session following news that a US-brokered ceasefire between Israel and Iran is now in effect, bringing a temporary end to nearly two weeks of military conflict.

To recap, the Israel-Iran escalation began on Thursday, June 13, after the breakdown of US-Iran nuclear negotiations. In response, Israel launched preemptive strikes targeting Iranian nuclear infrastructure, aiming to prevent further development of a potential nuclear weapon.

The US subsequently stepped in to contain the situation, and Iran’s retaliation was largely symbolic—paving the way for the current ceasefire agreement.

Despite elevated geopolitical tensions, equity markets remained resilient. While initial corrections followed the outbreak of conflict, indices never strayed far from their record highs, providing ample trading opportunities amid heightened volatility.

What’s notable is the bears' failure to trigger a deeper correction in Equities, which has fueled a strong reversal.

As of this writing, the Nasdaq just touched its all time-highs, reversing slightly from here.

Nasdaq 1H Chart as the Tech-Focused index touches its all-time highs

Nasdaq 100 CFD 1H Chart, June 24, 2025 – Source: TradingView

The Nasdaq is in a bullish frenzy in the past 24 hours and now trading less than 10 points from its 22,241 All-time highs, attained in February 2025 right before the majors Trump Correction.

One hurdle is the current overbought RSI on most short-term timeframes, however the strong momentum should take the prices to at least current all-time highs.

Levels to watch as markets are racing:

Resistance Zones

- ATH Resistance Zone +/- 20 points around 22,241

- Fibonacci Extension potential Resistance Zone 22,450

Support Zones

- 22,050 Immediate Pivot

- 21,900 Resistance turned support

- 21,500 Main Support (War lows 21,455)

What about other Global Indices?

Let's see where are other indices around the globe –

North American Indices:

- S&P 500 – 6,102 (0.75% from ATH: 6,152) + 1.16% on the session

- Dow Jones – 43,130 (4,20% from ATH: 45,097) +1.13%

- Canada's TSX – 26,760 (new ATH) +0.56%

Europe Indices:

- German DAX – 23,712 (3% from ATH: 24,491) + 1.16%

- EuroStoxx – 5,310 (4.56% from ATH: 5,568) +1.14%

- France CAC 40 – 7,616 (7.60% from ATH: 8,257) +1.06%

Safe Trades!

ECB’s Lane: Inflation fight largely completed, but a new set of challenges emerge

Philip Lane, ECB’s Chief Economist, said in a speech today that the disinflation process in the Eurozone is “largely completed”. But monetary policymakers now face a "new set of challenges". Trade tensions, geopolitical instability, and shifting fiscal strategies are now front and center in shaping medium-term inflation risks.

Lane pointed to a wide array of disruptors—from the redrawing of tariff regimes to tighter rules on foreign investment and increasing overlap between economic and security policy. The implications of structural forces like the green transition, AI, and evolving comparative advantages also remain unclear. He emphasized that these issues affect inflation from both demand and supply sides and may unfold on different timelines.

With so many moving parts, Lane called for continued data dependency and a flexible approach to rate decisions, "with no pre-commitment to any particular future rate path." In this environment, the central bank’s key mission is "make sure that any temporary deviations from target do not turn into longer-term deviations".

BoE’s Ramsden: Cites contraction in jobs, should respond to weaker outlook

BoE Deputy Governor Dave Ramsden defended his vote for a rate cut last week, pointing to signs of labor market weakness and a deteriorating outlook. Citing PAYE data, Ramsden noted that private sector payrolls are now “clearly in contractionary territory,” signaling rising slack in the economy.

Ramsden acknowledged the decision to vote for a cut was “finely balanced,” but emphasized that even at 4%, policy remains “clearly in restrictive territory.” With demand cooling and employment indicators weakening, he argued it was important for BoE to continue adjusting.