Sample Category Title

Fed’s Hammack warns against premature cuts, signals prolonged pause likely

Cleveland Fed President Beth Hammack pushed back against the idea of early rate cuts, saying there’s little evidence yet to justify easing. “I don’t see a weakening in the economy that would merit imminent rate cuts,” she said. Hammack emphasized that risks from holding steady are low and that any adjustments should be cautious and measured.

She reiterated the value of patience in uncertain times, noting that the current stance could be maintained “for quite some time” before Fed considers modest cuts toward neutral.

“I would rather be slow and move in the right direction than move quickly in the wrong one," she emphasized.

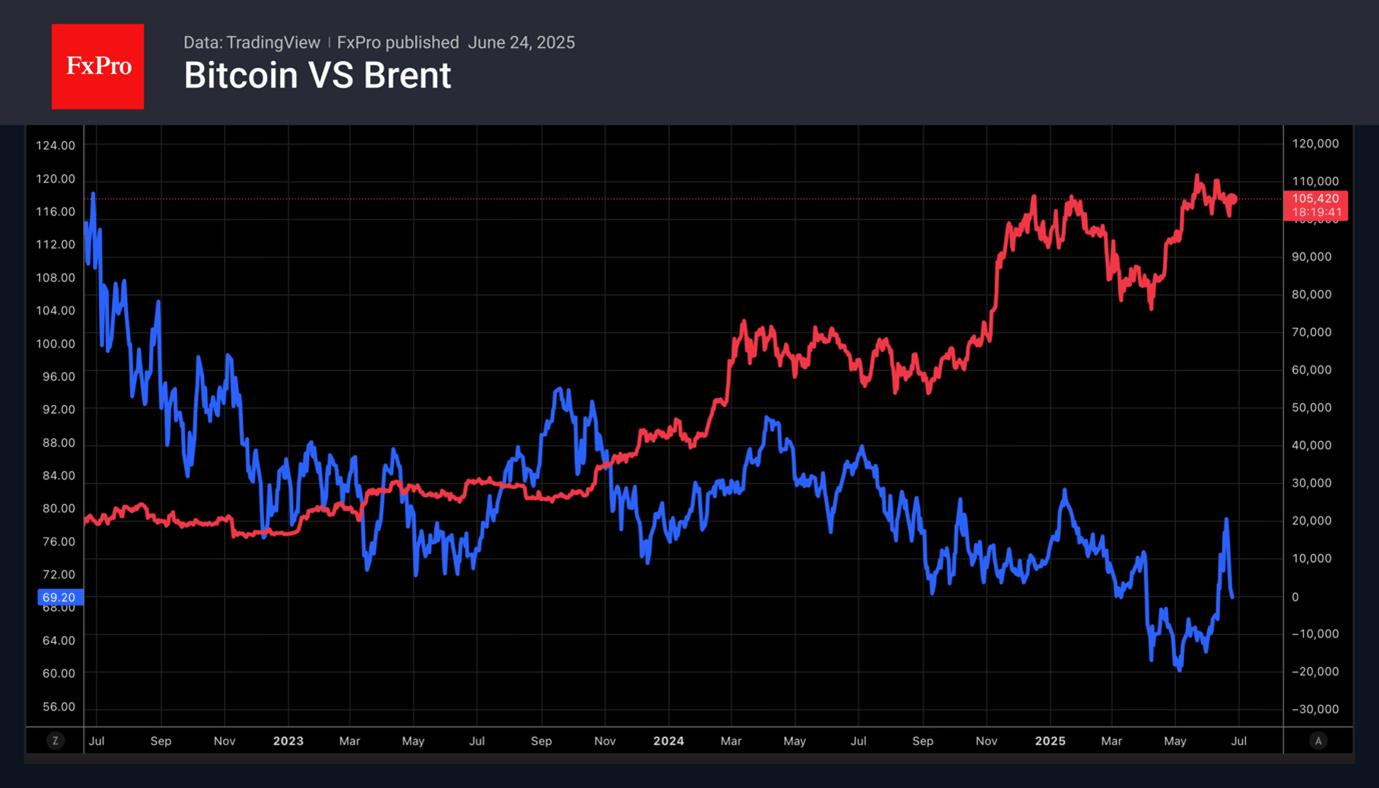

Bitcoin Profiting on the Returned Demand for Risk

Bitcoin has been on a rollercoaster ride. Firstly, quotes fell below the psychologically important round level of $100,000 in response to the United States’ bombing Iran. Then, the cryptocurrency recorded one of the best daily rallies in 2025 thanks to Donald Trump’s announcement of a ceasefire in the Middle East.

Along with the deterioration of global risk appetite amid the Israeli-Iranian conflict, fears about the growth of token supply put pressure on Bitcoin. Western sanctions are depriving the country of the opportunity to sell traditional assets. To attract resources, it may start selling cryptocurrency. Therefore, Tehran’s reduction in oil exports increased the risks of a further decline in Bitcoin prices.

The markets believed in the end of the Twelve-Day War and returned to a positive outlook. The reduction in the number of daily transactions on the Bitcoin network from 600-700K in 2024 to 500K in 2025, with the average payment volume remaining unchanged at $7 billion, is good news. According to Glassnode, this indicates institutional investors’ increased interest in digital assets.

Bitcoin is also supported by consistently high demand for Bitcoin-focused ETF products. Since their launch in January 2024, specialised exchange-traded funds have attracted more than $131 billion.

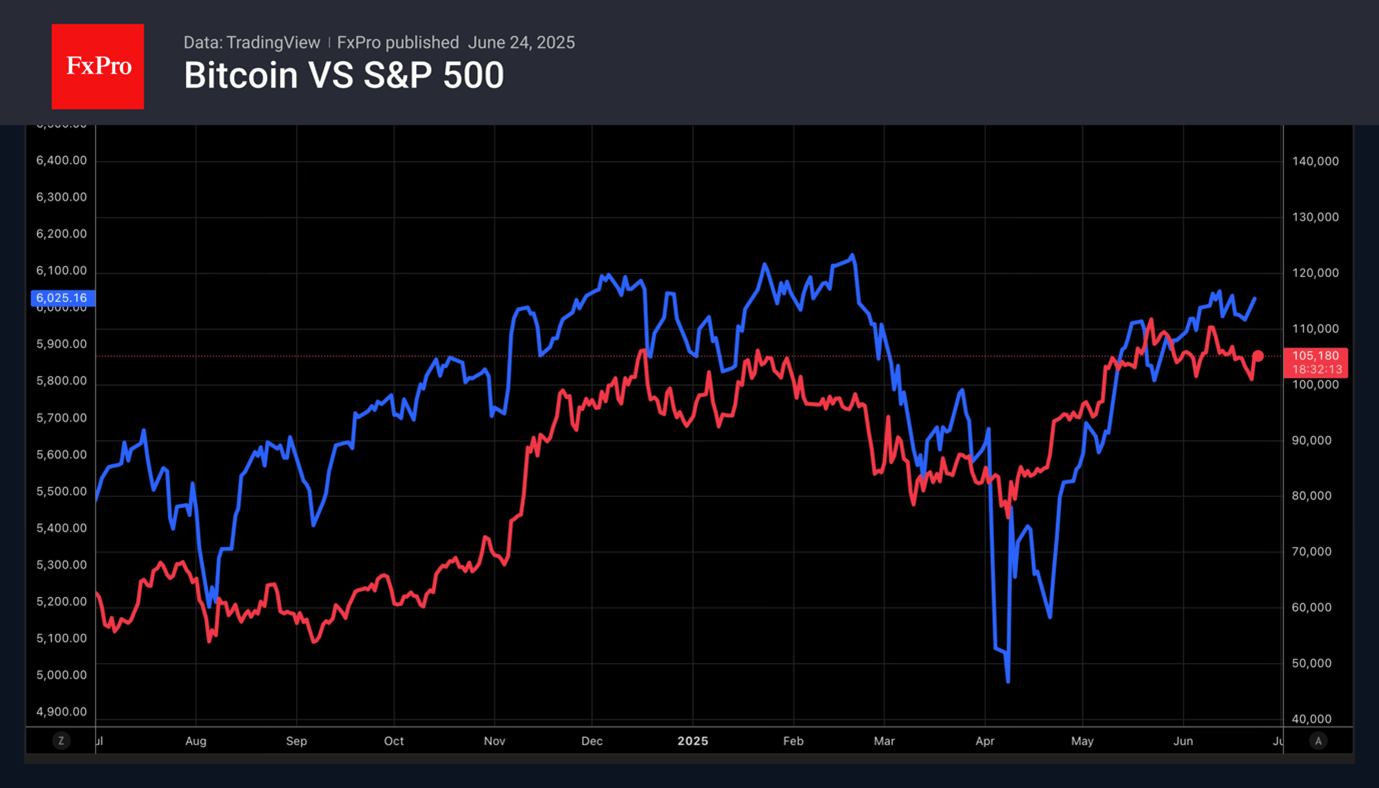

The turning point in the Israeli-Iranian conflict gives reason to expect a continuation of the rally in US stock indices. The return of the S&P 500 to record highs is strengthening global risk appetite and creating a tailwind for the first Crypto. Events in the Middle East have shown that Bitcoin has not become a hedge against turmoil, as its creators intended.

Nevertheless, the risky nature of cryptocurrency allows you to make good money on it during periods of market prosperity. How long will the current favourable period last? The answer will depend on the end of the war in the Middle East. It will also depend on Donald Trump’s unwillingness to escalate trade conflicts. There is not much time left before the end of the 90-day tariff delay. Are the markets and the S&P 500 waiting for a new round of trade wars?

US Dollar Slides on De-escalation of Iran Tensions — Powell Speaking at 10:00

Selling flows in the US Dollar have came back promptly after the Iranian repost on the US Base of Al-Udeid in Qatar – What was previously thought to have the potential to be a new phase of a prolonged conflict materialized into a cease-fire.

A build-up of angst through last week trading sent markets gapping strongly at the weekly open, but all of these moves largely reversed. The story is largely similar to August 2024 preceding tensions between Israel and Iran that led to similar reversals.

The Dollar index is now back into the 98 handle and back into its 2025 descending channel.

Equity markets just now turned from fear to greed and it seems that players have already turned the page on the conflict.

All eyes now turn to the upcoming FED Chair Powell's testimony at the US Senate, coming up at 10:00 A.M. ET.

Fear and Greed Index, June 24, 2025 – Source: CNN

Dollar Index Multi-Timeframe Technical Analysis

DXY Weekly Chart

Weekly charts still point to relatively bearish momentum, however the current 98.00 handle served as consolidation throughout the 2020 Covid repricing and the 2022 start of the hike cycle.

Hence, there are volume-and-price magnets for USD trading around this zone, where except for any particular bullish or bearish catalyst, markets may use as a zone for price consolidation.

The Weekly RSI is in the oversold region, therefore prices would have to consolidate before pursuing a continuation of the 2025 downtrend.

A reversal from here would however point to a retest of the 100.00 Main Resistance.

DXY Daily Chart

DXY Daily Chart, June 24, 2025 – Source: TradingView

The Daily picture for the Dollar is close to Neutral despite a major reversal of the weekly bullish open that tested the Daily 50-Moving Average at 99.50.

Sellers have failed to push below the 2025-lows situated at 97.60, and an indecision doji is forming at the highs of the Daily descending channel.

Momentum is still slightly bearish – Positioning seems to have been one-sided but some of that has been undone by the tensions.

We will get more clarity as markets now turn their eyes back to Federal Reserve speeches and Economic Data, which had by the way surprised to the downside in the past few weeks.

DXY 1H Chart

DXY 1H Chart, June 24, 2025 – Source: TradingView

The Greenback gapped down slightly in today's open and is now consolidating right at the 98.00 Psychological Level that bulls used as support in the week-ago bullish impulsive move.

The DXY is trading oversold as the correction exceeded 100 pips, and the rest of the story is to see if markets want to maintain their sell-side bias on the World's global currency.

A further breakdown from here points toward a test of the 97.62 lows attained right as Israel started its offense at Iran's Nuclear capacity, a further support just below at the 97.50 psychological zone.

A rebound from here would look to test the 98.50 pivot, however buyers will have to take prices out of the 2025 descending channel first.

Safe Trades!

Australian Dollar Jumps on Israel-Iran Cease Fire

The Australian dollar is up sharply on Tuesday. In the North American session, AUD/USD is trading at 0.6504, up 0.70% on the day.

Australian dollar jumps as risk appetite improves

Investors' risk appetite is higher today after Israel and Iran agreed to a ceasefire in their 12-day war. The markets have reacted favorably to lower oil prices as fears that Iran would close the Straits of Hormuz, which would have disrupted global oil supplies, have diminished. Risk appetite has returned and risk currencies like the Australian dollar have posted strong gains today.

The Israel-Iran war has triggered sharp swings in oil prices and there are fears of an oil price shock if the fragile ceasefire does not hold. An oil price shock would send petrol prices higher and boost inflation, complicating the Reserve Bank of Australia's plans to lower interest rates.

Australia CPI expected to ease to 2.3%

Australia releases the May inflation report early on Wednesday. Headline CPI has been stuck at 2.4% for three consecutive months, within the Reserve Bank of Australia's target of 2-3% and its lowest level since Nov. 2024. The market estimate for May stands at 2.3%. Trimmed Mean CPI, a key core inflation indication, edged up to 2.8% from 2.7% in April.

The Reserve Bank will be keeping a close eye on the inflation report, with the central bank making a rate announcement on July 8. The RBA trimmed rates by a quarter-point in May and has shifted to a more dovish stance - the Board discussed a jumbo half-point cut at the May meeting.

Fed's Powell to testify on Capitol Hill

Fred Chair Powell appears before Congress today and Wednesday and is likely to defend the Fed's wait-and-see stance. The Fed is concerned about President Trump's tariffs and the Israel-Iran war threatens stability in the Middle East, hardly the recipe for further rate cuts. Still, there appears to be some dissent within the Fed, as two members, Michelle Bowman and Christopher Waller, have suggested that the Fed could lower rates as early as September.

AUD/USD Technical

- AUD/USD is testing resistance at 0.6490. Above, there is resistance at 0.6522

- There is support at 0.6400 and 0.6342

AUDUSD 1-Day Chart, June 24, 2025

Sunset Market Commentary

Markets

The ceasefire, although cracking and squeaking, between Israel and Iran spurred a global risk-on move that benefited stock markets in the first place. European equities eke out a 1.4% gain. The main US indices built on yesterday’s gains with another 1%+ increase at the open. German Bunds are selling off. Yields add 1.6 (2-yr) to 7.5 bps (30-yr) in a bear steepening move. This is directly related to the German cabinet’s (belated) 2025 budget approval and the mid-term finance plan. It includes a surge in defense and infrastructure spending as well as other short-term growth-supporting initiatives that will raise net new borrowing during chancellor Merz’ term (2025-2029) by >€500bn. The finance agency has already lifted their debt sale forecasts for the upcoming quarter by €19bn. The fiscal boost has the potential to finally revive the economy and that’s starting to show in soft indicators including yesterday’s PMIs and today’s IFO business indicators. The expectations component in the latter matched the highest level (90.7) since the Russian invasion meant the end of cheap energy and ushered in a drawn out industrial malaise. Meanwhile, Trump’s massive bill is moving along a tight schedule to be signed by the president July 4. It’s currently in the Senate, where Republicans are closing in on agreeing to the contentious $40k cap on state and local tax deductions but with the phase down of the tax break to begin at a lower income threshold. This provision in the House version of the bill was a hard-fought one and some Senate Republicans wanted to keep the current $10k cap, potentially resulting in a stand-off between the two chambers and derailing the July 4 deadline. The very long end of the US yield curve in any case underperforms slightly with the 30-yr yield at some point adding 4.3 bps before paring gains to 2 bp. Short-term yields are flat on the day, unphased by Powell’s prepared remarks the Fed chair is to deliver before Congress after wrapping up this report. As expected, though, Powell held the wait-and-see line set out at last week’s policy meeting, offering nothing new. Money markets assume a first full rate cut to take place in September. The dollar on currency markets loses out against all G10 peers, a move which we see closely related to the sharp drop in oil prices (Brent tumbled from over $80/b yesterday to below $69 currently) following the ceasefire. EUR/USD again extensively tested the 1.16 YtD high area. The trade-weighted index is at a key technical juncture around 98. The Japanese yen finds some footing after slipping yesterday. USD/JPY fills offers around 145.1. GBP also recovers from a recent slump against the euro. EUR/GBP trades around 0.852.

News & Views

The monthly composite confidence indicator released by the Czech statistical office for June eased slightly from 101.0 to 100.1, but remained just above its long-term average. Business confidence fell from 101 to 100 while consumer confidence remained unchanged at 100.7. Confidence increased in the construction sector (+6.5 points) and slightly in industry (+0.3 points). It fell by 3.7 points in trade and by 2.8 points in selected service sectors. Regarding consumer confidence, the balance of consumers expecting the economic situation in the Czech Republic to deteriorate over the next twelve months was almost unchanged. Households were split in their financial situation expectations over the next 12 months. Households' concerns about unemployment and price increases over the next twelve months decreased slightly. Still confidence was lower compared to the same month last year. Despite a mixed economic picture, the Czech national Bank recently showed highly reluctant to ease the policy rate from current level of 3.5%.

The CBI industrial trends survey continues to pain a bleak picture on the UK industrial sector. Manufacturing output again fell at the steep pace in the three months to June -23% from -25% in May. Output decreased in 14 out of 17 sub-sectors in the three months to June, with the decline driven by chemicals, metal products and mechanical engineering. Looking ahead, firms anticipate the pace of the decline to slow over the three months to September. Total order books were reported as below “normal” in June and remained significantly below the long-run average. This was also the case for export orders. Expectations for average selling price inflation eased in June (+19% from +26% in May) but remained above the long-run average (+7%). CBI concludes that "The UK's manufacturing sector is under significant pressure, contending with high energy costs, rising labour costs, pervasive skills shortages, and a volatile global economic environment’.

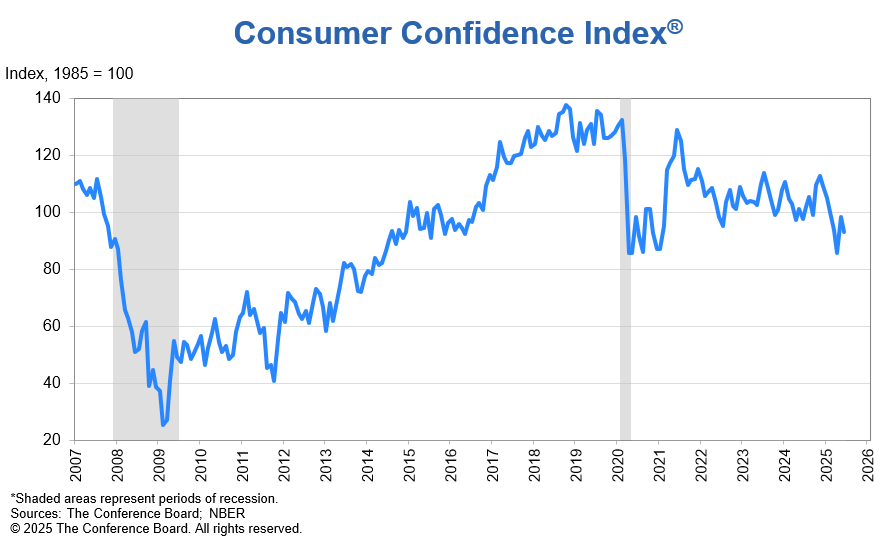

US consumer confidence slumps to 93.0, expectations signal recession risk

US consumer confidence deteriorated in June, with the Conference Board index falling from 98.3 to 93.0, missing expectations of 99.1. Present Situation Index dropped -6.4 points to 129.1. Expectations Index fell -4.6 points to 69.0, well below the 80 threshold that typically flags recession risks.

Senior Economist Stephanie Guichard noted that consumers were less upbeat about business conditions and job availability, with the latter weakening for a sixth straight month, albeit still consistent with a solid labor market.

More worryingly, the three key subcomponents of the Expectations Index—business outlook, job prospects, and future income—each declined. Consumers grew more pessimistic about economic conditions over the next six months, reflecting growing anxiety over both domestic headwinds and global uncertainties.

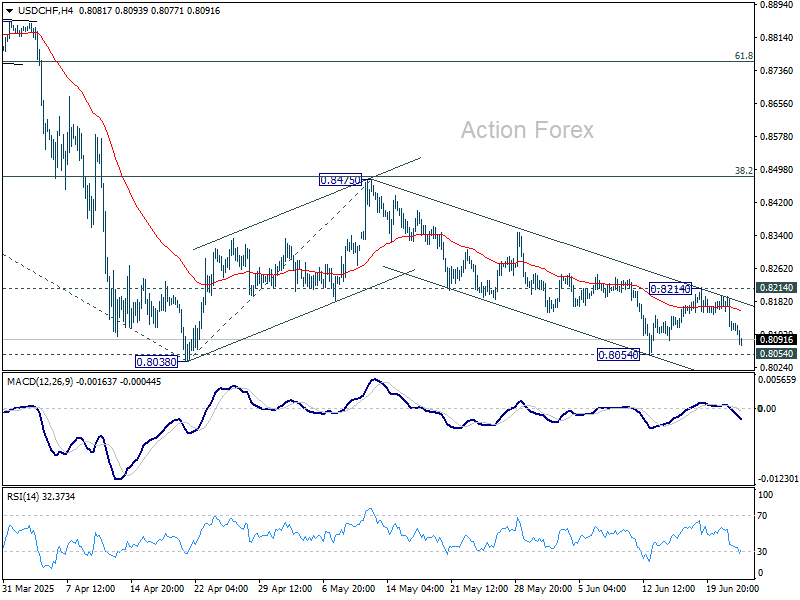

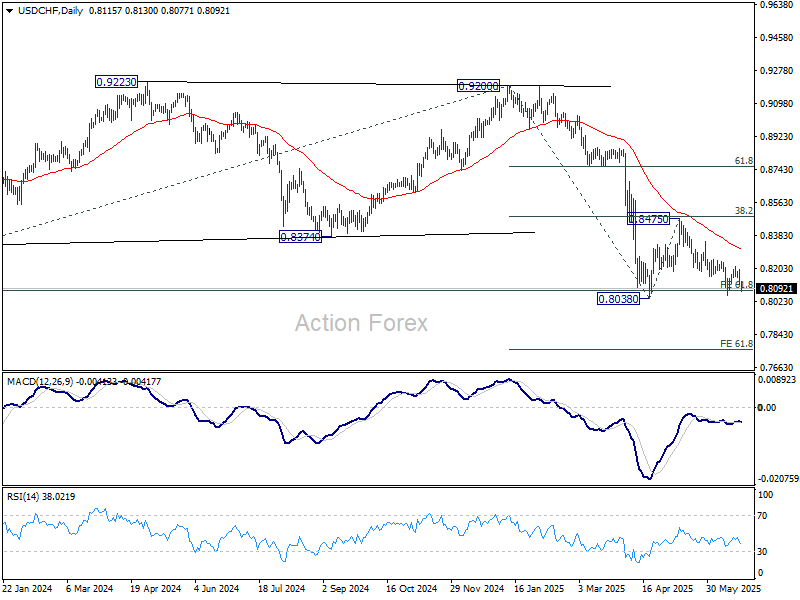

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8096; (P) 0.8146; (R1) 0.8176; More….

Intraday bias in USD/CHF remains on the downside at this point. Decisive break of 0.8038 low will resume larger down trend to 61.8% projection of 0.9200 to 0.8038 from 0.8475 at 0.7757. Nevertheless, break of 0.8214 resistance will extend the corrective pattern from 0.8038 with another rising leg, and target 0.8475 resistance again.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress and met 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.8079 already. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8640) holds. Sustained break of 0.8079 will target 100% projection at 0.7382.

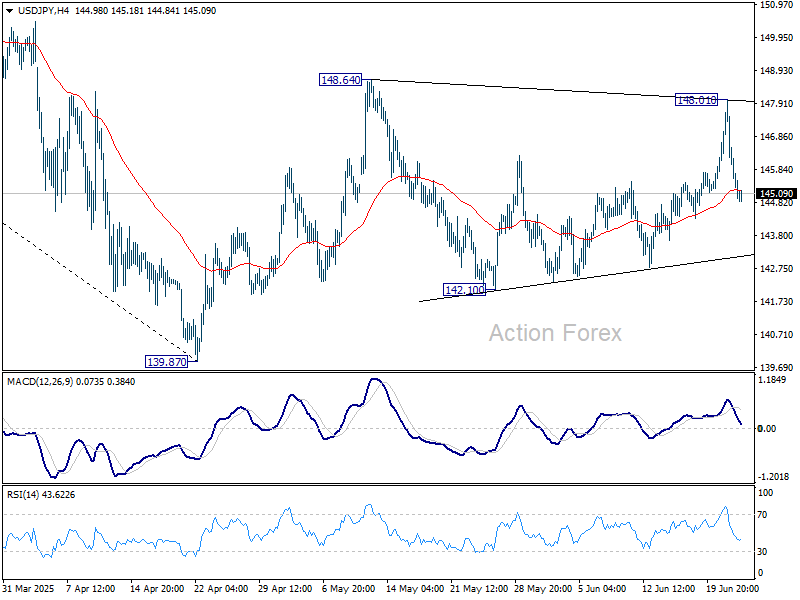

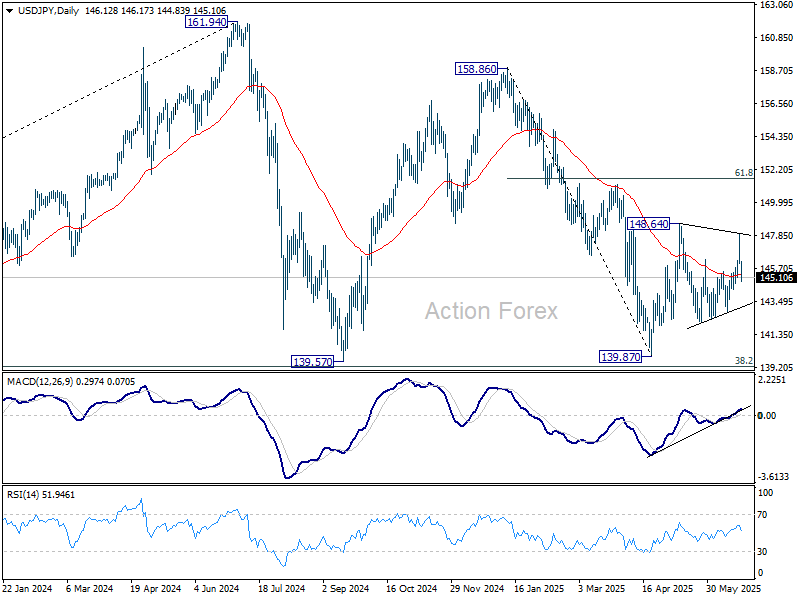

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 145.43; (P) 146.72; (R1) 147.44; More...

Intraday bias in USD/JPY remains neutral for the moment. Sideway pattern from 148.64 is extending with another falling leg. On the upside. firm break of 148.64 will resume the rise from 139.87 to 61.8% retracement of 158.86 to 139.87 at 151.22.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

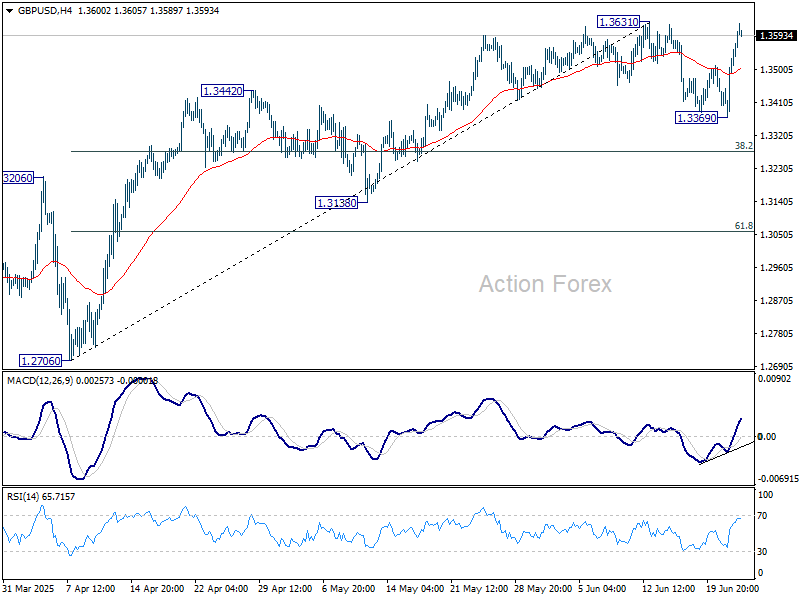

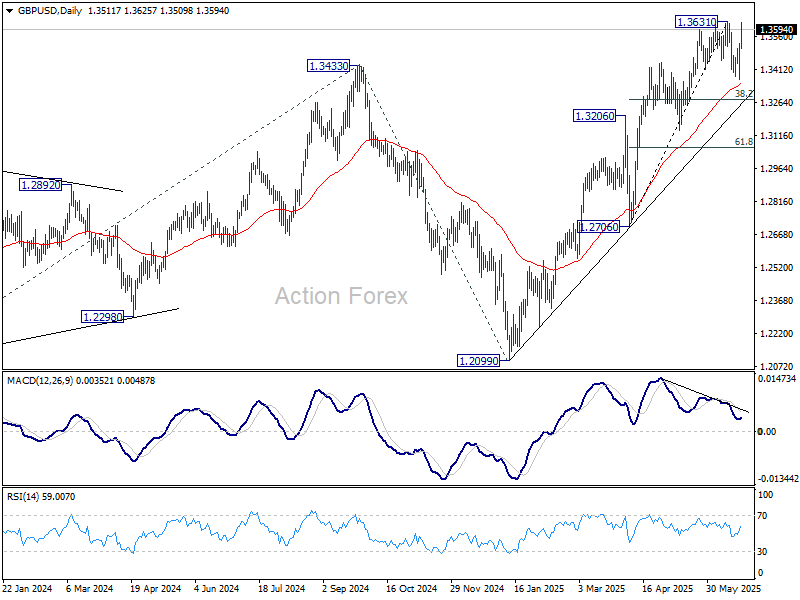

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3420; (P) 1.3475; (R1) 1.3580; More...

Intraday bias in GBP/USD remains on the upside for the moment. Decisive break of 1.3631 resistance will resume larger rally. Next target is 1.4004 projection level. Nevertheless, break of 1.3369 will extend the corrective pattern from 1.3631 with another falling leg instead.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.2948) holds, even in case of deep pullback.

Canada: Cooling Rents Help Temper May Inflation

Headline CPI inflation for May came in at 1.7% year-on-year (y/y), maintaining the pace from April and in line with expectations for a 1.7% y/y print.

The deceleration was due to a slowdown in rent inflation (4.5% y/y vs. 5.2% in April) and falling prices for travel tours (-0.2% y/y).

Inflation in new car prices ticked up, now 4.9% y/y, lifted higher by rising costs for electric vehicles.

The Bank of Canada's (BoC) preferred "core" inflation measures both ticked down to 3.0% y/y in May. The CPI excluding the eight most volatile components and indirect taxes (CPIX) and CPI excluding food and energy both followed the same pattern, ticking down to 2.5% y/y from 2.6% y/y the month prior. On a seasonally adjusted basis, all four measures of core inflation cooled in May.

Key Implications

After last month's unpleasant inflation surprise, May's data came in largely as expected. Top line inflation continues to be restrained as the impact of the end to the consumer carbon tax offset changes in energy prices. For core inflation there was good news too, as all four measures cooled amid falling travel tour and rent prices. The ongoing challenges in the housing market (particularly in Ontario) should help to temper further gains in rents in the coming months.

After last month's uptick in core inflation some giveback was expected. The labour market remains soft and tepid domestic demand growth should keep a lid on inflationary pressures. As has been the case this year, the outlook is heavily dependent on how trade negotiations evolve, but we believe that the soft economic backdrop should give the BoC space to deliver two more cuts this year.