Sample Category Title

USD/JPY Daily Outlook

Daily Pivots: (S1) 145.43; (P) 146.72; (R1) 147.44; More...

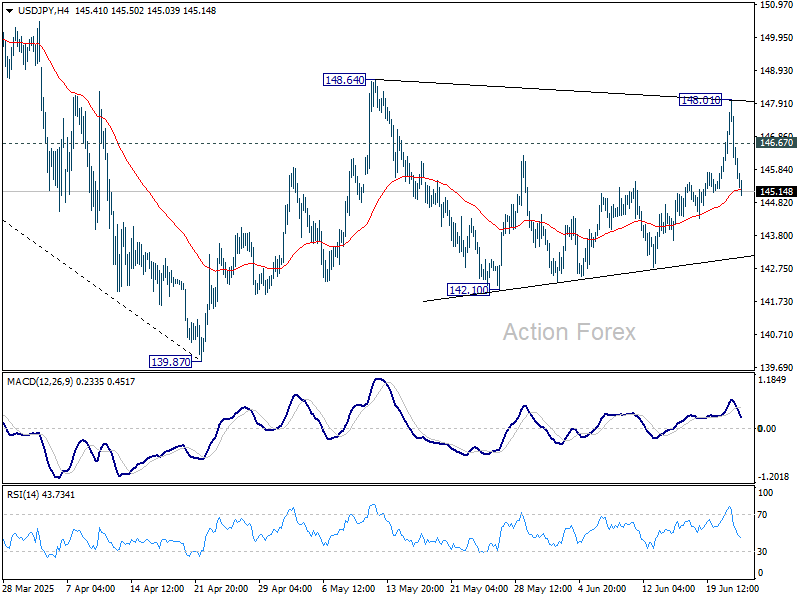

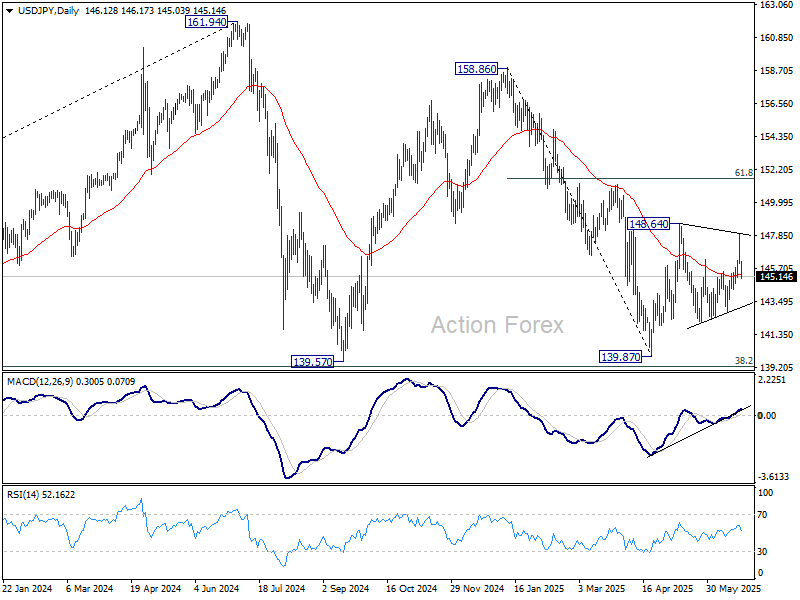

USD/JPY's steep fall suggests that rebound from 142.10 has completed at 148.01 already. Sideway pattern from 148.64 is extending with another falling leg. Intraday bias is turned neutral. On the upside. firm break of 148.64 will resume the rise from 139.87 to 61.8% retracement of 158.86 to 139.87 at 151.22.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8096; (P) 0.8146; (R1) 0.8176; More….

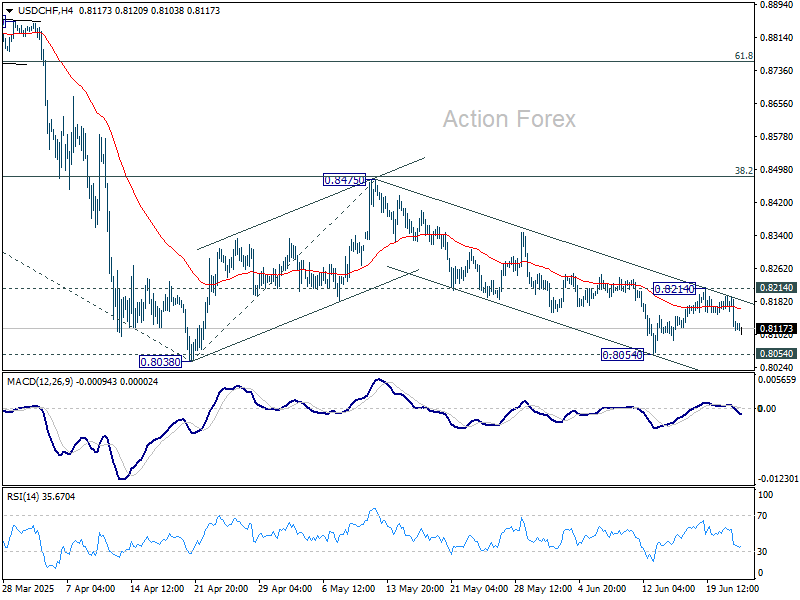

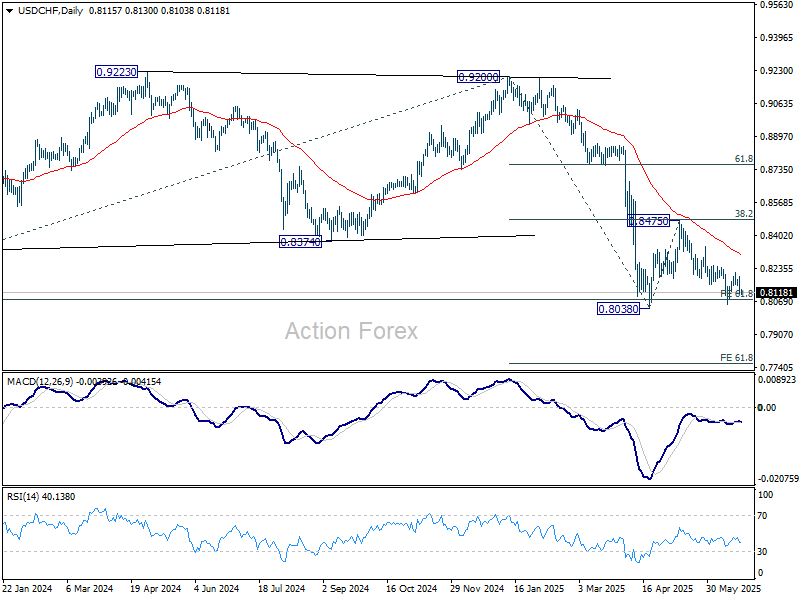

The extended fall in USD/CHF suggests that recovery from 0.8054 has completed at 0.8214 already. Intraday bias is back on the downside. Decisive break of 0.8038 low will resume larger down trend to 61.8% projection of 0.9200 to 0.8038 from 0.8475 at 0.7757. Nevertheless, break of 0.8214 resistance will extend the corrective pattern from 0.8038 with another rising leg, and target 0.8475 resistance again.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress and met 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.8079 already. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8640) holds. Sustained break of 0.8079 will target 100% projection at 0.7382.

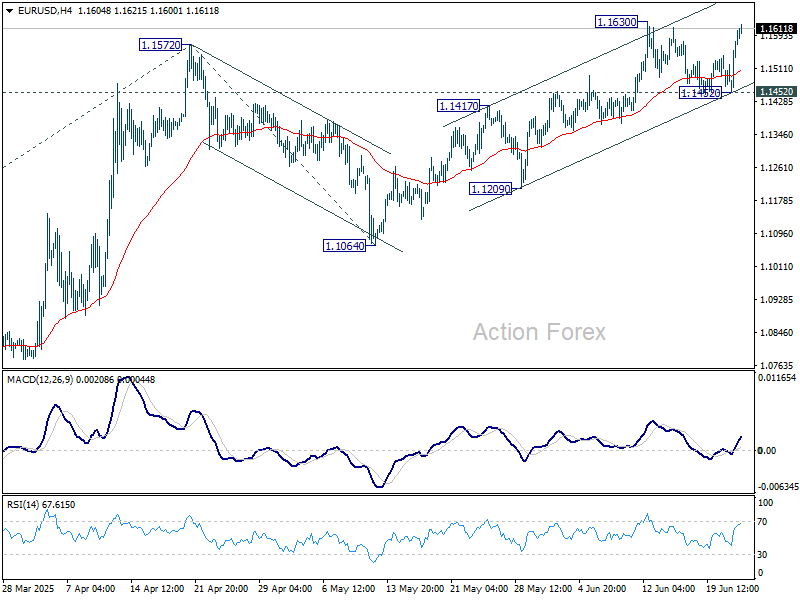

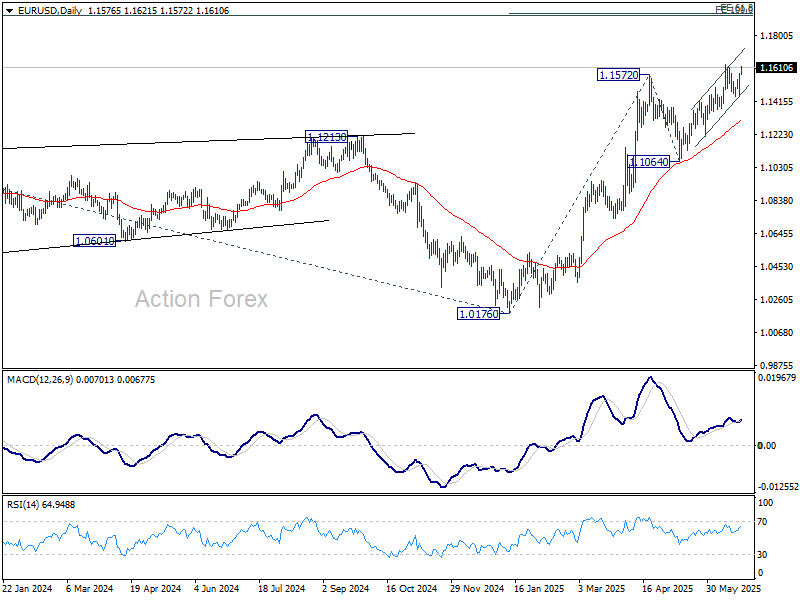

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1495; (P) 1.1538; (R1) 1.1623; More...

EUR/USD is still capped below 1.1630 despite today's rally. Intraday bias stays neutral first. With 1.1452 support intact, further rise is expected. Break of 1.1630 resistance will extend the rise from 1.0176. Next target is 61.8% projection of 1.0176 to 1.1572 from 1.1064 at 1.1927. However, break of 1.1452 support will indicate short term topping, and turn bias to the downside for deeper pullback.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 1.1604 support holds.

Mideast Tensions Put, Trade Uncertainties In

Middle East tensions suddenly waned after Iran fired missiles at a US air base in Qatar — having reportedly informed the US in advance. As a result, the missiles were intercepted. President Trump called Iran’s move ‘weak’ and announced a few hours ago that Israel and Iran had reached a ceasefire agreement. A surprisingly swift development. Once again, Iran appears to have retaliated just enough to save face — without triggering broader escalation. Tensions will likely ease from here if Israel reciprocates. However, it remains unclear whether an actual ceasefire is in place, as missiles reportedly continue to be fired across the border. Iran has said it will stop if Israel does, but Israel has yet to make a formal statement.

In energy markets, US crude tumbled nearly 10% yesterday, Brent crude dropped almost 9%, and natural gas lost nearly 5% — falling below its 100-DMA this morning. The sharp retreat reflects fading concerns that Iran might disrupt oil and gas flows through the Strait of Hormuz. Oil prices have now pulled back to levels seen before tensions between Israel and Iran flared earlier this month. While prices are rebounding slightly this morning amid ceasefire uncertainty, waning Middle East tensions — and the perception that the worst is over — could limit upside for US crude near the 200-DMA. Focus may now return to core fundamentals: OPEC’s production ramp-up plans, global demand trends, and softening growth outlook — all of which argue for weaker oil prices. Should the market revert to a pre-tension scenario, US crude could fall below $65 per barrel and resume its year-to-date bearish trajectory. If tensions re-escalate, prices may spike again — but geopolitically driven rallies tend to be short-lived and are better suited for tactical plays than long-term exposure.

Elsewhere, gold is softer this morning, and the US dollar — which had benefitted from safe-haven inflows — is giving back gains. The EURUSD has risen above 1.16, the USDJPY is sharply down to 145, and the AUDUSD is back to the 0.65 level. FX markets are clearly reflecting the de-escalation narrative.

Equities also reflect this shift. Chinese stocks are trading higher, and Japan’s Nikkei is testing the highest levels since April. European defense stocks rebounded from yesterday’s dip as NATO members gather in The Hague — where leaders are expected to reaffirm plans to spend around 3.5% of GDP on ‘hard defense’ (troops and weapons) and an additional 1.5% on defense-related areas like cybersecurity and military mobility. But with most of this already priced in, the upside may be limited. Meanwhile, the Stoxx 600 has slipped below its 50-DMA, weighed down by a lack of progress on trade negotiations. The July 9th tariff deadline is fast approaching — and yet, there’s been no meaningful update.

In contrast, US equities closed higher Monday, with futures pointing to further gains this morning. Gains in US equities are supported by improved risk appetite and rising expectations of a dovish Federal Reserve (Fed), which have pushed the 2-year Treasury yield further below the 4% mark. This is notable because the Fed’s hawkish stance — especially relative to the European Central Bank (ECB) — had been a key driver of the US-Europe convergence trade. Now, a reversal in that narrative could shift flows.

That said, Fed Chair Jerome Powell may temper dovish expectations during his semi-annual testimony, which begins today and continues tomorrow. He’s likely to maintain a cautious tone, emphasizing that inflation remains too high to justify a rate cut before the fall — especially amid ongoing geopolitical and trade uncertainty.

All in all, questions linger about the White House’s tariff strategy as the July deadline for the reciprocal tariff pause looms. Trump was expected to deliver clarity around now — but headlines have been dominated by Middle East events. If tensions continue to ease, trade talks could return to the spotlight and potentially shift risk sentiment on both sides of the Atlantic. However, tangible progress will be needed to keep the Stoxx 600 above the 200-DMA.

Trump Reports Ceasefire Amid Iran Missile Launch

In focus today

In the US, the Conference Board's consumer confidence survey for June will be published. Sentiment has improved across most surveys following the preliminary US-China trade deal in May.

In Germany, focus turns to the Ifo indicator for June. Yesterday's PMI data showed that the German economy improved in June, with the composite indicator rising more than expected to 50.4 from 48.5 in May. Hence, we expect the Ifo indicator to also improve in June.

In Sweden, Riksbank governor Thedéen and deputy governor Bunge will participate in Q&A sessions during Almedalen week (13.30 CET and 14.30 CET) on interest rates and the Swedish economy. We will look for any clues on the outlook. The Riksbank suggested a possible 12bp rate cut in the June MPR, despite core inflation forecasts around 3%. We believe rate cuts have been finished, but downside risks persist due to the Riksbank's communication and focus on economic recovery.

In Hungary, the central bank will announce its rate decision. We forecast an unchanged decision at 6.50%, aligning with consensus.

In the NATO summit (24-25 June), country leaders are expected to adopt a new 5% target for defence expenditure as a share of GDP, with 3.5% allocated to actual defence spending and 1.5% directed towards additional investments in resilience. Germany supports the target, while France and Italy call for flexibility, and Spain opposes it.

Today we have a series of speeches from both the ECB, including President Lagarde, and the BoE, alongside several Federal Reserve speakers. We will look out for more clues on monetary policy.

Economic and market news

What happened overnight

In the Middle East conflict, President Trump announced on Truth Social that Israel and Iran had agreed to a staged ceasefire to end the 12-day war, set to begin this morning. However, Iran denied the existence of such an agreement, stating they would stop hostilities if Israel ceased its aggression by 4am Tehran time. This morning, a wave of missiles was shot from Iran towards Israel. Israel has not yet issued an official response regarding the ceasefire.

What happened yesterday

In the Middle East, tensions appeared to escalate yesterday as Iran launched missile strikes on US air bases in Qatar and Iraq. However, the pre-warned attack was welcomed by Trump describing it as a "very weak response", with no causalities reported. As the immediate threat to the Strait of Hormuz diminished, Brent Crude oil saw one of its largest one-day declines in five years, as oil prices has dropped more than USD 7/bbl since yesterday.

In the euro area, June PMI came in slightly below expectations, reflecting economic stagnation. The composite indicator was unchanged at 50.2 (cons: 50.5, prior: 50.2), services rose to 50.0 (cons: 50.0, prior: 49.7) and manufacturing was unchanged at 49.4 (cons: 49.8, prior: 49.4). Manufacturing details were weak, with declines in output and employment offset by longer delivery times, keeping the index unchanged. Price pressures remain muted. We expect euro area GDP growth at 0.0% q/q in Q2 after the strong 0.6% q/q rise in Q1, that was driven by front-loading of exports to the US.

In the US, PMIs declined slightly to 52.8 from 53.0 in May, aligning with expectations. Inflation indicators present a mixed picture, with services prices falling and manufacturing prices rising. Subindices show minimal change, and new orders have decreased slightly, still indicating modest growth.

Fed governor Bowman made dovish remarks, expressing readiness for a July rate cut, citing job market risks and minimal inflation impact from tariffs, with inflation nearing the 2%-target.

Equities: For many investors, global markets probably displayed surprising composure yesterday given the severe escalation in the Middle East over the weekend. With Iran's retaliatory strike materialising as a relatively contained attack on a US military base in Qatar, risk sentiment notably improved late in the US session, after the close of European cash equity markets. The US equity market responded accordingly: 24 out of 25 sectors closed higher, with the only exception being Energy, which declined by 2.5% as crude prices dropped sharply. Oil is now down nearly 10% over the past two sessions, and the downward momentum continues in early Tuesday trading. The equity market reaction close to textbook example: energy stocks under pressure, while the broader market benefits from lower geopolitical risk premia. For whatever it is worth, we must once again admit that the geopolitical narrative is setting the tone in financial markets, while traditional macro models are playing a secondary role in day-to-day market movements. In the US yesterday, Dow +0.9%, S&P 500 +1.0%, Nasdaq +0.9% and Russell 2000 +1.1%. Asian markets have taken the cue from Wall Street's late-session relief, with South Korea leading regional gains this morning - up more than 3%. Futures across Europe and the US are markedly higher.

FI and FX: EUR/USD was in for a v-shaped price action during yesterday's session, initially hit by poor risk sentiment but later rallied towards the 1.16 mark as the USD weakened broadly. Markets interpreted Iran's retaliatory strike on a US base in Qatar as largely symbolic and Trump later announced a ceasefire between Israel and Iran. This pushed oil prices back below 70 USD/bbl and equities rallied. In rates space, 10Y Treasuries yields rose after having initially declined some 10bp earlier on Monday. The curve steepened modestly driven by the decline in the front-end US Treasury yields.

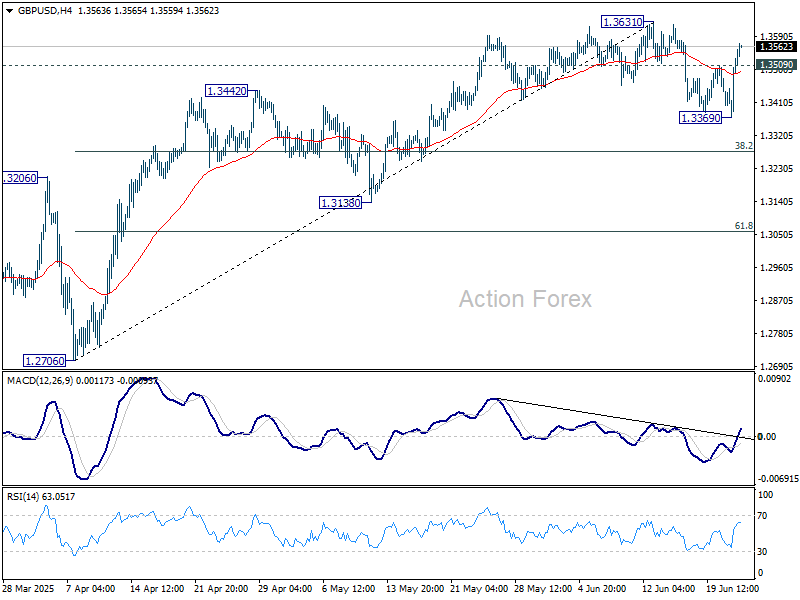

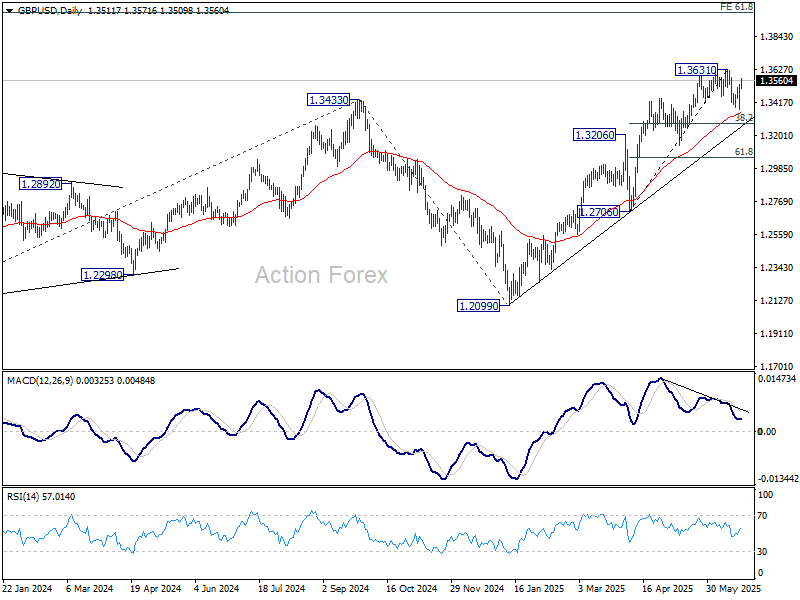

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3420; (P) 1.3475; (R1) 1.3580; More...

GBP/USD's strong rebound suggest that pullback from 1.3631 has already completed at 1.3369. Intraday bias is back on the upside for retesting 1.3631 first. Firm break there will resume larger rally to 1.4004 projection level next. Nevertheless, break of 1.3369 will extend the correction with another falling leg instead.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.2948) holds, even in case of deep pullback.

Fed Doves, Ceasefire Talk Sink Dollar as Risk Appetite Rebuilds

Dollar fell sharply overnight and extended its slide through Tuesday’s Asian session, as traders responded to dovish Fed commentary and easing geopolitical risks. Vice Chair Michelle Bowman signaled she would support a rate cut as soon as July if inflation pressures remain contained and labor market data weakens further. Her comments followed similar remarks from Governor Christopher Waller last week, suggesting the dovish wing of the FOMC may now be gaining traction.

Market pricing for a July cut jumped notably, rising from just 15% a day ago to around 25%. The timing couldn’t be more important, with Fed Chair Jerome Powell set to deliver his semiannual testimony to Congress starting today. If Powell signals any openness to a near-term rate cut, it would mark a meaningful departure from the Fed’s recent cautious stance, and potentially trigger another leg lower for the greenback this week.

A parallel driver of Dollar's weakness is the reversal in geopolitical sentiment. Oil prices' plunged after restrained retaliation by Iran. The sell off then intensified after US President Trump declared a ceasefire between Israel and Iran, triggering a further unwind in long crude positions. Although Iran launched final salvos of missiles after the announcement, Iranian state media framed the response as complete, reinforcing the view that tensions may be easing. That was enough to support a return to risk-on positioning in Asian markets and further erode Dollar’s safe haven appeal.

Trade developments also remain in focus. Japan’s top tariff negotiator Ryosei Akazawa is preparing to visit Washington for a new round of talks beginning June 26. The visit comes as Japanese officials press for relief from US tariffs on auto exports—a key pain point for Tokyo. The upcoming meeting will be the first high-level engagement since the June 16 summit between Prime Minister Shigeru Ishiba and President Trump, which failed to yield a breakthrough.

Meanwhile, Canada and the EU are reinforcing their transatlantic alliance through a new defense partnership. Canadian Prime Minister Carney reaffirmed Ottawa’s commitment to working with Brussels but maintained a cautious stance on US trade talks, reiterating that only the “right deal” would be acceptable.

In the currency markets, Dollar is now the weakest performer this week, followed by Loonie and Yen. Sterling leads the gains, while Kiwi and Swiss Franc follow. Euro and Aussie are positioning in the middle.

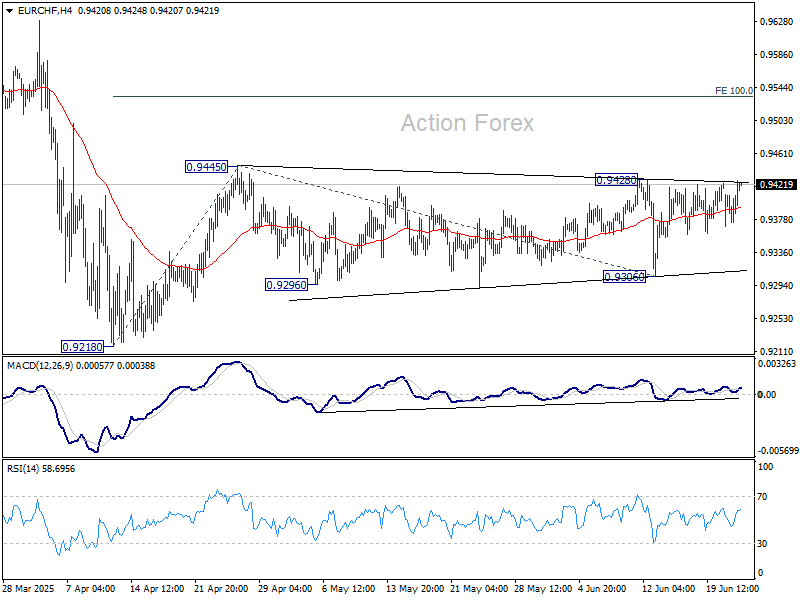

Technically, as geopolitical fears fade, EUR/CHF could be poised for an upside breakout. Firm break of 0.9428/45 resistance zone will resume whole rebound from 0.9218 and target 100% projection of 0.9218 to 0.9445 from 0.9306 at 0.9533. That would likely be accompanied by break of 1.1630 resistance in EUR/USD.

In Asia, at the time of writing, Nikkei is up 1.18%. Hong Kong HSI is up 2.17%. China Shanghai SSE is up 1.07%. Singapore Strait Times is up 0.51%. Japan 10-year JGB yield is up 0.006 at 1.417. Overnight, DOW rose 0.89%. S&P 500 rose 0.96%. NASDAQ rose 0.94%. 10-year yield fell -0.055 to 4.320.

Oil crashes on ceasefire hopes, market unwinds war premium

Oil prices plunged overnight as markets reassessed geopolitical risk following what appears to be a restrained Iranian response to US strikes and a potential ceasefire between Iran and Israel. WTI tumbled sharply after reports that Iranian forces attacked a US base in Qatar—an incident that was intercepted with no reported casualties. The muted retaliation defused immediate fears of further escalation, setting the stage for a pullback in crude. Sentiment turned further when US President Donald Trump declared a 12-hour ceasefire between Israel and Iran, announcing the end of what he called the “12 Day War.”

Technically, nonetheless, the steep selloff in WTI should have marked the complete of the whole rebound from 55.20 low at 78.87, well ahead of 81.01 key structural resistance. Short covering could come at around 61.8% retracement of 55.20 to 78.87 at 64.24, and bring bounce. That should set the range of sideway trading in the near term between 64/79.

Fed's Goolsbee: Tariff impact milder than feared, cuts still on the table

Chicago Fed President Austan Goolsbee struck a cautiously optimistic tone Monday, saying that the recent surge in tariffs has not delivered the economic shock many had feared.

Speaking at a mid-year business outlook event in Milwaukee, Goolsbee noted that the fallout so far has been “somewhat surprisingly” modest, particularly in terms of inflation. While uncertainty remains around future price pressures, the current evidence suggests that the economy may still be on a favorable course.

“If we do not see inflation resulting from these tariff increases,” Goolsbee said, “then, in my mind, we never left what I was calling the golden path before April 2.” That path—defined by disinflation without a major slowdown—would support the case for eventual rate cuts.

His remarks echo a growing sentiment within the Fed that policy easing could resume later this year, provided inflation continues to behave and growth risks mount.

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3420; (P) 1.3475; (R1) 1.3580; More...

GBP/USD's strong rebound suggest that pullback from 1.3631 has already completed at 1.3369. Intraday bias is back on the upside for retesting 1.3631 first. Firm break there will resume larger rally to 1.4004 projection level next. Nevertheless, break of 1.3369 will extend the correction with another falling leg instead.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.2948) holds, even in case of deep pullback.

GBPJPY Elliott Wave Outlook: Impulse Pattern Approaching End

The short-term Elliott Wave analysis for GBPJPY indicates that the cycle initiated from the April 9, 2025 low has reached a mature stage. The upward movement is unfolding as a five-wave impulse structure, a hallmark of Elliott Wave theory, signaling a strong bullish trend. Wave 1 concluded at 189.82, followed by a corrective pullback in Wave 2, which found support at 185.98. The subsequent rally in Wave 3, as depicted on the 1-hour chart, peaked at 196.84. Wave 4 then unfolded as a zigzag corrective structure. Its internal subdivisions completing as follows: Wave ((a)) declined to 194.75, and wave ((b)) rebounded to 195.33. Wave ((c)) finalized at 196, marking the completion of Wave 4 in the higher degree.

Currently, GBPJPY has resumed its ascent in Wave 5. From the Wave 4 low, the rally has so far developed in three waves. Wave (i) reached 196.7, followed by a dip in Wave (ii) to 196.09. Wave (iii) extended higher to 198.19. A corrective pullback in Wave (iv) is anticipated to find support within the 196.2–196.8 range, likely in a three-wave structure. Afterwards, one final push higher in Wave (v) should happen to complete Wave ((i)) of 5 in the higher degree. Following this, a larger-degree correction in Wave ((ii)) is expected to retrace the cycle from the June 19, 2025 low. Pullback is likely unfolding in a 3, 7, or 11-swing pattern before the pair resumes its upward trajectory.

GBPJPY 60-Minute Elliott Wave Technical Chart

GBPJPY Elliott Wave Technical Video

https://www.youtube.com/watch?v=pIrpGcMW9Ws

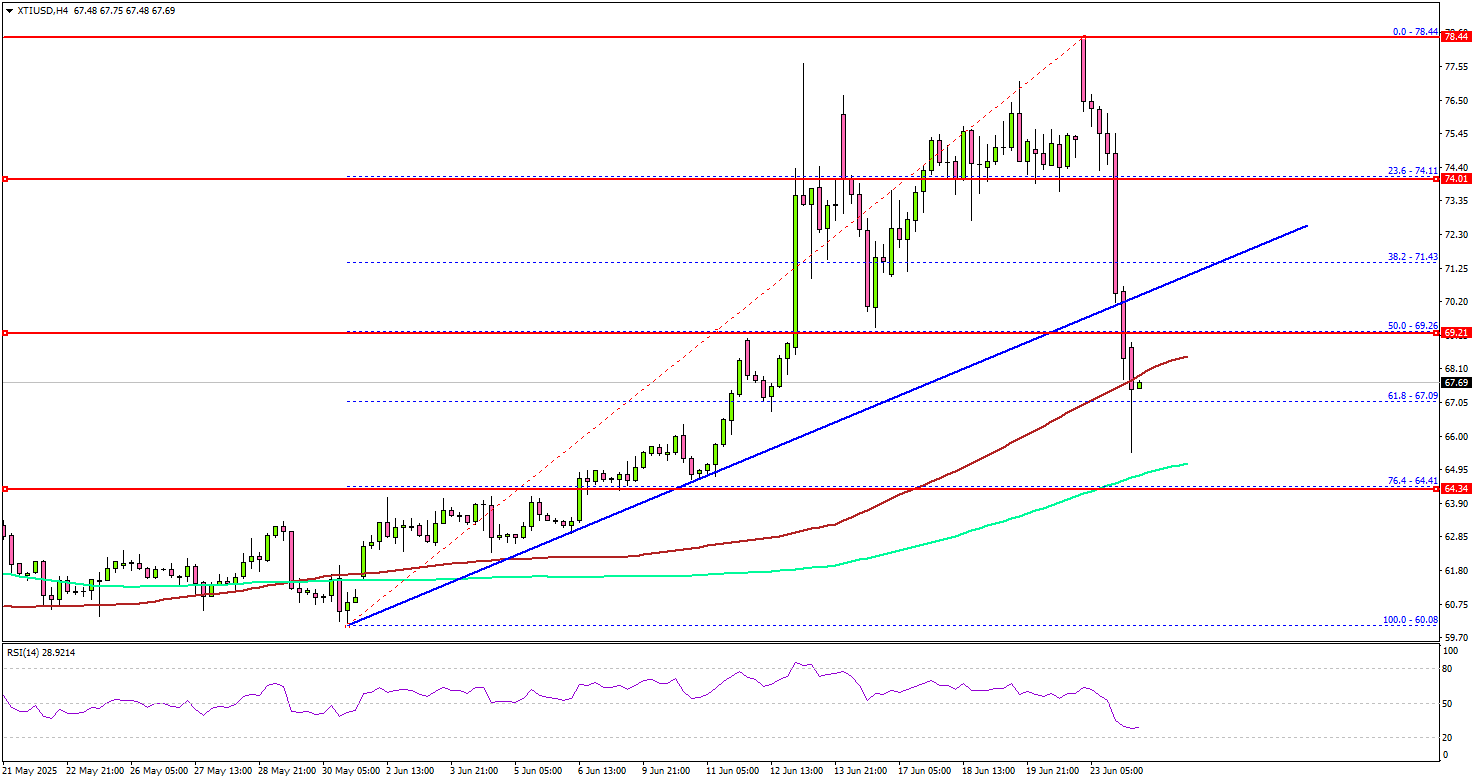

WTI Crude Oil Markets React Sharply — Prices Dive on Ceasefire Breakthrough

Key Highlights

- WTI Crude Oil prices started a major decline from the $78.50 zone.

- It traded below a key bullish trend line with support at $71.50 on the 4-hour chart.

- Gold prices are facing hurdles near the $3,400 resistance.

- EUR/USD regained traction and managed to clear the 1.1550 resistance zone.

WTI Crude Oil Price Technical Analysis

WTI Crude Oil price failed to continue higher above $78.50 against the US Dollar. There was a strong bearish reaction below the $75.00 and $72.00 levels.

Looking at the 4-hour chart of XTI/USD, the price settled below the $70.00 level and the 100 simple moving average (red, 4-hour). It also traded below a key bullish trend line with support at $71.50.

Finally, the price spiked toward the $66.000 level and traded close to the 200 simple moving average (green, 4-hour). On the downside, the first major support sits near the $66.50 zone. The next support could be $65.50.

A daily close below $65.50 could open the doors for a larger decline. The next major support is $64.40. Any more losses might send oil prices toward $60.00 in the coming days.

On the upside, immediate resistance is near the $68.50 level. The first key resistance sits near the $70.00 level. The main hurdle is now near the $72.00 zone, above which the price may perhaps accelerate higher. In the stated case, it could even visit the $75.00 resistance. Any more gains might call for a test of the $78.00 resistance zone in the near term.

Looking at Gold, the bears are active below the $3,400 level, and they might aim for a drop toward the $3,300 level.

Economic Releases to Watch Today

- Fed's Chair Powell testifies.

- BoE's Breeden speech.

- Fed's Williams speech.

Oil crashes on ceasefire hopes, market unwinds war premium

Oil prices plunged overnight as markets reassessed geopolitical risk following what appears to be a restrained Iranian response to US strikes and a potential ceasefire between Iran and Israel. WTI tumbled sharply after reports that Iranian forces attacked a US base in Qatar—an incident that was intercepted with no reported casualties. The muted retaliation defused immediate fears of further escalation, setting the stage for a pullback in crude.

Sentiment turned further when US President Donald Trump declared a 12-hour ceasefire between Israel and Iran, announcing the end of what he called the “12 Day War.” While his comments on social media were optimistic and celebratory, the official Iranian response was more guarded. Foreign Minister Seyed Abbas Araghchi emphasized that no agreement had been reached, though he indicated Iran would halt further retaliation if Israeli operations ceased by 4 a.m. Tehran time.

Technically, nonetheless, the steep selloff in WTI should have marked the complete of the whole rebound from 55.20 low at 78.87, well ahead of 81.01 key structural resistance. Short covering could come at around 61.8% retracement of 55.20 to 78.87 at 64.24, and bring bounce. That should set the range of sideway trading in the near term between 64/79.