Sample Category Title

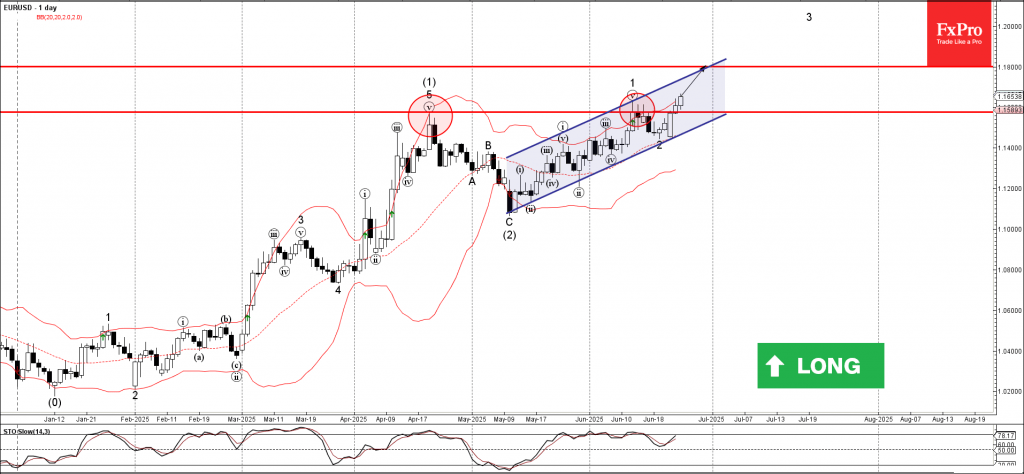

EURUSD Wave Analysis

EURUSD: ⬆️ Buy

- EURUSD broke resistance level 1.1575

- Likely to rise to resistance level 1.1800

EURUSD currency pair recently broke the resistance level 1.1575 , which is the former monthly high from the middle of April.

The breakout of the resistance level 1.1575 continues the active short-term impulse wave 3 of the intermediate impulse wave (3) from the start of May.

Given the strong daily uptrend, EURUSD currency pair can be expected to rise to the next resistance level 1.1800, which intersects with the daily up channel from May.

GBPUSD Wave Analysis

GBPUSD: ⬆️ Buy

- GBPUSD broke resistance level 1.3590

- Likely to rise to resistance level 1.3880

GBPUSD currency pair recently broke the resistance level 1.3590, which is the upper border of the narrow sideways price range inside which the price has been moving from May.

The breakout of the resistance level 1.3590 accelerated the active intermediate impulse wave (3).

Given the clear daily uptrend and the strong US dollar sales seen today, GBPUSD currency pair can be expected to rise to the next resistance level 1.3880.

Fed’s Collins: “Active patience” warranted as tariff uncertainty clouds outlook

Boston Fed President Susan Collins expressed her preference for what she termed an “actively patient” approach to monetary policy, saying it remains appropriate amid rising uncertainty. Speaking today, Collins pointed to the fluidity in tariff developments and broader government policy shifts, which she said “validate the careful approach” Fed has taken so far in 2025. While she still expects gradual policy normalization to resume later this year, she warned her view "could change significantly as events unfold".

Collins emphasized that much hinges on the nature of the “price shock” driven by tariffs. If price pressures fade quickly without unanchoring inflation expectations, and if the hit to real activity remains limited, she said it could support easing later in the year. However, if those conditions are not met, policy adjustments may be delayed.

For now, Collins views current monetary policy as “modestly restrictive,” and well-positioned to deal with a range of potential outcomes.

Sunset Market Commentary

Markets

Today’s NATO summit in the Netherlands should have been all about member nations stepping up efforts on defense spending. They effectively agreed to meet the US demand to target 5% of GDP by 2035. Instead, all questions went US President Trump’s way. A leaked, preliminary, intelligence report produced by the Defense Intelligence Agency suggested that the US airstrikes only set Iran’s nuclear progress back for about six months. Trump countered those rumours, talking about total obliteration and indicating that more detailed reports will come shortly. The NATO headlines equally proved the lack of other news in financial markets. Empty eco calendars on both sides of the Atlantic are testament to that. Bear steepening continued on European bond markets after German cabinet yesterday approved the expansionary multi-year budget which will result in net new debt issuance in excess of €500bn between this year and 2029. Higher term premia push long end bond yields higher. Daily changes in Germany today range between +1 bp (2-yr) and +4 bps (30-yr). The 30-yr yield sets a month-to-date high at 3.06% and shows tentative technical signs of heading to the YtD top above 3.20%. The long end of the US curve underperforms as well (+3 bps) with US Senate racing to get their version of Trump’s big beautiful bill voted in order to keep the self-imposed 4th of July deadline in alive. Succeeding implies putting US finances on an even more unsustainable path going forward and will again result in higher term/credit risk premia. Unlike in Europe, the steepening in the US is also driven by an outperformance of the front end of the curve after Fed Chair Powell for the first time emphasized the possibility of earlier rates cuts in case of a weakening labour market or modest impact from tariffs. July is ruled out, but September seriously comes into play. The subtle change of tone suggests asymmetric risks for next week’s US eco data update including ISM’s, ADP employment change and of course payrolls with markets (ST US bond yields & US dollar) especially sensitive to weaker numbers. EUR/USD is taking a breather at 1.16 today, but the technical picture suggests a continuation of the buy-the-dip pattern in place since the German fiscal U-turn early March.

News & Views

One in three central banks plan to increase gold holdings in the next one to two years after already having accumulated the bullion at breakneck pace, the Official Monetary and Financial Institutions Forum (OMFIF) said in a report. 40% of the 75 central bank’s surveyed plans to raise holdings over the next decade. The OMFIF found that 70% was discouraged in investing in the dollar due to the US political environment, though the vast majority (80%) still see the greenback as offering safety and liquidity. It nevertheless dropped from first place to seventh in terms of popularity as central banks are diversifying away from the currency. The euro was the most in demand with a next 16% planning to increase holdings over the next one to two years. That’s up from 7% last year. Over the next decade, however, the Chinese yuan is more favoured with a net 30% expecting to increase their holdings.

France appears to be leaving behind a period of relative political calm. Negotiations over a retirement reform have collapsed after four months. The 2023 reform amongst others included a raise in the minimum retirement age to 64 from 62. Some leftist lawmakers in return for their support in the minority government’s 2025 budget in February demanded some aspects of the 2023 law to be revised. The leftist parties including the Socialist Party have now proposed a vote of no confidence to topple the government. But this requires the support of the far-right National Rally, something it said it won’t give. Instead, the RN is preparing for a different battle: public finances. The French government led by PM Bayrou is due to present the main points of the 2026 budget by mid-July before formally presenting it in October. RN party leader Bardella last week said this finance bill will be “the moment of truth for censure.” Another RN lawmaker, Jean-Philippe Tanguy, today said that the party would seek to topple the government if Bayrou goes ahead with certain tax increases and spending cuts.

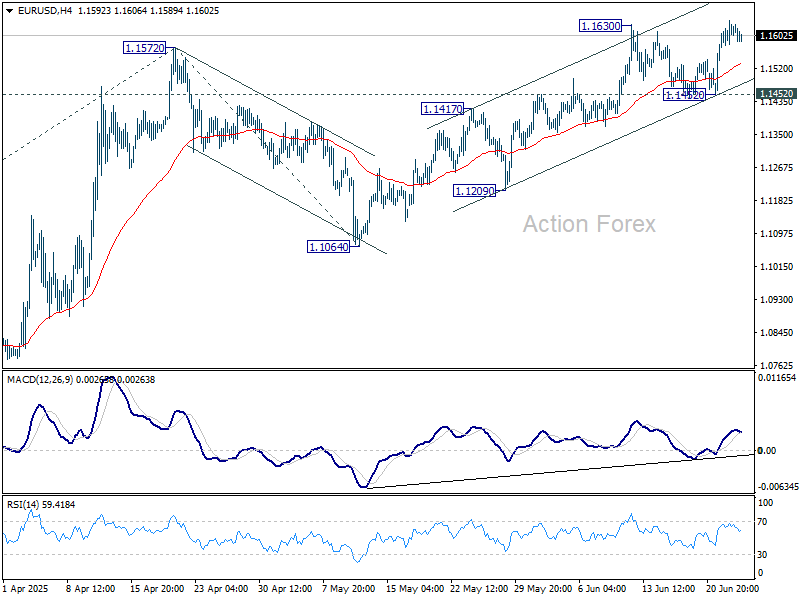

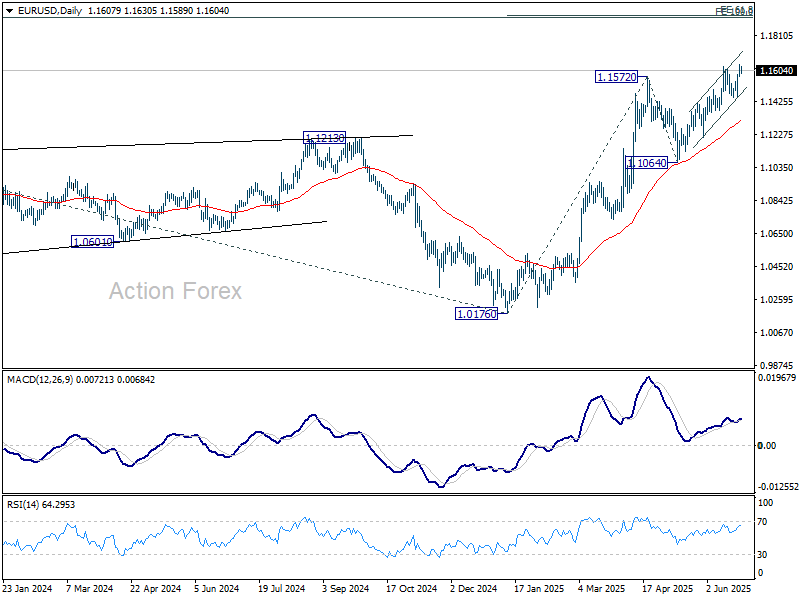

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1575; (P) 1.1608; (R1) 1.1643; More...

Intraday bias in EUR/USD stays mildly on the upside at this point. Sustained trading above 1.1630 will pave the way to 61.8% projection of 1.0176 to 1.1572 from 1.1064 at 1.1927. Outlook will stay bullish as long as 1.1452 support holds, in case of retreat.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 1.1604 support holds.

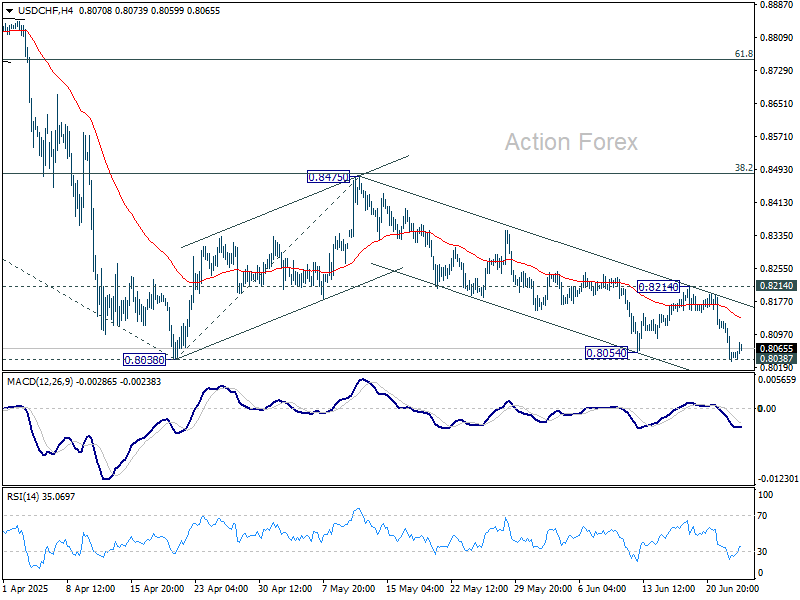

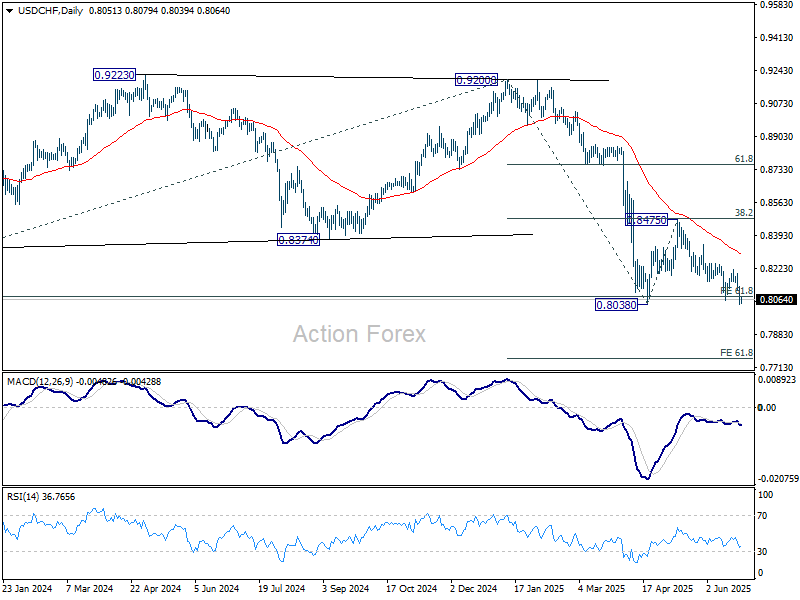

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8013; (P) 0.8074; (R1) 0.8114; More….

Intraday bias in USD/CHF stays on the downside with focus on 0.8038 low. Firm break there will confirm larger down trend resumption. Next target is 61.8% projection of 0.9200 to 0.8038 from 0.8475 at 0.7757. For now, risk will stay on the downside as long as 0.8214 resistance holds, in case of recovery.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress and met 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.8079 already. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8640) holds. Sustained break of 0.8079 will target 100% projection at 0.7382.

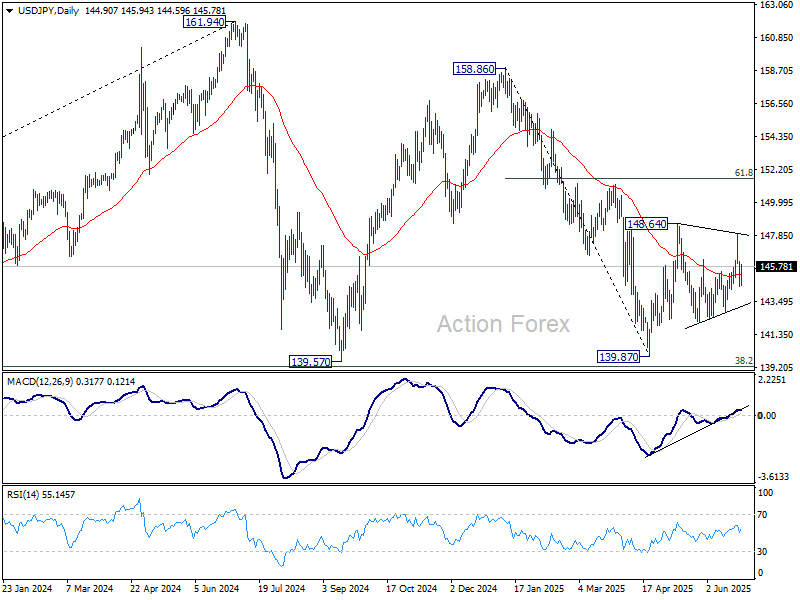

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 145.43; (P) 146.72; (R1) 147.44; More...

Range trading continues in USD/JPY and intraday bias stays neutral for the moment. Further rise will remain mildly in favor as long as 142.10 support holds. On the upside. firm break of 148.64 will resume the rise from 139.87 to 61.8% retracement of 158.86 to 139.87 at 151.22.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

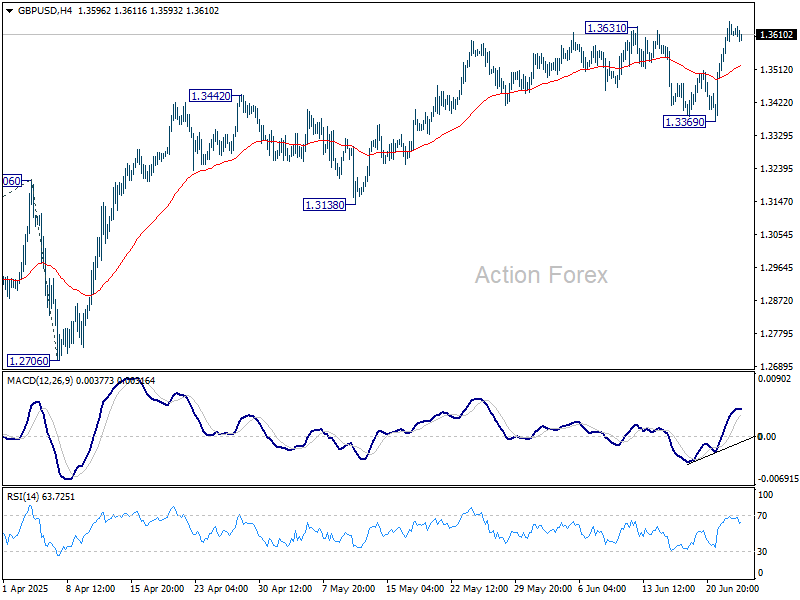

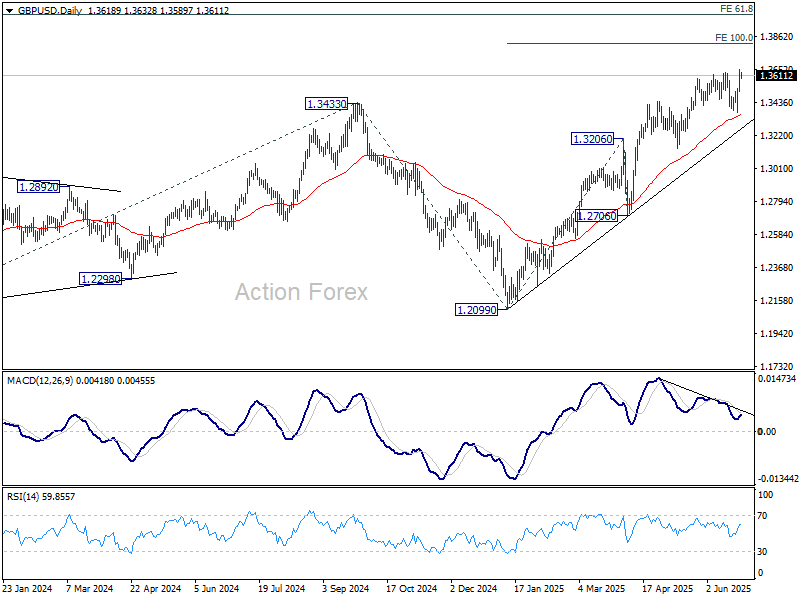

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3524; (P) 1.3586; (R1) 1.3678; More...

Intraday bias in GBP/USD stays on the upside despite today's slight retreat. Rally from 1.2099 is resuming, and should target 100% projection of 1.2099 to 1.3206 from 1.3138 at 1.3813. Outlook will now stay bullish as long as 1.3369 support holds, even in case of deeper pullback.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.2948) holds, even in case of deep pullback.

Dollar Stabilizes After Slide as Calm Returns to Markets

Wednesday brought a lull in FX volatility as Dollar’s selloff eased, though it remained broadly under pressure for the week. The geopolitical backdrop is calmer, with the Israel-Iran ceasefire appearing stable for now. Trade talks seemed to be on hold, and with no major data releases on deck, markets are drifting into the second half of the week awaiting fresh signals.

Fed Chair Jerome Powell’s second day of testimony will garner attention, but few expect new revelations. His message Tuesday emphasized policy caution amid tariff uncertainty, and reiterated that inflation must remain anchored to support labor market strength. The path of interest rates remains clouded by unanswered questions on how deeply and persistently tariffs will feed into prices.

Following dovish signals from Vice Chair Bowman and Governor Waller, markets briefly speculated on a possible July rate cut. But a series of pushbacks from other Fed officials has brought expectations back to earth. The probability of a July cut has cooled to around 20%, with traders now placing 85% odds on a move in September—still contingent on upcoming data, particularly next week’s June non-farm payrolls.

Currency markets reflect this recalibration. Dollar remains weak but has edged off its lows, now the second-worst performer of the week after Loonie. Yen is not far behind as the third worst. Swiss Franc continues to lead, followed by the Pound and Kiwi. Euro and Aussie are holding in the middle of the pack.

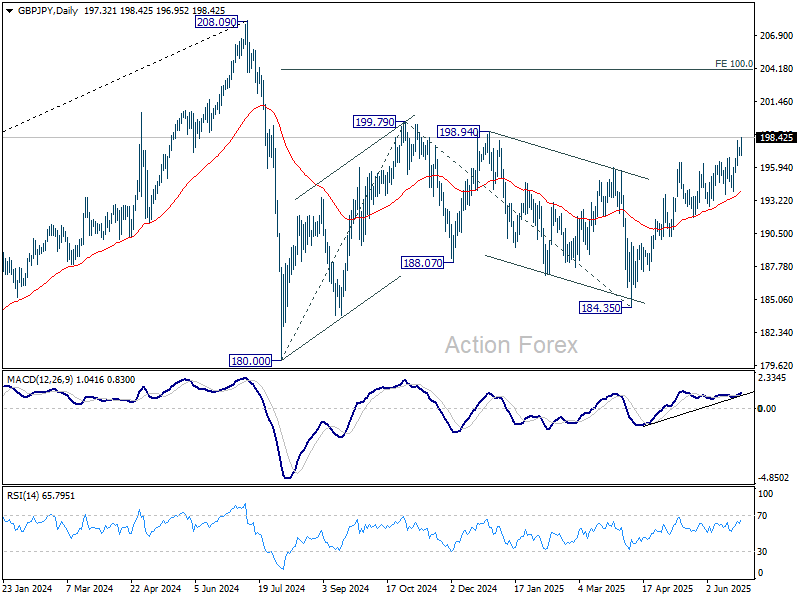

Technically, GBP/JPY's rally is advancing today. Looking a D MACD, recent rise from 184.35 is accelerating slightly. Focus now turns to 199.79 resistance. Firm break there will resume the rise from 180.00, and target 100% projection of 180.00 to 199.79 from 184.35 at 204.14.

In Europe, at the time of writing, FTSE is down -0.09%. DAX is down -0.49%. CAC is down -0.47%. UK 10-year yield is up 0.015 at 4.494. Germany 10-year yield is up 0.031 at 2.578. Earlier in Asia, Nikkei rose 0.39%. Hong Kong HSI rose 1.23%. China Shanghai SSE rose 1.04%. Singapore Strait Times rose 0.56%. Japan 10-year JGB yield fell -0.015 to 1.405.

BoJ: Split emerges over of tariffs impact and rising domestic prices

BoJ's Summary of Opinions from its June 16–17 meeting highlighted a growing divide among policymakers over the risks posed by US tariffs. While recent hard data for April and May "relatively solid", several officials warned that the real effects of the tariffs have "yet to materialize". One member emphasized the need to assess the impact carefully, as it would "certainly" weigh on business sentiment, while another described the economy as “somewhat stagnant.”

Still, the board was not unanimous in its pessimism. Some members maintained that the damage from tariffs would be limited, pointing to robust wage growth and stable consumer inflation. One member even highlighted the influence of rice prices on "perceived inflation and inflation expectations", urging close monitoring. Others noted that the domestic backdrop remains relatively firm, with wages rising and inflation slightly exceeding forecasts.

BoJ left its policy rate unchanged at 0.5% and decided to taper the pace of its bond holdings reduction more gradually starting next year.

BoJ’s Tamura: Will raise rates "without haste or delay" if outlook justifies It

BOJ board member Naoki Tamura said today that the central bank must remain prepared to adjust its policy rate “in a timely and appropriate manner” based on evolving data, even in the face of ongoing uncertainties. While real interest rates remain low, Tamura emphasized that rate hikes would be guided by evidence of sustained improvements in activity and inflation, stressing the need for being "without haste or delay".

Tamura added that uncertainty is a constant in policy-making, but that should not paralyze decision-making. If the risks to inflation shift meaningfully to the upside or the likelihood of hitting the 2% target increases, the BoJ should be ready to “act decisively.”

Australia CPI slows to 2.1% yoy in May, weakest since October 2024

Australia’s monthly CPI eased more than expected in May, dropping from 2.4% yoy to 2.1% yoy, the lowest level since October 2024 and below forecasts of 2.4% yoy.

Underlying inflation also softened, with trimmed mean CPI falling from 2.8% yoy to 2.4% yoy, reinforcing signs that underlying price pressures are easing across the economy. Excluding volatile items and holiday travel, inflation ticked down slightly to 2.7% yoy from 2.8% yoy.

The largest annual price increases came from food and non-alcoholic beverages (+2.9%), housing (+2.0%), and alcohol and tobacco (+5.9%).

The overall print strengthens the case for additional RBA rate cuts in the second half of the year, particularly as disinflation broadens.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3524; (P) 1.3586; (R1) 1.3678; More...

Intraday bias in GBP/USD stays on the upside despite today's slight retreat. Rally from 1.2099 is resuming, and should target 100% projection of 1.2099 to 1.3206 from 1.3138 at 1.3813. Outlook will now stay bullish as long as 1.3369 support holds, even in case of deeper pullback.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.2948) holds, even in case of deep pullback.