Sample Category Title

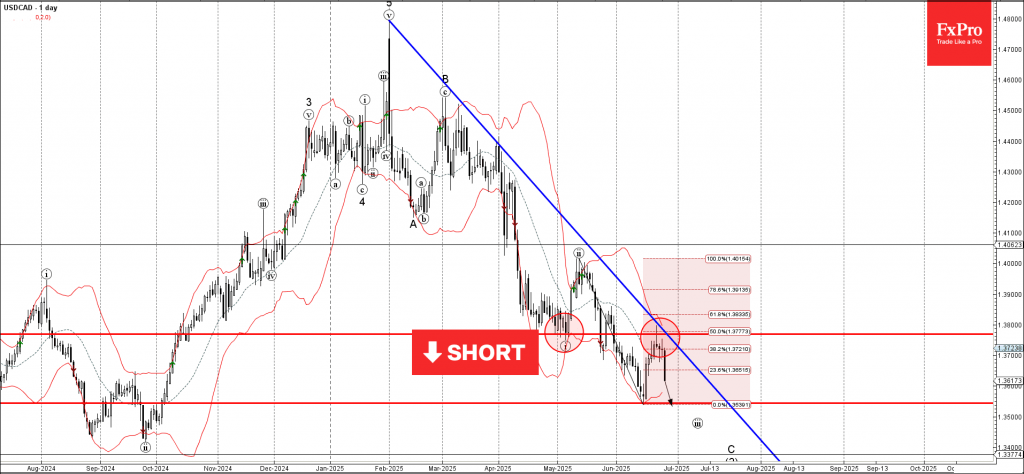

USDCAD Wave Analysis

USDCAD: ⬇️ Sell

- USDCAD reversed from the resistance zone

- Likely to fall to support level 1.3545

USDCAD currency pair recently reversed down from the resistance zone between the resistance level 1.3770 (former support from the start of May), upper daily Bollinger Band and the 50% Fibonacci correction of the downward impulse from last October.

This resistance zone was further strengthened by the resistance trendline from the start of February.

USDCAD currency pair can be expected to fall to the next support level 1.3545, which reversed the price in the middle of June.

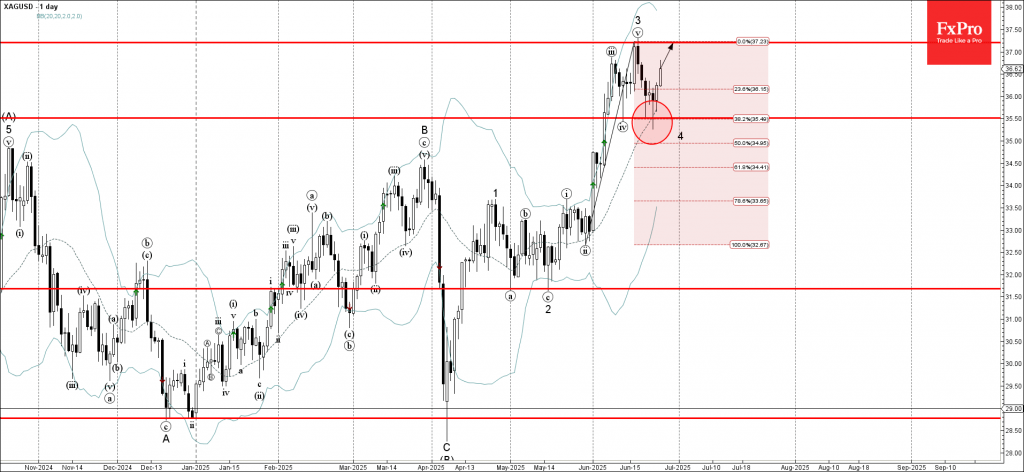

Silver Wave Analysis

Silver: ⬆️ Buy

- Silver reversed from key support level 35.50

- Likely to rise to resistance level 37.20

Silver recently reversed up from the key support level 35.50 (which stopped the previous minor correction iv at the start of June, as can be seen from the daily Silver chart below).

The support zone near the support level 35.50 was strengthened by the 20-day moving average and by the 38.2% Fibonacci correction of the sharp upward impulse from May.

Silver can be expected to rise to the next resistance level 37.20, which stopped the previous sharp impulse wave 3.

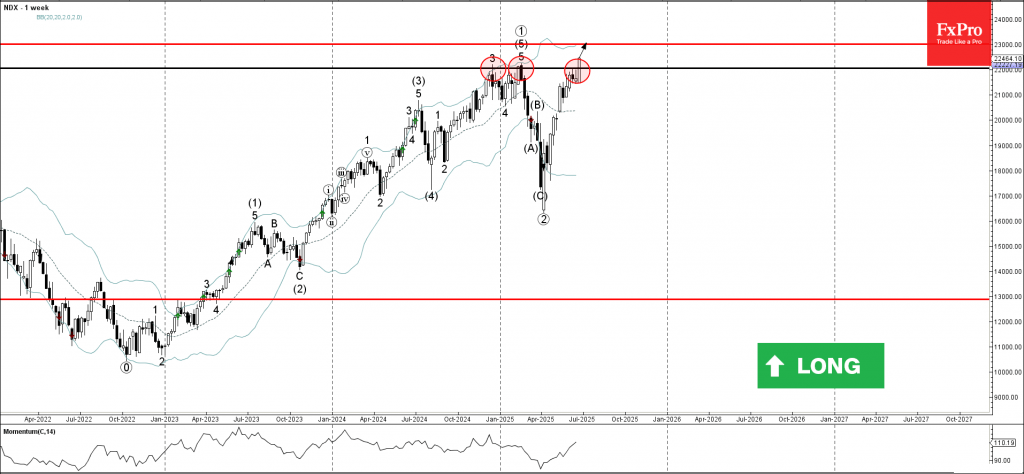

Nasdaq-100 Wave Analysis

Nasdaq-100: ⬆️ Buy

- Nasdaq-100 broke major resistance level 22100.00

- Likely to rise to resistance level 23000.00

Nasdaq-100 index recently broke above the major resistance level 22100.00 (which has been steadily reversing the index from the end of 2024 as can be seen from the weekly NDX chart below).

The breakout of the resistance level 22100.00 continues the active primary impulse wave 3 from the middle of 2025.

With the accelerating weekly momentum, Nasdaq-100 index can be expected to rise to the next resistance level 23000.00.

Fed’s Daly sticks to fall cut view, says policy in good place

San Francisco Fed President Mary Daly reiterated her long-standing view that the central bank could begin easing policy in the fall, telling Bloomberg TV, “My modal outlook has been for some time that we would begin to be able to adjust the rates in the fall, and I haven’t really changed that view.”

She added that current policy is in a “good place,” signaling comfort with Fed’s patient stance. Daly also noted that while the labor market is showing signs of cooling, it has not deteriorated enough to warrant immediate action.

Fed’s Barkin: Inflation pressure likely to rise, no urgency to cut

Richmond Fed President Thomas Barkin warned that tariff-driven inflation pressure is likely to intensify, even if its effects have been modest so far. “I do believe we will see pressure on prices,” Barkin said in a speech today, adding that while past tariff increases had only limited impact on measured inflation, “more pressure is coming.”

Barkin also signaled no urgency to adjust policy, saying the economy’s strength gives the Fed room to remain patient. “We have time to track developments patiently and allow the visibility to improve,” he said. “When it does, we are well positioned to address whatever the economy will require.”

Sunset Market Commentary

Markets

Bull steepening is name of the game this week in the US. From Friday’s close, yield changes currently range between -6.5 bps (30-yr) and -17 bps (2-yr). The outperformance at the front end of the curve is driven by a slew of disappointing US eco data, a subtle change of tone in Fed Chair Powell’s House testimony after some monetary doves already ruffled their feathers and the latest rant of US President Trump against that same Fed chair. To be clear: official Fed rhetoric still strictly focuses on fighting (upside) inflation (risks) by means of an unaltered policy rate (4.25%-4.5%) in restrictive territory. Fed Chair Powell at the press conference indicated that we’ll know a lot more over summer. For the first time he emphasized cutting policy rates sooner rather than later in case of a weakening of the US labour market or if inflation risks don’t materialize. By doing so, he starts creating room for maneuvering by the September Fed meeting. SF Fed Daly today also suggested that fall looks promising for a rate cut. Given the policy space left above neutral (3%) and with the Fed’s daring 50 bps opening rate cut last September in mind, we believe the US central bank might use a stealth normalization strategy once it is confident that the ultimate tariff level won’t significantly and structurally raise inflation (expectations). The set-up implies asymmetric risks going into next week’s ISM surveys, ADP employment change and payrolls with markets especially attentive to downside risks. Looking at the technical chart of the 2-yr yield, we see more downward potential in coming months in first instance towards 3.5% (low 2023/2024/2025) but likely even towards the 3%-zone. The relative loss of interest rate support adds to the long list of USD-negative factors. The US currency today touched multiyear lows against some majors after president Trump openly played with the idea of rapidly nominating Powell’s successor turning the current Fed chair into yesterday’s man: EUR/USD 1.1744, GBP/USD 1.3765, DXY 97. The greenback remains in a sell-on-uptickspattern. Apart from the data and Fed positioning, near term risks include the passage of Trump’s big beautiful, deficit-enlarging bill.

News & Views

The Swedish National Institute of Economic Research published its June Economic Tendency indicator. It declined from 94.5 to 92.8, which the NIER labels as weaker than usual. On the business activity side, sentiment softened across all sectors. Manufacturing confidence declined only marginally and stays close to the historical average, but pricing plans fell notably. While declining, construction sentiment signals a ‘normally strong mood’. The decline in the trade sector was one of the largest ever recorded, signaling a weak mood. Confidence in the services sector also declined, reaching the lowest level since February 2024. Consumer confidence rose slightly but remains at a low level. This weak Tendency Survey comes as the Minutes of the June Riksbank meeting yesterday showed ample support for the 25 bps cut to 2% on June 19. There was also broad support to at least keep the option open for further easing later this year as several MPC members acknowledged downside risks to growth that might warrant some policy support while (underlying) inflationary pressures are seen easing. Money markets almost fully discount an additional cut in H2. The krone declined after the last week’s decision with EUR/SEK holding above 11 (11.07).

The June retail sales measure of the Confederation of British industry was very poor. June sales declined sharply this month with the reported balance at -46% from -27% in May. This marked the ninth month in a row of declining volumes and retailers expect sales to fall further in July (-49%). Sales volumes for the time of year were judged to be “poor” to a greater extent than in May (-37% from -19%).Retail orders placed upon suppliers (-51 from -41) in the year to June declined at the fastest pace since December 2023 and retailers expect orders to fall at a similar pace next month. At the same time, retail stock volumes rose in relation to expected demand (+26% from +12%; long-run average of +17%) and are set to remain elevated in July (+27%). Wholesale sales declined at a slower pace in the year to June (-34) but are expected to fall again next month (-39%). The UK curve steepens further today. Sterling declines only marginally against the euro (EUR/GBP 0.8534). Cable even tests the strongest level against a weak dollar since October 2021 (GBP 1.372).

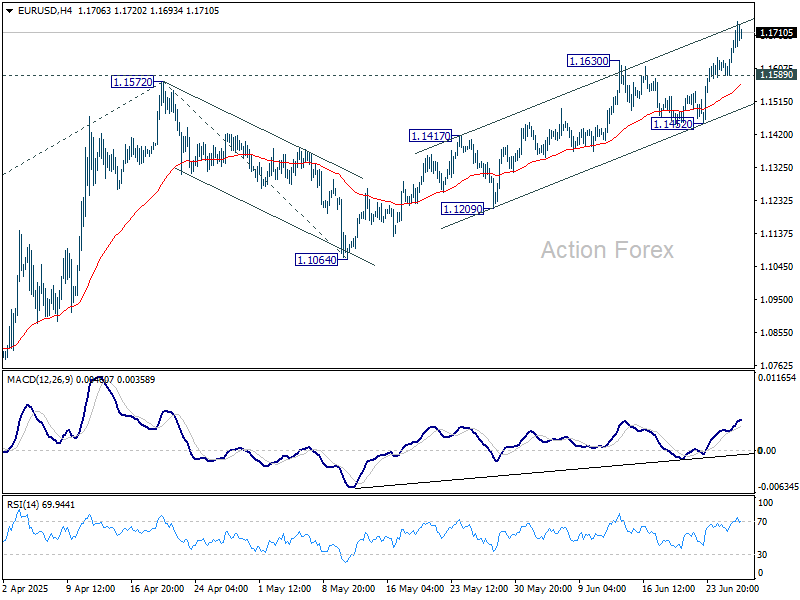

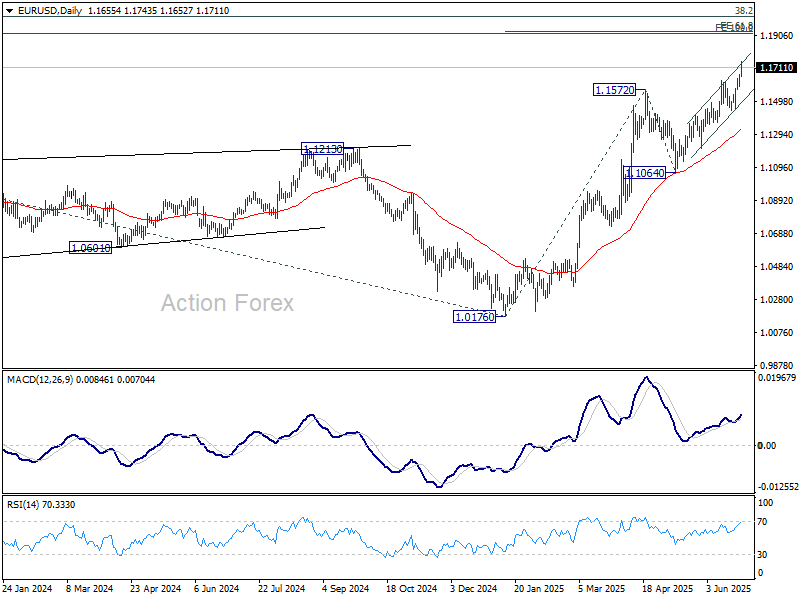

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1612; (P) 1.1638; (R1) 1.1687; More...

Intraday bias in EUR/USD remains on the upside, and current rally should target 61.8% projection of 1.0176 to 1.1572 from 1.1064 at 1.1927. Below 1.1589 minor support will turn intraday bias neutral and bring consolidations. But downside should be contained above 1.1452 support to bring another rally.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 1.1604 support holds.

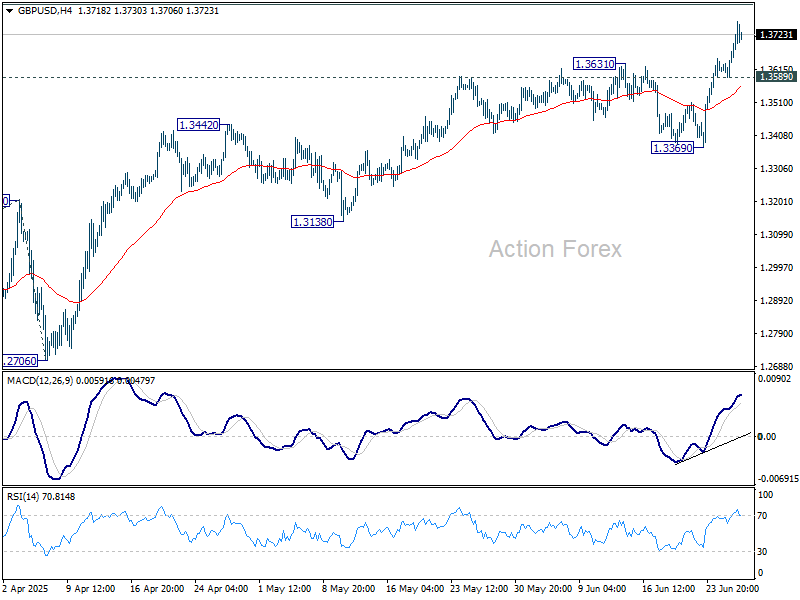

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3613; (P) 1.3642; (R1) 1.3694; More...

Intraday bias in GBP/USD remains on the upside, and current rally should target 100% projection of 1.2099 to 1.3206 from 1.3138 at 1.3813 next. On the downside, below 1.3589 minor support will turn intraday bias neutral and bring consolidations. But downside should be contained above 1.3369 support to bring another rally.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.2948) holds, even in case of deep pullback.

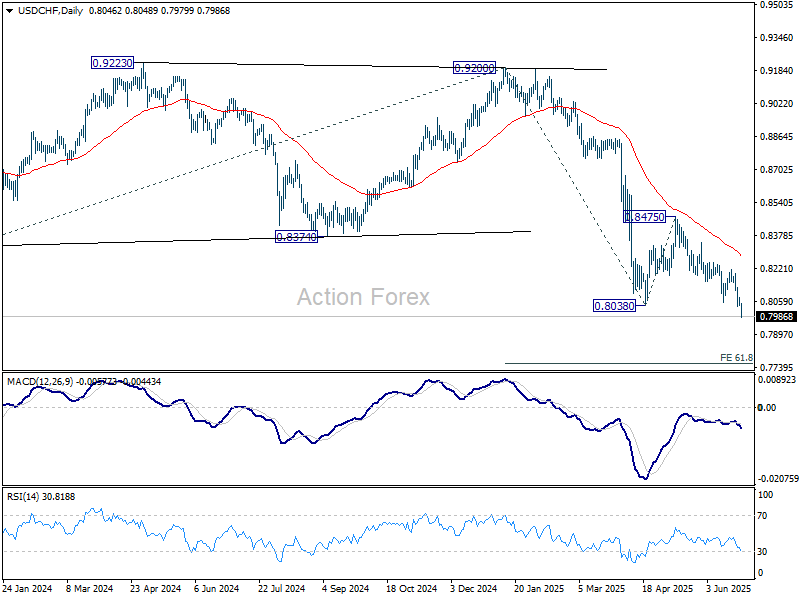

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8032; (P) 0.8056; (R1) 0.8073; More….

USD/CHF's down trend continues today and intraday bias stays on the downside for 61.8% projection of 0.9200 to 0.8038 from 0.8475 at 0.7757 next. On the upside, above 0.8079 minor resistance will turn intraday bias neutral and bring consolidations. But recovery should be limited below 0.8214 resistance to bring another fall.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8475 resistance holds.