Sample Category Title

US-China Trade Truce: A Genuine Breakthrough or a False Hope?

- US and China agree to lower tariffs for 90 days as tensions take toll.

- But what are the prospects for a permanent deal?

- Markets are unsure if this is a true turning point.

Boiling point

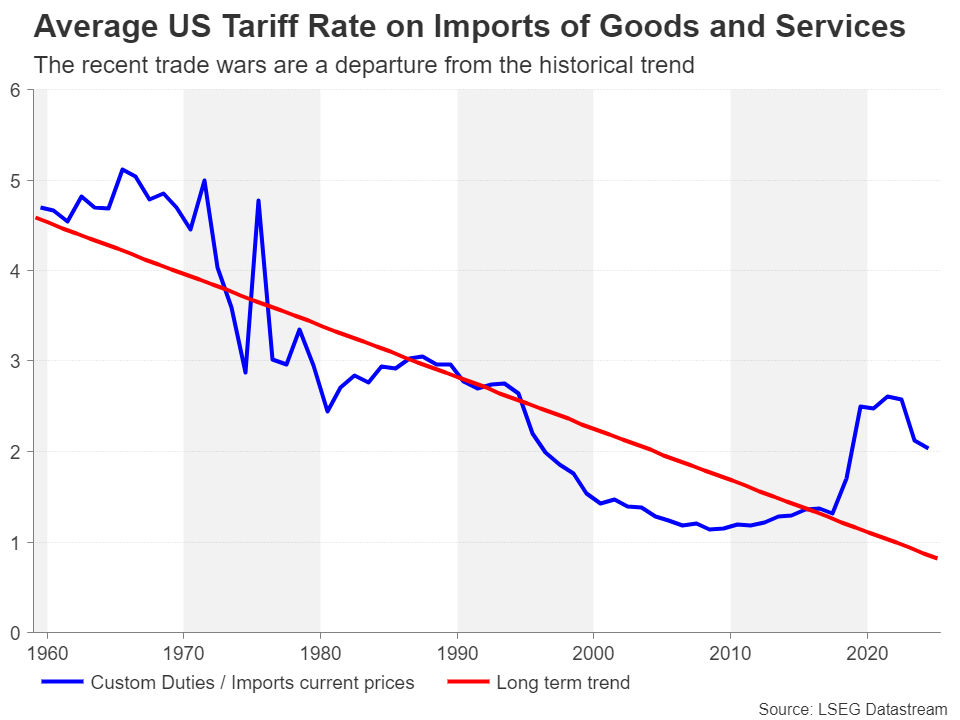

The trade war between the United States and the rest of the world reached a boiling point in April after President Trump unveiled reciprocal tariffs that were far greater than what anyone was expecting and as he flagged a new round of sectoral tariffs. The response by other countries varied, with many, like Australia, Japan and the United Kingdom, deciding not to retaliate. But others, such as the European Union and China, have not held back in responding with some counter measures.

China’s response has been the most aggressive, likely taking the White House by surprise. As expected, though, the tit-for-tat retaliation only infuriated Trump, escalating into a full-blown trade conflict. Prior to the weekend talks between US and Chinese officials aimed at diffusing the situation, Chinese businesses were staring at a staggering 145% tax on their exports to the US, while American imports were being charged a somewhat lower 125% rate.

Stepping back from the brink

All this suggests that a truce was inevitable. Reports on who initiated the talks vary, depending on the source. But most likely, both sides were seeking an urgent de-escalation, as such punitive tariffs can only be harmful to the world’s two largest economies. Hopes were high heading into the weekend meetings in Switzerland as Trump had hinted that he was willing to lower tariffs on China to 80%.

In a huge relief for investors, the outcome was far better than expected, as both sides agreed to slash each other’s tariffs by 115%, bringing the rate on Chinese imports to 30% and the rate on US goods entering China to 10%. Not forgetting the sectoral tariffs on steel and cars, this leaves the average level of levies between the two countries still above what it was prior to the start of the trade war in February.

No end to the uncertainty

More concerning for investors and other decision makers, especially business leaders and central bank policymakers, is that the temporary reprieve does little in removing the uncertainty. Reaching an initial trade deal was probably the easy part. Agreeing on a comprehensive trade pact that resolves differences on key areas such as intellectual property rights, the illegal flow of fentanyl and US access to Chinese markets will be much more difficult.

This leaves markets exposed and vulnerable to any potential setbacks during the 90-day pause, while failure to reach a more permanent agreement risks reviving fears about a US and global recession.

Dollar perks up

The easing trade tensions have helped the US dollar recover significant lost ground. The dollar index surged towards its 50-day moving average (MA) the day after the Sino-US deal was announced, extending its rebound from April’s three-year low of 97.92 to more than 4%. However, the 50-day MA has proven to be a tough obstacle to overcome, and the greenback has since retreated somewhat, casting doubt about its outlook even if trade frictions continue to de-escalate.

Inflation risks persist

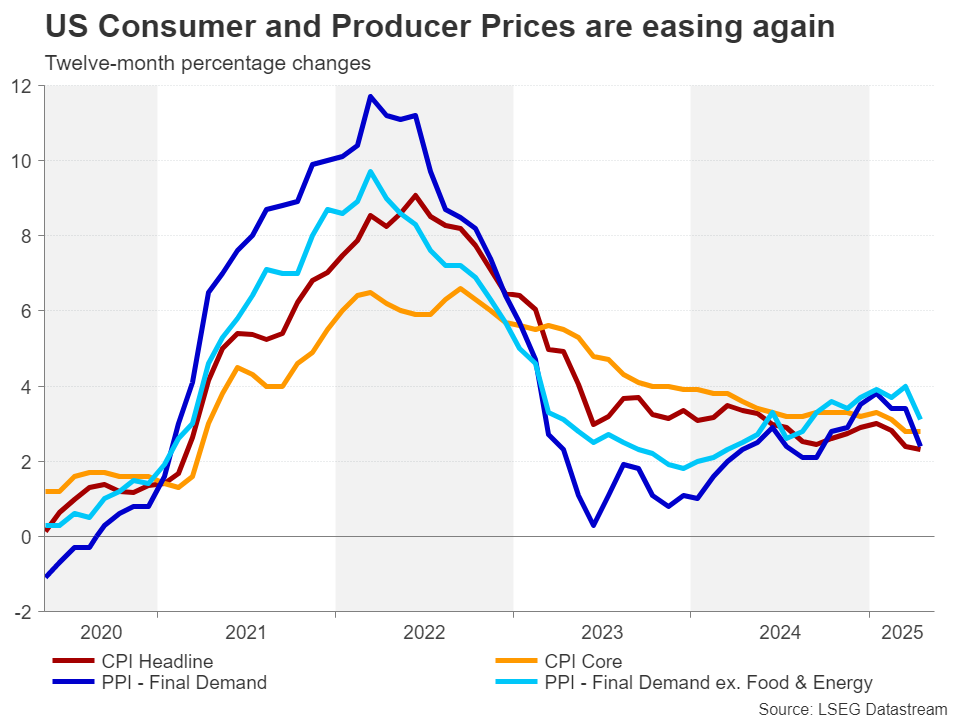

Apart from the ongoing risk that Trump could re-impose some of the suspended tariffs at any point, there is also huge uncertainty about what will happen to inflation. For now, US inflation appears to be gradually declining, putting the Fed in a strong position to resume its rate cuts at some point in the second half of the year.

However, the Trump administration has repeatedly indicated that the 10% baseline tariffs that were introduced on April 2 are here to stay. The 25% duties on specific sectors are also not likely to be abolished completely, even if there are some further exemptions in the future. Plus, tariffs on additional industries are possible.

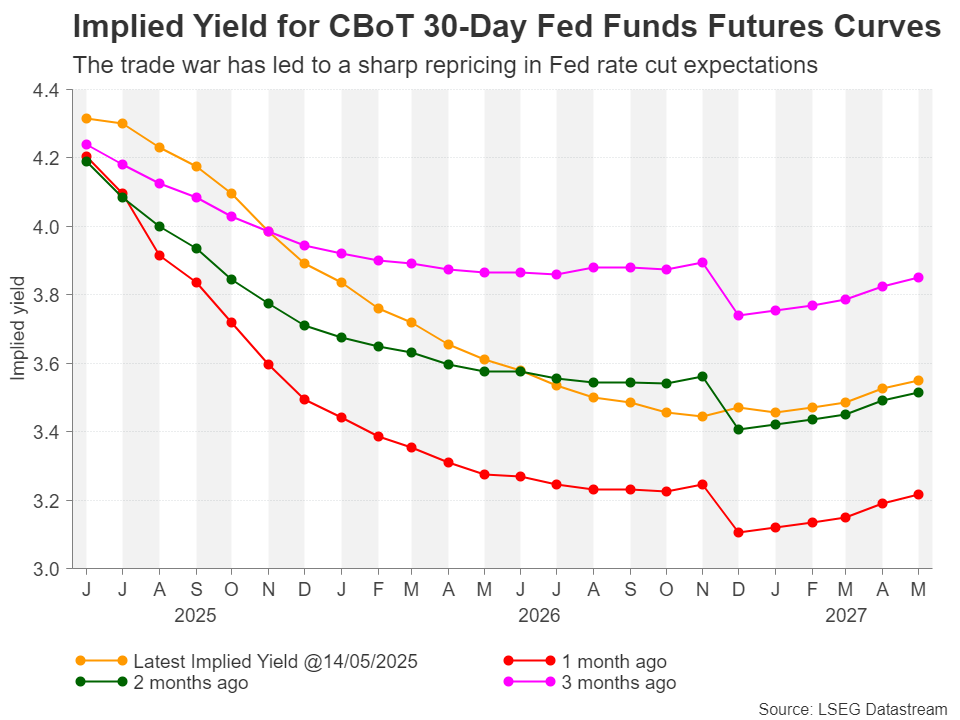

This makes it difficult for the Fed to feel confident about inflation maintaining its current downward path as there’s bound to be some impact from the higher tariffs on US prices even in the best cast scenario. Investors currently foresee just two rate cuts this year, with a full 25-basis-point reduction not fully priced in until September.

Fed still faces a dilemma

A long pause seems more justifiable now that exorbitant tariff levels have been scaled back and no longer pose a threat to the economy. But then why is the dollar’s rebound looking shaky?

It’s likely that investors still see a significant risk of stagflation, as the uncertainty about Trump’s policies will probably hold back business and consumer spending to some extent, suppressing growth while costs go up. It’s also the case that the supply chain landscape will go through an inevitable transformation, as many businesses will be forced either way to shift some or all of their production to the US, pushing up costs.

A China deal may not be easy

Investors should not be fooled into thinking that America’s quest to decouple from China will stop when Washington and Beijing finalise their deal, which itself may not bring an end to the broader economic war.

One reason why Trump is coming down hard on China in his second term is because of the failure of the Phase I agreement signed in January 2020 during his first term. The Chinese did not live up to their commitment of buying more US goods, so the White House will be wary not to repeat the same mistake and will seek better safeguards for enforcement of the deal.

Hence, the stakes are a lot higher this time, meaning a resolution of the trade dispute may take a lot longer than anticipated. This explains why many investors are maintaining a substantial degree of caution until there is a more convincing breakthrough in the negotiations.

Reason for optimism

Nevertheless, some optimism in the short term is warranted, as all the signs suggest the Trump administration wants to avoid another stock market meltdown and is determined to get more preliminary deals across the finish line. It’s also highly likely that the existing 90-day delays on reciprocal tariffs will be extended, while the evidence from the latest announcements on the chip and pharmaceutical sectors is that the White House is toning down its stance amid outcry from industry leaders.

For the dollar, a break above the 50-day MA is vital if the recovery is to gain any traction, with the next critical barrier likely to be found around 103.35, followed by the 200-day MA. Though, the 200-day may be too bullish a target at the moment as downside risks persist.

Doubts about Dollar’s reserve currency status

Trump’s constant flip-flopping on trade and undermining of America's democratic institutions is harming the dollar’s position as the world’s reserve currency. This may limit the dollar’s advances even if there is a further cooling in trade tensions.

But in the event that there is a re-escalation in the trade war and Fed rate cut expectations are ratcheted up, there is scope for the dollar index to slide all the way down to the 94.60 region towards 2021 lows.

Weekly Focus – Positive Trade Developments Spur Risk-On Sentiment

This week has been dominated by risk-on sentiment in markets following the positive outcome of the US and China trade negotiations during the weekend in Geneva. The cuts to tariff rates were larger than we and consensus had anticipated as the US announced a 115-percentage point reduction of the previous tariff rate from 145% to 30%. Adding the 10% universal tariff rate Chinese goods are now faced with a 40% tariff when entering the US compared to around 10% before Trump took office. We estimate there is a good chance of the US cutting tariffs by an additional 20 percentage points by striking a deal on the Fentanyl issue. Following the announcement, the risk of a recession in the US has been significantly reduced and we estimate that growth will likely experience a hit of around 0.5 percentage points which is manageable. For more details, see US-China Flash - Trade talks succeed in de-escalation, 12 May, and join our webinar on 21 May.

On the data front, we received a host of data this week from the US. Inflation data for April surprised slightly to the downside as headline inflation declined to 2.3% y/y (cons: 2.4% y/y) from 2.4% y/y and core inflation remained at 2.8% y/y, as expected. There was little evidence of tariff-driven price pressures, as core goods inflation remained slow (+0.06% m/m) and food prices even declined slightly (-0.08% m/m). Interestingly, core services inflation excluding shelter and healthcare remained negative for the second consecutive month (-0.02% m/m), which suggests that underlying price pressures have remained in check despite the trade war - a conclusion that was also supported by the April PPI data. The trade war does not seem to have caused US consumers to be significantly more cautious when evaluating the latest retail sales data for April. Retail sales recorded a small monthly decline in the control group due to weaker spending on clothing and electronics, while spending on restaurants and bars continue growing at a solid pace. We think the weak retail sales figure might reflect reversal of front-loading effects more than true underlying weakness.

In the euro area, data showed that employment continued to grow in the first quarter of the year, rising 0.3% q/q after growing 0.1% q/q in Q4 2024. Hence, the labour market continues the strong footing it has been on in the past years despite weak economic activity. Employment growth was once again driven by Spain that recorded 0.8% q/q higher employment while both France and Germany reported unchanged employment in Q1. The strong labour market is a hawkish argument for the ECB. In Germany, the final inflation data for April showed that much of the increase in core inflation was due to the timing of Easter pushing up costs for package holidays and airfares, which suggests the increase in April should be seen more as a one-off than a resurgence of price pressures in core services.

Next week, focus turns to the May PMI data for the US and euro area, which will be interesting to follow as they previously have remained stronger than feared amid the trade war uncertainty. On Monday, China releases a large batch of data for April, which will show the impact of the peak escalation of trade tensions, and the central bank announces its interest rate decision, and so does the Australian central bank. In Japan, we will receive inflation data on Thursday, and in the euro area we focus on the negotiated wage growth data for Q1 released on Friday and the EU Commission's economic forecasts on Monday.

Cliff Notes: The Promise of Detail

Key insights from the week that was.

In Australia, Westpac-MI Consumer Sentiment rose 2.2% to 92.1% in May, representing a partial rebound from a subdued result in April that partly captured President Trump’s ‘Liberation Day’. There have been many developments on the global trade front since – especially the latest de-escalation between the US and China which came just after our latest survey – which, combined with the calm attitude of financial markets, have supported sentiment. This was clearly captured in views on ‘family finances vs a year ago’ which rebounded +7.0% and, to a lesser extent, the year-ahead outlook for economic conditions, up +2.8%.

Consumers are accordingly less downbeat on whether it is ‘time to buy a major household item’, up +3.5%; however, that the sub-index remains 25% below its long-run average emphasises the weak starting point for the nascent recovery in consumer spending after a prolonged period of real income declines over 2023/24. On that front, the latest wages data struck a more positive tone for households, with the wage price index rising 0.9% (3.4%yr) in Q1. This was slightly firmer than expected and came as a result of wage increases delivered to aged care and childcare workers.

Households also remain positive on the labour market outlook, a view that was certainly given justification by the latest labour force survey. Following a couple of months of softer outcomes, employment surprised materially to the upside with an +89k surge. This also came alongside a significant rebound in the labour force, seeing the employment-to-population ratio and participation rate bounce back toward their historic highs. Meanwhile, the unemployment rate was little changed at its current year-average of 4.1%. Broadly, labour demand and supply still look to be moving broadly in tandem, allowing measures of labour market slack to hold steady.

Overall, this week’s data does not change our view that the RBA will deliver a 25bp rate cut at its policy meeting next week, but it will be interesting to see refreshed staff forecasts and the Board’s framing of risks around the domestic and global outlook. We note that the latest NAB business survey highlighted businesses were broadly unphased by the US’ tariff uproar, supporting the view that Australia remains well placed to weather this period of global uncertainty. And, as far as the latest US-China trade deal is concerned, this week’s essay from Chief Economist Luci Ellis discusses the implications in more depth.

Offshore, investors were focussed on the short-term trade deal agreed between the US and China. Tariffs imposed on Chinese exports were reduced to 30% (combining a 10% reciprocal rate and 20% tariff for fentanyl supply), while China will tariff US goods by 10%. These rates will be in place for 90 days from 12 May during which time the leaders of both countries will seek to negotiate a more permanent trade agreement. Industry tariffs also remain in effect for Chinese imports to the US, as is the case for other nations.

On the data front, the US CPI printed below expectations at 2.3%yr in April, the lowest rate since February 2021. Annual core inflation held steady at 2.8%. The detail of the April report was mixed, food prices edging higher as energy posted a partial rebound (a 0.7% gain after March’s 2.4% decline). Within the core basket, goods prices edged higher again (up 0.1% in the month and over the year). Services inflation meanwhile remained robust at 0.3%, 3.6%yr (ex energy). Shelter inflation (primarily rents) continues to track materially above average, a consequence of limited supply; but medical care services also saw an outsized gain 0.5% compared to its current annual pace of 3.1%yr. Overall, ahead of the impact of tariffs, the baseline for inflation in the US looks to have been inflation modestly above target, primarily as a result of constrained supply. This is not a trend that the FOMC can easily influence; but, as tariffs also impact, it will give the FOMC cause to be cautious over inflation expectations and risks.

FOMC members who spoke this week certainly supported a ‘wait and see’ approach to monetary policy. Although, it has to be noted, they are assessing the labour market as closely as inflation. We maintain our call for two rate cuts towards the end of 2025 and an on-hold stance through 2026 while awaiting a clearer read on the net effect of US domestic and trade policy.

In the UK meanwhile, the latest labour market data gave justification for the Bank of England to continue to ease through 2025. The three-month average pace of employment growth slowed to 112k in March, down from 206k in February; and the unemployment rate edged up from 4.4% to 4.5%. Annual growth in average weekly earnings decelerated from a revised 5.9%yr ex-bonus to 5.6%yr (3-month average basis). This deceleration in wages aligns with other survey indicators which indicate wage growth is unlikely to be a source of inflationary pressure over the coming year.

While there may be greater concern over US growth these days, for both the UK and Euro Area, the outlook is becoming brighter. UK GDP growth was strong as expected in Q1, gaining 0.7%, 1.3%yr. This is despite soft private consumption (0.2%) and a contraction in government spending (-0.5%), more than offset by a surge in business investment (2.9%) as export growth outpaced imports (3.5% versus 2.1%). The second release for Q1 Euro Area growth confirmed robust moment, quarterly growth edged down from 0.4% to 0.3% but the annual rate unchanged at 1.2%yr – around trend.

The balance of growth prospects between the US, UK, Europe and, further afield, Asia will have a material bearing on the outlook for financial markets. Current trends point to persistent downward pressure on the US dollar, as discussed recently in our May Market Outlook.

Sunset Market Commentary

Markets

“Time to go back home”. US President Trump wrapped up his road trip through the Middle-East, sealing substantial business and defense contracts with Saudi Arabia, Qatar and the United Arab Emirates. Those agreements cover slightly over €1tn with (Qatari) plans to significantly increase them further. The investment deals helped lift spirits on (US) equity markets this week (perhaps also as his busy schedule kept him away from social media) with main indices on track to record a fourth consecutive weekly gain and pushing them above levels on the eve of “Liberation Day”. During his trip, Trump lauded his Secretary Treasury Bessent and his prominent role in trade talks. “When Bessent talks, markets listen”. They do not only listen, but also tend to rally unlike when trade czar Navarro or Commerce Secretary Lutnick enter the scene. Bessent’s Geneva talks with Chinese vice-premier He Lifeng led to a 90-day truce in the Sino-US trade war and kickstarted this week’s rally. The US trade team remains focused on Asian countries, but the likes of Japan indicated they aim for a good rather than a fast deal. People close to talks indicate that Japan targets a complete removal of tariffs on the key car sector, rather than falling back to Trump’s floor rate of 10%. Lacking the manpower and capacity to hold talks with all countries involved in the reciprocal tariff plan during the current 90-day pause, Trump said that other trading partners over the next two to three weeks will get letters to inform them of the tariffs they will pay to do business in the US. Ongoing discussions with the likes of South Korea and Japan also cover FX policy. The US believes that appreciating currencies from trading partners are part of the solution to shrink the trade deficit on the US goods balance. By stressing this part of the equation, the dollar’s recovery already showed signs of fatigue this week. Recent trade developments significantly reduced the tail risk of a severe global growth slowdown and a US recession. It put the fiscal story back on investors’ radar as the US House is wrapping up its Reconciliation Bill. Trump hopes to see that on his desk by Independence Day, in time to raise the US debt ceiling and in time to extend tax cuts from his first term. The US Committee for a Responsible Budget already warned for the devastating impact on public finances based on available information. They fear that the debt ratio could hit 125% or worst-case even 129% of GDP by 2034 (from 100% currently and vs baseline path of 117%). Annual budget deficits of 6.9%-7.8% would be the new standard with interest rate costs rising to up to 4.2%-4.4% of GDP by end 2034. The CFRB warning kicked in for US Treasuries with the 30-yr yield testing the psychologic 5% mark for already the third time this year. The test failed as the Big Beautiful Bill is still in its early stages of being marked up in various House Committees. The House hopes to pass it somewhere early June. That’s an eternity in Trump’s high-speed world. US eco data helped creating a more stable market setting towards the end of the week as well. Activity data point to a slowdown in the chaotic month of April, but disinflationary CPI/PPI data and improving sentiment indicators for May keep the goldilocks dream (avoiding recession and keeping disinflation on track) alive for now. Next week’s eco calendar is light on data with May global PMI’s (Thursday) and EMU Q1 wage growth numbers (Friday) exception to the rule.

News & Views

The Central Bank of Romania (CBR) kept its policy rate unchanged at 6.5%. The decision came in a context of elevated political uncertainty that caused the CB to allow the leu to depreciate within its managed floating regime before stabilizing it via interventions at a weaker level (EUR/RON 5.1055 currently). This leu weakening might complicate the disinflation process. In its policy statement, the CBR assessed that inflation in Q1 declined less than anticipated to 4.86% in March from (5.14% in December) as decreases of fuel and tobacco prices, alongside non-food sub-components of core inflation, were partly countered by the swifter increase in energy prices, administered prices and processed food prices. Details of a new inflation report will be published on Tuesday. The CBR indicates that Y/Y inflation will fluctuate until 2025 Q3. It is expected to decrease later but on a significantly higher path than in the previous forecast, falling no sooner than in 2026 Q1 and only to marginally below the upper bound of the target band (1.5%-3.5%). On Sunday a second round of the presidential election takes place between far right candidate George Simion who won the first round and the Mayor of Bucharest, Nicusor Bank, who has a more centrist profile.

US UoM consumer sentiment falls to 50.8, inflation expectations surges to 7.3%

US consumer sentiment deteriorated again in early May, with University of Michigan’s index falling from 52.2 to 50.8, its lowest level since mid-2022 and well below expectations of 53.0.

The decline was broad-based, with Current Economic Conditions Index slipping from 59.8 to 57.6 and Expectations Index easing from 47.3 to 46.5. Since the start of 2025, overall sentiment has plunged nearly 30%.

The report also highlighted a surge in inflation fears, with year-ahead inflation expectations jumping from 6.5% to 7.3%.

According to the survey, nearly three-quarters of respondents spontaneously mentioned tariffs, a notable increase from April’s 60%.

Interviews for the survey were conducted between April 22 and May 13, capturing only limited responses after the May 12 announcement of a partial tariff pause on Chinese goods. The final May release may reveal whether that move tempers consumer concerns.

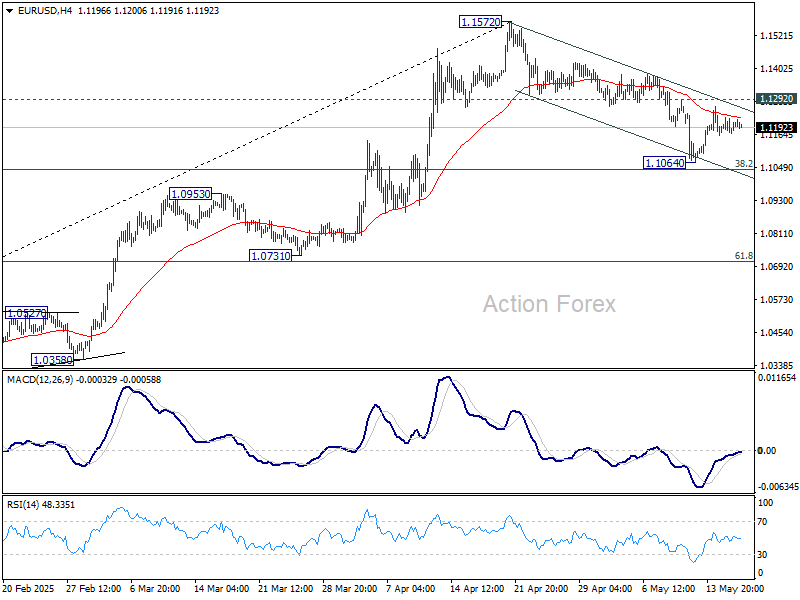

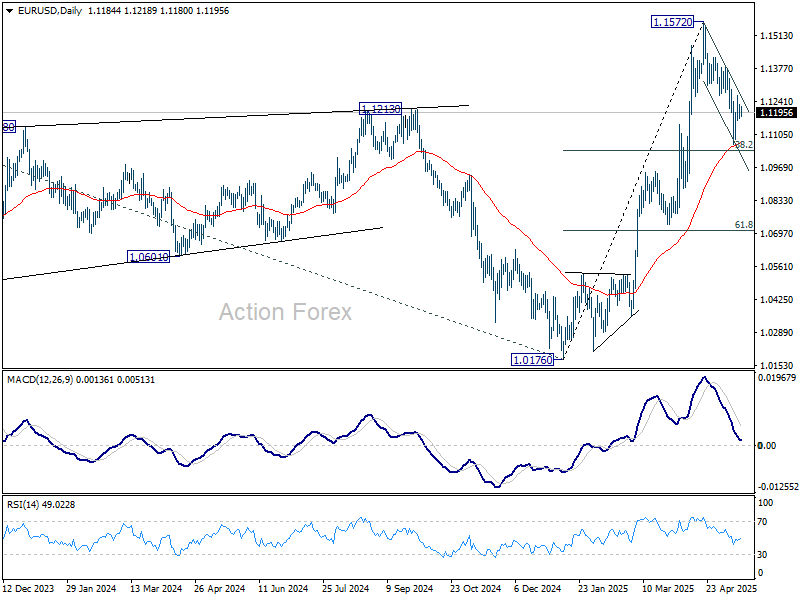

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1157; (P) 1.1192; (R1) 1.1220; More...

Intraday bias in EUR/USD remains neutral. On the upside, break of 1.1292 resistance will argue that correction from 1.1572 has completed after defending 38.2% retracement of 1.0176 to 1.1572 at 1.1039. Intraday bias will be back on the upside for retesting 1.1572. However, sustained break of 1.1039 will dampen this view and target 61.8% retracement at 1.0709 next.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0789) holds.

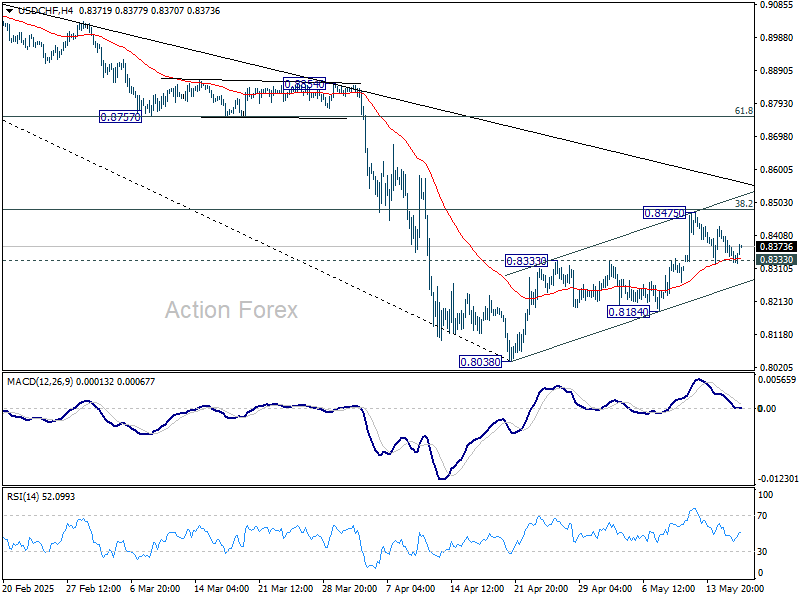

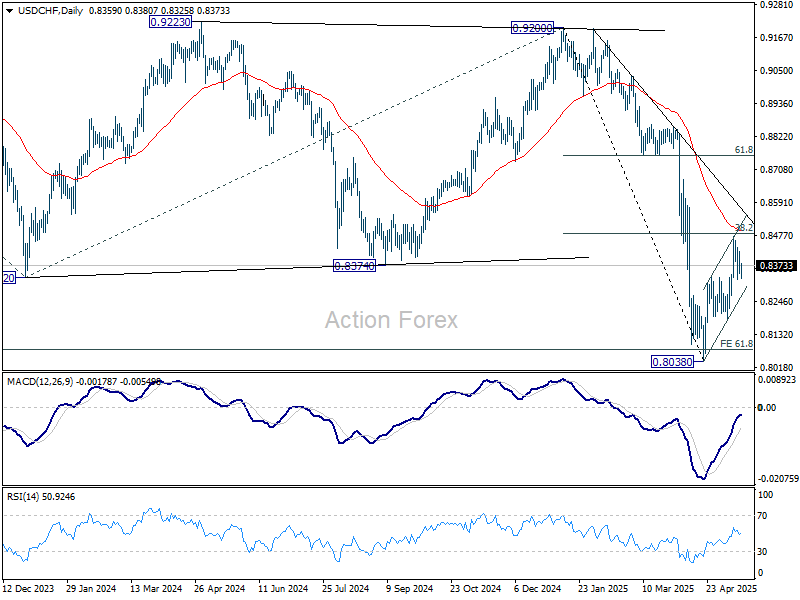

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8328; (P) 0.8377; (R1) 0.8409; More….

Intraday bias in USD/CHF stays neutral. On the downside, firm break of 0.8333 resistance turned support will argue that corrective rebound from 0.8038 has completed at 0.8475, after rejection by 38.2% retracement of 0.9200 to 0.8038 at 0.8482. Intraday bias will be back on the downside for 0.8184, and then retest of 0.8038 low. However, sustained trading above 0.8482 will dampen this bearish view and target 61.8% retracement at 0.8756 next.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress and met 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.8079 already. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8750) holds. Sustained break of 0.8079 will target 100% projection at 0.7382.

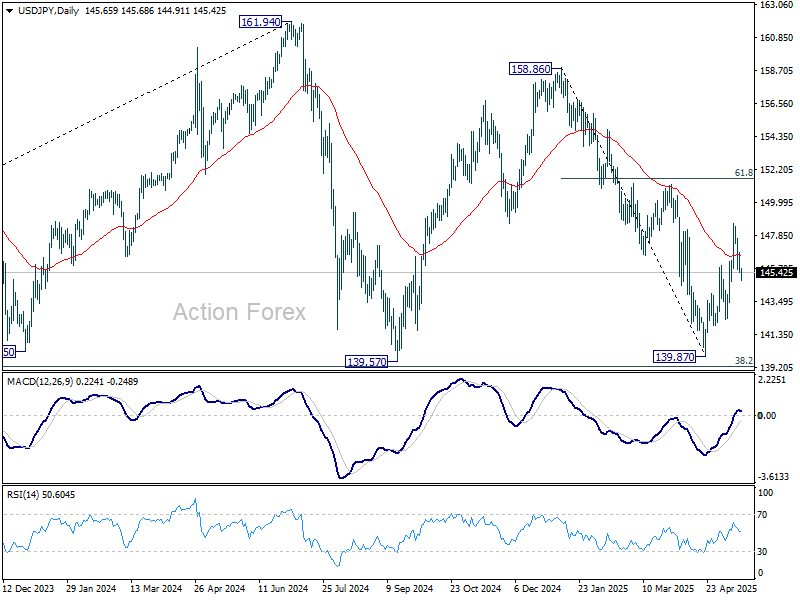

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 145.13; (P) 145.97; (R1) 146.53; More...

Intraday bias in USD/JPY stays neutral and further rally is expected as long as 144.02 resistance turned support holds. As noted before, fall from 158.86 could have completed 139.87 already. Above 148.64 will target 61.8% retracement of 158.86 to 139.87 at 151.60 next. However, firm break of 144.02 will bring retest of 139.87 low instead.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

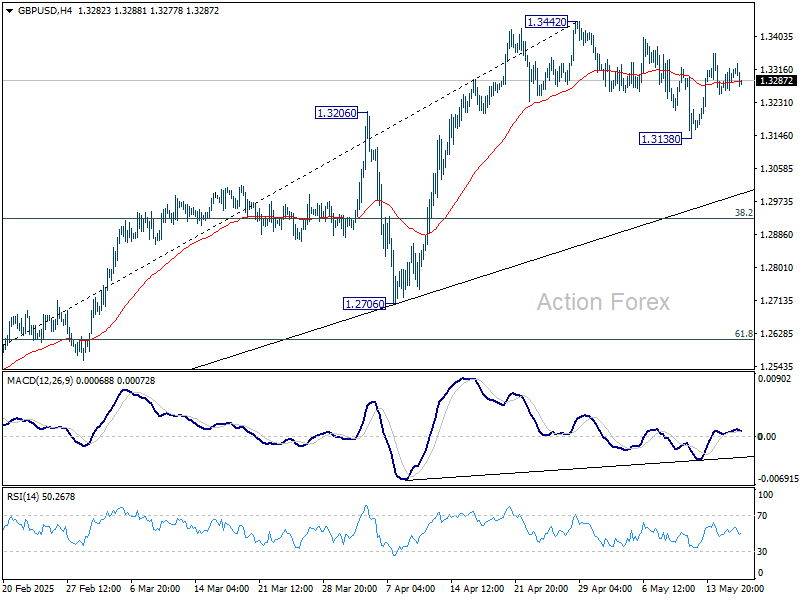

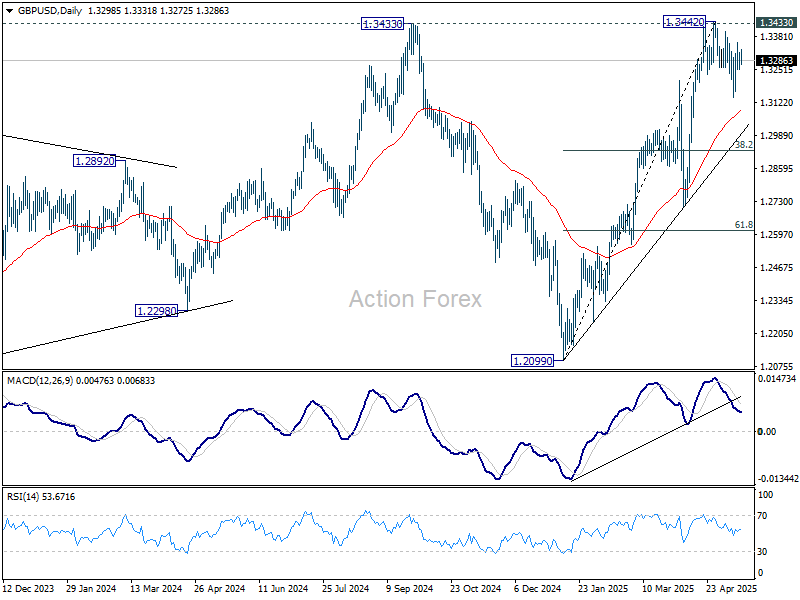

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3263; (P) 1.3292; (R1) 1.3331; More...

Intraday bias in GBP/USD remains neutral as range trading continues. On the upside, decisive break of 1.3433/42 key resistance zone will confirm larger up trend resumption. Nevertheless, below 1.3138 will resume the correction from 1.3442. But downside should be contained by 38.2% retracement of 1.2099 to 1.3442 at 1.2929 to bring rebound.

In the bigger picture, price actions from 1.3433 are seen as a corrective pattern to the up trend from 1.3051 (2022 low). Rise from 1.2099 could either be resuming the up trend, or the second leg of a consolidation pattern. Overall, GBP/USD should target 1.4248 key resistance (2021 high) on decisive break of 1.3433 at a later stage.

Markets Stuck in Ranges as Data Fail to Inspire

Market activity remains subdued ahead of the weekend, with major currency pairs and crosses locked within yesterday’s tight ranges. Earlier in the day, New Zealand Dollar received a brief lift from rise in inflation expectations, but the move lacked conviction and quickly faded. Similarly, Japan’s weaker-than-expected Q1 GDP figures failed to trigger much reaction, as traders largely shrugged off domestic data and remained directionless.

Broader risk sentiment is offering little help, with global equity markets also confined to narrow ranges. Investors are awaiting fresh cues, with some attention turning to the upcoming US University of Michigan Consumer Sentiment survey. While a bounce in sentiment is possible following the 90-day reciprocal tariff truce, lingering policy uncertainty may cap any gains. Of particular interest will be the inflation expectations component, as a notable uptick could reinforce concerns that tariffs are beginning to feed into price pressures.

For the week, Aussie is leading the pack, followed by Dollar and Sterling. On the weaker side, Swiss Franc is underperforming, trailed by Euro and Kiwi. Yen and Canadian Dollar are trading more neutrally.

In Europe, at the time of writing, FTSE is up 0.40%. DAX is up 0.45%. CAC is up 0.37%. UK 10-year yield is down -0.038 at 4.623. Germany 10-year yield is down -0.047 at 2.575. Earlier in Asia, Nikkei closed flat. Hong Kong HSI fell -0.46%. China Shanghai SSE fell -0.40%. Singapore Strait Times rose 0.15%. Japan 10-year JGB yield fell -0.024 at 1.455.

Fed’s Bostic sees only one rate cut in 2025, as uncertainty unlikely to resolve quickly

Atlanta Fed President Raphael Bostic reiterated his expectation for just one interest rate cut this year, citing persistent uncertainty surrounding global trade policy "is unlikely to resolve itself quickly.”

Speaking on Bloomberg’s Odd Lots podcast, Bostic pointed to the 90-day delay of reciprocal tariffs and the tentative nature of the recent US-China de-escalation, warning that the final outcomes of trade negotiations remain unclear.

Bostic emphasized that tariffs are expected to exert upward pressure on inflation, a view supported by the Atlanta Fed’s own analysis and echoed by many economists.

As a result, monetary policy may need to lean against those inflationary forces, limiting how far the Fed can ease. “Our policy is going to have to anticipate — and to some extent — potentially push against those inflationary forces,” he said.

EU exports jump 15.% yoy in March on strong US shipments

Eurozone trade data showed a strong performance in March, with exports rising 13.7% yoy to EUR 279.8B and imports up 8.8% yoy to EUR 243.0B, resulting in a solid trade surplus of EUR 36.8B. Intra-eurozone trade also rose 1.7% yoy to EUR 226.0B, indicating modest growth in internal demand.

For the broader European Union, the trade picture was similarly positive. Exports jumped 15.2% yoy to EUR 254.8B, while imports increased by 10.4% yoy to EUR 219.5B, yielding a EUR 35.3B surplus.

The standout development came from transatlantic trade: EU exports to the United States surged 59.5% yoy to EUR 71.4B, far outpacing the 15.8% yoy rise in imports from the U.S.

Meanwhile, trade with the UK also showed moderate growth, with exports rising 4.8% yoy and imports increasing 5.4% yoy. In contrast, trade with China as a weak spot. EU exports to China fell sharply by -10.1% yoy to EUR 17.9B, while imports surged 15.8% yoy to EUR 48.6B.

ECB’s Kazaks: Interest rates near terminal level of easing cycle

Latvian ECB Governing Council member Martins Kazaks indicated market pricing of a 25bps cut at the June 5 meeting is “relatively appropriate”.

Nevertheless, speaking to CNBC, Kazaks added that inflation developments are "by and large within the baseline scenario". Thus, ECB is “relatively close to the terminal rate” of its easing cycle.

Kazaks' comments argue that ECB may enter a phase of pause after the June rate cut.

Meanwhile, French Governing Council member Francois Villeroy de Galhau, in an interview with a regional French newspapers, acknowledged the risk of a trade war but dismissed the notion that central banks are currently engaged in a currency war.

Villeroy defined a currency war as using interest rates competitively to gain economic advantage. Instead, he said recent currency movements are more reflective of "revisions to economic forecasts."

BoJ’s Nakamura urges caution on rate hikes as economy faces mounting downward pressure

BoJ board member Toyoaki Nakamura, known for his dovish stance, warned that Japan’s economy is under “mounting downward pressure” and cautioned against "rushing" to interest rate hikes.

Speaking today, Nakamura highlighted the risks of tightening policy while growth slows, noting that higher rates could "curb consumption and investment with a lag".

Nakamura also pointed to growing uncertainty stemming from US tariff policy, which he said is already causing Japanese firms to delay or scale back capital spending plans.

He warned that escalating trade tensions could spark a “vicious cycle of lower demand and prices,” undermining both growth and inflation.

Japan’s GDP contracts -0.2% qoq in Q1, export drag offsets capex gains

Japan’s economy shrank by -0.2% qoq in Q1, marking its first contraction in a year and falling short of the -0.1% qoq consensus. On an annualized basis, GDP contracted by -0.7%, a sharp disappointment compared to expectations for -0.2%.

The weakness was largely driven by external demand, which subtracted -0.8 percentage points from growth as exports declined -0.6% qoq while imports jumped 2.9% qoq.

Domestically, the picture was mixed. Private consumption, comprising more than half of Japan’s output, was flat on the quarter. However, capital expenditure provided some support, rising by a solid 1.4% qoq.

Meanwhile, inflation pressures showed no sign of easing, with the GDP deflator accelerating from 2.9% yoy to 3.3% yoy, above expectations of 3.2% yoy.

RBNZ inflation expectations rise to 2.41%, further easing seen ahead

RBNZ’s latest Survey of Expectations for May revealed a notable uptick in inflation forecasts across all time horizons.

One-year-ahead inflation expectations climbed from 2.15% to 2.41%, while two-year expectations rose from 2.06% to 2.29%. Even long-term projections edged higher, with five- and ten-year-ahead expectations increasing to 2.18% and 2.15% respectively.

Despite the upward revisions in inflation outlook, expectations for monetary policy point clearly toward easing.

With the Official Cash Rate currently at 3.50%, most respondents anticipate a 25 bps cut by the end of Q2. Looking further ahead, the one-year-ahead OCR expectation also declined from 3.23% to 2.91%.

NZ BNZ manufacturing rises to 53.9, recovery gains ground

New Zealand’s BusinessNZ Performance of Manufacturing Index edged up from 53.2 to 53.9 in April. The gain was driven by improvements in employment and new orders, up to 55.0 and 51.4 respectively, with employment reaching its highest level since July 2021. However, production eased slightly to 53.8.

BNZ Senior Economist Doug Steel noted that while the sector isn’t booming, the recovery is clear, with the PMI rebounding sharply from a low of 41.4 last June.

Still, he cautioned, "there remain questions around how sustainable it is given uncertainty stemming from offshore”.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3263; (P) 1.3292; (R1) 1.3331; More...

Intraday bias in GBP/USD remains neutral as range trading continues. On the upside, decisive break of 1.3433/42 key resistance zone will confirm larger up trend resumption. Nevertheless, below 1.3138 will resume the correction from 1.3442. But downside should be contained by 38.2% retracement of 1.2099 to 1.3442 at 1.2929 to bring rebound.

In the bigger picture, price actions from 1.3433 are seen as a corrective pattern to the up trend from 1.3051 (2022 low). Rise from 1.2099 could either be resuming the up trend, or the second leg of a consolidation pattern. Overall, GBP/USD should target 1.4248 key resistance (2021 high) on decisive break of 1.3433 at a later stage.