Sample Category Title

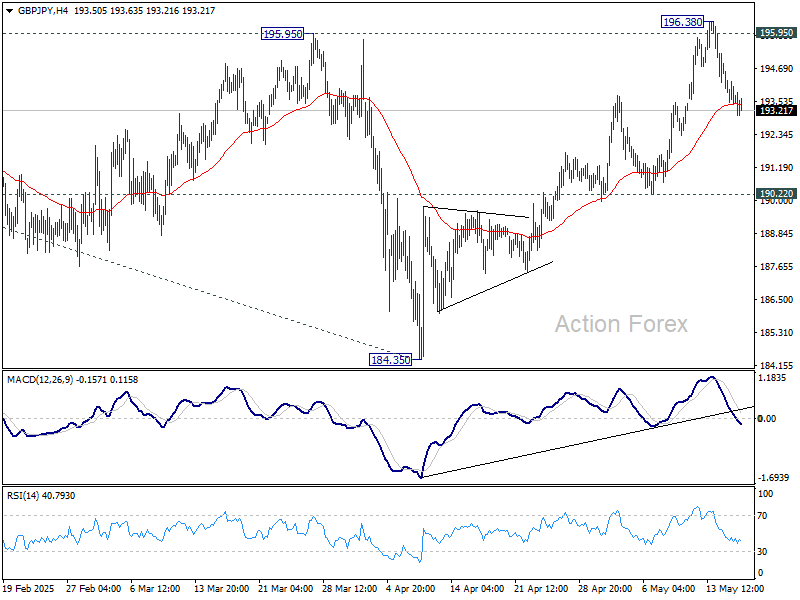

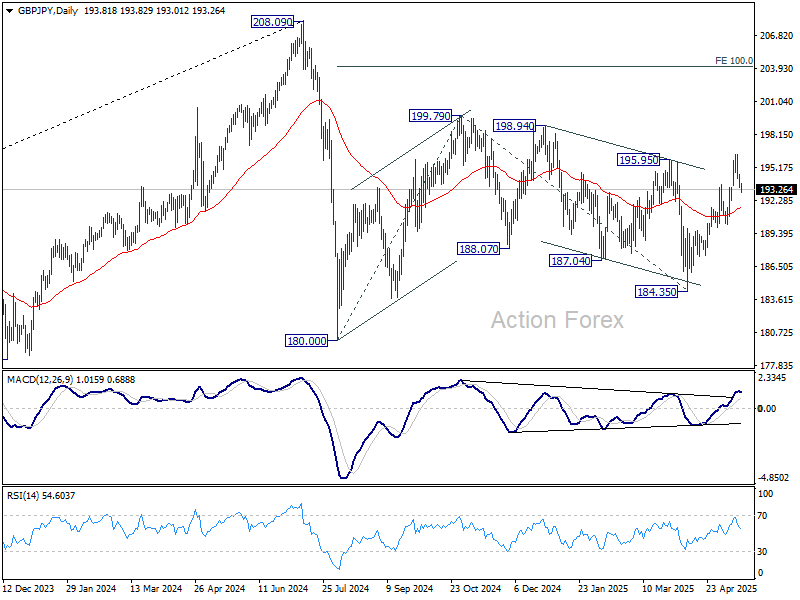

GBP/JPY Daily Outlook

Daily Pivots: (S1) 193.17; (P) 194.08; (R1) 194.73; More...

Intraday bias in GBP/JPY remains neutral and more consolidations could be seen below 196.38. Another rally is in favor as long as 190.22 support holds. Firm break of 195.95 will suggest that whole choppy decline from 199.79 has completed, and target this resistance next. However, decisive break of 190.22 will indicate near term reversal and turn bias back to the downside.

In the bigger picture, price actions from 208.09 are seen as a correction to rally from 123.94 (2020 low). Strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. However, sustained break of 175.94 will bring deeper fall even still as a correction.

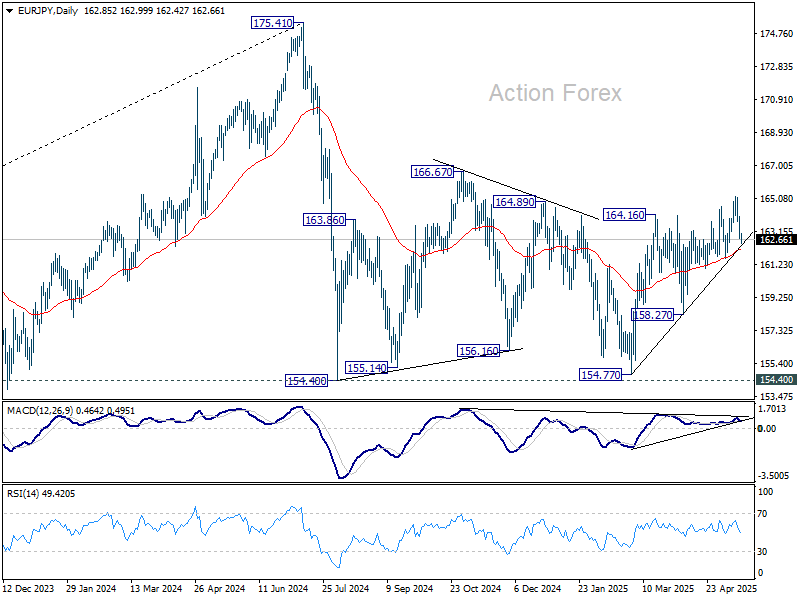

EUR/JPY Daily Outlook

Daily Pivots: (S1) 162.32; (P) 163.35; (R1) 163.94; More...

Intraday bias in EUR/JPY remains neutral and some consolidations could be seen below 165.19. Further rally is in favor as long as 161.57 support holds. Above 165.19 will resume the rally from 154.77 to 166.67 resistance. However, firm break of 161.57 will indicate near term reversal, and turn bias back to the downside.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

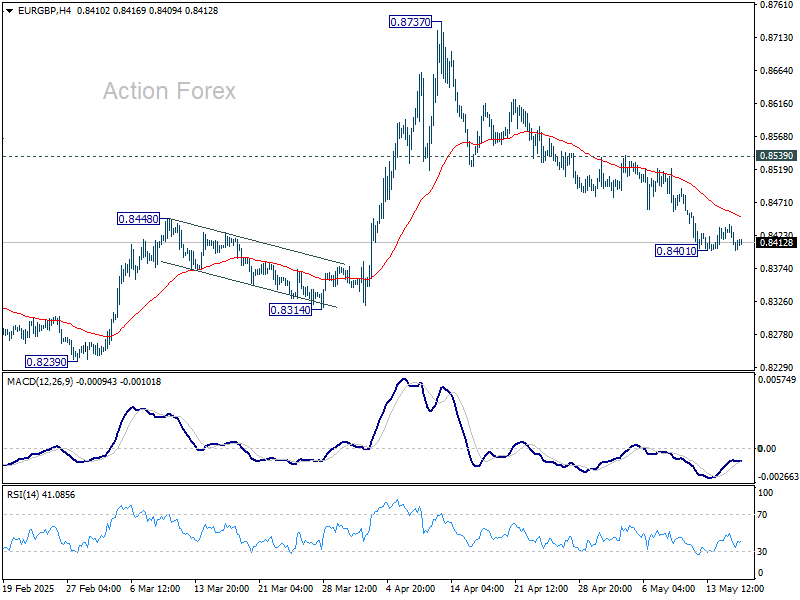

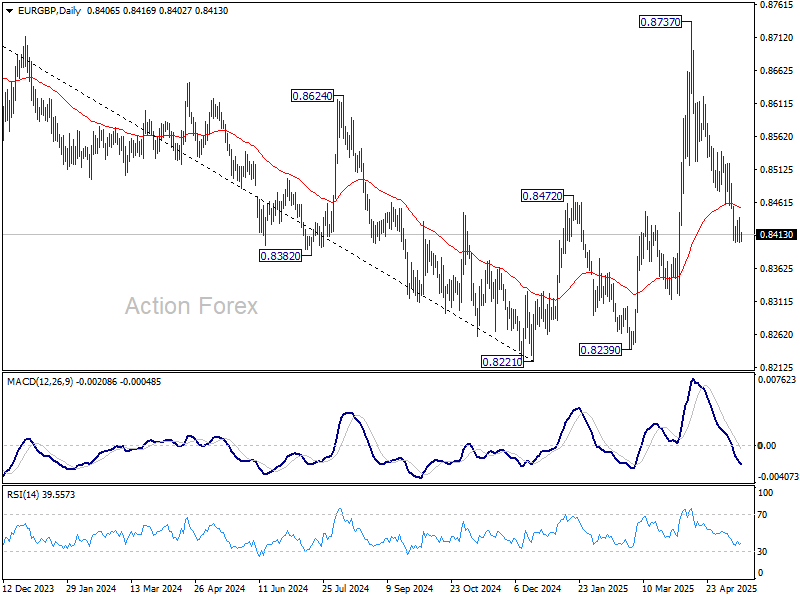

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8392; (P) 0.8417; (R1) 0.8430; More...

Intraday bias in EUR/GBP remains neutral and more consolidations could be seen above 1.8401. Another fall is expected as long as 0.8539 resistance holds. As noted before, rebound from 0.8221 might have completed as a corrective move. Break of 0.8401 will target retest of 0.8221/8239 support zone.

In the bigger picture, the extended decline from 0.8737 dampened the original bullish view. While a medium term bottom was in place at 0.8221, price actions from there could be a corrective pattern only. Larger down trend from 0.9267 (2022 high) might still be in progress. Sustained trading below 55 W EMA (now at 0.8438) will turn favor to this bearish case.

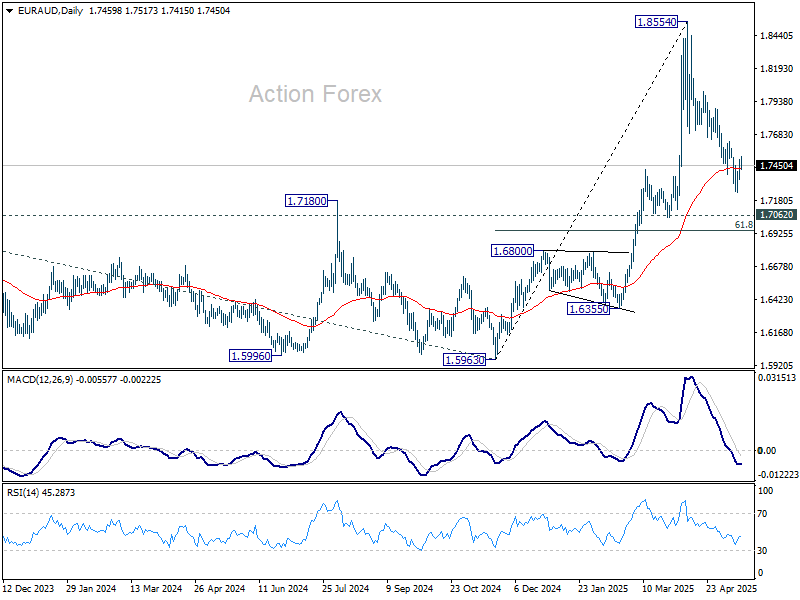

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7367; (P) 1.7431; (R1) 1.7521; More...

Intraday bias in EUR/AUD remains neutral at this point. Further fall is in favor as long as 1.7628 resistance holds. Below 1.7245 will target 61.8% retracement of 1.5963 to 1.8554 at 1.6953. On the upside, however, firm break of 1.7628 resistance will argue that fall from 1.8854 might be completed, and turn bias back to the upside for stronger rebound.

In the bigger picture, as long as 1.7062 resistance turned support (2023 high) holds, up trend from up trend from 1.4281 (2022 low) should still be in progress. However, sustained break of 1.7062 will confirm medium term topping and bring deeper fall back to 1.5963 support.

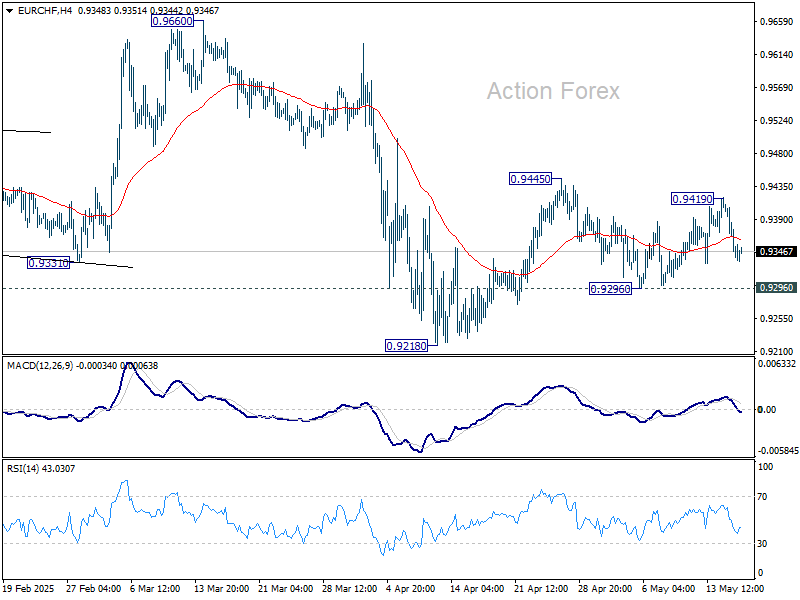

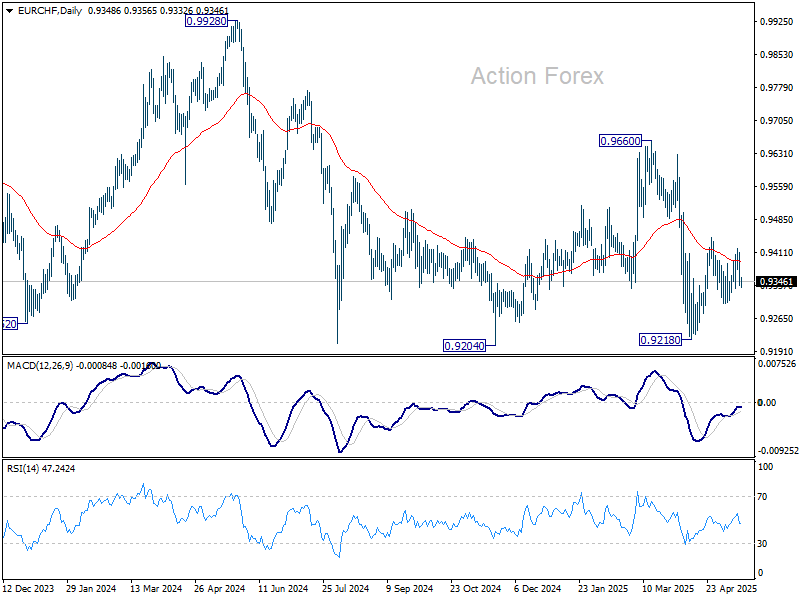

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9382; (P) 0.9402; (R1) 0.9430; More....

Intraday bias in EUR/CHF remains neutral as range trading continues. Rebound from 0.9218 is either as a corrective move or the third leg of the pattern from 0.9204. On the upside, break of 0.9419 resistance will target 0.9445 and above. Nevertheless, break of 0.9296 support will bring retest of 0.9204/18 support zone.

In the bigger picture, prior rejection by long-term falling channel resistance (now at 0.9548) retains medium term bearishness. That is, down trend from 1.2004 (2018 high) is still in progress. Firm break of 0.9204 (2024 low) will confirm resumption. This will remain the favored case as long as 0.9660 resistance holds.

Dollar Rebound Apparently Has Run Its Course

Markets

The new leg in the ‘reflation rebound’ as triggered by a promising outcome in US-Sino trade talks last weekend ran into resistance. US yields yesterday were closing in on some kind of a technical wall (2-yr 4.05/10% area, 10-y 4.55/60% area, 30-y key 5.0% barrier). Money markets had scaled back expectations on the EoY Fed easing to 50 bps. The debate for sure will remain subject to multiple reassessments, but for now this look a reasonable bet. While unlikely being conclusive for the timing and amount of Fed easing, mildly softer than expected US data in this respect provided a perfect excuse to move to some more neutral positioning. US PPI producer prices printed softer than expected. April retail sales were soft (0.1% M/M, -0.2% control sales), but came on the back of a very strong (and upwardly revised) March reading. Difficult to draw any conclusions on spending going forward. Idem for mixed industry surveys. Even so, it was enough for markets to not further scale back expectations on Fed easing. US yields eased between 11.3 bps (5-y) and 8.3 bps for the 30-y with the latter intraday briefly touching the 5.0% mark. Even without much high profile news, German yields followed in lockstep with yields easing 6.0 bps (2-y) and 8.0 bps (30-y). EMU money markets are now again fully in line with two additional ECB rate cuts towards the end of the year and a low in the ECB easing cycle at 1.75%. The equity rally stalled but with no retracement yet (S&P 500 +0.4%, Eurostoxx 50 +0.16%). USD trading of late mainly was driven by trade-related topics (was/is FX policy a topic in US trade negotiations, in particular with Asian trading partners?). Even so, yesterday’s US data and declining yields at least didn’t help. The dollar eased a bit further with the likes of the won and the yen still outperforming (close USD/JPY 145.7, DXY 100.88, EUR/USD marginally higher at 1.119). Decent UK GDP data kept sterling fairly well bid intraday, with EUR/GBP returning tot the low 0.84 support area.

Asian equities this morning trade modestly lower. US yields tentatively extend yesterday’s setback (minus 1-2 bps) as does the dollar (USD/JPY 145.2, EUR/USD 1.1215). Today’s eco calendar in the EMU is almost empty. In the US housing starts and permits and the U. of Michigan consumer confidence are scheduled for release. Confidence is expected to bottom after a steep setback since the start of the year. Markets will look out for the inflation expectations series after last month’s sharp leap higher, especially in the 1-yr ahead measure (6.5%). Given the repositioning this week, probably a substantial upward surprise is need for yields to change course north again. For now, we favour more consolidation as US yields are probably blocked by above-mentioned technical barriers. The dollar rebound earlier this week apparently has run its course. Especially for the likes of USD/JPY, direction south looks the path of least resistance.

News & Views

Japanese GDP shrank by slightly more than expected in Q1 2025. The -0.2% Q/Q contraction (-0.7% annualized) was the first negative number since Q1 2024. Available details showed consumption failing to contribute (0% Q/Q) following an already weak Q4 2024 (+0.1% Q/Q). Like in yesterday’s UK GDP release, there was a significant increase in business spending (1.4% Q/Q). Net exports cut 0.8 percentage point off Q/Q GDP with inventories adding 0.3 ppt. Rather weak growth was accompanied by rising inflation with the GDP deflator increasing from 2.9% Y/Y to 3.3% Y/Y, the highest levels since Q4 2023, and complicating the BoJ’s policy normalization process. Japanese money markets aren’t positioned for the continuation of the hiking cycle anytime soon, with the market implied probably of another 25 bps rate increase at only 67% by the end of the year.

The central bank of Mexico extended its rate cut cycle with a third consecutive 50 bps rate cut to 8.50%. Banxico stated that “it could continue calibrating the monetary policy stance and consider adjusting it in similar magnitudes.” This clearly hints at similar action at the June meeting. Both headline and core inflation came in at 3.93% Y/Y in April. Inflation forecasts were adjusted upwards in the short term, mainly due to a greater-than-expected increase in merchandise inflation but headline inflation is still expected to converge to the 3%-target in Q3 2026. Although the balance of risks remains biased to the upside, it has improved as global shocks have been fading. The inflation environment allows for a continuation of the rate cutting cycle, albeit maintaining a restrictive stance.

Bulls Need Fresh Catalyst

Market sentiment remained tilted toward the upside across the US and European markets yesterday. In Europe, UK growth and eurozone industrial production surprised to the upside, boosting bulls who see the European economies benefiting from lower energy prices and relatively higher currencies to deal with their inflation battle. Combined with government spending prospects, growth in Europe could improve. Yesterday’s numbers somehow supported that view – the Q1 growth in the eurozone was softer than expected, but industrial production made solid progress.

Across the pond, the news was less enchanting, for sure. US retail sales decelerated significantly, factory production declined for the first time in six months, and confidence among homebuilders worsened. The only bright spot was the dramatic easing in producer prices: the yearly figure fell from 3.4% to 2.4%, and the monthly number printed a deflationary reading of 0.5%. Some analysts started saying that the latter numbers point to a slowdown, not stagflation – meaning that the Federal Reserve (Fed) could lower rates and turn the tables. As such, the US 2-year yield was pulled below the 4% mark and brought the possibility of a July rate cut onto the table.

But wait... Walmart – the US retailer known for offering low prices to its customers – said it will be raising the prices of some products in accordance with the tariffs. Not all products will see price increases – the company will try to shield food prices from tariff-led hikes – but for others, depending on their sources, there will be inflation. A 30% tariff, for example, on products from China could lead to double-digit price increases, the company warned. So that aligns with the narrative of both slower spending and higher inflation – a mix the Fed will find hard to deal with.

If you ask me which camp I’m in, I’d say I’m closer to the stagflation camp than the Goldilocks – everything will be fine – camp. And despite the lower recession bets since the US/China de-escalation and the Middle East deals, economic worries for the US will remain.

And the news will continue to be hectic... Trump said yesterday that he had a problem with Tim Cook, that he doesn’t want Apple to move production to India. But Apple has been moving production from China to India to comply with Donald Trump’s will to get out of China. Producing iPhones in the US and selling them for $3000 is not a viable option, so the picture darkens again. Interestingly, Apple fell only 0.41% yesterday on the news, maybe on disbelief, maybe on the lack of alternative scenarios to help Apple get away with the US manufacturing ambitions.

Elsewhere, Nvidia consolidated gains on worries that some people at the White House are concerned that the huge sales to the Middle East would go against national security purposes and benefit China. Overall, the S&P500 started the session with limited appetite but found buyers throughout – hinting that appetite somehow improves despite less-than-ideal news. But gains are certainly at risk of trade news and policies. And the fact that the S&P’s low volatility ETF jumped nearly 2% could be a sign that the winds may be turning in the absence of further good news.

In FX

The US dollar index remains under pressure, and the dollar’s weakness is becoming a serious headache for foreign investors who didn’t previously feel the need to hedge against a weaker dollar – because in times of market turmoil and high volatility, the dollar typically gains on safe-haven flows. But recently, the dollar has been weakening despite rising volatility, and the latter increases hedging costs, leading to an unusual negative correlation between the dollar and volatility. What it ultimately warns is that – given how global portfolios are heavily invested in US companies – increased hedging against the US dollar could further weigh on the dollar’s valuation in the medium run.

In the short run, the dollar’s broad-based retreat helps the majors gain ground. The EURUSD rebounded past the 1.12 level after having tested the 50-DMA to the downside this week. Despite a set of stronger-than-expected inflation readings in major eurozone economies, the shiny industrial production numbers brought euro bulls back to the market. Sterling extended gains against the dollar as well, while the Japanese yen printed a very clear advance against the US dollar this week. The latter may have weighed on the Nikkei index throughout the week, but the Japanese blue-chip index is preparing to close a bearish week – in contrast to European peers – above its 100-DMA.

Chasing cheap deals in China?

In China, Alibaba’s profit missed estimates and led to a 7.5% selloff in the company’s shares yesterday. Part of the reason was gloomy consumer spending due to tariffs, and part was the company’s decision to divest from subsidiaries and the valuation of its equity holdings. But the company’s cloud revenue accelerated – as a sign of growing AI demand – and CEO Eddie Wu said their AI-related product revenue achieved triple-digit growth for the seventh consecutive quarter. They didn’t specify which product. Although investors were discouraged by the actual numbers, the developing AI story, various stimulus measures to boost Chinese consumption, and possible de-escalation of the trade war with the US remain promising factors for Alibaba in the medium run. As such, the price pullbacks could be interesting opportunities to buy dips. From a technical perspective, Alibaba managed to defy the bears into the $100 per share level at the heart of the trade storm and rebounded 40% from dip to peak. The positive trend will remain intact above the $120 per share level.

This Week Concludes With US Consumer Sentiment

In focus today

In the US, we await the preliminary May consumer sentiment survey from University of Michigan, which will provide markets with the latest sense of how consumers are feeling after the tariffs took effect. Earlier surveys have shown a sharp deterioration in future expectations and rapid upticks in inflation expectations.

In the euro area, the European Commission had scheduled to publish its spring economic forecast today, but the publication has been rescheduled for Monday following the trade war de-escalation between the US and China.

In China, early Monday, April's monthly data including retail sales, housing data and industrial production will be released. The month marks the trade escalation, making it crucial to observe any impact on consumption etc. Consensus looks for broadly unchanged growth in retail sales around 6% y/y. The housing market shows a decline in home prices but moderate improvement in home sales. These figures are somewhat outdated, as they precede the US-China trade deal on 11-12 May. We look for a decent recovery in China soon, as front-loading by US importers is set to give a big boost to Chinese exports over the next three months.

Have a great Friday and weekend!

Economic and market news

What happened overnight

In Japan, Q1 national account data reveals a sharper-than-expected decline in GDP at -0.2% q/q (cons: -0.1%), with lower external demand at -0.8% and stagnant consumption, which accounts for more than half of Japan's GDP, in the driver's seat. Capital spending rose by 1.4% q/q, surpassing the consensus of 0.8%. The figures mark the economy shrinking for the first time of the year, underscoring the fragile recovery and complicating the BoJ's rate hike path.

What happened yesterday

In the US, yesterday's data revealed m/m declines in core PPI and control group retail sales, with mixed signals from manufacturing data: the Philly Fed rebounded strongly, but the NY Fed's Empire Index continued to decline. Retail sales details were also mixed, suggesting that the weak retail sales may be a reversal of front-loading effects rather than true underlying weakness. The negative core PPI reading was due to weak services price pressures, while core goods inflation modestly accelerated due to tariffs. Overall price pressures thus seem to remain controlled. Markets reacted by sending yields modestly lower.

Moreover, the budget committee of the US House of Representatives is expected to finalize the reconciliation bill today, combining the extensions to Trump's 2017 tax cuts with other budget changes. The first vote on House floor will most likely take place already this month, but passing the bill through House and Senate is expected to be challenging.

Meanwhile, Fed Chair Jerome Powell opened a two-day conference to reassess the Fed's monetary policy framework, acknowledging the need for adaptation due to more frequent supply shocks and inflation trends.

In the euro area, employment continued to grow in the first quarter of the year, rising 0.3% q/q after growing 0.1% q/q in Q4 2024. Hence, the labour market remains on the strong footing it has been on in the past years despite weak economic activity. The strong labour market is a hawkish argument for the ECB.

Alongside the employment data we also got the second estimate of growth in Q1, which showed GDP rising 0.3% q/q compared to the 0.4% q/q in the first estimate. However, the revision was mainly due to rounding when evaluating the second decimal.

In Norway, mainland GDP rose by 1.0% q/q in Q1, surpassing consensus and Norges Bank's forecast in March, both at 0.6%. Private consumption increased by 1.5% q/q, corporate investments by 1.1% q/q, and residential investments by 0.4% q/q. Despite a drop in public investment and oil investments, the strong figures question the necessity for rate cuts. However, improvements in rate-sensitive sectors may reflect expectations of a rate cut in March that was never delivered. Monthly figures reveal a slowdown during Q1, with January at 1.2 % m/m, February 0.1 % m/m, and March at -0.2 % m/m.

The revised fiscal budget figures showed an increase in spending at 2.7% of the oil fund equity, aligning with Norges Bank's estimates. Support packages for Ukraine contribute to lifting spending to NOK 542.2bn, delivering a substantial fiscal impulse of 2.5%. Much of this spending is unlikely to directly impact the mainland economy.

In Sweden, inflation expectations decreased in April, with CPIF projections returning to 2.1% for both the one- and two-year horizons. The crucial five-year expectation, previously at 2.3% last month, has now aligned with the inflation target of 2%. Overall, this is a positive reading for the Riksbank, with inflation expectations presenting no obstacle should they decide to cut rates in the coming months.

In geopolitics, Russian delegation head Vladimir Medinsky announced that talks with Ukraine will start this morning in Istanbul. Zelenskiy criticised Putin's absence, and the US expressed low expectations for the talks until a meeting occurs between Trump and Putin.

Equities: Equities drifted gradually higher, with some interesting dynamics. Major indexes were 0.5-1% higher, but underlying sectors and style preferences flipped around. Equal weighted S&P 500 outperformed S&P 500 and Europe outperformed US. Interestingly, this happened despite yields plunging 5-10bp, which would normally result in US outperformance. Moreover, it was a defensive comeback, with utilities, consumer staples and real estate outperforming the Mag Seven. Some context is warranted: defensive sectors have lower valuation multiples than in April while cyclical sector valuation has fully recovered. This is not very intuitive and speaks for catch-up in those names, just like the session yesterday. Futures are little changed this morning while Asian stocks are retreating after a strong week.

FI&FX: The last 24 hours have been characterised by broad-USD and NOK weakness while the JPY and CHF have enjoyed souring risk appetite. Softer US figures contributed to sending USD rates meaningfully lower for the first time in a week with the US 10Y Treasury yield back close to 4.40. The EUR curve flattened driven by the long end while Scandi rates generally underperformed. BTP-Bund spreads continue to tighten while Treasury ASW spreads have been stable in recent sessions.

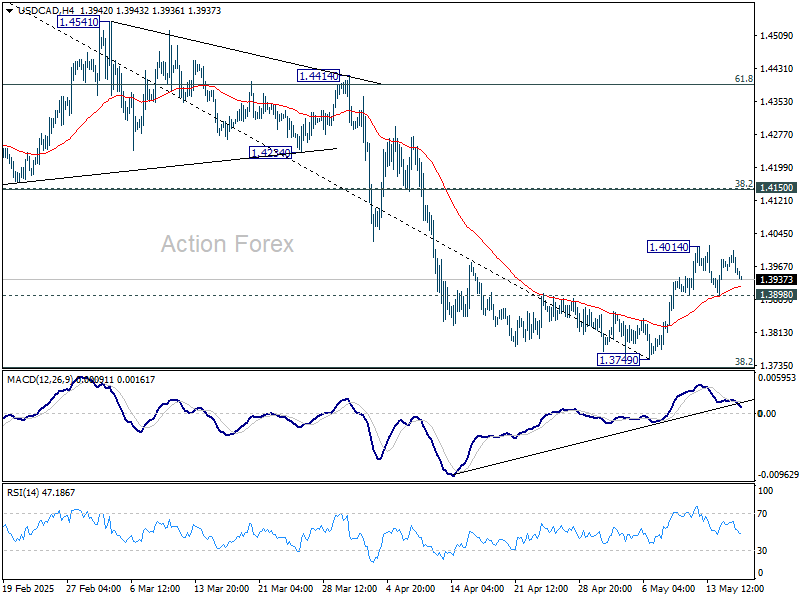

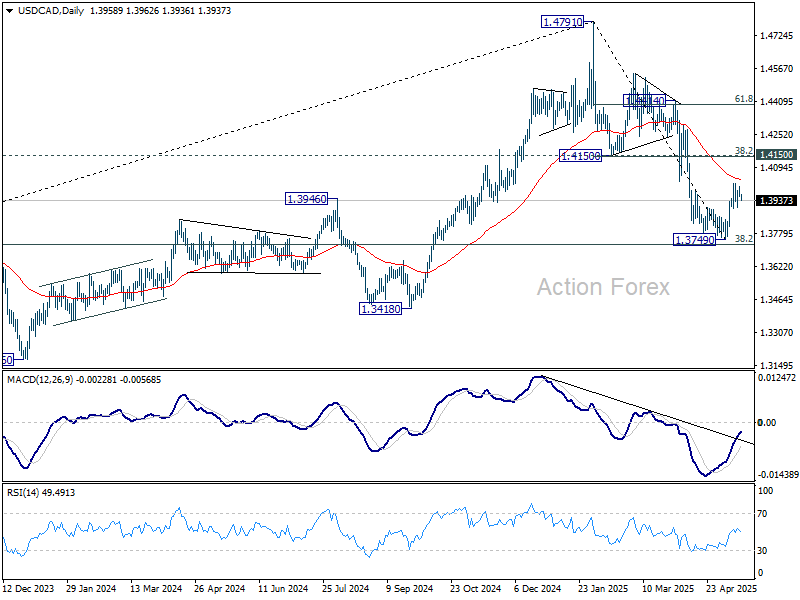

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3942; (P) 1.3973; (R1) 1.3991; More...

Intraday bias in USD/CAD stays neutral a this point. Further rise is in favor with 1.3898 minor support intact. Above 1.4014 will resume the rebound from 1.3749 to 1.4150 cluster resistance (38.2% retracement of 1.4791 to 1.3749 at 1.4147). However, break of 1.3898 minor support will indicate that the rebound has completed, and bring retest of 1.3749.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4150 resistance turned support holds. Firm break of 38.2% retracement of 1.2005 (2021 low) to 1.4791 at 1.3727 will pave the way back to 61.8% retracement at 1.3069.

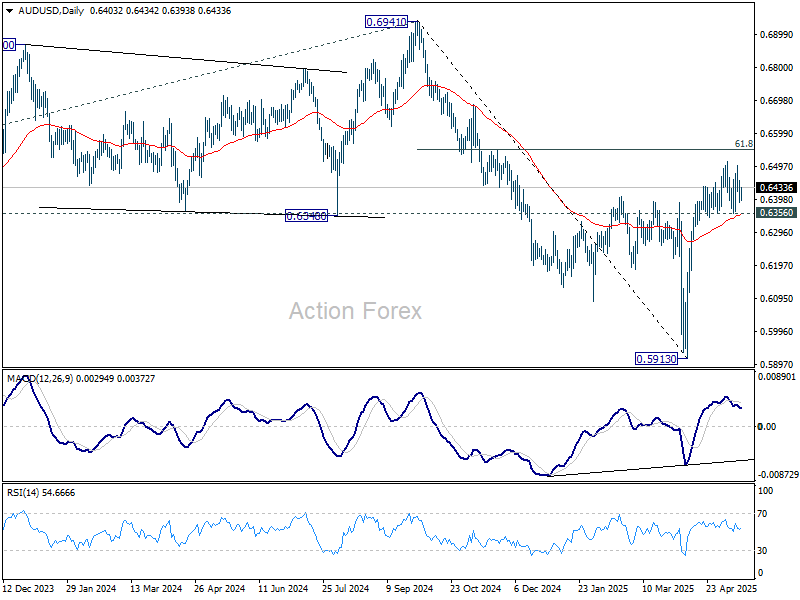

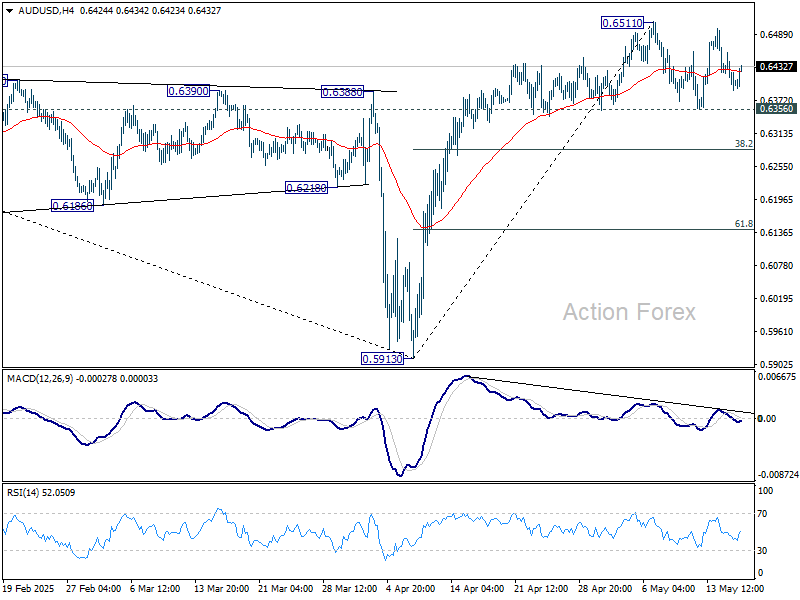

AUD/USD Daily Report

Daily Pivots: (S1) 0.6379; (P) 0.6418; (R1) 0.6446; More...

Intraday bias in AUD/USD remains neutral for the moment. On the upside, firm break of 0.6511 will resume the rally from 0.5913 to 61.8% retracement of 0.6941 to 0.5913 at 0.6548. However, break of 0.6356 will bring deeper pullback to 38.2% retracement of 0.5913 to 0.6511 at 0.6283.

In the bigger picture, as long as 55 W EMA (now at 0.6441) holds, down trend from 0.8006 (2021 high) should resume later to 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. However, sustained trading above 55 W EMA will argue that a medium term bottom was already formed, and set up further rebound to 0.6941 resistance instead.