Sample Category Title

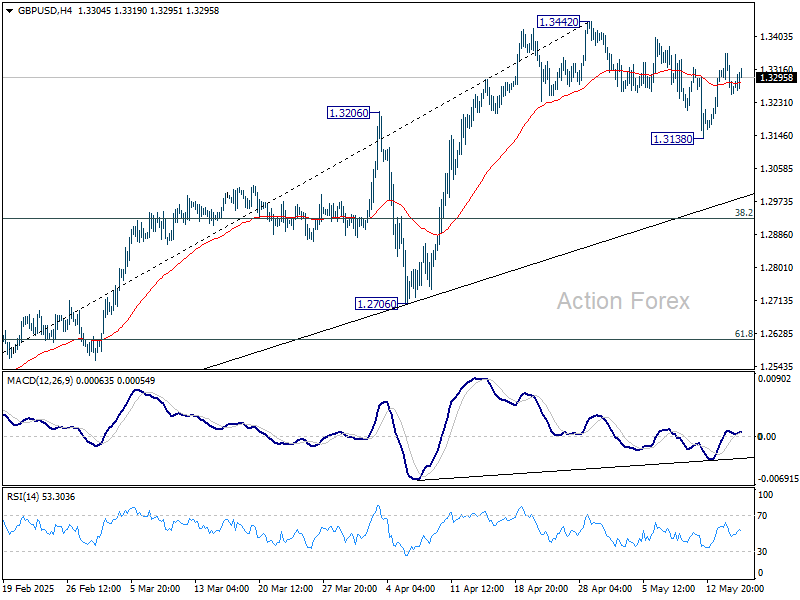

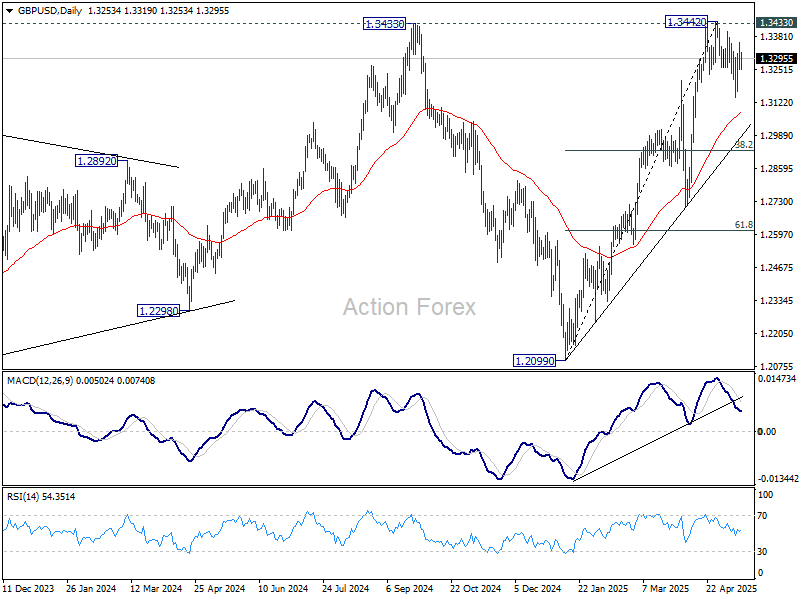

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3225; (P) 1.3292; (R1) 1.3331; More...

Intraday bias in GBP/USD remains neutral first. On the upside, decisive break of 1.3433/42 key resistance zone will confirm larger up trend resumption. Nevertheless, below 1.3138 will resume the correction from 1.3442. But downside should be contained by 38.2% retracement of 1.2099 to 1.3442 at 1.2929 to bring rebound.

In the bigger picture, price actions from 1.3433 are seen as a corrective pattern to the up trend from 1.3051 (2022 low). Rise from 1.2099 could either be resuming the up trend, or the second leg of a consolidation pattern. Overall, GBP/USD should target 1.4248 key resistance (2021 high) on decisive break of 1.3433 at a later stage.

US: Retail Sales Take a Breather in April

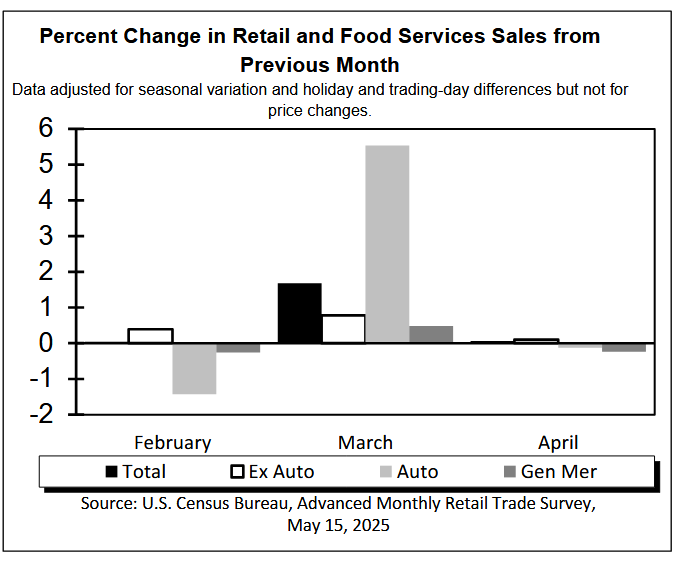

Retail and food services sales were little changed in April, edging up by just 0.1% month-on-month (m/m). The pause in activity in April comes after an outsized gain in March, which was revised higher to 1.7% m/m (previously 1.5% m/m).

Motor vehicle sales and parts edged lower by 0.1% m/m, though that came from very elevated levels as households continued to purchase vehicles ahead of the tariffs. Sales at gasoline stations were also lower, declining for the third consecutive month (-0.5% m/m) due to lower prices at the pump. Meanwhile, building materials and equipment stores had another decent month of growth, with sales rising by 0.8% m/m.

Sales in the "control group", which excludes the volatile components above (i.e., gasoline, autos and building supplies) declined by 0.2% m/m, well below expectations for a 0.3% gain.

Sales pulled back across most of the remaining categories, particularly in areas that saw large gains in March, including sporting goods & hobby stores (-2.5% m/m) and miscellaneous store retailers (-2.1% m/m). Furniture & home furnishings and electronics & appliance stores bucked the trend, with sales increasing by 0.3% m/m in each category. Online sales also edged modestly higher (+0.2%).

Sales at bars and restaurants remained strong, rising 1.2% m/m. This comes on the heels of an upwardly revised 3% m/m growth in March (previously reported as 1.9%).

Key Implications

Retail sales were little changed in April, but the easing in activity comes on the heels of a surge in March as consumers rushed to front-load purchases ahead of anticipated tariffs. There continued to be some evidence of this front-loading in April, with auto sales remaining at elevated levels, and consumers still purchasing large ticket items like furniture, electronics, and building materials. Households also showed a continued willingness to spend on discretionary items, as evidenced by another month of strong growth in bar and restaurant sales. While increased spending on goods—particularly cars – can be attributed to efforts to get ahead of potential tariff-related price hikes, robust spending on services like dining out suggests that consumer spending remains relatively resilient, despite downbeat sentiment.

The current divergence between forward-looking consumer sentiment and actual spending activity reflects both the front-loading of purchases and the still-resilient underlying economic fundamentals. The labor market continues to show strength, with job growth averaging 155,000 per month over the past three months, and wage growth remains positive. As for inflation, there have been no significant signs of price pressures stemming from tariffs so far. Corporate efforts to stockpile goods and limit the pass-through of costs to consumers appear to be containing price increases, at least in the short term. The temporary truce with China and the reduction in reciprocal tariffs should further ease pricing pressures in the near term. Looking through the recent volatility, we expect consumer spending to advance by around 1% in the second quarter as the boost from pre-emptive shopping fizzles out.

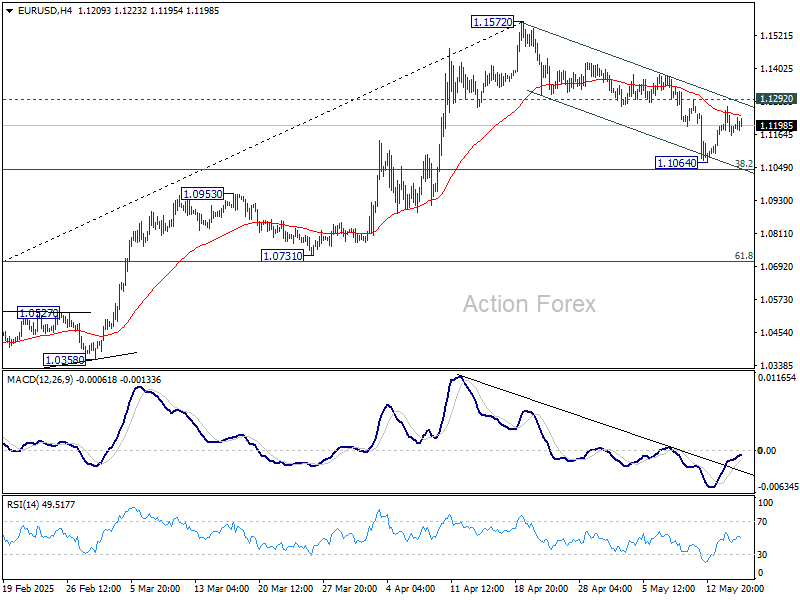

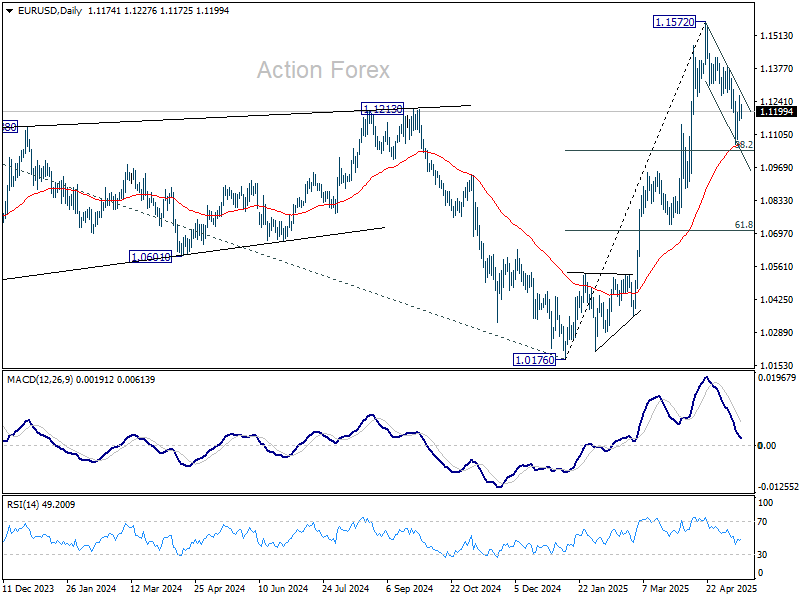

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1136; (P) 1.1201; (R1) 1.1238; More...

Range trading continues in EUR/USD and intraday bias stays neutral. On the upside, break of 1.1292 resistance will argue that correction from 1.1572 has completed after defending 38.2% retracement of 1.0176 to 1.1572 at 1.1039. Intraday bias will be back on the upside for retesting 1.1572. However, sustained break of 1.1039 will dampen this view and target 61.8% retracement at 1.0709 next.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0789) holds.

Markets Tread Water as Traders Shrug Off US PPI and UK GDP Surprises

Global financial markets are trading in tight ranges today, with little conviction seen across major asset classes. U.S. futures are pointing to a mildly weaker open. Despite a surprise decline in US producer prices in April, suggesting a possible easing of inflation pressures, there was little follow-through in market reaction. Earlier today, stronger-than-expected UK Q1 GDP data also offered limited support to the Pound. Overall sentiment remains contained as traders await further clarity on the trade front.

Much of the current hesitation in markets can be attributed to persisting trade uncertainty. The EU Foreign Affairs Council is holding a key meeting today in Brussels to discuss trade relations with the US and broader economic security. Ahead of the meeting, European trade ministers expressed dissatisfaction with the limited UK-US trade agreement announced last week, which retains a 10% tariff on British exports. EU officials signaled that such a deal would not suffice to deter retaliatory measures.

European Trade Commissioner Maros Sefcovic confirmed a recent conversation with U.S. Commerce Secretary Howard Lutnick and noted that both sides have agreed to step up engagement. Additional meetings are anticipated in Brussels or during upcoming OECD sessions. However, the complexity of negotiations and diverging expectations between the EU and US continue to cast doubt on a swift resolution.

Elsewhere, trade talks between the US and India also show signs of friction. US President Donald Trump claimed that India had offered a trade deal with “no tariffs” on American goods. However, India’s foreign minister Subrahmanyam Jaishankar quickly pushed back, saying that talks remain ongoing and nothing has been finalized. It's believed that India would demand strict reciprocity on tariffs, while it's unlikely to concede easily in politically sensitive sectors such as agriculture, where protectionist pressures remain high.

In the currency markets, Aussie is leading gains for the week, followed by Dollar and then Sterling. On the weaker side, the Swiss Franc is the laggard, with Kiwi and Euro also underperforming. Yen and Canadian Dollar are holding middle positions.

In Europe, at the time of writing, FTSE is up 0.34%. DAX is up 0.10%. CAC is down -0.19%. UK 10-year yield is down -0.042 at 4.674. Germany 10-year yield is down -0.061 at 2.64. Earlier in Asia, Nikkei fell -0.98%. Hong Kong HSI fell -0.79%. China Shanghai SSE fell -0.68%. Singapore Strait Times rose 0.54%. Japan 10-year JGB yield rose 0.022 to 1.479.

US retail sales rises 0.1% mom in Apr, ex-auto sales up 0.1% mom

US retail sales rose 0.1% mom to USD 724.1B in April, matched expectations. Ex-auto sales rose 0.1% mom to USD 582.5B, below expectation of 0.3% mom. Ex-gasoline sales rose 0.1% mom to USD 673.1B. Ex-auto & gasoline sales rose 02% mom to USD 531.5B.

Total sales for the February through April period were up 4.8% from the same period a year ago.

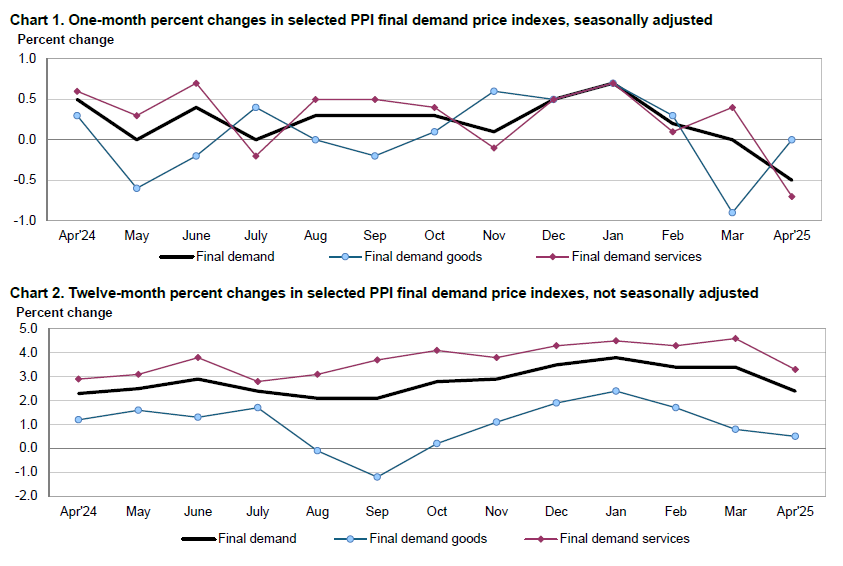

US PPI at -0.5% mom, 2.4% yoy in April, below expectations

US PPI fell -0.5% mom in April, below expectation of 0.2% mom. PPI services fell -0.7% mom while PPI goods was unchanged. PPI less foods, energy and trade services ticked down by -0.1% mom, the first decline since April 2020.

For the 12 months, PPI slowed from 2.7% yoy to 2.4% yoy, below expectation of 2.5% yoy. PPI less foods, energy and trade services rose 2.9% yoy.

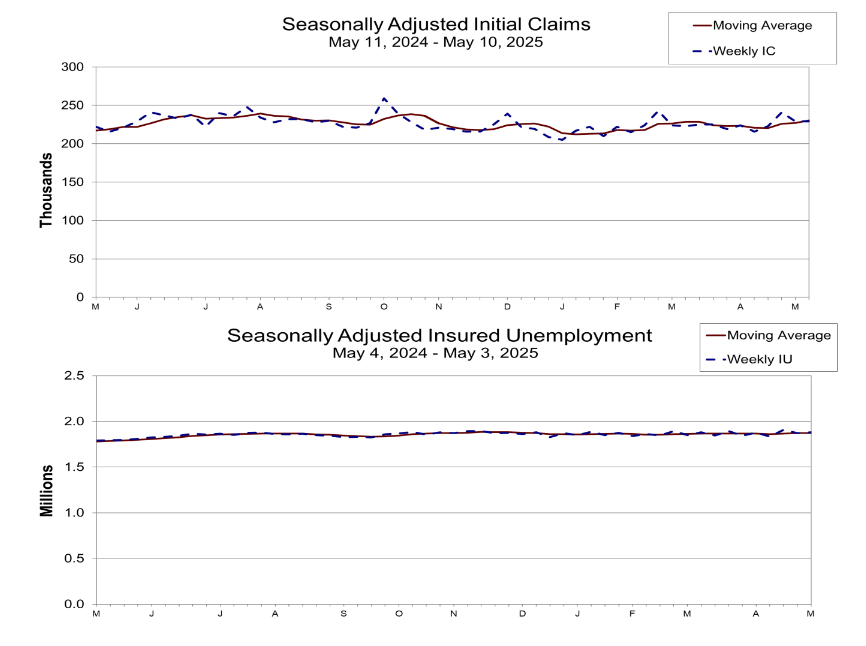

US initial jobless claims unchanged at 229k

US initial jobless claims was unchanged at 229k in the week ending May 10, slightly below expectation of 230k. Four-week moving average of initial claims rose 3k to 230.5k.

Continuing claims rose 9k to 1881k in the week ending May 3. Four-week moving average of continuing claims rose 1k to 1874k.

Eurozone industrial output surges 2.6% mom in March, led by capital goods

Eurozone industrial production jumped 2.6% mom in March, significantly outperforming expectations of 1.7% mom. The surge was driven by strong gains across key categories, including capital goods (+3.2%), durable consumer goods (+3.1%), and non-durable consumer goods (+2.3%). Intermediate goods also posted a modest 0.6% rise, while energy output dipped by -0.5%.

Across the broader EU, industrial production rose by 1.9% mom. Ireland led the gains with a remarkable 14.6% surge, followed by Malta (+4.4%) and Finland (+3.5%). However, there were notable declines in Luxembourg (-6.3%), Denmark, Greece (both -4.6%), and Portugal (-4.0%).

UK economy beats expectations with 0.7% qoq growth in Q1, 0.2% mom in March

The UK economy expanded by 0.7% qoq in Q1, slightly ahead of expectations at 0.6% qoq. Growth was led by a 0.7% qoq rise in the services sector and a robust 1.1% qoq increase in production output, while construction activity was flat. Importantly, real GDP per head also rose by 0.5% qoq, ending two consecutive quarters of contraction.

On the expenditure side, growth was underpinned by a 2.9% qoq rise in gross fixed capital formation, signaling strong business investment. Household consumption also edged up by 0.2% qoq, while net trade contributed positively as exports rose by 3.5% qoq and imports by 2.1% qoq.

Monthly data for March further supported the upbeat quarterly reading, with GDP rising by 0.2% mom, exceeding expectations of flat growth. Services output was the standout, rising 0.4% mom and contributing the most to overall GDP expansion. Meanwhile, construction rose by 0.5% mom, offsetting a -0.7% mom decline in production output.

Australia jobs surge 89k in April, unemployment rate unchanged at 4.1%

Australia’s labor market delivered a strong upside surprise in April, with employment rising by 89k, sharply above expectations of 20.9k. Full-time jobs accounted for 59.5k of the gain, while part-time employment rose by 29.5k.

Unemployment rate held steady at 4.1%, in line with forecasts, as the surge in employment was matched by a jump in labor force participation from 66.8% to 67.1%.

Despite the headline strength, hours worked were largely unchanged on the month. Nonetheless, the employment-to-population ratio rose by 0.3 percentage points to 64.4%, just shy of the record high reached in January.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1136; (P) 1.1201; (R1) 1.1238; More...

Range trading continues in EUR/USD and intraday bias stays neutral. On the upside, break of 1.1292 resistance will argue that correction from 1.1572 has completed after defending 38.2% retracement of 1.0176 to 1.1572 at 1.1039. Intraday bias will be back on the upside for retesting 1.1572. However, sustained break of 1.1039 will dampen this view and target 61.8% retracement at 1.0709 next.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0789) holds.

US initial jobless claims unchanged at 229k

US initial jobless claims was unchanged at 229k in the week ending May 10, slightly below expectation of 230k. Four-week moving average of initial claims rose 3k to 230.5k.

Continuing claims rose 9k to 1881k in the week ending May 3. Four-week moving average of continuing claims rose 1k to 1874k.

US PPI at -0.5% mom, 2.4% yoy in April, below expectations

US PPI fell -0.5% mom in April, below expectation of 0.2% mom. PPI services fell -0.7% mom while PPI goods was unchanged. PPI less foods, energy and trade services ticked down by -0.1% mom, the first decline since April 2020.

For the 12 months, PPI slowed from 2.7% yoy to 2.4% yoy, below expectation of 2.5% yoy. PPI less foods, energy and trade services rose 2.9% yoy.

US retail sales rises 0.1% mom in Apr, ex-auto sales up 0.1% mom

US retail sales rose 0.1% mom to USD 724.1B in April, matched expectations. Ex-auto sales rose 0.1% mom to USD 582.5B, below expectation of 0.3% mom. Ex-gasoline sales rose 0.1% mom to USD 673.1B. Ex-auto & gasoline sales rose 02% mom to USD 531.5B.

Total sales for the February through April period were up 4.8% from the same period a year ago.

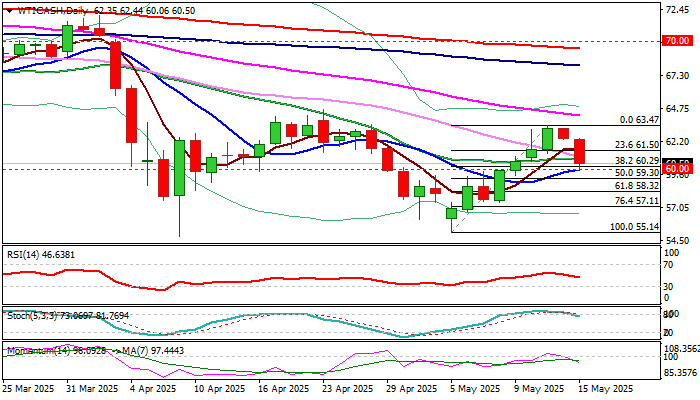

WTI: Oil Prices Drop on Oversupply Concerns as US and Iran Close to Reach a Deal

WTI oil price fell over 3% on Thursday morning, as positive sentiment was soured by the latest encouraging news about US-Iran nuclear talks which may result in easing of sanctions on Iranian oil export and unexpected strong build in US crude stocks that added to growing concerns about oversupply.

Thursday’s strong acceleration extends pullback from recovery top ($63.47) after repeated failure at important Fibo barrier at $63.38 (50% of $71.98/$54.77) and just under the base of falling daily cloud.

Fresh weakness cracked strong supports at $60.29/00 zone (Fibo 38.2% of $55.14/$63.47 recovery leg / psychological, reinforced by 10DMA).

Clear break here to generate fresh bearish signal for deeper drop.

The notion is supported by strengthening negative momentum and stochastic emerging from overbought zone, however bears may face increased headwinds due to significance of supports.

Consolidation above $60 zone may precede fresh push lower, but caution on bounce above $61.50 (broken Fibo 23.6%) which may sideline bears and generate initial signal of an end of corrective phase.

News about progress in US-Iran talks will be closely watched for further direction signals.

Res: 61.00; 61.50; 62.44; 63.00

Sup: 60.00; 59.30; 59.00; 58.32

Australia Employment Soars, Australian Dollar Calm

The Australian dollar is showing limited movement on Thursday. In the European session, AUD/USD is trading at 0.6412, down 0.12% on the day.

Australia job growth surges

Australia's economy added 89 thousand jobs in April, blowing past the market estimate of 20 thousand and above the upwardly revised gain of 36.4 thousand in March. Full-time employment was up an impressive 59.5 thousand. The unemployment rate was unchanged at 4.1%.

Today's jobs report indicates that the labor market remains strong, but that is not expected to change minds at the Reserve Bank of Australia. The money markets have priced in a quarter-point cut at next week's meeting, which would lower the cash rate to 3.85%.

RBA widely expected to lower rates next week

The central bank is expected to cut rates in response to weakening inflation and the uncertainty over US tariffs. Australia's reliant economy could take a significant hit if the US and China trade war continues, which makes the recent tariff deal between the two countries a welcome first step. The agreement, which slashes tariff rates between the US and China, is valid for 90 days and negotiations will continue during that time. Only a few weeks ago, escalating trade tensions threatened to spill into a global trade war but the US has taken a step backwards, reaching a trade deal with the UK and a truce with China.

President Trump's erratic trade policy has roiled the financial markets and made it difficult for the RBA to make inflation and growth forecasts. Still, the RBA appears ready to lower rates next week, which will boost domestic growth. The central bank is expected to remain cautious in its rate policy in the turbulent global economic environment. At home, the labor market has been resilient, inflation is generally under control but consumer spending has been weaker than expected.

AUD/USD Technical

- AUD/USD has pushed below support at 0.6426 and is testing support at 0.6410. Below, there is support at 0.6398

- There is resistance at 0.6438 and 0.6454

AUD/USD 4-Hour Chart, May 15, 2025

GBP/USD at a Crossroads: Momentum Needed for New Buying Opportunities

The GBP/USD pair has again lost direction, hovering around 1.3283 on Thursday after hitting a seven-day high mid-week.

Key drivers influencing GBP/USD movement

The US dollar weakened on Wednesday, allowing the pound to regain ground. This shift followed ongoing currency negotiations between the US and South Korea, where both parties agreed to continue discussions on exchange rate policies. The reduced demand for the greenback lent support to most major currencies, including sterling.

Domestically, the market focus shifted to the Bank of England (BoE) commentary. Deputy Governor Sarah Breeden emphasised the necessity of long-term reforms in the bond market. At the same time, Monetary Policy Committee (MPC) member Catherine Mann noted that further rate cuts would require more evident signs of easing price pressures – essentially, a sustained drop in inflation.

Meanwhile, the latest UK labour market data revealed an increase in the unemployment rate to 4.5%, the highest since 2021, accompanied by a slowdown in wage growth.

These factors have collectively reinforced expectations of further monetary policy easing by the BoE. Despite internal MPC dissent, last week’s 25bps rate cut caught markets off guard, as many expected a pause in the easing cycle.

Technical analysis: GBP/USD

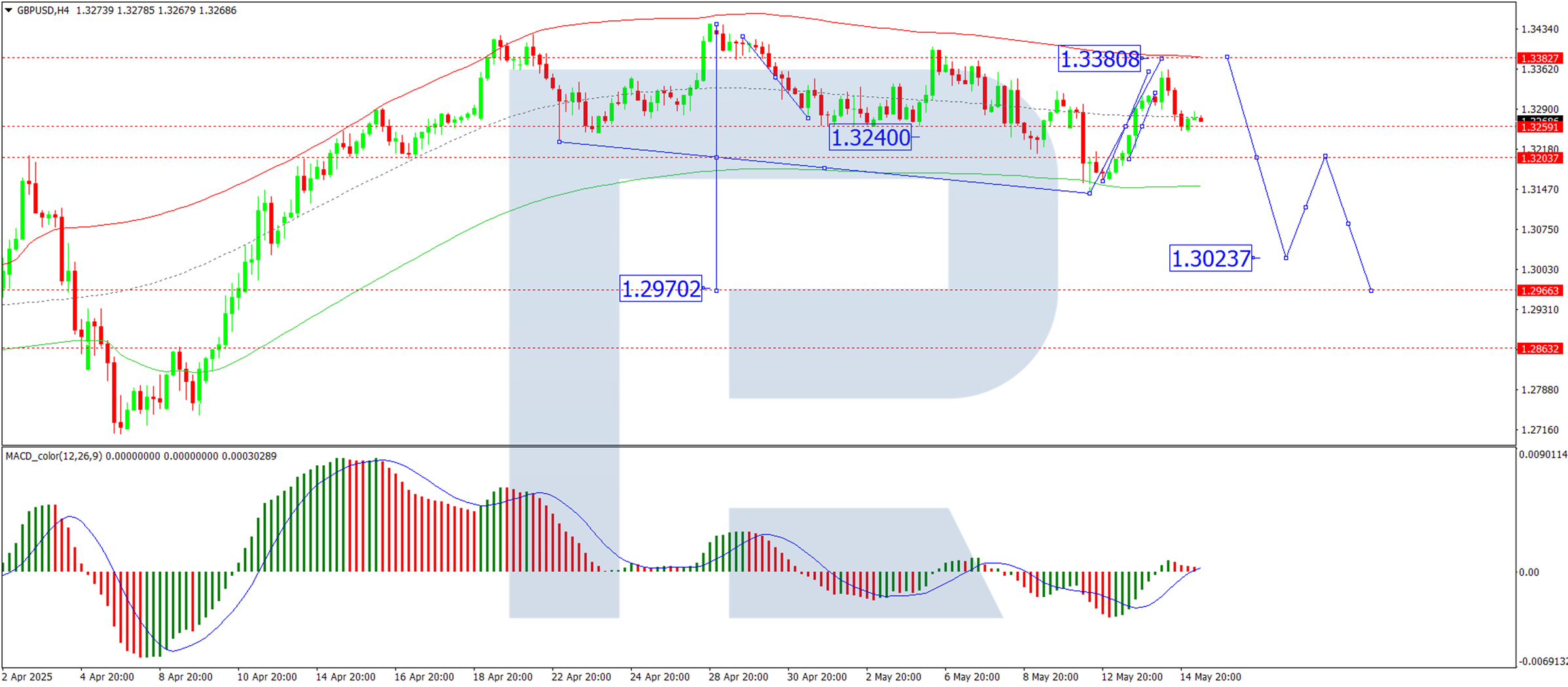

H4 Chart:

- The pair continues to trade within a broad consolidation range around 1.3260

- The current range extends to 1.3360, with a technical pullback to 1.3260 (testing from above) now underway

- A drop towards 1.3200 is anticipated. A break below this level could extend the downtrend to 1.3100, potentially stretching further to 1.3030

- This bearish outlook is supported by the MACD indicator, whose signal line remains above zero but is trending sharply upward

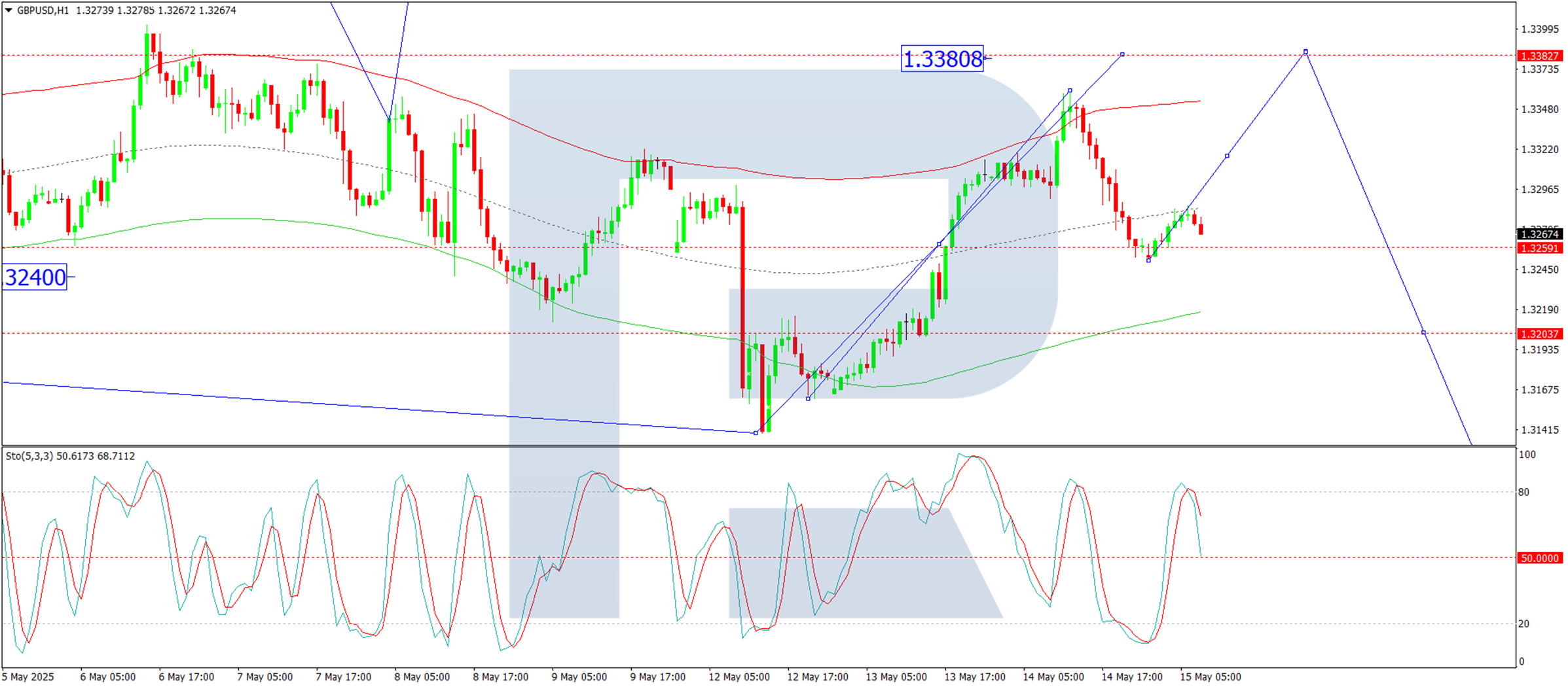

H1 Chart:

- The pair broke above 1.3260, reaching the local upside target of 1.3360

- Today’s corrective decline is testing 1.3260 again

- A renewed upward move towards 1.3380 is possible if support holds

- The Stochastic oscillator aligns with this scenario, with its signal line above 50 and rising towards 80

Conclusion

The GBP/USD remains in a holding pattern, awaiting fresh catalysts for a decisive move. While technical indicators suggest near-term volatility, the broader trend hinges on BoE policy signals and global risk sentiment. Traders should watch for a breakout beyond 1.3360 or a drop below 1.3200 for clearer directional bias.