Sample Category Title

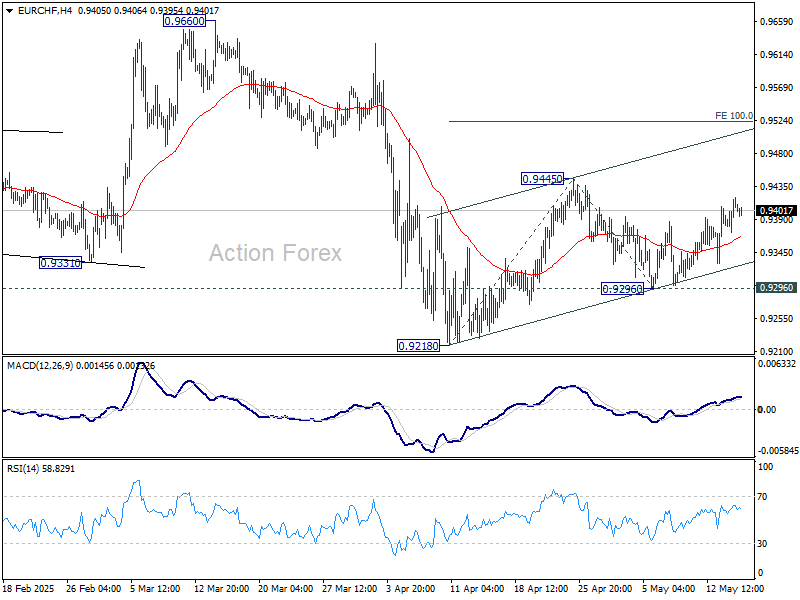

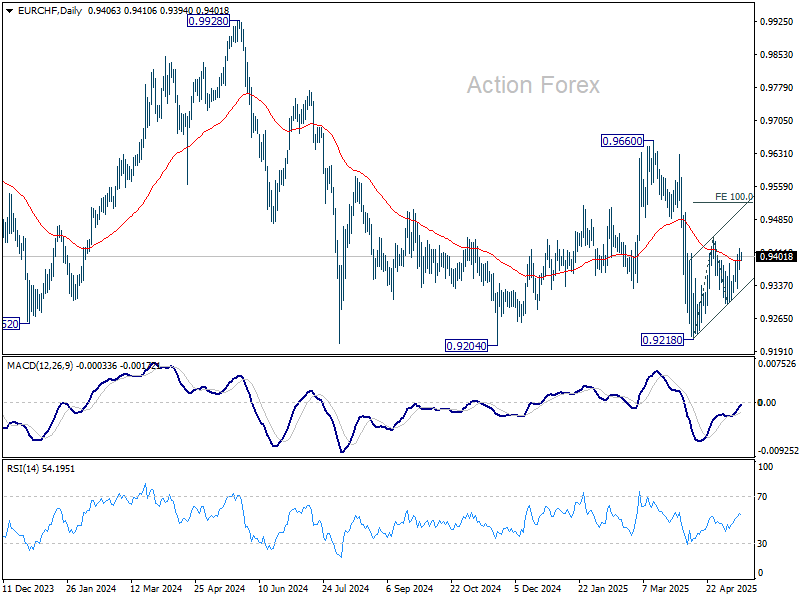

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9382; (P) 0.9402; (R1) 0.9430; More....

Intraday bias in EUR/CHF remains neutral for the moment. Outlook is unchanged that rebound from 0.9218 is either as a corrective move or the third leg of the pattern from 0.9204. On the upside, break of 0.9445 will target 100% projection of 0.9218 to 0.9445 from 0.9296 at 0.9523. Nevertheless, break of 0.9296 support will bring retest of 0.9204/18 support zone.

In the bigger picture, prior rejection by long-term falling channel resistance (now at 0.9548) retains medium term bearishness. That is, down trend from 1.2004 (2018 high) is still in progress. Firm break of 0.9204 (2024 low) will confirm resumption. This will remain the favored case as long as 0.9660 resistance holds.

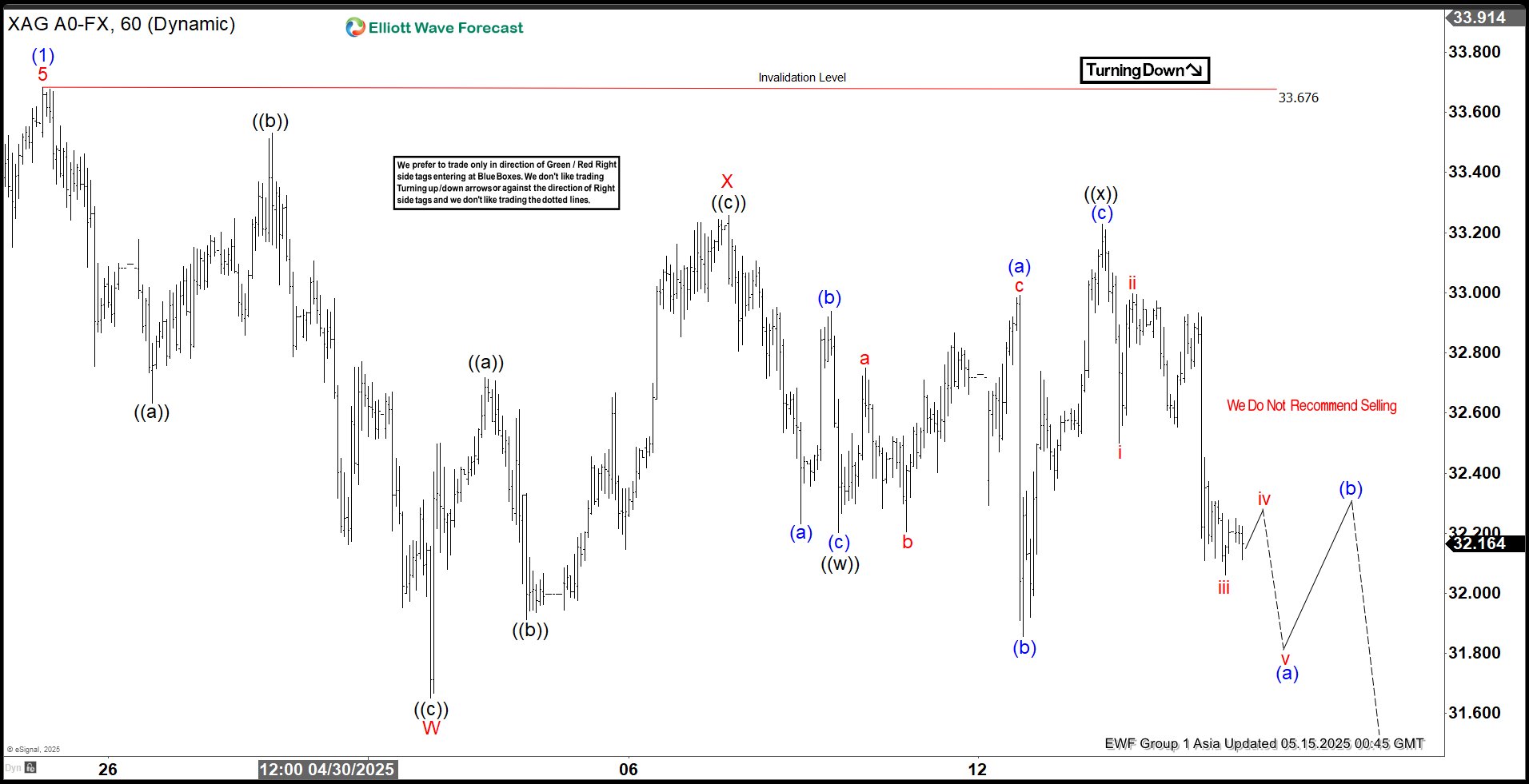

Elliott Wave Analysis: Silver (XAGUSD) Dip Anticipated to Spark Buyer Activity

Silver’s rally from its July 4, 2025, low has unfolded as an impulsive Elliott Wave structure, completing Wave (1) at $33.67. The metal is now in a corrective Wave (2) pullback. It is characterized by a double three Elliott Wave pattern, a common corrective formation in technical analysis. From the Wave (1) peak, Wave ((a)) declined to $32.63, followed by a recovery in Wave ((b)) to $33.53. The subsequent drop in Wave ((c)) reached $31.65, finalizing Wave W of the double three structure.

A corrective rally then formed Wave X, structured as a zigzag. Within Wave X, Wave ((a)) advanced to $32.70, Wave ((b)) pulled back to $31.91, and Wave ((c)) rose to $33.25, completing Wave X at a higher degree. Silver has since resumed its decline in Wave Y. From the Wave X high, Wave ((w)) fell to $32.20, and a minor recovery in Wave ((x)) hit $33.23. As long as Silver stays below the Wave (1) high of $33.67, further downside is expected, targeting $29.90–$31.18, based on the 100%–161.8% Fibonacci extension from the April 25, 2025, high. This range may attract buyers, potentially sparking a reversal. While the $33.67 pivot holds, rallies are likely to fail in 3, 7, or 11-swing patterns, leading to further declines. Traders should watch these levels for strategic entry points.

Silver (XAGUSD) 60-Minute Elliott Wave Technical Chart

Silver hourly chart showing current wave structure with projected targets and critical support

Video Breakdown: Silver Technical Outlook

https://www.youtube.com/watch?v=ms1yjvPLXbk

Chip Stocks Extend Rally Despite Waning Appetite

The news of fresh deals is coming in from the Middle East as Donald Trump seems very successful in getting the oil- and gas-rich countries to buy stuff from the US – including chips and planes – but appetite for trade optimism is starting to show signs of exhaustion. Despite the announcement of a $243bn deal with Qatar on top of the $600bn deal with Saudi Arabia, the S&P500 traded flat on Wednesday.

Big Tech stocks, including Nvidia and AMD, continued their rally at full speed – with Nvidia adding another 4% and AMD another 4.70%. Super Micro Computer jumped 15% yesterday on the announcement of a multi-year partnership agreement with Saudi Arabian DataVolt, and CoreWeave – the new AI play in town backed by Nvidia, remember – jumped to the highest levels since its IPO after announcing a 420% revenue growth in Q1.

In summary, the latest news and reports – and the market reaction – cement the idea that AI is a developing story that had remained in the dust but continues to attract funds as the dust settles. But sentiment elsewhere is waning. Gains at Meta remained limited to 0.51%, and Apple couldn’t extend gains – even on the news that it is bringing a technology that will allow us to scroll with our eyes in its new headsets. The stock price fell 0.28% yesterday, while Amazon retreated 0.53% on lingering worries that the trade war is still on, that the 30% tariffs on Chinese goods remain high, and there has been little-to-no progress with the EU.

What now?

Trade optimism is waning despite encouraging de-escalation with China and actual trade deals with the Middle East. Although the latter gives support to some industries – and I’m also looking at you, Boeing – looming uncertainties remain on the back of investors’ minds, and the narrative of a slowing US economy with rising price pressures remains the base theme. The US dollar remains under pressure from a soft economic outlook.

An avalanche of economic data will be in focus today. Among them, we will closely watch the April retail sales, the evolution of producer prices for the same month, the Philly Fed and NY Empire manufacturing data, and, of course, the weekly jobless figures.

Softer sales and activity figures would normally boost the Federal Reserve (Fed) doves, pull yields lower, and support equities (a typical ‘the good news is bad news’ reaction). But given the rising US inflation expectations, weak sales and manufacturing data would rather increase stagflation bets. Therefore, good news would be good news for the market, cementing the resilience of the US economy, whereas soft economic data would be bad news for risk appetite and could stall the rally.

Note that small- and mid-cap stocks are more sensitive to US yields – so despite bets that they could play catch-up with large-cap indices, the strength of US yields will certainly be a barrier to a strong rally.

Now moving to China

Tencent announced slightly better-than-expected revenue in Q1. Its net profit grew 82% compared to the same period last year – but still fell short of analyst expectations – while the company announced a $6.7bn stock buyback and plans to invest double-digit amounts into AI. The last bit is important for tech investors. The company spent $4bn on AI last quarter – up more than 90% from a year ago – and will continue to do so.

Tencent’s share price has been rebounding since last year, though the rebound has been bumpy with periods of hesitation and selloffs. But about two-thirds of the post-2021 crackdown losses have been recovered, and AI should help the company aim for fresh highs, especially since Tencent remains cheap – very cheap – compared to its American peers. Its P/E ratio is just around 22.

Speaking of earnings, Alibaba will announce its own results later today, and the focus will be on AI and cloud revenues. Note that Alibaba has been slower to recover from the post-crackdown losses, having only regained about a third of the 2020–2022 decline. But among Chinese tech stocks, it's probably the most promising when it comes to AI. Not only does the company develop its own language models and offer cloud services, but it also has a very large e-commerce platform, financial services where it could apply its models, and a huge amount of data in hand to fine-tune its technology to its needs. And the stock is trading at a P/E ratio of around 21.

All in all, the Chinese AI story is developing. It’s helping Chinese tech companies extend their rally, even though the rallies are interrupted by hesitation and trade worries. The fact that China cannot afford to miss the technology rally – and signs that they can still innovate despite chip restrictions – means that China could gain technological independence. I believe that’s the ultimate goal, which would then make Chinese tech stocks an excellent diversification opportunity for investors willing to stomach Chinese regime risk.

At the same time, politics across the Pacific are looking much shakier for the next 3.5 years...

In energy

The news that Iran is ready to curtail its nuclear program in exchange for sanctions relief is weighing on oil prices for the second session. The barrel of US crude eased below the $61.50/bbl level this morning on the back of rising Iranian supply prospects – which add to OPEC’s oil restoration plans – versus a fragile improvement in demand prospects.

From a technical perspective, oil remains in a bearish trend with solid resistance seen at the 50-DMA near $64.20 and the major 38.2% Fibonacci retracement on the YTD decline at the $65.30 mark. Note that Goldman Sachs suggests Trump wants oil at the $40–50 level. He’ll likely get what he wants in the second half of the year.

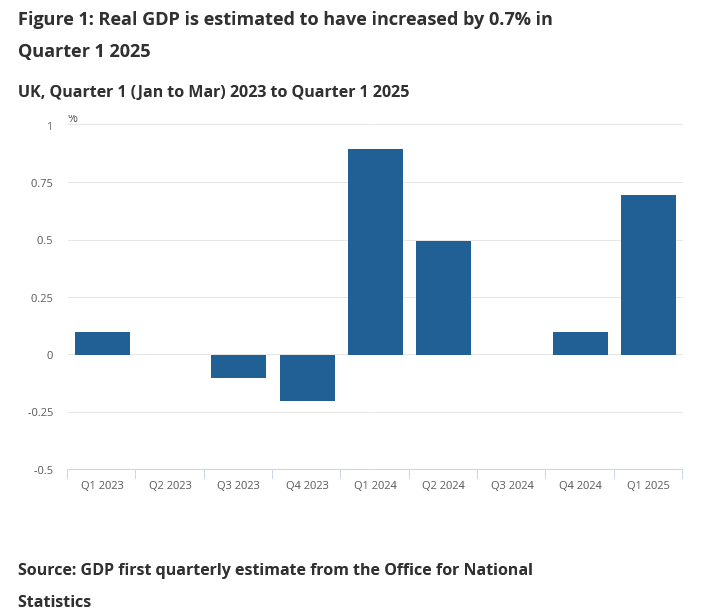

UK economy beats expectations with 0.7% qoq growth in Q1, 0.2% mom in March

The UK economy expanded by 0.7% qoq in Q1, slightly ahead of expectations at 0.6% qoq. Growth was led by a 0.7% qoq rise in the services sector and a robust 1.1% qoq increase in production output, while construction activity was flat. Importantly, real GDP per head also rose by 0.5% qoq, ending two consecutive quarters of contraction.

On the expenditure side, growth was underpinned by a 2.9% qoq rise in gross fixed capital formation, signaling strong business investment. Household consumption also edged up by 0.2% qoq, while net trade contributed positively as exports rose by 3.5% qoq and imports by 2.1% qoq.

Monthly data for March further supported the upbeat quarterly reading, with GDP rising by 0.2% mom, exceeding expectations of flat growth. Services output was the standout, rising 0.4% mom and contributing the most to overall GDP expansion. Meanwhile, construction rose by 0.5% mom, offsetting a -0.7% mom decline in production output.

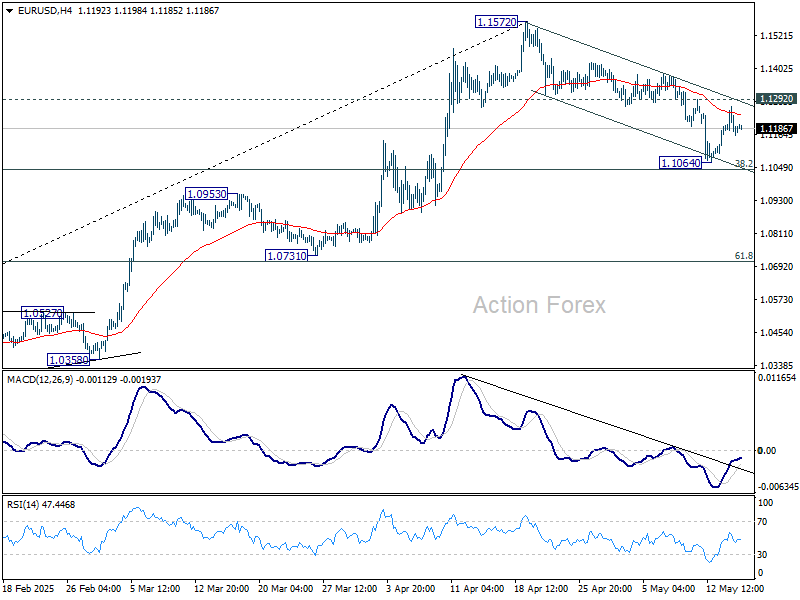

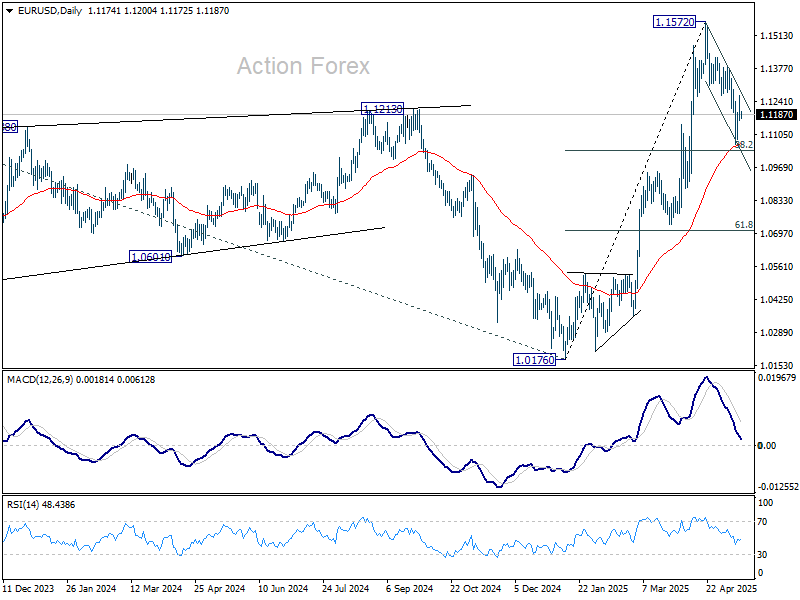

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1136; (P) 1.1201; (R1) 1.1238; More...

Intraday bias in EUR/USD remains neutral for the moment. On the upside, break of 1.1292 resistance will argue that correction from 1.1572 has completed after defending 38.2% retracement of 1.0176 to 1.1572 at 1.1039. Intraday bias will be back on the upside for retesting 1.1572. However, sustained break of 1.1039 will dampen this view and target 61.8% retracement at 1.0709 next.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0789) holds.

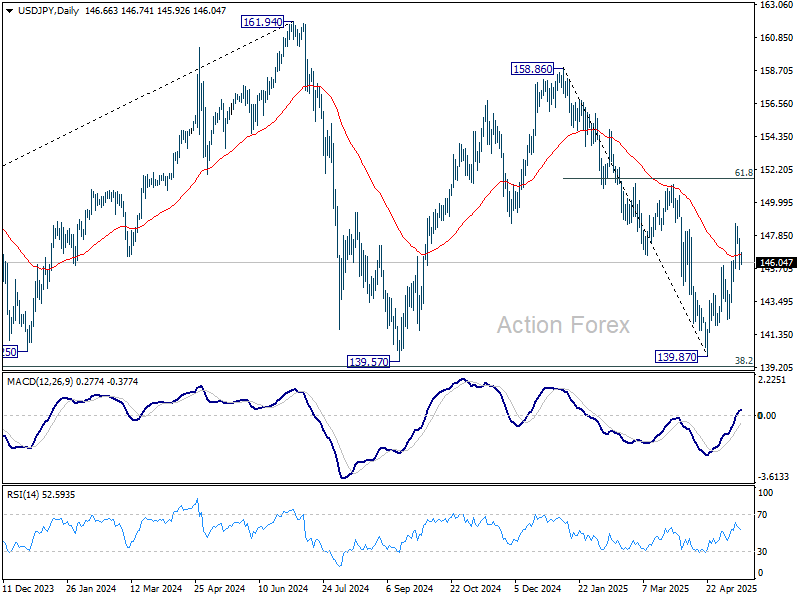

USD/JPY Daily Outlook

Daily Pivots: (S1) 145.68; (P) 146.68; (R1) 147.74; More...

Intraday bias in USD/JPY remains neutral at this point. Further rally is expected as long as 144.02 resistance turned support holds. As noted before, fall from 158.86 could have completed 139.87 already. Above 148.64 will target 61.8% retracement of 158.86 to 139.87 at 151.60 next. However, firm break of 144.02 will bring retest of 139.87 low instead.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

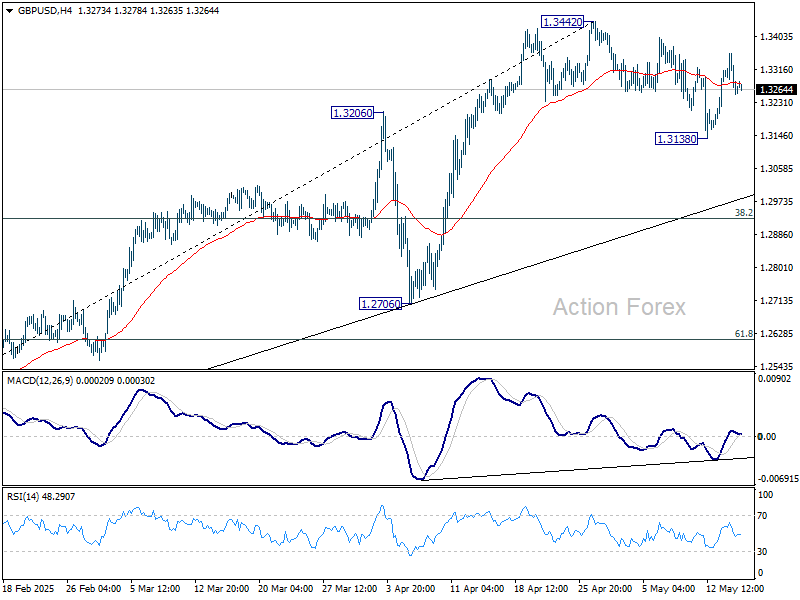

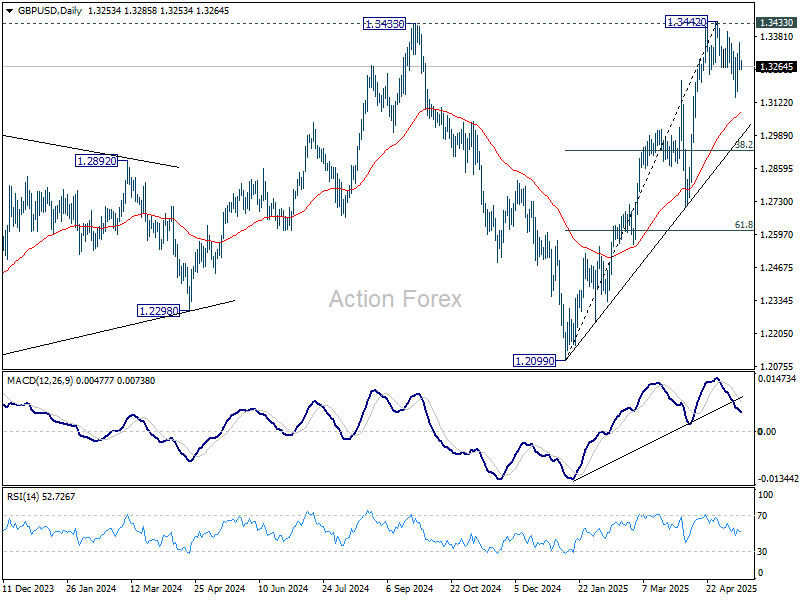

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3225; (P) 1.3292; (R1) 1.3331; More...

Intraday bias in GBP/USD is turned neutral first with current retreat. The view is unchanged that correction from 1.3442 might have completed at 1.3138 already. Decisive break of 1.3433/42 key resistance zone will confirm larger up trend resumption. Nevertheless, below 1.3138 will resume the correction. But downside should be contained by 38.2% retracement of 1.2099 to 1.3442 at 1.2929 to bring rebound.

In the bigger picture, price actions from 1.3433 are seen as a corrective pattern to the up trend from 1.3051 (2022 low). Rise from 1.2099 could either be resuming the up trend, or the second leg of a consolidation pattern. Overall, GBP/USD should target 1.4248 key resistance (2021 high) on decisive break of 1.3433 at a later stage.

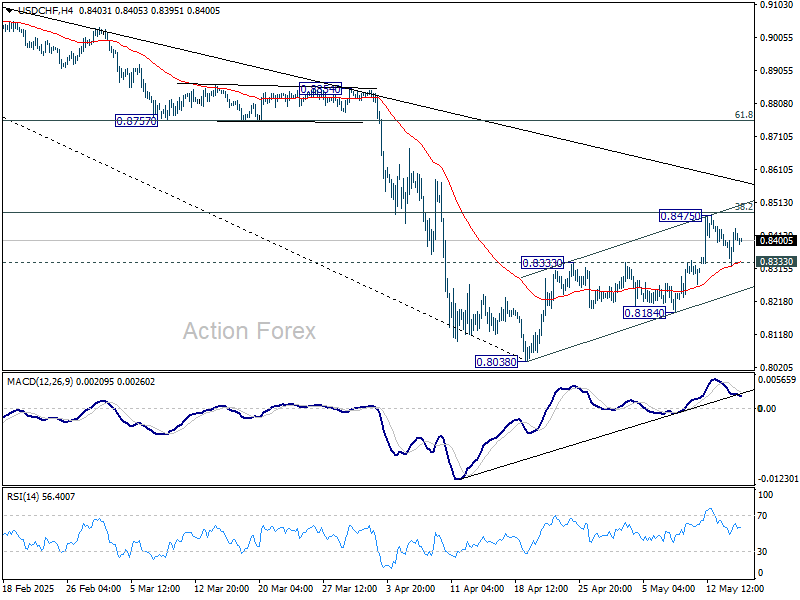

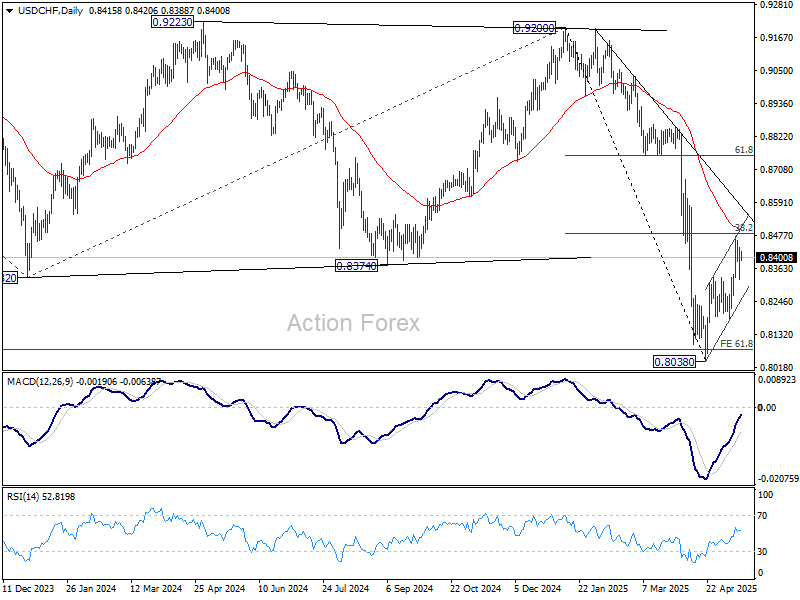

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8352; (P) 0.8394; (R1) 0.8463; More….

Intraday bias in USD/CHF stays neutral at this point. On the downside, firm break of 0.8333 resistance turned support will argue that corrective rebound from 0.8038 has completed at 0.8475, after rejection by 38.2% retracement of 0.9200 to 0.8038 at 0.8482. Intraday bias will be back on the downside for 0.8184, and then retest of 0.8038 low. However, sustained trading above 0.8482 will dampen this bearish view and target 61.8% retracement at 0.8756 next.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress and met 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.8079 already. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8750) holds. Sustained break of 0.8079 will target 100% projection at 0.7382.

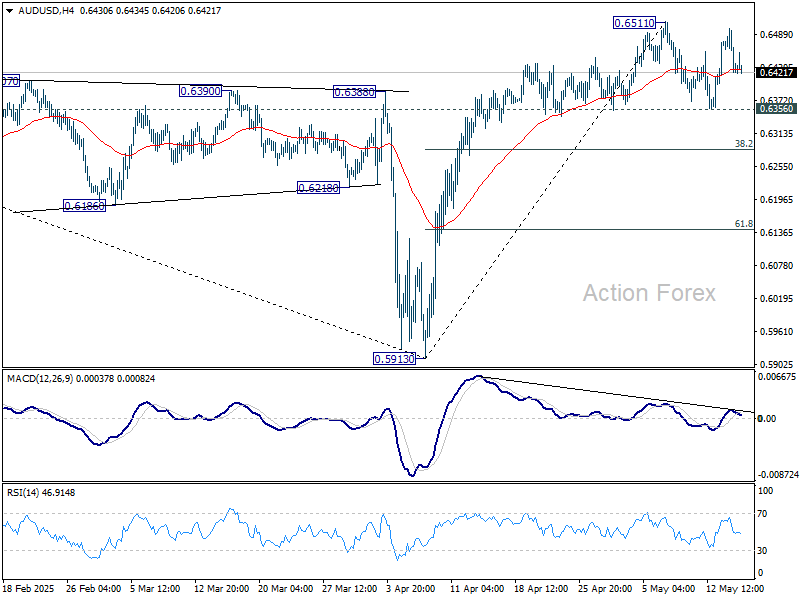

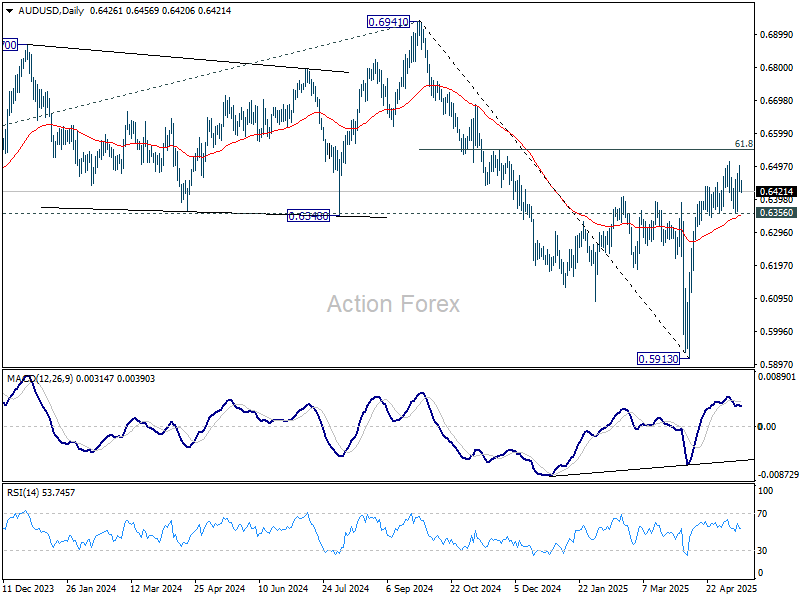

AUD/USD Daily Report

Daily Pivots: (S1) 0.6400; (P) 0.6451; (R1) 0.6478; More...

Range trading continues in AUD/USD and intraday bias stays neutral at this point. On the upside, firm break of 0.6511 will resume the rally from 0.5913 to 61.8% retracement of 0.6941 to 0.5913 at 0.6548. However, break of 0.6356 will bring deeper pullback to 38.2% retracement of 0.5913 to 0.6511 at 0.6283.

In the bigger picture, as long as 55 W EMA (now at 0.6441) holds, down trend from 0.8006 (2021 high) should resume later to 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. However, sustained trading above 55 W EMA will argue that a medium term bottom was already formed, and set up further rebound to 0.6941 resistance instead.

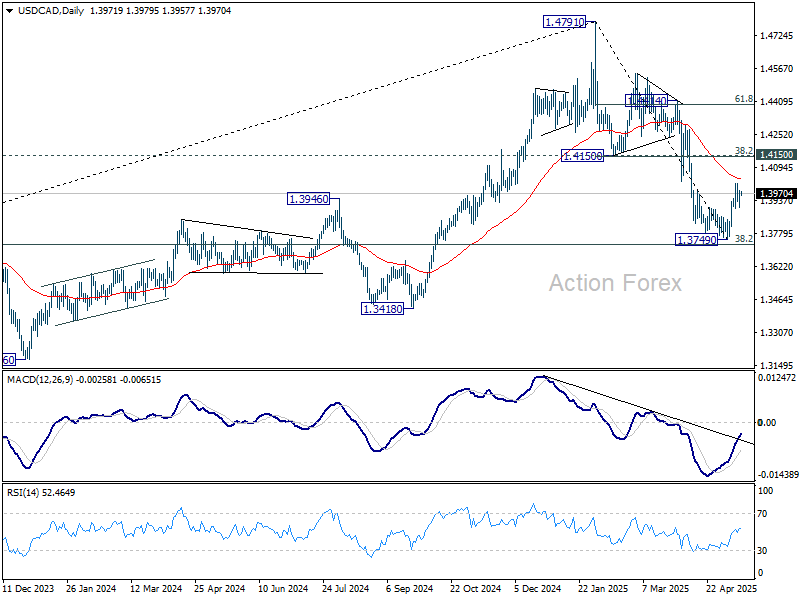

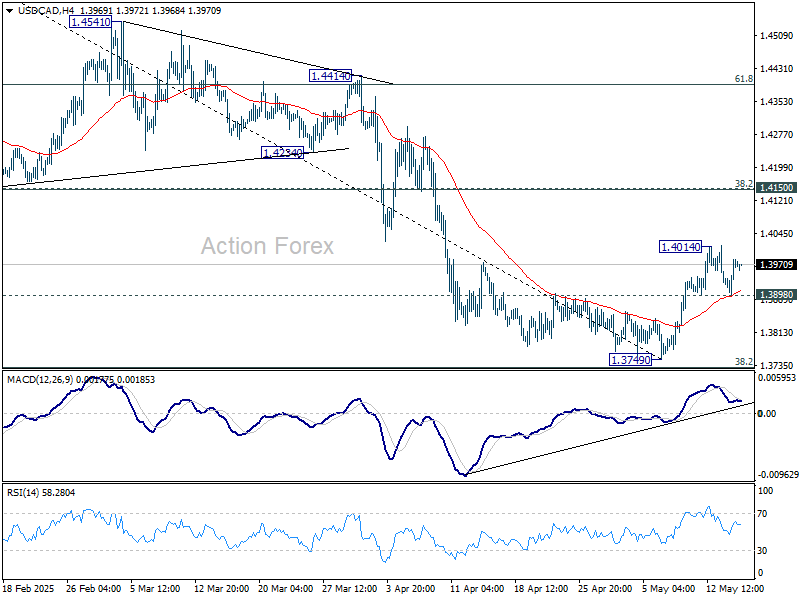

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3928; (P) 1.3957; (R1) 1.4012; More...

Intraday bias in USD/CAD remains neutral for the moment. Further rise is in favor with 1.3898 minor support intact. Above 1.4014 will resume the rebound from 1.3749 to 1.4150 cluster resistance (38.2% retracement of 1.4791 to 1.3749 at 1.4147). However, break of 1.3898 minor support will indicate that the rebound has completed, and bring retest of 1.3749.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4150 resistance turned support holds. Firm break of 38.2% retracement of 1.2005 (2021 low) to 1.4791 at 1.3727 will pave the way back to 61.8% retracement at 1.3069.