Sample Category Title

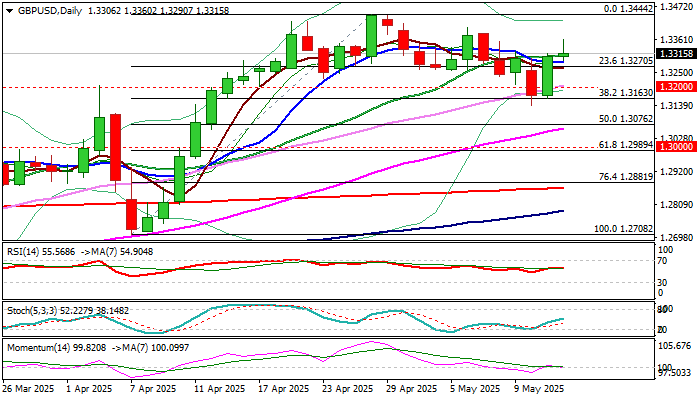

GBP/USD: Bulls Hold Grip Ahead of UK GDP Data

Cable keeps firm near term tone and extends recovery after Tuesday’s 1% rally generated positive signal on over 50% retracement of 1.3444/1.3139 pullback and completion of bullish engulfing pattern on daily chart.

Fresh extension higher on Wednesday rose above Fibo 61.8% retracement that adds to development of reversal signal, after strong bounce on Tuesday signaled that corrective phase from new 2025 high (1.3444) is likely over.

Formation of bear-trap under Fibo 38.2% of 1.3444/1.3139 contributes to positive near-term outlook, along with predominantly bullish daily studies.

Traders focus on tomorrow’s releases of UK GDP data, with expectations for 0.6% growth in Q1 being significantly above 0.1% growth in the first three months of 2024, although economists see flat growth in March compared to 0.5% expansion in the previous month.

Sterling would benefit from better than expected GDP data that would also ease pressure on BOE to cut rates again in June (bets for June cut have dropped significantly after May’s hawkish cut).

Also, a trade deal with the US would ease uncertainty and improve economic situation on removing one of major obstacles for economic growth.

Res: 1.3360; 1.3402; 1.3444; 1.3500.

Sup: 1.3270; 1.3232; 1.3200; 1.3162.

Yen Posts Sharp Gains as PPI Hit 4 Percent

The Japanese yen has posted strong gains for a second straight day. In the North American session, USD/JPY is trading at 146.32, down 0.79% on the day. The yen plunged 2.1% on Monday but has now recovered those losses.

Japan's PPI eases slightly to 4%

Wholesale inflation in Japan remained high, rising 4% y/y in April. This was slightly lower than the revised 4.2% gain in March and was in line with expectations. This is the fourth straight month that PPI has been at 4% or higher, as companies continued to pass on costs to consumers. Food prices have been rising, led by rice prices which have doubled over the past 12 months.

The Bank of Japan has been carefully monitoring inflationary pressures as it looks to continue hiking interest rates on the path to monetary normalization. The BoJ raised rates in January but has stayed on the sidelines since then and is in a wait-and-see mode until there is more clarity about President Trump's tariff policy. The Bank meets next on June 17.

The 90-day tariff deal between the US and China has raised hopes that Trump will reach trade deals with China and other countries. Japan sends 20% of its exports to the US, which is Japan's largest trading partner and trade talks are underway between the two countries.

Fed in a wait-and-see mode

The US inflation report was particularly important as Trump's tariffs took effect on many products in April. Inflation rose in April but was lower than expected. The full impact of the tariffs, which could send inflation lower, may not be seen until June or July.

The Federal Reserve is also in a wait-and-see mode. At last week's Fed meeting, Fed Chair Powell pushed back against Trump, who has called for the Fed to lower rates. The Fed is widely expected to hold rates at the June 18 meeting.

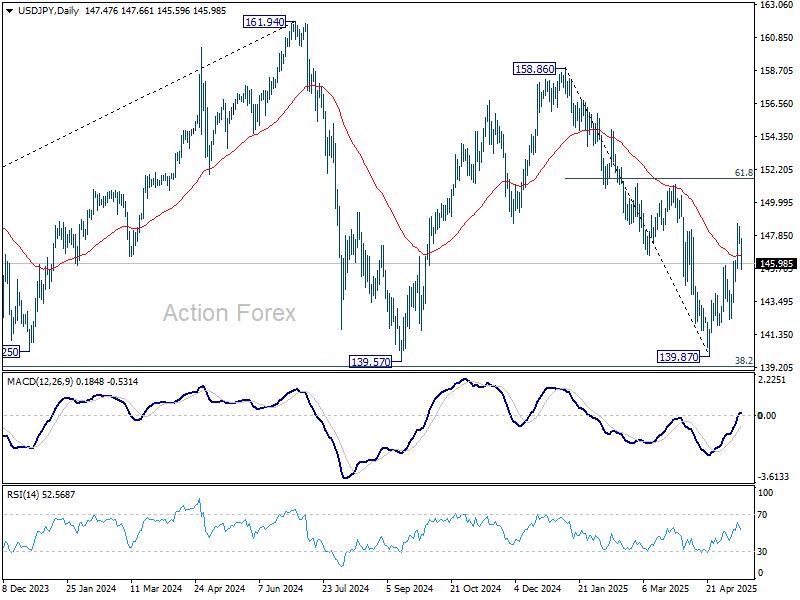

USD/JPY Technical

- USD/JPY has pushed below support at 147.06 and 146.64. The next support level is 145.91

- 147.79 and 148.21 are the next resistance lines

USDJPY 1-Day Chart, May 14, 2025

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3202; (P) 1.3259; (R1) 1.3363; More...

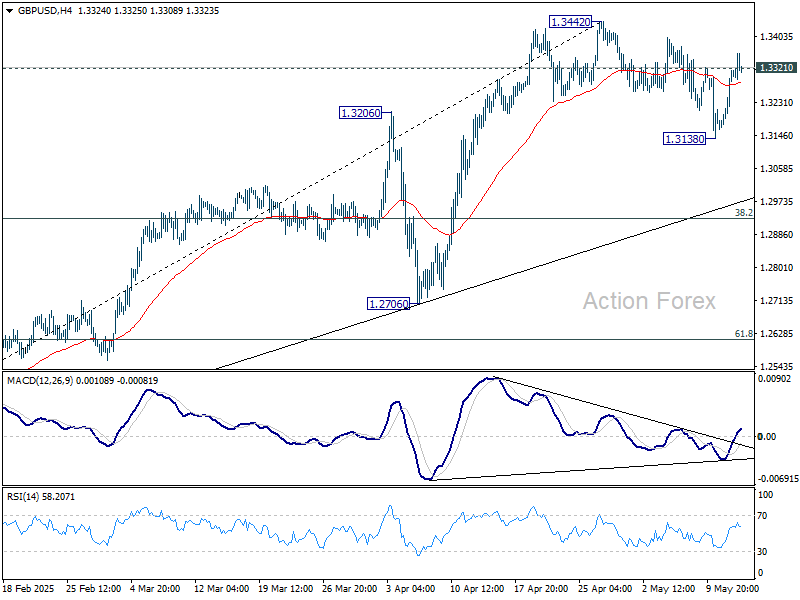

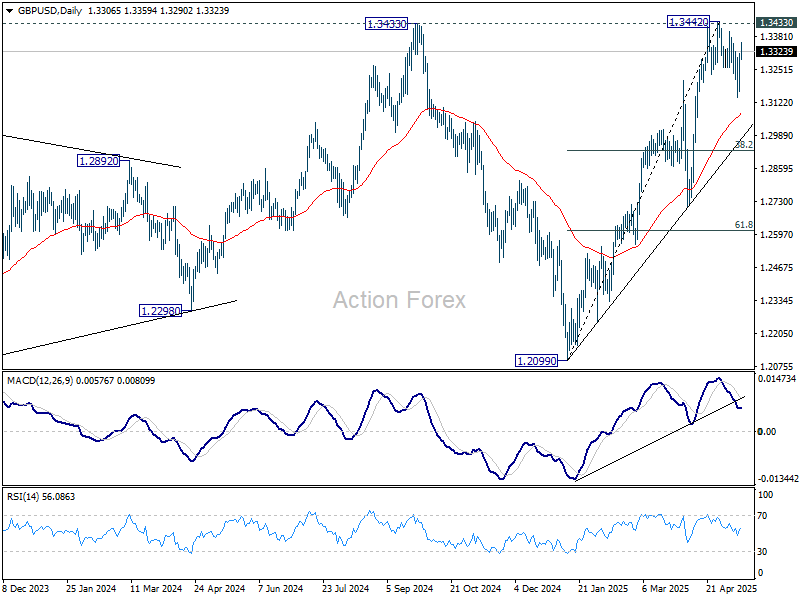

GBP/USD's correction from 1.3442 might have completed at 1.3138 already. Intraday bias is back on the upside. Decisive break of 1.3433/42 key resistance zone will confirm larger up trend resumption. Nevertheless, below 1.3138 will resume the correction. But downside should be contained by 38.2% retracement of 1.2099 to 1.3442 at 1.2929 to bring rebound.

In the bigger picture, price actions from 1.3433 are seen as a corrective pattern to the up trend from 1.3051 (2022 low). Rise from 1.2099 could either be resuming the up trend, or the second leg of a consolidation pattern. Overall, GBP/USD should target 1.4248 key resistance (2021 high) on decisive break of 1.3433 at a later stage.

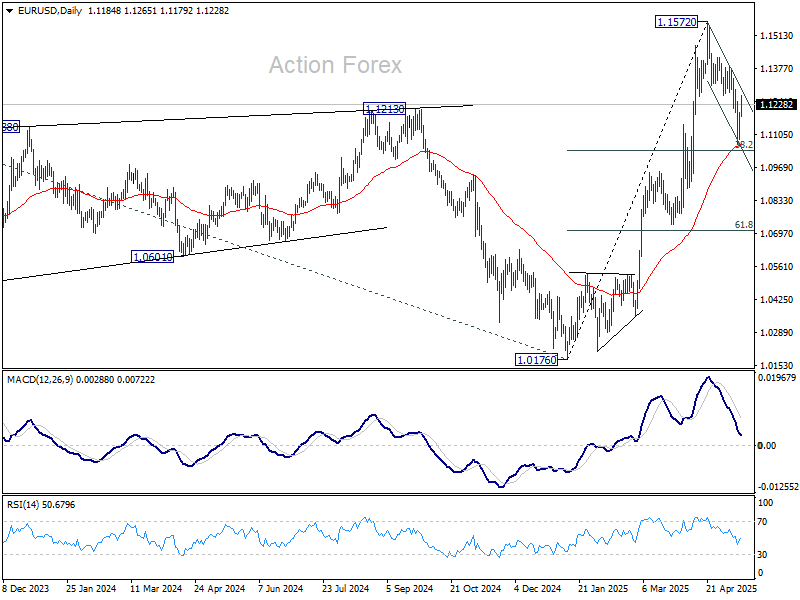

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1114; (P) 1.1155; (R1) 1.1225; More...

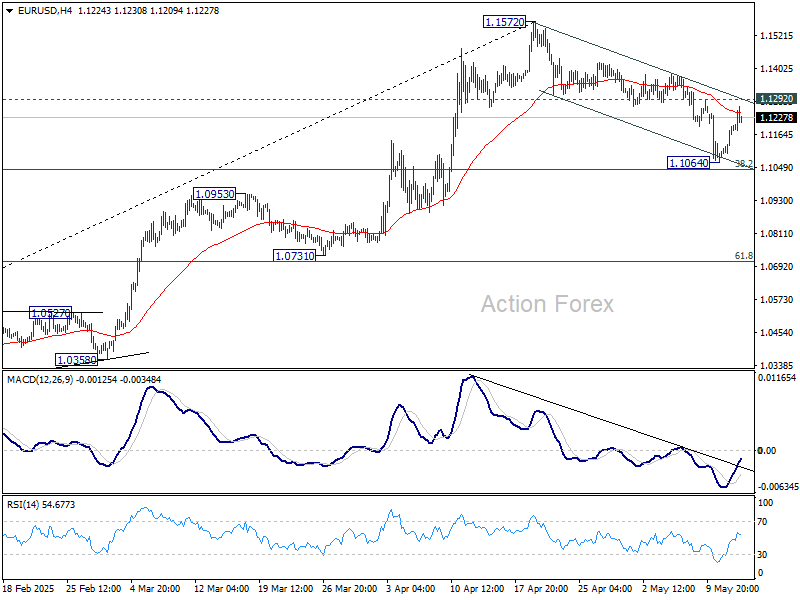

Intraday bias in EUR/USD stays neutral at this point. On the upside, break of 1.1292 resistance will argue that correction from 1.1572 has completed after defending 38.2% retracement of 1.0176 to 1.1572 at 1.1039. Intraday bias will be back on the upside for retesting 1.1572. However, sustained break of 1.1039 will dampen this view and target 61.8% retracement at 1.0709 next.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0789) holds.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 147.06; (P) 147.79; (R1) 148.21; More...

Intraday bias in USD/JPY remains neutral for the moment. Further rally is expected as long as 142.43 support holds. As noted before, fall from 158.86 could have completed 139.87 already. Above 148.64 will target 61.8% retracement of 158.86 to 139.87 at 151.60 next.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

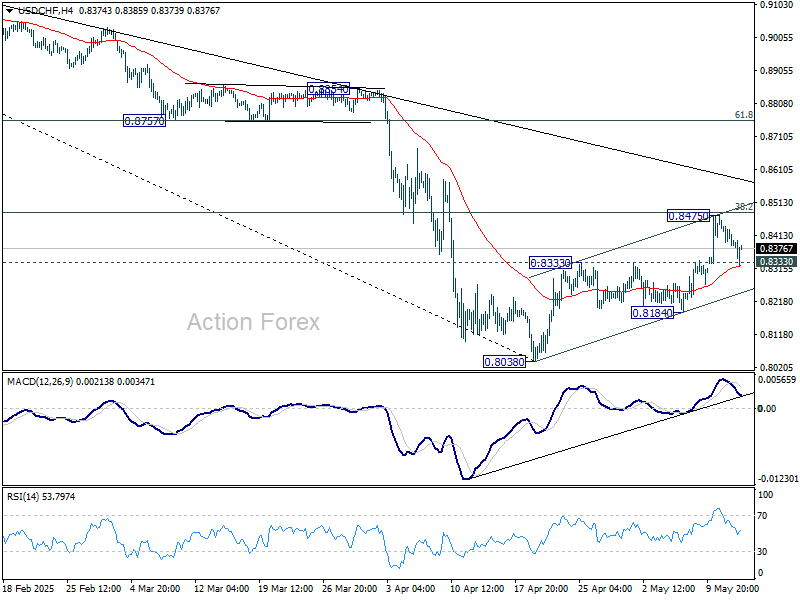

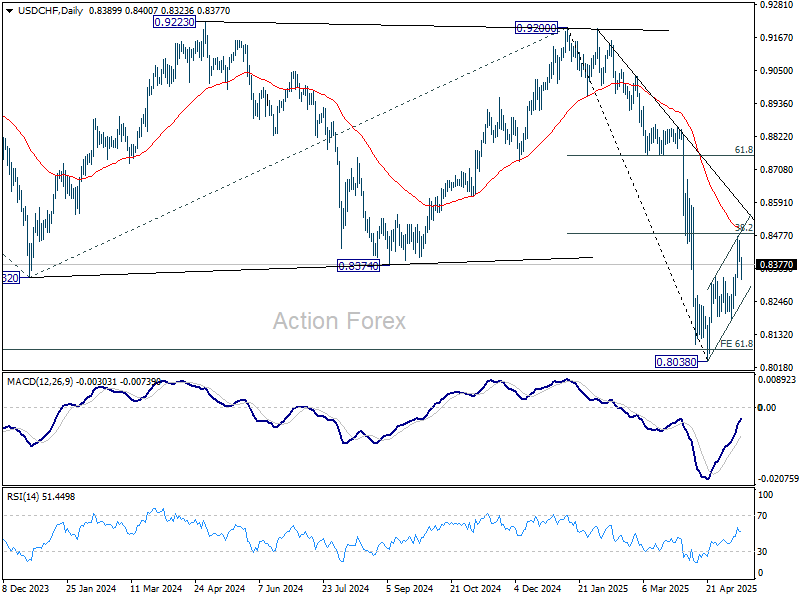

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8367; (P) 0.8415; (R1) 0.8442; More….

Intraday bias in USD/CHF remains neutral for the moment. On the downside, firm break of 0.8333 resistance turned support will argue that corrective rebound from 0.8038 has completed at 0.8475, after rejection by 38.2% retracement of 0.9200 to 0.8038 at 0.8482. Intraday bias will be back on the downside for 0.8184, and then retest of 0.8038 low. However, sustained trading above 0.8482 will dampen this bearish view and target 61.8% retracement at 0.8756 next.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress and met 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.8079 already. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8750) holds. Sustained break of 0.8079 will target 100% projection at 0.7382.

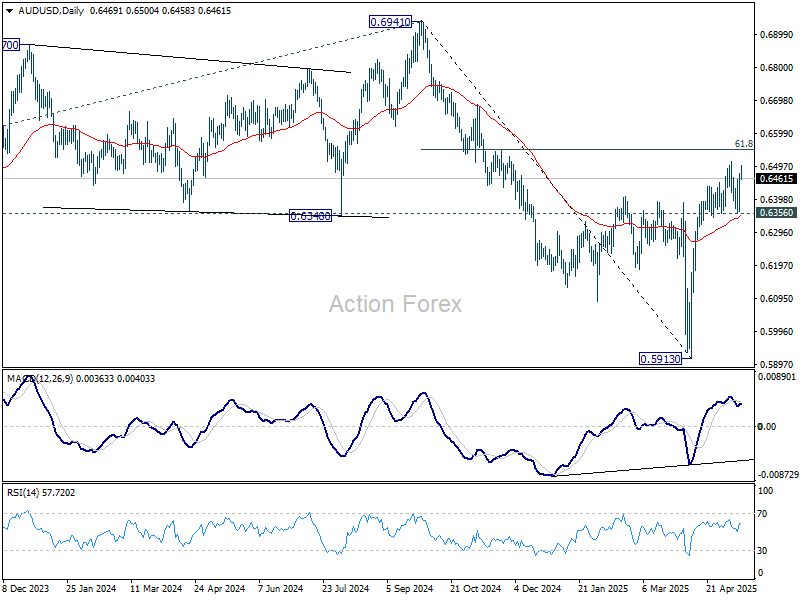

Dollar Steadies After Early Weakness, Focus Turns to Australia Jobs Data

Dollar faced broad selling pressure throughout the Asian and European sessions but has since found some footing as markets transition into the US trading day. However, direction remains murky, with traders appearing undecided on whether to push the greenback higher or extend the recent pullback. A similar tone of uncertainty is mirrored in equities, as European indexes drift sideways and US futures show little conviction. With no major catalysts in the immediate pipeline, both FX and equity markets are likely to stay range-bound until fresh data offers clearer cues.

Attention now turns to Thursday’s key releases, including Australia’s April employment report and the UK’s GDP figures. While Australia’s stronger-than-expected Q1 wage price index suggested some resilience in pay growth, the detail showed continued moderation in the private sector. This is unlikely to derail RBA's expected rate cut next week, as the central bank remains focused on cushioning the economy from tariff-related risks. The upcoming April employment data will be more telling—especially if it deviates significantly from the expected 20.9k job growth and 4.1% unemployment rate. A downside surprise could fuel speculation of faster easing later this year.

Technically, AUD/USD has struggled to establish momentum, despite a supportive risk-on backdrop. Even if a short-term rally resumes, 61.8% retracement of 0.6941 to 0.5913 at 0.6548 is likely to provide strong resistance to bring at least a near term pullback.

In Europe, at the time of writing, FTSE is up 0.09%. DAX is down -0.18%. CAC is down -0.29%. UK 10-year yield is up 0.039 at 4.715. Germany 10-year yield is up 0.005 at 2.686. Earlier in Asia, Nikkei fell -0.14%. Hong Kong HSI rose 2.30%. China Shanghai SSE rose 0.86%. Singapore Strait Times fell -0.26%. Japan 10-year JGB yield rose 0.008 to 1.457.

Fed’s Goolsbee urges patience amid ‘dusty’ data and tariff uncertainty

Chicago Fed President Austan Goolsbee cautioned against overinterpreting April’s softer inflation data, noting on NPR that it’s still too early to gauge the true impact of rising US import tariffs.

While recent consumer price figures suggest inflation may be easing, Goolsbee stressed that Fed needs more clarity before making firm policy judgments, describing the current environment as one filled with “a lot of dust in the air.”

He acknowledged that the data so far “suggest that it’s going okay,” but emphasized the difficulty of drawing long-term conclusions amid ongoing short-term volatility.

“It’s just not realistic,” he said, “to expect businesses or central banks to be jumping to conclusions” in such an uncertain setting.

ECB’s Nagel stresses Dollar’s global role, cautious on tariff impact ahead of June decision

German ECB Governing Council member Joachim Nagel emphasized the continued importance of the Dollar as a global reserve currency during remarks today. At the same time, he expected that Euro would gradually play a stronger role in the international financial system over the coming years.

Looking ahead to ECB’s June policy meeting, Nagel reiterated that the interest rate decision will be guided by incoming data. He acknowledged the uncertainty surrounding the impact of US tariffs on inflation and growth within the Eurozone.

The updated ECB staff projections, due next month, would be essential in shaping the decision. Nagel also stressed that central banks must increasingly adapt to operating in an environment characterized by persistent geopolitical and policy-driven uncertainty.

BoE hawk Mann: Labor market resilient, and firms yet to lose pricing power

BoE MPC member Catherine Mann explained her notable policy shift during an interview with CNBC, revealing why she moved from backing a 50bps rate cut in February to voting for a hold at last week’s meeting.

Mann cited the UK labor market’s resilience as a key factor in her reassessment. While recent data suggest some moderation "a slowing labor market", she argued that "it is not a non-linear adjustment."

Mann also flagged a new risk emerging from tariffs. She warned that rising US tariffs on countries like China could lead to an influx of diverted exports into markets such as the UK. While this could temporarily ease goods prices at the border, she cautioned that domestic retailers may use the opportunity to rebuild profit margins, keeping upward pressure on consumer price inflation rather than alleviating it.

Crucially, Mann emphasized the need to see a broad-based "loss of pricing power" in firms. "I need to see that firms are starting to be much more moderate in setting their prices across a broad range of products," she added. "Goods price inflation is actually going up, not down."

Japan’s PPI rises 4% yoy in April, record high for 8th straight month

Japan’s PPI rose 4.0% year-on-year in April, easing slightly from 4.3% yoy in March and matching market expectations. Despite the modest slowdown, the index climbed to a fresh record high of 126.3, marking the eighth consecutive month of new highs, highlighting persistent cost pressures at the wholesale level.

However, the data also showed little immediate impact from the sweeping US tariffs announced in early April, thanks in part to the 90-day suspension.

Japan’s Yen-based import price index fell sharply by -7.2% yoy in April, following a -2.4% yoy decline in March. The drop suggests that Yen's appreciation during the market turmoil have helped shield Japanese importers from some of the price shocks, at least for now.

Australian wage growth accelerates to 3.4% yoy in Q1, led by public sector

Australia’s Wage Price Index rose by 0.9% qoq in Q1, slightly above market expectations of 0.8% qoq. Public sector saw a stronger 1.0% qoq gain, outpacing the 0.9% qoq rise in private sector.

On an annual basis, wages grew by 3.4%, up from 3.2% in the previous quarter, marking the first uptick in annual wage growth since mid-2024.

The uptick in annual wage growth was driven primarily by the public sector, which saw a notable increase to 3.6% yoy from 2.9% yoy in Q4. Private sector wage growth was steady at 3.3% yoy.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8367; (P) 0.8415; (R1) 0.8442; More….

Intraday bias in USD/CHF remains neutral for the moment. On the downside, firm break of 0.8333 resistance turned support will argue that corrective rebound from 0.8038 has completed at 0.8475, after rejection by 38.2% retracement of 0.9200 to 0.8038 at 0.8482. Intraday bias will be back on the downside for 0.8184, and then retest of 0.8038 low. However, sustained trading above 0.8482 will dampen this bearish view and target 61.8% retracement at 0.8756 next.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress and met 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.8079 already. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8750) holds. Sustained break of 0.8079 will target 100% projection at 0.7382.

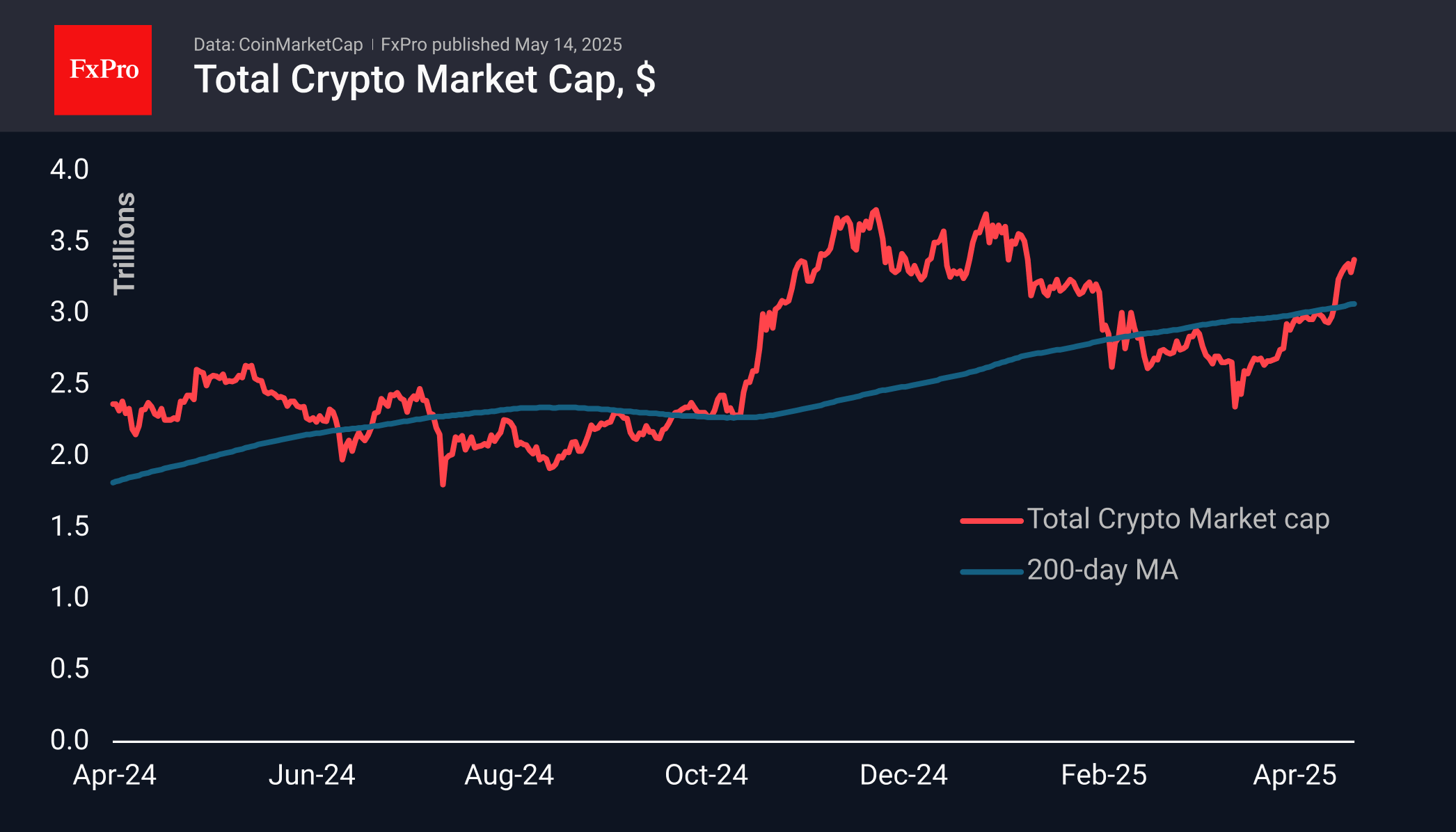

Crypto Market Grows on Altcoins

Market Picture

Market capitalisation rose 2.7% in the last 24 hours to $3.38 trillion, with the market reaching $3.40 trillion the previous evening. These are the highest values since early February, driven by increased altcoin buying.

The sentiment index reached 73, indicating that it is approaching extreme greed territory, but remains far from the overbought zone, giving the bulls reason for further gains.

Bitcoin has been hovering around the $104k level for the sixth day

Bitcoin has been hovering around the $104k level for the sixth day, experiencing increased rotation. This is quite expected behaviour as we approach the all-time highs of December and January, which served as turning points.

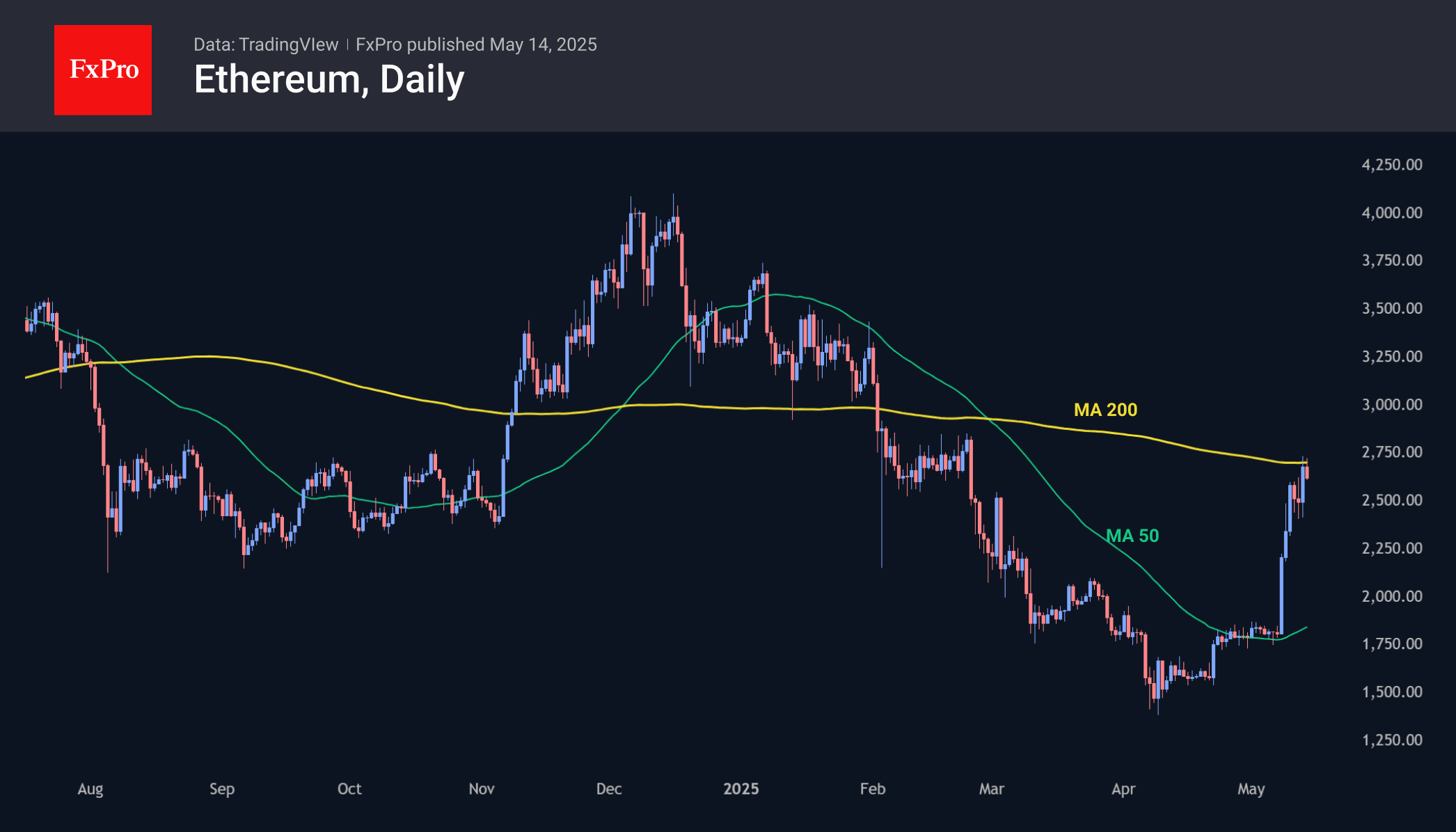

Ethereum is trading around $2615, having failed to consolidate above the $2700 mark, around which the 200-day moving average also passes. It is likely that after rallying 55% over the past seven days, the second-largest capitalised cryptocurrency will probably take a pause or start a correction with a potential target at $2400.

News Background

Bitcoin Magazine analysts point out that recent data points to a significant expansion of global liquidity (monetary aggregate M2), which historically accompanies bitcoin’s growth.

Glassnode experts note that the breakthrough of the psychological level of $100,000 has sparked interest from new bitcoin buyers, while experienced traders are cautious. According to Santiment, wallets with balances between 10 and 10,000 BTC have purchased an additional 83,105 BTC over the past 30 days.

Coinbase exchange shares will join the S&P 500 index from 19 May, replacing Discover Financial Services securities. Coinbase will become the first cryptocurrency company to be part of the U.S. broad market stock index. Bernstein estimates the new demand for the exchange’s shares from index funds to be $9bn.

Fed’s Goolsbee urges patience amid ‘dusty’ data and tariff uncertainty

Chicago Fed President Austan Goolsbee cautioned against overinterpreting April’s softer inflation data, noting on NPR that it’s still too early to gauge the true impact of rising US import tariffs.

While recent consumer price figures suggest inflation may be easing, Goolsbee stressed that Fed needs more clarity before making firm policy judgments, describing the current environment as one filled with “a lot of dust in the air.”

He acknowledged that the data so far “suggest that it’s going okay,” but emphasized the difficulty of drawing long-term conclusions amid ongoing short-term volatility.

“It’s just not realistic,” he said, “to expect businesses or central banks to be jumping to conclusions” in such an uncertain setting.

ECB’s Nagel stresses Dollar’s global role, cautious on tariff impact ahead of June decision

German ECB Governing Council member Joachim Nagel emphasized the continued importance of the Dollar as a global reserve currency during remarks today. At the same time, he expected that Euro would gradually play a stronger role in the international financial system over the coming years.

Looking ahead to ECB’s June policy meeting, Nagel reiterated that the interest rate decision will be guided by incoming data. He acknowledged the uncertainty surrounding the impact of US tariffs on inflation and growth within the Eurozone.

The updated ECB staff projections, due next month, would be essential in shaping the decision. Nagel also stressed that central banks must increasingly adapt to operating in an environment characterized by persistent geopolitical and policy-driven uncertainty.