Sample Category Title

Trade Talks and Inflation Data in Focus for the Week

In focus today

In a quiet start to the week on the macro data front, markets will continue to closely monitor any developments in negotiations related to the trade war. Specifically, US Treasury Secretary Schott Bessent has promised a complete briefing on the weekend's negotiations between the US and China today.

In Denmark, we will receive inflation data for April. We expect it to remain unchanged at 1.5% y/y, with March inflation decreasing from 2.0% to 1.5%. Easter could influence this, as prices for package holidays and air travel fluctuate, but the extent is uncertain.

For the remainder of the week, focus will turn to inflation data, with the star of the show being US CPI for April being released on Tuesday. Thursday will see US retail sales and PPI data, while Friday brings consumer confidence figures - all potentially influenced by higher tariffs. In the euro area, Thursday will feature the second GDP estimate and March industrial production data, followed by the European Commission's spring economic forecast on Friday. China's credit data is also expected though the date is uncertain. In Norway, mainland GDP data is scheduled for Thursday. Presidents Zelenskiy and Putin are set to meet on Thursday in what would mark the first direct peace negotiations between Ukraine and Russia since March 2022.

Economic and market news

What happened overnight

In the US, President Trump announced he would sign an executive order on Monday morning to lower prescription drug prices using the 'Most Favoured Nation' principle, a key pillar of the WTO. This aims to match drug costs in the US with those in other high-income countries, with Trump claiming that it could reduce costs by 30-80%. The move would have broader implications for drug pricing beyond current negotiations under the Inflation Reduction Act.

In the equity and commodities space, the dollar strengthened in early Asian trade following optimistic US-China talks, indicating resilience amid recent volatility. Gold prices eased, trading around USD 3,280 per troy ounce this morning, signalling lessened demand for safe-haven assets. Brent spot traded in the USD 63-64 range per barrel this morning, though increased supply plans by OPEC+ remain a potential headwind.

What happened over the weekend

In the trade war, US Treasury Secretary Bessent and Trade Representative Greer have reported 'substantial progress' in the trade talks with China that took place in Geneva over the weekend. Chinese officials confirmed that a joint statement containing "good news for the world" will be announced today. Despite ongoing challenges, the discussions were described as constructive, potentially easing tensions between the two largest economies. As economic pain is growing for both countries, we believe that tariffs will be lowered to around 60% soon.

In Norway, April core inflation surprised to the downside 3.0% y/y (March 3.0% y/y) on Friday. A look at the details showed that the slowdown was relatively broad-based, with lower price growth in food, other Norwegian-produced goods and imported goods. Price growth in services excl. rent rose from 3.5% y/y to 4.6% y/y, but this was entirely due to higher inflation on airline tickets. Both lower food prices and more expensive airline tickets are largely an Easter effect that will probably reverse in the coming months. However, if we exclude both these components, it shows that 'core-core' inflation decreased from 2.6% y/y to 2.35% y/y, which may indicate that underlying price pressures are on the decline.

In South Asia, India and Pakistan reached a ceasefire agreement late Saturday after several days of intense fighting. The agreement followed diplomatic efforts and pressure from the United States, with President Trump pledging to work towards a solution for Kashmir and increase trade with both countries. Despite the ceasefire, both sides reported overnight violations, with artillery fire in Kashmir.

In the Ukraine-Russia war, President Zelenskiy has agreed to meet President Putin in Turkey on 15 May, following Trump's urging to engage in direct talks. Putin's proposal follows significant pressure from major European powers in Kyiv, who demanded Putin to agree to a 30-day ceasefire or face 'massive' sanctions. Zelenskiy initially insisted on the ceasefire before negotiations. Trump, however, pressed for immediate talks, emphasising the potential to end the conflict. Read more in Geopolitical Radar: Another military conflict erupts, 9 May.

Equities: Equities were in a wait-and-see mode on Friday amid China-US talks this weekend. US investors appear to be cheering already with the S&P 500 future 1.5% higher and Nasdaq 2% higher. We disagree and believe that the risk reward is skewed to the downside when it comes to speculating on trade deals. Hence, we see a risk of this rally fading into the day. However, no matter whether the deals are good or bad, uncertainty comes down, which is positive for risk appetite. VIX is hovering just above 20, and if it goes below 20, driven by a decent deal today, we will see risk parity funds adding positioning support.

This was a down-week for most regions after a remarkable two-week rally. Risk appetite was still visible beneath the surface however, with cyclicals outperforming defensives (you can blame Eli Lilly for some of it). After lagging in the recovery, Europe outperformed US slightly. Interestingly, equities have not yet reacted much to the higher yields. However, if risk appetite continues to hold up, we should see higher yields resulting in more value rotation, to the benefit of Europe.

FI&FX: The improved risk-sentiment from last week is likely to continue following the positive reporting on US-China trade talks over the weekend. This week we have the expected syndication from the EU as indicated by its funding plan for Q2, possibly already taking place today.

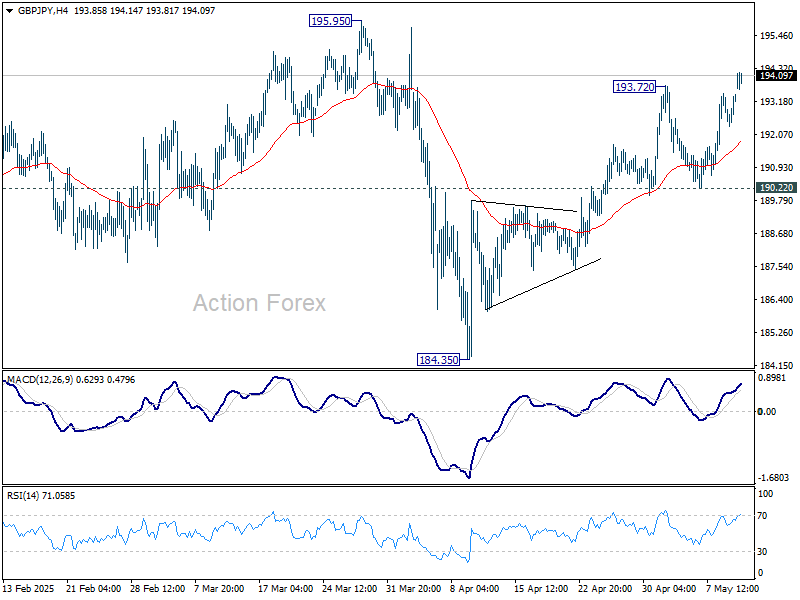

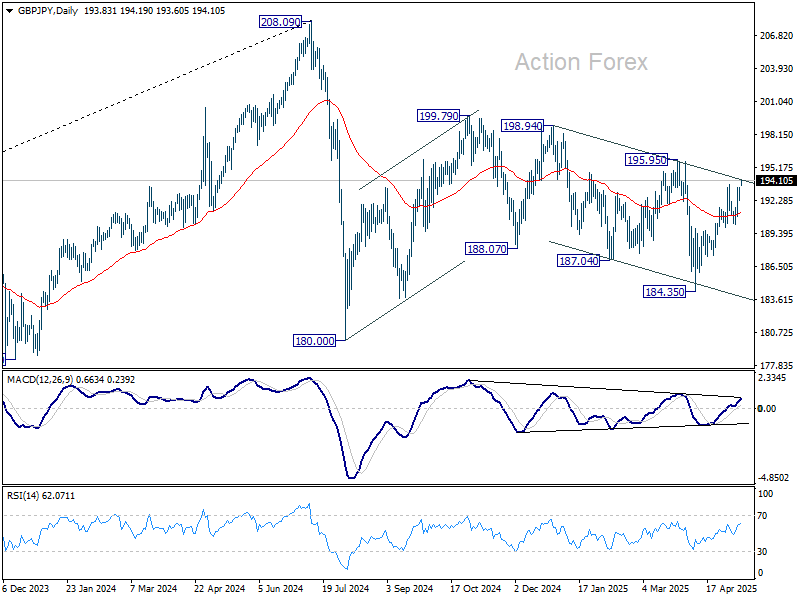

GBP/JPY Daily Outlook

Daily Pivots: (S1) 192.64; (P) 193.11; (R1) 193.86; More...

GBP/JPY's rise from 184.35 resumed by breaking through 193.72 resistance today. Intraday bias is back on the upside for 195.95 resistance next. Firm break there will suggest that whole choppy decline from 199.79 has completed. For now, risk will stay on the upside as long as 190.22 support holds, in case of retreat.

In the bigger picture, price actions from 208.09 are seen as a correction to rally from 123.94 (2020 low). Strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. However, sustained break of 175.94 will bring deeper fall even still as a correction.

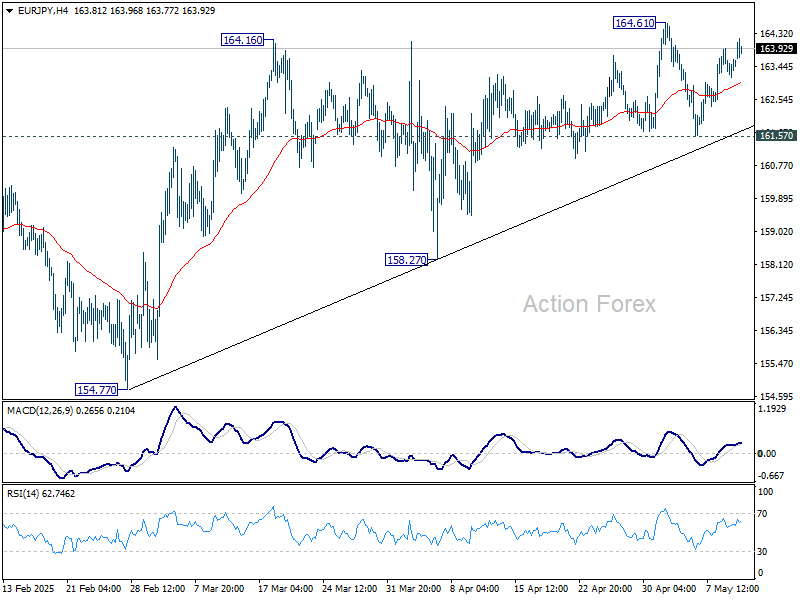

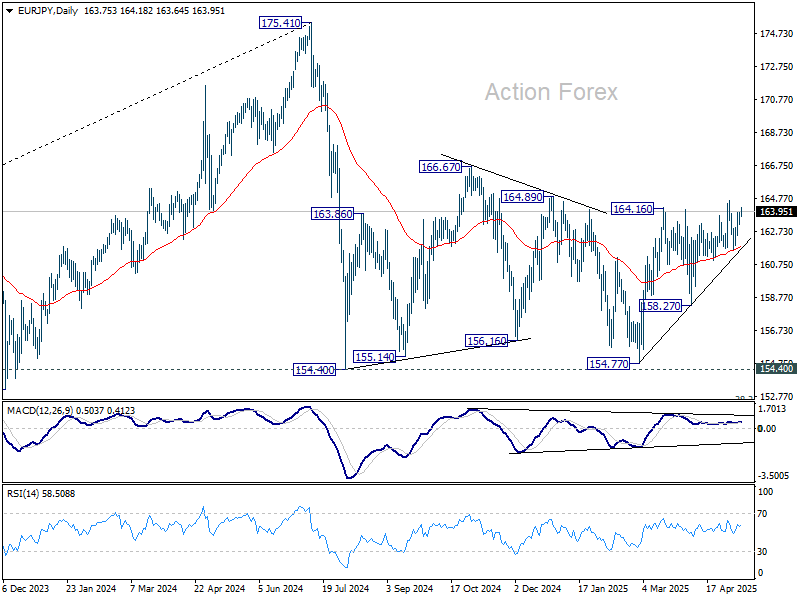

EUR/JPY Daily Outlook

Daily Pivots: (S1) 163.12; (P) 163.57; (R1) 163.99; More...

Intraday bias in EUR/JPY remains neutral first, but further rally is in favor with 161.57 support intact. On the upside, break of 164.61 will resume the rally from 154.77 to 166.67 resistance next. However, firm break of 161.57 support will indicate near term reversal and target 158.27 support instead.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

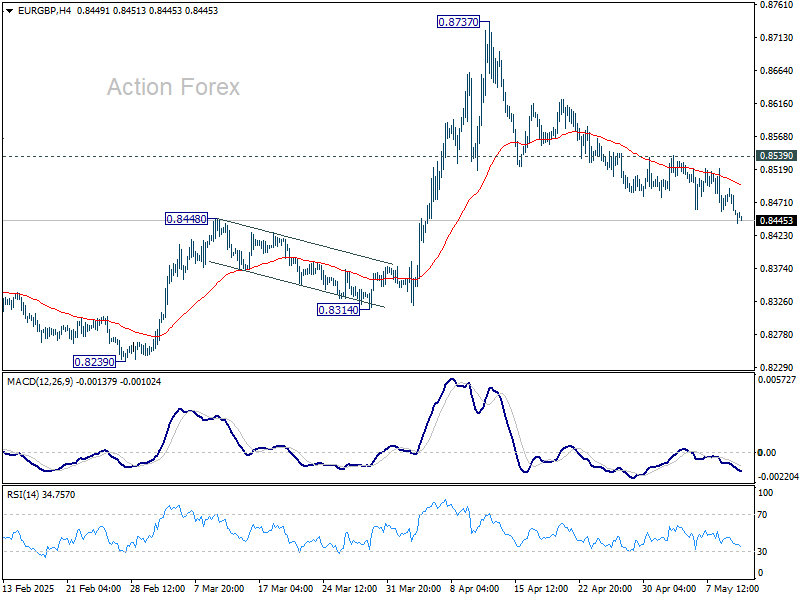

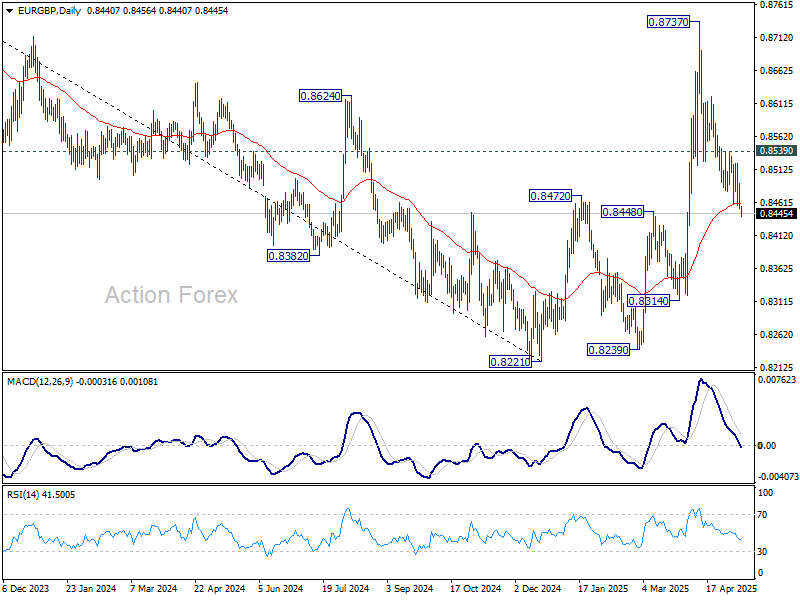

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8443; (P) 0.8468; (R1) 0.8481; More...

EUR/GBP's fall from 0.8737 continues today and intraday bias stays on the downside. Sustained trading below 55 D EMA (now at 0.8461) will argue that whole rise from 0.8221 has already complete. Near term outlook will be turned bearish for 0.8314 support first. On the upside, though, break of 0.8539 resistance will indicate that fall from 0.8737 has completed as a correction.

In the bigger picture, the extended decline from 0.8737 dampened the original bullish view. While a medium term bottom was in place at 0.8221, price actions from there could be a corrective pattern only. Larger down trend from 0.9267 (2022 high) might still be in progress. Sustained trading below 55 W EMA (now at 0.8438) will turn favor to this bearish case.

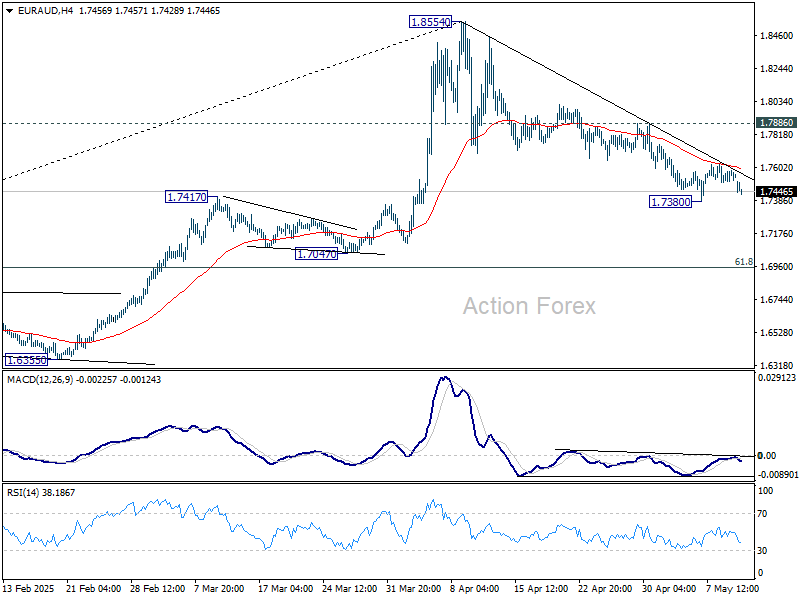

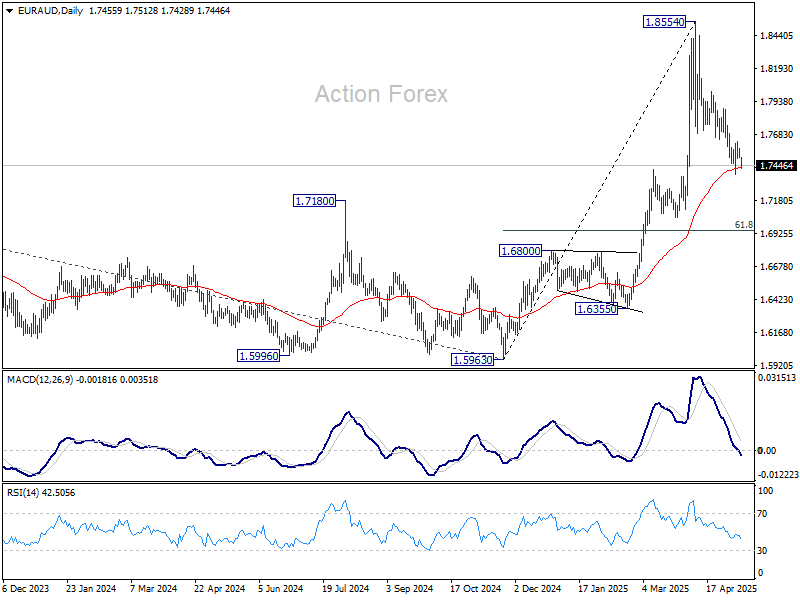

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7510; (P) 1.7547; (R1) 1.7579; More...

Intraday bias in EUR/AUD remains neutral for the moment. On the upside, firm break of 1.7886 resistance will argue that fall from 1.8553 has completed as a correction at 1.7380. Intraday bias will be turned back to the upside for retesting 1.8554. However, sustained trading below 55 D EMA (now at 1.7431) will target 61.8% retracement at 1.6953 next.

In the bigger picture, as long as 1.7062 resistance turned support (2023 high) holds, up trend from up trend from 1.4281 (2022 low) should still be in progress. Break of 1.8554 will target 100% projection of 1.4281 to 1.7062 from 1.5963 at 1.8744. However, sustained break of 1.7062 will confirm medium term topping and bring deeper fall back to 1.5963 support.

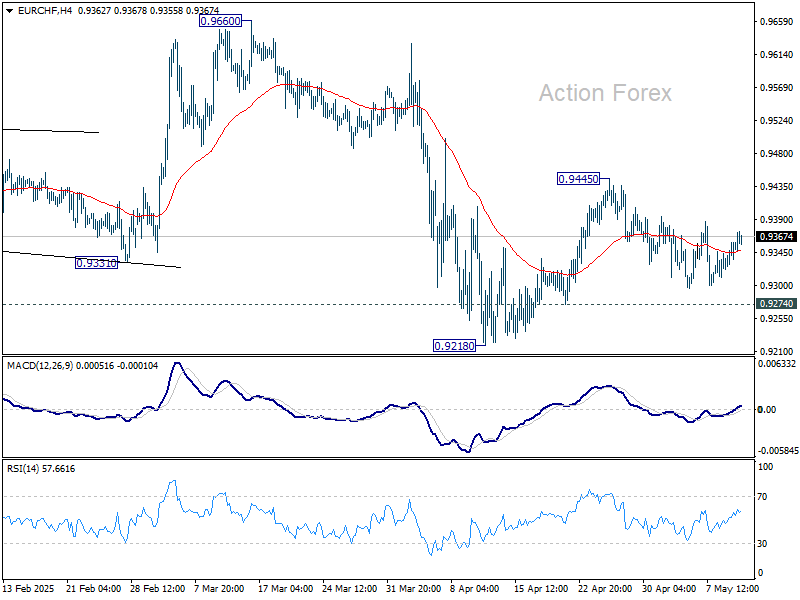

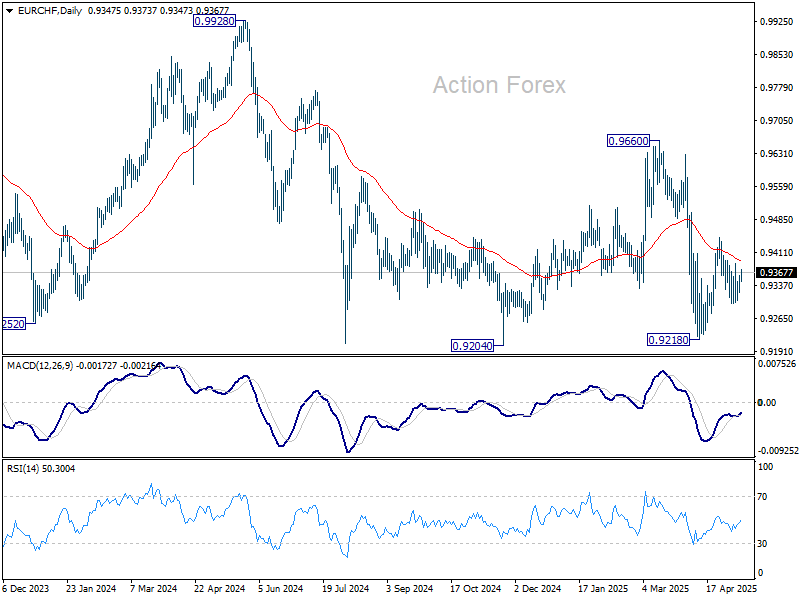

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9327; (P) 0.9344; (R1) 0.9370; More....

Range trading continues in EUR/CHF and intraday bias remains neutral. On the upside, above 0.9445 will resume the rebound from 0.9218, either as a corrective move or the third leg of the pattern from 0.9204. However, break of 0.9274 will suggest that that recovery has completed, and bring retest of 0.9204/18 support zone.

In the bigger picture, prior rejection by long-term falling channel resistance (now at 0.9548) retains medium term bearishness. That is, down trend from 1.2004 (2018 high) is still in progress. Firm break of 0.9204 (2024 low) will confirm resumption. This will remain the favored case as long as 0.9660 resistance holds.

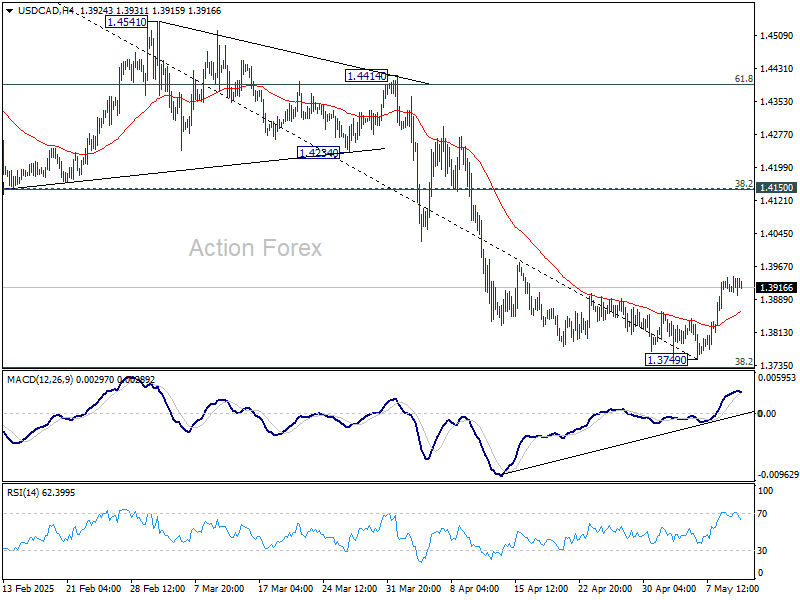

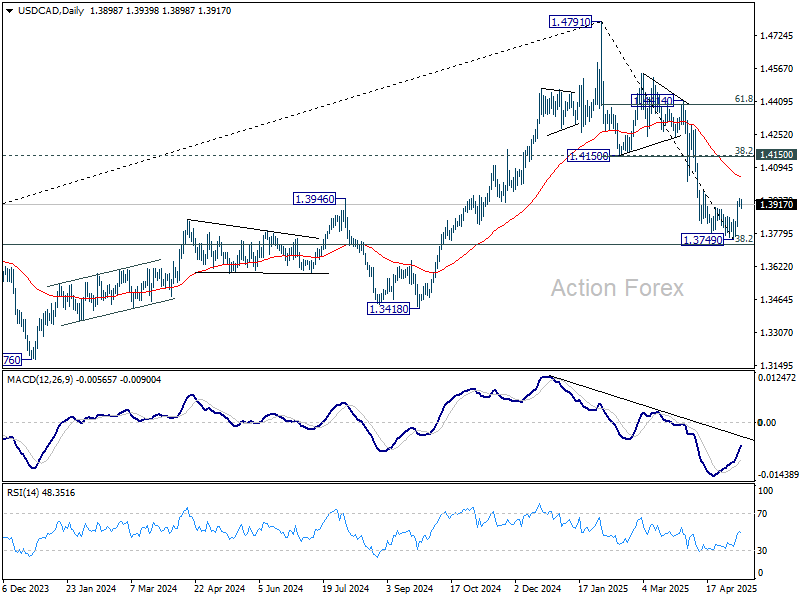

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3916; (P) 1.3930; (R1) 1.3954; More...

Intraday bias in USD/CAD stays mildly on the upside at this point. Rebound from 1.3749 short term bottom would target 55 D EMA (now at 1.4053). Break there will target 1.4150 cluster resistance (38.2% retracement of 1.4791 to 1.3749 at 1.4147). For now, risk will remain on the upside as long as 1.3749 holds, in case of retreat.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4150 resistance turned support holds. Firm break of 38.2% retracement of 1.2005 (2021 low) to 1.4791 at 1.3727 will pave the way back to 61.8% retracement at 1.3069.

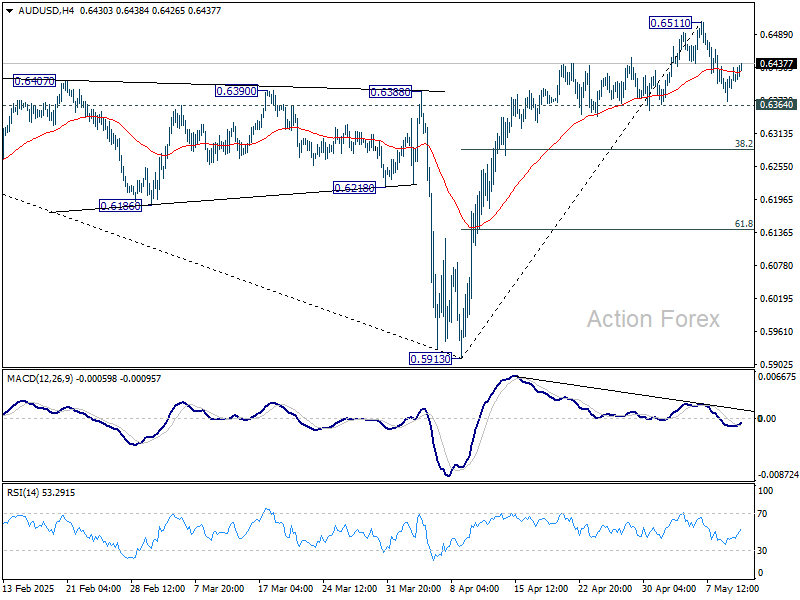

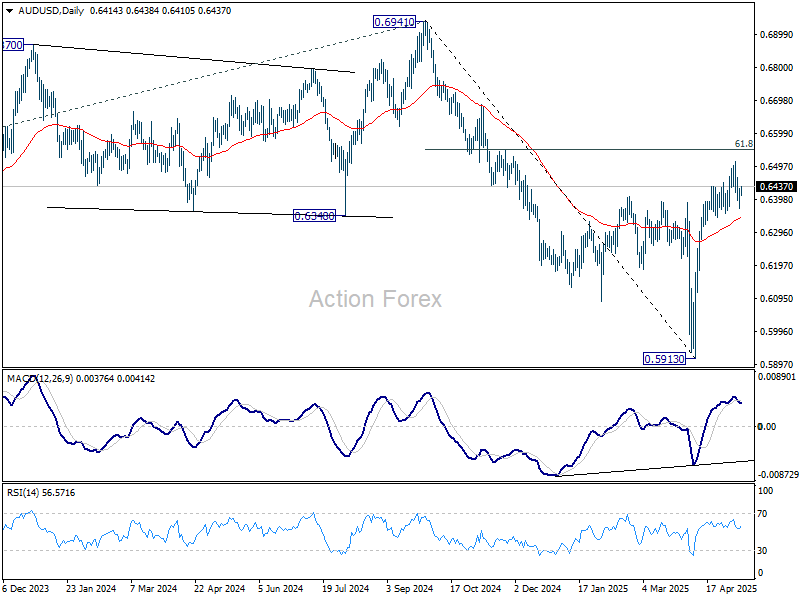

AUD/USD Daily Report

Daily Pivots: (S1) 0.6377; (P) 0.6405; (R1) 0.6439; More...

Intraday bias in AUD/USD remains neutral and more consolidations could be seen below 0.6511. On the upside, break of 0.6511 will resume the rally from 0.5913 to 61.8% retracement of 0.6941 to 0.5913 at 0.6548. However, considering bearish divergence condition in 4H MACD, break of 0.6364 support should confirm short term topping. Intraday bias will be turned back to the downside for 38.2% retracement of 0.5913 to 0.6511 at 0.6283.

In the bigger picture, as long as 55 W EMA (now at 0.6441) holds, down trend from 0.8006 (2021 high) should resume later to 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. However, sustained trading above 55 W EMA will argue that a medium term bottom was already formed, and set up further rebound to 0.6941 resistance instead.

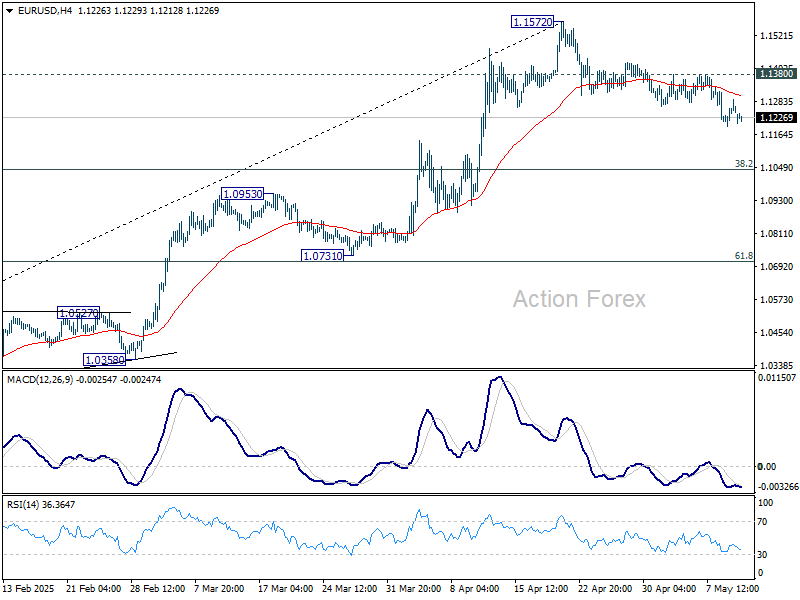

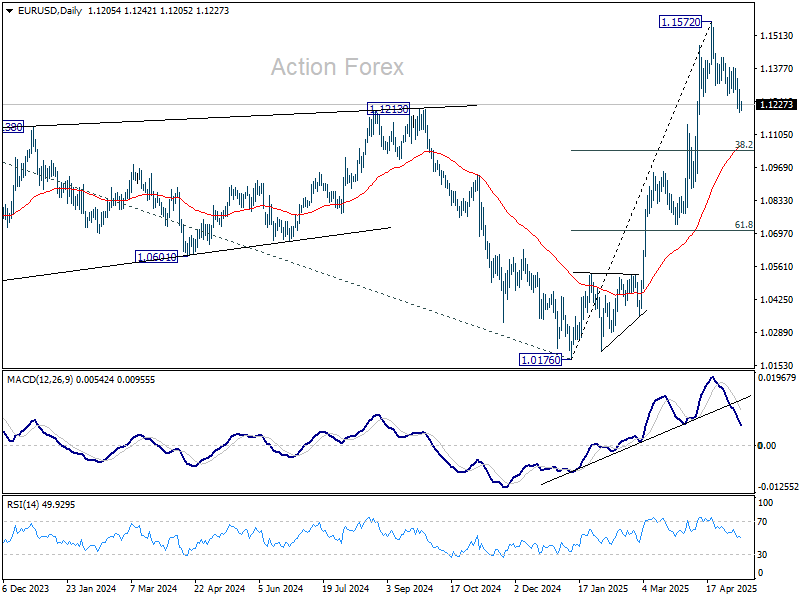

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1200; (P) 1.1246; (R1) 1.1296; More...

Intraday bias in EUR/USD's remains mildly on the downside for 55 D EMA (now at 1.1053) and possibly below. But downside should be contained by 38.2% retracement of 1.0176 to 1.1572 at 1.1039 to bring rebound. On the upside, break of 1.1380 will suggest that the correction from 1.1572 short term top has completed, and bring retest of 1.1572.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0789) holds.

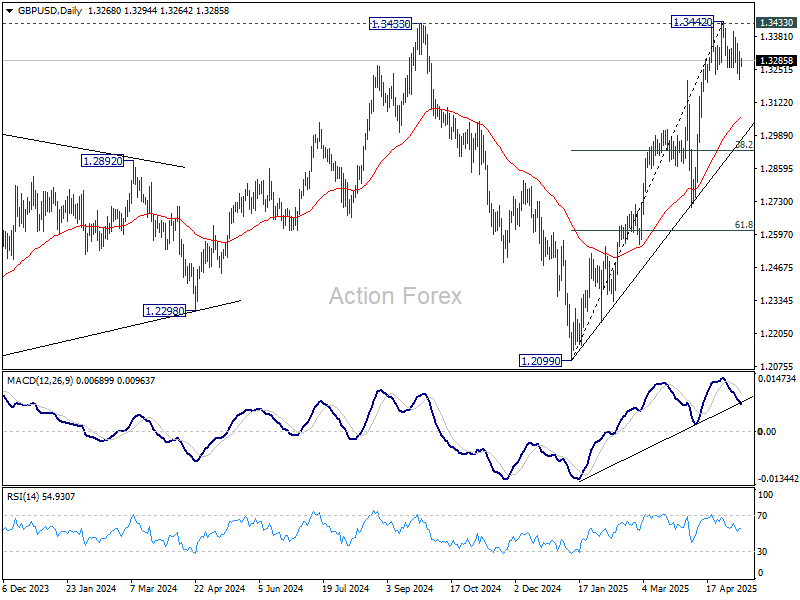

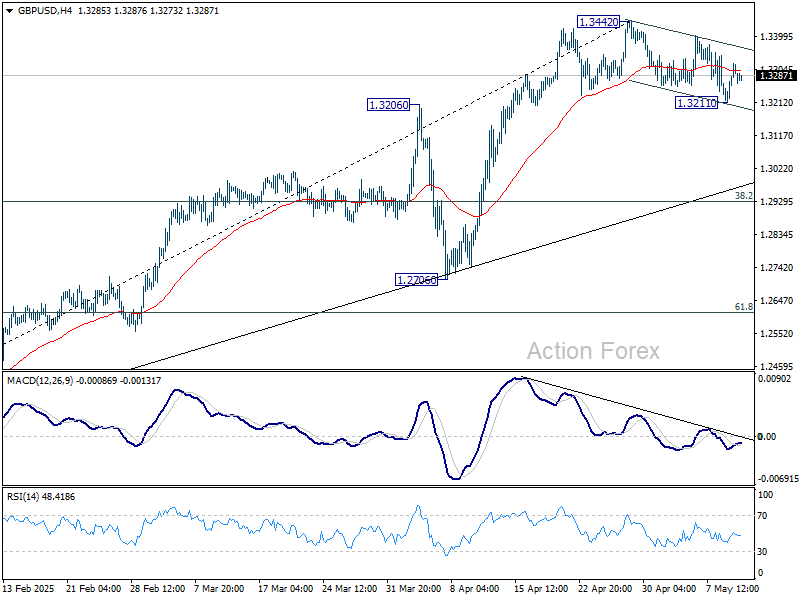

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3236; (P) 1.3279; (R1) 1.3347; More...

Intraday bias in GBP/USD remains neutral at this point. Risk will stay mildly on the downside as long as 1.3442 short term top holds. Below 1.3211 will target 55 D EMA (now at 1.3058). However, sustained break of 1.3433/42 resistance zone will confirm larger up trend resumption.

In the bigger picture, price actions from 1.3433 are seen as a corrective pattern to the up trend from 1.3051 (2022 low). Rise from 1.2099 could either be resuming the up trend, or the second leg of a consolidation pattern. Overall, GBP/USD should target 1.4248 key resistance (2021 high) on decisive break of 1.3433 at a later stage.