Sample Category Title

Yen Slides as BoJ Slashes Growth Outlook; Investor Resilience Faces ISM Test

Yen weakened broadly today following the BoJ’s decision to leave interest rates unchanged, while significantly downgrading its growth projections for the current fiscal year. Inflation outlook was also softened, with risks of undershooting the 2% target increased, albeit slightly.

This backdrop suggests that while BoJ remains on a slow tightening path, policymakers may take a more cautious approach in the near term. The prospect of a rate hike in June now appears less likely unless global trade negotiations between the US and its partners make meaningful progress.

Elsewhere, Wall Street showed surprising resilience overnight. After initially tumbling on the back of an unexpected Q1 contraction in US GDP, DOW and S&P 500 managed to close in positive territory, while NASDAQ was little changed. Fed rate expectations were also little changed, with markets still pricing in a 97% chance of a hold in May and a 66% chance of a rate cut in June.

Investor sentiment, while shaken, has not broken—at least not yet. Attention now shifts to the upcoming ISM manufacturing survey today and tomorrow’s US non-farm payroll report.

In the currency markets, Yen is the day’s weakest performer so far, weighed down by BoJ’s dovish lean. Sterling and Euro are also under pressure. On the other side, Kiwi leads gains, followed by Loonie and Aussie. Dollar and Swiss Franc are trading in the middle.

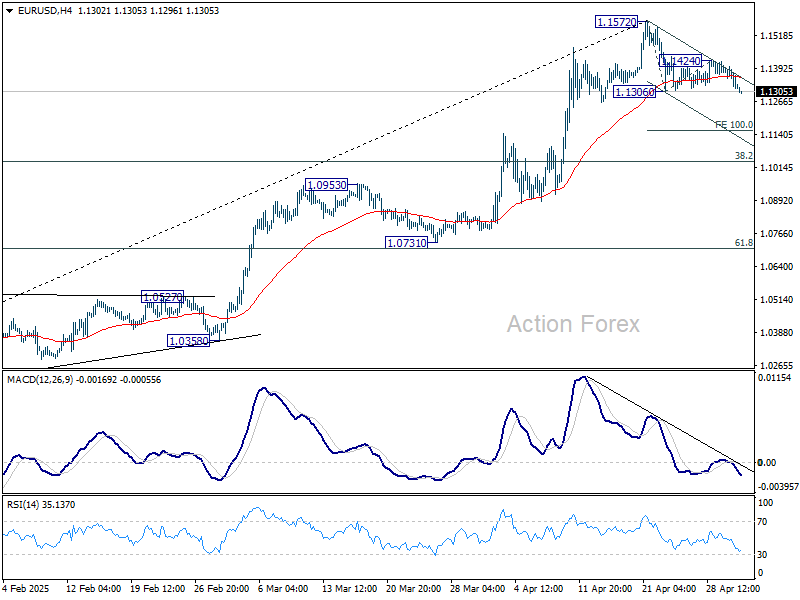

Technically, EUR/USD's correction from 1.1572 short term top is resuming through 1.1306 support. Deeper fall is now in favor to 100% projection of 1.1572 to 1.1306 from 1.1424 at 1.1158. But downside should be contained by 38.2% retracement of 1.0176 to 1.1572 at 1.1039 to complete the pullback.

In Asia, at the time of writing, Nikkei is up 0.93%. Japan 10-year JGB yield is down -0.038 at 1.277. Hong Kong, China and Singapore are on holiday. Overnight, DOW rose 0.35%. S&P 500 rose 0.15%. NASDAQ fell -0.09%. 10-year yield rose 0.004 to 4.177.

Looking ahead, Swiss retail sales and UK PMI maufacturing final will be released in European sesison. Later in the day, US will publish ISM manufacturing and jobless claims.

BoJ holds rates, slashes growth outlook on trade headwinds

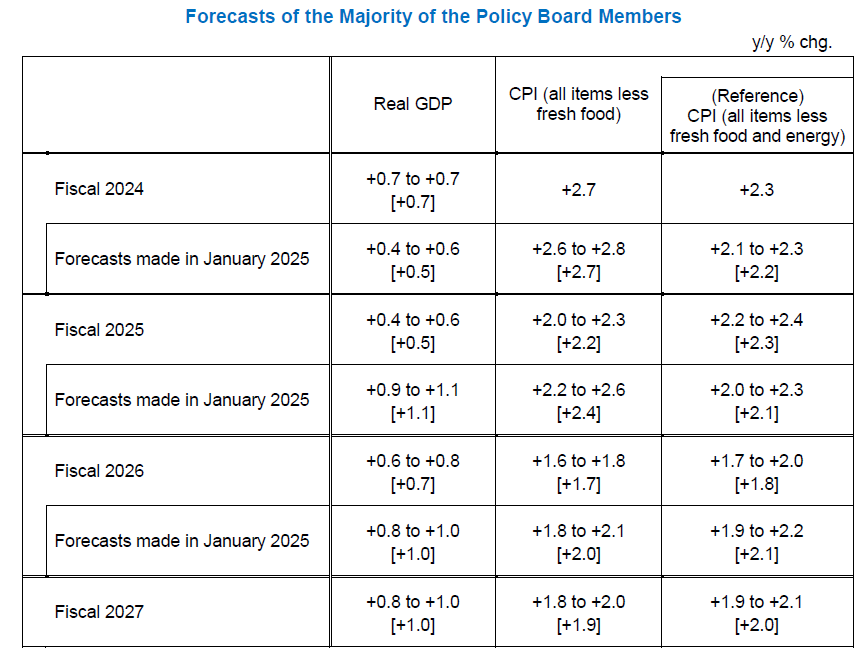

BoJ kept its benchmark interest rate unchanged at 0.50% today, by unanimous vote, in line with expectations. However, it struck a cautious tone on the economic outlook by sharply cutting its growth forecasts.

The central bank now projects Japan’s real GDP to grow just 0.5% in fiscal 2025, down from the 1.1% forecast in January, and 0.7% in fiscal 2026 (downgraded from 1.0%). Growth is expected to recover to 1.0% in fiscal 2027, assuming stabilization in global conditions.

In its statement, BoJ acknowledged that “Japan's economic growth is likely to moderate” as global trade and policy uncertainty weigh on external demand and corporate profitability. Still, the bank expects activity to reaccelerate once overseas economies resume “a moderate growth path.”

On inflation, BoJ maintained that price pressures are broadly on course toward the 2% target, but revised its CPI core forecast down from 2.4% to 2.2% for fiscal 2025, and from 2.0% to 1.7% for fiscal 2026.

BoJ raised its projection for the core-core CPI from 2.1% to 2.3% for fiscal 2025, reflecting persistent domestic inflation pressures. However, this is followed by a downgrade from 2.1% to 1.8% in 2026 before stabilizing at 2.0% in 2027.

Japan’s PMI manufacturing finalized at 48.7, slump persists amid trade uncertainty

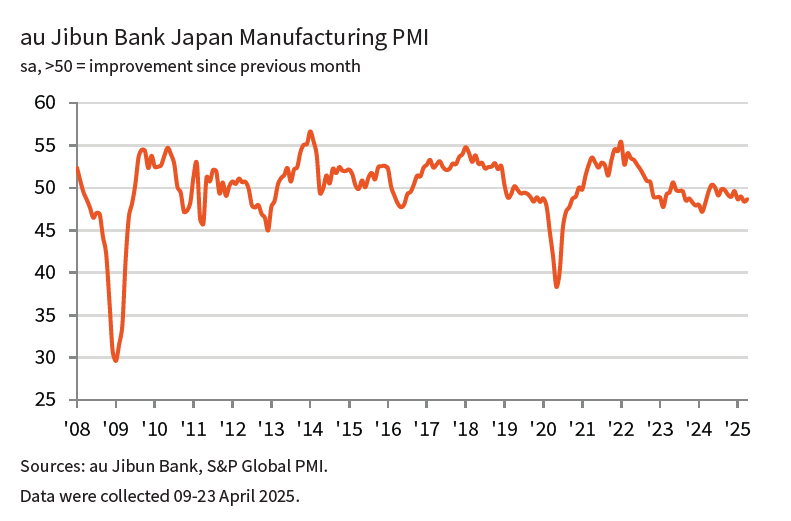

Japan’s manufacturing sector remained in contractionary territory in April, with the final PMI reading at 48.7, up slightly from March’s 48.4. While the deterioration in business conditions marked the tenth consecutive month of decline, it remained modest.

However, underlying components revealed more concerning trends, with sharper drops in new orders and exports, highlighting persistent demand-side weakness.

According to S&P Global, firms responded by scaling back purchasing and adjusting inventories, while overall sentiment worsened.

Business confidence around future output fell to its lowest since mid-2020, as companies expressed caution amid ongoing global trade tensions and muted demand. Without a significant turnaround in both domestic and external demand, "firms are likely to struggle to see a recovery in conditions".

BoC minutes: Dual uncertainties cloud policy path

BoC’s summary of deliberations from its April meeting revealed a divided Governing Council, as members weighed the case for another rate cut against the need for more clarity.

While some policymakers pushed for an immediate cut, citing a weakening domestic economy and subdued near-term inflation, others argued in favor of holding steady at 2.75% to better assess the evolving trade environment, especially with US tariffs in flux.

All members acknowledged the unusually high level of uncertainty. They agreed to be “less forward-looking than usual,” signaling a preference for data-dependence over proactive policy signaling.

The Council framed the current risks in two layers: the unpredictable path of U.S. trade policy, and the unknown economic impact of tariffs—including potential fiscal responses to soften the blow.

With no clear resolution on either front, the BoC leaned toward caution, holding policy steady at 2.75% while signaling a readiness to adjust as needed.

USD/JPY Daily Outlook

Daily Pivots: (S1) 142.42; (P) 142.81; (R1) 143.45; More...

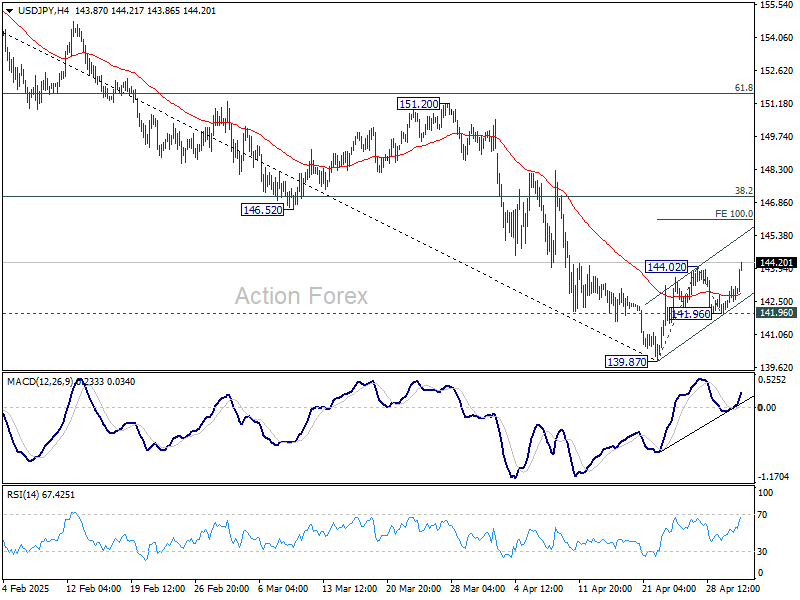

USD/JPY's rebound from 139.87 short term bottom resumed by breaking through 144.02 today. Intraday bias is back on the upside for 100% projection of 139.87 to 144.02 from 141.96 at 146.11. But still, near term outlook will stay bearish as long as 38.2% retracement of 158.86 to 139.87 at 147.12 holds. On the downside, firm break of 141.96 will argue that the rebound has completed as a corrective move. Retest of 139.87 should then be seen next in this case.

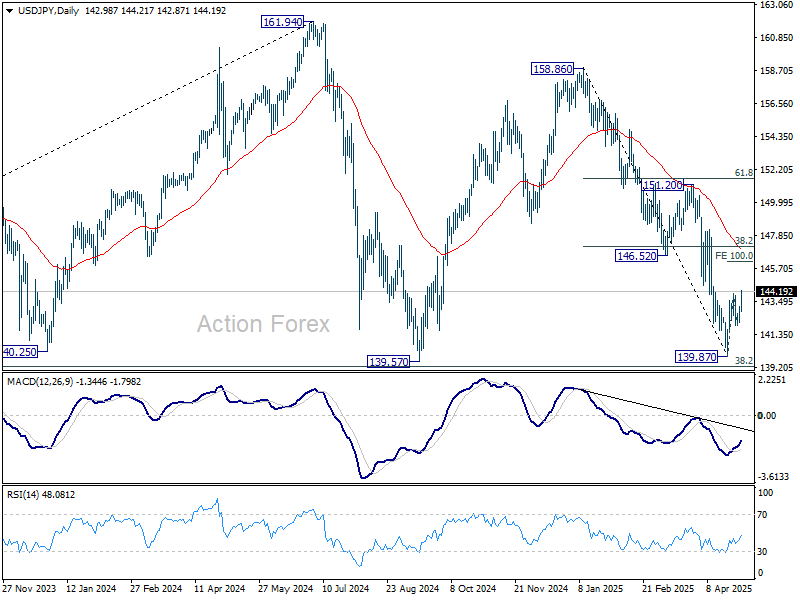

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

BoJ holds rates, slashes growth outlook on trade headwinds

BoJ kept its benchmark interest rate unchanged at 0.50% today, by unanimous vote, in line with expectations. However, it struck a cautious tone on the economic outlook by sharply cutting its growth forecasts.

The central bank now projects Japan’s real GDP to grow just 0.5% in fiscal 2025, down from the 1.1% forecast in January, and 0.7% in fiscal 2026 (downgraded from 1.0%). Growth is expected to recover to 1.0% in fiscal 2027, assuming stabilization in global conditions.

In its statement, BoJ acknowledged that “Japan's economic growth is likely to moderate” as global trade and policy uncertainty weigh on external demand and corporate profitability. Still, the bank expects activity to reaccelerate once overseas economies resume “a moderate growth path.”

On inflation, BoJ maintained that price pressures are broadly on course toward the 2% target, but revised its CPI core forecast down from 2.4% to 2.2% for fiscal 2025, and from 2.0% to 1.7% for fiscal 2026.

BoJ raised its projection for the core-core CPI from 2.1% to 2.3% for fiscal 2025, reflecting persistent domestic inflation pressures. However, this is followed by a downgrade from 2.1% to 1.8% in 2026 before stabilizing at 2.0% in 2027.

Japan’s PMI manufacturing finalized at 48.7, slump persists amid trade uncertainty

Japan’s manufacturing sector remained in contractionary territory in April, with the final PMI reading at 48.7, up slightly from March’s 48.4. While the deterioration in business conditions marked the tenth consecutive month of decline, it remained modest.

However, underlying components revealed more concerning trends, with sharper drops in new orders and exports, highlighting persistent demand-side weakness.

According to S&P Global, firms responded by scaling back purchasing and adjusting inventories, while overall sentiment worsened.

Business confidence around future output fell to its lowest since mid-2020, as companies expressed caution amid ongoing global trade tensions and muted demand. Without a significant turnaround in both domestic and external demand, "firms are likely to struggle to see a recovery in conditions".

BoC minutes: Dual uncertainties cloud policy path

BoC’s summary of deliberations from its April meeting revealed a divided Governing Council, as members weighed the case for another rate cut against the need for more clarity.

While some policymakers pushed for an immediate cut, citing a weakening domestic economy and subdued near-term inflation, others argued in favor of holding steady at 2.75% to better assess the evolving trade environment, especially with US tariffs in flux.

All members acknowledged the unusually high level of uncertainty. They agreed to be “less forward-looking than usual,” signaling a preference for data-dependence over proactive policy signaling.

The Council framed the current risks in two layers: the unpredictable path of U.S. trade policy, and the unknown economic impact of tariffs—including potential fiscal responses to soften the blow.

With no clear resolution on either front, the BoC leaned toward caution, holding policy steady at 2.75% while signaling a readiness to adjust as needed.

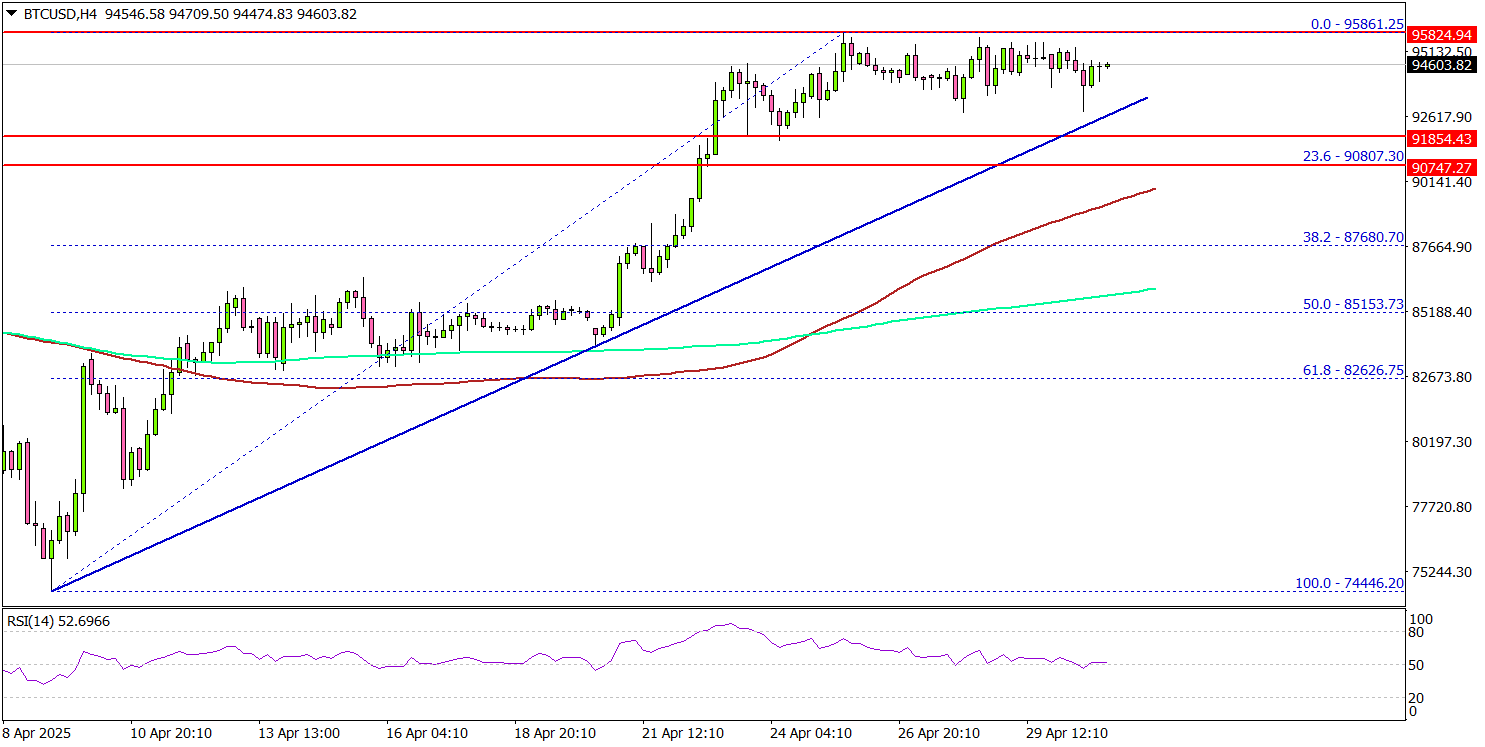

Bitcoin Bullish Bias Builds — Higher Ground Ahead?

Key Highlights

- Bitcoin price started a steady increase above the $92,000 resistance.

- A connecting bullish trend line is forming with support at $92,400 on the 4-hour chart of BTC/USD.

- Ethereum price is consolidating above $1,750 and aims for a fresh increase.

- Gold is correcting gains and might decline below the $3,220 support zone.

Bitcoin Price Technical Analysis

Bitcoin price started a fresh increase above the $88,000 zone against the US Dollar. BTC was able to surpass the $90,000 and $92,000 resistance levels.

Looking at the 4-hour chart, the price settled above the $92,000 level, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour). However, the bears seem to be active near the $95,000 and $96,000 levels.

On the upside, the price could face resistance near the $95,500 level. The next key resistance is $96,200. The main resistance could be $96,500. A successful close above $96,500 might start another steady increase.

In the stated case, the price may perhaps rise toward the $98,000 level. Any more gains might call for a test of $100,000.

Immediate support is near the $94,200 level. There is also a connecting bullish trend line forming with support at $92,400 on the same chart. The next key support sits at $90,800 or the 23.6% Fib retracement level of the upward move from the $74,446 swing low to the $95,861 high.

A downside break below $90,800 might send Bitcoin toward the $88,000 support. Any more losses might send the price toward the $85,200 support zone and the 50% Fib retracement level of the upward move from the $74,446 swing low to the $95,861 high.

Looking at Ethereum, the bulls seem to be in control and might soon aim for a move above the $1,850 resistance zone.

Today’s Economic Releases

- US ISM Manufacturing Index for April 2025 – Forecast 48.0, versus 49.0 previous.

- US Initial Jobless Claims - Forecast 224K, versus 222K previous.

US Dollar Looks for Support Ahead of Job Data: EUR/USD, USD/JPY, and USD/CAD Analysis

- The DXY currently trades ~1.73% higher than multi-year lows made in last week’s trading, now looks for support ahead of Friday’s NFP report

- A somewhat softened stance on tariffs, rumblings of the first successful trade deal, and a calming of Trump-Powell tensions have allowed the dollar to gain ground

USD: Uncertainty surrounding tariffs

The introduction of sweeping tariffs as part of Trump’s notorious “Liberation Day” has been undeniably negative for dollar pricing. Falling to levels unseen since early 2022, markets were quick to offload dollars in favour of other currencies with more stable policy environments.

The future, however, is somewhat uncertain. Agreeing to a temporary deferment in implementing further tariffs, markets are tentatively watching for any developments regarding potential trade deals, with the White House currently hinting that the first deal has been struck.

The $1,000,000 question remains whether Trump’s strong-arm tactics will encourage other nations to reach mutually beneficial trade agreements with the United States, with the last few weeks providing a glimpse of the alternative.

USD: Trump vs. Powell continues

Speaking today at a rally in Michigan marking 100 days in office, Trump has recently renewed criticism of the Federal Reserve, and by extension, Chair Jerome Powell.

A relationship marred by potshots from both parties, Trump has long argued that the Federal Reserve should cut rates more aggressively to stimulate economic growth, a request that has, at least so far, fallen on deaf ears, with the Federal Reserve yet to cut in 2025.

With Trump, perhaps more optimistic than most regarding the current US economy, it would seem that Powell and the Federal Reserve have different priorities for current monetary policy, voting for a more conservative and calculated cutting cycle.

Amid concerns about its autonomy from the White House, the Federal Reserve is set to meet next Wednesday to vote on monetary policy. Traders will closely watch for any commentary suggesting their likely next move.

EUR/USD technical analysis

EUR/USD currently trades around 1.13268, ~2.18% lower in value than recent highs. Trading in a period of consolidation, euro-dollar will have to break and maintain above key resistance at around ~1.13954 to continue the current bull trend, with the next target being around ~1.15182.

USD/JPY technical analysis

At the time of writing, USD/JPY trades above the key level of 143.000 at around 143.050. Unless price can close above the consolidation held between ~143.284 and ~143.836, dollar-yen remains firmly in bearish territory. If price breaks down further, bears will target 142.019.

USD/CAD technical analysis

Recently trading rangebound, USD/CAD has broken previously held consolidation to the downside and now trades at around ~1.37905. The MACD on the four-hourly time frame shows a strengthening bearish trend, with an increasing divergence between MACD and the baseline. If price breaks down further, bears will likely target 1.37528.

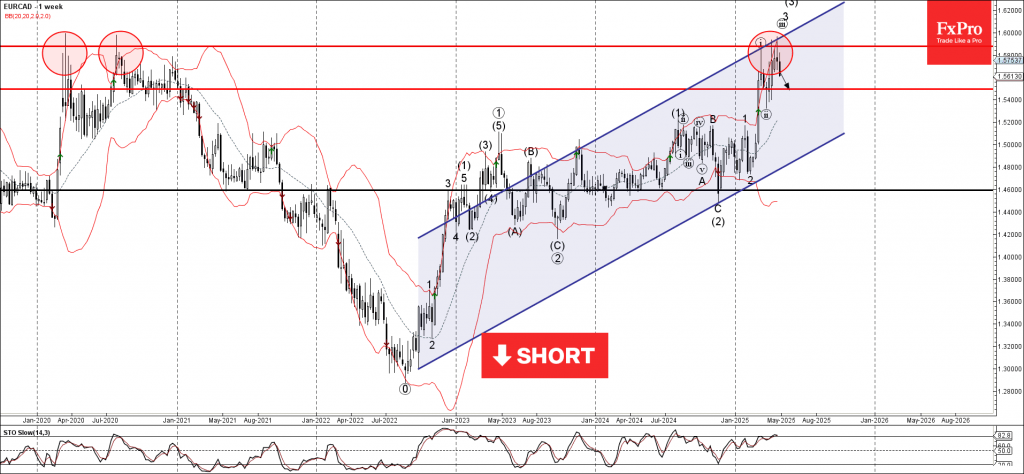

EURCAD Wave Analysis

EURCAD: ⬇️ Sell

- EURCAD reversed from resistance level 1.5880

- Likely to fall to support level 1.5495

EURCAD currency pair recently reversed down from the pivotal resistance level 1.5880 (which has been reversing the price from the start of July) intersecting with the upper daily Bollinger Band and the resistance trendline of the daily up channel from 2022.

The downward reversal from the resistance level 1.5880 created the weekly Shooting Star – a strong sell signal for EURCAD.

Given the overbought daily Stochastic and the strength of the resistance level 1.5880, EURCAD currency pair can be expected to fall to the next support level 1.5495.

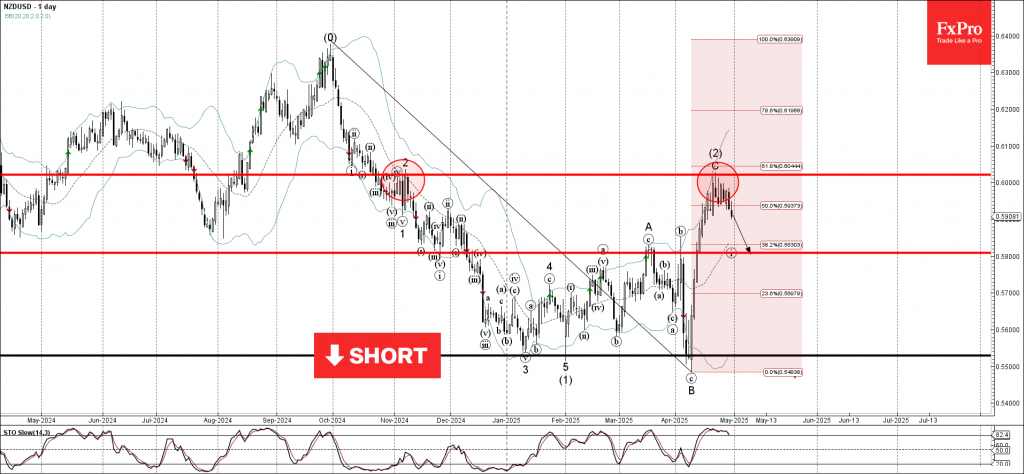

NZDUSD Wave Analysis

NZDUSD: ⬇️ Sell

- NZDUSD reversed from the resistance level 0.6020

- Likely to fall to support level 0.5800

NZDUSD currency pair recently reversed down from the pivotal resistance level 0.6020 (former top of wave 2 from November) intersecting with the 61.8% Fibonacci correction of the downward impulse from September.

The downward reversal from the resistance level 0.6020 started the active intermediate impulse wave (3).

Given the overbought daily Stochastic, NZDUSD currency pair can be expected to fall to the next support level 0.5800, the former resistance from March and the target for the completion of the active impulse wave 1.

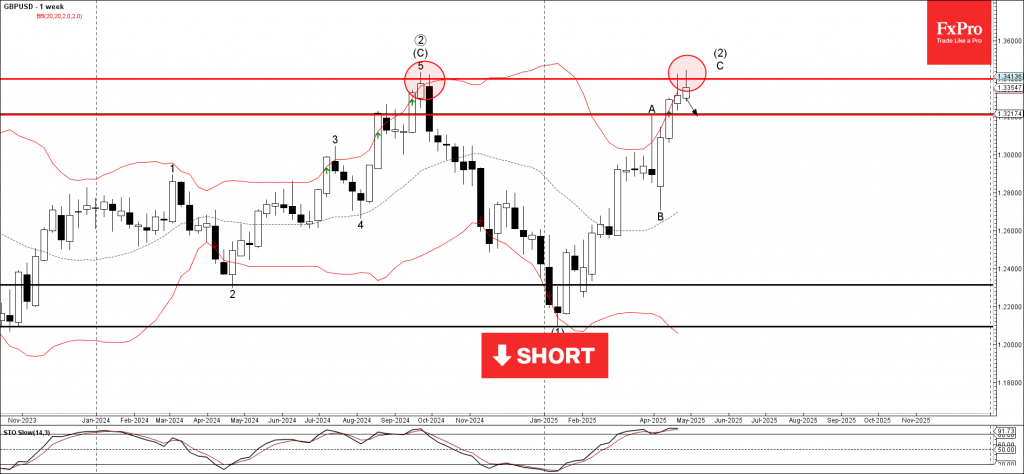

GBPUSD Wave Analysis

GBPUSD: ⬇️ Sell

- GBPUSD reversed from the long-term resistance level 1.3430

- Likely to fall to support level 1.3200

GBPUSD currency pair recently reversed down from the long-term resistance level 1.3430 (previous yearly high from last year) standing close to the upper daily and weekly Bollinger Bands.

The price also earlier reversed down from the resistance level 1.3430 creating the weekly Shooting Star last week.

Given the overbought weekly Stochastic and the strength of the resistance level 1.3430, GBPUSD currency pair can be expected to fall to the next support level 1.3200.