Sample Category Title

EUR/USD Bearish Breakout And Wave 5 Challenges 1.1820 Bottom

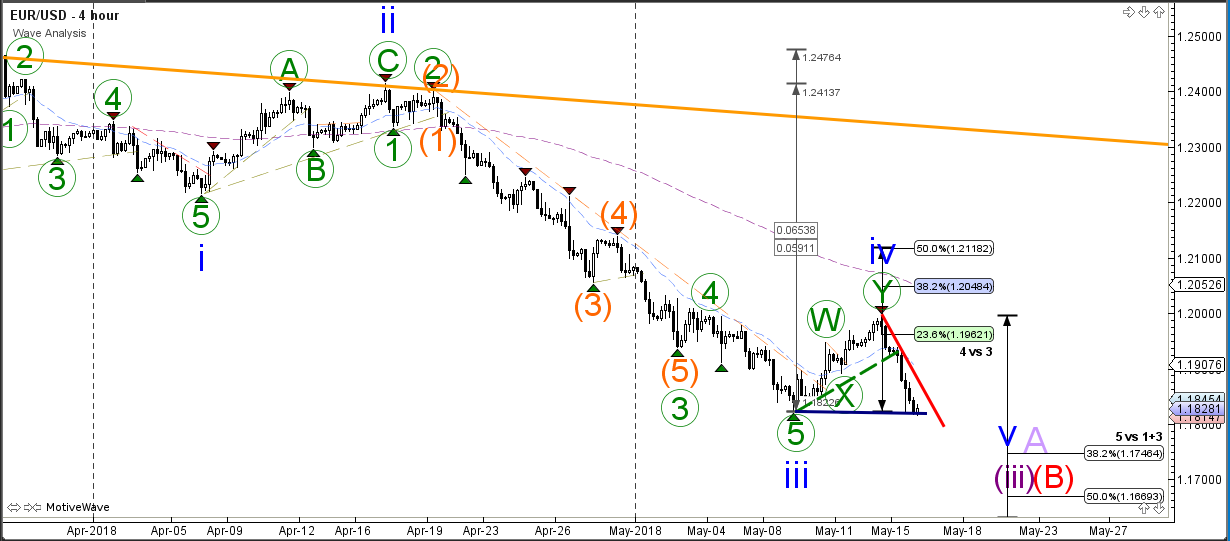

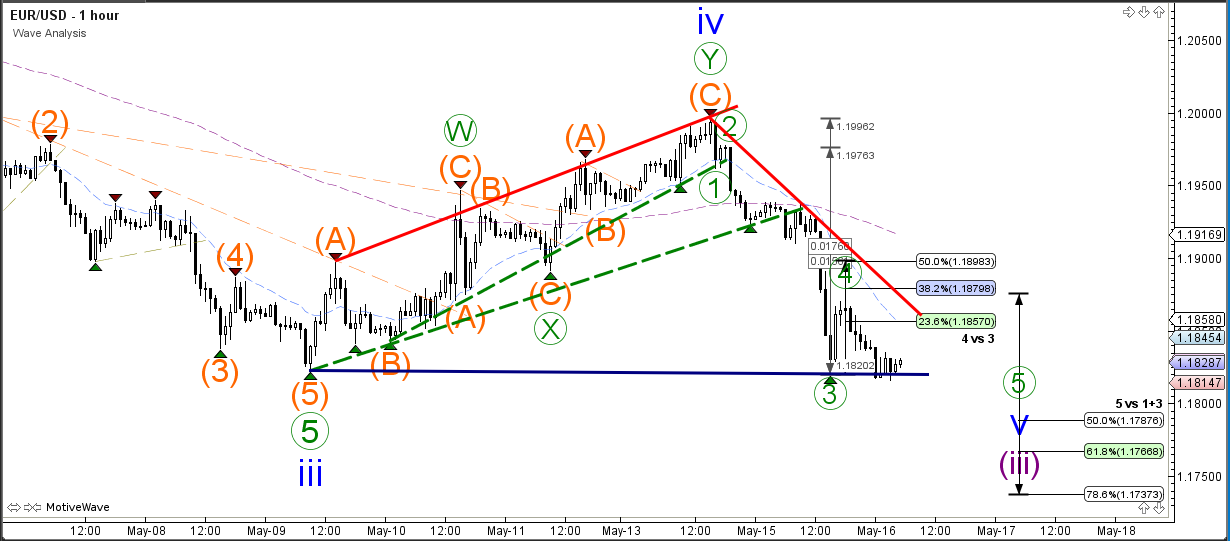

The EUR/USD reversed at Fibonacci resistance levels of wave 4 (green) and is now challenging the previous bottom (blue line) after a strong bearish break below the support trend lines (dotted green). A bearish breakout could indicate a continuation of the 5th wave (blue) and aim for the 1.1750 round level. This lower low could complete the 3rd wave (purple) and one more lower is possible after a wave consolidation (purple) within the larger wave A (correction). Technically speaking price already broke the previous bottom by 5 pips so a bullish reaction could already indicate the end of wave 5.

The EUR/USD seems to have completed a bearish wave 3 and 4 (green) and price is now in a wave 5 which could push lower if it manages to break below the support trend line (blue). A break above the 50% Fib of wave 4 could indicate that the wave 5 is already completed.

Eurozone CPI MoM Figures Expected To Fall

At 07:00 GMT, the ECB Non-Monetary Policy Meeting will take place. EUR crosses could be influenced by this event.

At 09:00 GMT, Eurozone Consumer Price Index – Core (YoY) (Apr) will be released. The consensus is for an unchanged reading of 0.7%. Consumer Price Index (MoM) (Apr) is expected to be 0.3% from 1.0% previously. Consumer Price Index (YoY) (Apr) is expected to be unchanged at 1.2%. Consumer Price Index – Core (MoM) (Apr) is expected at 0.2% from 1.4% prior. YoY Inflation rose to 2.0%, the highest levels in five years, in late 2016 and early 2017, but has since stabilized around 1.3%. The ECB is looking for inflation to “approach 2%”. CPI data is expected to show a decrease in the monthly figures, with yearly figures expected to remain in line with previous readings. EUR pairs may see volatility pick up due to this data.

At 12:00 GMT, ECB President Mario Draghi is due to deliver opening remarks at an ECB event held in honour of Vítor Constâncio, in Frankfurt. EUR pairs may be influenced by this event.

At 12:30 GMT, US Housing Starts (MoM) (Apr) is expected at 1.310M from a previous number of 1.319M. Building Permits (MoM) (Apr) is expected to come in at 1.350M from the prior reading of 1.354M. This data is expected to show a small decrease in activity from previous readings. These data points have been recovering since hitting lows of 0.46M and 0.49M respectively after the financial crisis. The readings in February were the highest since those lows in both cases. USD crosses could see increased volatility around this data release.

At 12:30 GMT, FOMC Member Bostic is due to speak about the economic outlook at the Augusta Cotton Exchange. Audience questions are expected. USD crosses may see spikes in volatility during this event.

At 13:15 GMT, US Industrial Production (MoM) (Apr) will be released. The consensus is for 0.6% from 0.5% previously. This measure rebounded strongly in March to reach the highest reading since December 2014, after having slipped below the zero line previously. Capacity Utilization (Apr) will also be released at this time, with an expectation for 78.4% v 78.0% previously. The expectation is for the number to exceed the two-year high from December. USD crosses may be impacted.

At 16:00 GMT, SNB Chairman Jordan is due to speak about the Sovereign Money Initiative at a Vollgeld event, in Zurich. CHF crosses may be affected by any comments made.

USD Strength Leads Currencies To Break Key Levels

Japanese GDP fell to -0.2% from 0.0% expected for the quarterly Q1 figure and -0.6% from 0.0% expected for the yearly figure. This drop was forecasted, with an expectation for a recovery to higher numbers going forward into Q2. USDJPY didn’t react much and is still trading in the same range around 110.275, after breaking above 110.000 yesterday. FX, in general, was stable overnight after some key levels were broken yesterday, with EURUSD falling back under 1.19000 and GBPUSD falling under 1.35000 on USD strength. Gold took a tumble under strong support at 1300.00, triggering bearish technical patterns. Equity markets also fell yesterday, with the US 500 dropping to test support at 2700.00.

UK Average Earnings excluding Bonus (3Mo/Yr) (Mar) came in at 2.9% as expected, from 2.8% previously. Claimant Count Change (Apr) was 31.2K against an expected 7.5K, from a previous reading of 11.6K, which was revised up to 15.7K. ILO Unemployment Rate (3M) (Apr) was as expected, unchanged at 4.2%. Average Earnings including Bonus (3Mo/Yr) (Mar) was as expected at 2.6%, from 2.8% previously. Claimant Count Rate (Mar) was 2.5% against 2.4% previously. Wage growth was expected to continue to tick up after stabilizing at 2.5% and moving up in February but failed to do so, falling below last month’s reading of 2.8%. The unemployment rate is at multi-decade lows, which is when wage growth would normally be higher as competition to attract workers takes hold. The BOE will study wage data for any indication of a change, in case they need to change their hawkish tone. GBPUSD moved higher from 1.35276 to 1.35582 after this data release.

Eurozone Gross Domestic Product s.a. (QoQ) (Q1) was as expected, unchanged at 0.4%. Gross Domestic Product s.a. (YoY) (Q1) was also as expected, unchanged at 2.5%. Industrial Production w.d.a. (YoY) (Mar) was released at 3.0% against a consensus of 3.7%, from a prior of 2.9%, which was revised down to 2.6%. Industrial Production s.a. (MoM) (Mar) was 0.5% against an expected 0.6%, from -0.8% previously, which was revised down to -0.9%. The monthly figure dipped to -1.0% in February but rebounded last month, with a much stronger rebound this time, marginally missing expectations. EURUSD moved higher from 1.19160 to 1.19290 after this data release, but then sold off later in the day.

US Retail Sales (MoM) (Apr) were as expected at 0.3%, from 0.6% previously, which was revised up to 0.8%. Retail Sales ex Autos (MoM) (Apr) were 0.3% against an expected 0.5%, from 0.2% prior, which was revised up to 0.4%. Retail Sales Control Group (Apr) came in as expected at 0.4%, from 0.4% prior, which was revised up to 0.5%. The sales slipped after last month’s beat, which was revised higher yesterday, with the current readings coming in as expected. USDJPY broke higher from 109.913 to reach a high for the day of 110.341 after this data release.

EURUSD is up 0.03% overnight, trading around 1.18418.

USDJPY is down -0.08% in early session trading at around 110.253.

GBPUSD is up 0.08% this morning, trading around 1.35131.

Gold is up 0.33% in early morning trading at around $1,294.40.

WTI is up 0.20% this morning, trading around $71.22.

Japanese Government Appears Unconcerned By Q1 GDP Contraction

General Trend:

- Asian equities trade mixed; bond yields in focus

- New Zealand NZX-50 index declines over 2%, largest intraday drop since late 2016

- Japanese megabank Mitsubishi UFJ declines over 3% after guidance and buyback announcement

- Japan Q1 GDP contracts for the first time since 2014, business investment unexpectedly declined; government suggests weakness is temporary

- Aussie declines as Q1 wage growth pace holds steady

- Asian bond yields generally track rise in US interest rates

- Indonesia 10-year bond yield rises over 10bps

- Asian currencies under pressure amid equity outflows : Indonesia Rupiah (IDR) trades at weakest level since late 2015

- North Korea cancels today’s high-level talks with South Korea, cites US/South Korea military drills

- China Delegation arrives to Washington for trade talks (as expected) - Xinhua

- China President Xi said China can come out of trade war in better shape - HK Press

- Starbucks accelerates China net new store opening plan

- Australia April employment data due for release on Thursday’s session

Headlines/Economic Data

Australia/New Zealand

- ASX 200 opened +0.1%, closed +0.3%

- ASX 200 Energy index +1.8%, Consumer Discretionary +1.1%, Resources +0.9%, Financials +0.7%; Utilities -1.1%, REIT -0.5% Telecom -0.2%

- (AU) AUSTRALIA Q1 WAGE PRICE INDEX Q/Q: 0.5% V 0.6%E; Y/Y: 2.1% V 2.1%E

- (AU) Australia May Westpac Consumer Confidence M/M: -0.6% v -0.6% prior: Index: 101.8 v 102.4 prior

China/Hong Kong

- Shanghai Composite opened -0.4%, Hang Seng -0.4%

- Hang Seng Info Tech index -0.3%, Energy -0.3%, Financials -0.1%; Industrial Goods +0.4%

- (CN) CHINA APRIL NEW HOME PRICE M/M: 0.6% V 0.4% PRIOR: Y/Y: 4.7% v 4.9% prior

- (CN) China PBoC sets yuan reference rate at 6.3745 v 6.3486 prior

- (CN) China PBoC Open Market Operation (OMO): Injects CNY260B in 7-day and 14-day reverse repos v CNY180B injected with 7-day and 14-day reverse repos prior; Net: CNY200B injection v CNY180B injection prior

- (CN) China Finance Ministry (MOF) sells 1 and 10-year bonds

Japan

- Nikkei 225 opened -0.4%; closed -0.4%

- Topix Info & Communication index -0.9%, Electric Appliances -0.2%; Securities +1%, Iron & Steel +0.3%

- (JP) Japan Economy Min Motegi: No change in view Japan economy is recovering 'moderately'; Economy is likely to recover, driven by consumption and Capex.

- (JP) JAPAN Q1 PRELIM GDP Q/Q -0.2% V % 0.0%E; ANNUALIZED Q/Q: -0.6% V -0.1%E (first contraction in 9 quarters); Business Spending Q/Q: -0.1% v +0.4%e (first drop in 6 quarters) ; Domestic demand contribution to GDP -0.2 pct point.

- (JP) Japan Mar Final Industrial Production M/M: 1.4% v 1.2% prelim; Y/Y: 2.4% v 2.2% prelim

Korea

- Kospi opened -0.5%

- (KR) North Korea cancels Weds high-level talks with South Korea; threatens to cancel Trump-Kim summit over US-South Korea military drills - Korean press

- (KR) South Korea Unification Ministry: North Korea decision to cancel high-level meeting with South Korea is 'regrettable'; military drills with US to proceed as planned

- (KR) North Korea: Will never engage in economic trade with US in exchange for giving up its nuclear program; will need to reconsider summit with US if Washington insists on North giving up nuclear program - KCNA

- (KR) There is speculation that North Korea may disclose its secret uranium enrichment facilities – South Korean Press

- (KR) South Korea April Unemployment Rate: 3.8% v 3.9%e

North America

- US equity markets ended mostly lower: Dow -0.8%, S&P500 -0.7%, Nasdaq -0.8%, Russell 2000 flat

- S&P 500 Real Estate -1.7%, Health Care -1.3%

- (US) Fed's Williams (moderate, voter): 3 to 4 rate hikes in 2018 is the right direction for policy; recent inflation pickup is 'very reassuring to me'

- (US) Weekly API Oil Inventories: Crude: +4.9M v -1.9M prior

Europe

- (UK) BOE's Broadbent: economy is entering a menopausal phase; BOE will not spoon feed markets with a meeting by meeting rate hike - press interview

- Paddy Power Betfair [PPB.UK]: Reportedly nearing deal to acquire FanDuel - Legal Sports Report

Levels as of 02:00ET

- Hang Seng +0.1%; Shanghai Composite -0.1%; Kospi +0.1%

- Equity Futures: S&P500 +0.1%; Nasdaq100 flat, Dax flat; FTSE100 +0.2%

- EUR 1.1815-1.1844 ; JPY 110.19-110.40 ; AUD 0.7447-0.7479 ;NZD 0.6851-0.6880

- Jun Gold +0.2% at $1,293/oz; Jun Crude Oil -0.3% at $71.08/brl; Jul Copper +0.1% at $3.061/lb

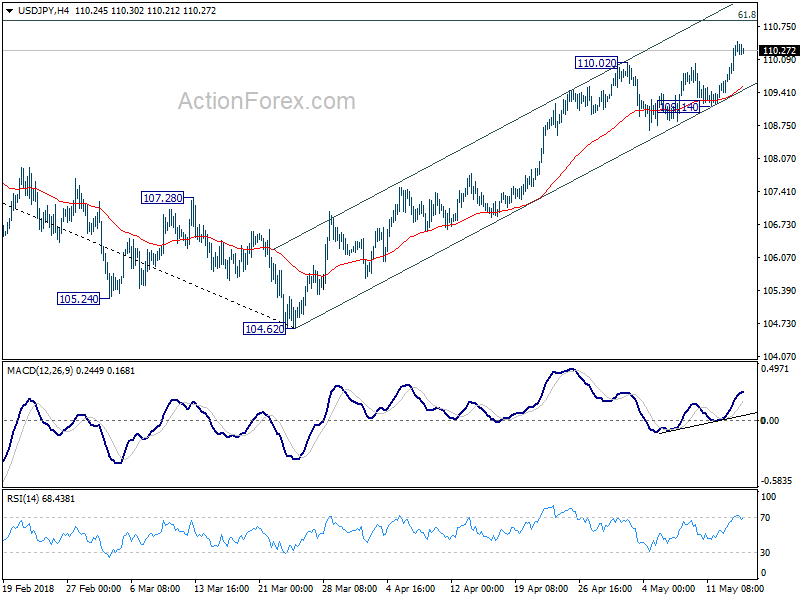

USD/JPY Daily Outlook

Daily Pivots: (S1) 109.84; (P) 110.15; (R1) 110.66; More...

Intraday bias in USD/JPY remains on the upside for the moment. Current rise from 104.62 is in progress for 61.8% retracement of 114.73 to 104.62 at 110.86 next. Firm break there will target medium term trend line resistance at 112.43. On the downside, below 109.14 support is needed to indicate short term topping. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Rise from 104.62 is possibly resuming the up trend from 98.97 (2016 low). This will be the preferred case as long as 55 day EMA (now at 108.30) holds. Decisive break of 114.73 resistance will confirm our view and target 118.65 and above.

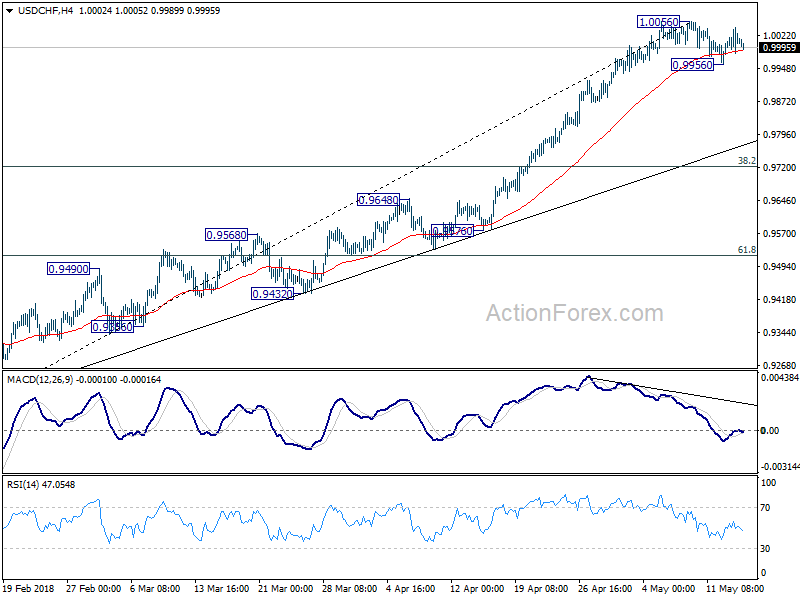

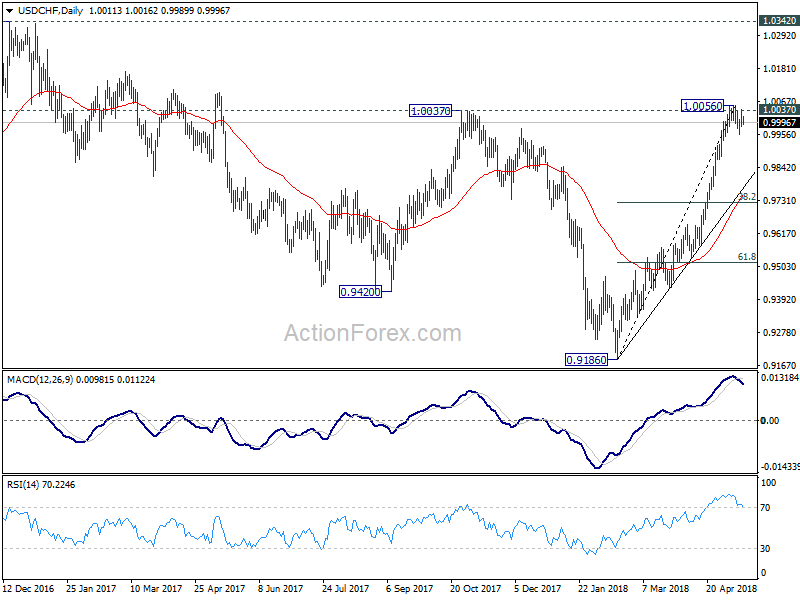

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9984; (P) 1.0013; (R1) 1.0043; More...

USD/CHF is staying in range below 1.0056 and intraday bias remains neutral. Consolidation from there could still extend. Break of 0.9956 will bring deeper pull back. But downside should be contained by trend line support (now at 0.9778) to bring rebound. On the upside, sustained break of 1.0037 will resume recent rise for 1.0342 key resistance next

In the bigger picture, medium term decline from 1.0342 has completed with three waves down to 0.9186. Rise from there is currently viewed as a leg inside the long term range pattern. Hence, while further rally would be seen, we'd be cautious on strong resistance from 1.0342 to limit upside. For now, further rise is expected as long as 38.2% retracement of 0.9186 to 1.0056 at 0.9724 holds.

US Equity Markets Traded Lower Yesterday

Market movers today

Final Euro CPI data should confirm that core inflat ion fell to 0.7% y/y in April, but more det ails will be revealed wit h t oday's release.

In the US, housing starts and indust rial product ion are due out , but they are not likely to move markets unless we see a big deviat ion from consensus. Housing starts are expected to fall 0.7% m/m whereas consensus looks for a rise in indust rial product ion of 0.6% m/m.

China's t op economic adviser, Vice P remier Liu He, yesterday arrived in Washington for further t rade talks. He will stay unt il Saturday.

In Sweden, it is t ime for the Valueguard house price data. Earlier this morning, the Maklarstat ist ik showed that Swedish apartment prices dropped 1% m/m while house prices were flat in April. In cent ral Stockholm, apartment prices were unchanged on th e month. See page 2 for further comment .

Selected market news

10Y US Treasury yields increased significantly yesterday and the 10Y US government bond yield broke through both its 2018 and 2014 highs to a new high of 3.09%. There was no particular trigger behind the break higher in US yields, which merely seems to be a consequence of a sustained underlying selling pressure on the US fixed income market .

US equity markets traded lower yesterday, likely in part due to the increase in US yields and USD. The S&P 500 index ended the day 0.68% lower, and most regional indices in Asia are also t rading lower this morning. In the FX market , the USD gained versus all other G10 currencies, primarily supported by higher US yields.

US data released yesterday was relatively solid: Retail sales came out more or less in line with expectat ions although the core control group was a bit weaker than expected (0.3% m/m versus consensus of 0.4%). However, taking the up revisions in the previous month into account it was st ill a solid report , confirming that private consumption will remain a main growth driver this year. The Empire Manufacturing index has risen to 20.1 in May from 15.8 in April and thus provided a posit ive first read on manufacturing activity in May.

In Italy, talks between the Five Star Movement and League part ies on forming a new government have entered their final lap, the leader of the League party, Mat teo Salvini, said last night . Talks will cont inue this morning.

In Japan, data released overnight shows that the economy shrank for the first t ime in two years, with GDP cont ract ing 0.6% q/q (annualised) in Q1. The decline was much steeper than expected and GDP growth in Q4 was revised down from 1.6% q/q (annualised) to 0.6% q/q. The main explanat ion behind the weak GDP figure in Q1 was an unexpected decline in business spending and flat private consumption.

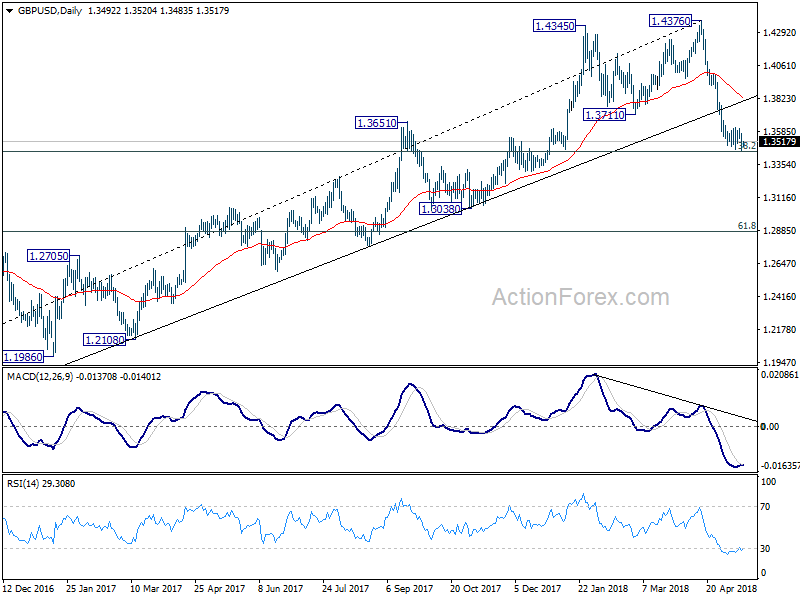

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3435; (P) 1.3524; (R1) 1.3598; More...

GBP/USD breached 1.3459 but cannot break through 1.3448 fibonacci level and recovered. Though, decline from 1.4376 is considered to be resuming and intraday bias stays on the downside. Sustained break of 1.3448 will pave the way to next one at 1.2874. On the upside, break of 1.3607 resistance is needed to indicate short term bottoming. Otherwise, outlook will stay bearish in case of recovery.

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4223). 38.2% retracement of 1.1936 (2016 low) to 1.4376 at 1.3448 was almost met. Break there will target 61.8% retracement at 1.2874 and below. Outlook will stay bearish as long as 55 day EMA (now at 1.3861) holds, even in case of strong rebound.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1793; (P) 1.1866 (R1) 1.1912; More....

Despite breaching 1.1822 support, there is no follow through selling seen in EUR/USD yet. Nonetheless, intraday bias remains on the downside side. The decline from 1.2555 is seen as resuming for 1.1708 medium term fibonacci level next. Break will target 1.1553 support. And, on the upside, break of 1.1995 resistance is needed to indicate short term bottoming. Otherwise, outlook will remain bearish in case of recovery.

In the bigger picture, current development suggests that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term was formed at 1.2555 already. Decline from there should extend further. Break of 38.2% retracement of 1.0339 to 1.2555 at 1.1708 will target 61.8% retracement at 1.1186. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 55 day EMA (now at 1.2162) holds.

Dollar Held by Near Term Resistance Despite Yield Inspired Rally

Dollar surged broadly as boosted by rally in US Treasury yield. 10 year yield hit as high as 3.90 overnight, the highest level since 2011, before settling at 3.08. While the greenback is strong, it's struggling to break through near term resistance levels decisively against Euro and Sterling for now. For now, EUR/USD is still holding above 1.1822 while GBP/USD is holding above 1.3459. Meanwhile, Swiss Franc somehow stole some spotlights from Dollar as EUR/CHF dived through 1.1864 support to as low as 1.1825, after failing 1.2 handle again earlier. Developments in yields and Dollar will remain the major focus for today.

San Francisco Fed Williams: Neutral rate will stay at 2.5% despite stronger growth

San Francisco Fed President John Williams said that the r-star neutral rate remains at 2.5% despite strong growth. He noted that "some economists and central bankers have pointed to signs that the fortunes of r-star are set to rise." However, he didn't see "convincing evidence" yet.

Fed has been describing monetary policy as "accommodative" for years. With federal funds rates just a few hikes from 2.5%, William saw the need to "revisit" the language. But "that would be a committee decision about how to best describe the committee's view around where monetary policy is positioned and where we see it going."

Japan GDP ended expansion streak... temporarily

Japan GDP contracted -0.2% qoq in Q1, worse than expectation of 0.0% qoq. On annualized basis,GDP contracted -0.6% versus expectation of -0.1%. The contraction marked the end of eight straight quarters of growth. And that was the longest streak since 1989. GDP deflator, however, rose 0.5% yoy, beating expectation of 0.3% yoy.

But it's generally believed that the contraction is temporary. In particular, a relatively weaker Yen at 100 against Dollar and global recovery, export led Japanese economy remains on solid footing for expansion.

Also from Japan, industrial production was revised up to 1.4% mom in March, from first estimate of 1.2% mom.

North Korea infuriated by Bolton, threatens to cancel Trump-Kim summit

North Korea threatened to cancel Trump-Kim summit after they're infuriated by comments from Trump's national security adviser John Bolton that North Korea could follow a Libyan model of nuclear disarmament. The meeting is scheduled to be on June 12.

North Korea's vice-foreign minister Kim Kye-gwan used strong words in a statement carried by the state news agency KCNA. He condemned that Bolton's suggestion was "not an expression of intention to address the issue through dialogue". And, "it is essentially a manifestation of awfully sinister move to impose on our dignified state the destiny of Libya or Iraq which had been collapsed due to yielding the whole of their countries to big powers."

Kim went further and warned that if the US "corners us and unilaterally demands we give up nuclear weapons we will no longer have an interest in talks and will have to reconsider whether we will accept the upcoming DPRK-US summit". And, "if President Trump follows in the footsteps of his predecessors, he will be recorded as more tragic and unsuccessful president than his predecessors, far from his initial ambition to make unprecedented success."

Elsewhere

Australia wage price index rose less than expected by 0.5% qoq in Q1. Westpac consumer confidence dropped -0.6% in May. Eurozone and Germany CPI final will be the main feature in European session. US will release housing starts and building permits, industrial production and capacity utilization later in the day. Canada manufacturing sales will also be featured.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1793; (P) 1.1866 (R1) 1.1912; More....

Despite breaching 1.1822 support, there is no follow through selling seen in EUR/USD yet. Nonetheless, intraday bias remains on the downside side. The decline from 1.2555 is seen as resuming for 1.1708 medium term fibonacci level next. Break will target 1.1553 support. And, on the upside, break of 1.1995 resistance is needed to indicate short term bottoming. Otherwise, outlook will remain bearish in case of recovery.

In the bigger picture, current development suggests that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term was formed at 1.2555 already. Decline from there should extend further. Break of 38.2% retracement of 1.0339 to 1.2555 at 1.1708 will target 61.8% retracement at 1.1186. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 55 day EMA (now at 1.2162) holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | GDP Q/Q Q1 P | -0.20% | 0.00% | 0.40% | |

| 23:50 | JPY | GDP Deflator Y/Y Q1 P | 0.50% | 0.30% | 0.10% | |

| 00:30 | AUD | Westpac Consumer Confidence May | -0.60% | -0.60% | ||

| 01:30 | AUD | Wage Price Index Q/Q Q1 | 0.50% | 0.60% | 0.60% | |

| 04:30 | JPY | Industrial Production M/M Mar F | 1.40% | 1.20% | 1.20% | |

| 06:00 | EUR | German CPI M/M Apr F | 0.00% | 0.00% | ||

| 06:00 | EUR | German CPI Y/Y Apr F | 1.60% | 1.60% | ||

| 09:00 | EUR | Eurozone CPI M/M Apr | 0.30% | 1.00% | ||

| 09:00 | EUR | Eurozone CPI Y/Y Apr F | 1.20% | 1.30% | ||

| 09:00 | EUR | Eurozone CPI Core Y/Y Apr F | 0.70% | 0.70% | ||

| 12:30 | CAD | Manufacturing Sales M/M Mar | 1.00% | 1.90% | ||

| 12:30 | USD | Housing Starts Apr | 1.33M | 1.32M | ||

| 12:30 | USD | Building Permits Apr | 1.35M | 1.35M | ||

| 13:15 | USD | Industrial Production M/M Apr | 0.60% | 0.50% | ||

| 13:15 | USD | Capacity Utilization Apr | 78.40% | 78.00% | ||

| 14:30 | USD | Crude Oil Inventories | -2.2M |