Sample Category Title

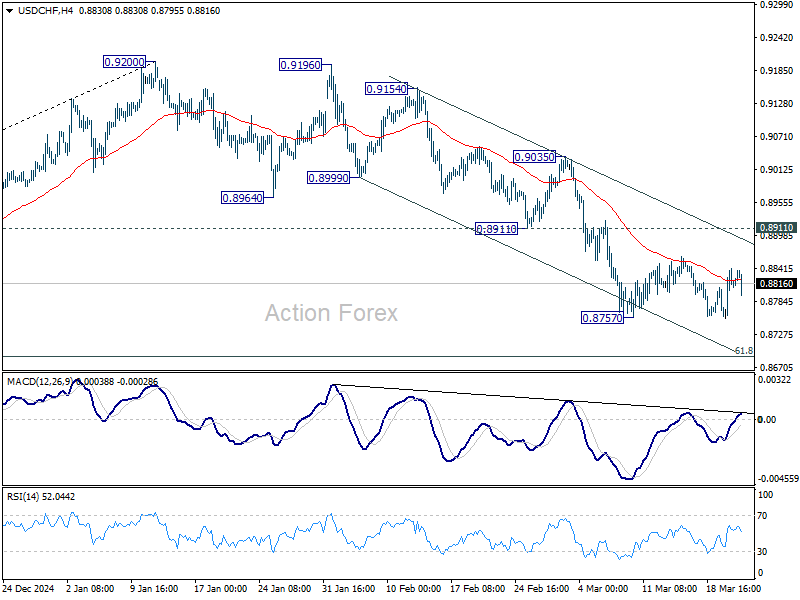

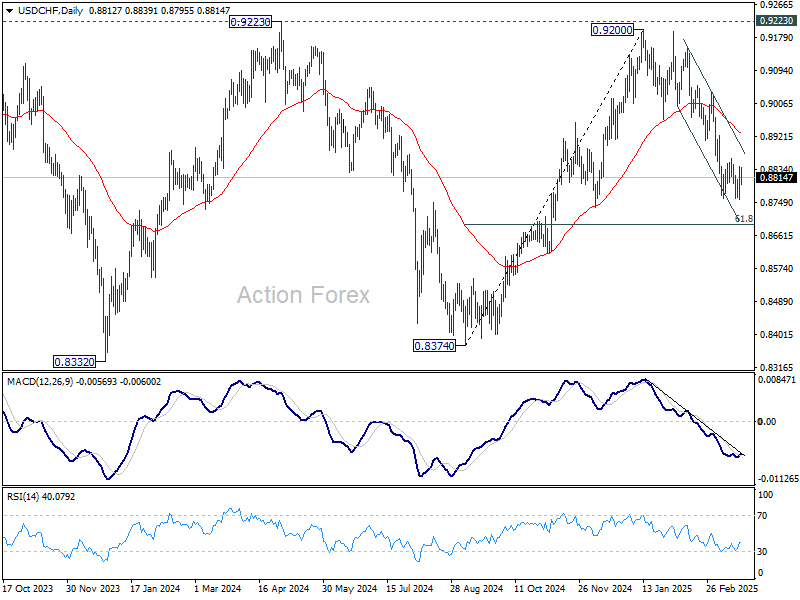

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8768; (P) 0.8806; (R1) 0.8855; More…

Intraday bias in USD/CHF remains neutral as consolidations from 0.8757 is still extending. While stronger recovery cannot be ruled out, upside should be limited by 0.8911 support turned resistance. On the downside, break of 0.8757 will resume the fall from 0.9200 to 61.8% retracement of 0.8374 to 0.9200 at 0.8690. Sustained break there will pave the way back to 0.8374 support.

In the bigger picture, rejection by 0.9223 key resistance keep medium term outlook bearish. That is, larger fall from 1.0342 (2017 high) is not completed yet. Firm break of 0.8332 (2023 low) will confirm down trend resumption.

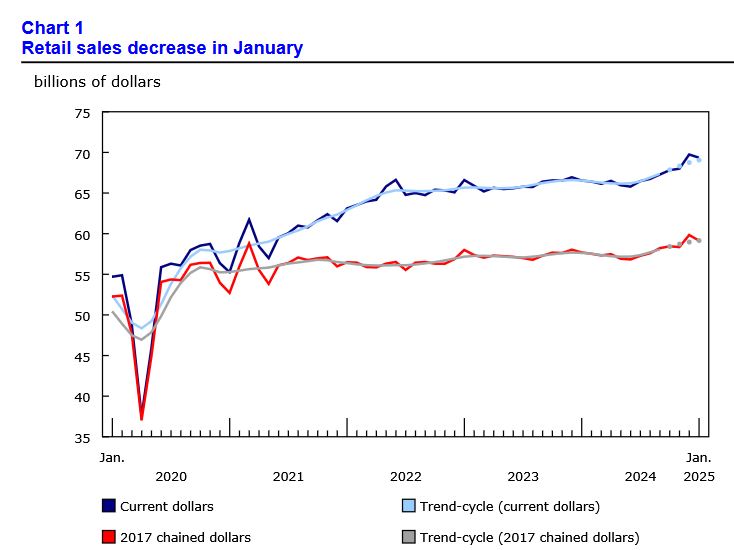

Canada: Retail Sales Edge Lower in January Ahead of Looming Tariff Storm

Retail sales declined by 0.6% month-on-month (m/m) in January, following December's outsized gain of 2.6% (previously reported as 2.5%). The result came in below the Statistics Canada's advanced estimate of 0.4%.

After adjusting for inflation, the volume of retail sales posted a sizeable decline of 1.1% m/m in January.

A big part of the weakness came from sales at motor vehicle and parts dealers, which dropped 2.6% m/m, reversing all of December's 1.8% gain. Ex-autos, sales rose 0.2% m/m, outperforming the consensus call for a 0.2% decline.

Receipts at gas stations and fuel vendors rose 3.2% m/m in nominal terms. This was largely due to higher prices, as volumes growth was negligible at just 0.1% m/m.

Excluding auto sales and receipts at gas stations, core retail sales declined 0.2% m/m in January. The weakness was driven primarily by a 2.5% drop in food and beverage stores.

Gains in other categories – furniture and home furnishings stores (+3.9% m/m), building material & garden equipment dealers (+1.6% m/m), health and personal care stores (+1.2% m/m), and general merchandise stores (+0.9% m/m) – were not enough to offset the losses.

E-commerce sales fell 0.9% m/m in January, following a 2.9% gain in December.

Statistics Canada's advanced estimate for February points to another decline in sales of 0.4% m/m.

Key Implications

Consumers tightened their belts to start the year with retail sales retreating more than expected in January after a strong showing in December. Since sales are reported in nominal terms, part of the decline may reflect a temporary drop in prices due to the HST/GST holiday. However, the pullback was even more pronounced in real terms.

Looking ahead, uncertainty looms. Our internal credit and debit card statistics points to a slight softening in spending through the first quarter, consistent with today's reading and the advance estimate for February. While there may be some stockpiling ahead of tariffs in March any boost would likely be short-lived. Consumers remain cautious and may restrain spending further until there is more clarity on the outlook for jobs, incomes and prices. We've penciled in a 2.7% (annualized) growth in consumer spending for Q1, and potentially a contraction in the following quarters (see QEF).

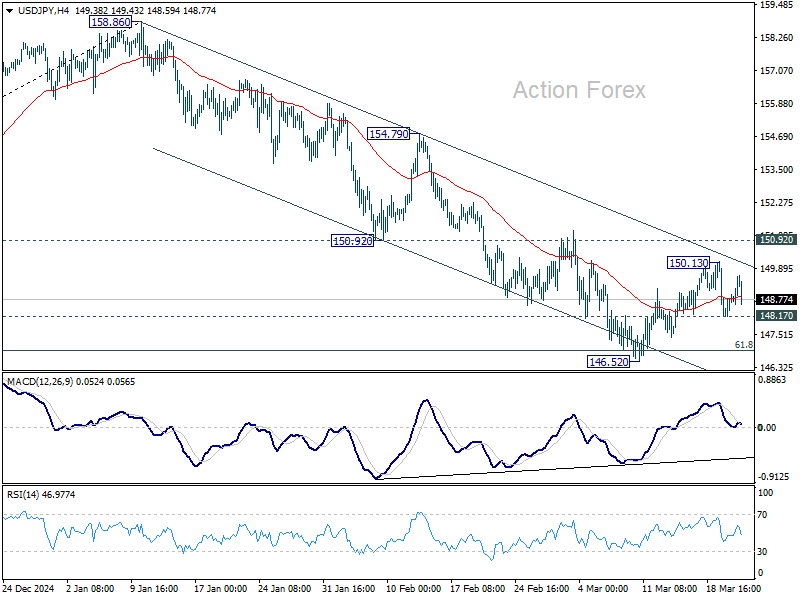

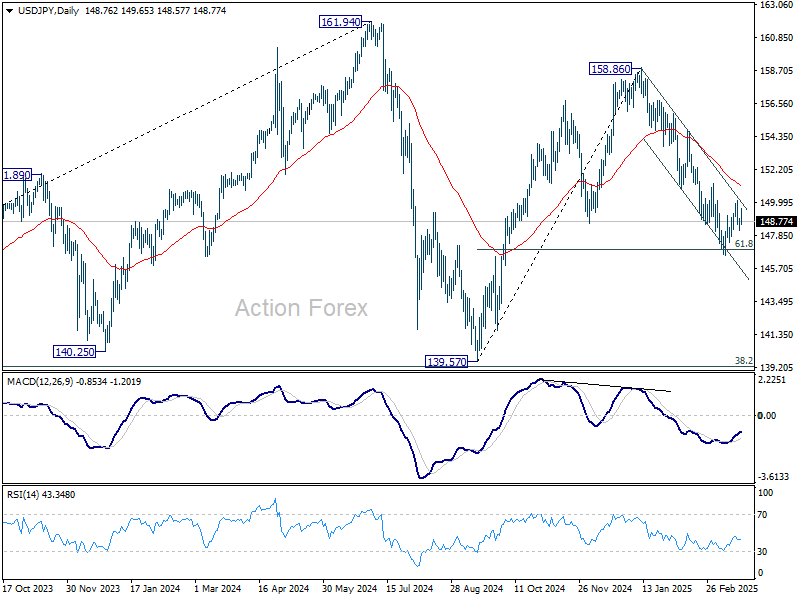

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 148.32; (P) 148.64; (R1) 149.10; More...

Intraday bias in USD/JPY remains neutral and outlook is unchanged. Corrective pattern from 146.52 might extend. But in case of stronger recovery, upside should be limited by 150.92 support turned resistance. On the downside, firm break of 148.17 support will bring retest of 146.52 first. Sustained trading below 61.8% retracement of 139.57 to 158.86 at 146.32 will resume the fall from 158.86 to 139.57 support.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

Loonie Softens on Retail Sales Miss, But BoC Inflation Focus Limits Losses

Canadian Dollar weakened modestly in early US session following disappointing retail sales data. January’s figures showed a larger-than-contraction, and more importantly, an advance estimate points to another drop in February. This suggests consumer spending might be in a weakening trend, raising fresh concerns about Canada’s economic momentum heading into Q2.

However, the selloff in the Loonie has been relatively limited so far. BoC Governor Tiff Macklem’s comments from Thursday may have offered some cushion. Macklem warned against allowing initial price spikes from tariffs to morph into broader inflationary pressures, highlighting the need for vigilance in monetary policy. This has fueled market speculation that BoC may pause its rate cutting cycle in April to better assess tariff impacts and inflation risks.

Meanwhile, Euro is coming under some pressure along with Germany’s DAX index, despite a historic win for the country’s fiscal policy. Germany’s Bundesrat passed a major spending package aimed at reviving growth and bolstering defense. However, traders seem to be locking in profits after weeks of rallying on anticipation of this very outcome, suggesting the news may have been fully priced in.

For the week so far, Swiss Franc is now the top performer, followed by Kiwi and then Loonie. Aussie lags at the bottom, trailed by Euro and Yen. Dollar and Pound are stuck in the middle of the pack.

Canadian retail sales down -0.6% mom in Jan, more contraction in Feb

Canada’s retail sales dropped -0.6% mom to CAD 69.4B in January, marking a steeper-than-expected decline and signaling subdued consumer spending.

The largest drag came from motor vehicle and parts dealers, while overall sales fell in three of nine subsectors.

Core retail sales, which strip out gasoline and auto-related purchases, also slipped -0.2%.

Adding to the concern, Statistics Canada's advance estimate suggests retail sales fell another -0.4% in February.

Japan’s CPI core slows less than expected to 3% in Feb

Japan’s core consumer inflation eased for the first time in four months in February, but less than market expectations. While the data strengthens the case for another BoJ rate hike at the April 30–May 1 meeting, policymakers may still choose to wait until July to better assess the impact of US tariff escalation and broader global financial market risks.

CPI core (excluding fresh food) slowed from 3.2% yoy to 3.0% yoy, slightly above expectations of 2.9%. The moderation was partly due to the resumption of government subsidies on utility bills. Despite this, core inflation has stayed above BoJ’s 2% target since April 2022.

More significantly, core-core CPI (excluding food and energy) rose from 2.5% yoy to 2.6% yoy, marking the fastest pace since March 2024. This continued strength in underlying inflation, even as services inflation softened slightly from 1.4% yoy to 1.3% yoy, reflects steady pass-through of higher labor costs.

Meanwhile, headline CPI slowed from 4.0% yoy to 3.7% yoy.

New Zealand posts NZD 510m trade surplus as exports surge across key markets

New Zealand posted a surprise trade surplus of NZD 510m in February, defying expectations of a NZD -235m deficit.

Goods exports jumped 16% yoy to NZD 6.7B, led by strong demand from key trading partners including China, Australia, and the EU. Notably, exports to China surged by 16% yoy, while shipments to Australia and the EU rose by 17% yoy and 37% yoy, respectively. The only major decline was seen in exports to the US, which slipped by -5.5% yoy.

Goods imports edged up a modest 2.1% yoy to NZD 6.2B, with notable volatility in country-level data. Imports from the US spiked 41% yoy, while those from South Korea plunged -57% yoy. Imports from Australia (-9.3% yoy) and the EU (-3.3% yoy)also declined. Despite the pickup from the US and China (3.8% yoy), subdued import figures from other regions helped tilt the trade balance into surplus.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 148.32; (P) 148.64; (R1) 149.10; More...

Intraday bias in USD/JPY remains neutral and outlook is unchanged. Corrective pattern from 146.52 might extend. But in case of stronger recovery, upside should be limited by 150.92 support turned resistance. On the downside, firm break of 148.17 support will bring retest of 146.52 first. Sustained trading below 61.8% retracement of 139.57 to 158.86 at 146.32 will resume the fall from 158.86 to 139.57 support.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

Canadian retail sales down -0.6% mom in Jan, more contraction in Feb

Canada’s retail sales dropped -0.6% mom to CAD 69.4B in January, marking a steeper-than-expected decline and signaling subdued consumer spending.

The largest drag came from motor vehicle and parts dealers, while overall sales fell in three of nine subsectors.

Core retail sales, which strip out gasoline and auto-related purchases, also slipped -0.2%.

Adding to the concern, Statistics Canada's advance estimate suggests retail sales fell another -0.4% in February.

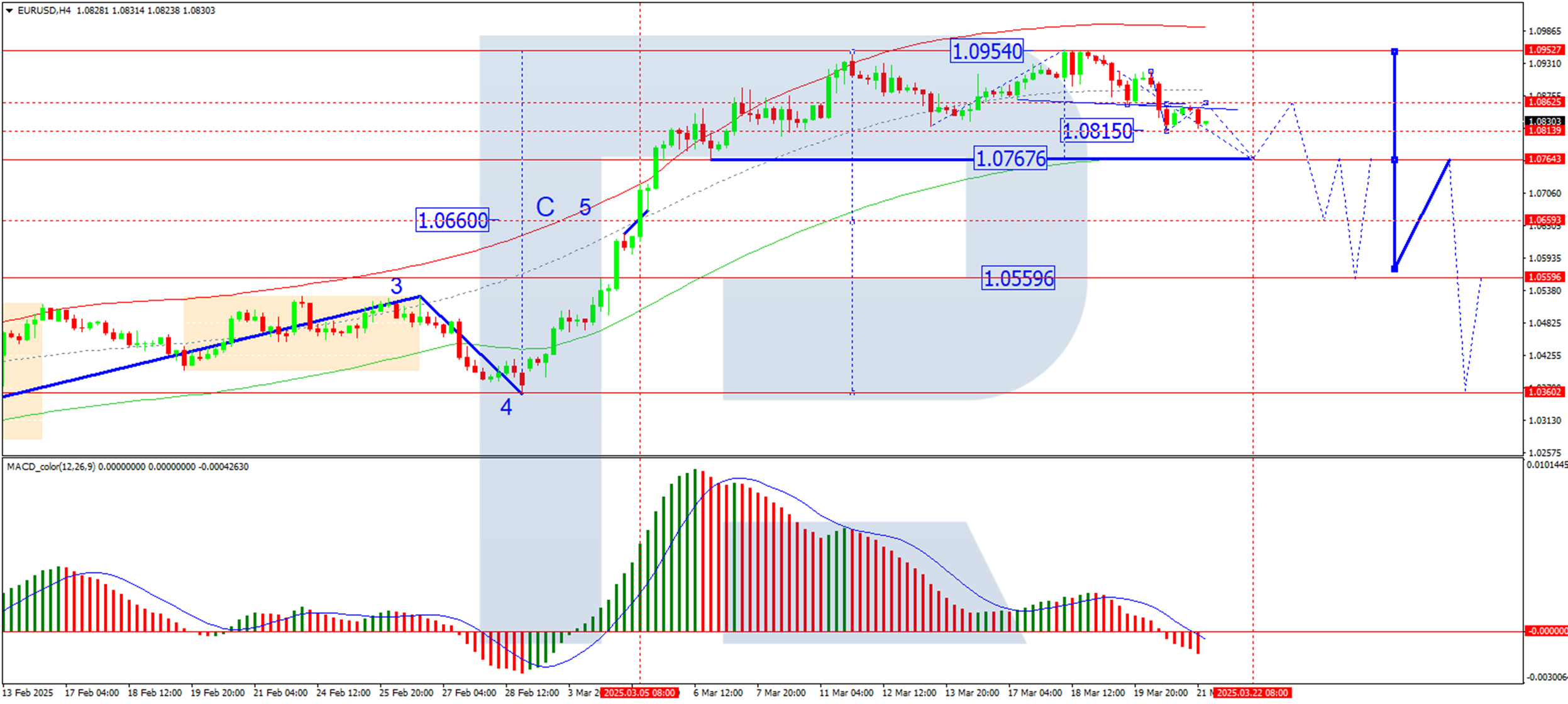

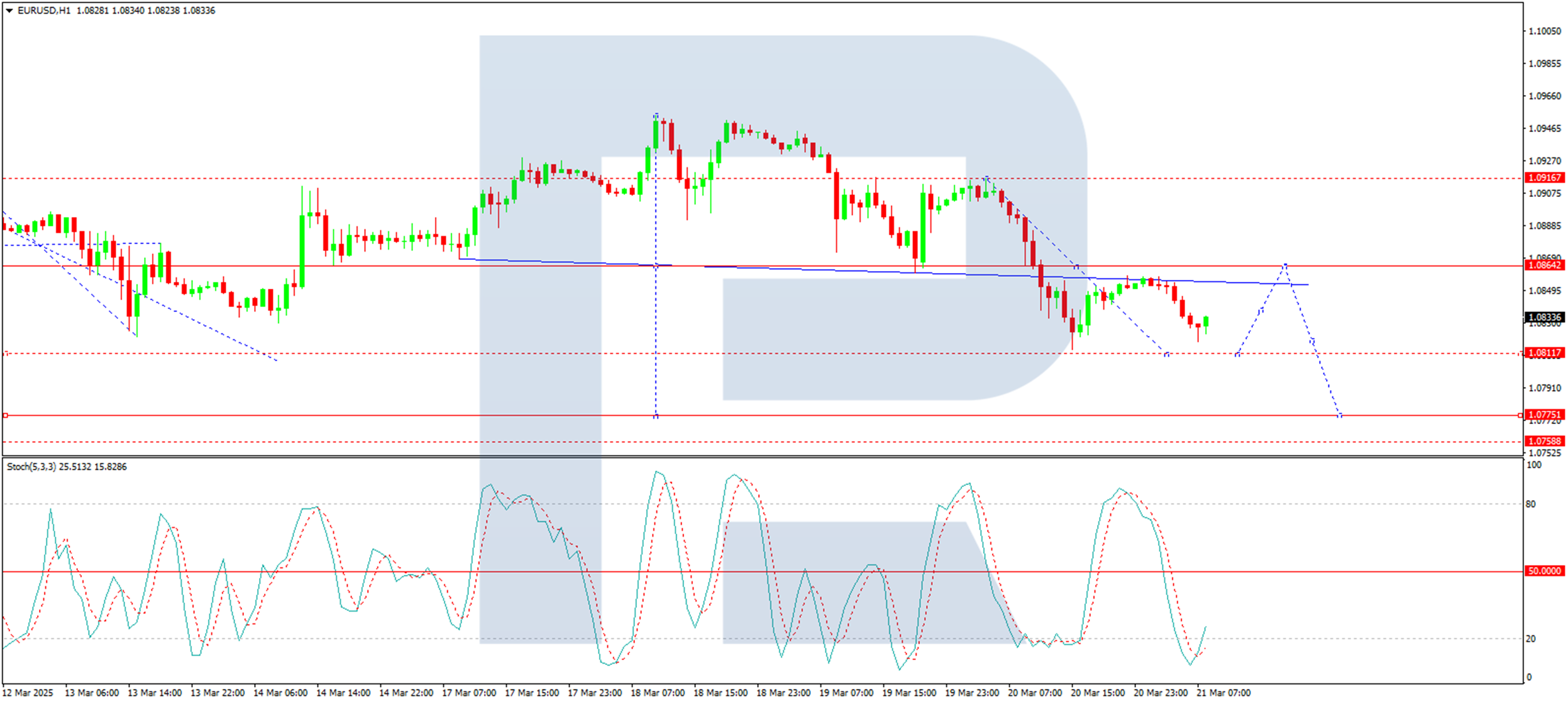

EURUSD Loses Momentum as Fed Bolsters the US Dollar

The EUR/USD pair is trending downward, approaching 1.0829 on Friday as investors evaluate the latest developments in US Federal Reserve monetary policy.

Key drivers behind EUR/USD movement

On Wednesday, the Federal Reserve held its current interest rate and overall monetary policy framework unchanged. However, the central bank signalled that two rate cuts could be expected later this year. In its commentary, the Fed highlighted growing risks to economic recovery, employment stability, and inflation trends.

Fed Chair Jerome Powell downplayed concerns about the inflationary impact of tariffs imposed by the Trump administration, describing them as temporary. Powell also emphasised that the Fed would not rush into further rate cuts, reinforcing a cautious approach to monetary easing.

Adding to market uncertainty, Trump’s retaliatory tariffs – targeting countries that have imposed duties on US goods – are set to take effect on 2 April. Over the past 24 hours, the US dollar has strengthened amid fears of slowing global economic growth and escalating trade tensions. These factors have reinforced risk-averse sentiment among investors.

Technical analysis of EUR/USD

On the H4 chart, EUR/USD declined to 1.0815, followed by a correction to 1.0860. A further decline towards 1.0765 is highly likely, with this level remaining the primary target. The MACD indicator supports this scenario. Its signal line is below zero, sloping sharply downward, indicating potential new lows.

On the H1 chart, EUR/USD broke through the 1.0864 level and formed a bearish wave structure, reaching 1.0815. Today, a corrective move towards 1.0860 (testing from below) is likely. Once this correction concludes, the pair could resume its downward trajectory, targeting 1.0811. This movement marks the third wave of the downtrend. After reaching this level, another retracement towards 1.0864 is possible. The Stochastic oscillator supports this outlook, with its signal line below 20 and trending upward towards the 50 level.

Conclusion

The EUR/USD pair remains under pressure as the Fed’s cautious stance and global trade tensions bolster the US dollar. Technical indicators suggest further downside potential, with key support levels at 1.0765 and 1.0811. Investors should monitor upcoming economic data and trade developments for additional insights into the pair’s direction.

GBP/USD Analysis: Pair Fails to Hold Above Psychological Level

As shown in today’s GBP/USD chart, the pair failed to maintain its position above the psychological level of 1.3000 USD per pound, where it had reached its highest point since early 2025. The decline followed recent central bank decisions and statements, with both the Bank of England and the Federal Reserve keeping interest rates unchanged.

On one side, the Bank of England:

→ Warned of inflation risks, partly driven by external factors such as US trade tariffs.

→ Indicated a potential rate cut in the coming months.

On the other hand, the US dollar strengthened on Thursday after the Federal Reserve signalled reluctance to rush further rate cuts this year, despite uncertainties surrounding US tariffs.

These statements highlighted the challenges market participants face in assessing the risks posed by tariffs on global trade.

Technical Analysis of GBP/USD

In March, the pound followed an upward trend against the US dollar, forming an ascending channel (marked in blue). However, once the price moved above the key 1.3000 level, the upper boundary of the channel appeared out of reach—possibly signalling weakening buying momentum.

As a result, the price broke below the lower boundary of the channel, which has now shown signs of resistance (indicated by an arrow). If bearish pressure persists, the price could fall towards the dotted trendline below the channel, at a distance equal to its height. Additionally, a test of the previous local low around 1.2911 cannot be ruled out.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Elliott Wave View: Silver (XAGUSD) Pullback Remains Supported

Short Term Elliott Wave view in Silver (XAGUSD) suggests rally from 2.28.2025 low is in progress as a 5 waves impulse. Up from 2.28.2025 low, wave ((i)) ended at 32.76 and pullback in wave ((ii)) ended at 31.79 as a zigzag structure. Down from wave ((i)), wave (a) ended at 32.08 and wave (b) ended at 32.66. Wave (c) lower ended at 31.79 which completed wave ((ii)). Up from there, wave ((iii)) higher unfolded as a 5 waves impulse in lesser degree.

Up from wave ((ii)), wave (i) ended at 33.31 and dips in wave (ii) ended at 32.92. Wave (iii) higher ended at 34.08 and pullback in wave (iv) ended at 33.41. The final leg wave (v) ended at 34.23 which completed wave ((iii)) in higher degree. Pullback in wave ((iv)) is proposed complete with internal subdivision as a zigzag. Down from wave ((iii)), wave (a) ended at 33.43 and wave (b) ended at 33.94. Wave (c) lower ended at 33.07 which completed wave ((iv)). Near term, as far as pivot at 31.79 low stays intact, expect pullback to find support in 3, 7, or 11 swing for further upside.

Silver (XAGUSD) 45 Minutes Elliott Wave Chart

XAGUSD Video

https://www.youtube.com/watch?v=HKTiXBC6YuA

Bitcoin (BTC/USD) Analysis: Trump Impact, Whale Activity & Price Predictions

- Bitcoin's price dipped despite initial gains following President Trump's crypto event appearance.

- New "whale" investors have accumulated a large amount of Bitcoin, suggesting potential for a near-term price increase, but on-chain data shows weakening demand and liquidity.

- Bitcoin ETF flows turn negative after four consecutive days of gains as Gold ETFs thrive. A change in market dynamics?

Bitcoin failed to maintain the bullish momentum from yesterday as it finally broke above the 200-day MA. This all came about in anticipation of US President Trump’s speech at Blockwork’s crypto digital asset summit.

On Thursday, President Donald Trump shared a video at a crypto event, showing his support for cryptocurrency and claiming it will boost economic growth. However, he didn’t announce any new policies as attendees had expected.

The question though is why did Bitcoin fail to hold onto the gains made in anticipation of Trump's address?

The answer is simple, markets were buoyed by hopes that President Trump would address issues like debanking or crypto taxes, possibly with a new executive order. However, he didn’t announce any new actions and simply repeated what his administration has already done.

This was already priced in and with no new proclamations by the President, markets seemed to have lost its bullish momentum. Markets have however started today with a bit of a bullish move with the world's largest cryptocurrency up around 0.3% at the time of writing.

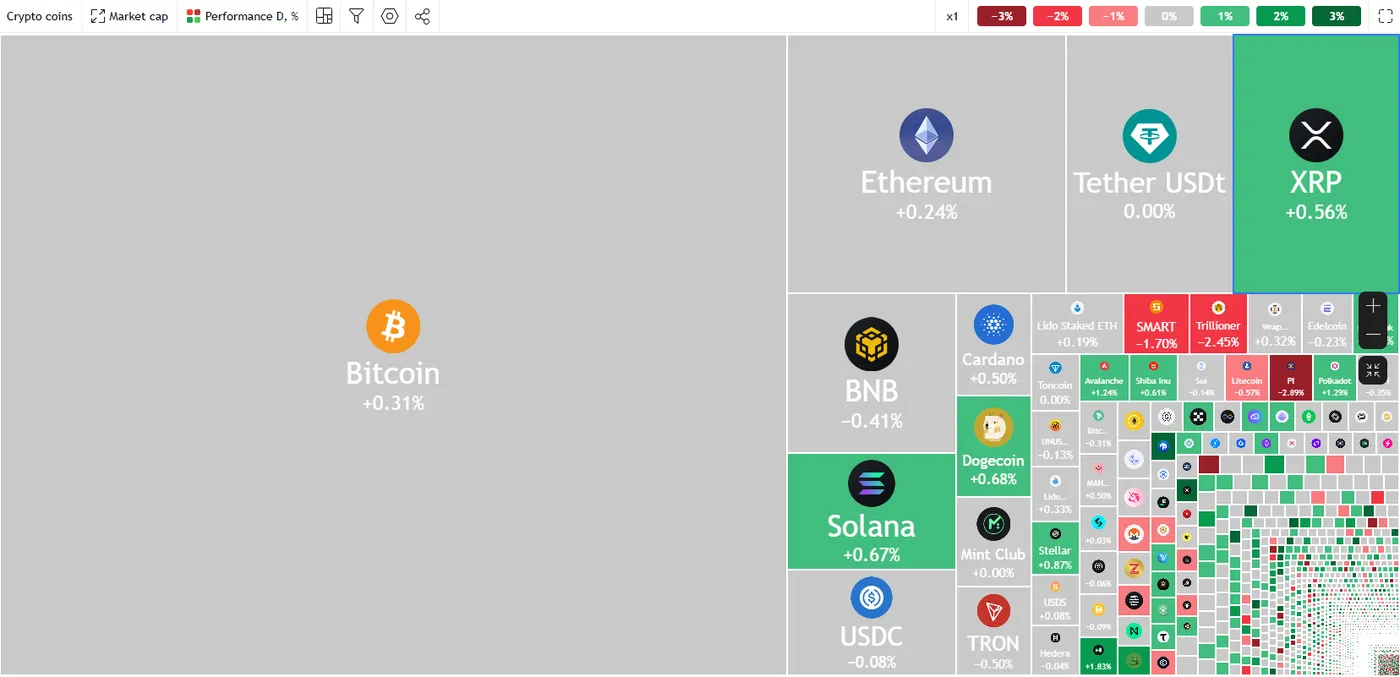

Crypto Heatmap, March 21, 2025

Source: TradingView

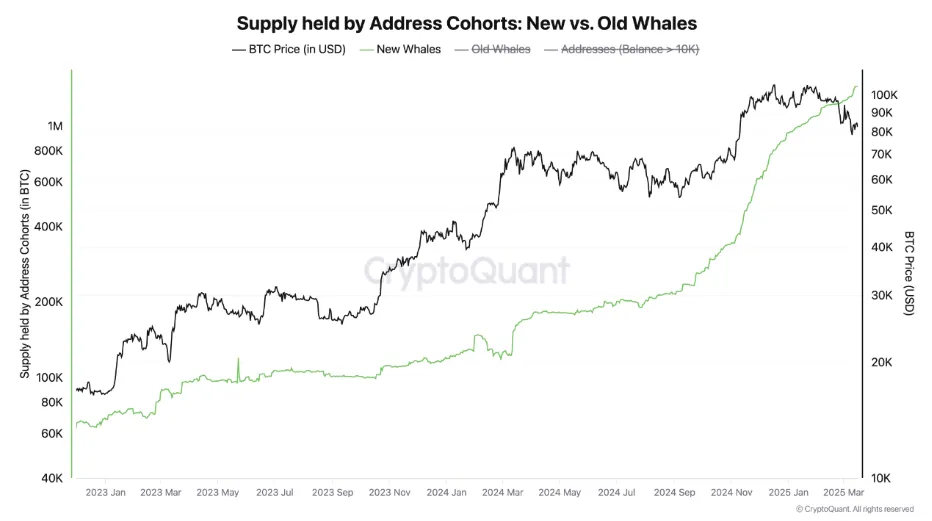

1 Million Bitcoin In New Whale Hands, A New Rally on the Way?

A new group of wealthy Bitcoin investors is diving into the cryptocurrency. Since late November, they’ve collected over a million Bitcoins, including 200,000 just last month.

Research from CryptoQuant shows these “new whales,” each holding at least 1,000 Bitcoin, are mostly beginners who’ve owned their coins for less than six months. They’re not in it for the long haul—they’re here for quick profits.

Market experts say when big players buy like this, it’s usually because they expect prices to rise soon, not years down the line, based on their fast-paced buying strategy.

Source: CryptoQuant

Will such a move come to fruition? Let us take a look at what Glassnode on-chain data tells us.

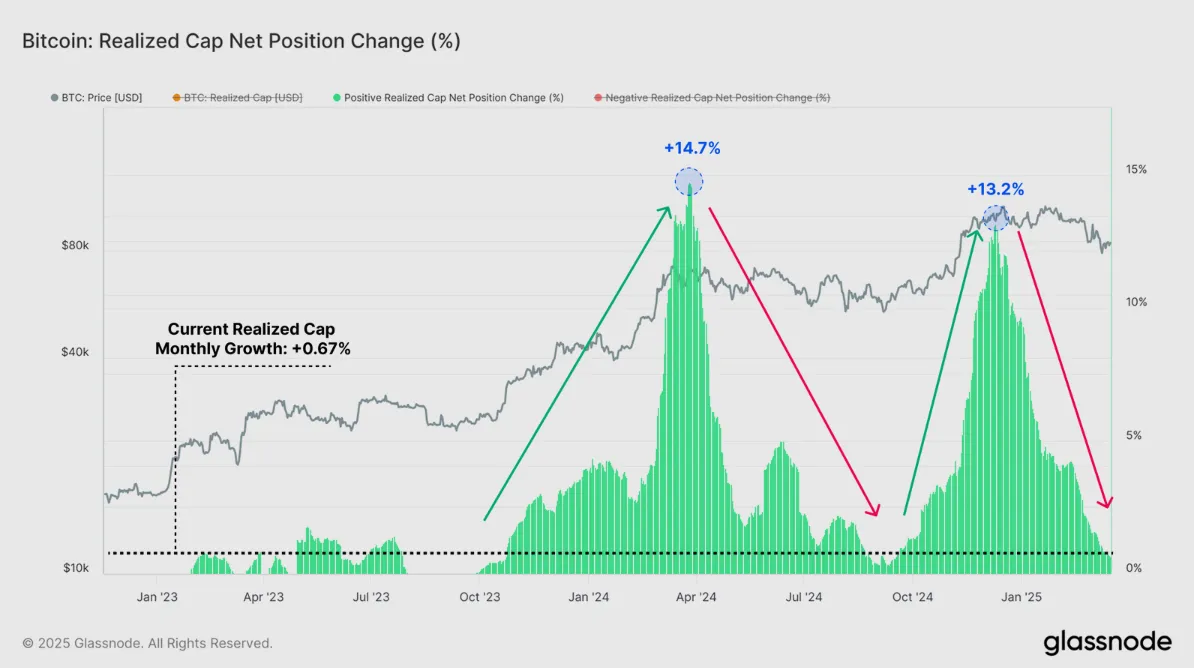

Glassnode - The Week On-Chain

Bitcoin’s price has lost around 30% from its highs with Glassnode stating that liquidity continues to contract across on-chain and spot markets, with net capital inflows grinding to a halt, and exchange inflows slowing down.

Meanwhile, long-term holders are staying inactive, adding to the view of a slow market with little movement in prices.

Liquidity is shrinking, contributing to the drop in value. New money flowing into Bitcoin has slowed significantly, with its Realized Cap growing by just +0.67% per month.

This leads to two main takeaways:

- There isn’t enough new money coming in to push prices higher.

- Volatility is expected to stay high as the market shifts from being profit-driven to a more balanced state.

Source: Glassnode

The ‘Hot Supply’ metric is one way to measure active capital in the market. It tracks the amount of wealth in coins that are one week old or less, acting as a gauge for coins ready to be traded.

Currently, the wealth held by the Hot Supply group has dropped from 5.9% of the circulating supply to just 2.8%. This is a more than 50% decrease in liquid coins, showing a reduced interest in trading and speculation.

A similar pattern is seen in exchange inflows, where daily Bitcoin inflows have fallen from +58.6k BTC at the market peak to +26.9k BTC now, a drop of over 54%. This matches the earlier noted decline in investor sentiment and market capital flows.

The similar scale of decline in both Hot Supply and Exchange Inflows highlights weaker overall demand in the market. This does not point to an imminent rally, does it?

ETF Flows

Bitcoin ETF flows marked a fourth consecutive day of net inflows with $11.8 million added. This is a small amount considering what we have seen in the past with only Bitwise’s BITB, Grayscale GBTC and BTC recording inflows.

This four-day run was snapped on March 20 however, with net outflows of $6.4 million. This decline in ETF flows support Glassnode's data of weaker overall demand in the market.

This also comes as Gold ETF flows have recently surpassed Bitcoin ETF flows. To read more about this, read: Gold Price Outlook: ETF Flows, Central Bank Buying, and XAU/USD Price Targets.Is this the start of a broader market shift and risks continue to rise in global markets?

Technical Analysis - BTC/USD

Bitcoin (BTC/USD) from a technical standpoint on the daily timeframe remains in a bearish trend.

A daily candle close above the 90000 handle will be needed for a change in structure and this remains some distance away at present.

Wednesday did see a rise above the 200-day MA which should have been a precursor for further gains. However yesterday saw a significant pullback as Bitcoin finished the day 3.12% down and back below the 200-day MA.

The 85000 handle is key now as the 200-Day MA rests here as well.

The 14-period RSI also shows signs that the bearish trend remains intact. The 50 neutral level is serving as resistance and a break above is also needed to show a shift in momentum.

A move above 85000 now faces resistance at 86845 before the 90000 handle comes into focus.

Looking at areas of support and we have the 82133 handle before the 80000 psychological handle comes back into focus.

Bitcoin (BTC/USD) Daily Chart, March 21, 2025

Source: TradingView.com

Support

- 82133

- 80000

- 78197

Resistance

- 85000

- 86845

- 90000

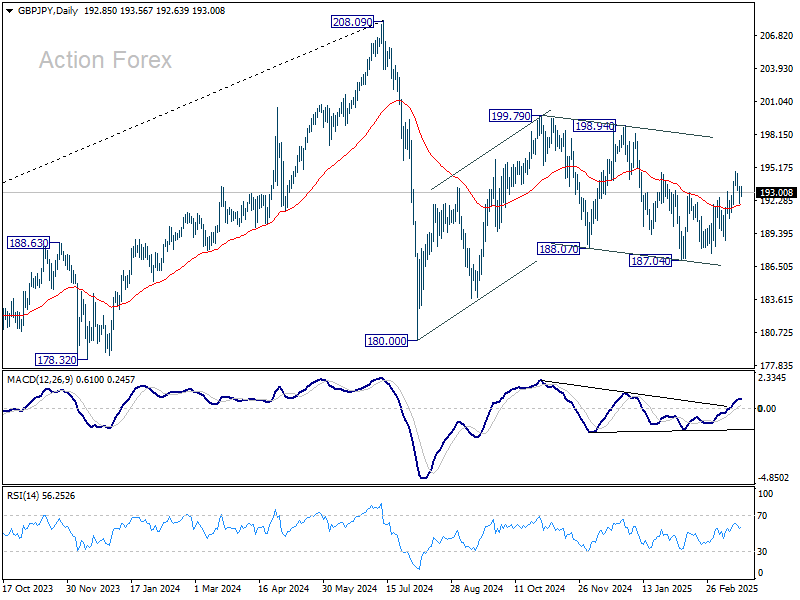

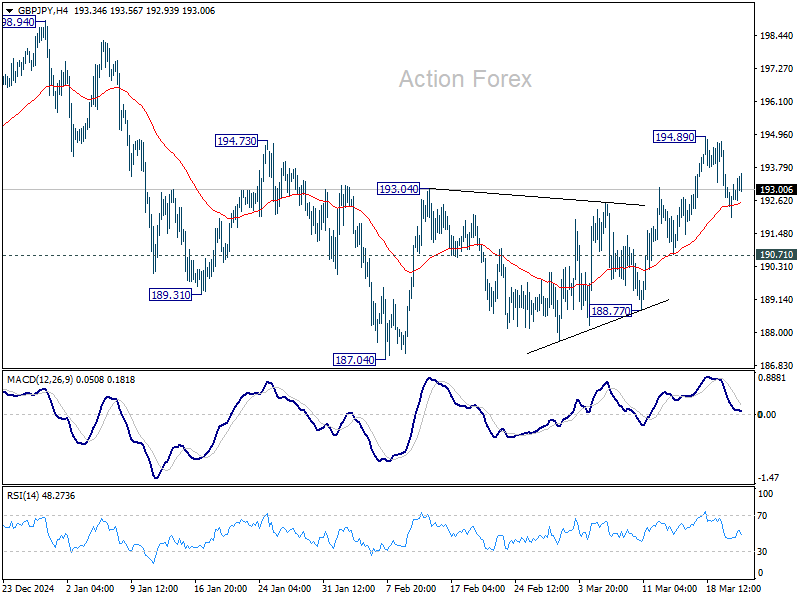

GBP/JPY Daily Outlook

Daily Pivots: (S1) 192.12; (P) 192.86; (R1) 193.66; More...

Intraday bias in GBP/JPY remains neutral for the moment. On the upside, break of 194.89 will resume the rebound from 187.04 to 198.94/199.79 resistance zone. Nevertheless, break of 190.71 support will turn bias back to the downside for 188.77. Overall, corrective pattern from 208.09 is still in progress, with price actions from 180.00 as the second leg.

In the bigger picture, price actions from 208.09 are seen as a correction to rally from 123.94 (2020 low). Strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.