Sample Category Title

Yen Rebounds on Risk-Off Mood in Asia, Focus Shifts to SNB and BoE

Asian markets are showing signs of mild risk-off sentiment today, with Hong Kong and China stocks retreating from recent gains. The weaker regional tone contributed to a stronger Yen. Additionally, Yen’s rebound is also fueled by post-FOMC Dollar softness. The technical picture suggests that the recent pullback in Yen against Dollar has likely run its course, allowing the currency to regain some ground.

Meanwhile, the weaker regional sentiment has put pressure on New Zealand Dollar, despite the strong GDP data that showed the country exiting recession. Aussie is also under pressure, not just due to the broader market risk aversion but also because of softer-than-expected employment data, which saw a surprise contraction in jobs. While both the Kiwi and Aussie have had some resilience earlier this week, today's price action suggests that traders are probably turning more cautious.

SNB rate decision will be the first major focus in the European session, with the central bank widely expected to deliver another 25bps rate cut. A key question is whether SNB signals that the current easing cycle is nearing its end. Attention will then shift to BoE, which is widely expected to keep its benchmark interest rate steady. The focus will be on the voting composition within the MPC.

For the week so far, Dollar is currently the worst performer, followed by Euro and Aussie. On the other hand, Swiss Franc is the strongest, followed by Kiwi and Sterling. Loonie and Yen are positioning in the middle, with Yen's outlook improving due to today’s risk-off flows.

In Asia, Japan is on holiday. Hong Kong HSI is down -1.51%. China Shanghai SSE is down -0.25%. Singapore Strait Times is up 0.67%. Overnight, DOW rose 0.92%. S&P 500 rose 1.08%. NASDAQ rose 1.41%. 10-year yield fell -0.025 to 4.256.

US stocks recovered as Fed sticks to two rate cut outlook for 2025

US stocks closed higher overnight, and extended their near-term consolidations. Investors were somewhat relieved that Fed maintained its outlook for two rate cuts this year. However, the central bank also introduced a note of caution, warning in its statement that “uncertainty around the economic outlook has increased” and that it remains “attentive to the risks to both sides of its dual mandate.”

In the post-meeting press conference, Chair Jerome Powell explicitly addressed the impact of tariffs. He warned that “the arrival of tariff inflation may delay further progress” on disinflation. He also noted that Fed’s quarterly summary of economic projections does not show further downward progress on inflation this year, attributing this to new tariffs coming into effect.

This acknowledgment reinforces the stance that while rate cuts remain in the pipeline, the timing and extent of policy easing will depend on how inflation evolves in the face of trade disruptions and supply chain adjustments.

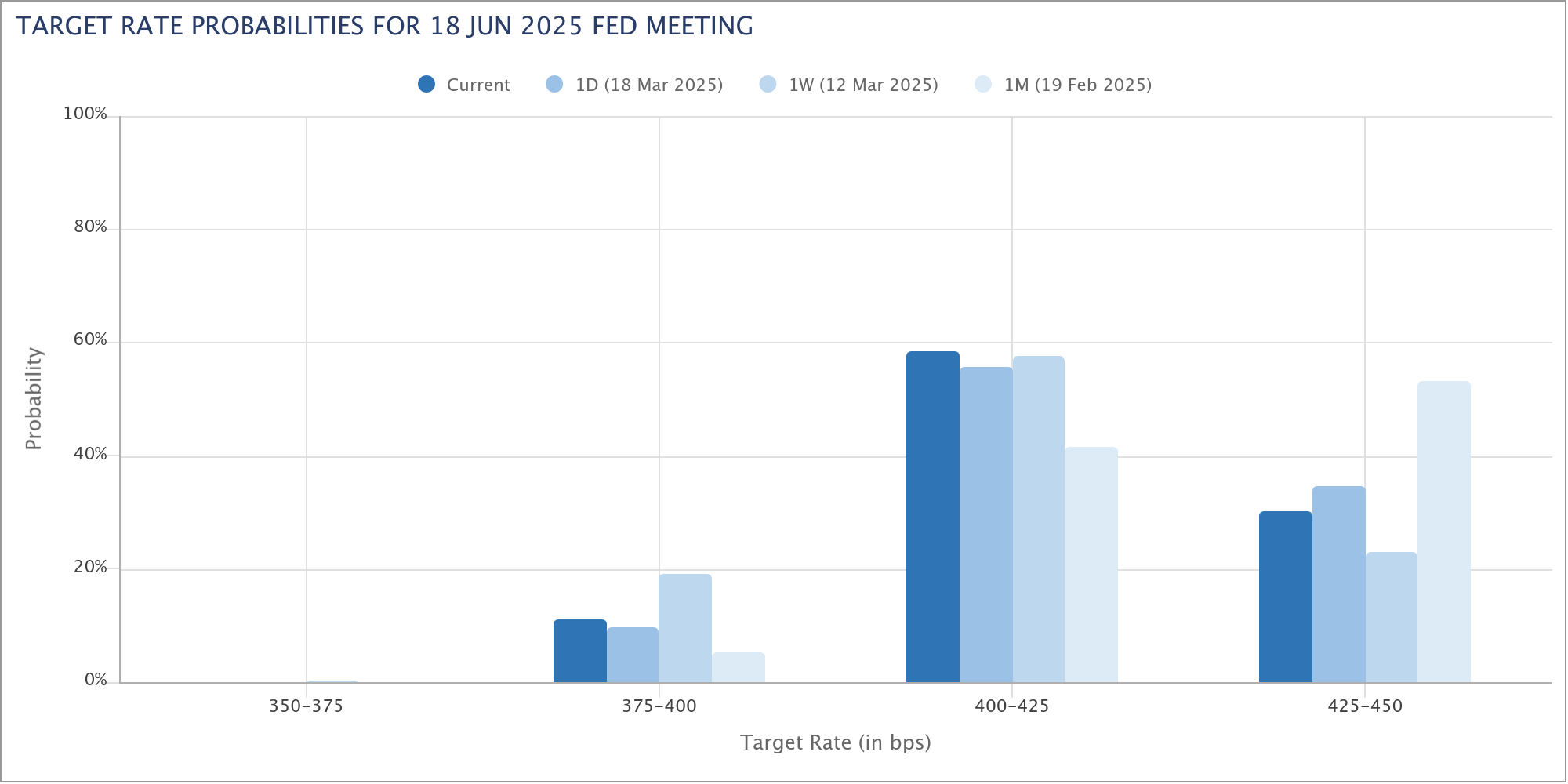

Fed left its benchmark interest rate unchanged at 4.25-4.50%, a widely expected move. Fed fund futures now assign roughly 70% probability that the next rate cut will come in June, compared to just 47% a month ago.

Technically, S&P 500 turned into consolidations after falling to 5504.65 last week. 55 W EMA (now at 5596.07) could offer some support for a near term recovery. But risk will stay on the downside as long as 55 D EMA (now at 5873.77) holds.

On resumption, fall from 6147.43, as a correction to the rise from 3491.58, should target 38.2% retracement at 5132.89.

New Zealand GDP exits recession with stronger-than-expected 0.7% qoq growth in Q4

New Zealand’s economy expanded by 0.7% qoq in Q4, surpassing expectations of 0.4% qoq and officially pulling the country out of recession. However, the broader picture remains mixed, as GDP still declined by -0.5% yoy, reflecting the lingering impact of previous contractions.

The positive quarterly growth was driven by expansions in 11 out of 16 industries, with the rental, hiring, and real estate sector, retail trade, and healthcare services leading the gains.

Despite the overall improvement, some key sectors struggled, with construction and information media & telecommunications posting declines.

Still, a major positive takeaway from the report is that GDP per capita rose by 0.4% in Q4, marking its first increase in two years.

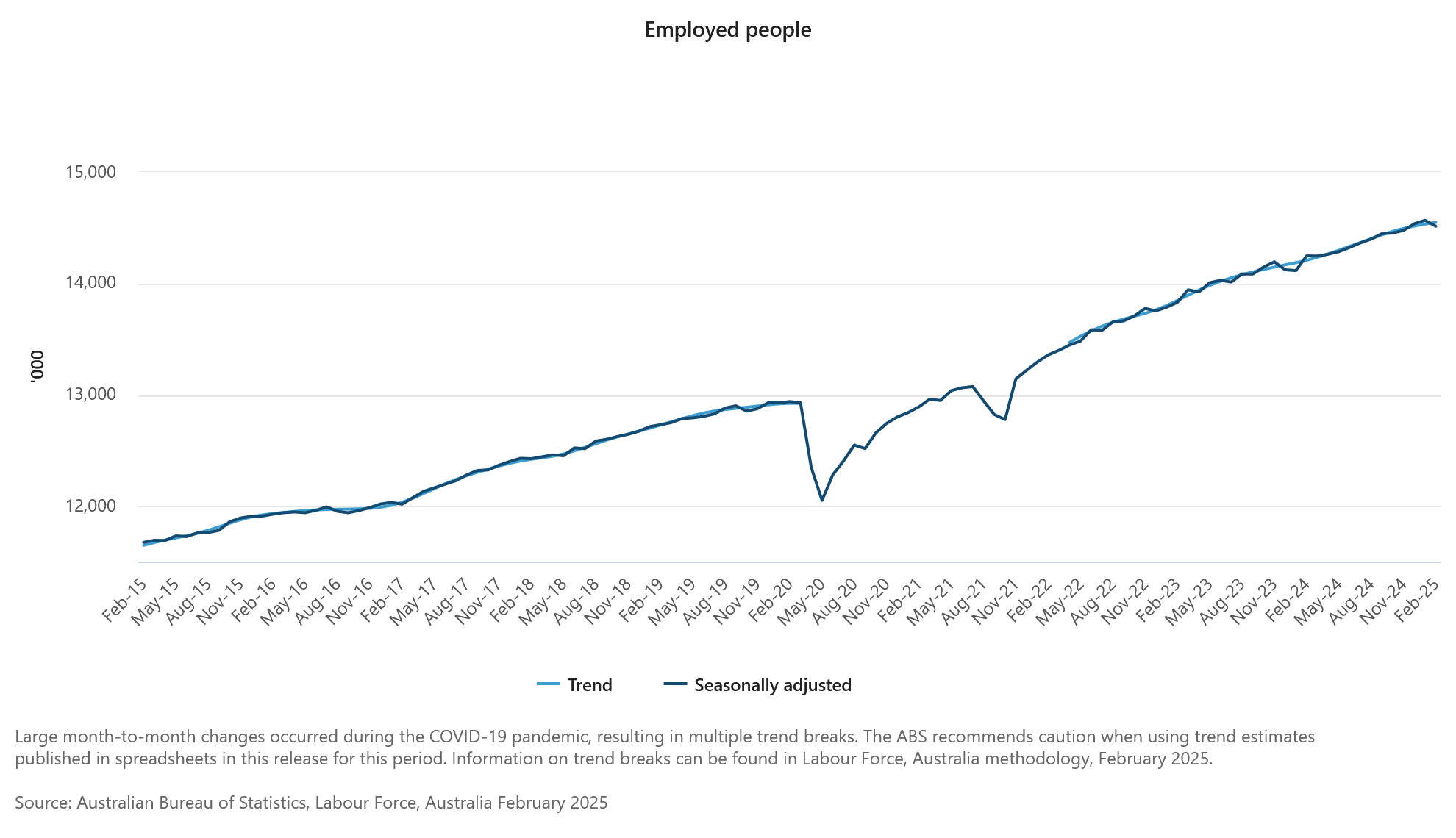

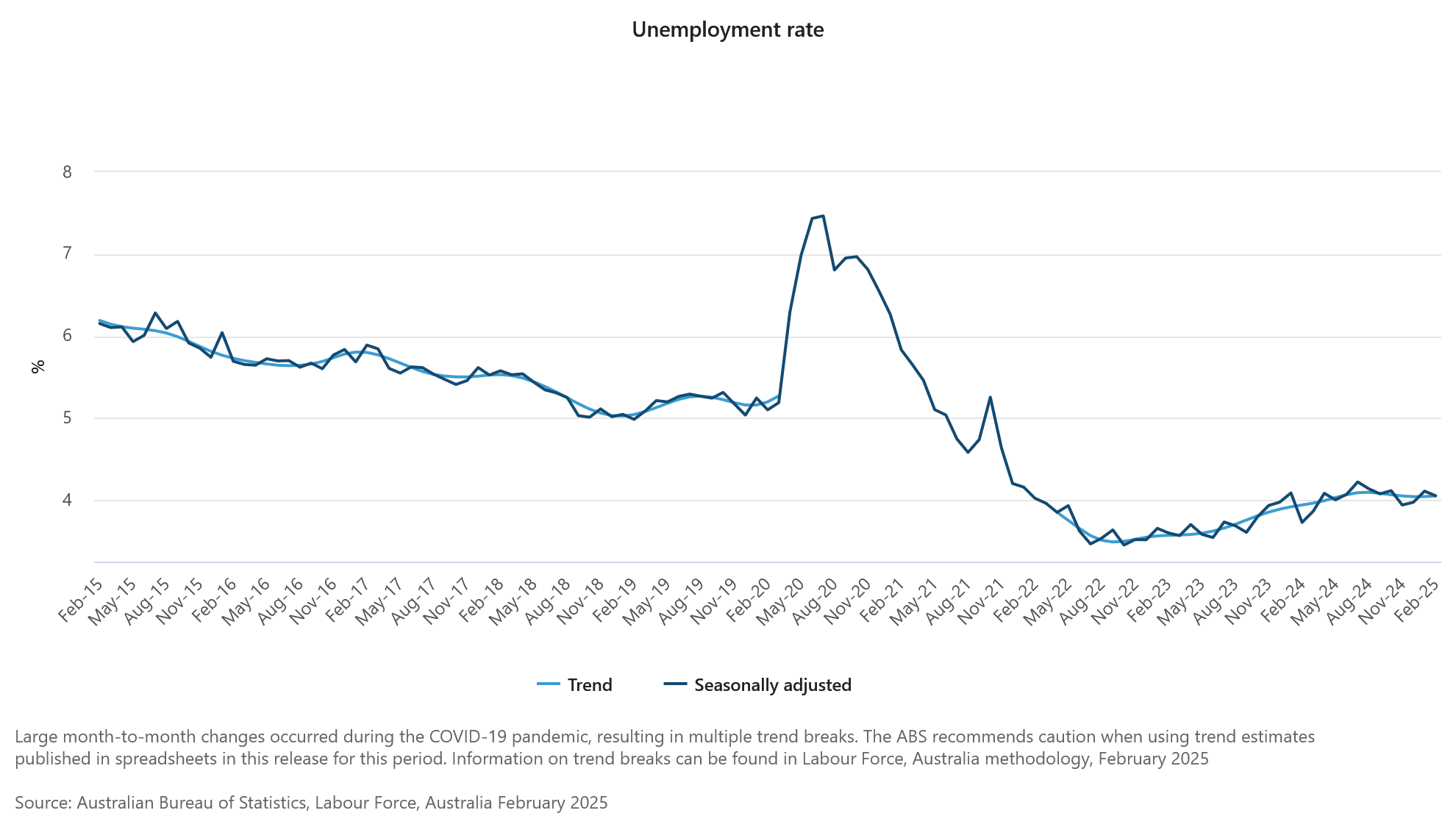

Australian employment plunges -52.8k in Feb, unemployment rate unchanged at 4.1%

Australia’s employment dropped sharply by -52.8k in February, significantly missing market expectations of 30k gain. The decline was broad-based, with full-time jobs falling by -35.7k and part-time employment down by -17k.

Unemployment rate remained steady at 4.1%, in line with forecasts. The participation rate declined by -0.4% to 66.8%, suggesting that fewer people were actively seeking work, which helped keep the jobless rate from rising. Additionally, monthly hours worked fell by -0.4% mom, reflecting softer labor market conditions.

The Australian Bureau of Statistics attributed part of the decline in employment to fewer older workers re-entering the labor force. However, the broader trend still points to resilience in the job market, with employment up by 266k people, or 1.9%, compared to last year. The annual employment growth rate remains close to the 20-year pre-pandemic average of 2.0%.

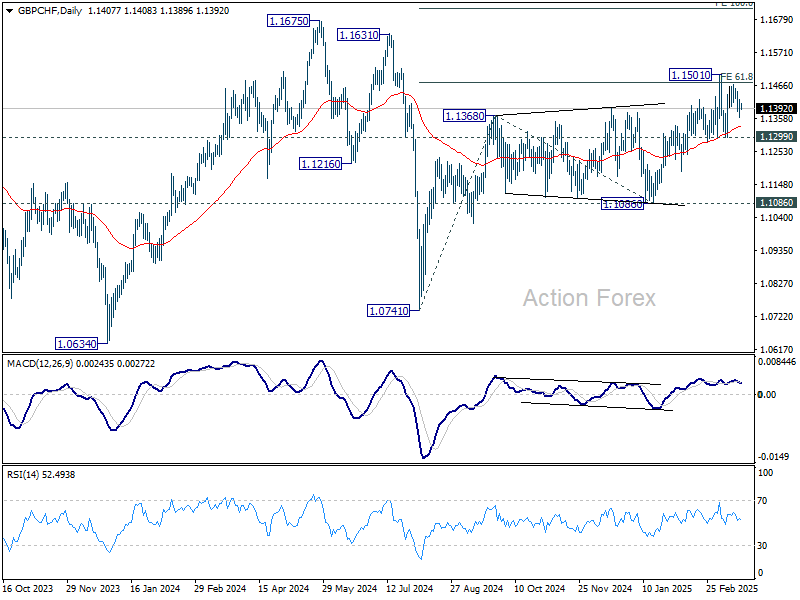

SNB to cut, BoE to hold, a look at GBP/CHF

Two major central banks will announce their monetary policy decisions today, with SNB leading, followed by BoE.

SNB is widely expected to lower its policy rate by 25bps to 0.25%. With inflation at just 0.3% in February, well below the mid-point of target range, there is both room and necessity for further easing to keep medium-term inflation expectations anchored closer to 1%.

However, the urgency for additional policy support appears to be diminishing, especially with growing optimism around Eurozone economy. Stronger Eurozone growth, driven by major fiscal expansion plans, is expected to lift Euro and boost demand for Swiss exports, which could help mitigate recession and deflation risks in Switzerland.

A Reuters poll of economists showed that most expect rates to remain at 0.25% by year-end, while 10 foresee a move to 0%, and only three expect SNB to maintain the current 0.50% level.

Meanwhile, BoE is widely expected to hold its Bank Rate steady at 4.5%, with little change to its cautious forward guidance. A Reuters poll of 61 economists showed unanimous expectations for a rate hold today, with the next cuts projected for May, August, and November.

The key focus for markets will be whether any additional Monetary Policy Committee members join Catherine Mann and Swati Dhingra in voting for an immediate rate cut, which could signal a shift toward a more dovish stance in the coming months.

Technically, while GBP/CHF extended the rally from 1.1086, it has clearly struggled to find convincing momentum. It's plausible that this rise is the third leg of the corrective rebound from 1.0741, which has already completed after meeting 61.8% projection of 1.0741 to 1.1368 from 1.1086 at 11437. Break of 1.1299 support will solidify this bearish case and bring deeper fall back to 1.1086 support. Nevertheless firm break of 1.1501 will pave the way to 1.1675 resistance next.

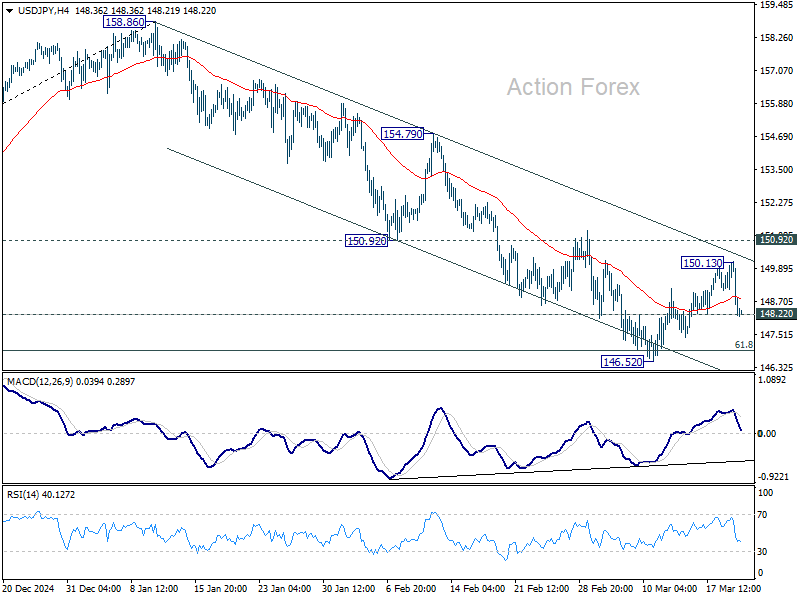

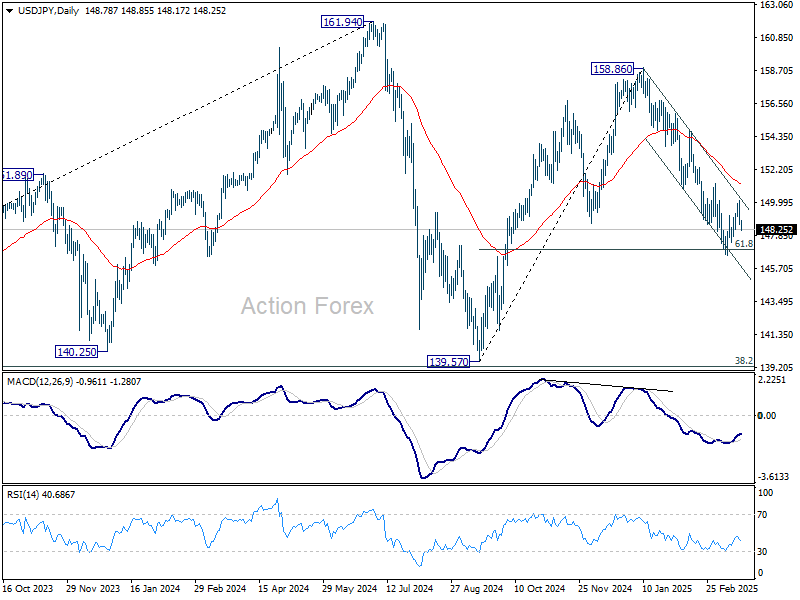

USD/JPY Daily Outlook

Daily Pivots: (S1) 148.15; (P) 149.15; (R1) 149.69; More...

USD/JPY's currently steep decline suggests rejection by near term falling channel resistance. Immediate focus is now on 148.22 minor support. Firm break there will indicate that corrective rebound from 146.52 has completed and bring retest of this low first. Sustained trading below 61.8% retracement of 139.57 to 158.86 at 146.32 will resume the fall from 158.86 to 139.57 support. In case of another recovery, upside should be limited by 150.92 support turned resistance.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

SNB to cut, BoE to hold, a look at GBP/CHF

Two major central banks will announce their monetary policy decisions today, with SNB leading, followed by BoE.

SNB is widely expected to lower its policy rate by 25bps to 0.25%. With inflation at just 0.3% in February, well below the mid-point of target range, there is both room and necessity for further easing to keep medium-term inflation expectations anchored closer to 1%.

However, the urgency for additional policy support appears to be diminishing, especially with growing optimism around Eurozone economy. Stronger Eurozone growth, driven by major fiscal expansion plans, is expected to lift Euro and boost demand for Swiss exports, which could help mitigate recession and deflation risks in Switzerland.

A Reuters poll of economists showed that most expect rates to remain at 0.25% by year-end, while 10 foresee a move to 0%, and only three expect SNB to maintain the current 0.50% level.

Meanwhile, BoE is widely expected to hold its Bank Rate steady at 4.5%, with little change to its cautious forward guidance. A Reuters poll of 61 economists showed unanimous expectations for a rate hold today, with the next cuts projected for May, August, and November.

The key focus for markets will be whether any additional Monetary Policy Committee members join Catherine Mann and Swati Dhingra in voting for an immediate rate cut, which could signal a shift toward a more dovish stance in the coming months.

Technically, while GBP/CHF extended the rally from 1.1086, it has clearly struggled to find convincing momentum. It's plausible that this rise is the third leg of the corrective rebound from 1.0741, which has already completed after meeting 61.8% projection of 1.0741 to 1.1368 from 1.1086 at 11437. Break of 1.1299 support will solidify this bearish case and bring deeper fall back to 1.1086 support. Nevertheless firm break of 1.1501 will pave the way to 1.1675 resistance next.

Australian employment plunges -52.8k in Feb, unemployment rate unchanged at 4.1%

Australia’s employment dropped sharply by -52.8k in February, significantly missing market expectations of 30k gain. The decline was broad-based, with full-time jobs falling by -35.7k and part-time employment down by -17k.

Unemployment rate remained steady at 4.1%, in line with forecasts. The participation rate declined by -0.4% to 66.8%, suggesting that fewer people were actively seeking work, which helped keep the jobless rate from rising. Additionally, monthly hours worked fell by -0.4% mom, reflecting softer labor market conditions.

The Australian Bureau of Statistics attributed part of the decline in employment to fewer older workers re-entering the labor force. However, the broader trend still points to resilience in the job market, with employment up by 266k people, or 1.9%, compared to last year. The annual employment growth rate remains close to the 20-year pre-pandemic average of 2.0%.

New Zealand GDP exits recession with stronger-than-expected 0.7% qoq growth in Q4

New Zealand’s economy expanded by 0.7% qoq in Q4, surpassing expectations of 0.4% qoq and officially pulling the country out of recession. However, the broader picture remains mixed, as GDP still declined by -0.5% yoy, reflecting the lingering impact of previous contractions.

The positive quarterly growth was driven by expansions in 11 out of 16 industries, with the rental, hiring, and real estate sector, retail trade, and healthcare services leading the gains.

Despite the overall improvement, some key sectors struggled, with construction and information media & telecommunications posting declines.

Still, a major positive takeaway from the report is that GDP per capita rose by 0.4% in Q4, marking its first increase in two years.

US stocks recovered as Fed sticks to two rate cut outlook for 2025

US stocks closed higher overnight, and extended their near-term consolidations. Investors were somewhat relieved that Fed maintained its outlook for two rate cuts this year. However, the central bank also introduced a note of caution, warning in its statement that “uncertainty around the economic outlook has increased” and that it remains “attentive to the risks to both sides of its dual mandate.”

In the post-meeting press conference, Chair Jerome Powell explicitly addressed the impact of tariffs. He warned that “the arrival of tariff inflation may delay further progress” on disinflation. He also noted that Fed’s quarterly summary of economic projections does not show further downward progress on inflation this year, attributing this to new tariffs coming into effect.

This acknowledgment reinforces the stance that while rate cuts remain in the pipeline, the timing and extent of policy easing will depend on how inflation evolves in the face of trade disruptions and supply chain adjustments.

Fed left its benchmark interest rate unchanged at 4.25-4.50%, a widely expected move. Fed fund futures now assign roughly 70% probability that the next rate cut will come in June, compared to just 47% a month ago.

Technically, S&P 500 turned into consolidations after falling to 5504.65 last week. 55 W EMA (now at 5596.07) could offer some support for a near term recovery. But risk will stay on the downside as long as 55 D EMA (now at 5873.77) holds.

On resumption, fall from 6147.43, as a correction to the rise from 3491.58, should target 38.2% retracement at 5132.89.

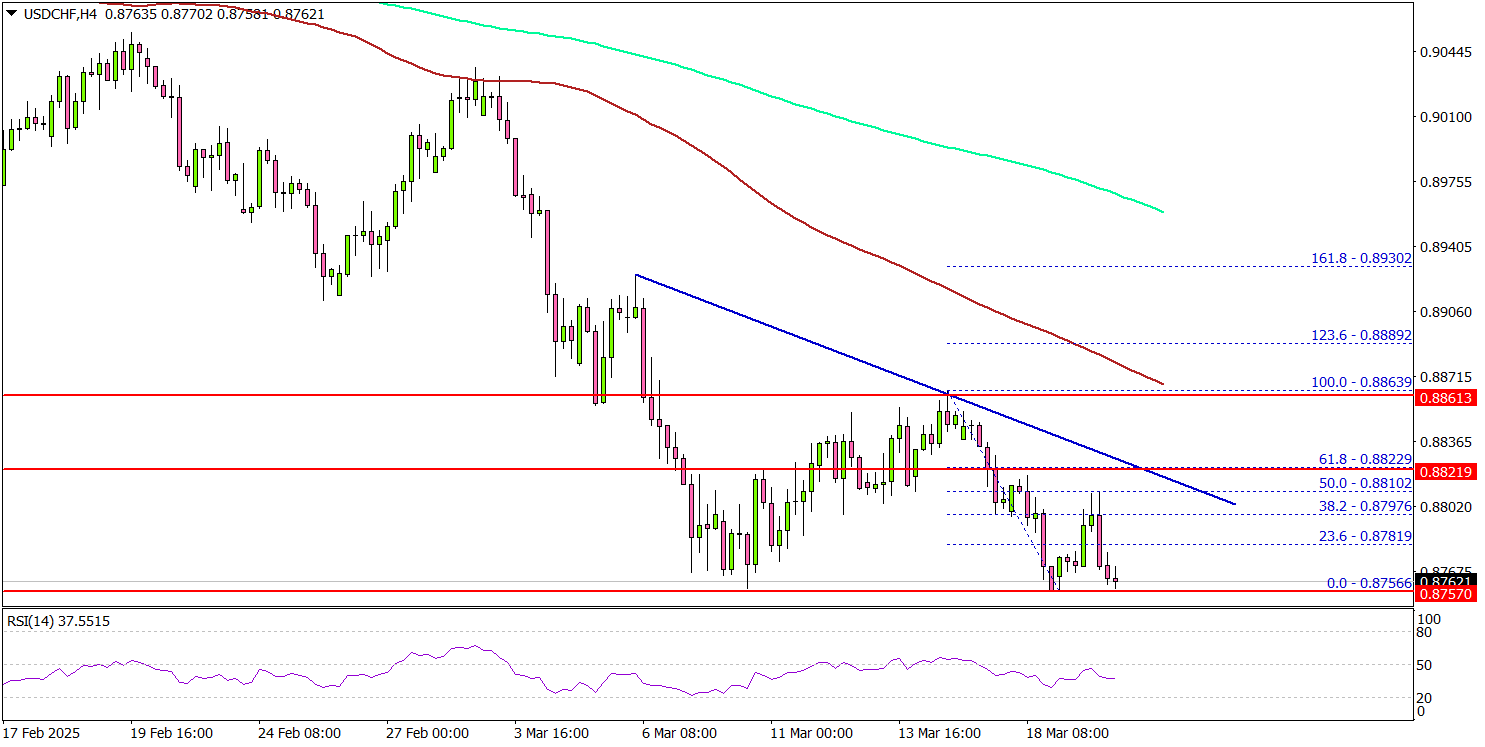

USD/CHF Recovery Could Stall—Key Resistance Levels Ahead

Key Highlights

- USD/CHF started a consolidation phase above the 0.8755 level.

- A connecting bearish trend line is forming with resistance at 0.8825 on the 4-hour chart.

- EUR/USD started a minor pullback from the 1.0950 resistance zone.

- Gold remained elevated above the $3,030 zone.

USD/CHF Technical Analysis

The US Dollar declined heavily below the 0.8850 level against the Swiss Franc. USD/CHF even spiked toward 0.8750 before it found some support.

Looking at the 4-hour chart, the pair settled below the 0.8825 level, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour). The pair started a consolidation phase and might face many hurdles.

On the upside, the pair is facing resistance near the 0.8825 level. There is also a connecting bearish trend line forming with resistance at 0.8825 on the same chart.

The next major resistance is near the 0.8850 level. The main resistance is now forming near the 0.8880 zone. A close above the 0.8880 level could set the tone for another increase. In the stated case, the pair could even clear the 0.8950 resistance.

On the downside, immediate support sits near the 0.8755 level. The next key support sits near the 0.8720 level. Any more losses could send the pair toward the 0.8700 level. The main support could be 0.8680.

Looking at EUR/USD, the pair struggled to continue higher and might see a pullback toward the 1.0820 support zone.

Upcoming Economic Events:

- BoE Interest Rate Decision - Forecast 4.5%, versus 4.5% previous.

- US Initial Jobless Claims - Forecast 224K, versus 220K previous.

First impressions: NZ GDP, December quarter 2024

New Zealand’s GDP rose by 0.7% in the December quarter, ahead of market forecasts. Seasonal issues are overstating the strength of the rebound, but there’s some genuine growth in there as well.

Key results

- Quarterly change: +0.7% (last: -1.1%, Westpac f/c: +0.5%, market f/c: +0.4%, RBNZ +0.3%)

- Annual change: -1.1% (last: -1.6%)

New Zealand’s GDP rose by 0.7% in the December quarter of 2024, providing some relief after steep consecutive declines of 1.1% in the two previous quarters. Revisions to recent history were minimal, with the September quarter being revised down slightly from -1.0%.

The December quarter result was ahead of our forecast of +0.5%, which in turn was at the higher end of the range of market forecasts (median +0.4%). We’d call this a genuine upside surprise, in the sense that the growth was driven more by real activity and less by the seasonal issues that we identified in our preview.

Sector-by-sector growth added up to around 0.3%, with better-than-expected contributions from a range of service sectors including healthcare, professional services, and art and recreation. The non-additive component remains an issue for the interpretation of this data though, adding 0.4% to the growth rate for the quarter.

On an annual basis, GDP was down 1.1% on the same time a year ago. Again, that was better than the -1.3% that we expected, and was an improvement on the -1.6% in the September quarter.

Implications

While the result was ahead of the RBNZ’s forecast, they have tended to downweight the GDP figures in recent times, due to the difficulty of interpreting its volatility and the extent of revisions – instead focusing on a range of higher-frequency indicators. That said, with the RBNZ’s most recent projections sitting somewhere between two and three more OCR cuts this year, these figures favour our view that it’s more likely to be two.

Dow Jones (DJIA), S&P 500 React to Fed Rate Decision

- The Federal Reserve kept interest rates steady but hinted at possible rate cuts later in the year.

- The Fed also expects slower economic growth and higher inflation.

- US stock indexes, including the Dow Jones and S&P 500, rose following the Fed's announcement.

- Technical analysis suggests the Dow Jones faces immediate support at 42000 and potential resistance at 42446 and 42764.

Wall Street Indexes continued their advance after the Federal Reserve kept rates unchanged. The central bank decided to keep interest rates steady at 4.25%-4.50% but suggested two small rate cuts might happen later this year, staying consistent with earlier predictions. The Fed also expects slower economic growth and higher inflation ahead.

Policymakers were divided on what to do next, showing uncertainty about how to address the impact of the Trump administration's policies.

The Fed also announced it would slow down the reduction of its large balance sheet. This comes as the central bank faces difficulties evaluating market conditions during a standoff in Congress over raising the government’s borrowing limit.

Source: LSEG

Summary of Fed Chair Powell's Comments

- Economy is strong, inflation remains "somewhat elevated"

- Tariffs have driven inflation expectations higher

- Fed is not "in a hurry" and will await further clarity

- If the labor market weakens, Fed can ease if needed

- If economy remains strong, policy restraint can be maintained

- Made technical decision to slow balance sheet decline

The Fed remains in "wait and see" mode.

US Indexes had risen prior to the FOMC meeting with the meeting injecting some fresh liquidity and pushing all major indexes higher. The S&P 500 is trading up around 1.70% with the Dow Jones up around 1.47%.

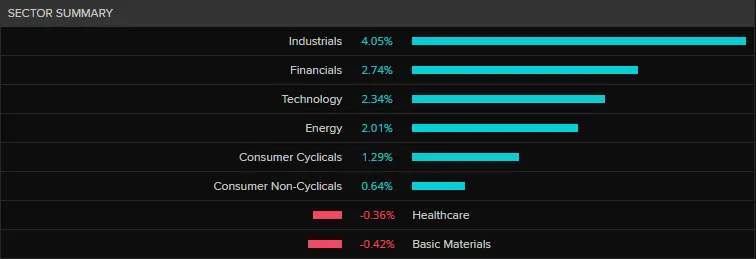

From a sector perspective, Industrials were the big winners with gains of around 4.05% followed by Financials and Tech, with gains of 2.74% and 2.34% respectively.

Source: LSEG

Individual stocks on the move include Boeing with gains of around 7% followed closely by NVIDIA and American Express with gains of 3.2% and 3.3% respectively.

Technical Analysis - Dow Jones

From a technical standpoint, the Dow Jones has moved above a key area of resistance around the 42000 handle.

The question will be whether the daily candle will close above this handle which would hint at further upside. The Dow has had a slight pullback from the post FOMC highs and is currently flirting with support at the 42000.

The 14 period RSI is approaching the neutral 50 level with a break above further supporting the idea of a deeper recovery. A rejection of the 50 level may be seen as a sign that momentum still remains with the bears and could lead to a retest of recent lows.

Immediate support rests at 42000 before the 41400 and 41100 handles come into focus.

If the bullish momentum continues, immediate resistance rests at 42446 and 42764.

Dow Jones (US30) Daily Chart, March 19, 2025

Source: TradingView (click to enlarge)

Support

- 42000

- 41400

- 41100

Resistance

- 42446

- 42764

- 43402

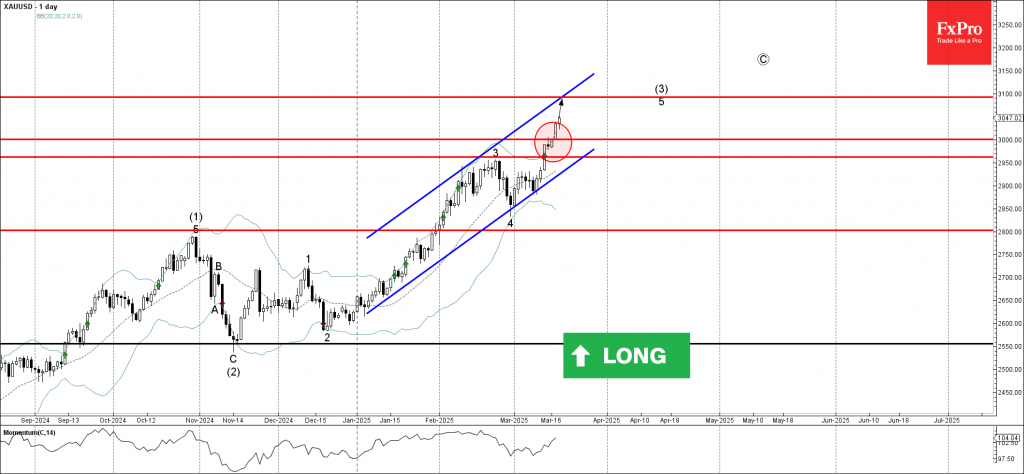

Gold Wave Analysis

Gold: ⬆️ Buy

- Gold continues daily uptrend

- Likely to rise to resistance level 3100.00

Gold rises sharply after breaking the resistance zone between the resistance 2956.00 (top of the previous impulse wave 3) and the round resistance level 3000.00.

The breakout of this resistance zone accelerated the active impulse wave 5 of the higher order impulse wave (3) from November.

Given the clear uptrend, Gold can be expected to rise to the next resistance level 3100.00 (target price for the completion of the active impulse wave 5).

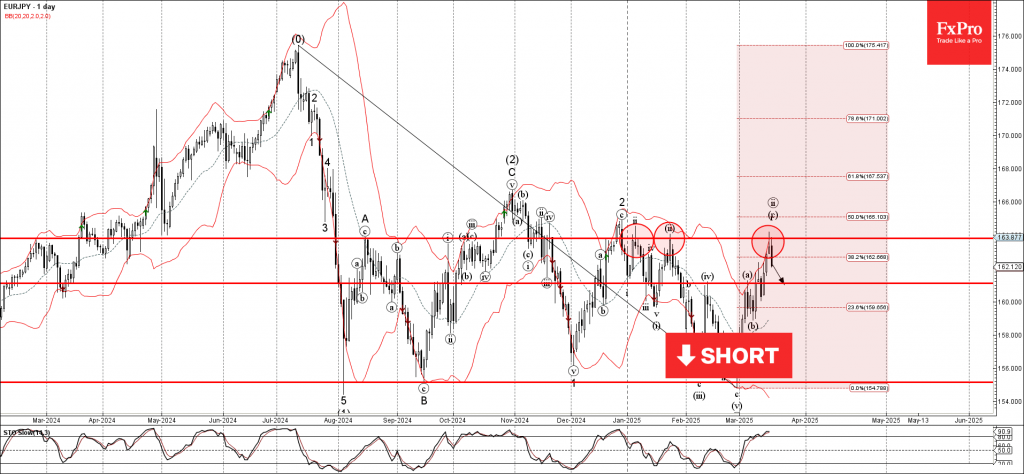

EURJPY Wave Analysis

EURJPY: ⬇️ Sell

- EURJPY reversed from resistance zone

- Likely to fall to support level 161.00

EURJPY currency pair recently reversed down from the resistance zone between the resistance level 163.80 (which has been reversing the price from January) and the upper daily Bollinger Band.

The downward reversal from this resistance zone created the daily Japanese candlesticks reversal pattern Shooting Star.

Given the overbought daily Stochastic, EURJPY currency pair can be expected to fall to the next support level 161.00.