Sample Category Title

Central Bank in the US Takes Center Stage Later Today

Markets

Core bonds gained slightly yesterday with US Treasuries marginally outperforming Bunds. German yields eased 1.3 bps at the front while remaining flat at the long end of the curve. The outgoing parliament greenlighted a historical debt plan that paves the way for hundreds of billions of investments in defense and infrastructure. Its approval triggered a minor profit-taking (short-covering) move in Bunds without technical implications. US rates fell between 0.4 and 1.8 bps in volatile trading and ahead of the Fed meeting today with a decent 20-yr bond auction adding to momentum. EUR/USD gained ground to 1.0945, despite a poor US risk sentiment. The common currency brushed off kneejerk weakness coming from Bloomberg reporting that Russian president wants all arms supplied to Ukraine to be halted as part of a truce. Upping the ante like this dented hopes for a quick win. Eventually though, the US and Russia during the highly anticipated talks agreed to a 30-day ceasefire strictly confined to energy infrastructure. That’s well short of the unconditional and general truce the US and Ukraine proposed. The US Middle East envoy Steve Witkoff after the meeting said talks with Russia will continue on Sunday in Saudi Arabia. Sterling traded stoic after hearing about the £5bn welfare spending cuts per year by 2030. The weakening economic outlook (and rising bond yields) force UK Chancellor Reeves into additional spending squeezes at next week’s Spring Statement.

The Japanese yen is among the weaker performers this morning against an overall stronger USD. It follows the Bank of Japan meeting earlier (cfr. infra). The central bank in the US takes center stage later today. The March meeting is accompanied with an updated dot plot and new inflation and growth forecasts. Data recently have added to a growing market narrative of stagflation, mostly in soft indicators (e.g. consumer confidence, NY manufacturing index). But hard economic data wasn’t so bad (services ISM, solid payrolls growth, IP, housing). That should prevent the Fed (and therefore the new projections) from getting carried away by the recent bearish (stock) sentiment, especially with uncertainty on the tariff narrative still this big. It’s not until April 2, when Trump’s reciprocal tariffs are to be announced, it’s worth making an analysis. In theory there’s little to push the Fed off the January track (extended pause) but the devil for US rates and the dollar could be in the details. Any touch of dovishness by Powell during the presser is likely to be picked up by markets. The downside in (front-end) US yields is nevertheless limited with the March correction low serving as solid support. At that time, markets were pricing around three cuts this year, deviating from the current (and probably new) dot plot. EUR/USD is catching a breather now, but we stick to the view of upside potential (1.12 in first instance).

News & Views

The Bank of Japan as expected left its policy rate unchanged at 0.5%. The domestic economy is continuing a gradual improving trend. Private consumption has been on a moderate increasing trend despite the impact of price rises and other factors, as is business fixed investment. Exports and industrial production have been more or less flat. CPI inflation (ex fresh food) has been in the range of 3.0-3.5% recently, amid rising services prices (wage increases) and a rollback of government energy measures. The BOJ expects the economy to keep growing above potential, with overseas economies continuing to grow moderately and as a virtuous cycle from income to spending gradually intensifies. Underlying CPI inflation is likely to be at a level that is generally consistent with target. The BOJ earmarks the international developments regarding trade as an important risk to the outlook. Domestic developments suggest room to gradually normalize policy, but the BOJ creates space to adapt the timing to cope with international developments. The next BOJ policy decision is May 1. The 2-y bond yield this morning adds 2 bps (0.84%). The 10-y adds 1.2 bps (1.52%). The yen continues its recent correction with USD/JPY nearing the 150 barrier.

Fitch in a comment yesterday said that Hungary’s recently announced fiscal measures highlight the authorities’ balancing of policy priorities ahead of parliamentary elections in spring 2026. The rating agency thinks authorities will calibrate economic stimulus measures to avoid increasing financial market volatility, especially given the greater inflationary pressures at the start of this year. The government recently announced targeted fiscal measures of HUF 900bln over 2025/28 to support families. Fitch raised its deficit forecast to 4.5% of GDP in 2025 and 4% in 2026, from 4.2% and 3.7%, respectively. The revision reflects weaker macroeconomic conditions, higher inflation and government bond yields, and additional tax exemptions. Still Fitch doesn’t expect aggressive monetary easing or fiscal expansion on a scale similar to that ahead of 2022’s parliament election.

Will Fed Save the Day?

Nvidia yesterday revealed new products at the company’s annual GPI Technology Conference at San Jose. The CEO Jensen Huang showed off its new AI system Vera Rubin, called after nothing less than the astronomer who discovered the evidence of dark matter, and announced new partnerships with GM and Taco Bell. The new Vera Rubin, the next, next generation chip, is more than twice as fast as its predecessor Blackwell. GM will integrate Nvidia’s technology into its self-driving cars and will also benefit from their systems for improving the performance of its factories and robots, while Yum Brands is looking to boost its AI-powered drive-thru ordering. A year ago, investors would be popping champagnes on the news, but this time around, they just weren’t impressed. The stock price fell 3.43% yesterday.

Of course, it was not about Nvidia or the AI conviction, it was about the overall market mood that’s been souring due to a number of reasons including the tariff war, the high tech valuations, the rotation trade, the uncertain Federal Reserve (Fed) outlook and the ugly geopolitics. As such, the S&P500 reversed two-session gains and fell 1%, Nasdaq 100 lost 1.66% and the Dow Jones eased 0.62%. Facebook became the last of the Magnificent 7 stocks to give back all of its ytd gains. If Nvidia’s AI news couldn’t wet investors’ appetite, it means that the correction is poised to extend deeper. The S&P500 could shed additional 5-10% from the actual levels. For the short-term investors, there could be a tactical opportunity in the selloff, for the long-term investors, the periods of correction are not particularly enjoyable, but there has always been light at the end of the tunnel.

Jawohl!

Across the Atlantic Ocean, the spring winds are gently blowing across the markets. The Germans agreed to pass a bill that will allow the government to increase its spending without being laid back by the strict borrowing rules. Germany could borrow up to EUR 500bn in the context of a special, off-budget fund to finance infrastructure and defence needs. The other European nations will feel free do the same, of course. Rheinmetall jumped more than 5.5%, the BAE systems added more than 1%, The Select Stoxx 600 Europe Aerospace & Defence ETF – that includes these names among other defence names - gained another 1.46% and the Stoxx 600 was up by 0.61% in a continued contrast with the American peers’ morose performances. Cherry on top, the German 10-year yield eased as the government’s intention to boost spending was fully priced in, and the EURUSD traded above 1.0950. The traders are now shifting their focus to today’s Fed meeting to find out whether the Fed could, and will do something to reverse the negativeness among the US market investors.

What does the Fed think about it?

The Fed is expected to maintain its rates unchanged today. But the committee will update its dot plot, growth and inflation projections and will provide a hint regarding where the policymakers are planning to put pressure in the changing economic landscape. Is the Fed worried about a renewed uptick in inflation due to the government’s hectic tariff policies? Is it more worried about the negative impact of the wide-ranging White House policies on employment and growth? Is it worried about the stock market selloff?

What investors are explicitly wishing is to hear that Powell and the Fed are ready to step in in case the market selloff gets worse to ensure a minimum financial stability – a thing that it’s beautifully done in the past by lowering rates and buying bonds. Economists expect the Fed to cut the rates two times this year as a response to economic slowdown with limited progress toward the 2% inflation goal. Traders see three cuts as a response to a potentially ugly selloff in equity markets. Either way, activity on Fed funds futures hints to around 65% chance for the next rate cut to arrive in June. The dot plot will tell who is closer to the Fed’s mind and when we could expect a rate cut. A dovish stance could help slow the equity selloff and give a minor rebound to equities and the US dollar, while a cautious stance could sent the S&P500 back into the correction territory – meaning 10% or more lower than its February peak – and extend the scope for deeper losses for both US equities and the US dollar.

The US 2-year yield is hovering around the 4% mark this morning, the 10-year yield sits near the 4.30%. The US dollar index remains under the pressure of the waning growth prospects, the EURUSD bulls are waiting in ambush to push the pair above the 1.10 psychological mark.

Note that yesterday’s conversation between Trump and Putin didn’t hint at a sustainable peace anytime soon, but the Russians agreed to not bomb the Ukrainian energy infrastructure for a month. Crude is extending losses this morning below the $67pb level. The candlesticks of the past days have long upper wicks hinting at a lack of conviction from the price rebounds that suggest that the bearish trend remains strong in the short run and we could see further losses toward the $65pb mark.

Anticipation Building for Powell’s Outlook on US Economy

In focus today

The main event will be the FOMC meeting tonight. We expect an unchanged rate decision which is also fully priced in the markets, but all eyes will be on Powell's communication about the outlook for further rate cuts as well as the updated rate and economic projections. The Fed could also provide signals about further tapering or even completely ending QT over coming months.

Economic and market news

What happened overnight

In Japan, the Bank of Japan concluded its two-day policy meeting, keeping the policy rate at 0.5% as expected. They highlighted that exchange rate developments are, compared to the past, more likely to affect prices. The market reaction to the decision was muted. With the outlook for another significant wage bump this year, we anticipate the BoJ will find room to hike rates again in July. We will keep an eye on the 07.30 CET press conference to look for clues on the future rate path.

What happened yesterday

In Ukraine, Russian President Putin agreed to a 30-day halt to strikes against energy infrastructure in Ukraine following talks with President Trump. While President Putin did not agree to the full 30-day ceasefire proposal like Ukraine, the US and Russia have agreed to work quickly towards more extensive peace agreements. Further discussions are set to take place in Saudi-Arabia on Sunday between the US and Russia.

In Germany, the new German government has successfully passed the significant fiscal package through the Bundestag, with support from The Green party. The package is expected to pass the Bundesrat on Friday, backed by a two-thirds majority between the CDU/CSU, SPD, Greens, and Bavarian Free Voters. The ECB anticipates upside risks to inflation and growth from this package, supporting a slower pace of rate cuts. While Germany will experience a positive demand shock, we expect the bulk of growth impacts to occur from 2026 onwards, with GDP growth potentially rising by 1-2 percentage points in 2027. Germany's shift towards fiscal spending may influence EU-level agreements on increased defence spending and common borrowing, although growth impacts depend on rising production capacities in Europe.

Equities: Global equities were lower yesterday, primarily due to the US pulling global indices down with its significant weight in global indices. In Europe, the belief that Germany would pass the historic spending package in the Bundestag grew throughout the day, leading to indices ending higher, buoyed by Germany, manufacturing-related cyclicals, and notably banks. Consequently, Europe, not just Germany, is now outperforming the US by more than 15% year-to-date in local currency, and by more than 20% when measured in common currency. In the US, we once again saw Mag 7 and cyclicals under pressure. Banks, on the other hand, had a better day, finishing as the best-performing industry in the S&P 500. Yesterday in the US, Dow -0.6%, S&P 500 -1.1%, Nasdaq -1.7%, and Russell 2000 -0.9%. This morning presents a mixed bag in Asia, and the same could be said about Western futures. To be clear, calmness, days with sub-1% moves, and fewer noisy political headlines would be beneficial for equities at the moment.

FI&FX: EUR/USD rose to a new high yesterday following the passing of the German fiscal package in the Bundestag and progress on Russia-Ukraine ceasefire. The Bund ASW spread was about unchanged on the news. In Scandies, EUR/SEK fell back below 11.00, which also sent NOK/SEK lower again. The NOK curve steepened considerably driven by a decline in the short end.

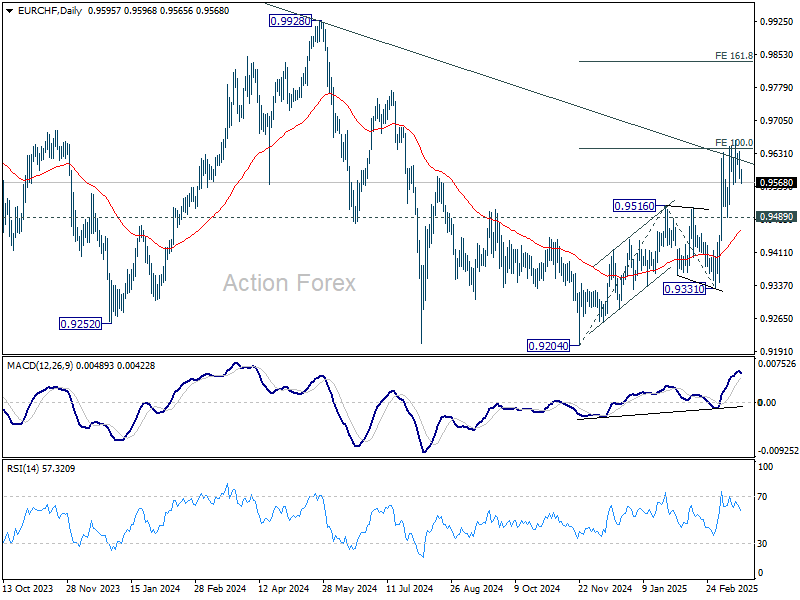

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9569; (P) 0.9603; (R1) 0.9630; More....

Intraday bias n EUR/CHF remains neutral and some more consolidations could be seen below 0.9660. However, further rally is expected as long as 0.9489 support holds. Sustained trading above 100% projection of 0.9204 to 0.9516 from 0.9331 at 0.9643 will pave the way to 161.8% projection at 0.9836 next.

In the bigger picture, prior strong break of 55 W EMA (now at 0.9487) is a medium term bullish sign. Sustained break trading above long-term falling channel resistance (at around 0.9620) would suggest that the downtrend from 1.2004 (2018 high) has bottomed at 0.9204. Stronger rally should then be see to 0.9928 key resistance at least.

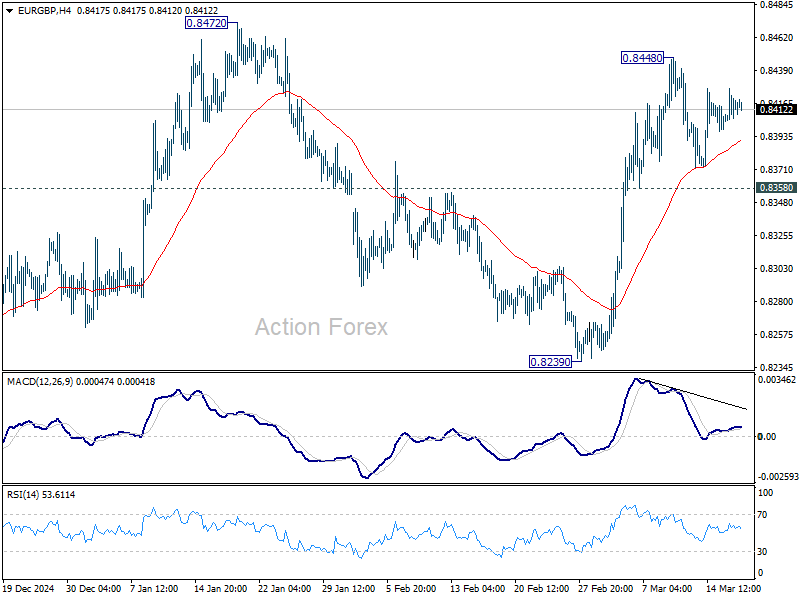

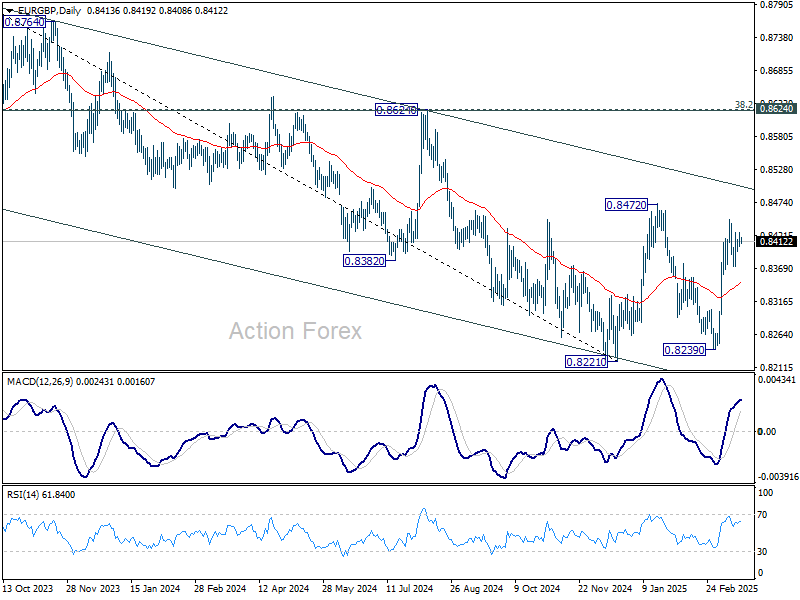

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8403; (P) 0.8416; (R1) 0.8430; More...

Intraday bias in EUR/GBP stays neutral as range trading continues below 0.8448. Further rally is expected as long as 0.8358 minor support holds. On the upside, break of 0.8448 will target 0.8472 resistance first. Firm break there will resume whole rebound from 0.8221 to medium term falling channel resistance (now at 0.8508). Nevertheless, break of 0.8358 will suggest that rise from 0.8239 has completed and turn bias back to the downside instead.

In the bigger picture, EUR/GBP is still bounded inside medium term falling channel. While rebound from 0.8221 might extend higher, it could still develop into a corrective pattern. Overall outlook will be neutral at best and down trend from 0.9267 (2022 high) could extend, at least until decisive break of channel resistance (now at 0.8508).

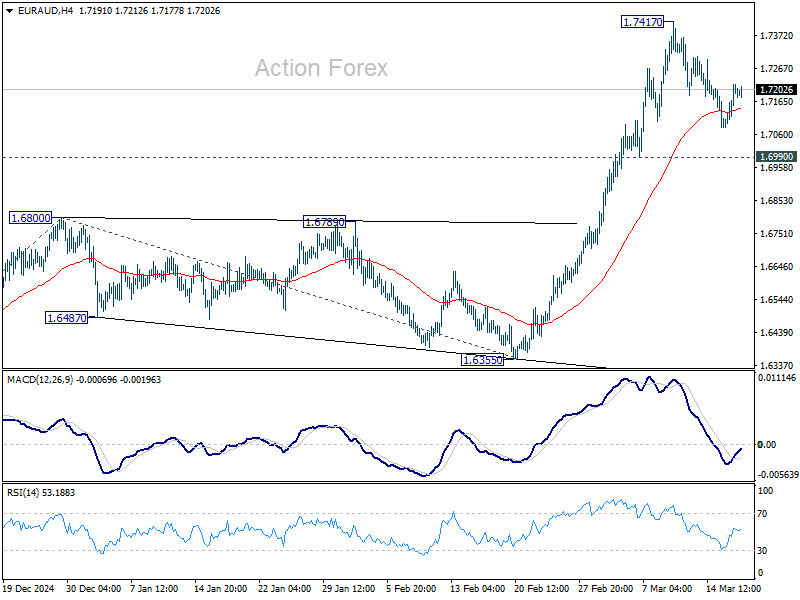

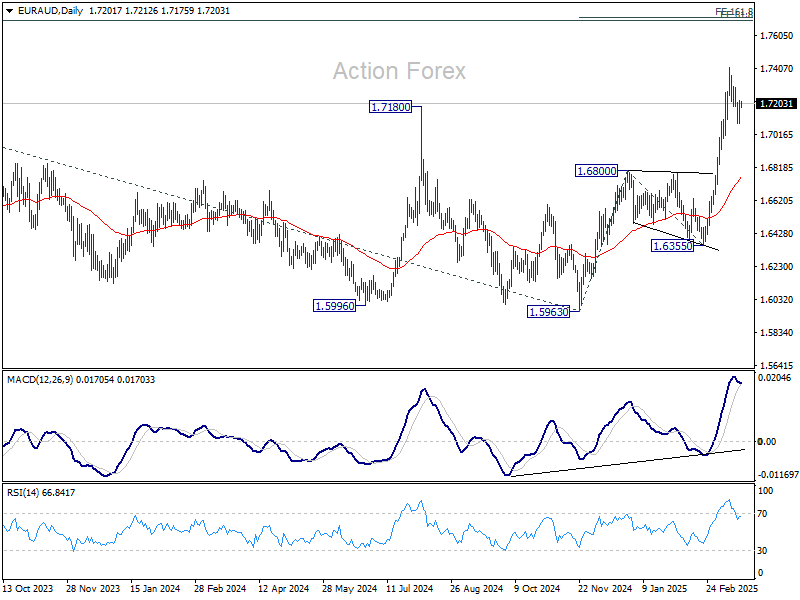

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7121; (P) 1.7171; (R1) 1.7256; More...

EUR/AUD is staying in consolidation below 1.7417 and intraday bias stays neutral. Downside of retreat should be contained by 0.6990 support to bring rebound. On the upside, break of 1.7417 will resume rise from 1.6335 to 161.8% projection of 1.5963 to 1.6800 from 1.6355 at 1.7709 next.

In the bigger picture, the breach of 1.7180 key resistance (2024 high) suggests that up trend from 1.4281 (2022 low) is resuming. Sustained trading above 1.7180 will confirm and target 61.8% projection of 1.4281 to 1.7062 from 1.5963 at 1.7682, which is also close to 61.8% retracement of 1.9799 (2020 high) to 1.4281 at 1.7691. For now, this will remain the favored case as long as 1.6800 resistance turned support holds, even in case of deep pullback.

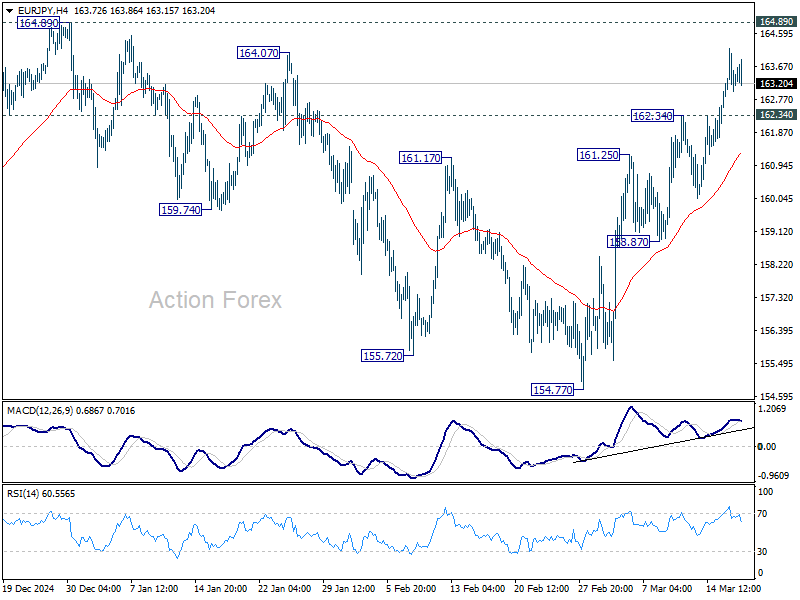

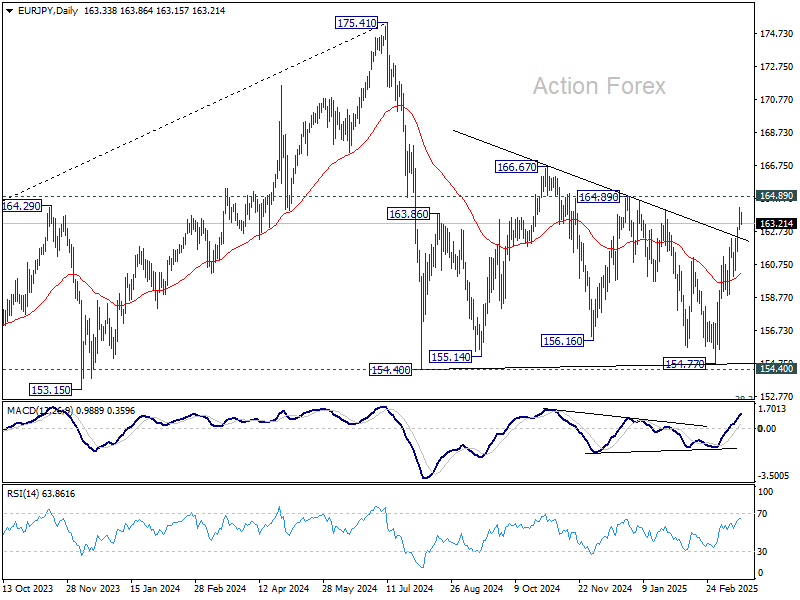

EUR/JPY Daily Outlook

Daily Pivots: (S1) 162.72; (P) 163.45; (R1) 164.14; More...

Intraday bias in EUR/JPY stays on the upside for the moment. Rise from 154.77, as another rising leg in the consolidation from 154.40, should target 164.89 resistance. On the downside, below 162.34 will turn intraday bias neutral again and bring consolidations first.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

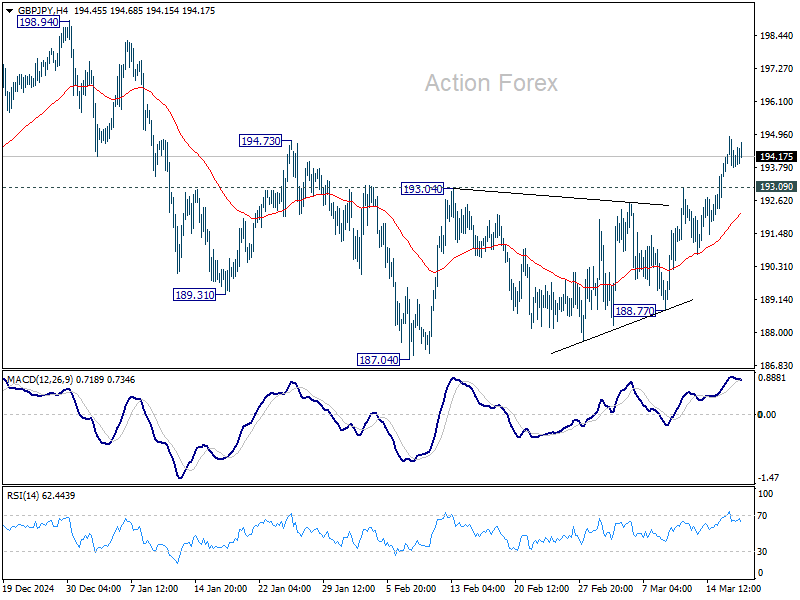

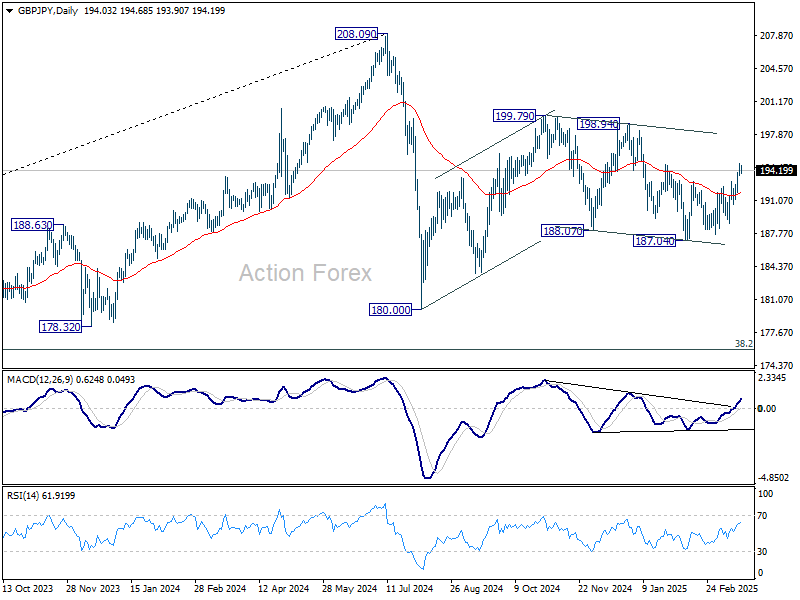

GBP/JPY Daily Outlook

Daily Pivots: (S1) 193.52; (P) 194.22; (R1) 194.80; More...

Intraday bias in GBP/JPY remains on the upside for the moment. Sustained break of 194.73 will extend the rise from 187.04 to 198.94/199.79 resistance zone. On the downside, below 193.09 support will turn intraday bias neutral again first. Overall, corrective pattern from 208.09 is still in progress, with price actions from 180.00 as the second leg.

In the bigger picture, price actions from 208.09 are seen as a correction to rally from 123.94 (2020 low). Strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

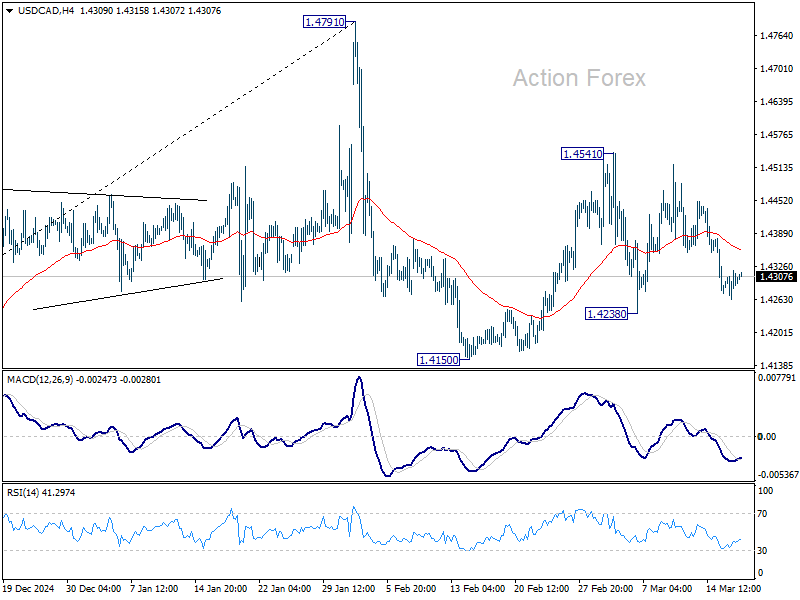

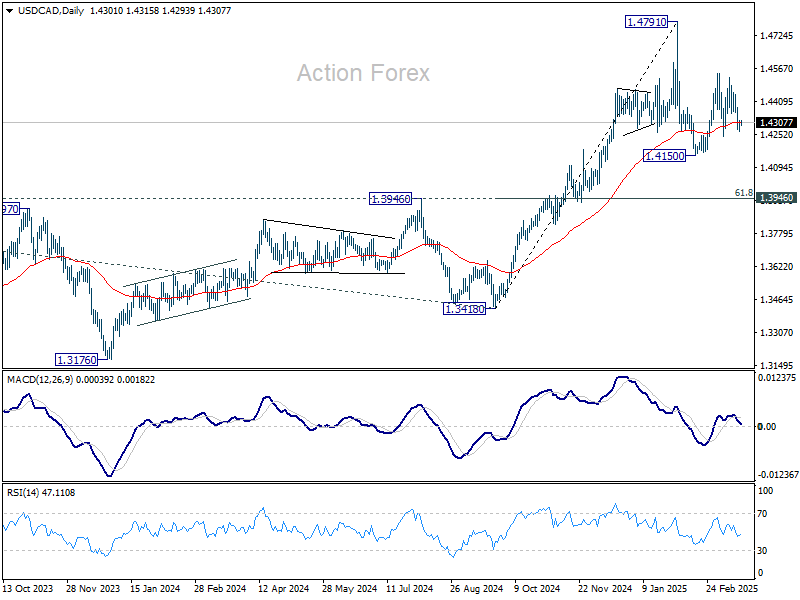

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4272; (P) 1.4296; (R1) 1.4323; More...

Intraday bias in USD/CAD remains neutral for the moment as range trading continues. On the downside, break of 1.4238 support will argue that corrective pattern from 1.4791 has started the third leg already. Intraday bias will be back on the downside for 1.4150 support and below. On the upside, though, break of 1.4541 will resume the rebound from 1.4150, as the second leg of the pattern.

In the bigger picture, long term up trend is tentatively seen as resuming with prior breach of 1.4667/89 key resistance zone (2020/2015 highs). Next target is 100% projection of 1.2401 to 1.3976 from 1.3418 at 1.4993. This will remain the favored case as long as 1.3976 resistance turned support holds (2022 high), even in case of deep pullback.

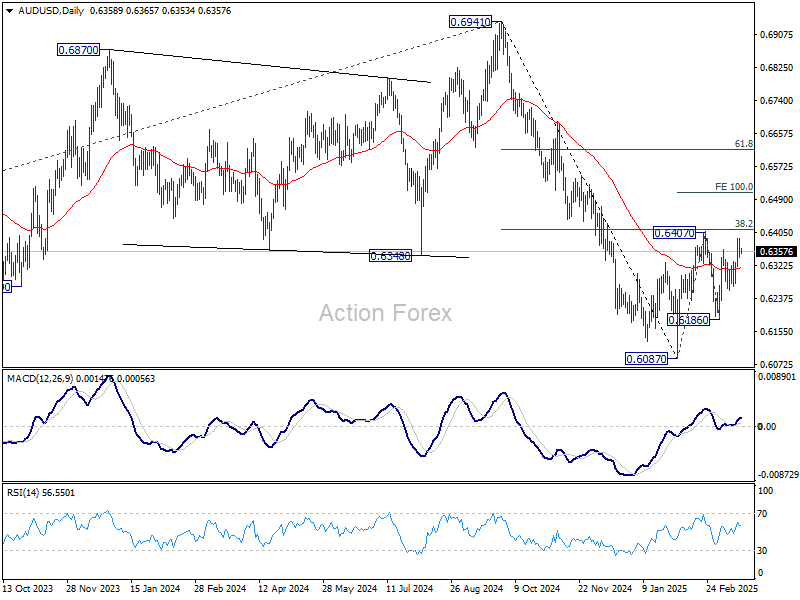

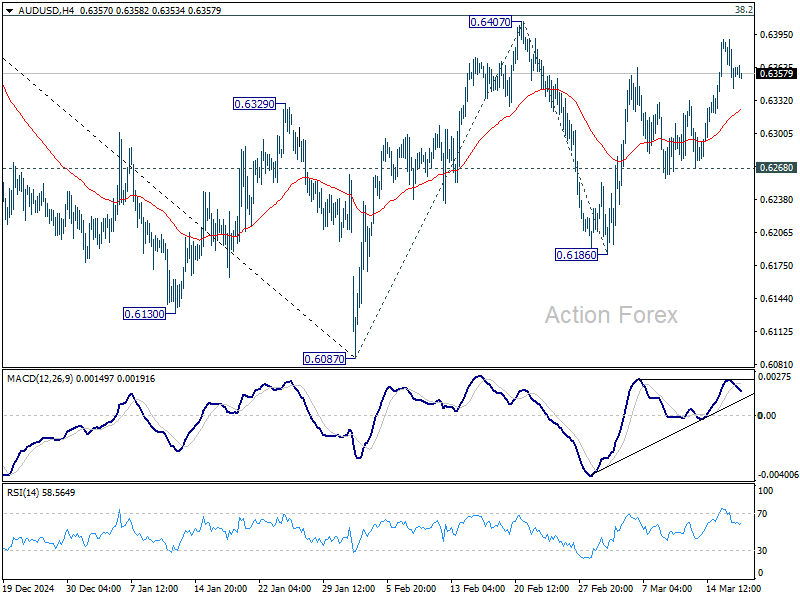

AUD/USD Daily Report

Daily Pivots: (S1) 0.6340; (P) 0.6365; (R1) 0.6387; More...

Range trading continues in AUD/USD and intraday bias remains neutral for the moment. On the upside, sustained break of 0.6407 will resume the rebound from 0.6087 to 100% projection of 0.6087 to 0.6407 from 0.6186 at 0.6506, even still as a corrective move. On the downside, below 0.6268 will turn bias back to the downside for 0.6186 support.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6482) holds.