Sample Category Title

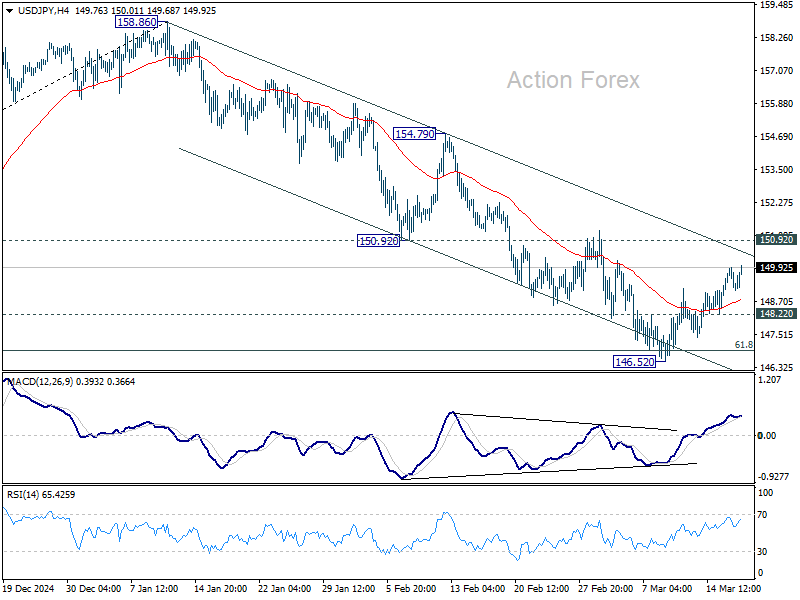

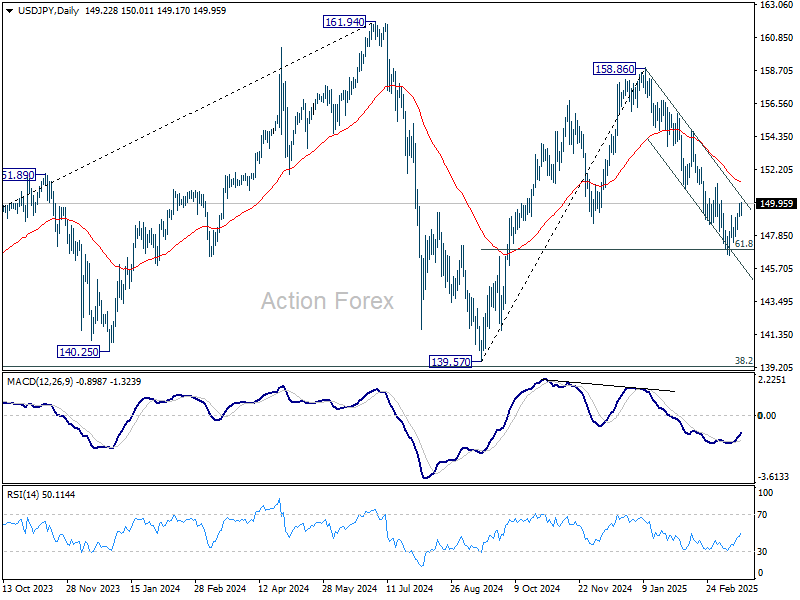

USD/JPY Daily Outlook

Daily Pivots: (S1) 148.89; (P) 149.42; (R1) 149.81; More...

While USD/JPY's rebound from 146.52 might extend, upside should be limited by 150.92 support turned resistance. On the downside, below 148.22 minor support will bring retest of 146.52 low first. Sustained trading below 61.8% retracement of 139.57 to 158.86 at 146.32 will pave the way to 139.57 support. However, decisive break of 150.92 will dampen this bearish view and turn bias to the upside for 154.79 resistance instead.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

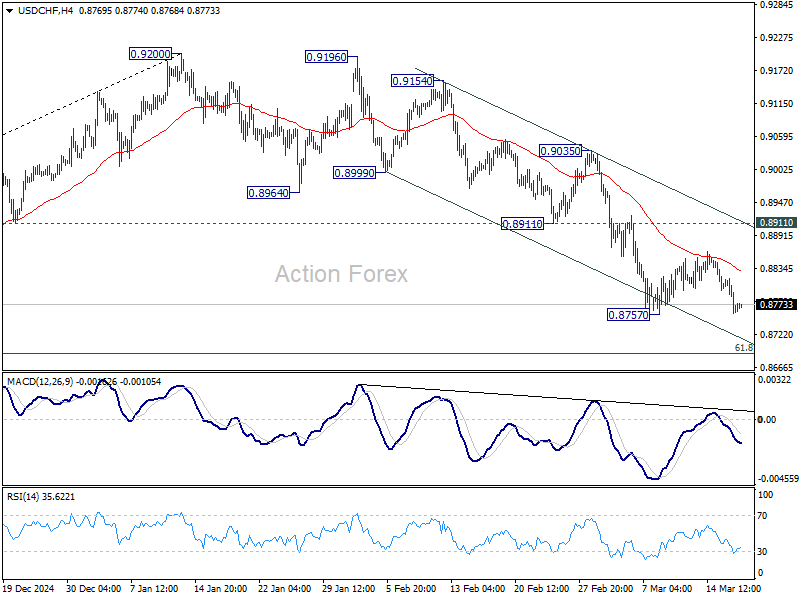

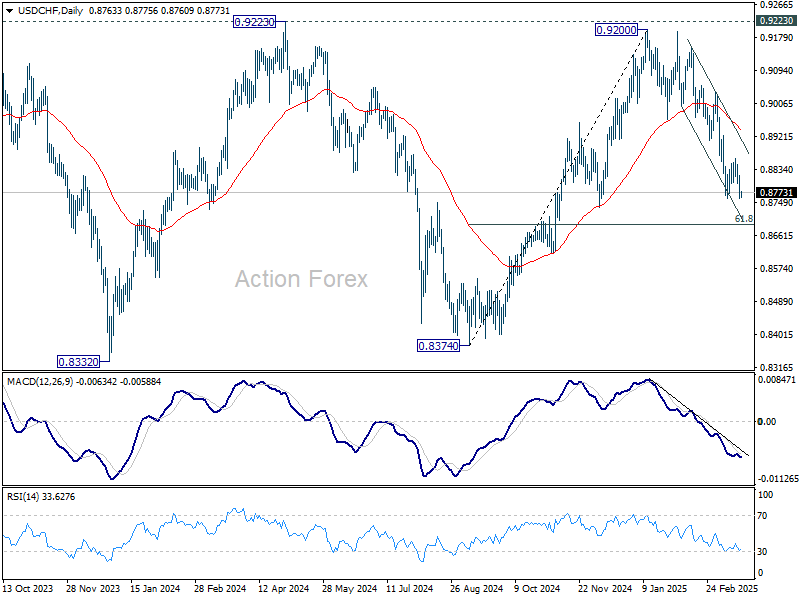

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8744; (P) 0.8782; (R1) 0.8805; More…

USD/CHF is staying above 0.8757 support despite current dip. Intraday bias stays neutral for the moment. In case of another recovery, upside should be limited by 0.8911 support turned resistance. On the downside, break of 0.8757 will resume the fall from 0.9200 to 61.8% retracement of 0.8374 to 0.9200 at 0.8690. Sustained break there will pave the way back to 0.8374 support.

In the bigger picture, rejection by 0.9223 key resistance keep medium term outlook bearish. That is, larger fall from 1.0342 (2017 high) is not completed yet. Firm break of 0.8332 (2023 low) will confirm down trend resumption.

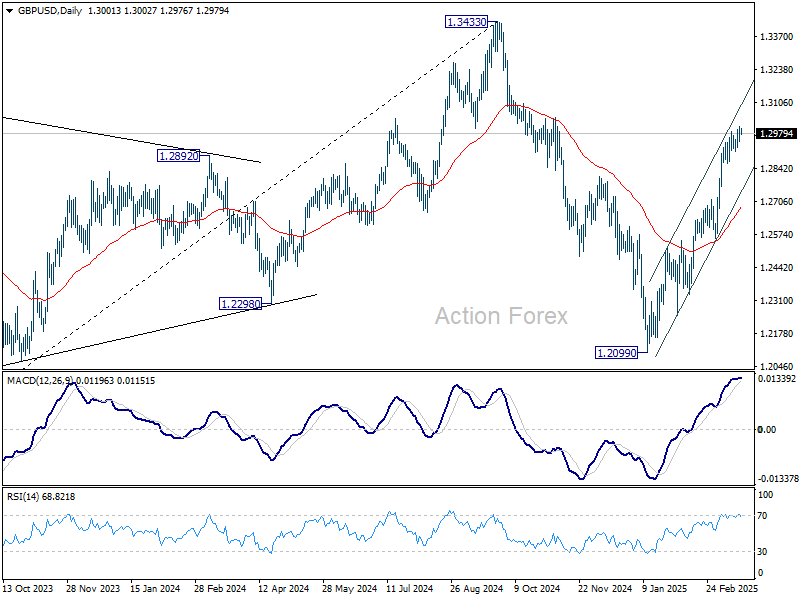

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2967; (P) 1.2988; (R1) 1.3025; More...

GBP/USD's rally from 1.2099 is still in progress, and further rise should be seen to retest 1.3433 high. On the downside, break of 1.2910 support will indicate short term topping, likely with bearish divergence condition in 4H MACD. That would turn intraday bias back to the downside for deeper pullback.

In the bigger picture, up trend from 1.3051 (2022 low) is not completed. Resumption is expected after corrective pattern from 1.3433 completes. Next target will be 1.4248 key resistance. This will now remain the favored case as long as 1.2099 support holds.

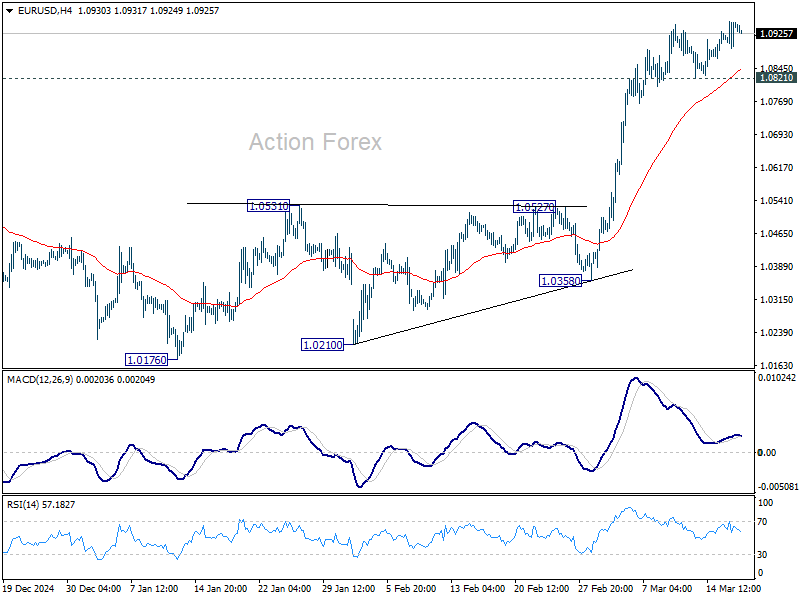

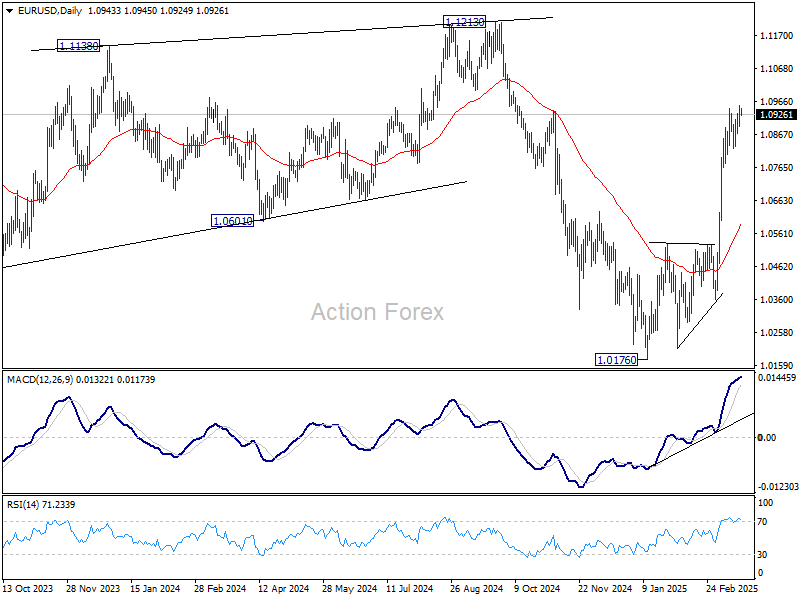

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0907; (P) 1.0931; (R1) 1.0969; More...

Intraday bias in EUR/USD remains on the upside for the moment. Current rally from 1.0176 should target 1.1274 key resistance. On the downside, though, break of 1.0821 support will indicate short term topping, likely with bearish divergence condition in 4H MACD. That will turn bias back to the downside for deeper pullback.

In the bigger picture, prior strong break of 55 W EMA (now at 1.0675) suggests that fall from 1.1274 (2024 high) has completed as a three wave correction to 1.0176. Rise from 0.9534 is still intact, and might be ready to resume. Decisive break of 1.1274 will target 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. Also, that will send EUR/USD through a multi-decade channel resistance will carries larger bullish implication. This will now be the favored case as long as 1.0531 resistance turned support holds.

Dollar Stays Weak as Markets Await Fed Guidance, Yen Softens After BoJ Hold

Dollar remains under pressure as markets await FOMC rate decision and, more crucially, the updated economic projections. While the central bank is widely expected to hold rates steady at 4.25-4.50%, traders are looking for any signs that Fed officials are adjusting their outlook in response to mounting trade tensions. Meanwhile, US stocks saw another selloff overnight, led by the tech sector, though major indexes have so far held above last week’s lows. Sentiment remains fragile, and any dovish elements in Fed’s projections could trigger another round of risk aversion and Dollar weakness. However, the biggest market move may be on hold until April 2, when the final decision on reciprocal tariffs is expected.

Japanese Yen is also soft in a tight range after BoJ left monetary policy unchanged earlier today. While this decision was widely anticipated, some market participants noted that the earlier-than-usual timing of the announcement suggested that the BoJ was not yet ready to accelerate rate hikes. Yen has also weakened this week on broader risk-on sentiment in Asia, despite the selloff in US equities.

On the other hand, Euro remains firm, though lacking decisive upside momentum. Germany’s parliament approved the massive fiscal expansion plan yesterday, marking a historic departure from the country’s long-standing fiscal conservatism. This move has given CDU/CSU leader Friedrich Merz a significant political boost as he continues talks with the Social Democrats to form a centrist coalition government. While some economists argue that Germany’s fiscal expansion is the most significant since reunification, they also warned that structural reforms will be necessary to turn this spending into sustainable growth.

Looking at currency performance this week, Kiwi is leading gains, followed by Swiss Franc and Aussie. In contrast, Yen remains the weakest performer, followed by Dollar and Sterling. Euro and Loonie are positioned in the middle of the pack.

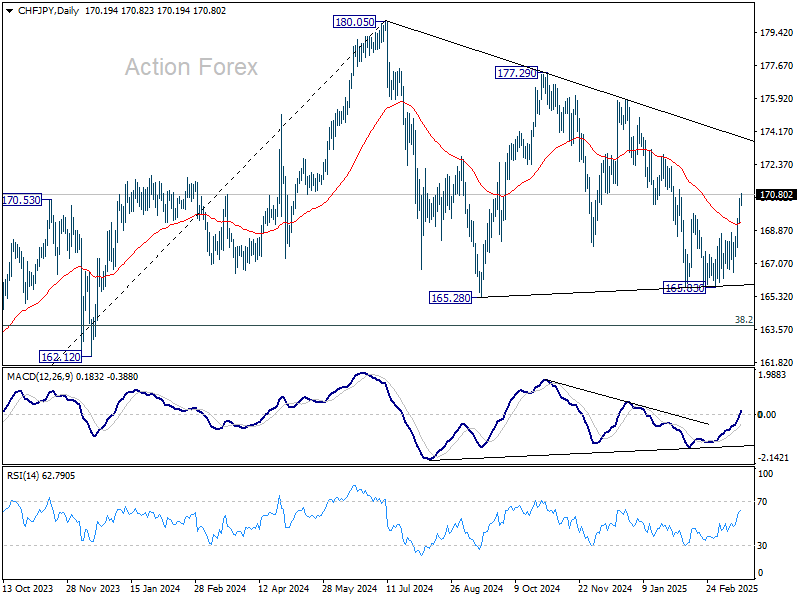

Technically, CHF/JPY is among the top movers this week so far. The extended rebound and firm break of 55 D EMA (now at 162.27) suggests that fall from 177.29 has completed at 165.83 already. The whole corrective pattern from 180.05 might have finished too. Further rise is now expected to trend line resistance at 173.95 first. Firm break there will solidify this bullish case and target 177.29/180.05 resistance zone next.

In Asia, at the time of writing, Nikkei is up 0.03%. Hong Kong HSI is down -0.09%. China Shanghai SSE is down -0.18%. Singapore Strait Times is up 0.34%. Japan 10-year JGB yield is up 0.011 at 1.517. Overnight, DOW fell -0.62%. S&P 500 fell -1.07%. NASDAQ fell -1.71%. 10-year yield fell -0.025 to 4.281.

BoJ holds rates, flags exchange rate as key inflation factor

BoJ kept its uncollateralized overnight call rate unchanged at around 0.50%, as widely expected.

In its statement, BoJ noted that growth is expected to remain above potential, while inflation progress remains on track toward its 2% target. However, policymakers flagged high levels of uncertainty, particularly citing global trade tensions and policy shifts in major economies as key risks.

A notable shift in BoJ’s tone was its heightened focus on exchange rate movements as a key factor influencing inflation. The central bank acknowledged that with firms increasingly raising wages and prices, exchange rate developments are, compared to the past, "more likely to affect prices".

This suggests that further depreciation in Yen could accelerate price increases, and influence future monetary policy decisions.

Japan’s export rises 11.4% yoy in Feb, up for fifth straight month

Japan’s exports surged 11.4% yoy to JPY 9,191B in February, marking the fifth consecutive month of growth, driven by strong demand from both the US and China. Exports to the US rose 10.5% yoy, while shipments to China saw an even stronger 14.1% yoy increase.

Meanwhile, imports declined by -0.7% yoy, marking their first drop in three months, as demand for crude oil and coal weakened. This shift in trade dynamics helped Japan return to a trade surplus of JPY 584.5B, the first positive balance in two months.

On a seasonally adjusted basis, exports rose 4.0% mom to JPY 9,688B, while imports fell -4.1% mom to JPY 9,505B, leading to a JPY 182B surplus.

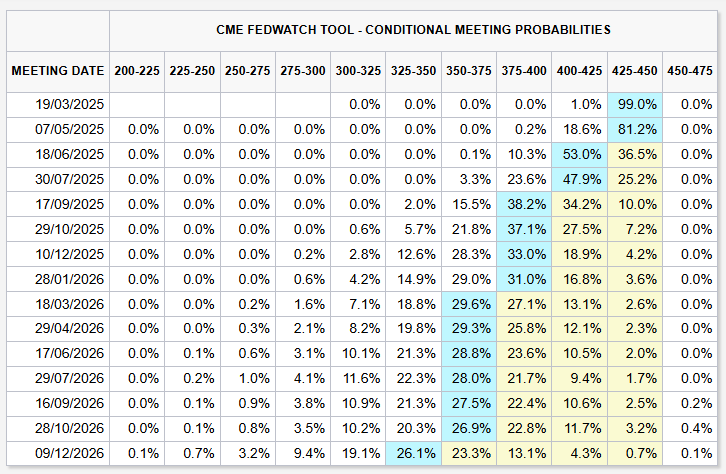

Fed to stand pat, watch for signs of trade war fallout in new projections

Fed is set to keep interest rates unchanged at 4.25-4.50% today. The focus will be on the updated economic projections, which may drop hints that Fed is beginning to pre-empt a full-blown trade war into its outlook. Additionally, another key element to watch will be the closely followed “dot plot”, which will reveal whether Fed still expects two rate cuts this year.

Chair Jerome Powell’s press conference is important as usual, as he will need to balance Fed’s current economic assessment with the risks posed by US President Donald Trump’s trade policy. However, with no details on the big event of reciprocal tariffs on April 2, Powell is unlikely to offer any concrete guidance. Instead, he may just reiterate the central bank’s stance that it is “in no hurry” to cut rates and emphasize a data-dependent approach.

Currently, Fed fund futures indicate that June and September are the most likely timing for policy easing.

One key market reaction to watch will be 10-year Treasury yield, which recovery has clearly lost momentum well ahead of 55 D EMA (now at 4.389). Any dovish tilt from Fed today could push yields back toward 4.106 support. That would in turn keep Dollar under pressure.

Though, firm break of 61.8% retracement of 3.603 to 4.809 at 4.063 is not anticipated for now, at least until the tariff picture is cleared or there are more signs of recession in the US. On the upside, any rebound should be limited by 55 D EMA.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0907; (P) 1.0931; (R1) 1.0969; More...

Intraday bias in EUR/USD remains on the upside for the moment. Current rally from 1.0176 should target 1.1274 key resistance. On the downside, though, break of 1.0821 support will indicate short term topping, likely with bearish divergence condition in 4H MACD. That will turn bias back to the downside for deeper pullback.

In the bigger picture, prior strong break of 55 W EMA (now at 1.0675) suggests that fall from 1.1274 (2024 high) has completed as a three wave correction to 1.0176. Rise from 0.9534 is still intact, and might be ready to resume. Decisive break of 1.1274 will target 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. Also, that will send EUR/USD through a multi-decade channel resistance will carries larger bullish implication. This will now be the favored case as long as 1.0531 resistance turned support holds.

Fed to stand pat, watch for signs of trade war fallout in new projections

Fed is set to keep interest rates unchanged at 4.25-4.50% today. The focus will be on the updated economic projections, which may drop hints that Fed is beginning to pre-empt a full-blown trade war into its outlook. Additionally, another key element to watch will be the closely followed “dot plot”, which will reveal whether Fed still expects two rate cuts this year.

Chair Jerome Powell’s press conference is important as usual, as he will need to balance Fed’s current economic assessment with the risks posed by US President Donald Trump’s trade policy. However, with no details on the big event of reciprocal tariffs on April 2, Powell is unlikely to offer any concrete guidance. Instead, he may just reiterate the central bank’s stance that it is “in no hurry” to cut rates and emphasize a data-dependent approach.

Currently, Fed fund futures indicate that June and September are the most likely timing for policy easing.

One key market reaction to watch will be 10-year Treasury yield, which recovery has clearly lost momentum well ahead of 55 D EMA (now at 4.389). Any dovish tilt from Fed today could push yields back toward 4.106 support. That would in turn keep Dollar under pressure.

Though, firm break of 61.8% retracement of 3.603 to 4.809 at 4.063 is not anticipated for now, at least until the tariff picture is cleared or there are more signs of recession in the US. On the upside, any rebound should be limited by 55 D EMA.

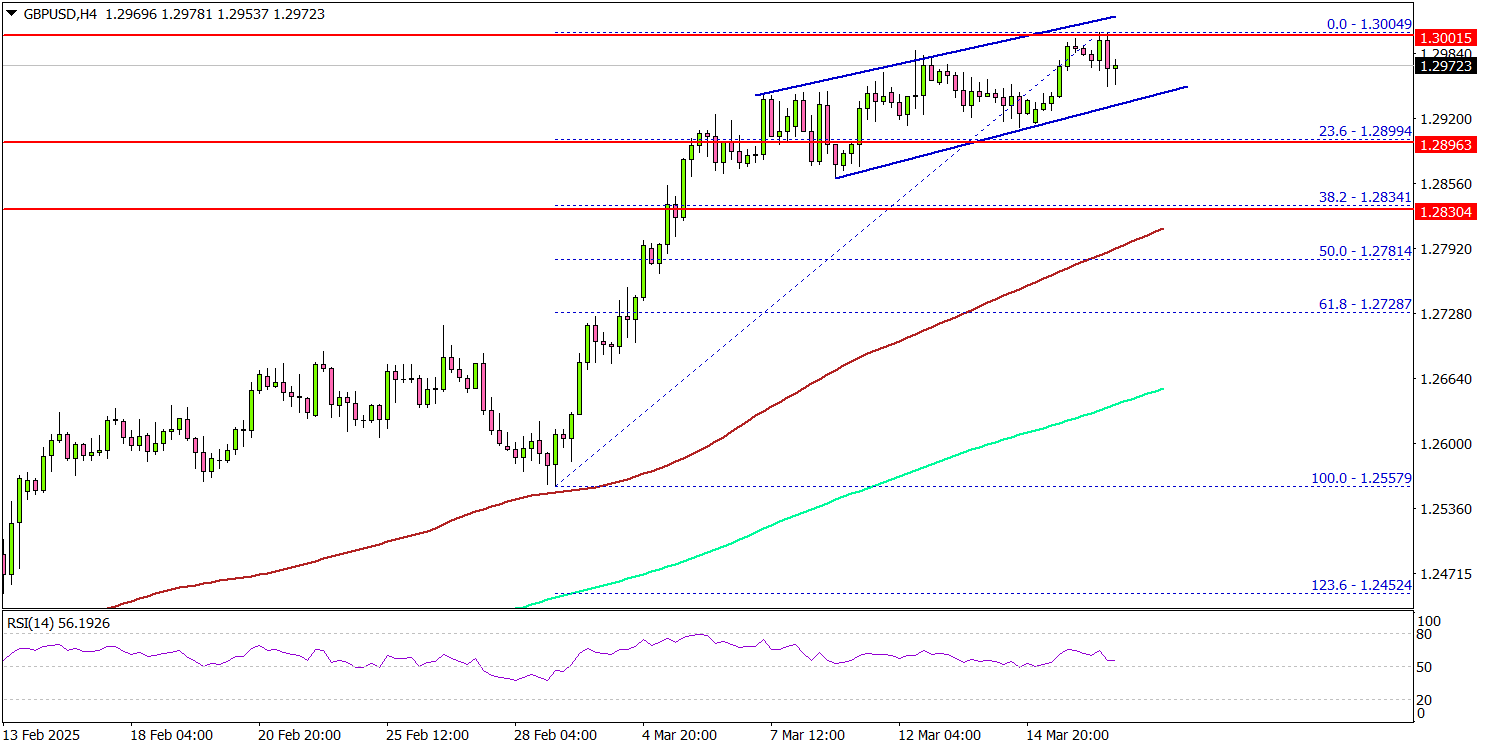

Sterling Strengthens—GBP/USD Eyes More Gains Ahead

Key Highlights

- GBP/USD started a fresh increase above the 1.2800 resistance.

- A short-term rising channel is forming with support at 1.2930 on the 4-hour chart.

- EUR/USD is consolidating gains above the 1.0820 resistance zone.

- Gold surged to a record high and tested the $3,035 zone.

GBP/USD Technical Analysis

The British Pound remained strong above 1.2800 against the US Dollar. GBP/USD formed a base and climbed above the 1.2850 resistance zone.

Looking at the 4-hour chart, the pair settled above the 1.2880 level, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour). The pair even tested the 1.3000 zone before it started a consolidation phase.

There was a move below the 1.2975 level. On the upside, the pair is facing resistance near the 1.3000 level. The next major resistance is near the 1.3040 level.

The main resistance is now forming near the 1.3120 zone. A close above the 1.3120 level could set the tone for another increase. In the stated case, the pair could even clear the 1.3200 resistance.

On the downside, immediate support sits near the 1.2930 level. The next key support sits near the 1.2880 level. Any more losses could send the pair toward the 1.2820 level. The main support could be 1.2750.

Looking at EUR/USD, the pair remained stable and might soon now aim for a move toward the 1.1000 resistance.

Upcoming Economic Events:

- Fed Interest Rate Decision - Forecast 4.5%, versus 4.5% previous.

BoJ holds rates, flags exchange rate as key inflation factor

BoJ kept its uncollateralized overnight call rate unchanged at around 0.50%, as widely expected.

In its statement, BoJ noted that growth is expected to remain above potential, while inflation progress remains on track toward its 2% target. However, policymakers flagged high levels of uncertainty, particularly citing global trade tensions and policy shifts in major economies as key risks.

A notable shift in BoJ’s tone was its heightened focus on exchange rate movements as a key factor influencing inflation. The central bank acknowledged that with firms increasingly raising wages and prices, exchange rate developments are, compared to the past, "more likely to affect prices".

This suggests that further depreciation in Yen could accelerate price increases, and influence future monetary policy decisions.

Japan’s export rises 11.4% yoy in Feb, up for fifth straight month

Japan’s exports surged 11.4% yoy to JPY 9,191B in February, marking the fifth consecutive month of growth, driven by strong demand from both the US and China. Exports to the US rose 10.5% yoy, while shipments to China saw an even stronger 14.1% yoy increase.

Meanwhile, imports declined by -0.7% yoy, marking their first drop in three months, as demand for crude oil and coal weakened. This shift in trade dynamics helped Japan return to a trade surplus of JPY 584.5B, the first positive balance in two months.

On a seasonally adjusted basis, exports rose 4.0% mom to JPY 9,688B, while imports fell -4.1% mom to JPY 9,505B, leading to a JPY 182B surplus.

FOMC & Market Impact: Inflation, Rates, and the US Dollar

- The Fed is expected to maintain current interest rates (4.25%-4.50%) and a cautious approach, emphasizing data-driven decisions.

- Market participants will focus on the Fed's "dot plot" and Chair Powell's press conference for clues about the timing and trajectory of future rate cuts.

- Technically, the US Dollar Index (DXY) is showing signs of potential recovery after hitting a low, with RSI divergence suggesting a possible rebound. Will the FOMC prove to be the catalyst?

The FOMC meeting tomorrow is poised to be a pivotal moment for financial markets. Weakening US data off late have ramped up recessionary fears as inflation expectations have also increased on tariff fears.

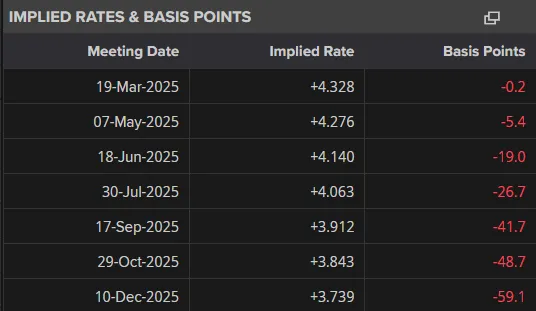

The result of these developments has led to an increase in rate cut expectations as market participants weigh up a host of uncertainties for the rest of year. As things stand, heading into tomorrow's meeting and markets are pricing in around 59 bps of rate cuts through December 2025. This has increased from 50 bps a month ago.

Source: LSEG

The question heading into tomorrow's meeting will be whether the Fed will persist with its cautious approach, or will any subtle shifts in rhetoric signal changes to its long-term policy trajectory?

What to Expect from the FOMC Meeting?

The Fed’s decision-making process for this meeting hinges on several critical economic factors:

- Inflation Trends: Although inflation is gradually edging closer to the Fed’s 2% target, disparities across different sectors persist. The Consumer Price Index (CPI) data is trending positively but still demands careful scrutiny from policymakers.

- Labor Market Observations: Unemployment rates remain near historical lows, but there are signs of cooling in job creation and wage growth. These metrics are a critical component of the Fed’s dual mandate of maximum employment and price stability.

- Consumer Sentiment: With consumer sentiment dipping to a 29-month low, the Fed must weigh how declining optimism from consumers may affect overall economic activity.

- Broader Economic Indicators: Housing market data, retail sales, and manufacturing output present a mixed picture, complicating the Fed’s policy choices.

The Federal Reserve is expected to keep interest rates between 4.25% and 4.50%. They are being cautious because the economy is sending mixed signals. Chair Jerome Powell has noted that while inflation is easing, they need to avoid cutting rates too soon, which could bring inflation back. The strong job market also gives the Fed no reason to change its current strategy.

Market participants have also shown that their inflation expectations for the next 12 months are on the rise. That coupled with the unknown impact of universal tariffs will in my opinion keep the Fed rhetoric steady and in line with the previous FOMC meeting.

Federal Reserve Communication and Powell Press Conference

Markets are anticipating that the March FOMC meeting will deliver more than just clarity on short-term interest rates. The Fed’s updated “dot plot”, showcasing projections of future rates, is expected to offer insights into the long-term trajectory of monetary policy.

The Fed faces mounting pressure to clarify its timeline for potential rate cuts. Economic growth concerns and easing inflation trends have already led markets to speculate that the first cuts could occur in the latter half of 2025.

Chair Powell’s press conference will be key to understanding when the Fed might start cutting rates. Traders should analyze the exact wording of the Fed statement to spot policy changes, as even small edits can affect markets. Chair Powell will likely stress that decisions depend on data and avoid making long-term promises. This lets the Fed stay adaptable while giving markets some direction.

This would be a wise move in my opinion as Geopolitical risks and uncertainty continue to be an issue.

Technical Analysis - US Dollar Index

From a technical standpoint, the US Dollar continues to struggle since its peak on January 13, 2025.

The DXY printed a fresh low today running into support at 103.18 ahead of the FOMC meeting.

There is a sign that the US Dollar might be ready to recover from a technical aspect as the RSI and price action are flashing signs of divergence. The RSI has made a higher low while price action has made a lower low which could be a warning sign that a recovery might be imminent.

Will the FOMC be the catalyst?

US Dollar Index (DXY) Daily Chart, March 18, 2025

Source: TradingView.com (click to enlarge)

Support

- 103.18

- 102.95

- 102.64

Resistance

- 103.65

- 104.00

- 104.96